29 Dec 2025

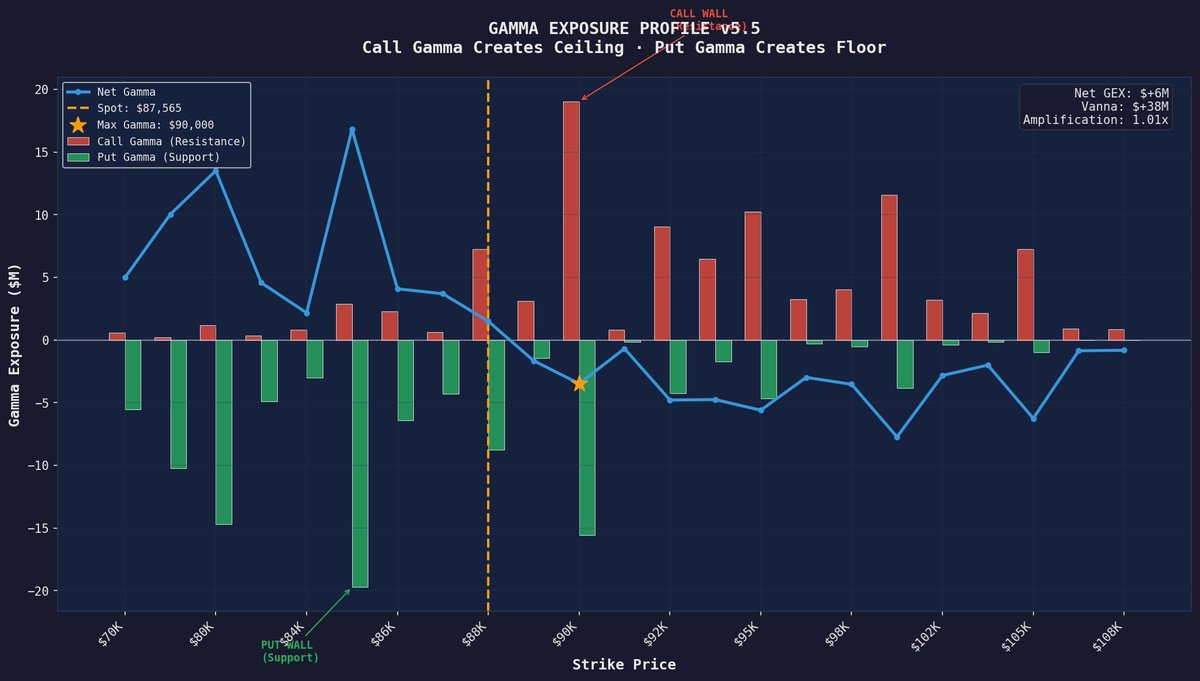

🚀 Bitcoin Options Gamma Exposure Update: Massive Call Wall at $95K Acting as Resistance!

Deribit data shows heavy positive Call Gamma concentrated around $95K-$100K strikes – creating a strong ceiling that's pinning BTC upside for now.

Meanwhile, Put Gamma provides solid support down at $80K, forming the current floor.

Net GEX: $6M | Max Gamma: ~$90K | Spot: $87,565

This setup explains the recent consolidation – dealers hedging calls suppress volatility and cap rallies. A break above $95K gamma wall could trigger explosive upside as shorts get squeezed.

Watching closely for gamma flip. 📊🔥

#AltcoinPioneers #Bitcoin #OptionsGamma #Deribit #CryptoDerivatives

1

213

3 Oct 2025

TOBACCO VANGUARD Est. 1977

Not for all and sundry.

Today’s Cash, Tomorrow’s Story

By M. Reuven

Investors are paying record prices for tomorrow's promises while the tobacco companies continue to distribute money to their owners today. The contrast reflects two different economies. One rests upon cash flows that arrive with predictable regularity. The other rests upon narratives about future revenues that must be very large to justify its inflated price.

Tobacco is unpopular, yet the system around it is settled. Tax is high, visibility is restricted, and sales occur within firm rules. Within those constraints management converts revenue into distributable cash with almost mechanical regularity. Dividends arrive on a timetable. Buybacks lower the share count. The equity case does not require a leap of faith. It asks whether the current stream of cash, plus modest growth from price and mix, will continue under the same apparatus that already exists. The answer, judged over time, has been yes more often than not.

