May 20

Good #Q4FY26-20/5/26 post 5pm

JNK India

#JNK

#JNKIndia

Solid Q4FY26🔥👏

Big QoQ and YoY uptick across all parameters

Solid beat vs all estimates

Rev at 338cr vs 190cr, Q3 at 203cr

PBT at 43cr vs 22cr, Q3 at 23cr

PAT at 33cr vs 13cr, Q3 at 18cr

FY26 PBT at 85cr vs 44cr

FY26 PAT at 65cr vs 30cr

1750 cr orderbook

OCF at -2cr vs -65cr

International Gemological Institute

#IGIL

Solid quarter with guidance of 15% rev growth and 20% EBITDA growth for FY27

Good QoQ and YoY uptick across all parameters

Continuess to deliver consistent growth qtrs

Rev at 369cr vs 304cr,last qtr at 320cr

PBT at 239cr vs 191cr, last qtr at 188cr

PAT at 180cr vs 140cr,last qtr at 134cr

OCF at 624cr vs 393cr

Z Tech India

#ZTech

Good Q4FY26 and H2FY26

Good growth in FY26 vs FY25

Rev at 59cr vs 35cr, Q3 at 42cr

Other income at 3.8cr

PBT at 21cr vs 13cr, Q3 at 11cr

PAT at 19cr vs 9cr, Q3 at 8cr

FY26 PBT at 45cr vs 27cr

FY26 PAT at 36cr vs 20cr

Recievables at 94cr vs 47cr

OCF at -38cr vs -91cr

Cosmo First

#CosmoFirst

Solid Q4FY26 with big QoQ and YoY uptick across all parameters

Good margin expansion

Rev at 1020cr vs 746cr, Q3 at 899cr

PBT at 64cr vs 32cr, Q3 at 31cr

PAT at 37cr vs 27cr, Q3 at 20cr

OCF at 397cr vs 166cr

GPT Infraprojects

#GPTInfra

Solid Q4FY26

Good QoQ and YoY uptick across all parameters

Rev at 414cr vs 381cr, Q3 at 284cr

PBT at 41cr vs 29cr, Q3 at 27cr

PAT at 30cr vs 22cr, Q3 at 20cr

OCF at 64cr vs 29cr

Apollo Hospital Enterprises

#ApolloHospital

Good Q4FY26

Consistent performer, despite base getting bigger

Rev at 6605cr vs 5592cr, Q3 at 6477cr

PBT at 721cr vs 515cr, Q3 at 701cr

PAT at 551cr vs 414cr, Q3 at 516cr

OCF at 2855cr vs 2136cr

Blue Water Logistics

#BlueWater

Solid H2FY26

Good uptick vs H1FY26 and H2FY25

Rev at 135cr vs 52cr, Q3 at 112cr

PBT at 12cr vs 6cr, Q3 at 10cr

PAT at 9cr vs 4cr, Q3 at 7cr

FY26 PBT at 33cr vs 14cr

FY26 PAT at 25cr vs 11cr

Metro Brands

#MetroBrands

Good Q4FY26

Seasonality in the business

QoQ isn't comparable as Q3 was a festive quarter

Rev at 773cr vs 642cr

PBT at 157cr vs 126cr

PAT at 118cr vs 95cr

OCF at 473cr vs 698cr

Krishna Defence and Allied Industries

#KrishnaDefence

#KrishnaDef

Rev at 65cr vs 46cr,flat QoQ

Good margin expansion QoQ and YoY

PBT at 16.5cr vs 10.2cr, Q3 at 13.4cr

PAT at 12.3cr vs 7.4cr, Q3 at 10.1cr

OCF at 86cr vs -11cr

Talbros Auto

#Talbros

Rev at 237cr vs 206cr, Q3 at 214cr

PBT at 40cr vs 34cr, Q3 at 34cr

PAT at 32cr vs 27cr, Q3 at 27cr

OCF at 84cr vs 80cr

Bosch

#Bosch

Lower other income makes PBT and PAT look muted

Rev at 5566cr vs 4913cr, Q3 at 4885cr

Other income at 156cr vs 237cr

PBT at 809cr vs 698cr, Q3 at 660cr

OCF at 2175cr vs 2373cr

Indo Tech Transformers

#IndoTech

QoQ slightly muted. Healthy growth YoY

Rev at 238cr vs 206cr, Q3 at 196cr

PBT at 32cr vs 21cr, Q3 at 34cr

PAT at 24cr vs 21cr, Q3 at 25cr

OCF at 57cr vs 55cr

Jay Ambe SuperMarkets

#JayAmbe

Good H2FY26

Rev at 41cr vs 29cr H1 at 31cr

PBT at 4.5cr vs 2cr H1 at 2cr

PAT at 3.3cr vs 1.4cr, H1 at 1.5cr

OCF at 3cr vs -3cr

Finkurve Financial Services

#Finkurve

Rev at 67cr vs 40cr, Q3 at 52cr

PBT at 10cr vs 5cr, flat QoQ

PAT at 8cr vs 4cr, Q3 at 7cr

GNPA and NNPA sharply down YoY

Rajshree Sugars

#RajshreeSug

Rev at 188cr vs 174cr, Q3 at 98cr

PBT at 43cr vs 15cr, Q3 was a loss qtr

OCF at -20cr vs 83cr

Neptune Petrochemicals

#Neptune

Rev at 645cr vs 607cr, H1 at 407cr

PBT at 21cr vs 17cr, H1 at 19cr

PAT at 16cr vs 12cr, H1 at 14.5cr

OCF at -63cr vs 56cr

Remus Pharma

#Remus

Rev at 453cr vs 348cr, H1 at 400cr

PBT at 31cr vs 25cr, H1 at 28cr

PAT at 25cr vs 21cr, H1 at 22cr

OCF at 18cr vs 7cr

XPro India

#XPro

Rev down at 134cr vs 158cr

PBT at 18cr vs 9cr, Q3 at 10cr

PAT at 13cr vs 7cr, Q3 at 7cr

OCF at 20cr vs 13cr

Arvind SmartSpaces

#ArvindSmart

Rev down at 155cr vs 163cr, Q3 at 166cr

PBT at 54cr vs 36cr, Q3 at 39cr

PAT at 44cr vs 22cr, Q3 at 29cr

OCF at -170cr vs -84cr

Decent:

#PEAnalytics

#ACE

#LMW

#Honeywell

#PrimaPlastics

5

19

298

31,105

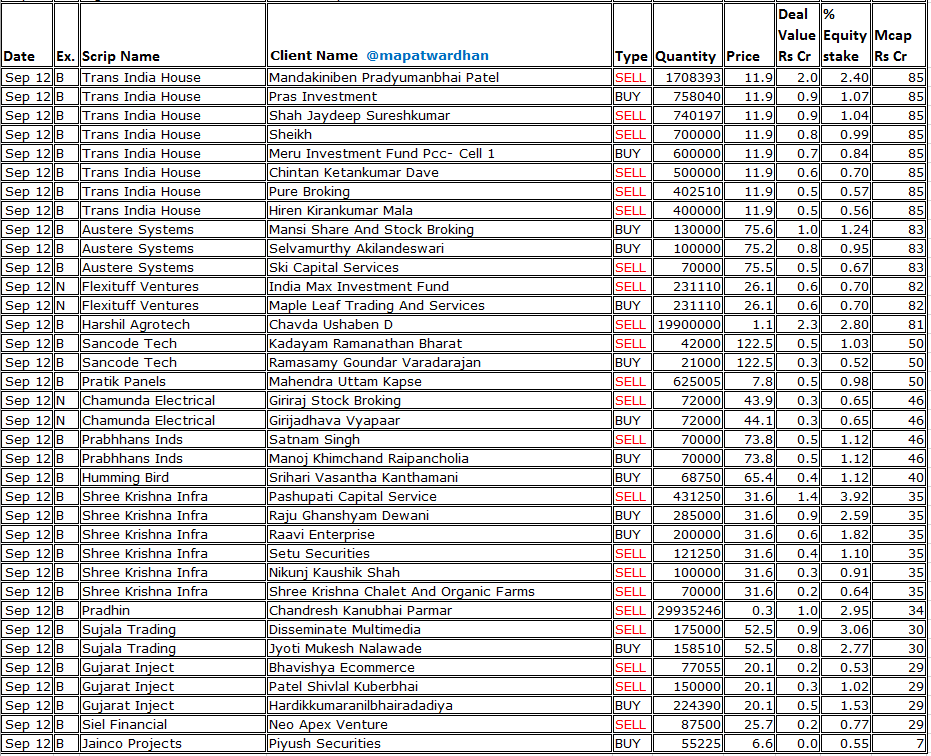

12 Sep 2025

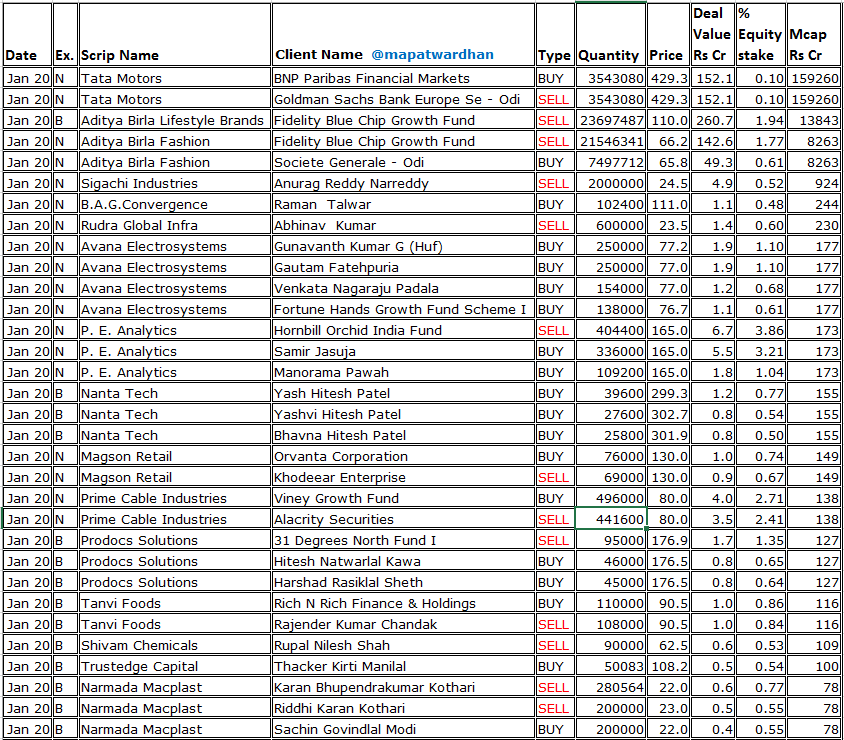

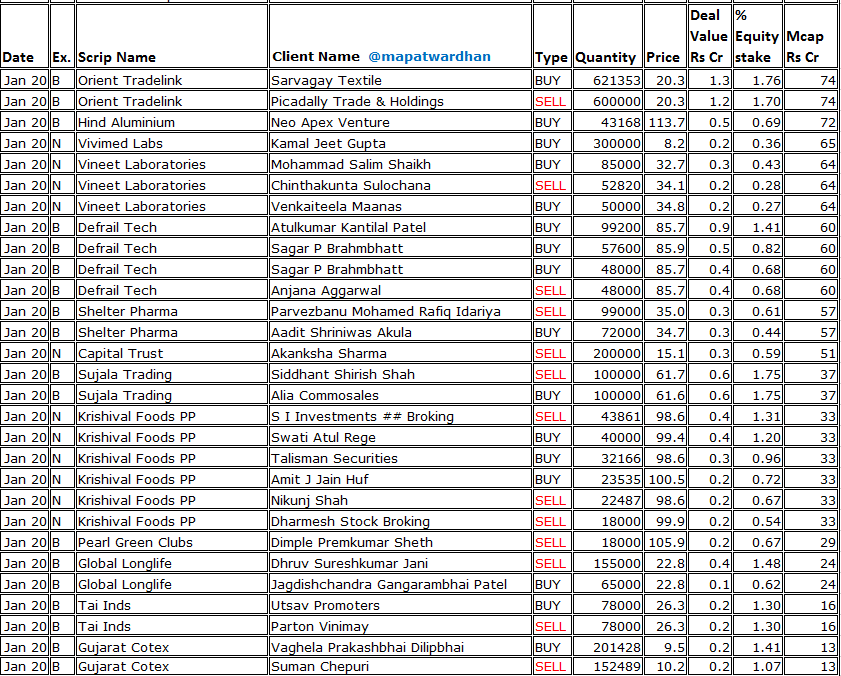

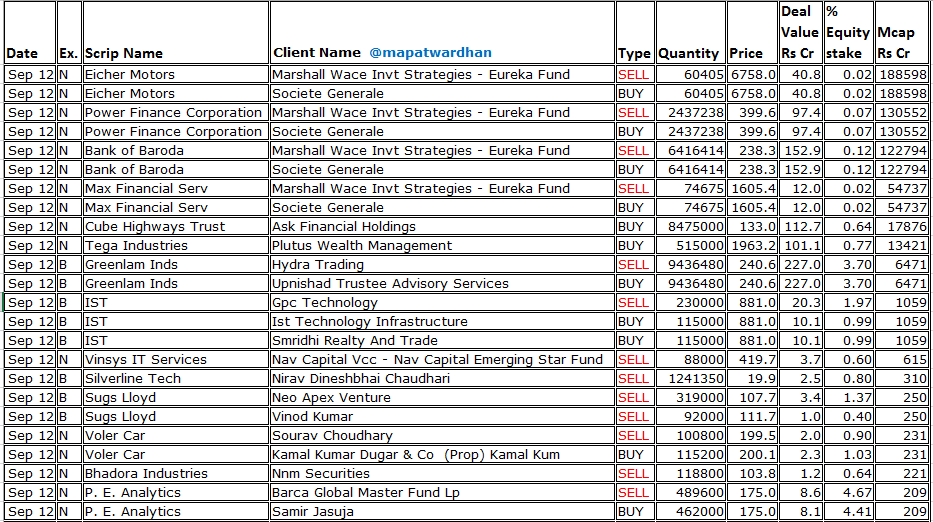

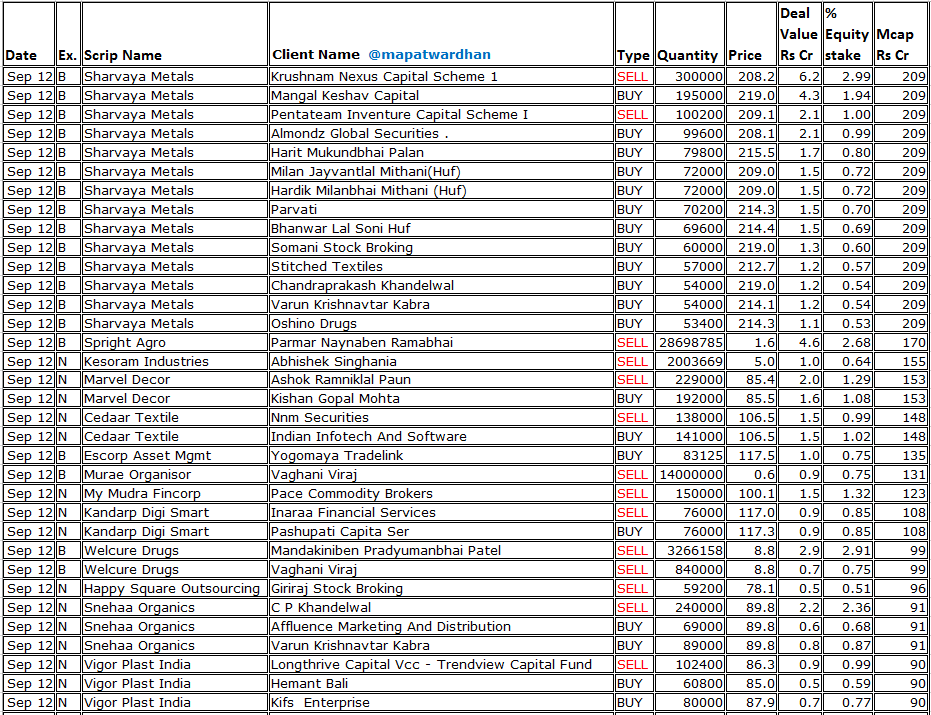

*Today's bulk / block deals*

#EicherMotors #PowerFinance #MaxFinancial #CubeHighways #TegaIndustries #GreenlamInds #IST #VinsysIT #SilverlineTech #SugsLloyd #VolerCar #BhadoraInds #PEAnalytics #SharvayaMetals #SprightAgro #KesoramInds #MarvelDecor #CedaarTextile #WelcureDrugs

1

15

2,386

19 Dec 2024

Curiosity fuels opportunity. A mention of PropEquity in Business Today prompted deeper research into this 40% EBITDA margin, debt-free SME with significant scalability potential.

A conversation with the promoter revealed how their cash-cow database is funding innovative growth initiatives. At KamayaKya, we emphasize identifying businesses where operating leverage drives exponential growth - proving once again that reading and research are invaluable.

SEBI Research Analyst Registration No: INH000009843

Disclosures: bit.ly/DisclosuresKK

.

.

#kamayakya #stockmarket #stockmarketindia #investing #investors #sme #smallcap #propequity #peanalytics #realestate #database #smartinvesting #financereels #reelsvideo #reels

