Jun 11

Star Imaging and Path Lab Ltd upgrades diagnostic centre at Tilak Nagar, New Delhi

#StarImagingandPathLab

equitybulls.com/category.php…

131

May 25

#SME #StarImagin #StarImagingandPathLab

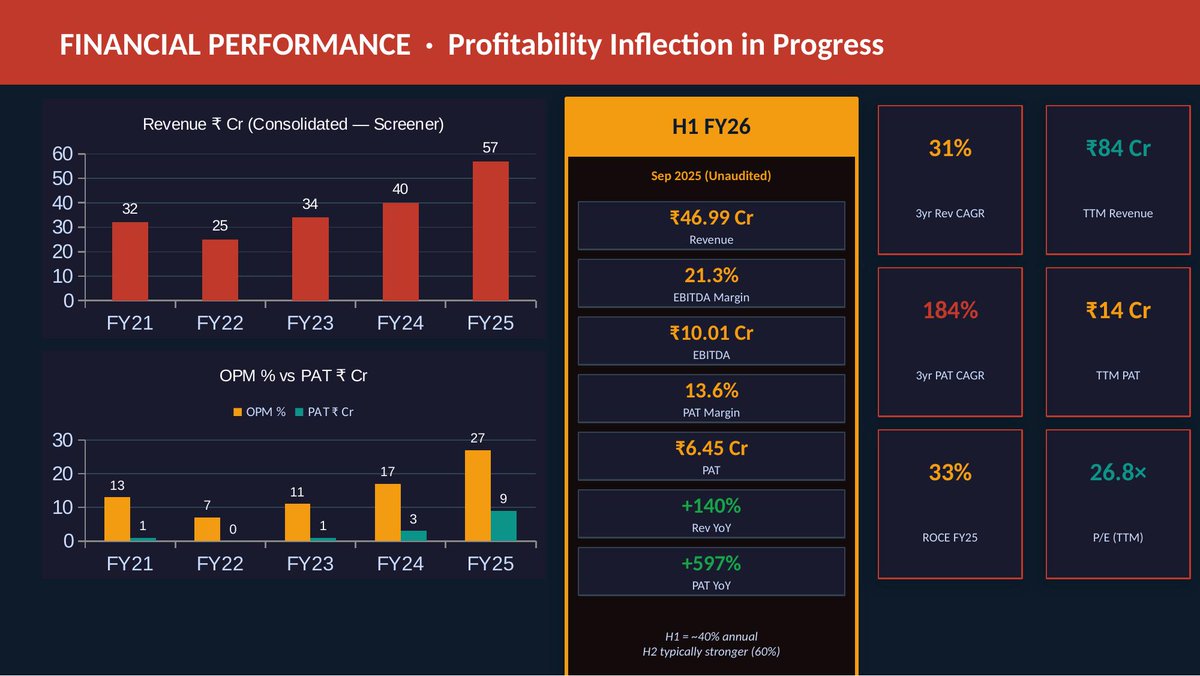

Star Imaging and Path Lab Limited H2FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️Management reiterated 25-30% YoY revenue growth guidance for FY27

💠Expects this momentum to remain consistent over the next 2–3 years.

💠Key drivers include new center ramp-ups, B2C expansion, B2B hospital tie-ups, and operating leverage on a stable cost base.

▫️EBITDA margins expected to stay sustainable around 37.5%

💠PAT margins likely to remain healthy in the 21–22% range.

▫️Capex guidance for FY27: ₹20–25 crores, primarily for new centers, equipment, and upgrades.

💠Dwarka center (major B2C project) already opened; expected to contribute meaningfully from H1 FY27.

👉 Current Projects, Expansions & Pipeline

▫️Dwarka B2C Center:

💠New flagship center with ~₹14 crores capex.

💠Expected initial annual revenue ₹5–6 crores, blended EBITDA margins 35–40%.

💠Break-even targeted in 6–12 months (12 months for this larger center); project payback 2.5–3 years.

💠Response so far described as encouraging though still in early gestation.

▫️Existing Center Upgrades:

💠Vikaspuri center expanded and upgraded with new MRI and CT machines (already operational).

💠Tilak Nagar center upgraded with 640-slice CT scan.

▫️B2B / Hospital Tie-ups: Network significantly expanded to 100 hospitals (added 40–45 new empanelments during the year).

💠Tied up with RG Hospital (CT machine installed and commercialized).

💠4 additional tie-ups with RG Stone in pipeline (smaller capex ~₹2 crores each, faster break-even expected).

▫️B2G: Empaneled with Central Government Health Scheme (CGHS) – provides revenue stability.

💠Regulatory challenges caused delays in past projects; management confident these are now largely addressed, with two new centers already operational and more coming online soon.

▫️Pipeline remains healthy with additional B2C and B2B projects in various stages; focus remains on B2C as primary growth lever (B2G tender-dependent, B2B complementary).