The speculative complex is different. It begins with a claim about tomorrow and builds valuation first, utility second. The large technology stories promise a step change in productivity. They require customers to absorb vast new costs today in order to make or save more later. That may happen, yet it must happen at a scale that lifts free cash flow far beyond present levels. If the revenues do not compound as imagined, or if discount rates rise, the arithmetic turns quickly. Price has run ahead of cash, and cash is the only thing that ultimately counts.

Our view is structural and realist. Markets are governed fields. Institutions do not merely referee activity, they shape it. Ministries set tax and advertising rules. Courts define liability. Index stewards fix the weight of a share in a benchmark. Bank capital rules decide whose balance sheet can support which risks. These arrangements assign roles and habits to firms and savers. Tobacco has learned its part in this play. It prices its product within legal limits, contains its costs, and returns the surplus to holders. Tech asks for a re-write of the scene. It asks regulators, accountants, and investors to treat long horizons as present value and to confer a grace period where earnings are light and capital is heavy.

There is nothing immoral in either approach. The question is what follows once the stage directions are read. In tobacco the direction is simple. Cash goes to the register, cash goes to the holder. In tech the direction is indirect. Capital pours into data centres, software, and stock-based pay. The firms tell us that operating leverage will arrive later. We do not deny that it may. We note only that the system must carry the cost until it does, and that the cost is immense.

State and legal frameworks produce outcomes that look like private choice but are patterned by structure. When a government constrains display, it also entrenches incumbents who can live with regulation and convert scarcity into price. When benchmark rules concentrate weight, they pull flows into the leaders regardless of valuation. When compensation practice prefers options, it invites a culture that values multiple expansion as much as profit. None of this is conspiracy. It is arrangement. Tobacco sits in an apparatus that pays the owner now. The speculative complex sits in an apparatus that pays the employee today and asks the owner to wait.

A critical realist insists on mechanisms. The mechanism in tobacco is cash conversion under constraint. The mechanism in the speculative trade is expectation under scale. The former does not require an expansion of the profit share of the economy. The latter either expands that share or takes it from others. If AI truly raises productivity, the pie will grow and the claims may hold. If it is merely a costly reshuffle of spend, the pie will not grow enough and the claims will not hold.

None of this settles the question of return, which is always a function of price paid. Tobacco is not a free lunch. It faces litigation risk, illicit trade, and policy change. Yet its returns are anchored in distributions that arrive regardless of fashion. The speculative complex can be a winning ticket if the world moves to its script. It can be cruel if the script is revised.

Our editorial position is consistent. We do not worship price. We respect cash, margin discipline, and the work of capital allocation under law. We prefer sectors where the rules are clear, the costs are known, and the cheques clear. If the age of promise becomes the age of delivery, we will mark it. Until then, we treat today’s cash as the base and tomorrow’s story as an option, and we pay as little as we can for the option.

The practical consequence is straightforward. Holders should weigh portfolios toward enterprises that fund themselves and pay their owners without ceremony. Where one wishes to own promise, size it as promise and remember that structure, not slogans, decides who gets paid and when.

#TobaccoVanguard #TodayVsTomorrow #CashFlow #Dividends #Buybacks #Yield #Valuation #DCF #DiscountRate #ProfitShare #MarketStructure #PassiveFlows #OptionsGamma #Regulation #Benchmarking #CriticalRealism #Althusser #StructuralCausality #Reflexivity #AI #TechStocks #NVDA #TSLA #AutosAndEnergy #IncomeInvesting #ValueDiscipline

2

3

187

21 Aug 2025

Marknadsinsikt torsdag: Uppdatering på optionsgamma och potentiella flöden från CTAs 👇🏻

marketmate.se/ctaer-kan-komm…

6

18

6,303

This chart is pure 🔥 for anyone watching $GME.

Just look at the red zones: every time short volume spikes with VWAP around key price levels, it sets the stage for an explosive move ...and we’re right back in that danger zone again.

Current short volume? 2.28M.

Short ratio? 1,882.28% (yes, seriously).

