📊 HDFC Bank (HDFCBANK)

Today's market context: elevated focus on stock-specific stories within broader index moves.

FUNDAMENTAL LENS:

• Sector: Banking & Financial Services

• Business mix:

• Core business with strong brand and market positioning

• Multiple growth drivers across domestic and export markets

• High operating leverage once capacity is fully utilised

• Financial quality focus:

• Clean balance sheet focus – emphasis on prudent leverage

• Consistent operating profitability through cycles

• Disciplined capital allocation with focus on return ratios

• Valuation framework: historically trades in appropriate sector valuation bands

• Key things informed investors usually monitor:

• Evolution of margin profile over next 4–6 quarters

• Management commentary on demand visibility and order book

• Any large capex / inorganic announcements impacting balance sheet

TECHNICAL LENS (EDUCATIONAL VIEW):

• Price structure: sideways consolidation after a strong prior upmove

• Recent price action: multiple inside bars signalling compression before expansion

• Indicator snapshot: price staying above 50-DEMA, acting as dynamic support

• Reference zones on chart:

• Immediate reference support zone on daily chart

• Nearby resistance band where supply has previously emerged

• Psychological round-number levels watched by market participants

• Risk/volatility notes:

• Sharp moves after extended rallies can lead to mean reversion phases

• Gap moves around news/earnings can create volatility pockets

EDUCATIONAL TAKEAWAYS (NOT A BUY/SELL CALL):

• This is a study-style breakdown to understand how market participants often analyse HDFC Bank.

• Purpose is to learn how fundamentals, valuations and technical structure come together in one framework.

• Always combine multiple timeframes, risk management and personal research before making any decision.

#StockReport #IndianMarkets #HDFCBANK #MarketEducation

2

167

Feb 9

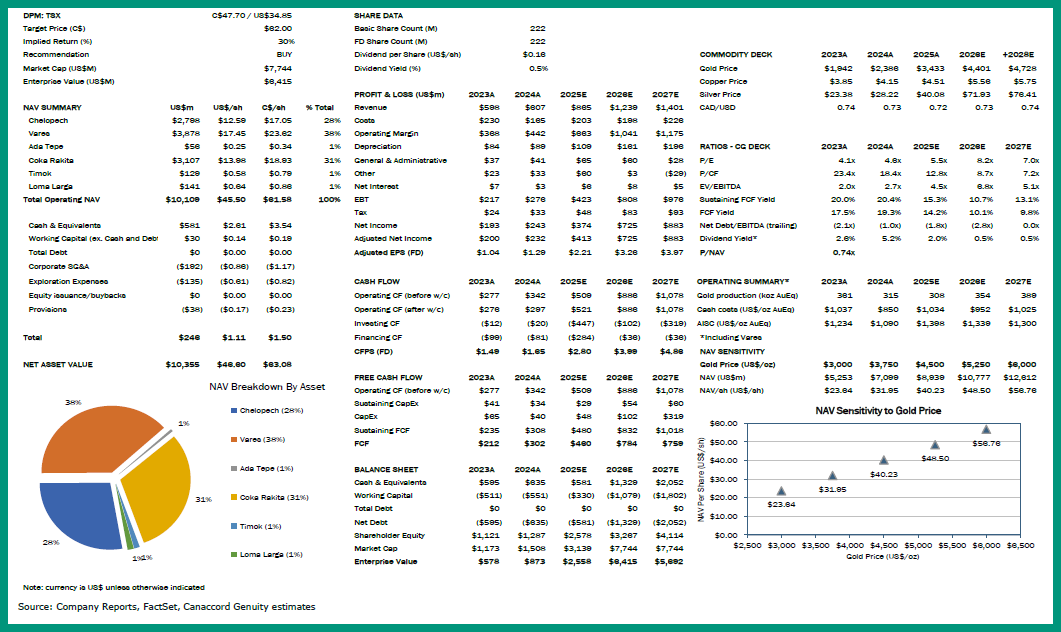

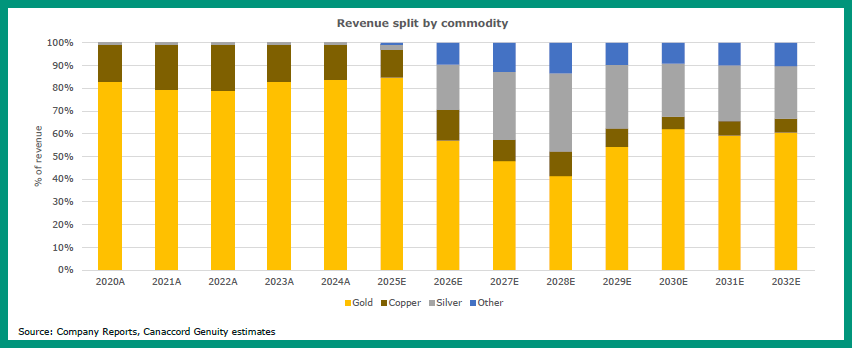

CG || DPM Metals Inc.

Longer legs at Chelopech: mine life extended to 2036

Event: Yesterday evening, February 5, DPM released an updated reserve and resource (R&R) estimate and a new life-of-mine (LOM) plan for its Chelopech mine in Bulgaria. Our take: Positive. Total AuEq reserves (AuEq calculated using our long-term commodity price assumptions) increased 4% versus the prior update in November 2023, despite two years of depletion, albeit at a 21% lower grade.

Total AuEq resources (all categories, including reserves) increased 7%. Based on the updated R&R, Chelopech’s mine life has been extended from 2032 to 2036, notably with modestly higher planned throughput levels.

We have updated our model to reflect the revised LOM plan. We have also increased unit operating costs, in line with recent operating performance, and increased capital assumptions, incorporating sustaining capital of approximately $200/oz Au sold over the LOM to support the extended operating life (broadly consistent with comparable underground operations). As a result, our NAV5% for Chelopech increases 32% to $2.8B, representing 28% of total operating NAV.

Our equally weighted target price components — NAV/sh and NTM EBITDA/sh — increase 7.0% and 0.3%, respectively. We leave our target multiples unchanged (1.0x NAV; 10.0x NTM EBITDA), raise our target price to C$62.00/sh (from C$60.00/sh), and maintain our BUY rating.

