30 May 2025

SME RESULT REVIEW: We covered several Stocks Yesterday (check profile). Comments on rest of the main ones, are listed here:

😡AWFULLY POOR: Aelea, Drone Destination, Innomet turned out to be awful! Sona Machinery too.

🌟🌟GOOD: Vdeal, Rudra Gas and Beezaasan (posted Yesterday) Rest Below: Ztech, CLN Energy, Qualitek Labs, Nexxus Petro,

🌟AVERAGE: (Posted Yesterday) Vinyas , Shree OSFM, Nisus (gone haywire), Sattrix, Kalyani, SAR Tele (Foreign Income 90%) , Ganesh Green (Very quiet), Winsol , K2 Infragen, Rest Below: SHRI TECHTEX, BR Goyal, Paramount Forgings (May be will work in future), Divine Energy (high Valuation) , SD Retail (not accelerated)

For Rest of the Stocks, Brief Comments Below:

ZTECH : 🌟🌟 Rs.584 was at 60pe. Now 41x. Excellent growth during the year from Rs.67Cr to 95Cr and PAT moved up from 8.5Cr to 20Cr with rising op margin.

CLN ENERGY: 🌟🌟 Rs.453 was at 50 pe. Now 37x. Annual Rev is up from 132Cr to 220Cr . But PAT up from 9.3 to 12.9Cr only . 10Cr IPO funds is spent on capex. So there could be revenue uptick this year too.