That’s like lighting a match in a room full of gas.

Oh...and those past spikes around $22–$28?

They didn’t just fade.

They erupted. 💥

Add in technicals showing compression and reversal potential, and this isn't just a setup...

It’s a warning shot.

#GME #ShortSqueeze #OptionsGamma #T35 #GameOn

1

12

579

$GME got hit with real buy pressure today...but price barely moved.

Why?

Because market makers played goalie with spoof walls and dark pool absorption. 🥅

It’s not a lack of demand… it’s demand getting stuffed in a box.

They can only hold it down so long.

$22.50 and it’s game on.

#GME #Computershare #DarkPoolGames #OptionsGamma

1 Aug 2025

These large $GME block trades seem reactionary to the price and look like they are being used to absorb buy pressure.

The bond trades happen in response to a change in price, because sharp price changes create an arbitrage opportunity between stock and bond price, but the resultant trade effectively allows institutions to block upwards movement by using these QCTs.

1

3

19

901

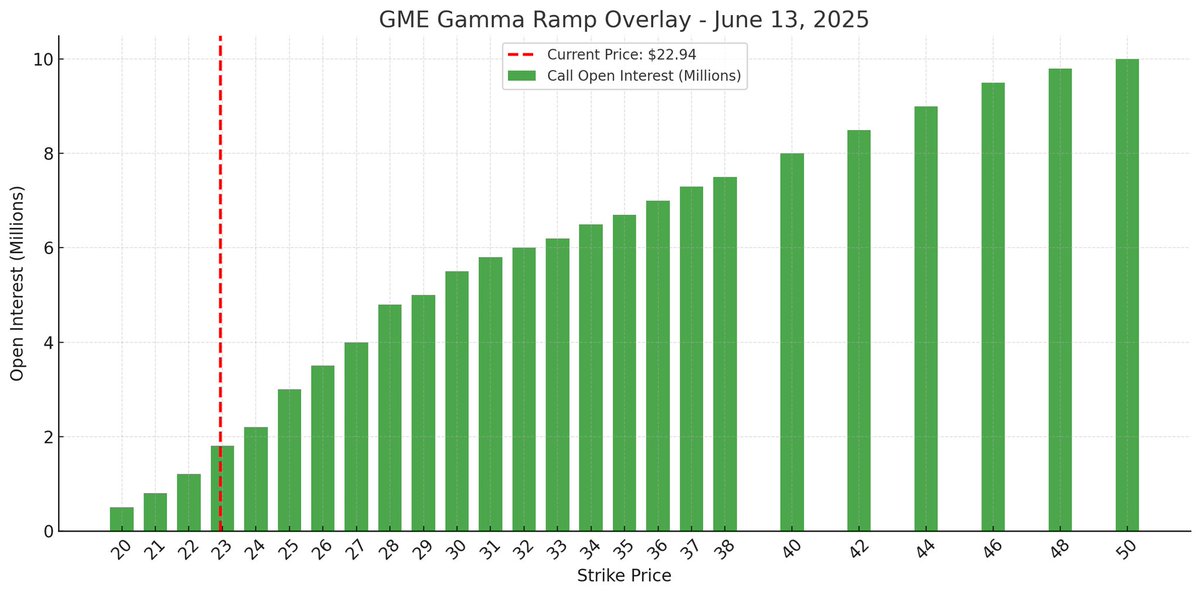

🚨 $GME Gamma Ramp – June 13, 2025

Current Price: $22.94 Strike wall begins: $23

Just look at that curve 📈

As each $1 up unlocks millions of new delta hedge demand, the pressure compounds.

This is a literal gamma ladder.

