Is AXISCADES moving up the aerospace value chain or selling the business that built its credibility? business-news-today.com/is-a… #AXISCADES #AXISCADEStechnologies #Akkodis #AerospaceManufacturing #DefenceManufacturing #NSE #BSE #SpaceTech #Power930 #IndianStocks

28

Jun 12

🚀 BIG MOVE by $AXISCADES 🚀

✈️ AXISCADES announces the strategic divestment of its Aerospace Engineering Services business to Akkodis, marking a major transformation journey!

🔥 Key Highlights: ✅ 51% stake to be acquired by Akkodis ✅ Fully funds the ambitious #Power930 growth plan ✅ New Space Division 🛰️ ✅ Stronger focus on Aerospace Manufacturing, Defence, AI & Semiconductors ✅ Strategic partnership with a global engineering leader

This isn't just a transaction—it's a bold step toward becoming a next-generation aerospace, defence, space & AI powerhouse. 💥

#AXISCADES #Aerospace #Defence #SpaceTech #AI #Semiconductors #MakeInIndia #AtmanirbharBharat #StockMarket #NSE #BSE

1

127

Jun 8

Fair point on needing clearer visibility.

If you go through their earlier concalls , mgmt has outlined a broad Power930 roadmap — not quarterly milestones, but a clear strategic shift:

Moving from pure services to products solutions (targeting ~80:20 product/services mix eventually) — monetising decades of design/engineering work into manufacturing & recurring revenue.

Massive capex underway:

DAL (Devanahalli Aeroland) — already operational (1.65L sq ft).

DAC (Devanahalli Atmanirbhar Complex) — Phase 1 by Mar’27 (~₹1300 Cr planned).

MAC (Hyderabad Missile Complex) — by Mar’27 (~₹300 Cr).

Defence-focused strategy: Strong ties with DRDO, MoD orders, and foreign OEMs (e.g., MBDA partnership for missile integration at DAC).

Strategic acquisitions to bolt on capabilities.

Essentially, the thesis is Defence Aerospace ESAI (Electronics, Semiconductor, AI) manufacturing.

They’re building platforms, leveraging global OEM partnerships, and scaling existing design relationships into large production programs. Execution risk is real (as with any 9x growth in ~4 years)

Lets see how far and what they can achieve, the mgmt was very bullish though in latest concall.

1

85

May 27

x.com/i/status/1969414889627…

🚨 AXISCADES TECHNOLOGIES 🚨

At first glance:

Q4 looked weak. (सिर्फ headline नंबर padhna यहां खतरनाक है)

PAT collapsed:

⚠️ ₹31 Cr → almost breakeven.

Retail panic:

“Business kharab ho gaya?”

But REAL story is MUCH deeper.

---

BIGGEST thing happening inside AXISCADES:

🚨 Defence becoming the MAIN ENGINE.

FY26 Defence EBIT:

🔥 ₹43 Cr → ₹83 Cr.

Almost:

⚡ 2X jump.

This is NOT normal.

Management clearly shifting company from:

❌ generic engineering services

towards

✅ defence

✅ aerospace

✅ high-value engineering.

And market usually gives:

MUCH higher multiples to this transition.

---

Now understand the STRATEGIC MASTERSTROKE.

Company announced:

🚨 sale of heavy engineering automotive energy engineering business

to #Akkodis.

Why important?

Because management basically saying:

❌ commoditized low-margin work

→ exit gradually.

✅ focus capital on:

- defence

- aerospace

- electronics

- mission-critical engineering.

Honestly?

This is EXACTLY what smart capital allocation looks like.

---

But NOW comes the REAL concern.

Q4 profitability collapse wasn’t random.

Company booked:

⚠️ goodwill impairment.

Meaning:

some acquired assets likely underperforming expectations.

This is VERY important.

Because market currently loves:

🔥 defence narrative

🔥 aerospace theme

🔥 Make in India story.

But acquisition quality eventually matters.

---

Another hidden positive?

🚨 Receivables sharply improved.

Trade receivables:

₹411 Cr → ₹301 Cr.

This matters A LOT.

Because engineering companies often:

⚠️ show profits

but

⚠️ cash gets stuck in receivables.

Improvement here:

positive signal.

---

BUT,

cash balance declined.

And goodwill still remains HIGH.

Meaning:

execution risk still exists.

This is NOT:

❌ clean predictable compounding story yet.

This is:

🚨 transformation execution story.

---

Most important thing investors should track now:

✅ Defence order execution

✅ Aerospace scaling

✅ Akkodis transaction completion

✅ Margin stability

✅ Cash-flow quality

✅ Future impairments.

Because honestly,

market currently pricing:

🔥 future defence potential.

Not current stable earnings quality.

---

If management successfully transforms AXISCADES into:

🚀 defence-focused engineering platform,

then rerating can become VERY powerful.

But if:

⚠️ execution slips

⚠️ impairments continue

⚠️ acquisitions disappoint

market confidence can reverse quickly.

---

My REAL takeaway?

AXISCADES is no longer trying to be:

“another engineering services company.”

It is trying to become:

🚨 India’s aerospace defence engineering platform.

And THAT is the entire investment thesis now.

THIS IS MY INITIAL COMMENT,

WAITING FOR MANAGEMENT COMMENTARY.

In short run you can feel the pain and that pain you know what will i do. But growth trajectory is still intact.

#POWER930 VISION still intact

[Mngmt = FY2030 target

Revenue upto 9000 Cr

Net profit upto 960 Cr]

#AXISCADES #DefenceStocks #Aerospace #IndianStockMarket

20 Sep 2025

Back on 12 June 2024, when #Axiscades was at ₹478, many doubted.

I believed. I shared. I held.

📈 Today it’s ₹1692. A true multibagger journey 🚀🔥

👉Lesson: Markets reward conviction, patience & courage. Doubt fades, discipline pays.

#StockMarket

1

1

3

1,155

Apr 30

#Axiscades Given the Power930 vision, even if the company achieves 50% of FY30 revenue target-i.e. ~ 4500 crores, with ~900 cr EBITDA (20%) and at a very conservative 20 EV/EBITDA multiple, we are looking at a minimum EV of 18,000 crores.

5

707

Apr 19

👉 Funding locked with no equity dilution and no material long-term debt.

Key trackables:

• Margin expansion

• Revenue shift: services → high-margin products & manufacturing

• Defense evolution: sub-systems → full systems provider

• No External funding (no equity dilution or heavy debt)

Bottom line:

→ Axiscades is executing a rare transition - moving away from dying-margin services toward high-margin products, solutions and advanced manufacturing in Aerospace, Defense and AI.

→ Power930 vision of ₹9,000 Cr by 2030 has real legs now that facilities are coming alive, seekers are qualifying, hyperscalers are engaging deeper, and big-ticket partnerships are landing.

→ This isn’t another plain engineering services story. It’s India building real Atmanirbhar capability with global scale.

Disclaimer: I am personally invested, please do your own DD.

