Jun 14

Esta semana que viene volvemos a los campeonatos de Racecontrol en @LeMansUltimate . Correremos el WEC Xperience en Oro con los Hyper Car y los LMGT3

@SRPracingteam @SRPsimracingpro

13

May 19

I am fairly confident I can do most of the stuff, but I would need atleast one set of hands for racedays.

I mean, I cant do racecontrol, broadcast and stewarding at the same time.

If anyone would wanna do this with me please DM me or hit me up.

1

1

3

119

yea it was actually the car #911 who did this i was there @ racecontrol

2

5

129

5,352

May 10

With Motorsport Games $MSGM scheduled to report their Q1 earnings on Wednesday, May 13th, I wanted to walk through my updated earnings model and share my expectations for the quarter.

Overall, the underlying metrics are pointing in a highly positive direction, but I am keeping my official estimates slightly conservative to account for the timing of the ELMS Pack 3 release which happened on the last day of the quarter. Here is a breakdown of how I am modeling Q1 and the catalysts I'm watching closely.

Based on recent traffic and sales data, I am projecting Q1 total revenue to land between $4.2M and $4.6M, with $4.25M being the most probable scenario.

Here is the breakdown of the underlying data driving this model:

1. Game Sales: Up 15% quarter-over-quarter (QoQ).

2. Average Player Count: Up an impressive 34% QoQ.

3. RaceControl Revenue: Projected at $900K for the quarter, though the model indicates we could see an upside surprise of up to $1.05M.

4. RaceControl Traffic: Up 14% QoQ.

5. The DLC Dynamic: ELMS Pack 3 was launched (last one of the European Series) which will see deferred revenue recognition hitting the books for the players who previously purchased the season pass. Also, the massive influx of new players entering the ecosystem during Q1 creates a compounding effect whereby the new cohort now has a larger catalog of DLCs to purchase to catch up to the Q4 players. Management has already noted that the DLC attach rate is very strong, meaning this larger player base directly translates to a higher revenue per new user.

Why These Numbers Are Conservative

You might look at the 34% jump in average players and wonder why the revenue base case is sitting at $4.25M. The main reason is that unlike previous quarters where the DLCs were released a few days before the end of the quarter, ELMS Pack 3 dropped on the final day of Q1, there is a very high probability that a significant chunk of the direct revenue from the DLC purchase itself took a few days to fully realize, meaning it will spill over into the April (Q2).

My internal assessment was for the revenue to be around $4.5M for the quarter as the engagement numbers were very strong for Q1 with the game hitting the #29 spot on the Steam Top Sellers list.

May 8

$MSGM up 50% since my thesis less than 3 months ago. My Q1 projections are overwhelmingly bullish, so much so that I'm re-running the numbers with new data points this weekend just to be safe. It’s an incredibly misunderstood stock. If earnings drop next week, the current broader market PA could set us up for a highly volatile session, hopefully to the upside.

1

2

17

5,051

This guy spun out on the side of the track & I had to completely try to avoid him, He literally reported me & @LeMansUltimate actually looked at it / responded to me yet will not respond to any protests I file, or support tickets. Revenge reports ? Sure though that's all good ! I will be putting the clip up today ASAP.

" noreply@racecontrol.gg

05:04 (41 minutes ago)

to me

📷

Dear Andrew Leckie,

Your protest has been reviewed and a decision has been made for the following protest:

Event: European Le Mans Series: Week 5

Event Date: 2026-05-07 18:00:00

Protest By: Stefan Van Aken

Outcome: Dismissed

Stewards Judgement:

Dmmissed. Neither car made the corner at different points.

The following penalties have been applied to: Andrew Leckie

- No further action taken

All judgements are final and not subject to appeal

Thank you for your understanding and cooperation in making our events fair and enjoyable for all participants.

Kind Regards,

RaceControl Team "

4

1

4

1,285

Ik vind die gasten, met Allart kalf op racecontrol, wel een vooruitgang. Olav Mol wilde alles alleen doen, dat ging te snel.

Deze afwisseling kijkt juist wel lekker…

8

965

Get 10% off for new RaceControl subscribers with code 'SPRING10' for a limited time!

