May 2

🌅 GARCH Quant Academic Series|D. E. Shaw

📖 【Day 3/7】Design of a High-Performance Order Execution & Routing System

👤 Authors: D. E. Shaw (1998), IEEE Financial Systems Conference

📌 Summary

This pioneering paper from D.E. Shaw details the architecture of their proprietary high-performance order execution and routing system. It covers low-latency network communication, order management algorithms, market data processing, and optimal routing strategies — an early classic that laid the engineering foundation for modern high-frequency trading systems.

🏛️ Key Academic Contributions

• Proposed core architectural principles for low-latency trading systems, including memory mapping and zero-copy networking

• Designed multi-layer order routing algorithms that effectively balance execution costs and market impact

• Introduced real-time risk monitoring and order flow control mechanisms

📚 Why It’s Essential Reading

A must-read for anyone building quant trading infrastructure!

Published in 1998, this paper showcases D.E. Shaw’s early mastery of high-performance system engineering and remains highly relevant today.

#DEShaw #HighFrequencyTrading #OrderExecution #QuantInfrastructure #GARCHQuant

1

5

90

You click “Buy.” But what really happens next? 👀

👉 Watch the video to understand how order books, liquidity, and price matching bring your trade to life.

Trading isn’t just a click; it’s a process.

#KoinBX #Crypto #TradingCommunity #OrderExecution #TradingBasics

5

96

31 Jul 2025

Q&A Session: Investor Queries & Management Responses 💬

13/ ❓ Can you expand on defense/aerospace orders, their size, and whether you’re making full drone/anti-drone systems or components?

💬 Manikandan: Defense is 44.2% of Dec’24 revenue. Orders: ₹45-50 Cr for HAL AMCA simulators, track-based missile systems, tank hulls .

🚀 Full drone/anti-drone systems, not components. Civil drone for high-rise cleaning adapted for defense with European tech (NATO-proven).

📈 EoI for 3,000 drones for HAL, targeting 200-300/month. 80% local content, importing motors. #defensetech

14/ ❓ Timeline for future defense projects?

💬 Manikandan: Drone & anti-drone prototypes by Mar ‘26, leveraging civil drone tech & Israeli partner 🛩️.

🌍 Radar system likely FY27 due to capital needs. Defense is long-gestation, but confident with European tie-up.

📅 Drone/anti-drone on track for FY26, radar in FY27. #Aerospace

15/ ❓ : Existing railway order book and completion timeline?

💬 Manikandan: Order book ₹30,635.67 Lakhs (95% railways), expected to reach ₹600-700 Cr in 2-3 months 🚆.

⏳ 70% this FY, rest FY27. New orders (12-18 months).

📈 Participated in ₹800 Cr tender, finalizing soon. #railwaysafety

16/ ❓How much of the order book will be executed in the next 12 months?

💬 Manikandan: Conservatively, ₹350 Cr this FY (achievable) 📊.

🚄 Next FY, targeting ₹500 Cr. Numbers conservative; we’ll exceed with existing capacity. #OrderExecution

17/ ❓ EBITDA margins at 28.14%—sustainable or improvable?

💬 Manikandan: Margins sustainable at ~28% 💰.

🔍 Post-COVID strategy: high-margin projects only. Aerospace/defense focus to maintain/boost margins.

🚀 Selective bidding ensures profitability. #Financials

18/ ❓₹13.44 Cr from IPO for machinery—what are these, and extra revenue?

💬 Manikandan: Machinery for metro coach roofs (currently Chinese-made) & bogie frames/body shells 🏭.

📈 Adds ₹150 Cr this FY, ₹500 Cr FY27. Enables full coach body building (3,000 outsourced coaches/year). #Capex

19/ ❓ Production capacity increase post-machinery installation?

💬 Manikandan: Machinery usable FY27, adding ₹500 Cr capacity 📊.

🏗️ New facility for full car body building. Current infra hits ₹350 Cr this FY with 2 shifts. #CapacityExpansion

20/ ❓Capacity utilization ~83%. Can FY26 targets be met with remaining capacity?

💬 Manikandan: Yes, FY26 targets achievable 🚆.

🔄 Two 8-hour shifts from one. Existing capacity sufficient for ₹350 Cr this FY. No new infra needed yet. #Operations

21/ Possibility drone orders won’t materialize post-prototype?

💬 Manikandan: 0.01% uncertainty (e.g., COVID) ⚠️.