Target Price C$62.00 from C$60.00

P&L and NAV summary

Revenue split by commodity

#research #EquityResearch #BrokerageReport #MiningResearch #StockReport

2

164

17 Dec 2025

Almost a Year later since you put 5K ON IT

Sibanye Stillwater Limited

JSE: SSW Stock Report

#JSE #SSW #STOCK #STOCKREPORT #StockMarket #SIBANYE

2

2

12

1,009

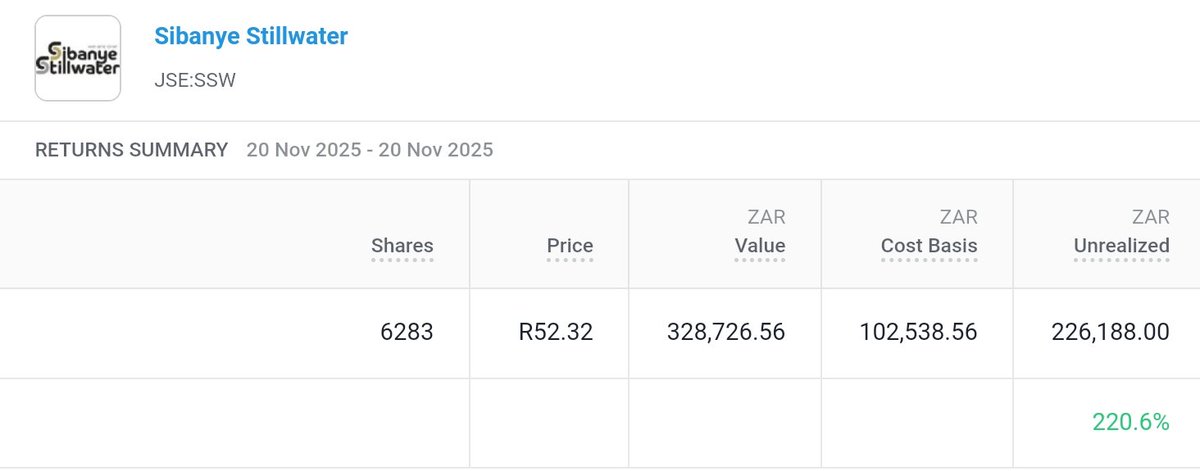

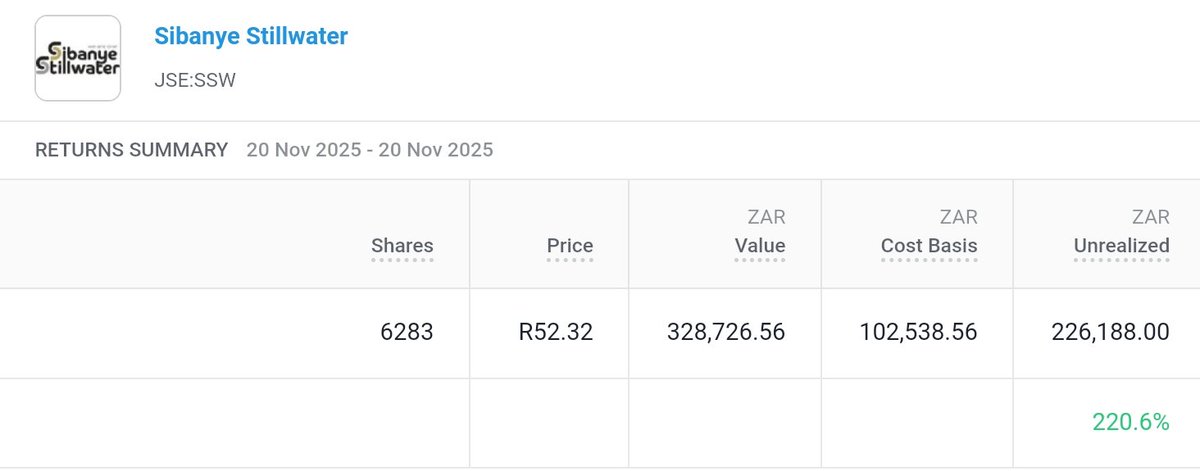

20 Nov 2025

Almost a Year later since you put 5K ON IT

Sibanye Stillwater Limited

JSE: SSW Stock Report

#JSE #SSW #STOCK #STOCKREPORT #StockMarket #SIBANYE

1

2

6

821

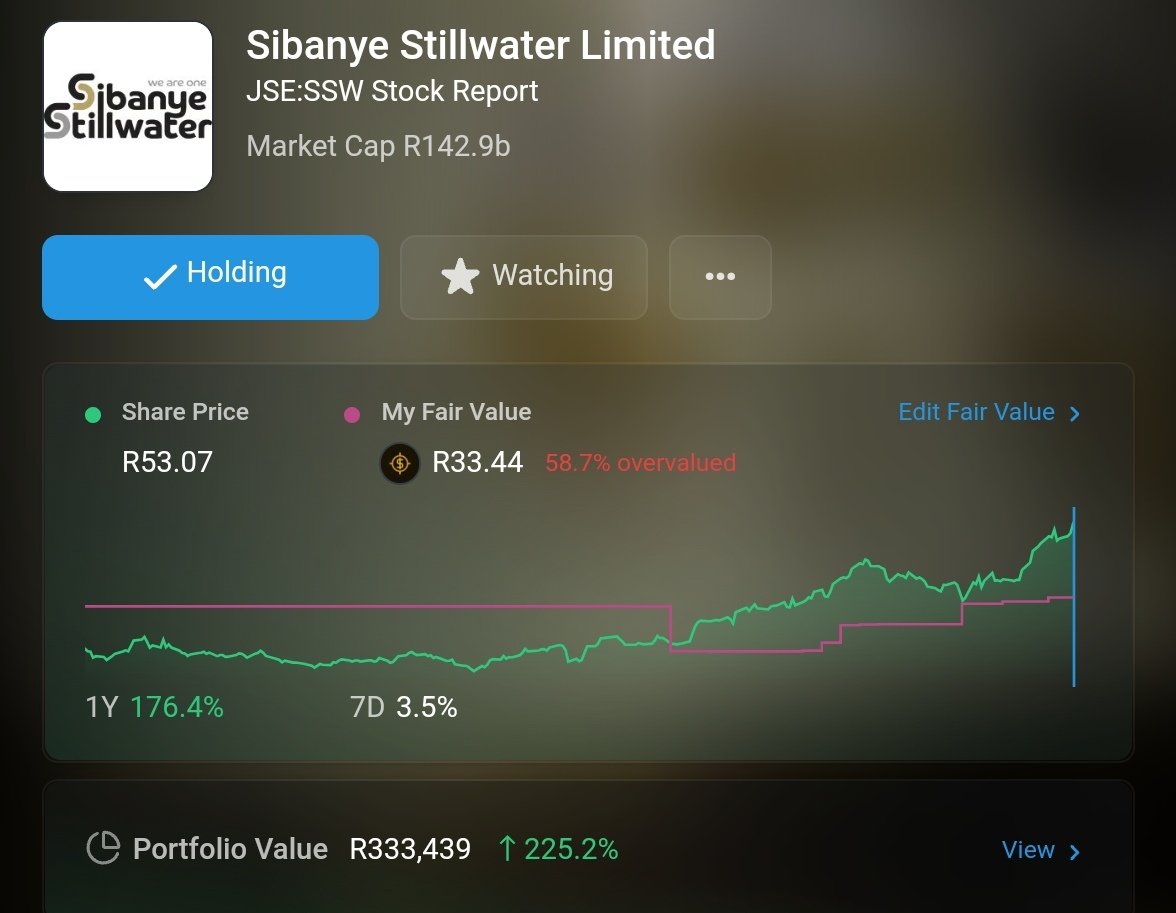

20 Nov 2025

Sibanye Stillwater Limited

JSE: SSW Stock Report

#JSE #SSW #STOCK #STOCKREPORT #StockMarket #SIBANYE

8 Oct 2025

Sibanye Gold now at R53.07 per share

If you took R5000 and bought at R17.00

You'd have R15 600 at current share price

You would have made a R10600.00 profit

#JSE #SSW

1

2

12

1,345

2 Sep 2025

Sibanye Stillwater Limited

JSE: SSW Stock Report

#JSE #SSW #STOCK #STOCKREPORT #StockMarket #SIBANYE

2

2

13

796

2 Sep 2025

Sibanye Stillwater Limited

JSE: SSW Stock Report

#JSE #SSW #STOCK #STOCKREPORT #StockMarket #SIBANYE

7 May 2024

Gold miners decline as dollar edges higher, the reduction in the value of Dollar could result in an increase in the value of GOLD, we could see Sibanye Stillwater Ltd recover its previous years (2021,2022 and 2023) losses

Long-term Bullish outlook

5

487

2 Sep 2025

Sibanye Stillwater Limited

JSE: SSW Stock Report

#JSE #SSW #STOCK #STOCKREPORT #StockMarket #SIBANYE

2

1

14

913

11 Jun 2025

Brokerage Reports: 7 शेयरों में दिखेगा फुल एक्शन- रिपोर्ट में आया नया टारगेट और पूरी जानकारी