With Online Championships Season 10 starting today, there's never been a better time to join the community!

🎨Custom liveries

🏁Online Championships

🔓All DLC (Pro )

👉racecontrol.gg/pro

5

58

4,384

It‘s also on LMU and LMU can‘t seem to recognize my actual racecontrol account @LeMansUltimate any help here? 🥲

1

3

298

Mar 28

おはようございます🌤️

昨夜はWECSS Vol.2 Rd6 COTAでした。

RaceControlに色々不具合があってバタバタしたものの、実況解説に相棒がいてくれたお陰で、普段より面白い配信になったかな?と。

レース自体も見てて面白かったです。

仕事しつつ集計します。

しごとー。

今夜22:00よりWEC Sprint Series Vol.2 Round6 COTA開催🏁

配信は21:50から開始します!

是非ご視聴下さい🙇

youtube.com/live/8eF8gN8he7U…

3

14

377

Mar 12

📺 NEW TECH: SRO America will continue its partnership with Vbrick, which introduces SRO RaceControl powered by Vbrick, a powerful new Live Experience Platform designed to enhance the fan viewing experience across SRO America’s live race broadcasts.

➡️ sportscar365.com/sro/world-c…

11

62

3,244

SRO America is proud to continue its partnership with Vbrick, which has now been named as the Official Enterprise Video Partner of SRO America. The collaboration introduces SRO RaceControl powered by Vbrick, a powerful new Live Experience Platform (LXP) designed to enhance the fan viewing experience across SRO America’s live race broadcasts.

Read more 🔗 gt-world-challenge-america.c…

1

2

17

1,247

Mar 12

Big news for motorsports fans. 🏁

SRO America has named Vbrick its Official Enterprise Video Partner, launching SRO RaceControl powered by Vbrick—a new live multiviewer platform that lets fans customize how they watch the race.

Multiple camera angles, onboard car views, live timing, and Twitch chat—all in one place.

It’s a more immersive way to experience GT racing during the 2026 SRO America season.

Read the press release: buff.ly/EqIw1eu

1

3

120

Mar 11

I agree with everything there. I do wonder how much of this volume is Mike Zoi selling his shares. We’ll find out later this week.

I added after the print when the stock was down to $4.50 AH. The game could completely fall off, but I had to increase my position. I wasn’t expecting RaceControl to already be at around $3M ARR for $MSGM (my estimate was $2.5M). This vertical alone should be worth the market cap, to be honest. Then we have the RaceControl platform, licensing revenue, game sales, DLC sales, console port, upcoming virtual event (which will contribute to revenue and was $0 for the last two years), and the platform with substantial NRV no one talks about.

It makes no sense, but I’m glad the market doesn’t appreciate it yet; hence the opportunity.

2

2

172

Mar 11

$MSGM delivered a brilliant quarter across all metrics imo.

The valuation disconnect is baffling. The company has roughly 5.1 million shares o/s and a market cap of around $23 million. With a $6 million cash position (as of February 2026), the enterprise value is just $17 million. EBITDA for the year was $7.3 million, putting the stock at 2.4x EV/EBITDA. They carry zero debt, maintains a clean balance sheet, and generated consistent positive operating cash flow (~$300K/month in 2025).

Deferred revenue grew sequentially from $1.11 million to $1.13 million. Since the v1.2 DLC was fully delivered in Q4, that revenue should have been recognized in Q4, implying the remaining balance is almost entirely driven by RaceControl subscriptions. Management confirmed ~26,000 subscribers generating $200,000 in monthly recurring revenue (MRR) at year-end implying an ARPU of ~$7.50/month, heavily suggesting widespread adoption of the sticky $84 annual package.

Management also noted that January and February 2026 saw the largest subscription revenue jumps yet. The company appears on track to hit a $3 million ARR run rate for RaceControl sooner than I expected, potentially as early as March. I was expecting to happen in June driven by the Le Mans 24 hour race. This segment along with the licensing segment has over 90% margins and significantly enhances the profitability profile. Q1 is shaping up to be even stronger, with a $1M per quarter high-margin baseline from RaceControl and licensing, plus immediate top-line contribution from the new DLC pack launched on March 23rd.