Light the wick. 🔥

#GME #OptionsGamma #GammaRamp #MOASS

5

40

932

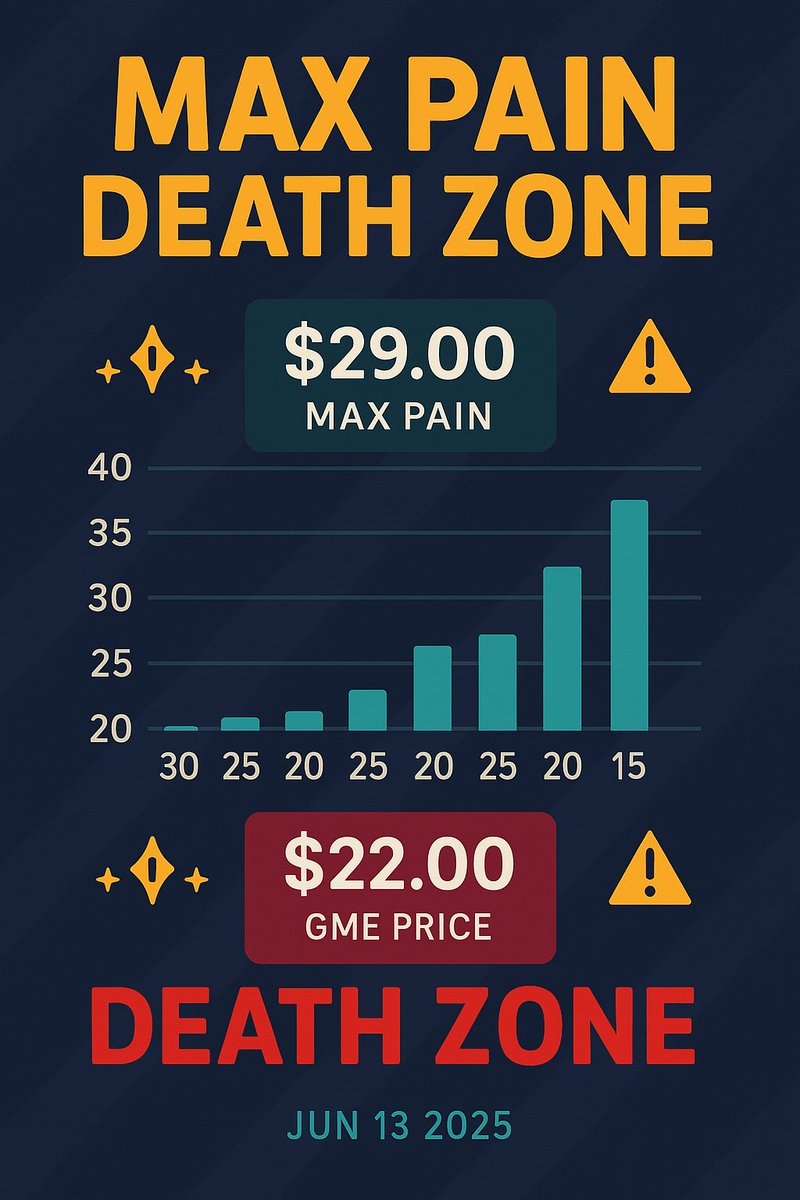

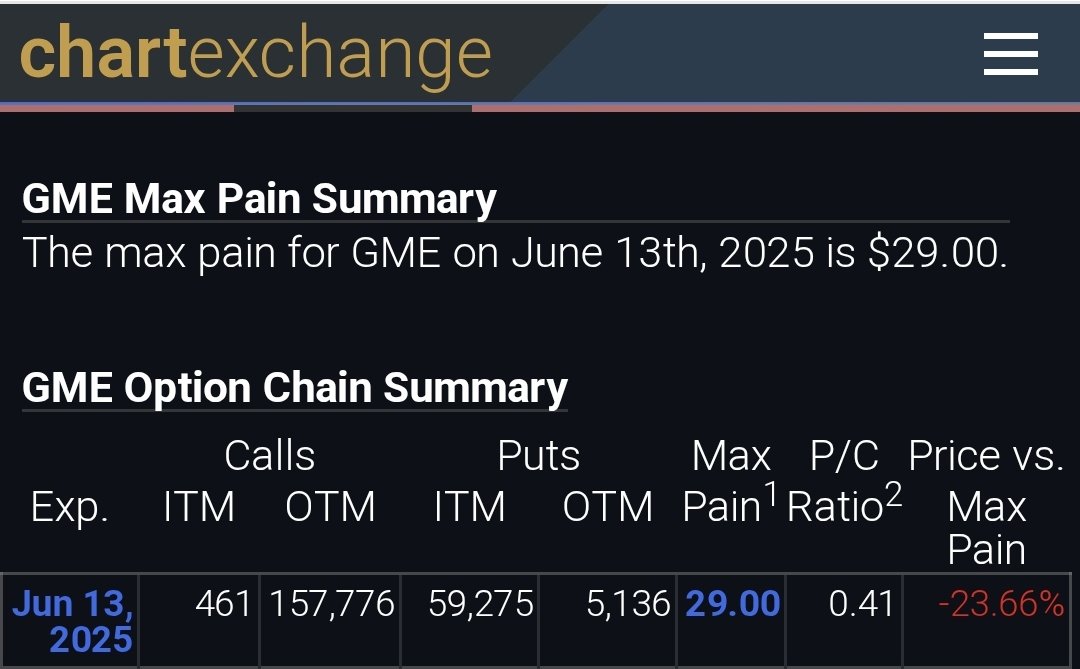

$GME max pain is $29 for 6/13

Current price: $22

That’s -23.66% under.

If market makers want delta-neutral exposure, they have to buy back shares used to hedge deep ITM puts.

You saw it in Jan ‘21.

You just might see👀it again.

#GME #MaxPain #OptionsGamma #MOASS

13 Jun 2025

$GME

If this is still accurate for today I would expect to see the same thing we saw in January but to the upside. Market makers are going to want to stay delta neutral, they don't want all those puts being ITM.

1

3

25

1,628

23 May 2025

‼️ #MODERNA UNDER SHORT ATTACK: 17.6% SHORT INTEREST AND AN EXPLOSIVE SHORT SQUEEZE SETUP ‼️

📊 Q1 2025 Results:

• 💰 Revenue: $108M (−35% YoY)

• 📉 Adj. EPS: –$2.52 (improved from –$3.07 YoY)

📅 2025 Guidance:

• 📎 Revenue: $1.5–2.5B (–53% to –22% YoY)

• 🧪 Excludes potential sales from new product approvals

🔬 Key Products & Pipeline:

• 💉 Spikevax (COVID vaccine): sales –50% YoY to $84M

• 📦 Distributor stockpiles from 2024 likely dragged down demand

• 🌍 Market now seasonal (annual fall shots), but demand fading in EMs strong competition from $PFE and $NVAX

• ⚠️ 2026 forecast: sales may fall below $1B