#stockmarketsindia #StocksToWatch #StockReport

hindi.cnbctv18.com/share-mar…

2

1

2,506

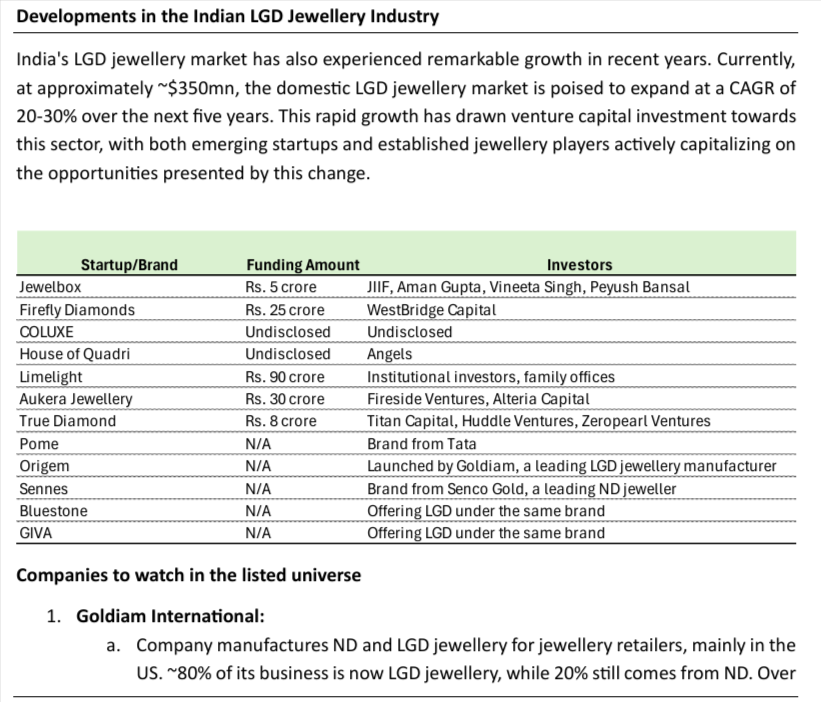

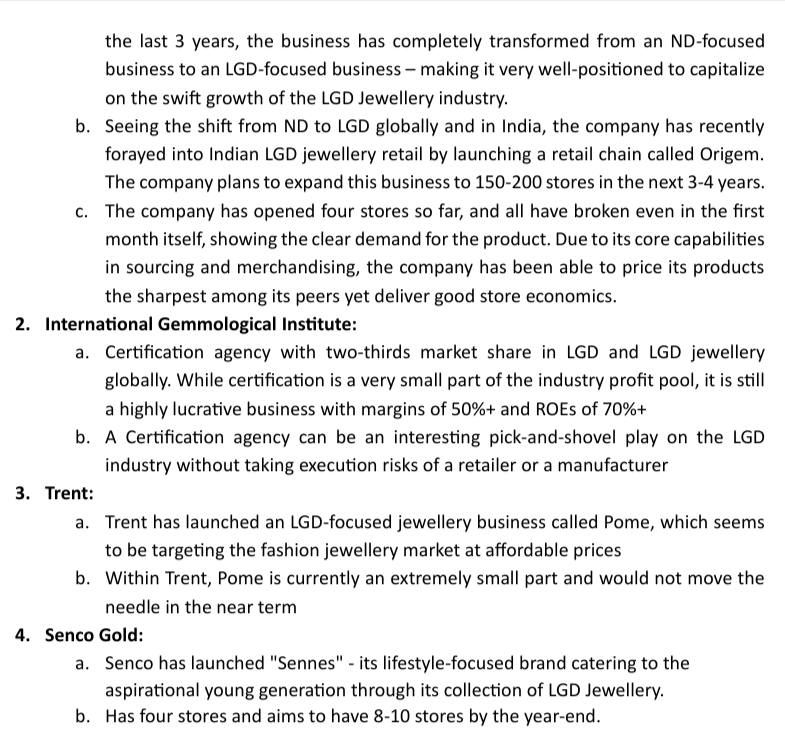

24 Apr 2025

#India | #LabGrownDiamonds

✔️ LGD market @ ₹3,000 Cr; growing 25% CAGR

✔️ Giants like #Goldiam (Origem), #Senco (#Sennes), #Trent (#Pome) entering retail

✔️ 80% biz of Goldiam now LGD-driven

✔️ VC $ pouring into brands like Jewelbox, Limelight, Firefly

#StockReport #Jewellery

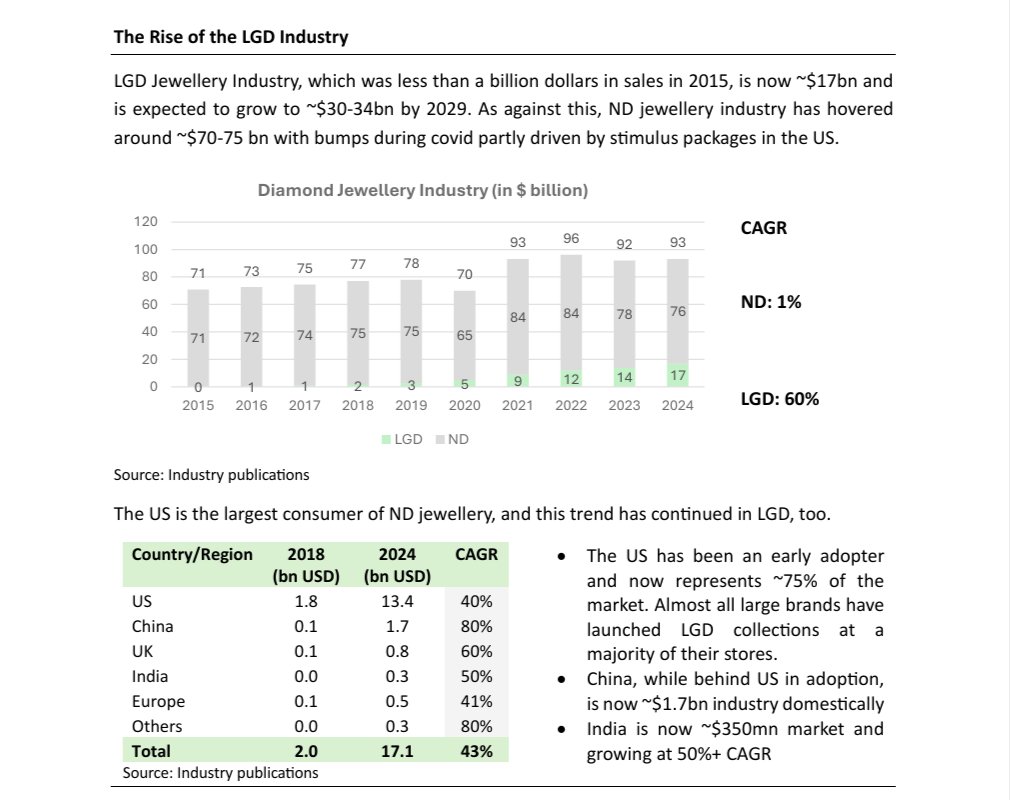

24 Apr 2025

#LabGrownDiamonds 💎

✔️ $17B LGD mkt 📈 8x growth since 2018

✔️ Natural Diamonds flat @ $75B 🚫 zero sparkle in growth

✔️ 🇮🇳 leads in CVD tech 95% polishing 🛠️

✔️ De Beers down from $12.8B → $4.1B

✔️ LGD: 80% cheaper, eco-friendly, indistinguishable 🔬

#Luxury is evolving.