The core business is scaling rapidly, yet the stock is priced as if bankruptcy is imminent. The ongoing selling overhang from Mike Zoi remains the primary artificial drag on the share price imo. Once that clears, the strong fundamentals should drive a dramatic rerating. I don’t see another reason for the current valuation. The presence of the Sidoti analyst on today’s call (first time in a long while) suggests institutional interest is building, and we may see coverage initiations soon.

The turnaround appears complete and hopefully aggressive growth should follow from here.

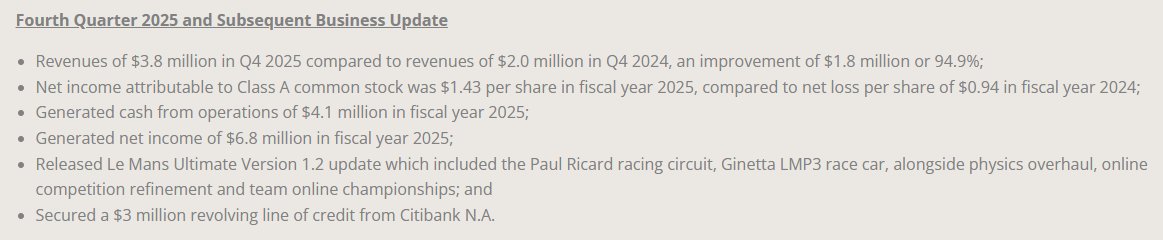

Mar 10

$MSGM came in at $3.8M as we projected. Recall, Q1'26 might be better than this. RaceControl subscriptions continue to grow as the deferred revenue is flat eventhough we had a huge monetization event in Q4. Full commentary after reviewing the 10-Q and earnings call. Congratulations to anyone who believed in the thesis.

3

1

15

4,641

Mar 10

$MSGM came in at $3.8M as we projected. Recall, Q1'26 might be better than this. RaceControl subscriptions continue to grow as the deferred revenue is flat eventhough we had a huge monetization event in Q4. Full commentary after reviewing the 10-Q and earnings call. Congratulations to anyone who believed in the thesis.