• 🦠 mRESVIA (RSV vaccine): only $2M in sales

• 📆 FDA decision for high-risk adults (18–59) expected June 12

• 📈 Bull case: $200M in 2025 revenue

• 🤝 $MRK partnership: ~20% of Q1 revenue from collaboration (funding mRNA-4157 trials)

🎯 The Real Bet: mRNA-4157

• 🧬 Key oncology pipeline candidate

• 🏦 $5.98B in cash (as of Mar 31, 2025) — fully funds trial completion

• ⏳ Results expected late 2025–2026

• 🧨 Make-or-break asset — either massive upside or collapse

🐻 SHORT INTEREST SPIKING:

• 🚨 April short interest: 17.6% (up from 14.6% in March)

• ⚖️ Fundamentals still weak, but…

• 🔥 Setup for a violent short squeeze is forming

Bullish Catalysts:

• 💼 Strong partnership with $MRK

• 🚫 No shareholder dilution

• 🔒 Tight float

• ⚡ Any positive clinical/regulatory news = explosive upside

🧾 Short Interest Across Healthcare:

🔝 Most Shorted:

1. $MRNA – 17.58%

2. $DVA – 6.62%

3. $RMD – 6.47%

4. $CRL – 5.45%

5. $HSIC – 5.09%

🔻 Least Shorted:

1. $BSX – 1.07%

2. $UNH – 0.98%

3. $MDT – 0.87%

4. $LLY – 0.87%

5. $JNJ – 0.82%

#ShortSqueeze #HighShortInterest #ShortCovering #SqueezeSetup #BiotechSqueeze #OptionsGamma #MarketSqueeze #ShortAttack #ExplosiveMove #ShortTrap #MRNASqueeze

2

161

22 Aug 2024

Hej Amir,

Tack för inlägget.