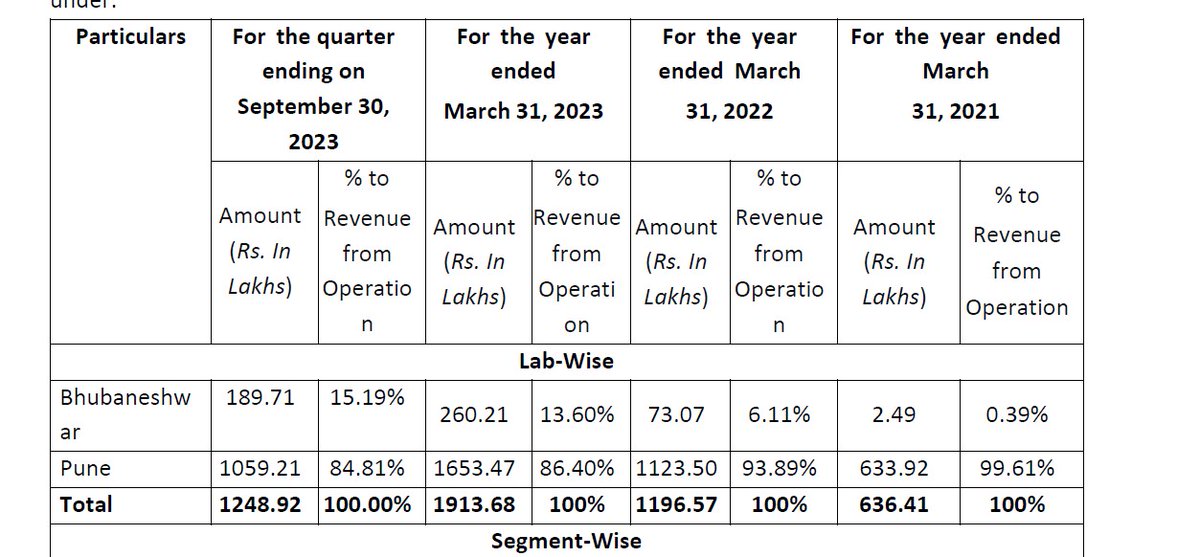

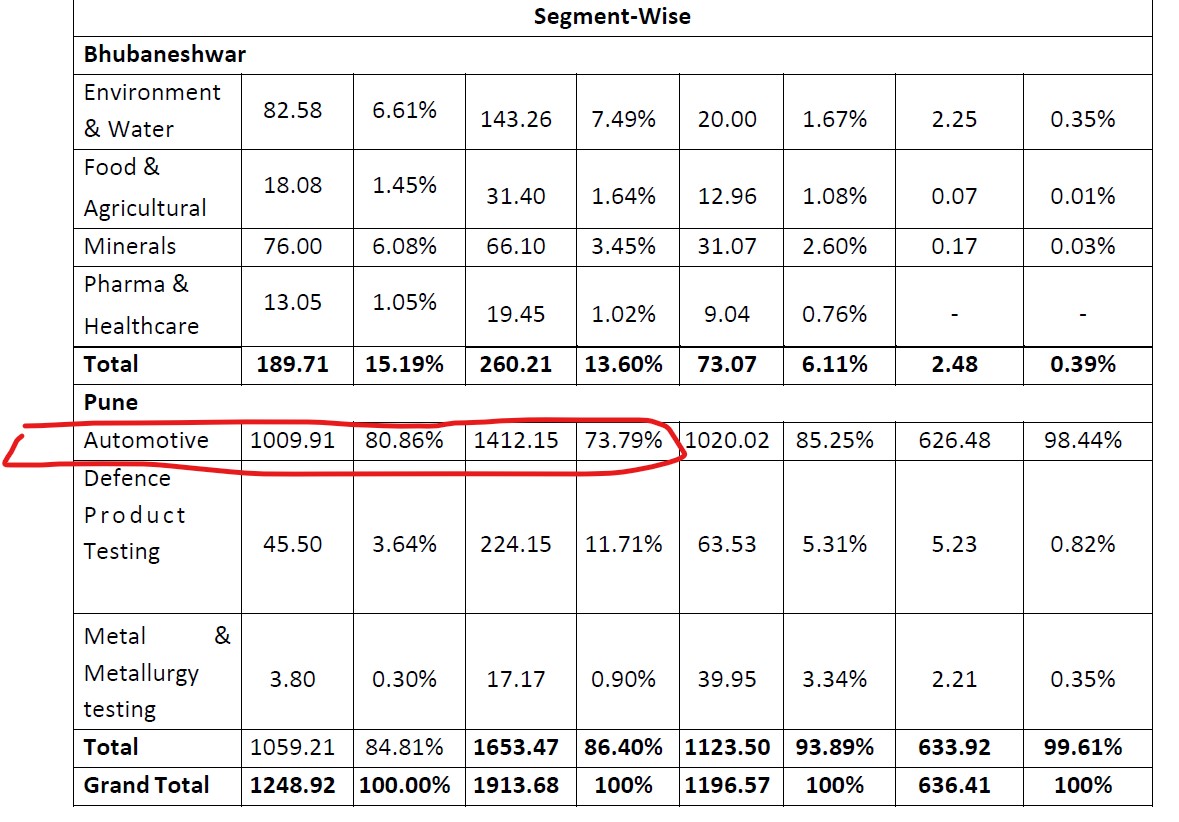

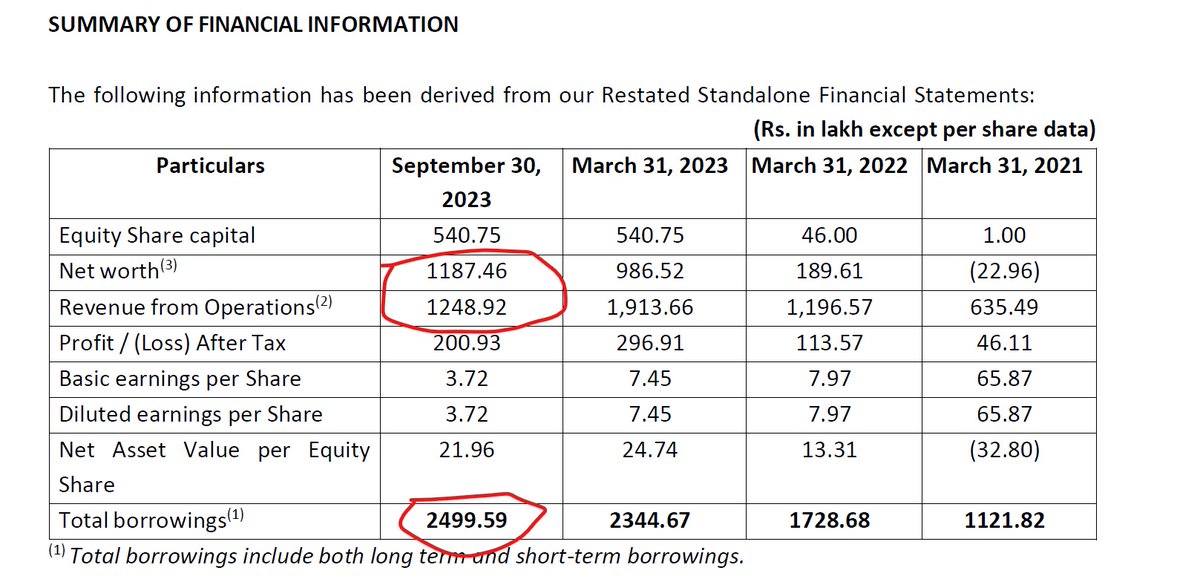

QUALITEKLAB: 🌟🌟 Rs.308 was at 77p/e. Now 40x. Big leap in rev from 30Cr in Fy24 to 70Cr in Fy25. Yearly PAT up from 4Cr to 7.7Cr. Very Good! But valuation still looks high unless there is some big expansion plan for labs