4

1

9

1,482

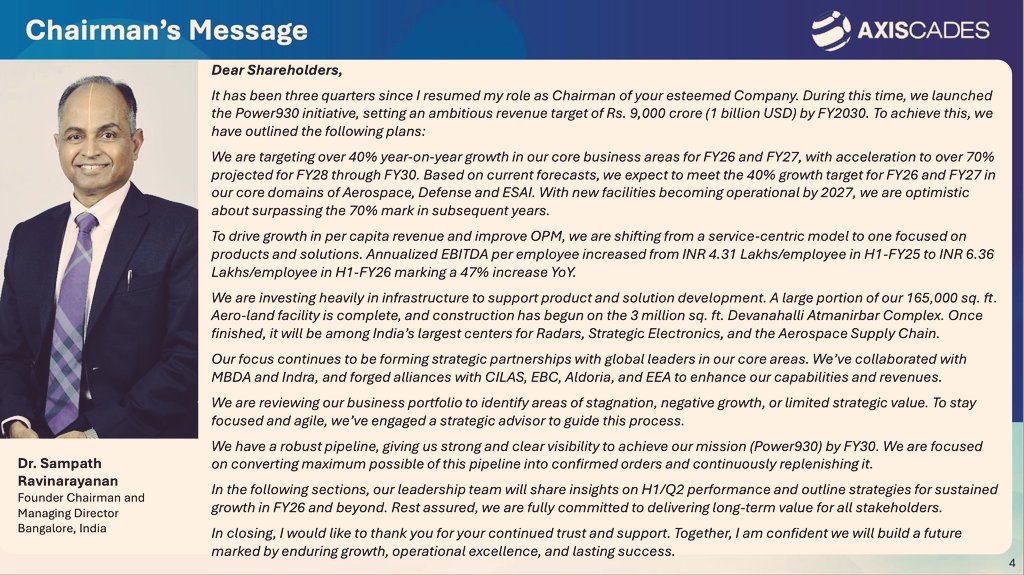

Mar 28

AXISCADES Technologies: Key Catalysts

#AxiscadesTech

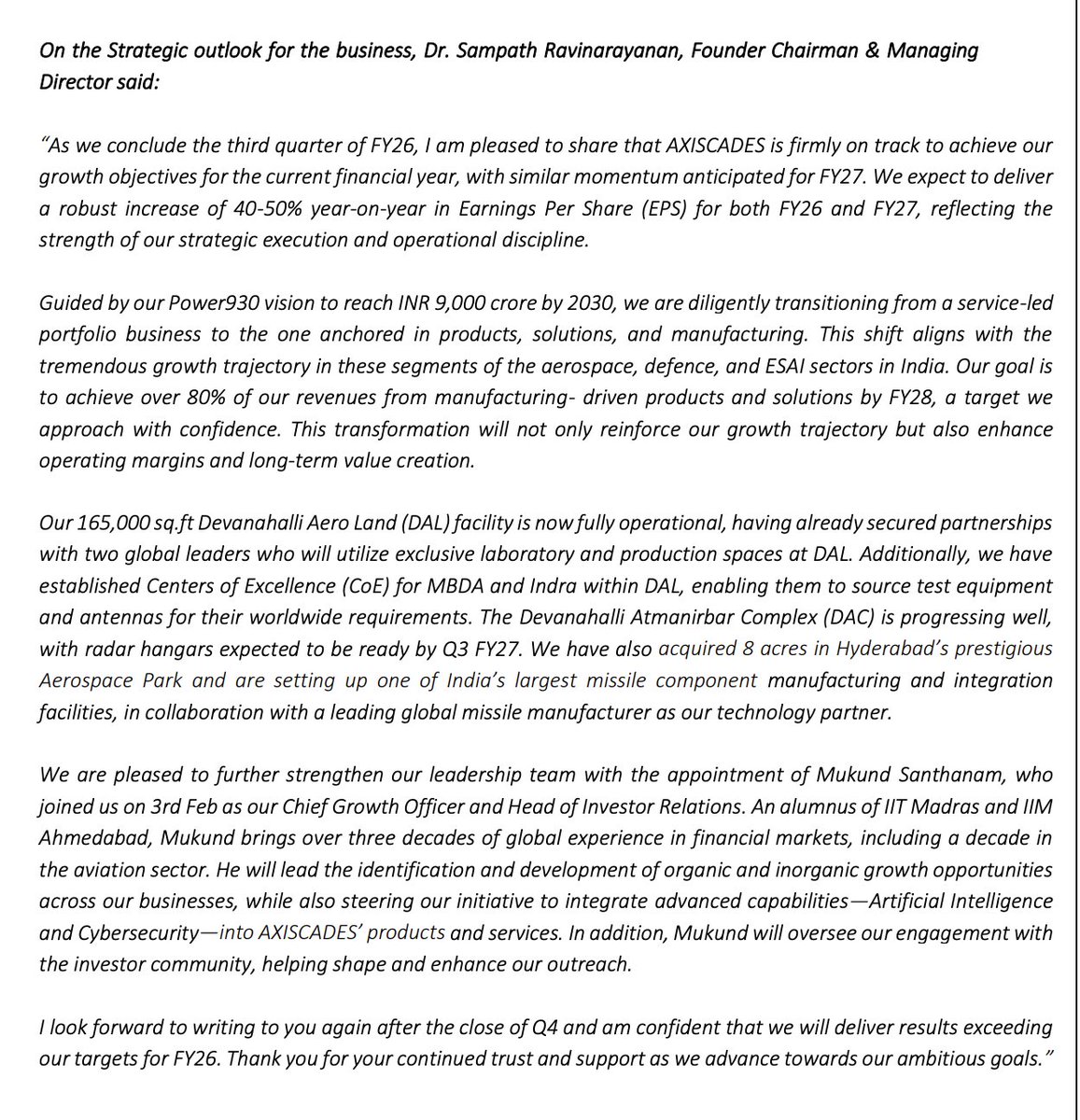

AXISCADES is developing RF seeker technologies for advanced missile platforms including BrahMos and Kusha programs, with successful trials completed in February 2026, strengthening its position in strategic defence electronics.

The company is expanding into AI-driven unmanned systems through collaboration with a globally established U.S. defence technology partner to bid for large-scale unmanned combat management programs.

Management has guided for strong financial growth, with:

EPS growth: 40%–50% annually in FY26 & FY27

Revenue growth: 40% YoY (core business)

EBITDA growth: At least 45% targeted by FY27

The company has strong revenue visibility, supported by:

Order book: Rs. 3,300–3,400 crore

Qualified pipeline: Rs. 14,000 crore over the next 4 years

High expected conversion from OEM programs and defence contracts

Under its Power930 vision, the company is targeting revenue of Rs. 9,000cr by 2030, supported by expansion into defence manufacturing, electronics, semiconductors, and advanced aerospace systems.

Disclaimer: This is for educational purposes only and not a recommendation to buy or sell.