🛩️ Drones are carriers; applications vary. Defense budget: ₹56,000 Cr for drones/anti-drones. 2% share makes us ₹1,000 Cr company. Confident in 5% share. #DroneMarket

22/ ❓Other geographies targeted besides Mozambique & Sri Lanka?

💬 Manikandan: Targeting 200 coaches for Bangladesh via RCF 🌍.

🚄 Exploring African & South American markets (developing countries). Developed markets saturated; focus on tech transfer. #ExportMarkets

23/ ❓Drone tech in-house or collaborations? Future expectations?

💬 Manikandan: Civil drone 100% in-house, defense drones use European motors & tech (NATO-proven) 🤝.

🔋 Local battery tie-ups. Future: 80% local content, mass production. No Chinese components. #TechTransfer

24/ ❓Drivers for higher margins than peers?

💬 Manikandan: Post-2021 focus on projects, not products 💡.

👷 Labor & engineering edge, own design team, maxed infra (saving ₹40-45L/month). Tech products & defense to boost top/bottom lines. #Margins

25/ ❓Raw material procurement mechanism? Main materials?

💬 Manikandan: Stainless steel & aluminum sheets/extrusions (Jindal, SAIL, Hindalco) 🛠️.

📉 No mild steel. Contracts have price escalation clauses for commodity swings. #SupplyChain

26/ ❓

Why high FY24 attrition? Future outlook?

💬 Manikandan: High FY24 attrition due to KPA-based cleanup for Vande Bharat 👷.

📈 Stabilized, added 70-75 performance-based staff. Hiring design & project execution talent, building R&D center.

27/ ❓

Any project delays in railways or defense?

💬 Manikandan: Railways: No delays, monthly schedules like automotive 🚆.

Defense: Long gestation, but no delays except COVID (penalties waived). Just-in-time supply, in-house inspections. #Execution

28/ ❓ IPO size and bifurcation?

💬 Manikandan: IPO size ₹90 Cr 💰.

📊 14.9% capex (₹1,343.82 Lakhs), 58.3% working capital (₹5,246.18 Lakhs), 6.7% debt repayment (₹600 Lakhs). Valued at ~₹350 Cr, P/E ~13.5. #IPODetails

29/ ❓R&D in-house for defense, or tech transfer?

💬 Manikandan: Tech transfer from European partners for drones/anti-drones, initial engineering support 🤝.

🏭 Full buildup in-house (composites, machining). 80% local content, importing motors.

30/ ❓ Assembling or manufacturing defense products?

💬 Manikandan: Manufacturing in-house 🏭.

🛠️ Composites (carbon/aramid fibers), high-precision machining locally. Motors imported, controllers by Indian partner.

31/ Design team (2 in deck) sufficient for high-end products?

💬 Manikandan: Deck error; 25 engineers, separate design facility 👷.

🔍 Setting up R&D division for drones/anti-drones. Team sufficient for current projects.

32/ ❓Railway product line? Market share?

💬 Manikandan: Entire interiors: floors, seats, panels (aluminum/composites), windows, doors, lights, luggage racks, toilets, gangways 🚆.

📊 ~30-40% market share in tenders. Peers: Kineco (FRP-focused), Hindustan Fiberglass, DTL.

33/Tech transfer or patents in railways, aerospace, defense?

💬 Manikandan: MOU signed 10-11 days ago for drone/anti-drone/radar tech transfer from European partner 🤝.

📜 Transfer pending commercial terms. No patents yet, recent defense/aerospace entry

34/ ❓Raw material procurement constraints?

💬 Manikandan: No constraints, using stainless steel & aluminum (Jindal, SAIL, Hindalco) 🛠️.

⚖️ Limited suppliers reduce negotiation power, but availability fine.

35/ ❓ Bid win ratio and book-to-bill in the past?

💬 Manikandan: Bid win ratio ~30-40% for interior tenders, bid only where eligible 📈.

📚 Book-to-bill: Maintain 2x order book (this FY next FY) vs. revenue.

36/ ❓Past execution track record? Delays or penalties?

💬 Manikandan: COVID caused delays, penalties waived by Finance Ministry 🚨.

🚆 Just-in-time supply, in-house inspections ensure no rejections. Extensions granted if needed.

37/ ❓ ₹500-600 Cr railway order book—execution timeline?

💬 Manikandan: Orders typically 12-18 months ⏳.

🚄 Scheduled monthly with customers (Siemens, Alstom, BEML). Targeting ₹350 Cr this FY, rest FY27.