1

5

892

24 Apr 2025

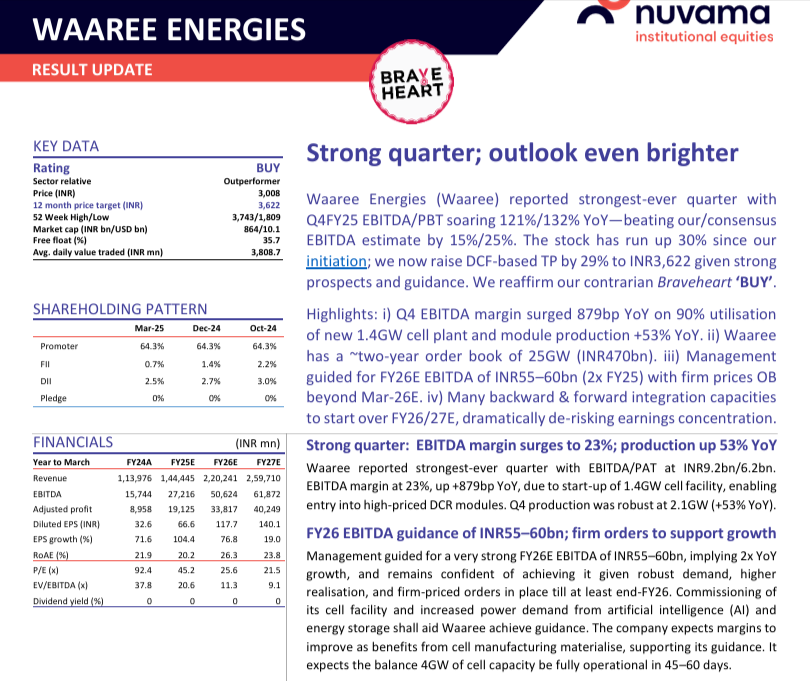

#WaareeEnergies ☀️| TP: ₹3,622

✔️ Record-breaking Q4 – EBITDA/PBT 🔼121%/132% YoY

✔️ 53% production jump; 90% plant utilisation ⚙️

✔️ ₹47,000 Cr order book (25GW) locked-in 🔐

✔️ FY26E EBITDA: ₹55–60B guidance

🌍 Multi-decade green energy play in motion!

#Nuvama #StockReport

6

724

21 Apr 2025

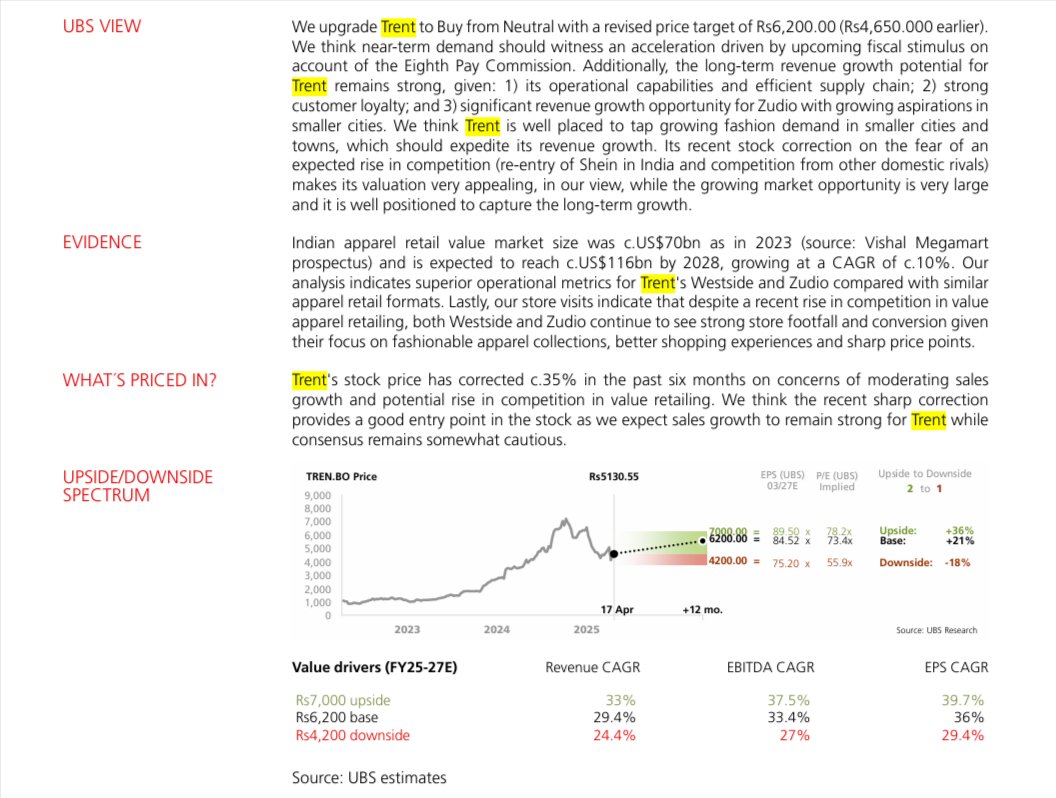

#Trent 🛍️: Tier-2/3 retail goldmine

✅ Zudio store count CAGR: 50% (FY20-25)

✅ Plans: 400 Zudio 36 Westside stores by FY27

✅ EPS CAGR: 36% | Target price : ₹6,200

Premium valuation, but massive growth runway

#Retail #StocksToBuy #FMCG #UBS #Stockreport

21 Apr 2025

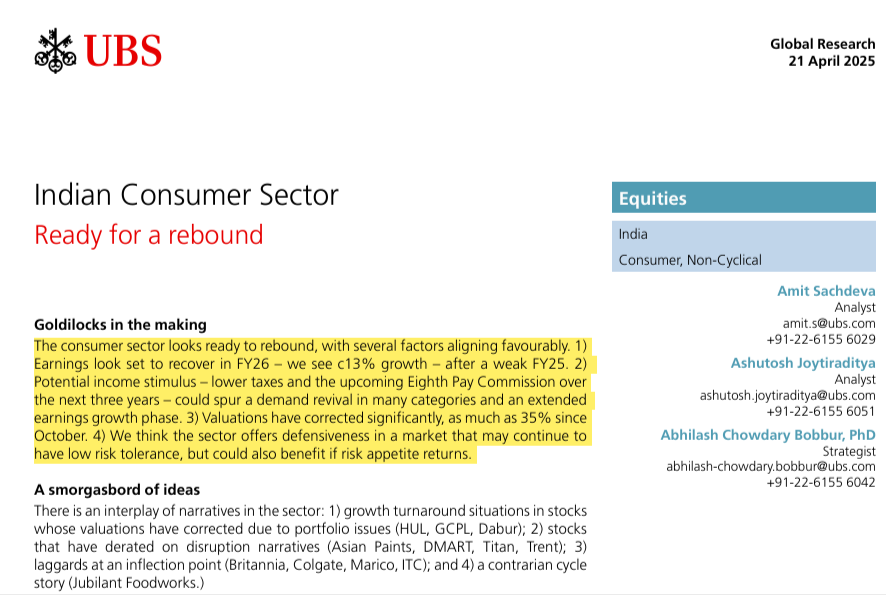

🍕Indian Consumer Sector | #FY26 Outlook by #UBS

✅ Earnings rebound: 13% EPS growth in FY26 (vs 1% in FY25)

✅ Income stimulus: 8th Pay Commission Tax cuts

✅ Valuations corrected: 35% off peak (since Oct'24)