Mar 7

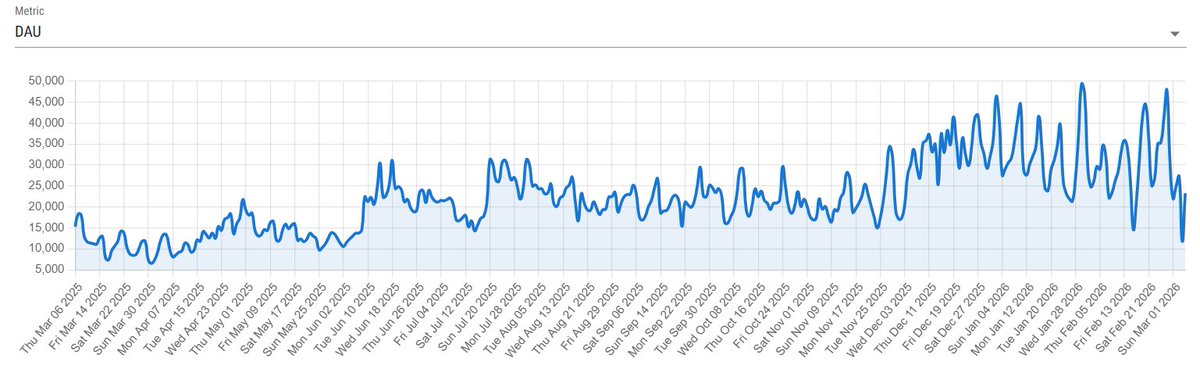

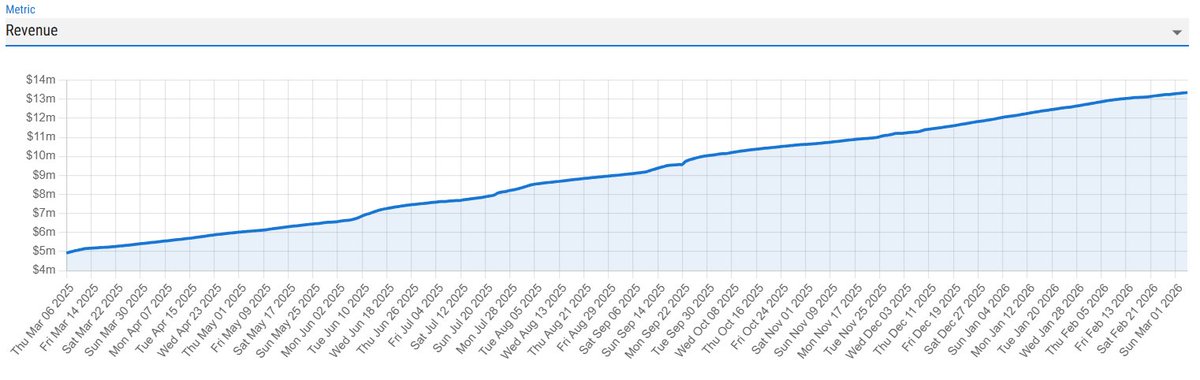

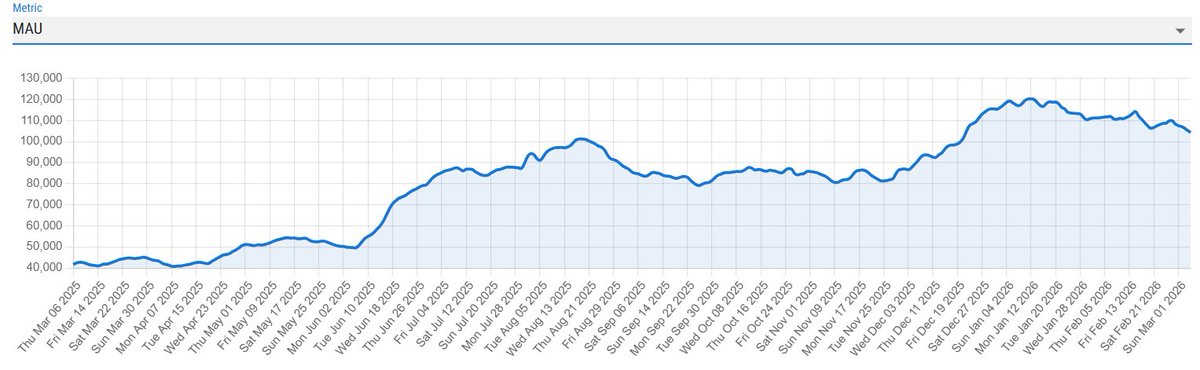

$MSGM some important charts for anyone interested and some analysis regarding the same.

1. DAUs & MAUs: DAU and MAU numbers have maintained the elevated levels observed since the Version 1.0 release, and the baseline lifted significantly following the v1.2 update in December. As the charts show, the numbers have held this higher baseline, which bodes incredibly well for Q1'26. The game almost broke its highest DAU record during the 12-hour testing event last weekend.

We might see a slight seasonal dip here, but expect a recovery later this month driven by the new DLC launch, alongside anticipated bug fixes and announcements regarding the Virtual Le Mans event. Keep in mind that the e-gaming segment has generated no revenue for two years, any contribution here will be a pure tailwind against $0 comps.

2. Revenue Estimate: The model suggests that revenue from base game sales will likely be flat QoQ. I am not concerned about this, as I expect top-line lift to be driven by Deferred Revenue converting to realized revenue this quarter. We should also see a better attach rate from DLC sales (following the large December release) and RaceControl revenue exiting the quarter at a potential $2.5M ARR. The average playtime chart proves our core thesis; players spending more time in game leads to higher retention and directly aids add-on sales.