38/ Differentiator in crowded drone segment?

💬 Manikandan: Tech (European partner) proven in Ukraine war, unlike Indian startups 🛩️.

📈 High-end tech & mass production (200-300/month). Anti-drone is niche, less competitive.

39/ ❓Working capital needs and margins/ROE across segments?

💬 Manikandan: Railways: ₹300 Cr achievable this FY, receivables clear by Sep 💰.

Defense: ₹15 Cr for prototyping, may need bank/fund for ₹1,000 Cr orders. Margins vary, targeting high-margin tech products.

40/ ❓Top 1-2 clients’ revenue contribution?

💬 Manikandan: Indian Railways dominates (95% order book) 🚆.

🚄 Titagarh, Kinet, TMH emerging as key clients FY27.

41/ ❓Team strength by department?

💬 Manikandan: 255 employees, 54 engineers 👷.

🏭 Production: 195, QC: 5, maintenance: 18, admin: 2, BD: 4, tool stores: 7, accounts: 6, purchase: 4, HR: 1, design: 8, planning: 2, security: 3. Expanding R&D.

42/ ❓Team size (255, 80% labor, 8-10 design engineers) aligns with R&D-heavy company?

💬 Manikandan: Dec’24 numbers outdated. Now 270 employees, 54 engineers 👷.

🔍 Strengthened design team, setting up R&D division. In-house design for specialized products.

43/ ❓Valuation for the IPO?

💬 Manikandan: IPO size ₹90 Cr for 26.25% stake, valuing ~₹350 Cr 💰.

📊 Post-IPO P/E ~13.5 (Mar ‘25), targeting trailing P/E of 8 FY27.

44/ ❓Revenue split (45% railways)? Future norm?

💬 Manikandan: Incorrect, railways ~55.8% (Dec’24), 95% order book 🚆.

Defense/aerospace 44.2%. Railways to remain dominant, defense growing. Margins vary by project.

45/ ❓Other tender participants?

💬 Manikandan: Kineco & Hindustan Fiberglass Works are main competitors 🤝.

🚄 We secure 25-30% share as L1/L2/L3.

46/ ❓ FY25 numbers and in investor presentation?

💬 Manikandan: FY25: ₹192 Cr revenue, 30% EBITDA, 12% PAT 📈.

📜 Not in presentation (DRHP based on Dec’24). March numbers shared here.

3

1,215

25 Mar 2025

🧭 New Article: How Reservation Strategies Shape Optimal Trading

📖 Read here: axon.trade/how-reservation-s…

#AlgorithmicTrading #ExecutionRisk #OrderExecution #TWAP #VWAP #SmartExecution #QuantTrading #Finance #Markets #Crypto #Cryptocurrency #FinTech

3

10

121

Ready to take your Node.js testing to the next level?

Explore this in-depth tutorial featuring Mocha and Chai: 👉 keploy.io/blog/community/mas…

👏 Appreciation to the author @abbhishekstwt for their valuable insights!

#MochaJS #JavaScriptTesting #NodeJS #AsynchronousTesting #FeatureRich #ChaiFramework #SimpleTesting #EnjoyableTesting #OrderExecution #TestFramework

1

4

258

5 Oct 2024

📚 Analysts are asking: Can Anup keep up with this scalability? Management assured them, focusing on their 95% on-time delivery track record and a robust execution plan for FY25. #Scalability #OrderExecution #AnalystConfidence #EngineeringSuccess