3

210

Feb 26

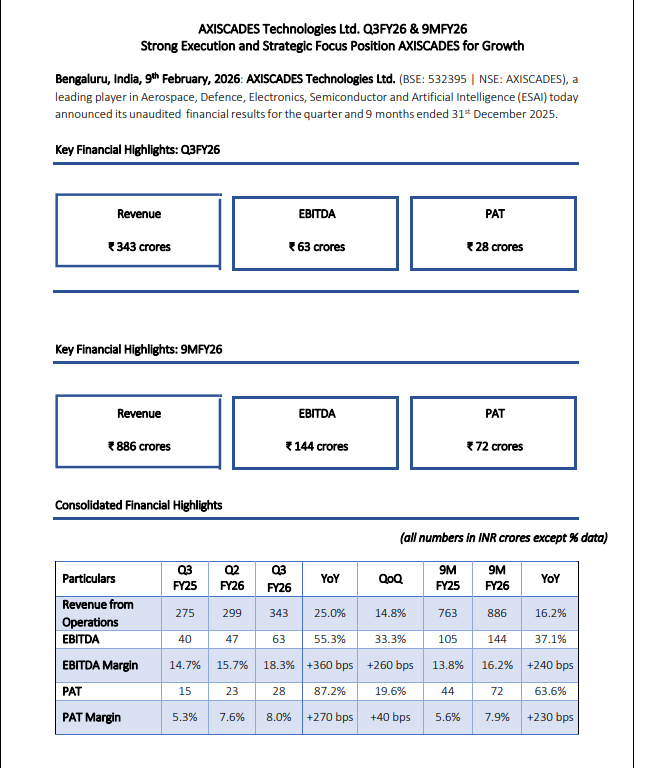

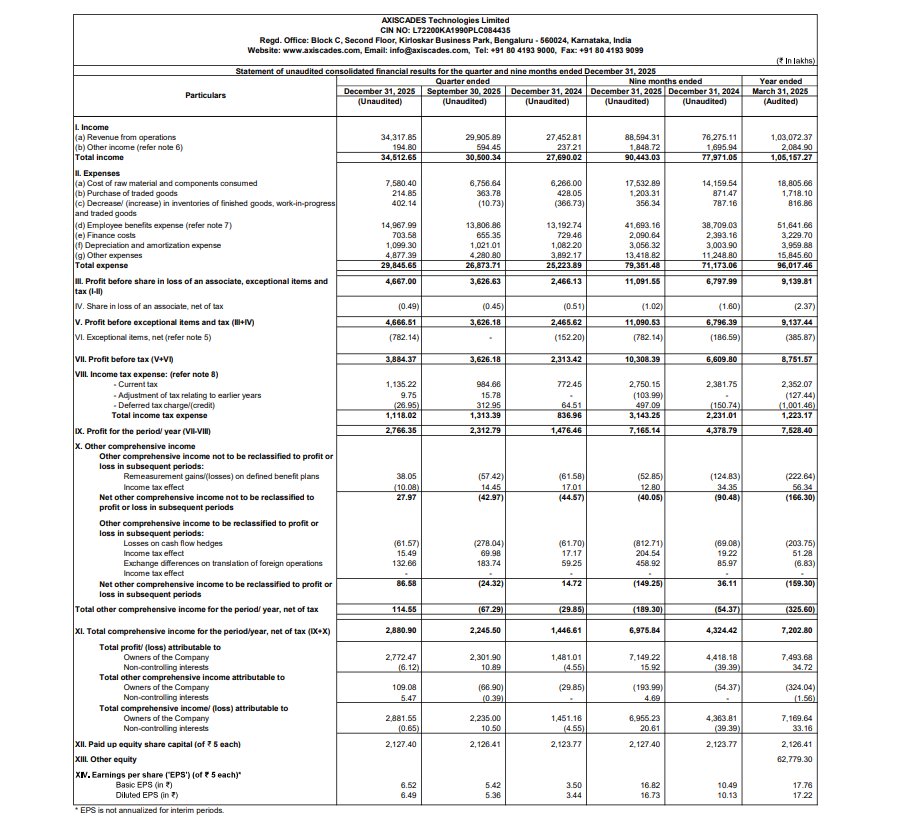

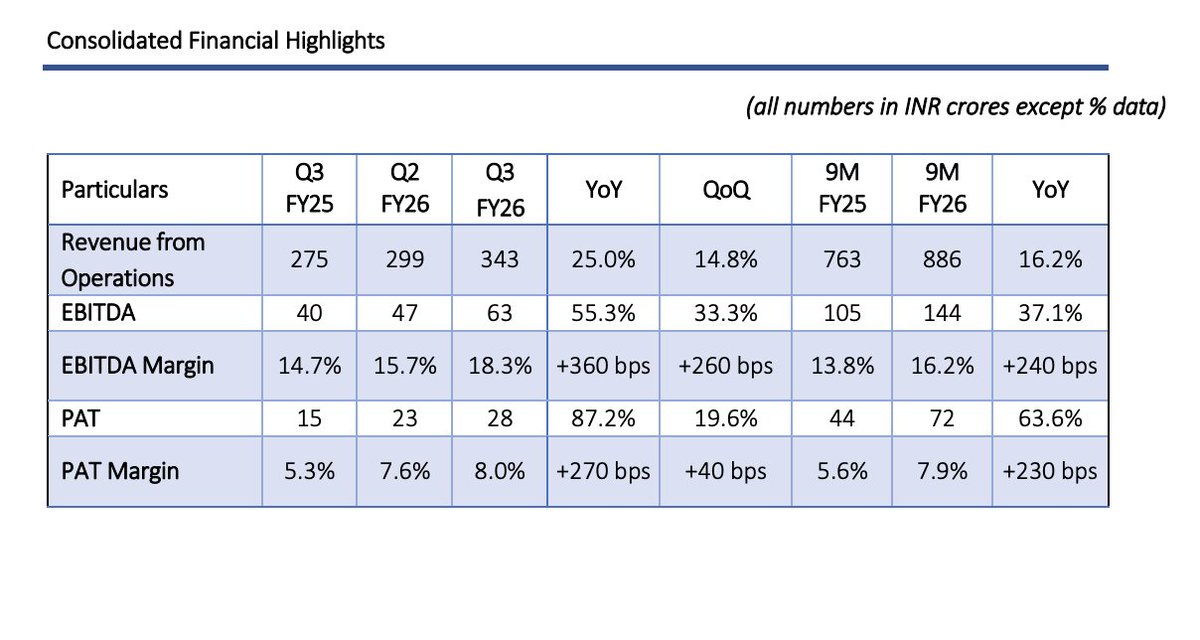

AXISCADES Technologies Ltd Concall Summary for Q3FY26

1) Financial Performance

• Q3 Revenue: ₹343 Cr ( 25% YoY · 14.8% QoQ)

• 9M Revenue: ₹886 Cr ( 16.2% YoY)

• 9M EBITDA: ₹144 Cr (Exceeds FY25 full-year) · Margin ~20% ( 240 bps YoY)

• Q3 PAT: ₹28 Cr ( 87% YoY) · Margin ~8%

• 9M PAT: ₹72 Cr reported · ₹79.5 Cr adjusted (ex-Labour Code impact)

• ESOP Expense: ₹5 Cr (9M) · ~₹2 Cr/quarter run-rate

• Depreciation: ~₹1 Cr/quarter (to rise as capex capitalizes)

2) Order Book & Revenue Visibility

• Total Order Book: ₹3,400–3,500 Cr

• Core Domain FY26 Order Book: ₹1,260 Cr

• FY26 Pipeline: ₹1,060 Cr expected · ₹200 Cr shifted to FY27

• Near-Term Wins: ₹400 Cr expected next month

• Sales Pipeline (4-year): ₹14,000 Cr

• Strong visibility aligned with current order book execution

3) Product & Segment Mix

• Defence Revenue Contribution: ~40% of total

• Revenue Mix: 39% products/solutions · 61% services

• 78% revenue from defence, aerospace & ESAI ( 36% YoY)

• Core Business Contribution: 21.4% ( 270 bps YoY)

• Product Margin: 25–26%

• Services Margin: ~18.5% (pressure in core services <5% EBITDA)

• Strategic pivot toward product-led model by FY27

4) Defence & Aerospace Highlights

• RF seekers trial success for BrahMos & Kusha missiles

• Mission computer deployed across Tejas platforms (scalable to Sukhoi & others)

• TACAN development completed; production orders expected

• Active programs in AI-enabled combat systems & autopilot technologies

• Aerospace transitioning toward manufacturing-led execution

5) Manufacturing & Capex Expansion

• Multi-year Capex Cycle: FY26–FY28

• MAC Facility: 8 acres (missile electronics focus)

• Radar Hangar: 60 ft height capacity for retrofit programs

• DAL & DAC facilities enabling end-to-end defense solutions

• Test Kit scalability: 50x–100x growth potential

• Hyderabad & Bangalore hubs centralizing missile & radar ops

6) Customer & Partner Pipeline

• MOU with Indra Sistemas – preferred India partner

• OEM offset-driven growth gaining traction

• ESAI pilot orders: $1.5–2M per project

• QRSM order expected closure shortly

• Strong hyperscaler engagement; India emerging as manufacturing hub

• U.S. facility certification to unlock global OEM orders

• AI-driven drone partnership with global defense player

7) Risks & Order Uncertainty

• MOD/PSU orders remain lumpy & timing-dependent

• Large defense order conversion probability ~10% (high bid risk)