1

3

416

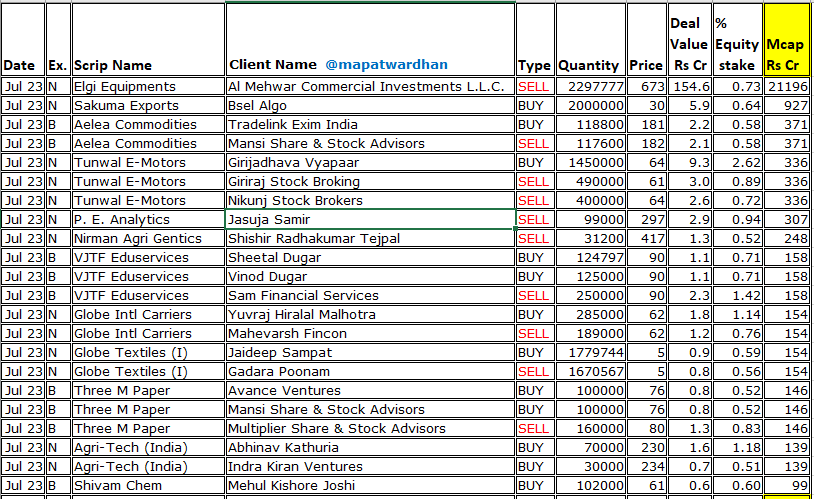

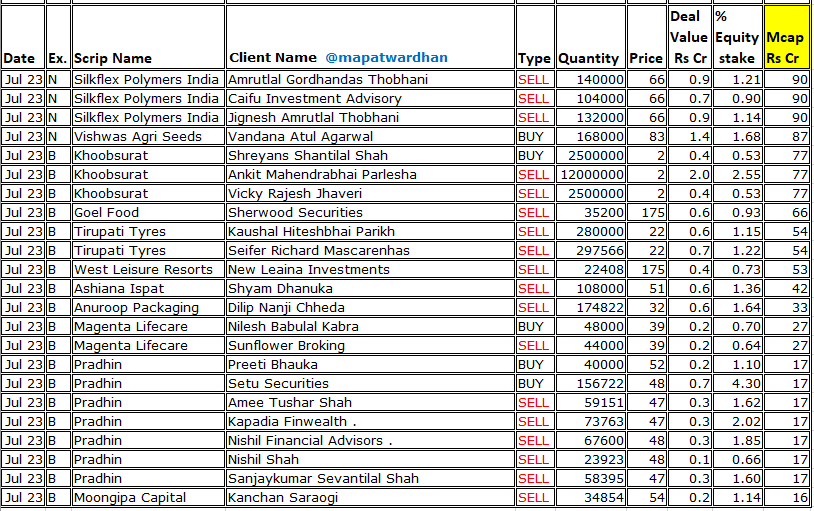

23 Jul 2024

*Today's bulk / block deals*

#ElgiEquipments #SakumaExports #AeleaCommodities #TunwalEMotors #PEAnalytics #VJTFEDuservices #GlobeCarriers #GlobeTextiles #ThreeMPapers #AgriTech #ShivamChem #SilkflexPolymers #VishwasAgri #Khoobsurat #GoelFood #TirpuatiTyres #WestLeisure

1

1

15

4,107

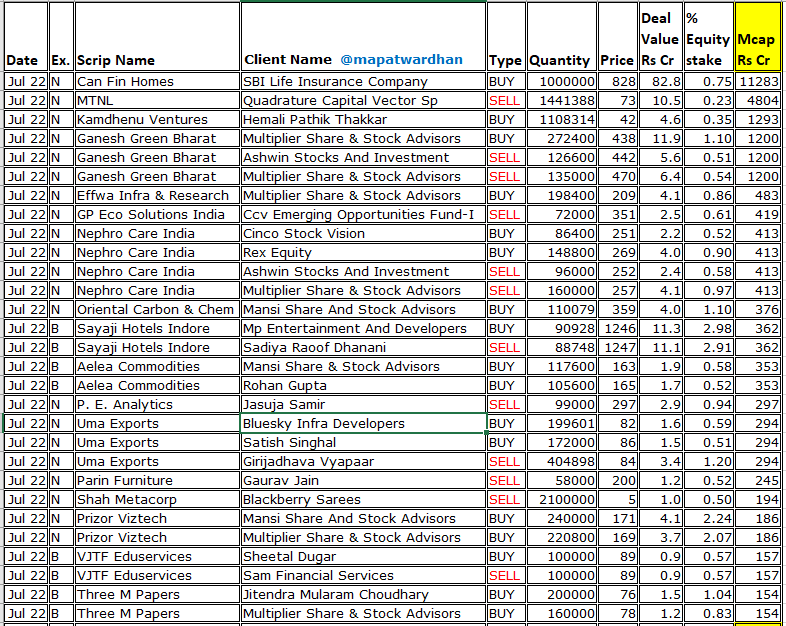

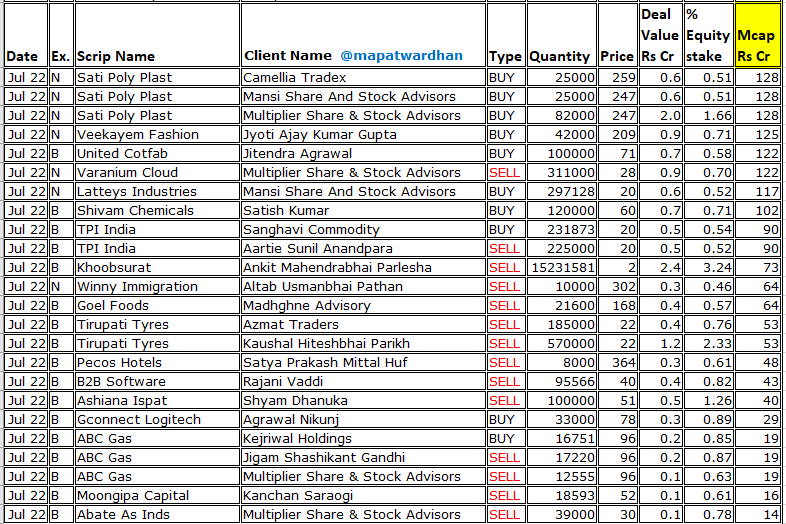

22 Jul 2024

*Today's bulk /block deals*

#CanFinHomes #MTNL #Kamdhenu #GaneshGreen #EffwaInfra #GPEco #NephroCare #OrientalCarbon #SayajiHotels #AeleaCommodities #PEAnalytics #UmaExports #ParinFurniture #ShahMetacorp #PrizorViztech #VJTFEduservices #ThreeMPapers #SatiPoly #VeekayemFashion

1

1

19

8,337

22 May 2024

Key Summary from PropEquity Analytics Ltd. Q4FY24 Concall

Follow 📢, Retweet ♻️ and Share 🔗 for Support Me.

Expansion into Education Vertical

- Leveraging online education with a focus on YouTube following.

- Capitalizing on existing industry connections for employment opportunities.

- Association with industry veterans like Mr. Satish Mehta and Mr. Satish Sachin Tandon.

Delayed Launch

- Education business launch postponed by two years due to current workload.

Monetization Strategies

- Exploring real estate broking for brand monetization.

- Varying unit economics: auto valuation vs. home valuation.

Lead Generation and Inquiries

- Generating leads but not yet passing them to brokers.