1

2

16

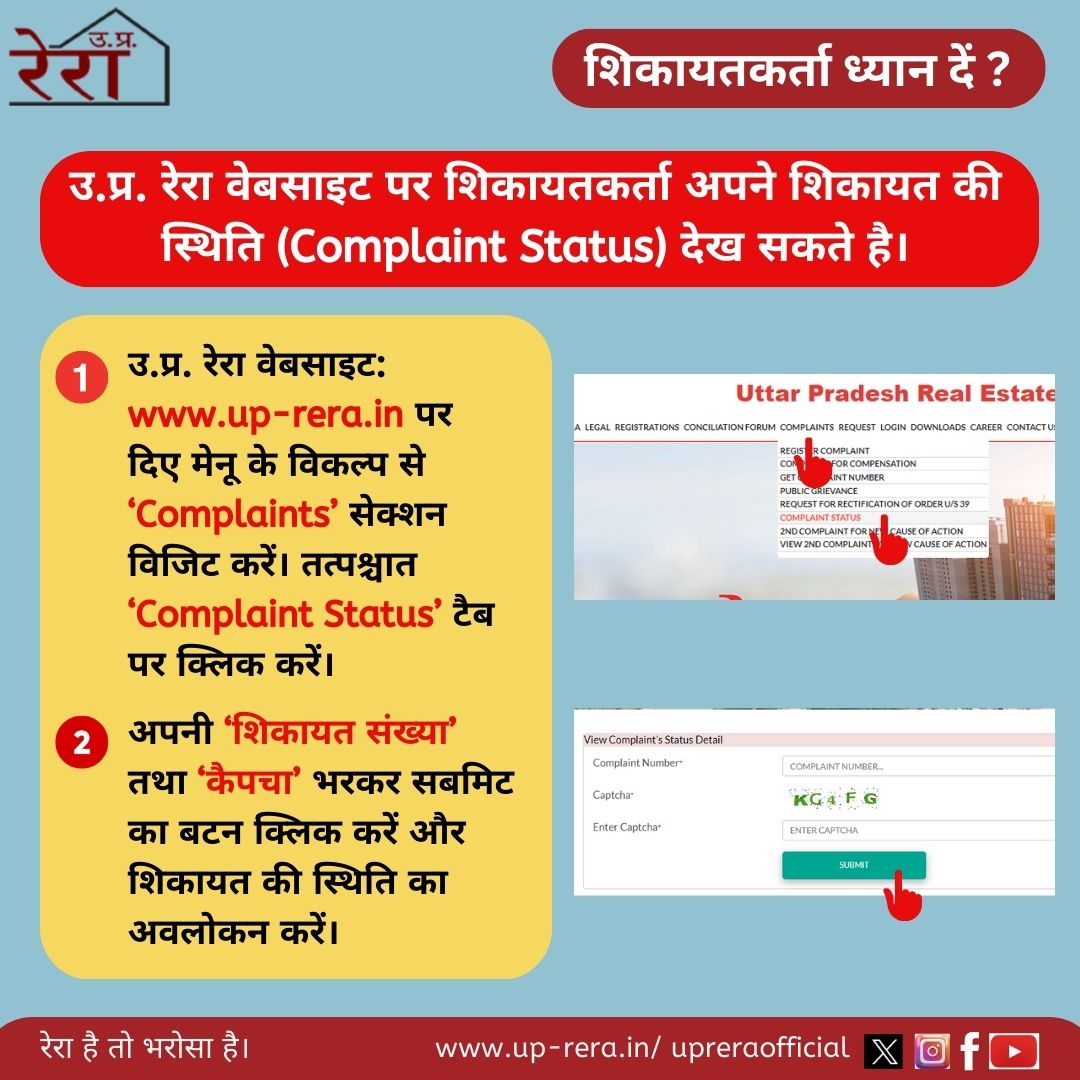

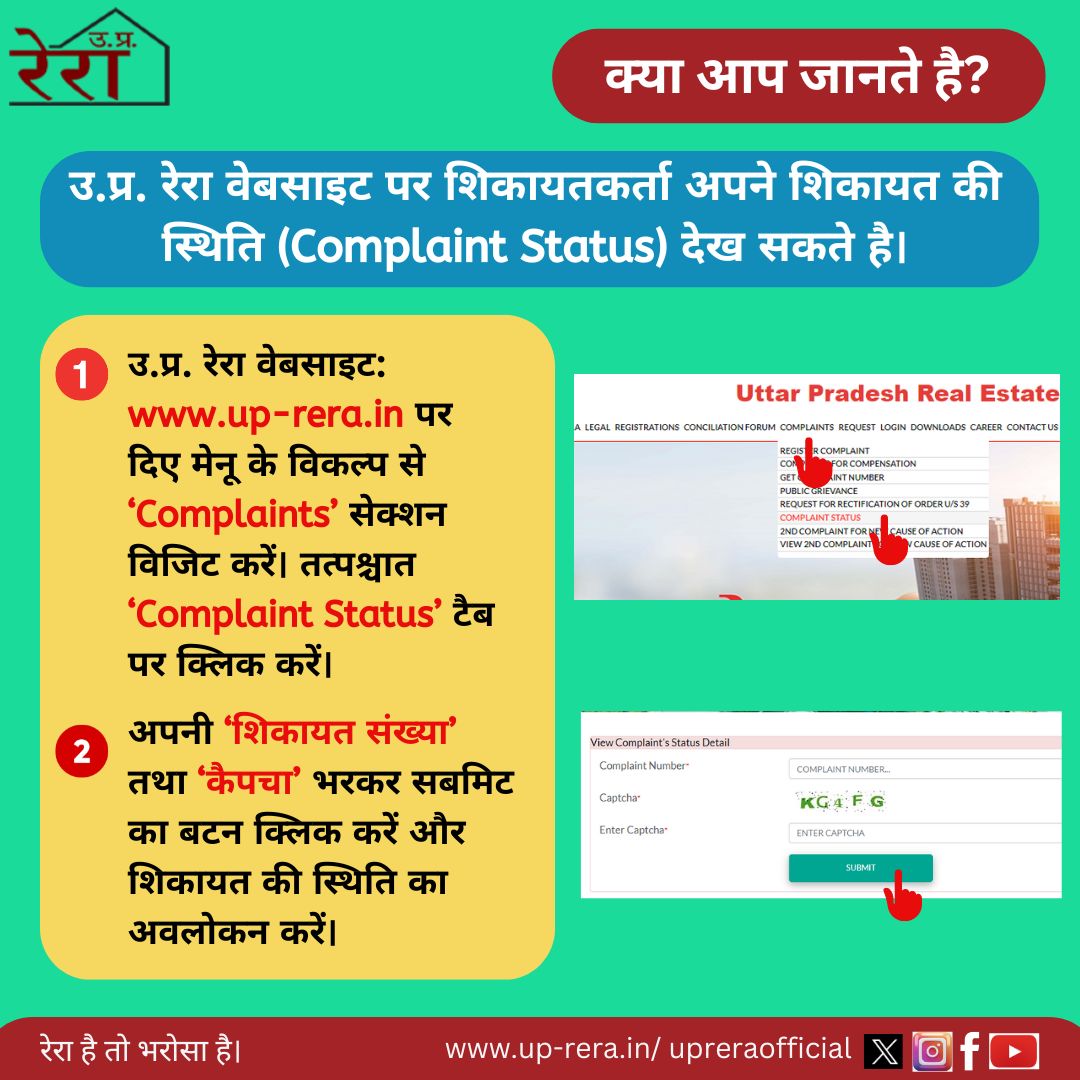

शिकायतकर्ताओं की सुविधा के लिए उ.प्र. रेरा पोर्टल- up-rera.in, पर दर्ज की गई शिकायत की स्थिति (Complaint Status) देखने की सुविधा दी गई है।

#UPRERA #complaint #complaintstatus #complainant #orderexecution #orders #proceedings

1

3

480

उ.प्र. रेरा द्वारा मा.पीठों में शिकायतों की सुनवाई की प्रक्रिया तथा पारित आदेशों के क्रियान्वयन के सम्बन्ध में नवीनतम मानक संचालन प्रक्रिया (#NewSOP) दिनांक 08.08.2024 को पोर्टल पर अपलोड कर दी गई है।