👉 Other Notable Points

▫️Balance Sheet & Working Capital:

💠Trade receivables stood at ₹49.9 crores (elevated due to B2G payment cycles of ~6 months).

💠Net cash position ₹31.0 crores; total debt ₹20.6 crores.

💠Management actively working on faster collections and expects further normalization.

💠 Aim to remain largely debt-free, though selective borrowing possible for large tender opportunities.

▫️Business Mix (FY26): Radiology ~83%, Pathology ~14%. Multi-channel model – B2C 18%, B2B 10%, B2G stable. 24 diagnostic centers, team of 236, 7.1 lakh tests conducted.

▫️AI Impact:

💠Currently nascent in radiology (helps with preliminary reporting on X-rays/CTs) but requires radiologist sign-off.

💠No material disruption expected; viewed as productivity enhancer rather than replacement.

▫️Competition & Strategy:

💠Company continues to compete effectively with larger players (e.g., Dr Lal PathLabs is primarily pathology-focused).

💠Emphasis on latest technology, quality accreditations (NABL, NABH), brand strength, and strategic location selection.

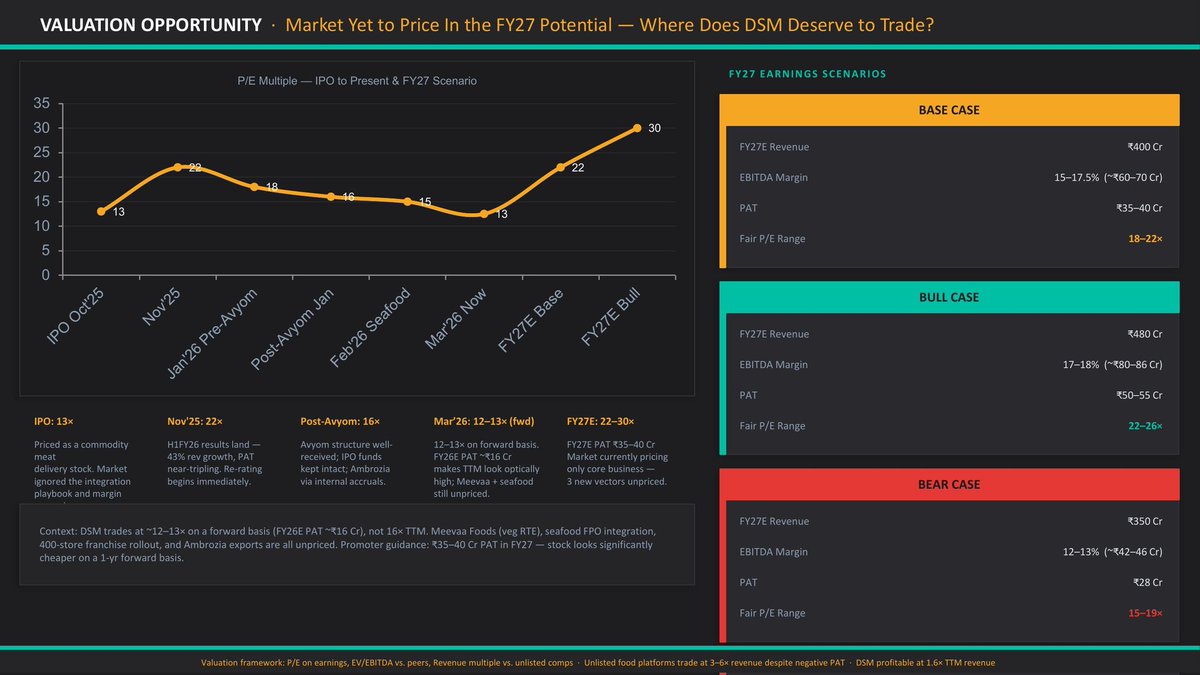

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

1

1

17

2,521

28 Jul 2024

नजफगढ़: गोपाल नगर में निःशुल्क स्वास्थ्य मेडिकल कैंप का आयोजन | @News24bhartvrsh

#नजफगढ़ #दिल्लीनजफगढ़ #नजफगढ़दिल्ली #दिल्लीकानजफगढ़ #दिल्लीकानजफगढ़इलाका #निशुल्ककैम्प #फ्रीमेडिकलकैंप #निःशुल्कचिकित्साशिविरकाकियागयाआयोजन #starimagingandpathlab

youtu.be/aipyv3JMDvI

1

2

9

This Doctor's Day, let’s take a moment to reflect on the immense value our #doctors bring to society.