• Competitive intensity limited → supports sustainable margins

• Make-in-India tailwinds from 2025–26 missile indigenization

8) Guidance & Outlook

• Core Business Growth: >40% in FY26

• FY27 Target: 40–50% growth

• FY28 Projection: ~70% growth

• EPS Guidance: 40–50% CAGR (FY26–FY27) · ₹25–26 expected this year

• FY27 Core Order Book for Execution: ~₹1,050 Cr

• Long-Term Target: ₹9,000 Cr revenue by 2030 (Power930 vision)

• Margin Aspiration: 25% overall margin in 4–5 years

• Product Mix Target: 80% products/solutions over time

Key Takeaway

• Strong Q3 revenue acceleration with sharp PAT growth

• EBITDA run-rate already ahead of FY25 full-year

• Structural shift toward high-margin product-led defense model

• Massive capex building one of India’s largest private defense ecosystems

• ₹14,000 Cr pipeline offers multi-year growth visibility

• Execution & MOD order timing remain key monitorables

2

164

Feb 20

AXISCADES Technologies Ltd - Q3FY26 | Concall Insights

Financial Highlights:

•Q3FY26 revenue ₹343cr; 25% YoY; 14.8% QoQ

•Q3FY26 EBITDA ₹63cr; 55% YoY

•Q3 EBITDA margin 18.3%; 360bps YoY (highest ever)

•Q3 PAT ₹28cr; 87% YoY; 8% margin

•Adjusted Q3 PAT ₹35cr; 10.3% margin (ex-Labour Code impact)

•9MFY26 revenue ₹886cr; 16.2% YoY

•9MFY26 EBITDA ₹144cr; margin 16.2% vs 13.8% YoY

•9MFY26 PAT ₹72cr; adjusted ₹79.5cr (exceeded FY25 full-year PAT)

•9MFY26 EPS ₹16.73; 65% YoY

•Net worth ₹730cr; net debt ~₹67cr

Growth Domains (Aerospace, Defence, ESAI):

•Growth domains contribute 78% of revenue; 36% YoY growth

•EBITDA margin in growth domains 21.4% vs 18.7% YoY

•Core FY26 execution target ~₹1,050cr (vs ₹750cr FY25; 40% growth)

•FY27 core growth guided at 40%–45%

•EPS growth target 40%–50% annually; FY26 EPS ~₹25–26 indicated

Margins:

•Services EBITDA ~18.5%; product & solutions 25%–30%

•Target FY27 consolidated EBITDA margin ~20%

•Long-term aspirational margin 25% with 80% product mix

•ESAI EBITDA ~26%; Defence ~25% currently

•ESOP cost ~₹5cr (9MFY26); expected to rise in FY27

Order Book:

•Forecast visibility ₹3,300–3,400cr

•Qualified pipeline ₹14,000cr over next 4 years

•Overall conversion ratio estimated 50%–60%

•₹200cr of FY26 core revenue deferred to FY27 (facility dependent)

•₹400cr defence orders expected near term

Product Mix:

•Product vs services mix 39:61 (vs 33:67 YoY)

•Target to flip mix towards products majority by FY27

•Transition from services-led to manufacturing & solutions-led model (Power930 vision)

•Long-term revenue vision ₹9,000cr by 2030

•Focus areas: Defence, ESAI, advanced manufacturing, AI-driven systems

Defence Business:

•RF seeker for BrahMos & Kusha progressing; trials ongoing; qualification expected by Q2

•Mission computer developed for LCA; platform agnostic

•Focus on missile electronics, seekers, data links, integration (Missile Atmanirbhar Complex)

•Radar integration & MRO facility under development (DAC)

•Unmanned AI-enabled combat systems bidding with global partner

•QRSM order decision expected shortly

Hyperscalers:

•Pilot orders from hyperscalers; potential 10x–100x scale over time

•Box-build & test solutions for global OEMs

•Recurring annual replacement cycle for test kits

•Large lab capability build-out (acoustic, IR, mmWave, sensor fusion)

•Major revenue ramp expected from FY28 onward

Capex:

•Devanahalli Aero Land (DAL) operational

•Devanahalli Atmanirbhar Complex (DAC) under development (radar, aerospace, simulators)

•Missile Atmanirbhar Complex (MAC) in Hyderabad (8 acres) for missile electronics & integration

•Capex cycle continues through FY27–FY28

•Facilities to enable manufacturing-led growth & OEM partnerships

Divestment:

•Non-core verticals ~22% revenue; recalibration underway

•Divestment on track; expected resolution by next investor call

•Headcount rationalization ongoing; attrition not backfilled

Geographical Mix:

•Balanced 1/3 U.S., 1/3 Europe, 1/3 India target mix

•U.S. growth driven by ESAI & hyperscalers

•Europe strength in aerospace & defence; benefit from EU FTA

Other Key Updates:

•Annualized revenue per employee ₹0.54cr; 38% YoY

•Strong deal momentum & global OEM partnerships

•Focus on AI-driven autonomous systems, radar, missile electronics

•Target to be leading private-sector defence electronics & advanced systems player

•Long-term structural shift toward high-margin product platforms

3

176

🚀 AXISCADES Q3 FY26: The Defence-Tech Transformation Story You Need to Know

Just analyzed Axiscades' latest earnings call, and this is shaping up to be one of India's most exciting defence-tech turnaround stories. Here's the deep dive 🧵

💰 THE NUMBERS THAT MATTER

Q3 FY26 was nothing short of exceptional:

Revenue: ₹343cr ( 25% YoY, 15% QoQ)

EBITDA: ₹63cr at 18.3% margin (360 bps expansion!)

Adj. PAT: ₹35cr at 10.3% margin

EPS (9M): ₹16.73 ( 65% YoY)

But here's the kicker - 9M EBITDA of ₹144cr has ALREADY surpassed FY25's full-year EBITDA. They've essentially delivered last year's annual performance in just 9 months.

THE POWER930 VISION: FROM SERVICES TO MANUFACTURING

This isn't just another IT services story. Chairman Dr. Ravinarayanan is orchestrating a fundamental business model transformation:

Current State (9M FY26):

Products & Solutions: 39%

Services: 61%

FY27 Target:

Products & Solutions: 61%

Services: 39%

FY28 Aspiration:

Products & Solutions: 80%

Services: 20%

Why does this matter? Product margins are at 25-30% vs services at 18.5%. This flip will fundamentally reshape profitability.

The endgame? ₹9,000 crores by 2030 (Power930 vision).

⚔️ DEFENCE: THE CROWN JEWEL (50% YoY GROWTH!)

Defence has become the star performer with ₹311cr revenue (9M) at 23.7% EBITDA margins.

The Triple-Engine Strategy:

1️⃣ DRDO/PSU Programs (Stable base):

5-year visibility on most programs

Current major revenue contributor

50% win rate (2 winners per program)

2️⃣ MOD Direct Bids (High upside):

Government procurement programs

Multiple RFPs in pipeline

Results expected Q1-Q2 FY27

3️⃣ Global OEM Offsets (Growth driver):

Management's main focus area

Near 100% conversion on relationship-based deals

Long-term partnerships being signed

✈️ AEROSPACE: PIVOTING TO MANUFACTURING

₹282cr revenue (9M) at 18.3% EBITDA margins

President KP Mohanakrishnan (20 years in greenfield manufacturing) is driving the shift: "AXISCADES is evolving into a product-oriented business anchored around supply chain, manufacturing, and aftermarket solutions"

Strategic partnership with OGMA, Portugal for aerospace engineering & MRO adds European capabilities.

5th consecutive diamond supplier award from Bombardier validates quality standards.

🔌 Electronics Semi Conductors and AI (ESAI): THE HYPERSCALER OPPORTUNITY

₹98cr revenue (9M) at 24.4% EBITDA margins (highest across segments!)

100% revenue from US market.