3. F1 Arcade: The Las Vegas F1 Arcade opened in October (their largest location with the most sims), which will meaningfully boost the licensing revenue portion of the business. My estimation is that this segment is already doing > $1M ARR. There are 8 F1 Arcades open right now, and Kindred Concepts plans to scale to 30 by the end of 2027. This business alone could add more than $3M in recurring revenue by the end of next year at 85% gross margins. To put that into perspective, the company's total revenue for 2024 was ~$8.7M.

It is entirely possible this stock goes from being completely ignored to a darling of FinTwit. Execution risks remain elevated, but the setup has the potential to deliver a $DBO.TO like move.

5

13

4,358

Stop-and-go penalty for Franco Colapinto.

The driver must serve the penalty after being found guilty of a starting procedure infringement earlier in the race.

A major setback in the early stages of the Australian Grand Prix.

#F1 #AustralianGP #Colapinto #RaceControl

2

1,294

Mar 7

$MSGM some important charts for anyone interested and some analysis regarding the same.

1. DAUs & MAUs: DAU and MAU numbers have maintained the elevated levels observed since the Version 1.0 release, and the baseline lifted significantly following the v1.2 update in December. As the charts show, the numbers have held this higher baseline, which bodes incredibly well for Q1'26. The game almost broke its highest DAU record during the 12-hour testing event last weekend.

We might see a slight seasonal dip here, but expect a recovery later this month driven by the new DLC launch, alongside anticipated bug fixes and announcements regarding the Virtual Le Mans event. Keep in mind that the e-gaming segment has generated no revenue for two years, any contribution here will be a pure tailwind against $0 comps.

2. Revenue Estimate: The model suggests that revenue from base game sales will likely be flat QoQ. I am not concerned about this, as I expect top-line lift to be driven by Deferred Revenue converting to realized revenue this quarter. We should also see a better attach rate from DLC sales (following the large December release) and RaceControl revenue exiting the quarter at a potential $2.5M ARR. The average playtime chart proves our core thesis; players spending more time in game leads to higher retention and directly aids add-on sales.

3. F1 Arcade: The Las Vegas F1 Arcade opened in October (their largest location with the most sims), which will meaningfully boost the licensing revenue portion of the business. My estimation is that this segment is already doing > $1M ARR. There are 8 F1 Arcades open right now, and Kindred Concepts plans to scale to 30 by the end of 2027. This business alone could add more than $3M in recurring revenue by the end of next year at 85% gross margins. To put that into perspective, the company's total revenue for 2024 was ~$8.7M.

It is entirely possible this stock goes from being completely ignored to a darling of FinTwit. Execution risks remain elevated, but the setup has the potential to deliver a $DBO.TO like move.

Mar 5

$MSGM looks like people were waiting for the earnings date announcement to position long.

3

1

10

5,108

ちなみに

昨日iRacingで不具合があったんだけど

サポートにメールしたら

30分以内に返事が来て

的確なやりとりであっという間に解決した

某RaceControlとはだいぶ練度が違うなと感じたよw

3

131

Mar 4

I know most people didn’t read the SS post, so I wanted to share my thoughts on the $MSGM setup, which I believe is extremely compelling heading into 2026. Thanks to @DMetropolitan for bringing this to my attention.

I believe the set up is massively misunderstood and offers asymmetric upside. Currently trading at a market cap of roughly $20 million and essentially 1x forward sales, the market is mispricing the equity as a distressed, capital-destructive legacy gaming publisher.

The company has executed a structural turnaroundand is now completely debt-free with $4.5 million in cash reserves. Driven by the shift from physical retail sales to the high-margin RaceControl SaaS platform, gross margins have expanded to an exceptional 80.7%. Over the coming quarters, I believe, the underlying intrinsic value of this recurring revenue ecosystem will become the narrative which will drive the stock higher.

Social Arbitrage & Capturing the Competitor Vacuum

LMU is aggressively cannibalizing market share in a landscape currently defined by lackluster competition. The historical king of GT3 racing, Assetto Corsa Competizione (ACC), has been effectively abandoned by its developers in favor of Assetto Corsa Evo, a title currently facing heavy community criticism and OVERWHELMINGLY NEGATIVE rating on Steam.