✅ Rural revival easing inflation = demand kicker

#FMCG #Nifty50

2

456

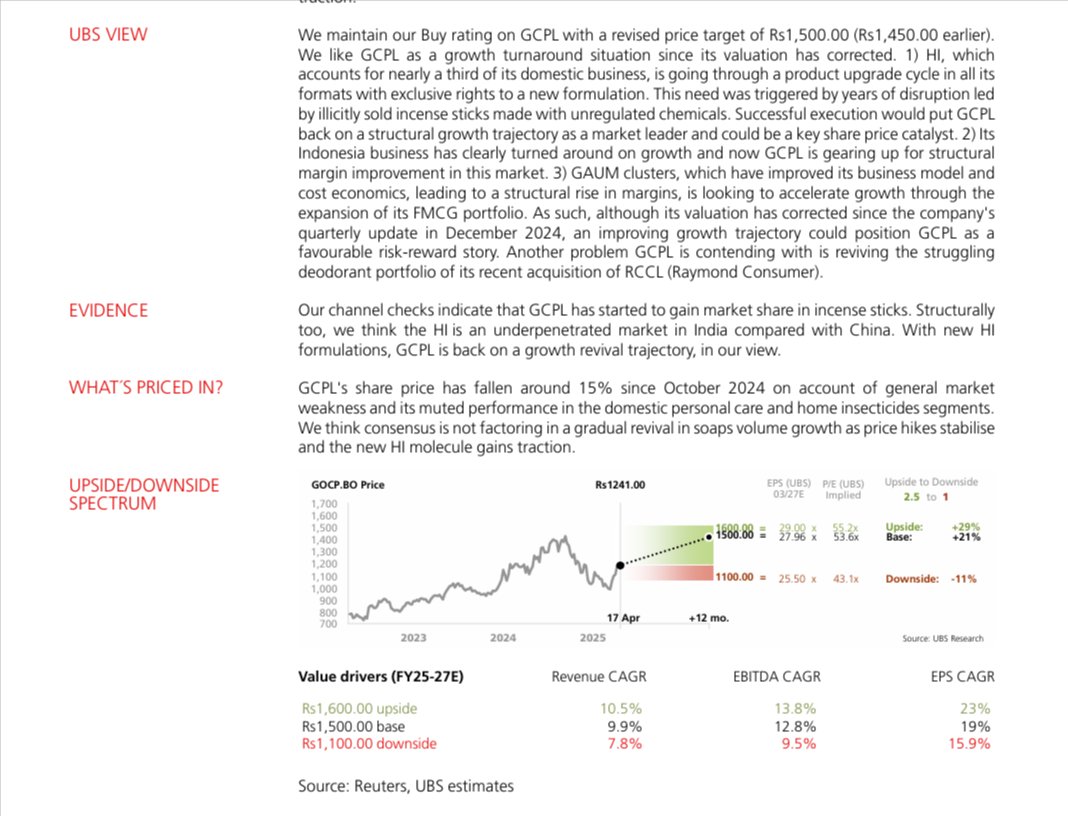

21 Apr 2025

Godrej Consumer Products Ltd🚿

🎯 Target Price: ₹1,500 | EPS CAGR: 19%

✅ HI revamp exclusive new formulation

✅ Indonesia revival Africa margins 🔁

✅ Valuation rerating ahead if execution sticks

#FMCG #TurnaroundStock #UBS #Stockreport

21 Apr 2025

🍕Indian Consumer Sector | #FY26 Outlook by #UBS

✅ Earnings rebound: 13% EPS growth in FY26 (vs 1% in FY25)

✅ Income stimulus: 8th Pay Commission Tax cuts

✅ Valuations corrected: 35% off peak (since Oct'24)

✅ Rural revival easing inflation = demand kicker

#FMCG #Nifty50

2

233

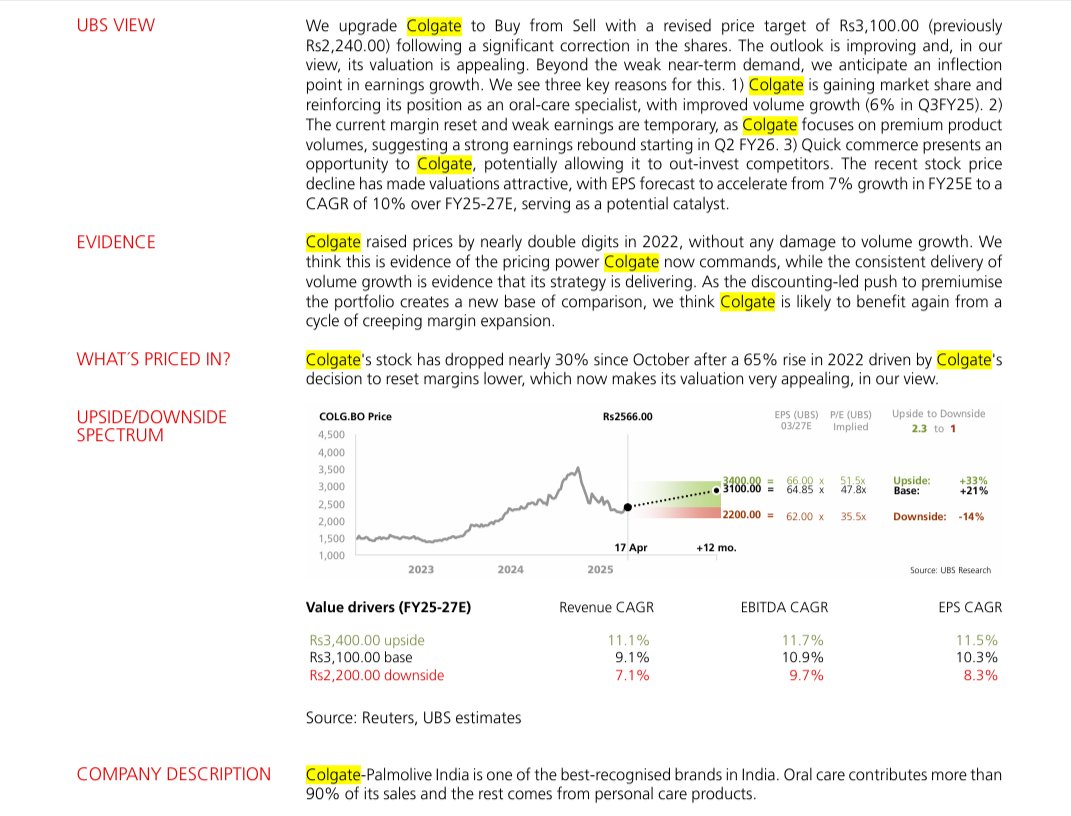

21 Apr 2025

#Colgate 🦷 from Sell → Buy @UBS

✅ Market share reversing after 10-yr dip

✅ Premiumisation driving EPS CAGR of 10.3%

✅ EBITDA margin reset = short-term pain, long-term gain

🎯 Target: ₹3,100 ( 21%)

#StockReport #DefensiveCompounder #FMCG

21 Apr 2025

🍕Indian Consumer Sector | #FY26 Outlook by #UBS

✅ Earnings rebound: 13% EPS growth in FY26 (vs 1% in FY25)

✅ Income stimulus: 8th Pay Commission Tax cuts

✅ Valuations corrected: 35% off peak (since Oct'24)