The Hyperscaler Play:

Recent wins: $1.5-2mn pilots with 3 major global customers

One hyperscaler (home automation/sensors)

One US homeland security major

Multiple silicon OEMs

Scale-up potential? Chairman's bold projection: "50-100x from current levels if we do it right"

But temper expectations - FY27 will see order book build. Real revenue impact: FY28 onwards.

The Recurring Revenue Goldmine:

For a major hyperscaler manufacturing in India:

a) Axiscades provides test kits for EVERY production

station

b) These kits must be changed EVERY YEAR

Currently: 1-2 items for 1 production line

Opportunity: Multiple lines global scale

Chairman: "Margins are very, very good, as good as defence margins or even more in certain cases"

Competition? Only 3-4 players globally.

🏭 INFRASTRUCTURE: THE GROWTH MULTIPLIERS

Devanahalli Aero Land (DAL) - FULLY OPERATIONAL

165,000 sq ft

EMS line, Acoustic Lab, ESD Test Labs complete

Secured 2 global leaders for exclusive lab/production spaces

CoEs for MBDA & Indra established

Enabling "Make in India" global opportunities

Devanahalli Atmanirbhar Complex (DAC) - IN PROGRESS

Radar hangars ready by Q3 FY27

"Arguably one of the biggest radar facilities in India"

Capabilities: Building large radars, maintenance, retrofitting, performance-based logistics

Missile Atmanirbhar Complex (MAC) - Hyderabad

8 acres in Aerospace Park acquired

Partnership with leading global missile manufacturer

"One of India's largest missile component manufacturing facilities"

Focus: Seekers, onboard electronics, data links

Timeline: Operational in 2 years

"One of the finest facilities outside public sector

📊 THE ORDER BOOK & PIPELINE

1) Forecast Visibility (Firm): ₹3,300-3,400cr

a) Enough to deliver FY27 targets comfortably

b) 5-year visibility on most DRDO programs

2) Total Pipeline: ₹14,000cr over next 4 years

a) 50-60% overall conversion rate expected

b) OEMs: ~100% conversion (relationship-based)

c) DRDO: 50% conversion (2 winners per program)

d) MOD: Variable (competitive bidding)

3) Near-term catalysts:

a) QRSM order expected "within 2 weeks"

b) ~₹400cr of wins expected in next month

c) Multiple customer visits at DAL in Feb-March

💡 THE MARGIN STORY

FY27 Target: 20% EBITDA margin (vs 17% in FY26)

Aspirational (Post-FY28): 25% EBITDA margin

Chairman: "We want to be among the top margin companies in the country"

How?

a) Shift to 80% products/solutions (25-30% margins)

b) Services margin declining (struggling at 18.5%)

c) Operating leverage from new facilities

d) Non-core business divestment (on track)

Core domain margins already at 21.6% (vs 16.2% overall).

🌍 GLOBAL FOOTPRINT

1) Target mix: 1/3 US | 1/3 Europe | 1/3 India

2) US Growth: ESAI-driven (hyperscalers silicon OEMs)

3) Europe Growth: Aerospace & Defence partnerships

Strategic partnerships with MBDA, Indra, OGMA

4) International pipeline: $300mn for Q4 FY26 & Q1 FY27 closures

Not impacted by tariffs in current business model

📈 THE GUIDANCE (Management's Own Words)

1) FY26: 40-50% EPS growth ✅

a) Target EPS: ₹25-26 (vs ₹17.63 in FY25)

b) On track with Q4 expected to be "very good"

2) FY27: 40-50% EPS growth (reconfirmed)

a) 45% EBITDA growth (conservative estimate)

b) 40% core business growth

c) Chairman: "We are firmly on track. I can assure you"

3) FY28: Strong growth with facility contribution

a) 3-pronged approach: Organic Inorganic Facility-based

b) Multiple acquisitions being evaluated

c) Heavy dependency on DAL, DAC, MAC becoming operational

⚠️ THE NON-CORE

Heavy Engineering, Auto, Energy: ₹194cr (22% of revenue)

-3% EBITDA margin (dragging down overall margins)

De-growth of 8.5% YoY

Macro headwinds customer-specific issues

Good news? Divestment on track.

Chairman: "Very much on track... Definitely by next investor call, we should be able to share all the details"

Once this exits, watch the margin profile transform.

🧠 LEADERSHIP STRENGTHENING

New hire: Mukund Santhanam (Feb 3, 2026)

IIT Madras IIM Ahmedabad

30 years global financial markets experience

10 years in aviation sector

Role: Chief Strategy & Growth Officer Head of IR

Focus areas:

Organic & inorganic growth opportunities

AI & Cybersecurity integration into products

Acquisition framework institutionalization

Investor relations

This signals seriousness about scaling through M&A.

💼 BALANCE SHEET & CAPITAL ALLOCATION

Net Worth: ₹730cr

Net Debt: ₹67cr (very manageable)

Capex cycle continues through FY26-28 for facilities.

ESOP costs: ₹5cr (9M), increasing in FY27 for senior leadership retention.

"Disciplined framework for acquisitions focused on capabilities, customer relationships, and financial value creation"

🚩 RISKS TO WATCH

1️⃣ Facility execution delays

₹200cr of FY26 orders pushed to FY27 due to facility dependencies

2️⃣ ESAI ramp-up timeline

Pilot phase ongoing

Meaningful revenue only from FY28

3️⃣ Defence program uncertainties

MOD bids are competitive

Timing of order closures unpredictable

4️⃣ Non-core drag continues

Until divestment closes, margins will be suppressed

5️⃣ Increased competition

As defence manufacturing gets policy push, more players entering

🎯 INVESTMENT THESIS

Positives:

✅ Structural shift to high-margin products/solutions

✅ Defence tailwinds (indigenization, OEM offsets)

✅ Unique hyperscaler ESAI opportunity with recurring revenue

✅ Best-in-class facilities (DAL, DAC, MAC) as moats

✅ Strong order book ₹14,000cr pipeline

✅ Management executing on guidance consistently

✅ Platform products with multi-program applicability

✅ Non-core exit will unlock hidden value

✅ Clean balance sheet for growth investments

What to Watch Out For:

❌ Execution risk on facility ramp-ups

❌ 22% revenue from loss-making non-core (till divestment)

❌ Long gestation for ESAI hyperscaler opportunity

❌ Defence program timing uncertainties

❌ High dependence on few large customers

❌ Capex cycle pressure on near-term cash flows

🔮 MY TAKEAWAY

This is a company in the middle of a fundamental transformation. The shift from 61% services to 80% products/solutions is not cosmetic - it's a complete business model overhaul.

Three things stand out:

1) Management Credibility: They're beating their own guidance. 9M PAT already exceeded FY25 full year. When they commit to 40-50% EPS growth for FY26-27, track record suggests taking it seriously.

2) Timing: Defence indigenization China 1 hyperscaler India shift = multiple tailwinds converging. The DAL/DAC/MAC infrastructure positions them uniquely.

3) Hidden Optionality: The Radio Frequency (RF) seeker, if it becomes "first to qualify," opens up the entire BrahMos/Kusha ecosystem. The hyperscaler recurring revenue model (test kits changed annually) is a SaaS-like business in hardware.

🎬 FINAL WORD

Axiscades isn't your typical defence stock. It's a product-play being born from a services company, riding multiple secular themes - defence indigenization, hyperscaler hardware, and electronics manufacturing.

The next 18-24 months will be defining. If the facility ramp-ups deliver and the non-core exit happens, this could be a very different company by FY28.

For now, management is doing what matters most: Underpromising and overdelivering. That's rare.

