Ron Westfall, #HyperFRAMEResearch retweeted

New PrivacyOps capabilities and AI readiness research build on Veeam's DataAI vision as orgs face growing pressure to demonstrate measurable outcomes from AI investments.

Read more from @HyperFRAME_Res @RonWestfallDX. bit.ly/4vbHmrs

#VeeamON

1

1

218

Jun 12

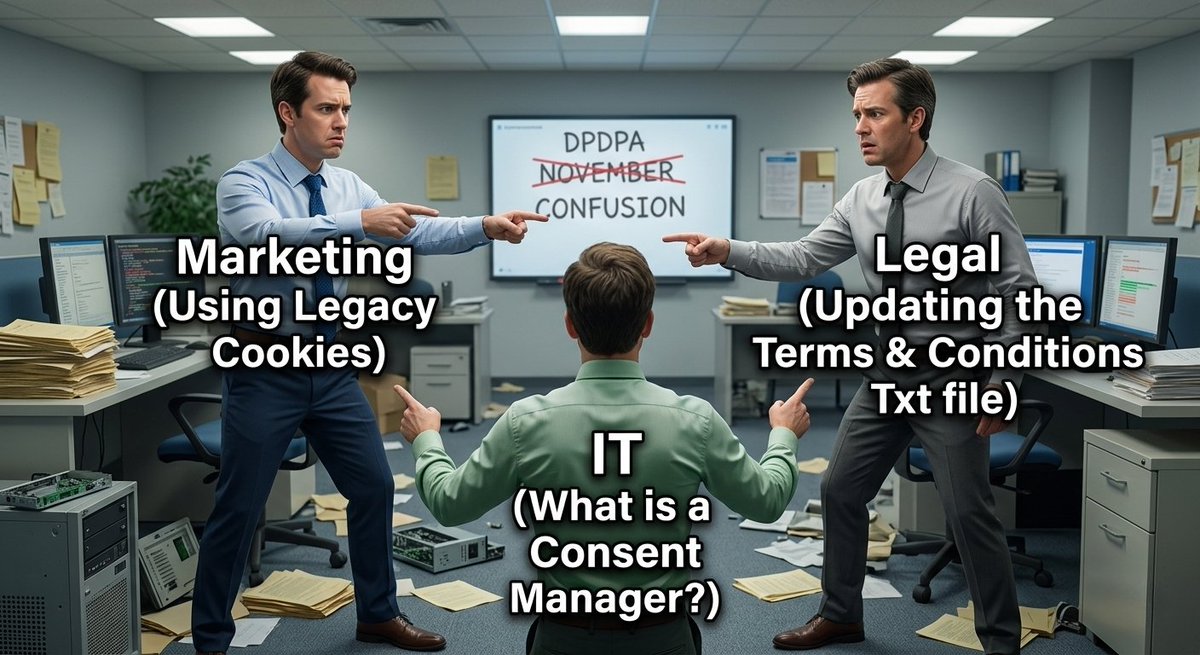

POV: Your company receives a privacy audit request.

Marketing: "Legal approved it."

Legal: "IT implemented it."

IT: "Marketing collected it."

Everyone: 😳😳😳

Auditor:

"Great. Now show me the consent records, data lineage, and retention evidence."

Whether it's GDPR, CCPA, DPDPA, or PDPA, accountability cannot be outsourced.