- Focusing on customer traction before brokerage.

Real Estate Private Equity Fund

- Interest in setting up a fund, seeking partnership for distribution.

- Aim to utilize data advantage and market expertise.

Project Monitoring Focus

- Prioritizing project monitoring over other ventures.

- Stabilization of YouTube precedes education business launch.

Market Potential

- Project monitoring market size estimated at 2,300 crores.

- Vision to become a 100 crore company within two to three years.

Advertising and Promotion

- Planned expenditure of 2-3 crores per year for business promotion.

- Willingness to increase spending for substantial customer acquisition.

Prop Equity's Growth Strategy:

- Prop Equity aims for significant growth but is cautious about spending, limiting expenses to three crores for model validation.

- The company is expanding its operations in the Middle East with partnerships to leverage shared responsibility and profits.

Valuation Approach:

- Prop Equity emphasizes individualized valuation for properties, contrasting with auto valuations that allow for more aggregated assessments.

- They express confidence in their CEO's capabilities and are open to dilution if suitable partners, especially in private equity, are found.

Subscription Business Potential:

- Prop Equity sees potential in a B2C subscription model but acknowledges the need for substantial marketing efforts to acquire customers.

- They believe in the workability of the model, leveraging their existing team and software infrastructure.

Market Analysis and Projections:

- The company tracks 44 cities and observes 23 lakh properties under construction, signaling a substantial market size.

- They estimate the subscription vertical alone to potentially reach 100 crores, banking on their existing infrastructure and market demand.

Financials and Shareholder Returns:

- Prop Equity aims to maintain a balance between growth and profitability, targeting a turnover between 15% and 25%.

- While they're profitable, they plan to stabilize new business ventures before considering buybacks or dividends for shareholders.

Expansion Plans:

- Prop Equity plans to diversify its offerings into project monitoring, developer asset management, and education, with a focus on stability before further expansion.

- They aim to get listed on the main board of NSE once certain criteria are met, potentially within the next year.

Competition and Market Positioning:

- Prop Equity remains confident in its competitive position, aiming to differentiate itself through specialized offerings and profitability.

- They see themselves as distinct from competitors who may have lower turnovers and less focus on data analytics.

Revenue Sources and Market Dynamics:

- Revenue sources include valuations ranging from 1200 to 3000 rupees per valuation, depending on the client and city.

- Prop Equity sees itself as resilient to market cycles, emphasizing their independence from real estate market fluctuations.

Project Monitoring Vertical:

- While details on the use case and value proposition for retail customers are not provided, Prop Equity is optimistic about the potential of their project monitoring vertical.

- They anticipate growth in this area but are cautious about divulging specific plans due to competitive concerns.

#PEAnalytics

#Concall

#Q4FY24

#TrendingNow

#Trending

#Stockstobuy

#StocksInFocus

#StocksToTrade

#stockstowatch

#BREAKOUTSTOCKS

1

5

1,327

19 Apr 2024

FII Buying Alert!!

FII Holding Increased in #PEAnalytics by 2.41% Compared to last Quarter

CMP: 283.5 | FII Holding: 6.6% | DII Holding: 0% | Promoter Holding: 70.2%

Promoter DII FII Holding = 76.8%

#fii #fiis #fiibuying #investing #StockMarket #IndianMarket #nifty #institution #stockstowatch @CNBCTV18News @ZeeBusiness