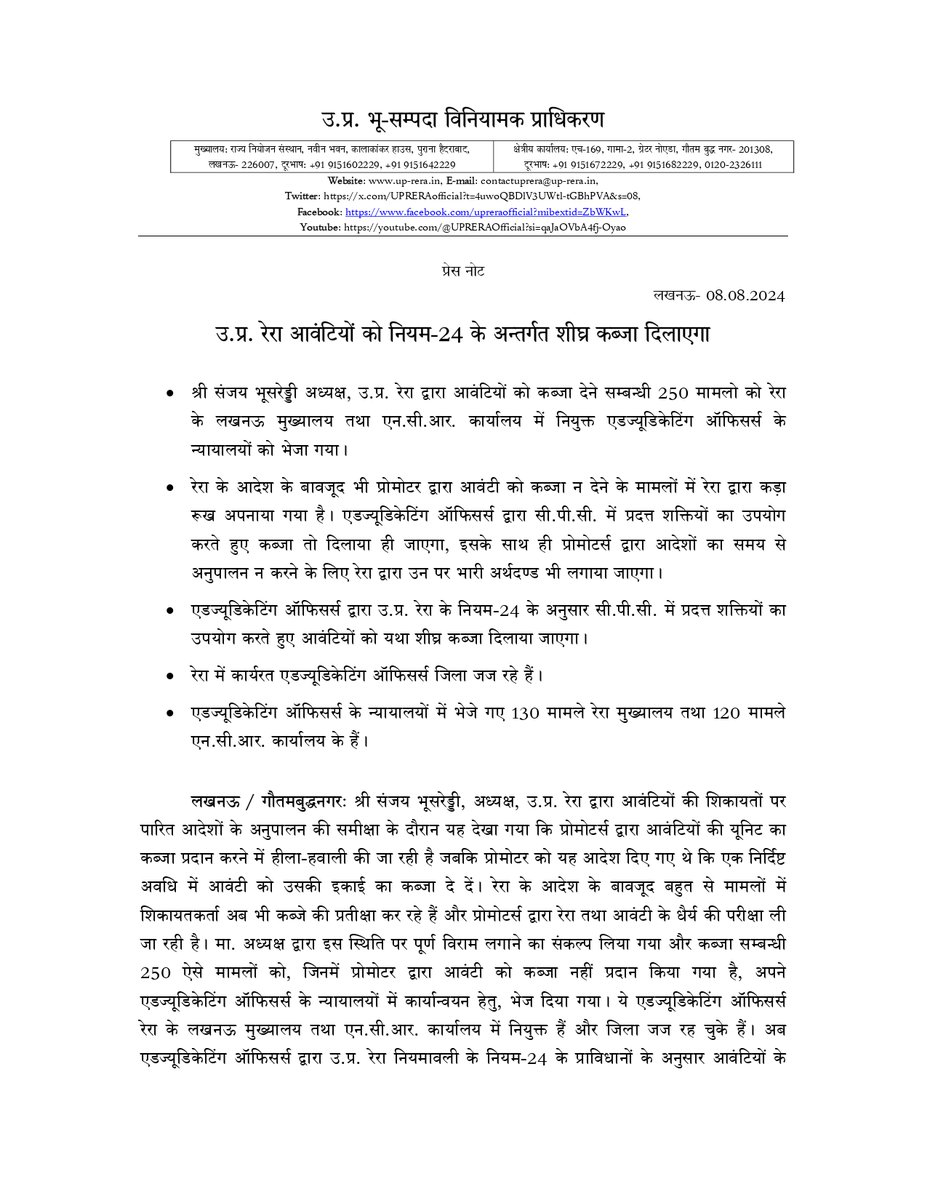

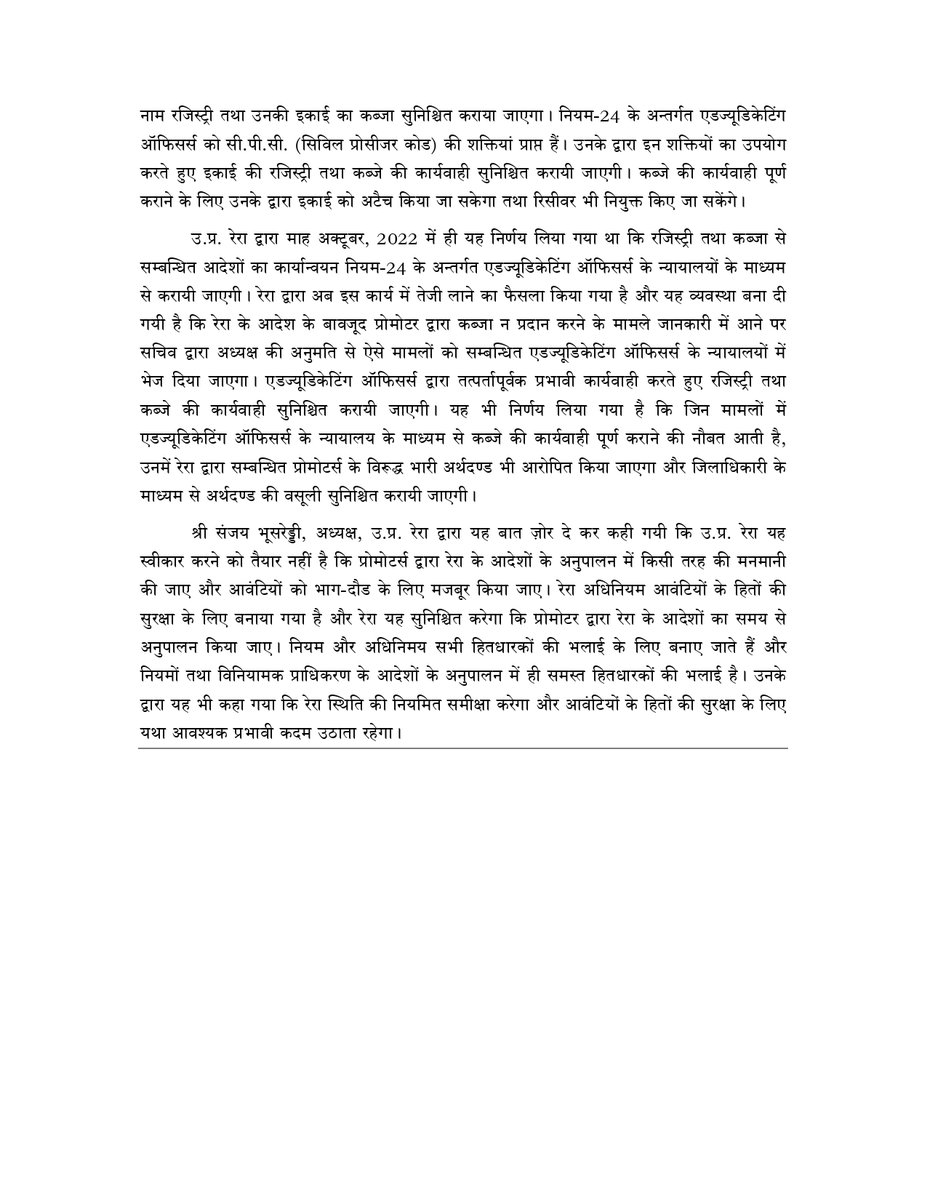

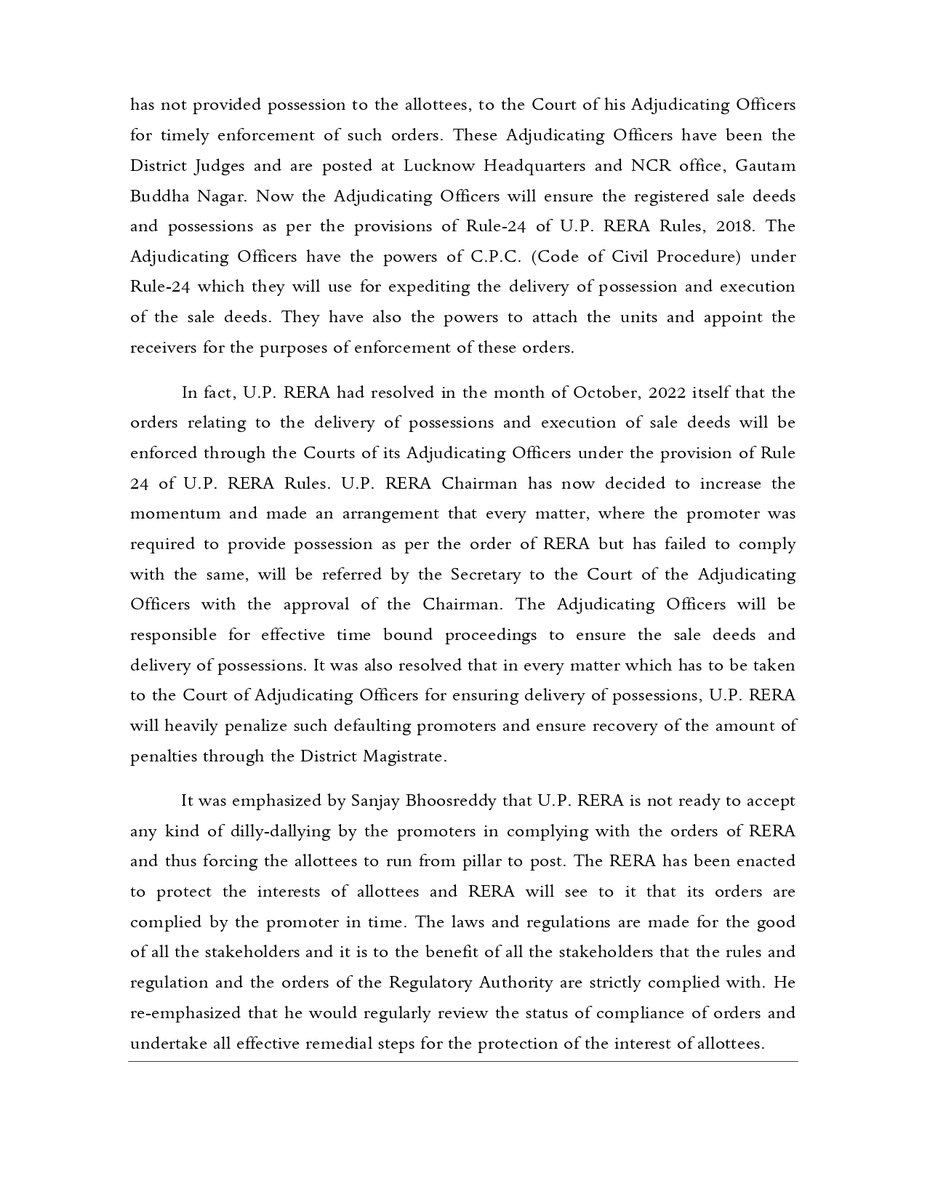

लिंक- up-rera.in/pdf/SOP-08-08-202…

#UPRERA #BenchProceedings #OrderExecution #RERAact

1

2

7

768

11 Sep 2024

BullX on tron

Start Bullx for free now: smpl.is/9lmlj

#bullx #solana #memecoins #crypto #trading #orderexecution #efficienttrading #Bullxtrading #cryptoexchange #Solana #tradingsuccess #tradeefficiency

2

16

8 Sep 2024

How to filter out potential tokens when researching on Bullx

Start Bullx for free now: smpl.is/9l91g

#bullx #solana #memecoins #crypto #trading #orderexecution #efficienttrading #Bullxtrading #cryptoexchange #Solana #tradingsuccess #tradeefficiency

1

17

उ.प्र. रेरा द्वारा आवंटियों को शीघ्र कब्जा देने सम्बन्धी 250 मामलो को रेरा के लखनऊ मुख्यालय तथा एन.सी.आर. कार्यालय में नियुक्त एडज्यूडिकेटिंग ऑफिसर्स के न्यायालयों को भेजा गया।