#DataPrivacy #GDPR #CCPA #DPDPA #Compliance #DataGovernance #PrivacyOps

5

Jun 10

Veeam added three agentic AI agents to its DataAI Command Platform for privacy and AI governance. The Data Subject Request Agent cuts DSR form launch time by ~50%. Consent Agent ships now; the other two in Q3. storagereview.com/news/veeam… #PrivacyOps #AIgovernance #Veeam @Veeam

1

2

445

Veeam® Software retweeted

. @Veeam Extends DataAI Strategy as AI Accountability Reaches the Boardroom: New PrivacyOps capabilities & AI readiness research build on Veeam's DataAI vision as firms face pressure to show AI investments boost business outcomes shorturl.at/Ud5Ng @Veeam_EMEA @Veeam_UKI

1

1

322

May 28

#SME #TECHD #TechDCybersecurity

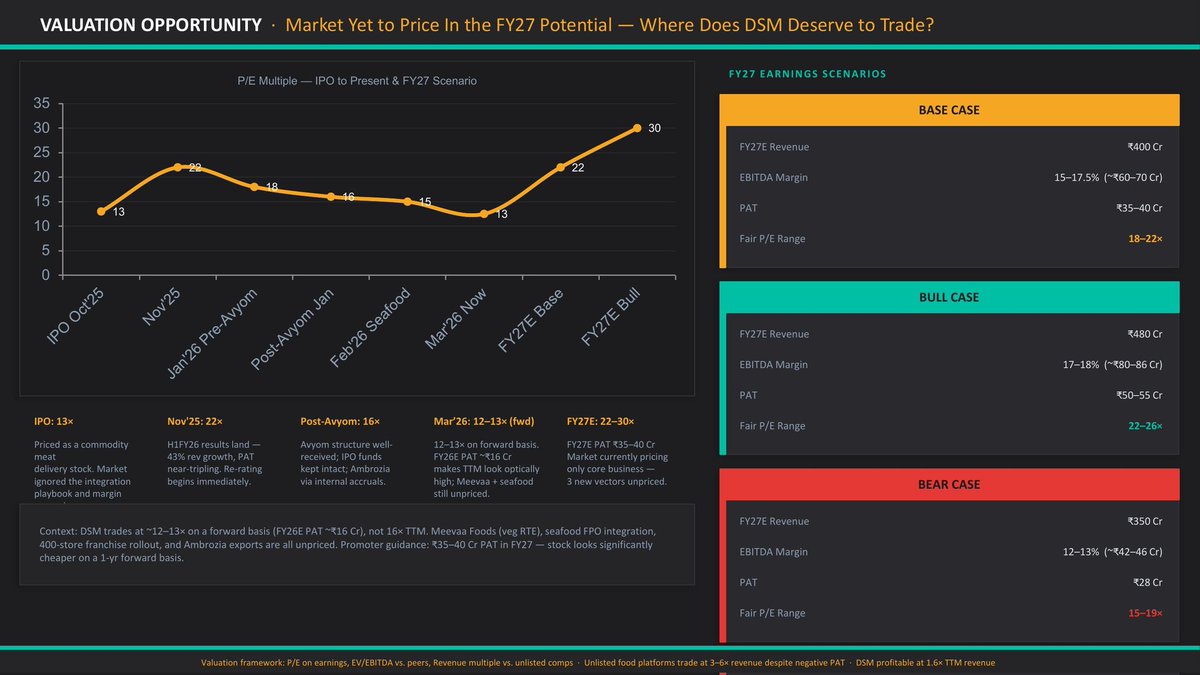

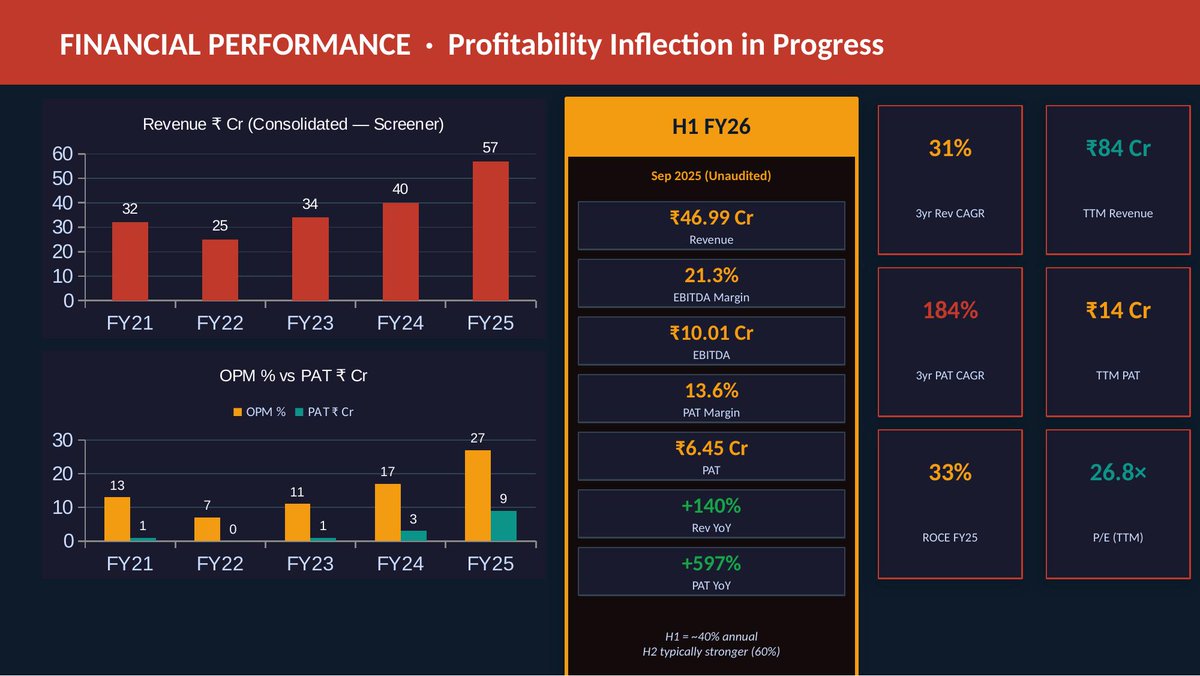

TechD Cybersecurity H2 FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️ Momentum continuing into FY27 with organic revenue guidance of ₹75-80 Cr.

💠With planned inorganic acquisitions, management targets ₹100 Cr total revenue.

💠 Business transitioning from services/training-led to AI-native cybersecurity platform company via TECHD ONE platform (Phase 1 – 4 modules already launched; Phase 2 modules expected in H2 FY27).

💠 Product revenue contribution expected at 15-20% in FY27, rising further in subsequent years toward a more balanced 50:50 product-services mix over 2-3 years.

💠High-margin SaaS/ARR model with cross-sell/upsell potential to existing 700 customers.