Jag vet inte om du är en ”offentlig person” som jag. Men det spelar mindre roll. Jag ska oavsett göra ett ärligt försök att bemöta ditt inlägg.

Sedan Marketmate lanserades i oktober i fjol har jag personligen publicerat 550 artiklar. Helt gratis och publikt på plattformen. Allt ifrån dagliga inlägg om global makro, positionering, sentiment, värdering, optionsgamma, buybacks, etc. Delar av verktygslådan som jag själv tycker är intressant att ta i beaktning.

Vad gäller ditt aktuella inlägg är det något som vi benämner som ”Dagens analys”. Där skriver jag inägg som det du belyser här, men mer vanligt affärsförslag på specifika tillgångsslag med väldigt tydliga nivåer om stop loss och målnivåer. Samt att jag följer upp dessa. Jag känner ett stort ansvar för de officiella tradingcasen som jag lanserar och också därmed äger privat.

Den svenska marknaden för börshandlade produkter ägs/ägdes till ca 80% av Avanza och Nordnet när vi startade Marketmate. Den första teamade upp med Morgan Stanley för mängder av år sedan och erbjuder ”gratis” courtage till slutlunden och Nordnet har liknande samarbete med Nordea. Vi har haft möten med både MS & NDA. Som alltid är ETP-handel inte prio 1 för gigantiska banker, men de har en position som de båda är nöjda med.

Som du vet är inget egentligen ”gratis” i världen. Även om man vill tro det ibland. Speciellt inte inom finansbranschen. Både du och jag vet ju det finns en intjäning i bakgrunden på något sätt.

Att visa traders att det finns ett större utbud än ”Avanza” och Nordnet” och dessutom göra det gratis i en effektivt screeningprocess genom ett gigantiskt ”Pricerunner 2.0 för ETPer”, ja där föddes fröet till som idag är Marketmate!

Får vi tick på volymer? Nej! Men Marketmate är ett sätt för emittenter att synas och lyfta fram sina produkter och egenskaper. Då marknaden ”ägs” av två storbanker genom sina respektive samarbeten med varsin nätmäklare, är det inte svårt att förstå att de andra emittenterna (7-9st) kan tänkas vilja öka sin marknadsandel. Vem har sagt att de skulle erbjuda sämre produkter? Troligtvis måste de vara vassare för att locka flöden, givet ”underläget” från början?

För dessa emittenter är Marketmate en kanal för marknadsföring. Alla 120 000 noterade ETPer i Sverige rankas dock mot varandra hela tiden oavsett emittent, så ingen kommer undan.

Med ärliga hälsningar, David

1

24

6,151

8 Jun 2024

Dagens graf lördag: Rekordstort optionsgamma inför junilösen! Vad betyder det och hur påverkar det börsen? Läs mer här 👇🏻

marketmate.se/record-long-ga…

5

2

34

14,084

17 May 2024

Dagens graf fredag: S&P 500 och aktuellt optionsgamma i marknaden.

marketmate.se/sp-500-och-gam…

1

18

8,203

17 May 2024

#ES $SPY $SPX #OptionsGamma

$2.5 Trillion worth of options expire today. 66% of the long gamma rolls off and now dealers may get shorter to the upside.