NEXXUS PETRO: 🌟🌟 Rs. 117 was at 32x. Now 13x! Pat up 3.5Cr to 6.1Cr. Annual Rev up from 238 Cr to 305Cr. Bitumen processing and trading similar to Agarwal Industrial Corp. Due to ongoing Road infra work Bitumen players are getting better valuation that others in SME.

SHRI TECHTEX: 🌟Though there is some sales growth , No improvement in TTM pat. Valuation remains at 14x at Rs.80. overall Flat. As discussed previously this company’s technical textile products are too common type and hence growth looks hard to come by

BR GOYAL INFRA: 🌟Rs.136 was at 20/pe. Now 13x . That gives some gap for price growth. Top line degrew from 596Cr in Fy24 to 515Cr in Fy25. But PAT is up from 22 to 25Cr.

SD RETAIL: 🌟 Rs.146 was at 27x. Now 32x. Only marginal topline growth and annual PAT fellshort of TTM at end of H2. Hence p/e is up. Company has almost fully used Capex funds for new stores. WC fund is still intact. So probably they will purchase stock to sell. As of now looks expensive due to the lackluster numbers.

PARAMOUNT SP FORGINGS: 🌟 Rs.50 was at 17pr. Now 22x. Annual topline marginally up from Rs.103 Cr to Rs.111Cr. PAT down from .’5 to 4.5 Cr.

The promoter stated urgency to do capex at time of IPO because they need larger machinery to grow. Now after 8 months, out of 24Cr they found need for only 4.5cr. March 24 was scheduled time line to complete works. Right now looks like stock could be under pressure. This company has good products and once expansion is complete should perform well. So track it for lowest price!

DIVINE POWER ENERGY: 🌟 Rs.152 was at 41p/e. Now 40x. Makes winding wires & strips of copper / aluminum. Exactly similar to DCG cables (16 p/e) . Annual sales is up from 223 to 346Cr. Annual PAT is up from Rs.6.4Cr in H1 to Rs.9.15Cr in H2. In H2 there is some margin reduction.

CANARYS: 🌟 Rs.31 was at 21p/e. Now 24.5x. Topline growth is good from 76Cr to 90Cr. But bottom line is flat indicating margin pressure . Overall company is yet to take off after promising so much. (Eq structure with Rs.2 FV and large 6.5Cr outstanding shars is throttling EPS. Bad eq structure for a small growing company)

SONA MACHINERY: 😡 Very poor bottomline. This was a case of too much, loose fund raise (over 50Cr) and was over-priced at Rs.123 at IPO. Agri machinery. Probably excess funds diverted. Not looking sound