Simultaneously, the reigning multiplayer titan, iRacing, continues to alienate newer players with sunk-cost fatigue, requiring hundreds of dollars just to participate. LMU is exploiting this friction well.

The games' momentum is being accelerated by major YouTube KOLs like Jimmy Broadbent and Danny Lee, who are actively redirecting their massive audiences into the MSGM ecosystem due to its superior, highly communicative tire physics and accessible pricing. The brand loyalty can also be seen from the positive comments on YouTube videos released by LMU. The development team and CEO Stephen Hood are receiving overwhelming praise for their transparency and community driven updates, proving they are actively listening to their player base.

Unprecedented Engagement & De-Risked Infrastructure

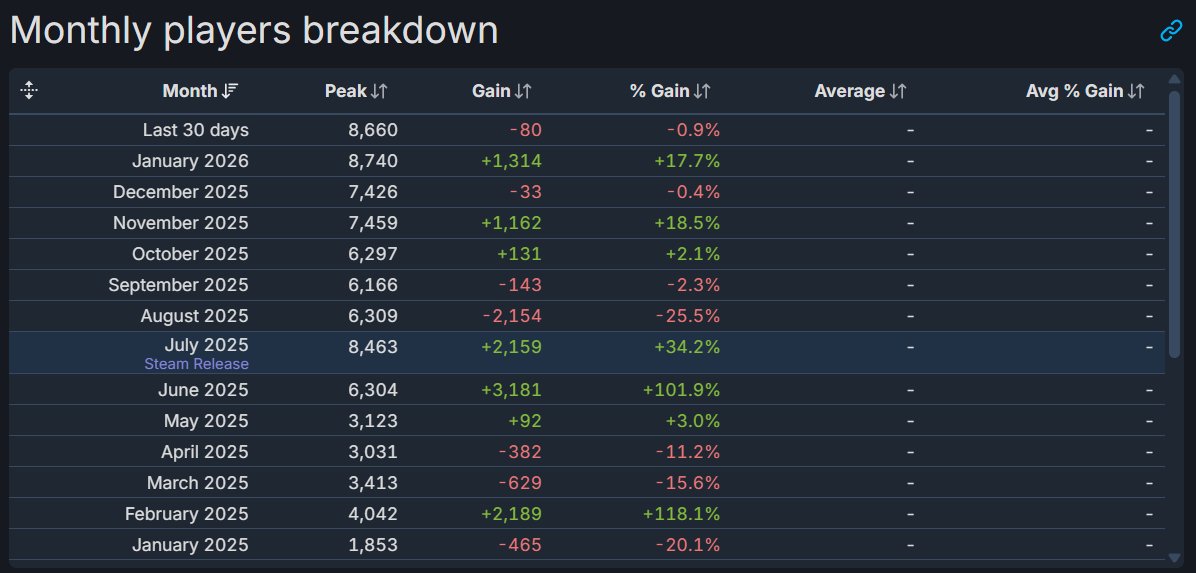

In their December 2025 press release, the company mentioned that players drove a staggering 12.5 million laps on RaceControl (608% YoY increase). That growth compounded into the new year, with Steam concurrent player peaks hitting all-time highs of 8,740 in January and 8,660 in February 2026. What makes these metrics truly explosive is that the real-world 24 Hours of Le Mans doesn't even take place until June, these numbers are strictly organic.

As MSGM continues to roll out new tracks, cars, and highly requested features like a single-player career mode, the adoption of their high-margin RaceControl Pro ($48/yr) and Pro ($84/yr) subscriptions will continue to scale rapidly.

This past weekend, LMU hosted stable 12-hour endurance races with complex driver swaps, the developers proved they have resolved the scaling bottlenecks that plagued the platform in the past. This was the Achilles heel of the company in 2023 and resulted in Max Verstappen getting disconnected during the 2023 virtual event which caused a lot of negative press.

Upcoming Catalysts & The Console Lottery Ticket

We are entering a compressed window of highly lucrative catalysts. The Q4 2025 earnings report will benefit from a massive deferred revenue tailwind, as the December launch of ELMS Pack 2 legally unlocked significant cash parked on the balance sheet under ASC 606 accounting standards. Q1 2026 is structurally positioned to be even stronger, leveraging all-time high player counts and aggressively optimized SaaS monetization.