✅ Rural revival easing inflation = demand kicker

#FMCG #Nifty50

2

219

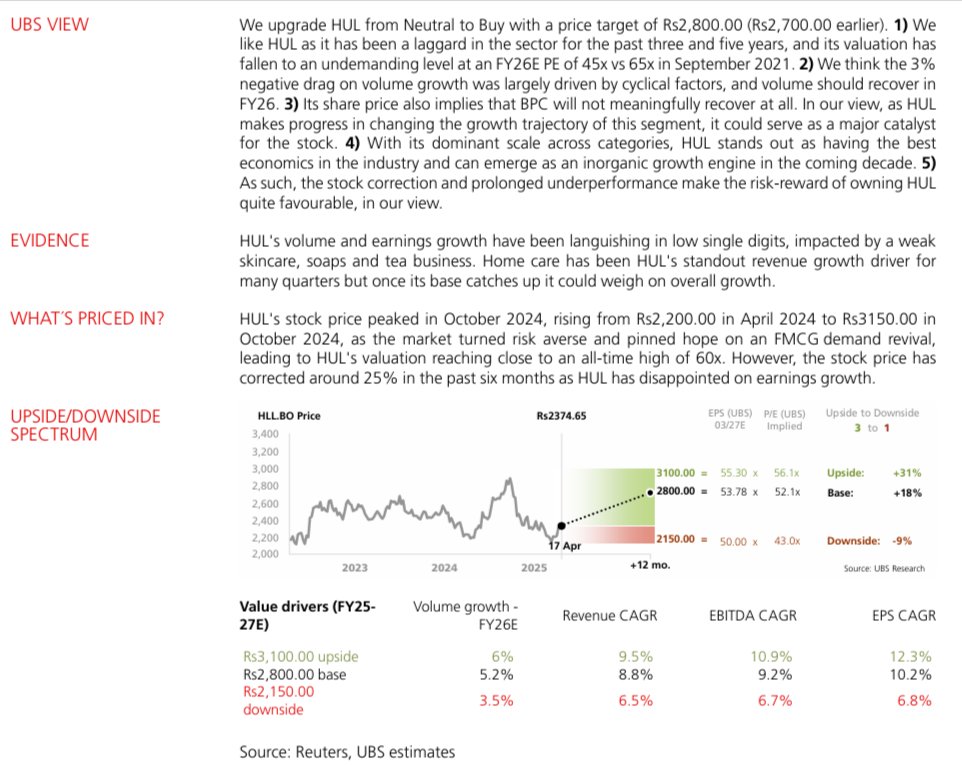

21 Apr 2025

#HUL 📦 Turnaround on radar

✅ Volume rebound in FY26 (est. 6-7%)

✅ New CEO’s India focus beauty/wellness revamp

✅ 30% below pre-Covid peak

🎯 Target Price: ₹2,800 | EPS CAGR: 10.8%

From darling to laggard – ripe for re-rating?

#StockMarketIndia #FMCG #UBS #stockreport

21 Apr 2025

🍕Indian Consumer Sector | #FY26 Outlook by #UBS

✅ Earnings rebound: 13% EPS growth in FY26 (vs 1% in FY25)

✅ Income stimulus: 8th Pay Commission Tax cuts

✅ Valuations corrected: 35% off peak (since Oct'24)

✅ Rural revival easing inflation = demand kicker

#FMCG #Nifty50

2

298

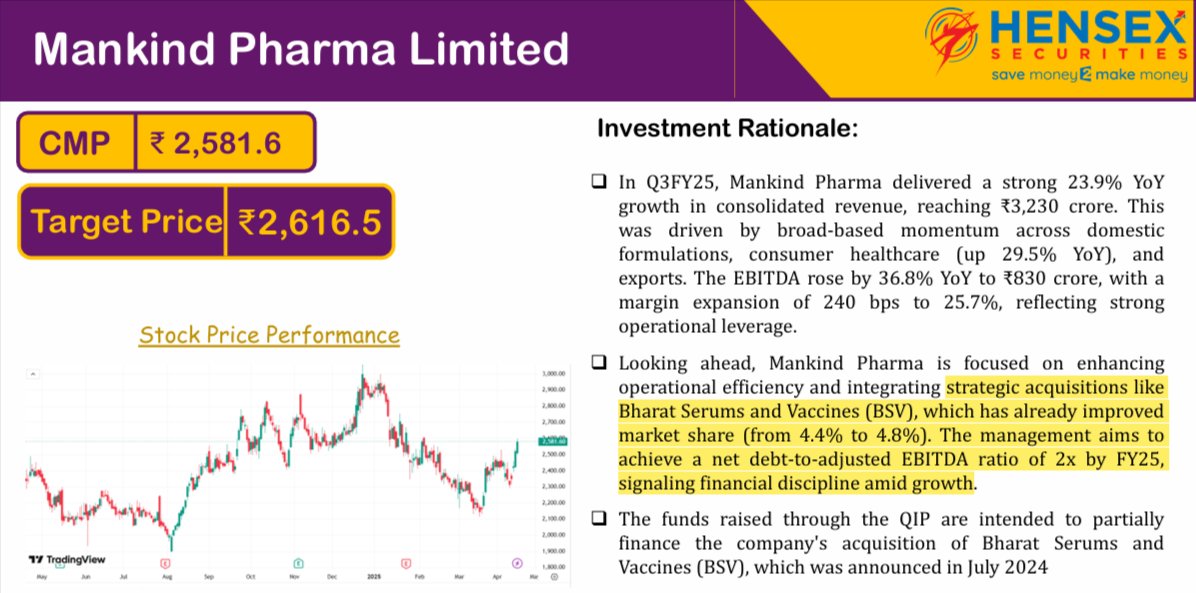

21 Apr 2025

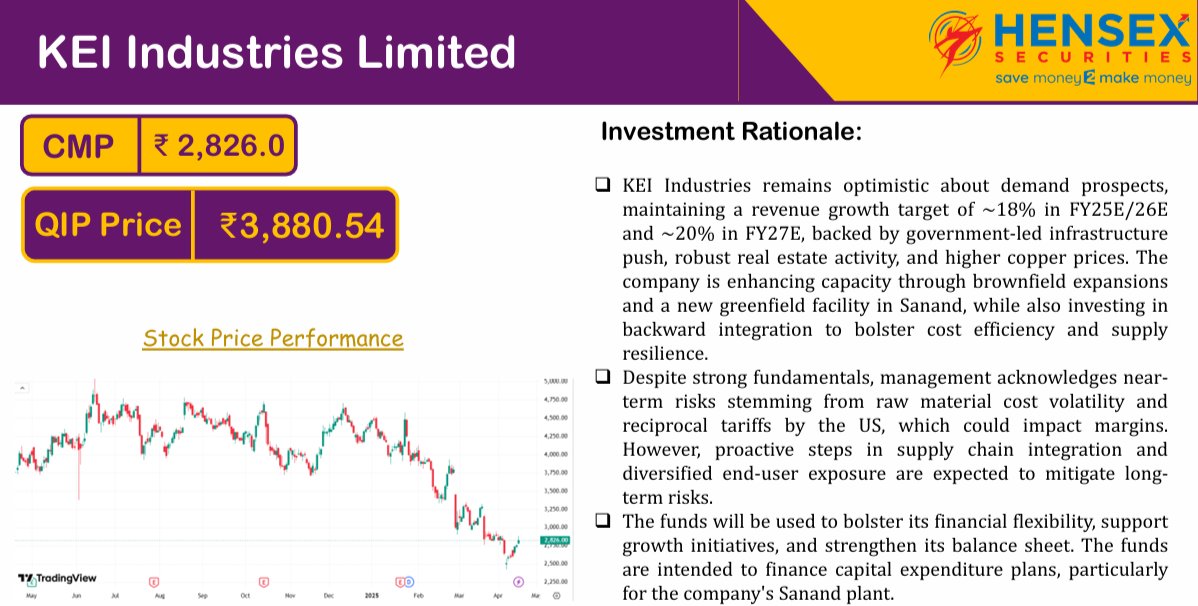

#MankindPharma💊 #KEI

✅ QIP Raised: ₹3,000 Cr | ₹2,000 Cr

✅ QIP Price: ₹2616 | ₹1065

✅ Mankind: BSV acquisition, 36% EBITDA growth

✅ KEI: Infra boom, Sanand plant capex

✅ Focused on efficiency scale

#Pharma #Infra #StockMarketIndia #QIP #stockreport

21 Apr 2025

QIP Frenzy in FY25 By #HensexSecurities

✅ QIPs up 87% YoY (₹1.33L Cr vs ₹71K Cr in FY24)