14

8

67

13,526

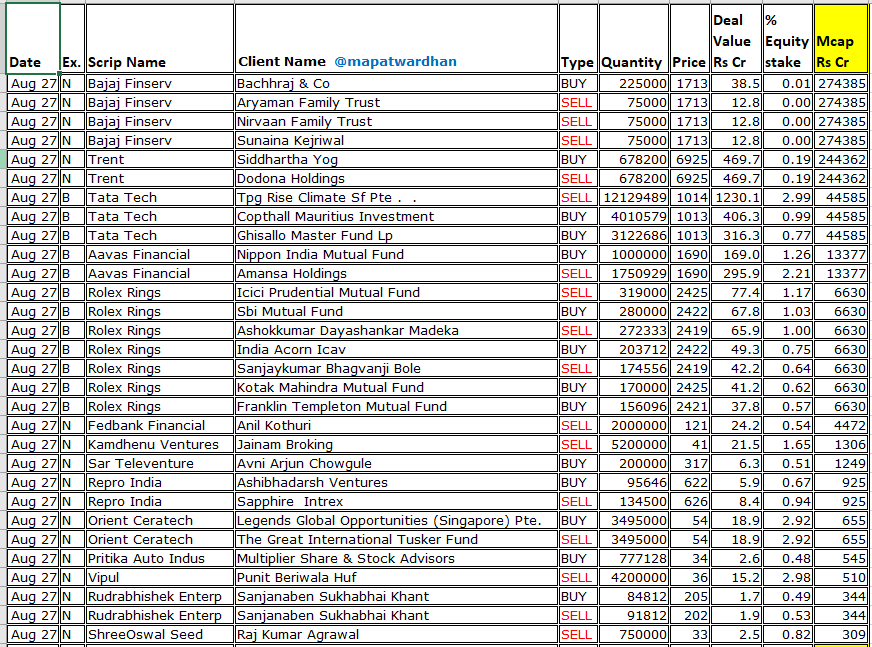

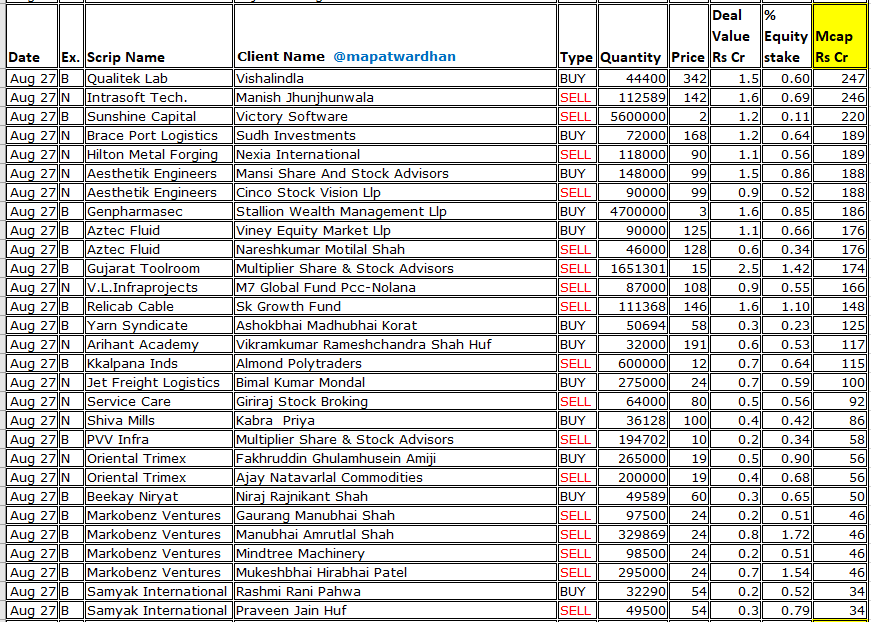

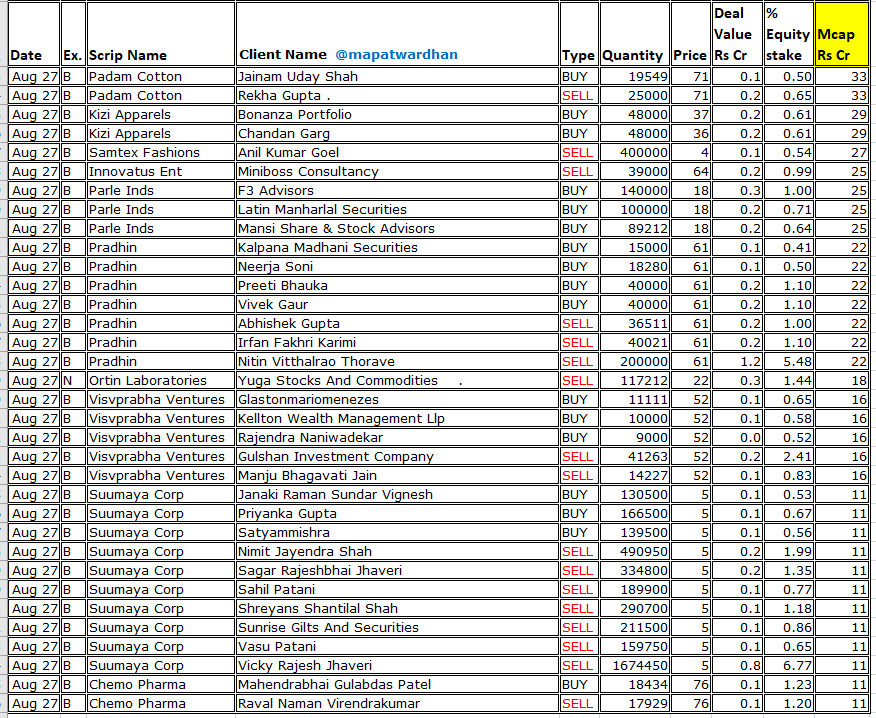

27 Aug 2024

*Todays' bulk / block deals*

#BajajFinserv #Trent #TataTech #AavasFin #RolexRings #FedbankFinancial #Kamdhenu #SarTele #ReproIndia #OrientCeratech #PritikaAuto #Vipul #Rudrabhishek #ShreeOswalSeed #QualitekLab #IntrasoftTech #SunshineCapital #BracePort #HiltonMetal #AesthetikEng