3

273

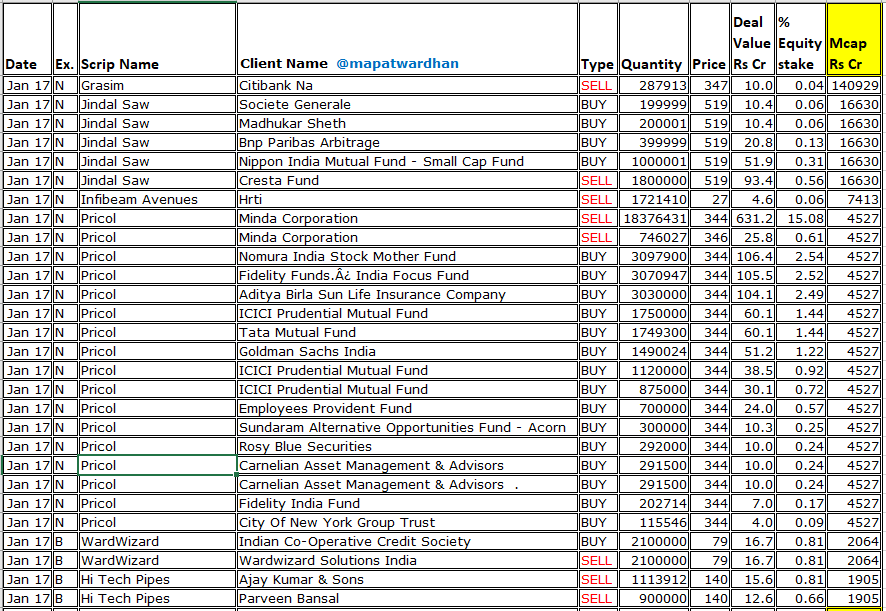

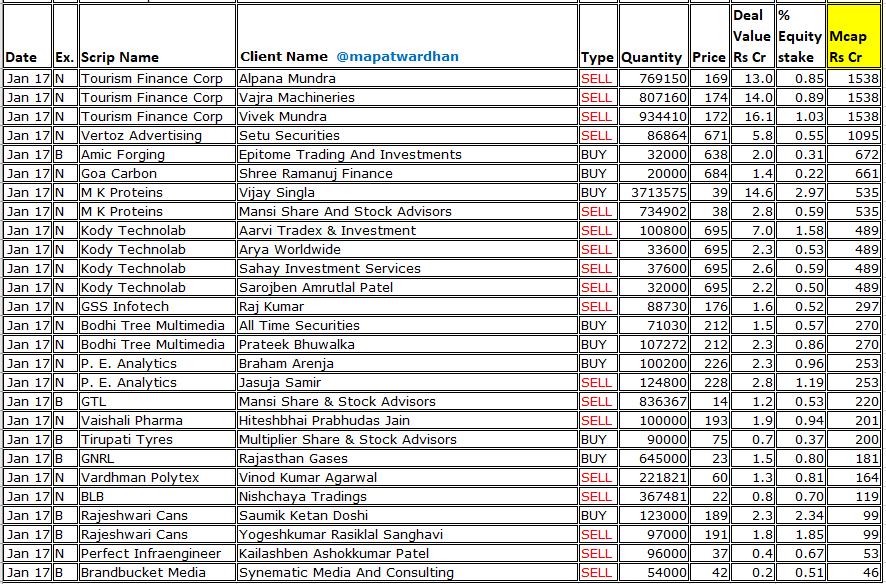

17 Jan 2024

*Today's bulk / block deals*

#Grasim #JindalSaw #Infibeam #Pricol #WardWizard #HiTechPipes #TFCI #VertozAdv #MKProteins #KodyTechnolab #GSSInfotech #BodhiTree #PEAnalytics #VaishaliPharma #GTL #TirupatiTyres #GNRL #VardhamanPolytex #BLB #RajeshwariCans #PerfectInfra #GoaCarbon