Worth watching closely. 👀

Disclaimer: Not Buy / Sell Recommendation

1

5

2,691

Feb 14

Axiscades

Snippets from confcall Q3FY26

40-50% growth Every year

Vision Power930 is committed

3

15

121

8,295

Feb 14

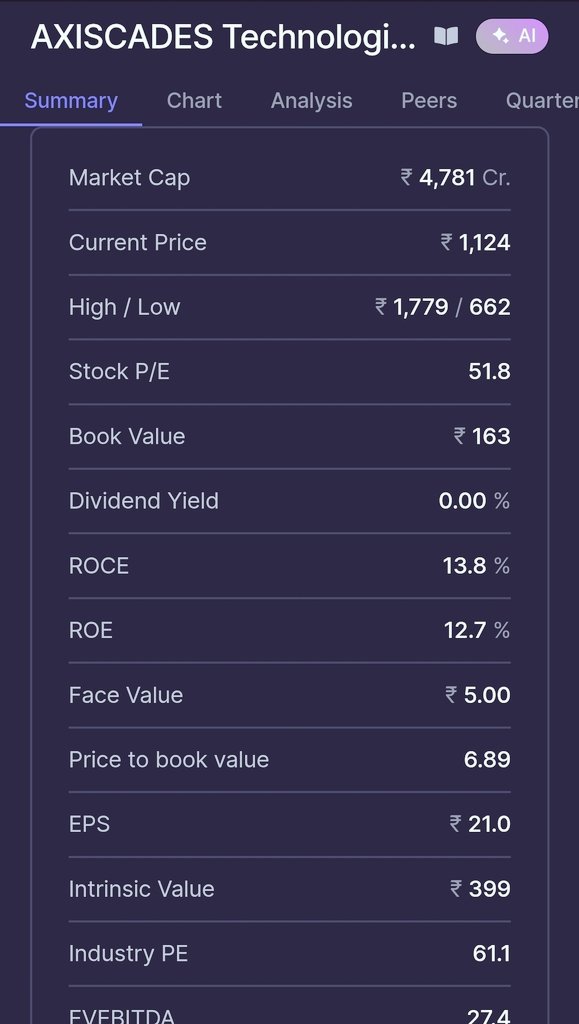

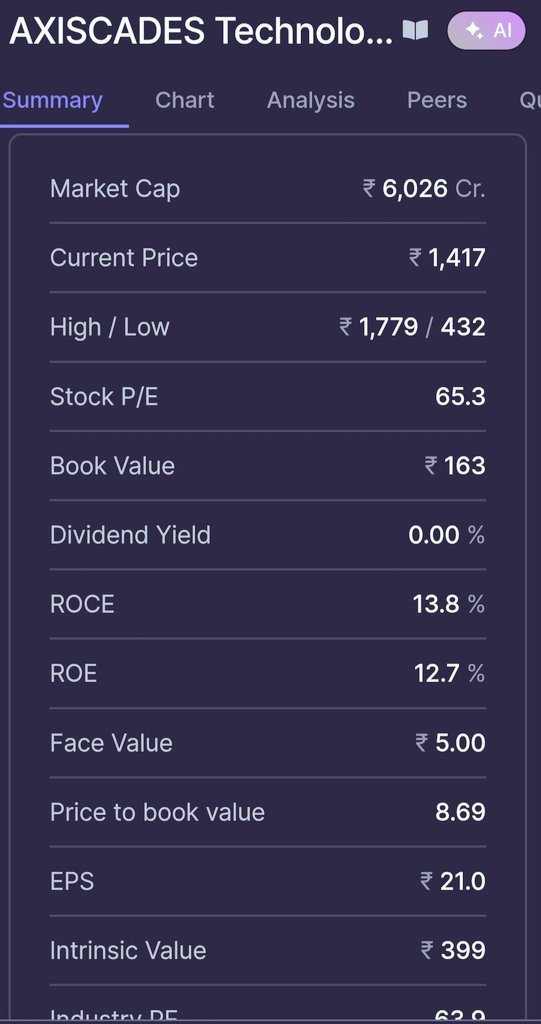

Axiscades Q3 FY26: Revenue Up 25% YoY, Margins Expand 🚀 | MCap 4,771.73 Cr

- Q3 FY26 revenue: ₹343 crores, up 25% YoY and 14.8% sequentially

- 9-month FY26 revenue: ₹886 crores, up 16.2% YoY

- Q3 EBITDA: ₹63 crores with 18.3% margin, a 360 bps YoY improvement

- Adjusted PAT for Q3: ₹35 crores (10.3% margin)

- Growth domains (aerospace, defense, ESAI) made up 78% of revenue, growing 36% YoY

- Growth domains achieved 21.4% EBITDA margin

- Product vs. service revenue ratio improved to 39:61 from 33:67 YoY

- Targeting product vs. service revenue flip to 80:20 by FY27

- Power930 vision aims for ₹9,000 crores revenue by 2030

- Targeting 40-50% annual EPS growth

- Order pipeline estimated at ₹14,000 crores over 4 years

- Current forecast visibility: ₹3,300-3,400 crores

- New facilities (DAL, DAC, MAC) to boost manufacturing in radar integration, missile electronics, and aerospace

- RF seeker for missiles successfully trialed, qualification expected by Q2 FY27

- Mission computer for LCA Mark 1 highlighted

- Divestment of noncore business on track for completion by March 2026

- Net debt: ₹67 crores; net worth: ₹730 crores as of December 31, 2025

Find Source & similar updates -> investorfeed.in/posts/85799

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 21 pages)

3

317

Axiscades Technologies Ltd Q3 FY26:-

#Q3Results #Q3FY26 #Stockmarket #Nifty #axiscades

➤ Q3FY26

✓ Revenue ₹343 Cr ( 25.0% YoY & 14.8% QoQ)

✓ EBITDA ₹63 Cr ( 55.3% YoY & 33.3% QoQ)

✓ EBITDA Margin 18.3% (vs 14.7% YoY & 15.7% QoQ)

✓ PAT ₹28 Cr ( 87.2% YoY & 19.6% QoQ)

➤ 9M FY26

✓ Revenue ₹886 Cr ( 16.2% YoY)

✓ EBITDA ₹144 Cr ( 37.1% YoY)

✓ EBITDA Margin 16.2% (↑ 240 bps YoY)

✓ PAT ₹72 Cr ( 63.6% YoY)

➤ 9M FY26 PAT (ex-labour code impact): ~₹79 Cr, surpassing full-year FY25 PAT

➤ Revenue growth driven by core domains ( 36%), despite a 9.5% YoY decline in non-core segments

✓ Defence revenue 50% YoY

✓ Aerospace revenue 28% YoY

✓ ESAI (Electronics, Semiconductor & AI) 18% YoY

✓ Heavy engineering, automotive & energy declined ~8.5% YoY due to seasonal softness and billing days

➤ Highest-ever quarterly EBITDA margin at 18.3%

➤ Margin expansion driven by:

✓ Higher share of defence & aerospace

✓ Improved execution

✓ Operating discipline

➤ EBITDA for 9M FY26 already exceeded full-year FY25 EBITDA

➤ Strong order intake momentum in core segments

➤ Outlook supported by:

✓ Increased procurement by Indian defence agencies

✓ Growing engagement with global aerospace & defence OEMs

➤ Strategic Transformation (Power930 Vision)

✓ Target ₹9,000 Cr revenue by 2030

✓ Transition underway from services-led to products, solutions & manufacturing-anchored model

✓ Ambition to derive >80% revenues from manufacturing-driven products & solutions by FY28

✓ Expected to structurally lift margins and ROCE

➤ Manufacturing & Infrastructure Expansion

✓ Devanahalli Aero Land (DAL) – 165,000 sq. ft. fully operational

- Partnerships with global aerospace leaders

- Centres of Excellence for MBDA and Indra

✓ Devanahalli Atmanirbhar Complex (DAC):

- Radar hangars expected by Q3 FY27

✓ Hyderabad Aerospace Park:

- Acquired 8 acres for missile component manufacturing & integration

- Collaboration with a leading global missile OEM

➤ Management Guidance & Outlook

✓ EPS growth guidance: 40–50% YoY for FY26 and FY27

✓ Strong confidence in:

- Defence-led structural upcycle

- Manufacturing transition

- Long-term value creation

Axiscades Technologies Ltd Q3 FY26 Results:-

#Q3Results #Q3FY26 #Stockmarket #Nifty #axiscades

Revenue 343.18 Cr vs 274.53 Cr

( 25.01% YoY┃ 14.75% QoQ)

PBT Ex-Exceptional Items 46.67 Cr vs 24.66 Cr

( 89.26% YoY┃ 28.69% QoQ)

PAT 27.72 Cr vs 14.81 Cr

( 87.20% YoY┃ 20.44% QoQ)

Other Income 1.94 Cr vs 2.37 Cr YoY & 5.94 Cr QoQ

This Q3 Exceptional loss of 7.82 Cr

In Q3FY25 Exceptional loss of 1.52 Cr

1

10

1,807

#Axiscades - posted solid set in Q3

Mgmt guides to deliver a robust increase of 40-50% year-on-year in Earnings Per Share (EPS) for both FY26 & FY27

Power930 vision to reach INR 9,000 crore by 2030

165,000 sq.ft Devanahalli Aero Land (DAL) facility is now fully operational

#Axiscades - this can be studied in this correction, from here execution matters!!

1

5

47

3,989

Axiscades Technologies Strong Q3FY26; Guidance Intact

Revenue rose25% YoY and 14% QoQ

EBITDA rose 55.3% YoY and 33.3% QoQ

PAT grew 87.2% YoY and 19.6% QoQ

Defence, Aerospace and ESAI (core domains) continued to outperform, with Defence revenues up 50% YoY, Aerospace up 28% YoY, and ESAI up 18% YoY.

Core revenues for 9M FY26 grew 26% YoY, underscoring sustained demand momentum.

Order intake in core businesses strengthened materially, accompanied by an expanding customer base.

Management expects this momentum to sustain, driven by higher defence procurement and increasing engagement with global OEMs.

Strategic transition towards product-led growth progressed further, with commissioning of the Aeroland facility and commencement of construction at the DAC land, positioning the Company for scalable, non-linear growth.

Guidance & Strategic Outlook

Management reiterated confidence in delivering 40–50% YoY EPS growth for FY26 and FY27, supported by strong core segment traction and margin expansion.

Under the Power930 vision, the Company remains on track to scale revenues toward ₹9,000 crore by 2030, with a targeted shift to 80% revenues from manufacturing-driven products and solutions by FY28.

1

5

698

Axiscades Q3 FY26: Revenue Up 25% YoY, Margins Expand 🚀 | MCap 4,771.73 Cr

• Q3 FY26 revenue: ₹343 crores (25% YoY growth, 14.8% QoQ growth)

• 9M FY26 revenue: ₹886 crores (16.2% YoY growth)

• Defence revenue: ₹311 crores (39% YoY growth)

• Aerospace revenue: ₹282 crores (17% YoY growth)

• ESAI revenue: ₹98 crores (13% YoY growth)

• Q3 FY26 EBITDA margin: 18.3% (360 bps YoY improvement)

• Q3 FY26 EBITDA: ₹63 crores (55.3% YoY growth)

• 9M FY26 EBITDA: ₹144 crores (37.1% YoY growth)

• Devanahalli Aero Land facility fully operational with global partnerships

• Power930 vision targets >80% manufacturing-driven revenue by FY28

• International order pipeline exceeds USD 300 million for near-term deals

Find Source & similar updates -> investorfeed.in/posts/80339

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 18 pages)

4

446

Feb 6

🚨 AXISCADES: THIS IS NOT A SAFE STORY. [REVISION MODE]

THIS IS A TRANSFORMATION BET. 🧵

x.com/i/status/1998617632627…

[[ALREADY PART OF 100%CLUB]]

UPCOMING QUARTERLY RESULT ON 9 FEB 2026

Most people are reading AXISCADES like an IT stock.

That’s the first mistake.

🎬 ACT 1: WHAT AXISCADES IS EXITING

AXISCADES is slowly walking away from:

❌ Low-margin IT services

❌ Linear engineering manpower

❌ Revenue without pricing power

Management has openly said:

“We will divest non-core businesses.”

That’s rare. That’s uncomfortable. That’s capital discipline.

🎬 ACT 2: WHAT IT IS BETTING THE COMPANY ON

AXISCADES is rebuilding itself around:

• Defense electronics

• Missile seekers

• Radars & counter-drone systems

• Aerospace systems integration

This is not services.

This is systems engineering.

Higher complexity = higher entry barriers.

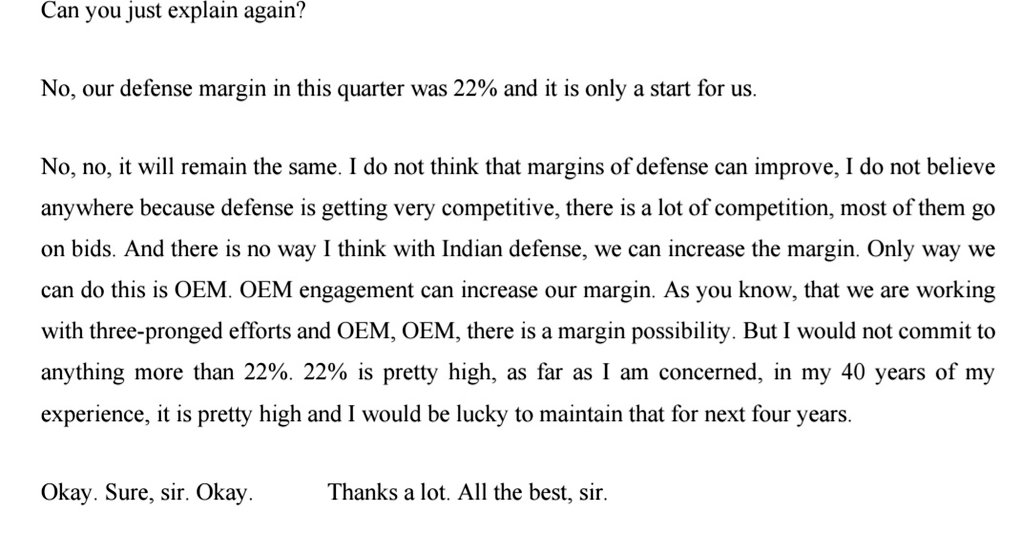

🎬 ACT 3: THE NUMBER MOST PEOPLE MISSED

Defense EBITDA margin: 👉 ~22%

And management clearly said:

“Margins won’t go beyond this.”

No fantasy.

No 30% PowerPoint margins.

Just execution.

🎬 ACT 4: THE ₹9,000 CRORE DREAM (POWER930)

Management vision:

• ₹9,000 Cr revenue by 2030

• Requires ₹1,200-1,500 Cr capex

• Multiple new facilities

• Strategic partners divestments

This is a company-defining gamble.

If executed → rerating monster

If delayed → balance-sheet stress

No middle ground.

🎬 ACT 5: THE RISK MOST FINFLUENCERS WON’T SAY

Defense orders are:

• Event-driven

• Trial-based

• Politically timed

Missile seekers, #QRSAM, #LLTR - all need successful trials first.

Delays are normal. Markets hate waiting.

🎬 ACT 6: WHY THIS IS NOT FOR EVERYONE

#AXISCADES requires:

• Tracking capex

• Tracking cash flows

• Tracking order wins vs promises

This is NOT a “buy and forget” stock.

This is a monitor-every-quarter stock.

🎯 FINAL SCENE: THE REAL VERDICT

AXISCADES is not broken.

But it’s not easy either.

It’s a high-risk, high-conviction transformation play.