Join us in honoring these incredible heroes. #Tag a doctor who has made a positive impact on your life..🩺💙👩⚕️

youtu.be/CDBdjsr-Cx8

#StarImagingAndPathLab #DoctorsDay2023

5

210

30 Jun 2023

Dr. @DrSameerBhati , Director, Star Imaging & Path Lab sharing his expertise & enlightening us on the significance of staying #hydrated this #summer.

fb.watch/luvwdUC6-1/?mibexti…

Share these tips with your friends and family & let's #BeatTheHeat together!☀️

#StarImagingAndPathLab

4

107

Everything we do comes from the heart! 🌍❤️ Star Imaging & Path Lab honors the selfless dedication of the Red Cross and pledges to contribute to a healthier future for all. Together, we can make a difference! 🔬#StarImagingAndPathLab #WorldRedCrossDay

3

63

Your health, our priority - right at your doorstep! 🚪🌟 Star Imaging & Path Lab offers free home sample collection, making it easier than ever to take charge of your well-being. Simplify your wellness journey with our trusted services. 💉🔬 #StarImagingAndPathLab #HomeCollection

3

56

Detect early, act wisely, and live fully! 🌟 Star Imaging & Path Lab's disease detectives are here to unmask hidden illnesses. Choose the path of prevention and stay ahead in your health journey. 🔬💪 #StarImagingAndPathLab

3

47

Celebrating our healthcare heroes at Star Imaging & Path Lab on this World Workers Day! 🌟🔬 Thank you for shining light on our path to better health. 💉🩺

#WorldWorkersDay #HealthcareHeroes #StarImagingAndPathLab #MedicalWarriors #PathLabPioneers #HealthcareAppreciation

1

4

92

28 Apr 2023

Your well-being, our priority! 🌟💼 Celebrating World Day for Safety and Health at Work with our dedicated team. #StarImagingAndPathLab #WorkplaceSafety #HealthAtWork #WorldDayForSafetyAndHealth #LabHeroes #HealthyWorkforce

1

5

218

22 Apr 2023

Taking care of our 🌍 is everyone's responsibility - even in the lab! Star Imaging & Path Lab is committed to sustainable practices for a healthier planet. Let's make every day Earth Day 🌳💚 #InvestInOurPlanet #WorldEarthDay #StarImagingAndPathLab

6

65

22 Apr 2023

Wishing you a healthy and blessed Eid-ul-Fitr from Star Imaging and Path Lab! 🌙💉 May this joyous occasion bring you and your loved ones good health and happiness. ✨👩⚕️👨⚕️ #StarImagingAndPathLab #EidUlFitr2023 #EidMubarak #HealthIsWealth #LabTests #Pathology #StayHealthy

6

148

20 Apr 2023

Honored to receive the "Best Legend of the Year 2023" in Pathology & Imaging Center Category at SMEBIZZ Legends Star Awards! 🌟 Grateful to Shantanu Thakur, esteemed Member of the Lok Sabha, for presenting this prestigious award. At Star Imaging and Path Lab, we'll continue providing quality diagnostic services & pushing the boundaries of innovation. 💫🩺 #SMEBIZZLegendsStarAwards2023 #PathologyAndImaging #DrSameerBhati #HealthcareInnovation #StarImagingAndPathLab

1

7

95

15 Apr 2023

Feeling feverish? 🤒 Don't ignore the early signs! Get your complete CBC test at Star Imaging & Path Lab today 🌟 It could be typhoid, dengue, or malaria – let's catch it early! 💪 #HealthFirst #StarImagingAndPathLab #StayAwareStayHealthy

#FeverCheck #CBCtest

3

67

14 Apr 2023

Star Imaging and Path Lab wishes you a healthy and prosperous Baisakhi! 🌾 Let's celebrate new beginnings together, as we continue providing top-quality diagnostics for a healthier future. 💉🔬💪 #Baisakhi2023 #StarImagingAndPathLab #HealthForAll

5

110

13 Apr 2023

Love your liver, feed it right! 🌟🍏 Celebrate Liver Day with Star Imaging & Path Lab by nourishing your body with liver-friendly foods. Cheers to a healthier you! 💚🔬 #LiverDay #StarImagingAndPathLab #HealthyLiver #FoodForYourLiver

4

61

🌟 Dr. Kanika Mahajan lights up our lab, making a difference one test at a time! 💉 Celebrating #WorldHealthDay with our shining star at Star Imaging & Path Lab 🌍🩺✨ Let's strive for a healthier future together! 💪 #StarImagingAndPathLab #HealthForAll #DrKanikaMahajan #LabLife

5

122

🌍 Celebrating World Health Day 2023 with Star Imaging & Path Lab! 🎉 As we strive for #HealthForAll, remember the importance of early detection and accurate diagnosis. 🩺💉 🌟💚 #WorldHealthDay #StarImagingAndPathLab #YourHealthMatters

4

155

🔬Starry insights at your service! 🌟 Navigate the maze of health with us. Follow these do's ✔️ and don'ts ❌ to banish that nagging feeling for good! 💪 #StarImagingAndPathLab #HealthWarriors #DosAndDonts

5

62

24 Mar 2023

Join us in the fight against abdominal TB this World TB Day. Together, we can shine a light on this silent killer and work towards a healthier future. #WorldTBDay #AbdominalTB #StarImagingAndPathLab

3

58