1

1

14

6,722

3 Feb 2024

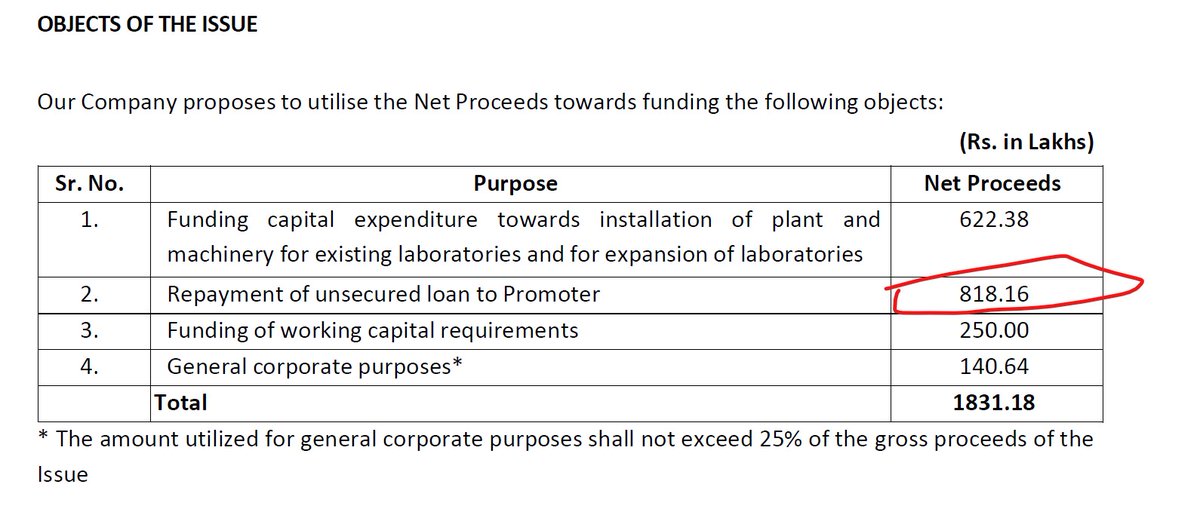

I am holding 1 lot of recently listed SME @QualitekLab, what is your view on this? Is it worth to hold for 1-2 yrs.

1

1

3

1,972

22 Jan 2024

#QLL #qualiteklab #SMEIPO

good- OPM is good. entry barrier due 2 lab setup with imported m/c , company growing with decent pace. listed competitor not growing, settin up new lab 2 cater 2 NCR & adding more M/c in Pune lab

Bad- high debt, unsecured loan repay to promoter

1/n

2

2

39

8,110

28 Nov 2023

Qualitek Lab provides comprehensive testing for Automobiles. Your trusted partner.

Call us to know more - 91-76207-37704, 91-7682857555

#QualitekLab #QualityAssurance

2

65

17 Nov 2023

Qualitek Lab exceeds not only customer expectations by delivering quality but also pocket friendly and offers tailored solutions to meet their specific needs.

#QualitekLab #QualityAssurance

2

49

3 Nov 2023

Are you looking for reputable organization for products' quality testing needs??? Look no further! Your search ends with Qualitek Lab. Contact us today to know more.

#QualitekLab #QualityAssurance #TestingLab

2

50

20 Oct 2023

Qualitek Lab ensures adequate packaging for quality assurance. Get you packaging quality tested with us. Call us to know more.

#QualitekLab #QualityAssurance #TestingLab

1

4

57

15 Sep 2023

In the lab, we engineer solutions one test at a time. Happy Engineer's Day to all my fellow testers! 🧪🔍

#EngineersDay #TestingLabLife #QualitekLab #TestingLab

2

45

8 Sep 2023

Quality is our signature.

#CustomerFirst #QuoteOfTheDay #QualitekLab #TestingLab #CareerGoals #WorkHardPlayHard #HardWorkPaysOff #WorkMatters

1

3

28