Looking ahead to the summer, the June Le Mans Virtual event will most likely completely shatter existing records, driving an immense top of funnel lift for the RaceControl platform. If MSGM successfully secures commitments from massive real-world drivers to join the simulation, a strategy currently in motion according to the management, the mainstream cultural exposure could trigger a viral explosion for the game.

The sticky PC player base could also give MSGM immense leverage in their late-stage negotiations with third-party partners to fully fund the console port. Porting an already-optimized PC architecture to PlayStation and Xbox is a manageable transition that instantly unlocks a TAM multiple times larger than their current footprint. If management can smooth out the remaining minor VR bugs and penalty system friction, 2026 is destined to be a watershed year for the company.

Feb 20

Not my idea, but one I'm really liking for earnings is $MSGM. Working on an SS post and hoping to share it this weekend, link in the bio (no paywall). Medium-risk play but could be a potential multibagger.

The current quarter is shaping up to be a material turning point, as significant revenue tailwinds from the Q4 "Track and Pack" release suggest a potential blowout performance. The December 2025 update, which introduced the Paul Ricard circuit and the innovative "Team Online" feature, has acted as a massive catalyst for both high-margin DLC sales and recurring "RaceControl Pro" subscriptions.

Alternative data and web traffic metrics support this narrative, showing a 126% spike in traffic between community hubs and the storefront, while traffic to the "Pro" subscription paywall has soared by 60%. This momentum has carried directly into January 2026, which saw the game hit an all-time peak of 8,740 concurrent players, a 4x increase over the previous year an This suggests to me that the market is missing a surge in deferred revenue and ARPU (Average Revenue Per User) that could make the next earnings report a landmark event for the company's valuation. The company could post revenue numbers close to $3.5M which would represent a significant QoQ growth and a material lift in the bottom line owing to the 80% margins from DLC and RaceControl Pro subscription.

Motorsport Games $MSGM is a possible turnaround story with great social traction, where a company has successfully pruned its distractions and is now focusing on its high margin business. Historically, MSGM was a bloated license collector and burdened by expensive, underperforming contracts for NASCAR and IndyCar that drained cash at a rate of $2 million per month.

Under the leadership of returning CEO Stephen Hood, the company has cleaned up its act materially and is divesting the NASCAR license and refocusing entirely on its crown jewel: Studio 397 and the Le Mans Ultimate (LMU) platform. The company has shrunk its footprint to a boutique team of 41 people who develop the industry-leading rFactor 2 physics engine, one $FWONK & $DBO.TO $DBOXF use for their F1 Arcades. MSGM has reduced its monthly cash burn to less than $100,000 and I believe will be cash flow positive in Q4 creating a lean foundation for a possible multi-bagger opportunity.

The story today is about their pivot towards a technology centric SaaS model via the RaceControl platform. The broader market is incorrectly focused on a perceived slowdown, alternative data and social sentiment analysis from community hubs like Reddit and Discord reveal a thriving, highly engaged ecosystem.

MSGM has teased a potential new game, as noted they provide the physics engine for the F1 Arcade, MSGM has established a strategic moat that could realistically lead to a full-scale F1 simulation title in the future. This is currently ignored by Wall Street, yet it provides a free lottery ticket on future high-profile developments. In the near term, the return of the Le Mans Virtual championship serves as a material catalyst, likely driving peak user numbers and lucrative sponsorships that will lift ARPU.

Finally, the most significant catalyst is the impending console port for PS5 and Xbox. Management is in late-stage negotiations with a funding partner to foot the entire bill for development, effectively eliminating MSGM’s financial risk while opening the door to a user base 4X larger than the current PC market. With growing deferred revenue and material catalysts in the current quarter, the market’s pessimistic view of MSGM is a textbook mispricing. MSGM offers the rare combination of a "boring" niche business, a proven tech moat, and massive multi-platform growth potential that is currently underfollowed by the institutional crowd.

2

1

17

6,950