#UPRERA #ADJbench #possession #orderexecution #Rule24 #courtreceiver #CPC #homebuyers #realestate

5

7

1,193

शिकायतकर्ताओं की सुविधा के लिए उ.प्र. रेरा पोर्टल- up-rera.in, पर दर्ज की गई शिकायत की स्थिति (Complaint Status) देखने की सुविधा दी गई है।

#UPRERA #complaint #complaintstatus #complainant #orderexecution #orders #proceedings

8

7

490

पोर्टल पर प्राप्त 54,560 शिकायतों में से 46,315 का निस्तारण किया जा चुका है, आदेश अनुपालन के 15,610 अनुरोध में से 12,274 मामलों में अनुपालन कराया जा चुका है तथा कन्सिलीएशन फोरम के माध्यम से रुपये 600 करोड़ से अधिक की सम्पत्ति विवाद मुक्त कराई जा चुकी है।

#UPRERA #orderexecution

36

10

41

3,204

उ.प्र. रेरा के न्यायनिर्णायक अधिकारी श्री आर.पी सिंह द्वारा एक आवंटी की शिकायत की सुनवाई नियम-24 के प्राविधानों के अन्तर्गत करते हुए उसकी इकाई का कब्जा दिलाना सुनिश्चित कराया।

#UPRERA #Rule24 #possession #UPRERArules2018 #promoter #allottees #orderexecution #complaint