▫️ EBITDA & PAT margins to remain healthy;

💠Agentic AI has already reduced employee benefit expenses (from ₹12 Cr to ₹9.36 Cr) and improved H2 FY26 EBITDA margin.

💠 Further margin expansion expected from reduced OEM dependency, automation, and product mix shift.

💠 H2 remains seasonally heavy; management is actively normalizing quarterly performance through multi-year contracts and better renewal timing.

💠Quarterly results likely to be released starting next year for improved visibility.

▫️ Long-term vision: Build one of India’s largest Global Security Operations Centers (GSOC) under Techdefence Cyber Valley (60,000 sq ft) and become a globally competitive AI-driven cybersecurity powerhouse from India.

👉 Current Order Book / Projects and Future Pipeline

▫️ Current: ₹43 Cr as on 31 March 2026 (multi-year contracts, regulatory renewals, and visible revenue).

💠 Management expects 60-70% execution in H1 FY27 from this book, with the balance in H2.

💠Visibility from 5-year contracts being signed with several customers.

▫️ Pipeline:

💠 Government pipeline: ₹150 Cr (empanelments with NIC, BSNL, CRISP Bhopal, NFSU-RIC, state PSUs, and dedicated CyberAGI vehicle).

💠 Private/Enterprise pipeline: ₹50 Cr .

▫️ Key Projects & Initiatives Underway:

💠 TECHD ONE AI Platform – Digital Risk Protection, Human Trust AI (Human Risk Management), OTShield, Zero-day & software supply chain security), plus upcoming SecOps, PrivacyOps AI, Identity Guard, etc.