3

618

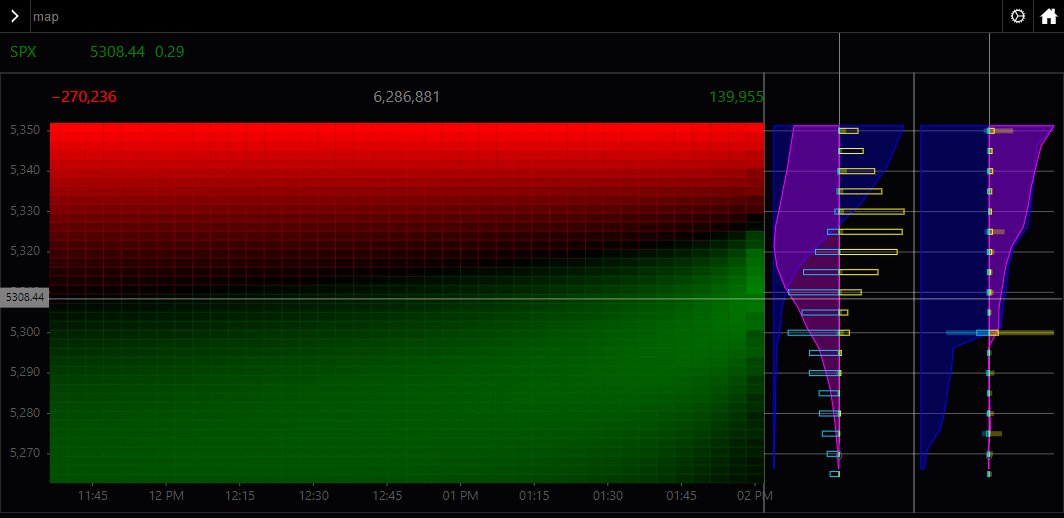

16 May 2024

Massive change in convex over the last 40 minutes.

Paths of least resistance 5320 or 5300?

We tapped 5301. I think 5300 is a huge key psych level.

NVDA setting up for a vomy on the hourly, or possible bounce on the hourly 21ema.

$SPY $SPX $NVDA #optionsflow #optionsgamma #gamma #gex

16 May 2024

All out at 5.75

There was our dip to 5305 - now do we bounce to the upside? Convex still showing a move towards 5330

There is also some darkness bottom left 5270

#btfd #buythedip #spx #spy $spy #options #0dte

2

317

5 Jan 2024

مقطع فيديو يشرح فلاتر الاختراقات والحراق والفوليوم والانفجارات السعرية بالمؤشرات المجانية من تريدنق فيو

🌐youtu.be/AI0T_JByWwQ

#السوق_الامريكي

#الاسهم_الامريكيه

#الاوبشن

#اوبشن

#التحليل_الفني

#OptionsGamma

#OPTION_TS

#SPX #SPY #AAPL #TSLA

4

15

1,124

17 Nov 2023

🧵 1/ Options enthusiasts, it's time to demystify one of the most intriguing aspects of the trade: Gamma. Let's dive into what it means for your strategies! 📊 #OptionsGamma #TradingGreeks

1

1

3

1,169

16 Nov 2023

🏎️ Gamma Gear: #OptionsGamma is the acceleration to Delta's speed, showing how fast the Delta changes as the underlying stock moves. High Gamma can turbocharge your strategy in a volatile market, so buckle up for a thrilling ride! 🚀 #TradingStrategy

1

316

27 Sep 2023

$LCID

التنبيهات تظهر بشكل متنوع دخول كميات عقود كبيرة على $LCID

وسترايكات بعيدة تبعد اكثر من 5٪ من سعر السهم

نتوقع ارتفاع قوي للسهم

#السوق_الامريكي

#ThinkoScript #Options

#الاسهم

#تاسي

#الاسهم_الامريكيه

#التحليل_الفني

#OptionsGamma

#القاما #الجاما

3

2

8

2,206

29 Jun 2023

🔼🔼ظهور كميات #تنبؤ على $SPY

ملاحظة العقود شهرية

وهذا يعطى انطباع على ارتفاع السوق

#السوق_الامريكي

#ThinkoScript #Options

#الاسهم

#تاسي

#الاسهم_الامريكيه

#التحليل_الفني

#OptionsGamma

#القاما #الجاما

2

2

3,813

21 Jun 2023

مقطع حصري يوضح كيف تحصل على الاختراقات والانفجارات السعرية في #السوق_الامريكي

#ThinkoScript #Options

#الاسهم

#تاسي

#الاسهم_الامريكيه

#التحليل_الفني

#OptionsGamma

#القاما #الجاما

$spy

$spx

$nvda

$amzn

youtu.be/AI0T_JByWwQ

1

5

458

14 Jun 2023

⚡⚡مقطع حصري يوضح كيف تحصل على الاختراقات والانفجارات السعرية في #السوق_الامريكي

#ThinkoScript #Options

#الاسهم

#تاسي

#الاسهم_الامريكيه

التحليل_الفني

#OptionsGamma

#القاما #الجاما

$spy

$spx

$nvda

$amzn

youtu.be/AI0T_JByWwQ

4

10

1,563