4

1

5

1,640

उ.प्र. रेरा ने पीठ द्वारा पारित आदेश का अनुपालन ना किए जाने पर उप्पल चड्ढा हाई-टेक डेवलपर्स प्रा. लि. तथा हेबे इन्फ्रस्ट्रक्चर प्रा. लि. को कठोरतम कार्यवाही किए जाने की चेतावनी देते हुए आदेश का अनुपालन सुनिश्चित करने हेतु अंतिम अवसर प्रदान किया।

#UPRERA #OrderExecution #homebuyer

5

1

2

841

20 Feb 2024

Check out how Enfusion continues to make portfolio management processes efficient and compliant. There's a reason why it's the best in the industry and Oleg Movchan shares why fund managers repeatedly chose Enfusion. #Compliance #FundManagement #OrderExecution

1

1

94

उ.प्र. रेरा अध्यक्ष श्री संजय भूसरेड्डी की पीठ में आवंटियों व प्रोमोटर के मध्य 'यूनिट का कब्जा', 'रिफंड', 'डिले अवधि के ब्याज सहित कब्ज़ा' तथा अन्य प्रकार की शिकायतों का समाधान सुनिश्चित करवाया गया।

#UPRERA #possession #orderexecution #settlement #refund #delayinterest

8

1

7

897