✅ 85 companies tapped QIPs

✅ Key sectors: #RealEstate, #Utilities, #Auto, #PSUBanks

✅ Big names: #Zomato, #AdaniEnergy, #VarunBeverages

✅ #JMFinancial led with ₹38.7K Cr via 15 deals

3

332

20 Apr 2025

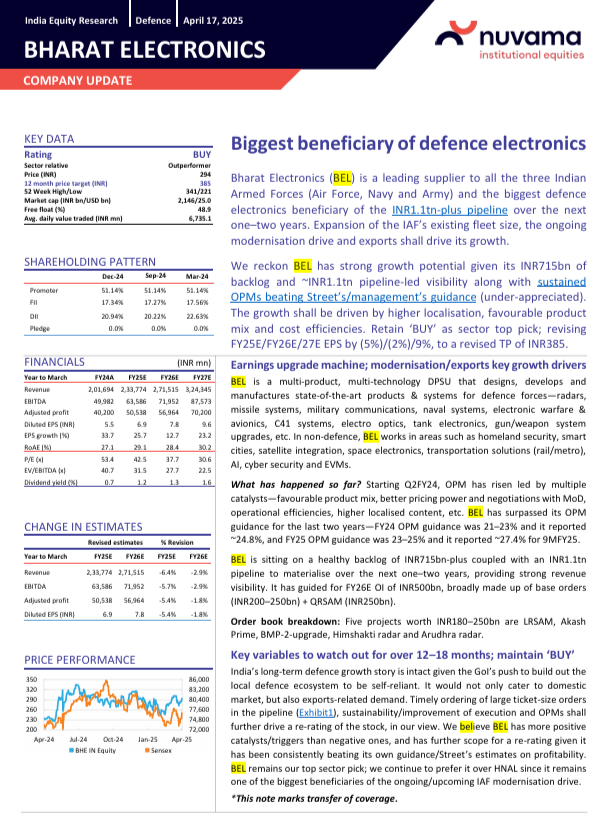

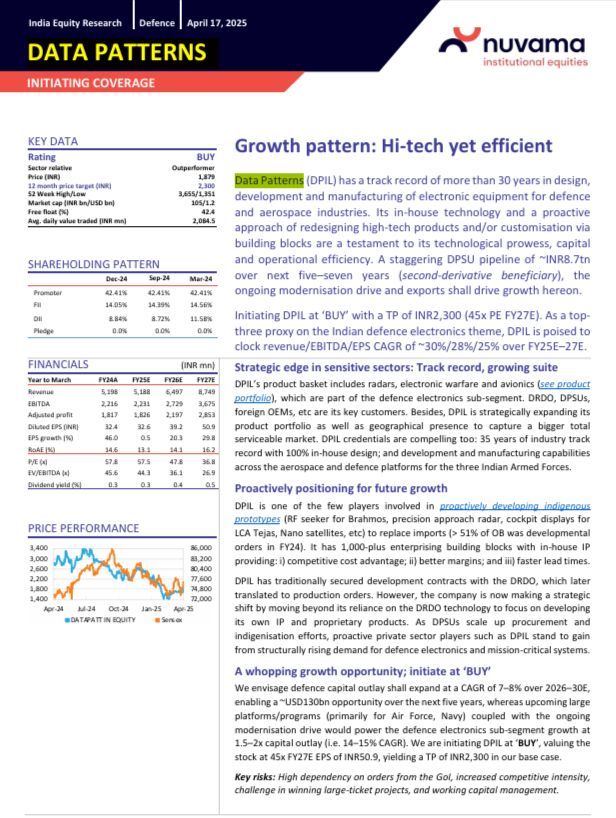

Top Picks 🎯 | #Nuvama #StockReport

#BEL 🛰| TP: ₹385

✔️ Robust execution & cost efficiency

✔️ Higher asset turns, cash conversion & RoE

✔️ ₹1.1L Cr order pipeline

#DataPatterns 📡| TP: ₹2,300

✔️ R&D driven; system integrator journey

✔️ Key play in Defence Electronics segment

20 Apr 2025

#IndiaDefence 💣 | #Nuvama sees a $130bn opportunity by FY30

✅ Defence capex to grow at 7–8% CAGR

✅ FY29 targets: ₹3L Cr production, ₹50,000 Cr exports

✅ Air Force & Navy = bulk of capex (LCA Mk1A, P75I, AMCA, QRSAM)

✅ Private cos to clock 25–40% EPS CAGR vs DPSUs’ 15–18%

1

2

1,671

20 Apr 2025

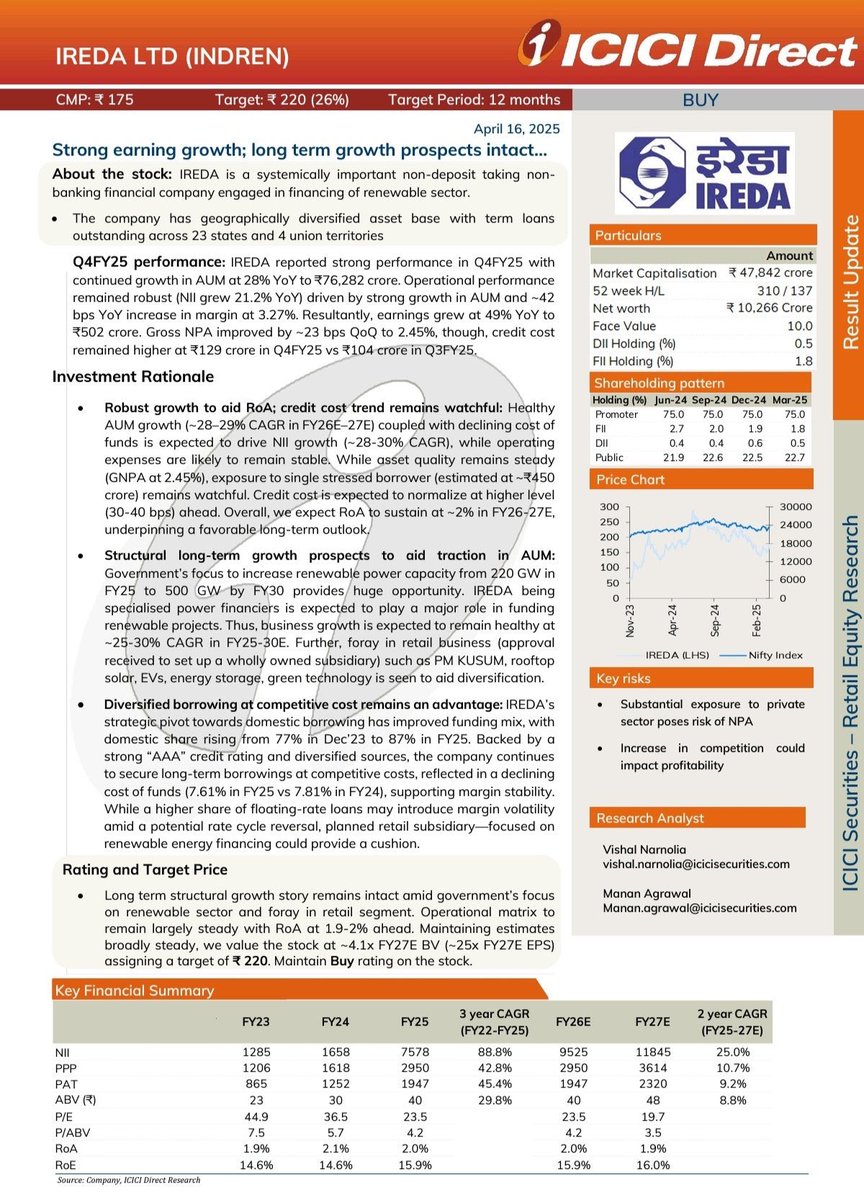

📢 ICICI Direct initiates coverage on IREDA with a BUY rating

CMP: ₹174 | Target: ₹220 | Upside: 26%

📊 ICICI Direct’s Investment Rationale:

▪️ AUM growth estimated at ~28–29% CAGR (FY26–FY27E)

▪️ RoA expected to normalize at ~2%

▪️ Government’s renewable energy push seen aiding loan growth

▪️ Diversified funding mix and AAA rating supporting low-cost borrowings

▪️ Retail expansion through new subsidiary also seen as a growth lever

⸻

📉 Key Risks (as per ICICI Direct):

▪️ Substantial exposure to private sector could impact NPAs

▪️ Rising competition may pressure margins

⸻

🔍 Key Highlights from Q4FY25:

📈 AUM up 28% YoY to ₹76,282 Cr

💰 Earnings up 49% YoY to ₹502 Cr

📉 Gross NPA improved 23 bps QoQ to 2.45%

⚙️ Credit cost steady at ₹129 Cr vs ₹104 Cr QoQ

⸻

📘 Valuation View:

Stock valued at ~4.1x FY27E BV (~25x FY27E EPS).