1

3

15

6,996

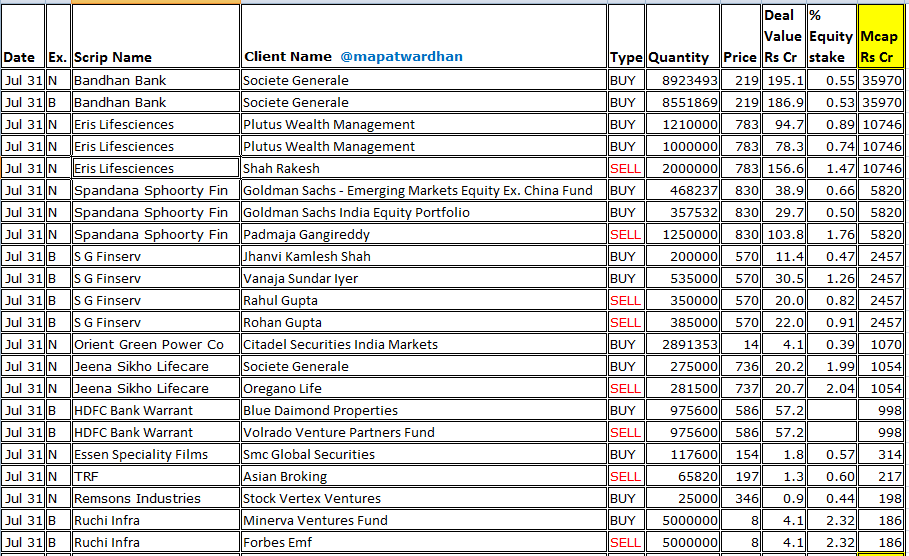

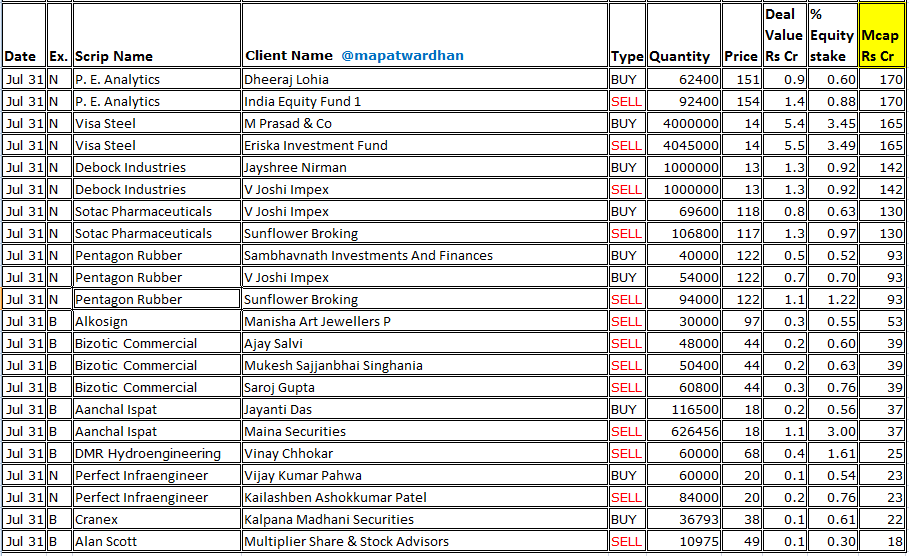

31 Jul 2023

*Today's bulk / block deals*

#BandhanBank #ErisLife #spandanasphoorty #SGFinserv #OrientGreen #JeenaSikho #HDFCBank #EssenSpeciality #TRF #Remsons #RuchiInfra #PEAnalytics #VisaSteel #Debock #SotacPharma #Alkosign #Bizotic #Aanchal #DMRHydro #PerfectInfra #Cranex #AlanScott

1

8

6,411

19 Oct 2022

#DenisChem #KPEnergy

#AvailableFinance #KreonFinanncial #SunilHealthcare #CareerPoint #MarutiInterior #SunEdisonInfra #PEAnalytics #KintechRenewables

Discl: Consider vested interest and bias in all of them. Not recommendations. Do your own due diligence n/n

2

1

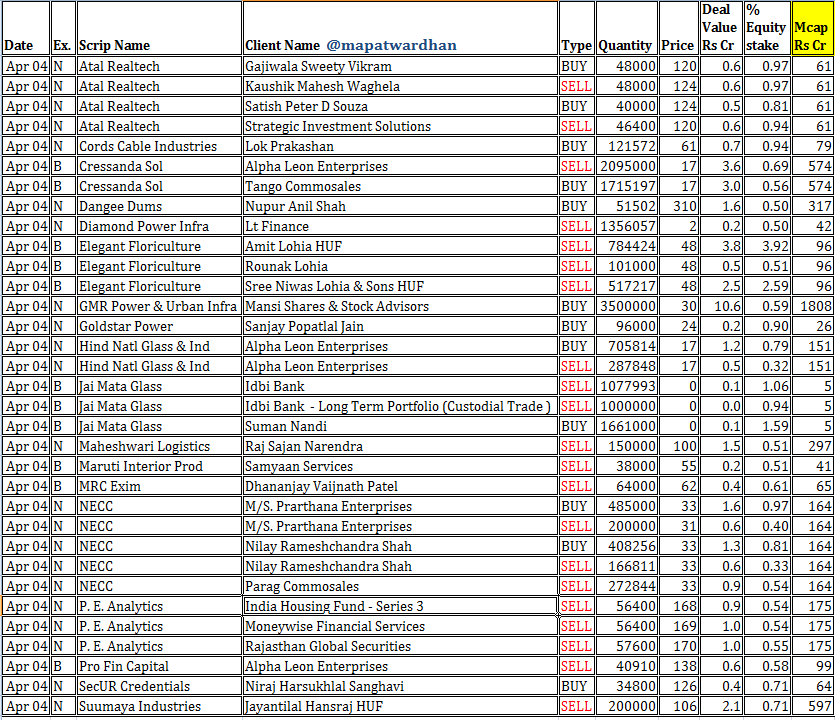

4 Apr 2022

*Today's bulk /block deals*

#Atal #CordsCable #Cressanda #Dangee #DiamondPower #Elegant #GMR #Goldstar #HindGlass #JaiMata #Maheshwari #Maruti #MRC #NECC #PEAnalytics #ProFin #SecUR #Suumaya

1

2

4 Apr 2022

#PEanalytics #PropEquity #IPO

BREAKING - PE Analytics lists with bumper listing gains of 49% on allotment price

ow.ly/BHXg50IzkN4

1

3

31 Mar 2022

Unpredictable nature of #SME

#EmpyreanCahews #Krishival listed at 42 against issue price of 37 at end of day at 44.10

Profit on listing:15000/-

Profit at end of day: 21300/-

Here subscription was

NII: 2.92

Retail: 1.63

Total: 2.28

#KrishnaDefence

#PEAnalytics #hariomipo

2

30 Mar 2022

#PEanalytics #PropEquity #IPO

BREAKING - PEanalytics' IPO allotment status available now

ipocentral.in/pe-analytics-i…

1

2

25 Mar 2022

#TCS acceptance ratio 26%

Baba Ramdev's #RuchiSoyaFPO supported by employees.

Final day final hour of #PEAnalytics

QIB 9.79

NII 69.40

Retail 53.84

Total 34.17

Grand first day subscription for #KrishnaDefence till now 5.5x.

3 more #SME and #HariomPipe (mainline)from 30 to 5.

2

23 Mar 2022

But will not repeat figures of KNAgri because KN was total fresh issue but PEAnalytics is combination of Fresh Issue 1,452,000 Eq Shares OFS 1,320,000 Eq Shares. Again lot of funds will shift toward mainline IPO which is a much safer option than SME IPO.

1