Markets will reward:

✔ Execution

✔ Capital discipline

✔ Order conversion

Markets will punish:

❌ Delays

❌ Overpromising

❌ Cash stress

📌 SAVE THIS LINE:

AXISCADES is betting on complexity.

Complexity creates moats but only for disciplined operators.

🔁 Repost if this added clarity

💾 Save before next concall

DISCLAIMER = THIS IS NOT A BUY OR SELL RECOMMENDATIONS. SHARING HERE ONLY FOR STUDY PURPOSES.

ALREADY SHARED THIS IN NOV 2025 IN CLOSED GROUP. JUST SHARING HERE FOR REVISION PURPOSES.

JUST MAKING CHRONOLOGY HERE 🙂

#AXISCADES

10 Dec 2025

#IMPORTANT NEWS ON

AXISCADES is entering the “serious radar zone.”

[ALREADY SHARED ON X when no one is talking about this company] PINNED

From 478 to cmp 1335 🔥🔥

x.com/SharePurana/status/196…

A clean proxy to defence, aerospace, drones, and even semiconductors the highest-conviction themes of this decade.

The company is mid-turnaround:

• Moving from services → products (hello margin expansion)

• Management guiding 40% growth in core verticals

• Aggressive hiring to support scale

The real trigger?

Their 165,000 sq.ft Aeroland facility is almost ready and construction has begun on the 3 million sq.ft Devanahalli Atmanirbhar complex -

a future powerhouse for radars, strategic electronics & aerospace supply chain.

Near term: Q3 & Q4 may look “normal” because defence seasonally peaks later & aerospace is soft.

But if management executes what they’re signalling margins growth can rerate sharply.

This story is getting interesting.

Watching closely.

Full breakdown soon on the 100% Club.

#AXISCADES #TrendingNow

5

767

10 Dec 2025

6⃣AXISCADES Technologies Ltd

Q1. Is a 65–70% CAGR (Power930) achievable?

🔹Management believes yes, because defence (EW, missile systems, radars), semiconductor engineering, and aerospace each have high visibility. Large manufacturing complexes coming online by FY28 provide scale.

1

4

550

29 Nov 2025

AXISCADES - Defence & Aerospace

Shared my study at 478 As you see in my pinned X account.

From 478 to cmp 1425 🔥🔥

x.com/SharePurana/status/196…

Now sharing my followup about co.

This is not an IT-services company anymore.

This is a missile-radar-counter-drone powerhouse in the making.

Let’s decode the whole story. 👇🚀🇮🇳

Q2 & H1 RESULTS = BLOWOUT 🔥

Q2 FY26

📈 Revenue: ₹299 Cr ( 13% YoY)

💣 EBITDA: ₹47 Cr ( 41% YoY)

📊 Margin: 15.7% (lifetime high)

💥 PAT: ₹23 Cr ( 89% YoY)

H1 FY26

Revenue ₹543 Cr ( 11%)

EBITDA margin: 14.9%

Core domain EBITDA: ~19%

EPS: ₹10.21 ( 53%)

Margins are EXPLODING.

Execution is tight.

Growth is real.

The Whole Business Is Undergoing a Transformation 🔄

Company split into:

1. Core (75% revenue)

✈ #Aerospace

🛡 #Defence

🤖 ESAI (Electronics Semiconductors #AI)

2. Non-Core (25% revenue)

Legacy heavy engineering & US verticals

➡️ COMPLETE divestment/restructuring by March 2026.

Cleaner. Sharper. High-margin focused.

DEFENCE = The Engine of the Next 5 Years 🚀🇮🇳

The company has publicly laid out the 3 pillars ⬇️

🔹 PILLAR 1: Missiles

Working on motors, seekers, computers, launchers, assembly

#BrahMos, #Kusha, #QRSAM

Indigenous ESA radar seeker in final trial stage

Seeker = 30% cost of each missile 🚀

BrahMos production going from 100 → 150 missiles/yr

👉 Defence revenue me missile segment ka target: 40%

🔹 PILLAR 2: Radars & Antennas 📡

Large radars, aircraft radars, ground radars

Diving deep with new Atmanirbhar Complex

Multiple antennas already qualified

A TACAN order expected within weeks

👉 Target: 30-35% defence revenue

🔹 PILLAR 3: Counter-Drone (Hard Soft Kill) 🚁🛑

This is MAD:

Laser-based hard-kill system with #Cilas (France)

Tested in Ukraine & #NATO region

Claimed to be “best in the world for weight-range-power”

India trials underway

Emergency orders already received for man-portable systems

👉 Goal: Top 3 global player in counter-drone solutions.

THIS alone can re-rate the stock 3x over years.

AEROSPACE = Cash Cow Upgrade Story ✈

Q2 growth: 16%

H1 growth: 12%

Target margin: 18.5%

New machine shop aero supply-chain from 2026 onwards

Aerospace keeps the base strong while defence explodes.

ESAI – Electronics, Semiconductors, AI 🤖

Right now: moderate growth.

Future: HYPER GROWTH.

Working with 2 global hyperscalers

One hyperscaler 3x revenue jump next year

EMS box-build capability ready

Flex board acoustic lab internationally benchmarked

FY27 = breakout year for ESAI.

CAPEX STORY = Company Is Becoming a GIANT 🏭

Phase 1 -Ready/Operational

📍 Aeroland (EMS Semi systems)

Phase 2 - Defence Mega-Complex (DAC)

📍 3 million sq ft superfacility

Radars

Antennas

Counter-drone

Test systems

Missile electronics

Phase-I: Sept 2026

Phase-II: Dec 2026

Hyderabad Missile Complex

📍 Complete missile subsystem plant

Target completion: March 2027

Total capex: ₹1,500 crore over 3 years

This is a BHEEM-level infra buildout.

HOW WILL THEY FUND SUCH BIG CAPEX? 💰

Surprisingly smart plan:

No dilution in parent

Strategic equity from foreign OEMs at SPV level

Divestment of non-core verticals

Internal accruals

Small bridge debt (₹40-50 crore)

Balance sheet right now:

Net debt: ₹50 crore only

Gross debt: ₹163 crore

Net worth: ₹700 crore

Midcap defence me itna clean BS milna rare hai.

FY26–30 GROWTH PLAN = INSANE (BUT POSSIBLE) 🚀

FY26-27

40-45% growth

Margin expansion

FY28-30

70% CAGR expected

This is #Power930:

₹9000 crore revenue target by FY30 (~$1 bn).

Bold?

Yes.

But the building blocks are REAL.

🔍 RISKS – VERY IMPORTANT ⚠

Capex is huge vs company size → execution risk

Many defence orders still in trial/ approval stage

ESAI depends on certification timelines

Big revenue targets in Q2-Q3 because Q4 will have shifting downtime

Non-core divestment timeline still fuzzy

This stock is high risk, high reward - not for weak stomachs.

⭐ DISCLAIMER =Not a buy/sell recommendation.:Just for research purposes. 🚀🇮🇳

#AXISCADES

20 Sep 2025

Back on 12 June 2024, when #Axiscades was at ₹478, many doubted.

I believed. I shared. I held.

📈 Today it’s ₹1692. A true multibagger journey 🚀🔥

👉Lesson: Markets reward conviction, patience & courage. Doubt fades, discipline pays.

#StockMarket

1

2

441

29 Nov 2025

AXISCADES Revenue Guidance & CAPEX - The company is aiming ₹9,000 Crore Revenue by 2030

Just analyzed their concall. This is too ambitious

Let me break down the numbers 👇

The "Power930" Target:

Current revenue (FY26E): ~₹1,200 cr

Target by FY30: ₹9,000 cr

That's 7.5x in just 5 years

Required CAGR: ~65%

For context:

BEL grows at 15%

Data Patterns at 25-30%

This is INSANE ambition

29 Nov 2025

Indian Defense is getting very competitive, there is a lot of competition

11

25

125

33,541