RoA estimated to remain in the 1.9–2% range in the near term.

⸻

#IREDA #ICICIDirect #StockReport #GreenEnergy #NBFC #MarketUpdate #Renewables #StockCoverage #FinancialResults

✅ follow

@plus_trades

🚀join our free Telegram channel for daily stock updates, breakout ideas, and the latest crypto news!

t.me/plusstocks

1

4

630

21 Mar 2025

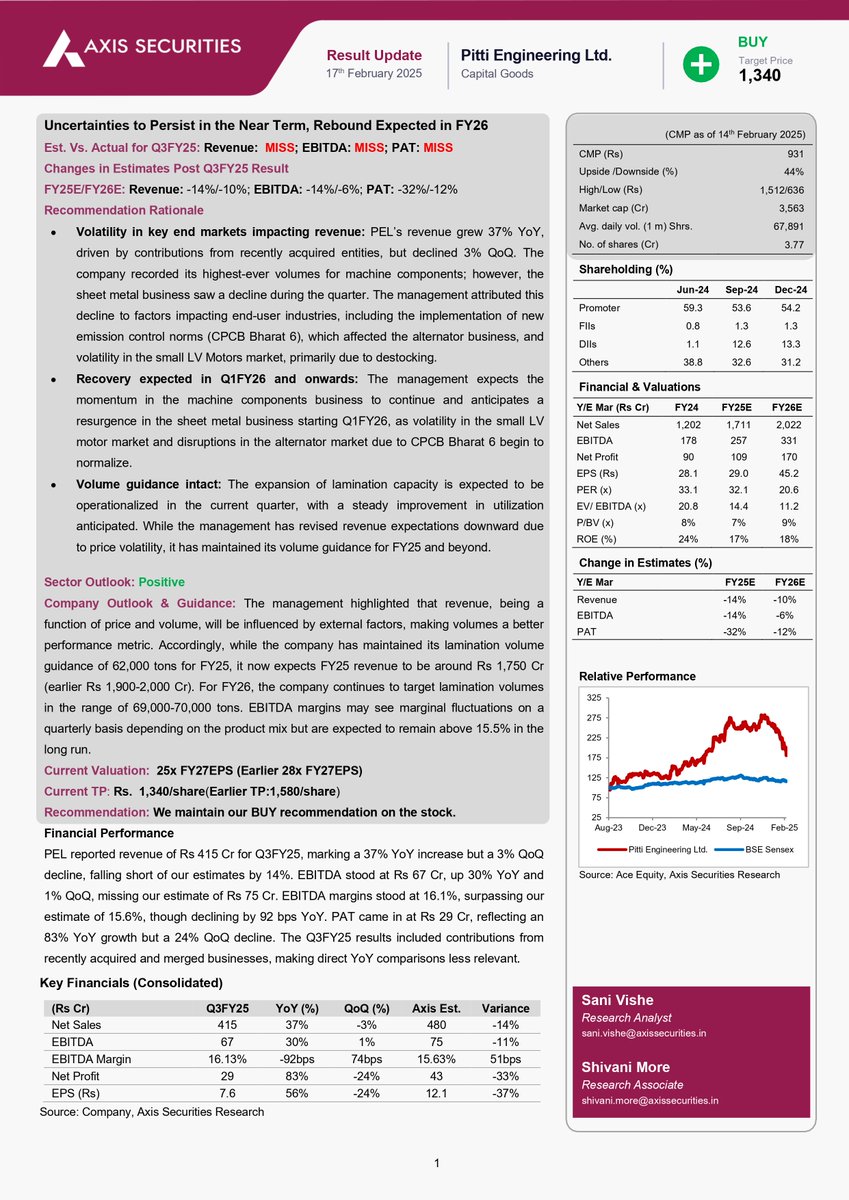

#PittiEngineering ⚙️| Axis Direct TP: ₹1,340

✅ Strong growth in machine components

✅ Sheet metal business to recover from Q1FY26

✅ Volume guidance: 62,000T (FY25) & 69,000-70,000T (FY26)

✅ 30% upside potential | Valuation at 25x FY27 EPS

#StockReport #Investing #StocksToBuy

6 Mar 2025

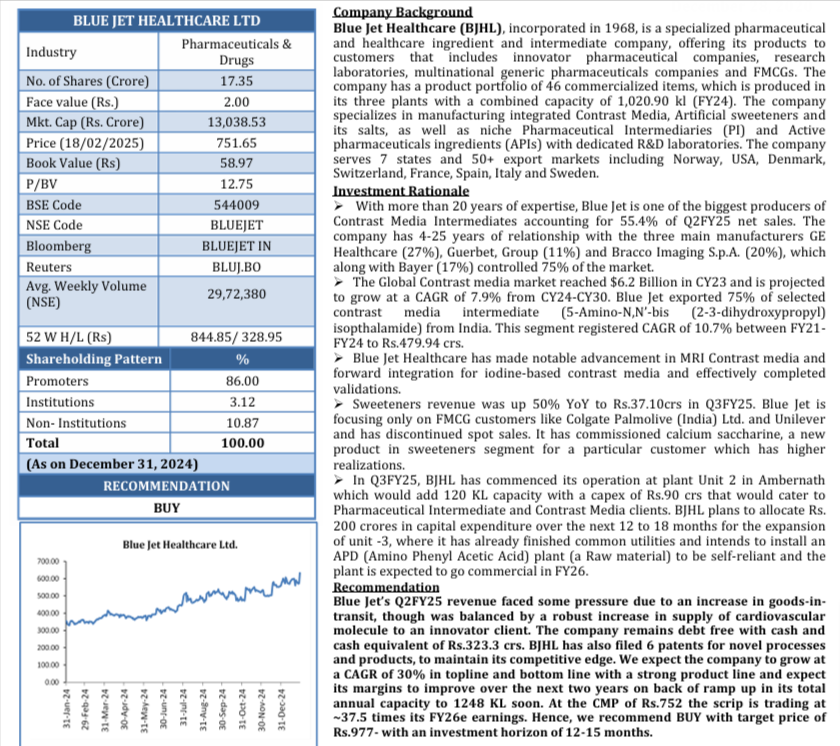

#BlueJetHealthcare 💉 | AUM Capital TP: ₹977

✅Leader in Contrast Media Intermediates

✅Strong clients: GE, Bayer, Guerbet, Bracco

✅Market growth: $6.2B (CY23) → 7.9% CAGR (CY24-30)

✅Sweeteners biz up 50% YoY

✅ ₹200Cr capex | Debt-free | 30% CAGR growth

#CDMO #stockreport

6

1,498

6 Mar 2025

#BlueJetHealthcare 💉 | AUM Capital TP: ₹977

✅Leader in Contrast Media Intermediates

✅Strong clients: GE, Bayer, Guerbet, Bracco

✅Market growth: $6.2B (CY23) → 7.9% CAGR (CY24-30)

✅Sweeteners biz up 50% YoY

✅ ₹200Cr capex | Debt-free | 30% CAGR growth

#CDMO #stockreport

1

7

1,194