💠Roadshows and channel partner program starting June 2026.

💠 Techdefence Cyber Valley (GSOC): 60,000 sq ft facility in Ahmedabad – PEB erection completed; civil & interiors targeted by Aug-Sep 2026. Will house IT/OT/Vehicle SOC, AI labs, experience center, and incubation.

▫️ Global Expansion: Wholly-owned subsidiaries in Canada (North America hub), GIFT City IFSC, and Dubai (Middle East).

💠Expect ₹10-15 Cr contribution from subsidiaries in FY27.

💠 Inorganic Opportunities: Final stages of discussions with (1) Australian MSSP (~3M AUD revenue, high-margin, ANZ focus) – expected to add ~₹30 Cr annualized if closed; (2) larger Indian SI company diversifying into MSSP (200 Cr topline, currently low EBITDA).

👉 Other Notable Points

▫️ Financial Performance (FY26):

💠 Renewal rate & NPS: 98% | 700 clients served | 150 new clients in H2 | 365 clients added in FY26.

💠 1,20,000 EPS (Events Per Second) processed in SOC; targeting 1 million EPS.

▫️ Operational Highlights & Differentiation:

💠 Agentic AI deployment across operations, sales, reporting, and repetitive tasks → significant cost optimization and faster delivery (days → hours).

💠 High client stickiness with multi-year & 5-year contracts; focus on recurring revenue (MSSP/SOC).

💠 Major logos: Adani, JM Financial, Havmor, Zee Learn, Astral, Star Health, MCX, Torrent Group, etc.

💠 Recent wins: BSNL National Skill Development Partner, SPU Gujarat 3-year partnership, NFSU-RIC empanelment, CRISP Bhopal MoU.

💠 IPO proceeds utilization on track; significant unutilized portion earmarked for product development, GTM, and GSOC.

▫️ Q&A Key Insights:

💠 Recurring revenue — ₹43 Cr order book is largely recurring; top-10 customers contribute ~43-45% of revenue, with active cross-sell/upsell pushing revenue-per-customer higher.

💠 Product gross margins targeted at ~85% ; net margins 40-50% expected after channel/distributor costs and infra.

💠 DPDP compliance slow due to lack of enforcement/penalties so far; expected acceleration once penalties begin.

💠 Government business to accelerate via dedicated vehicles and new empanelments; private sector driven by regulatory mandates and AI threats.

💠 Cost optimization via AI & internal talent pipeline "

💠Intern-to-employee model, National Internship Yojana remains a key moat vs global peers.

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

1

2

19

4,059

May 13

Our directory of AI mentors is growing!!!

Happy to share that Salma Khan has joined us a mentor.

Salma is an AI and PrivacyOps strategist focused on the intersection of artificial intelligence, data governance, and operational privacy transformation.

1

1

2

177

22 Oct 2025

מי ראה את זה בא?

🎉 Veeam 🤝 Securiti AI · $1.7B 🎉

קמו ב2019, גייסו עד היום $156M, התחילו כפתרון PrivacyOps, הוסיפו DSPM, הוסיפו עוד יכולות Data Security, הוסיפו AI Security, ועכשיו נמכרים לVeeam (שבעצמם נמצאים בואליואציה של $15B לפי הסקנדרי האחרון).

תוהה (לא באמת) מה ה M&A הזה יחמם יותר - את שוק הDSP או את הAI Security...

קיצר, עוד זוכה בתחרות של RSA (2020) מסיים עם מה שנראה כאקזיט מרשים ביותר - הסיבוב האחרון היה $75M לפני 3 שנים 😮

1

43

3,327

📢 2 days. Endless insights.

Join us Sept 18–19 in Boston for IAPP AI Governance Global 2025 & explore the future of intelligent #PrivacyOps with TrustArc.

🔗 trustarc.com/aigg25

#AI #Compliance #IAPP #TrustArc

3

49

17 Jul 2025

@tenprotocol, stealth is the default — encrypted ops, zero leaks, zero trust required.

Cross-chain extraction?

Let’s just say... the spy game just went on-chain. 🛰️🔒 #TENProtocol #PrivacyOps

1

2

30

12 Jun 2025

If you can't say what data you collect and why, you're not compliant.

A RoPA is an audit shield. Track processing activities and keep it current as your tools evolve.

Need help structuring one? Drop a question.

@ovedjerory

#Day22 #100DaysOfDSL

#GDPR #PrivacyOps #Accountability

1

6

130

23 Aug 2024

I'm keeping my learning streak going by completing Module 3 of Securiti's PrivacyOps Certification Course. This module discussed Sensitive Data Intelligence highlighting the meaning and importance of SDI to organizations. I also learnt the

education.securiti.ai/badge/…

1

2

78

22 Aug 2024

Glad to have earned the Privacy Law Compliance and Privacy Ops badge by completing Module 2 of Securiti's PrivacyOps Certification Course.

education.securiti.ai/badge/…

1

3

55

21 Aug 2024

To further my interest and knowledge in Cybersecurity and Data Privacy Management, I enrolled in Securiti's PrivacyOps Certification course.

I'm glad to have earned this badge from completing Module 1 of the course which extensively covered the meaning

education.securiti.ai/badge/…

1

1

3

152

18 Aug 2024

7 𝐅𝐑𝐄𝐄 𝐂𝐞𝐫𝐭𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐢𝐧 𝐃𝐚𝐭𝐚 𝐏𝐫𝐢𝐯𝐚𝐜𝐲 : 𝐁𝐫𝐞𝐚𝐤𝐢𝐧𝐠 𝐈𝐧𝐭𝐨 𝐃𝐚𝐭𝐚 𝐏𝐫𝐢𝐯𝐚𝐜𝐲

1-PrivacyOps - lnkd.in/dxnhBRe3 -

2-Onetrust :lnkd.in/dSzD5Wdh :

3-Infosec Train :lnkd.in/dvR2tcTx -

4-GDPR: lnkd.in/dGCmCGfB

5-Data privacy Fundamental- Notherneast University lnkd.in/dC7ECv7h

6-Data Protection and Data Security by NCFE - lnkd.in/deKUSm7c

7-Diploma in GDPR and Data Protection -lnkd.in/d5m4g4vD

12

26

1,905

30 Jul 2024

AU Privacy Act revamp? 🇦🇺 Our #IAPP (@privacypros) webinar helps you navigate changes! (Aug 14, 11AM AEST).

Learn compliance best practices, automation & team collaboration. Register Now! buff.ly/3LRVpx3

#DataPrivacy #Australia #PrivacyOps #Compliance #PrivacyAct

5

2

41

10 Nov 2023

Ongoing talk from Cepha Okoth on PrivacyOps: A Segue to Privacy Operations Center (POC). Get you privacyops shoes on.

@ExperienceUSIU @BSidesNairobi #BsidesNairobi #BsidesNairobi2023 #DataBreach

4

24

2,314

8 Nov 2023

We are thrilled to announce a strategic partnership with Securiti, a recognized leader in the realm of data privacy, protection, and compliance. This collaboration brings together Infinitive's expertise with Securiti's PrivacyOps platform.

Learn more: hubs.la/Q027B9V_0

1

2

56

30 Oct 2023

PrivacyOps: A Segue to Privacy Operations Center (POC)

by Cephas Okoth (@CiACephas)

bit.ly/bsidesnrb23

1

6

11

747

24 Oct 2023

Elevating my cybersecurity game with the PrivacyOps certification from @SecuritiAI .Thanks to Securiti for the valuable knowledge and skills. Let's secure the digital realm!. 📚🔒 #PrivacyOps #Certification #Cybersecurity #infosec #defense

1

67