3 Dec 2025

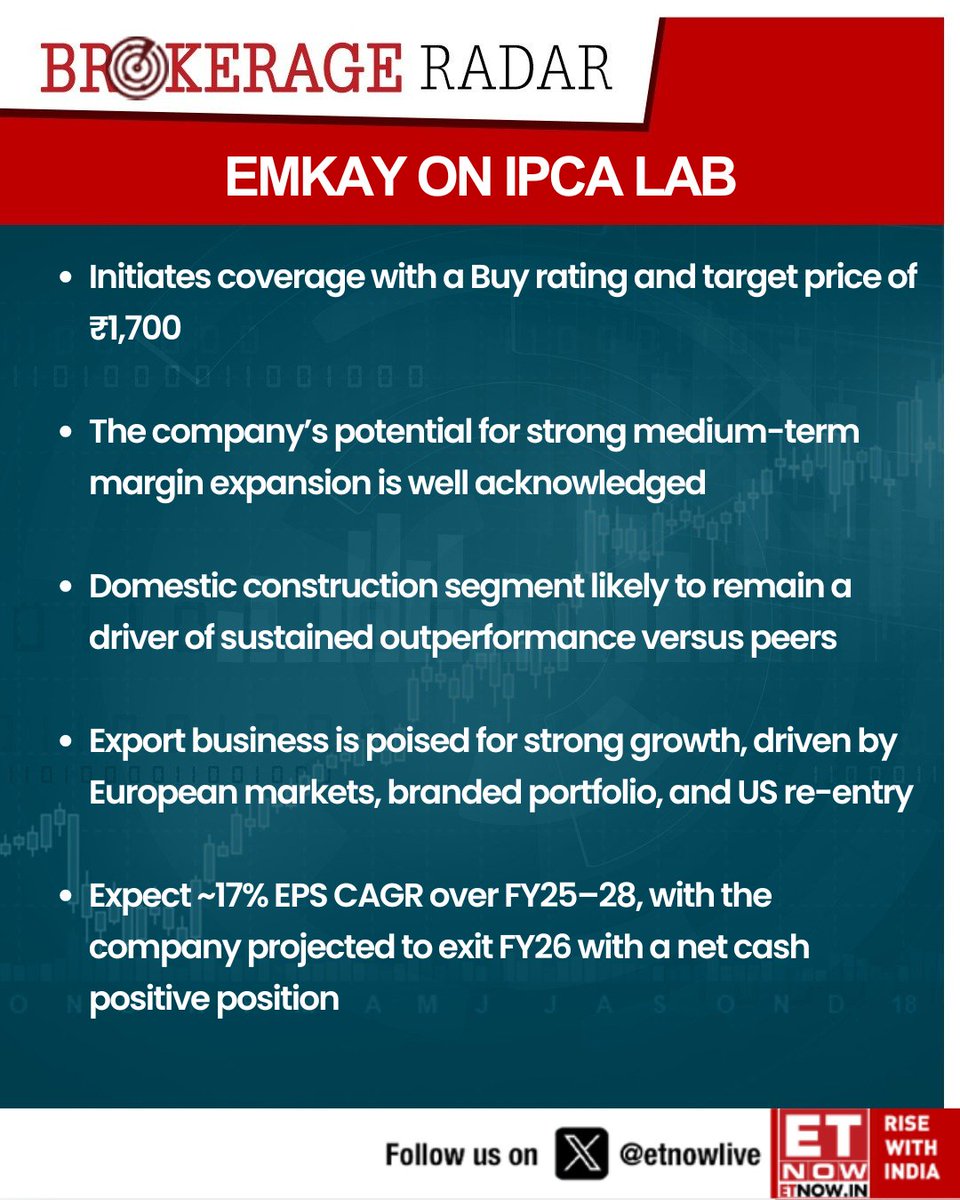

#BrokerageRadar | Emkay on IPCA LaB: Initiates coverage with a Buy rating and target price of ₹1,700

@EmkayGlobal #EquityResearch #StockCoverage #TargetPrice #InvestmentIdeas #EPSGrowth

2

13

2,147

5 Jun 2025

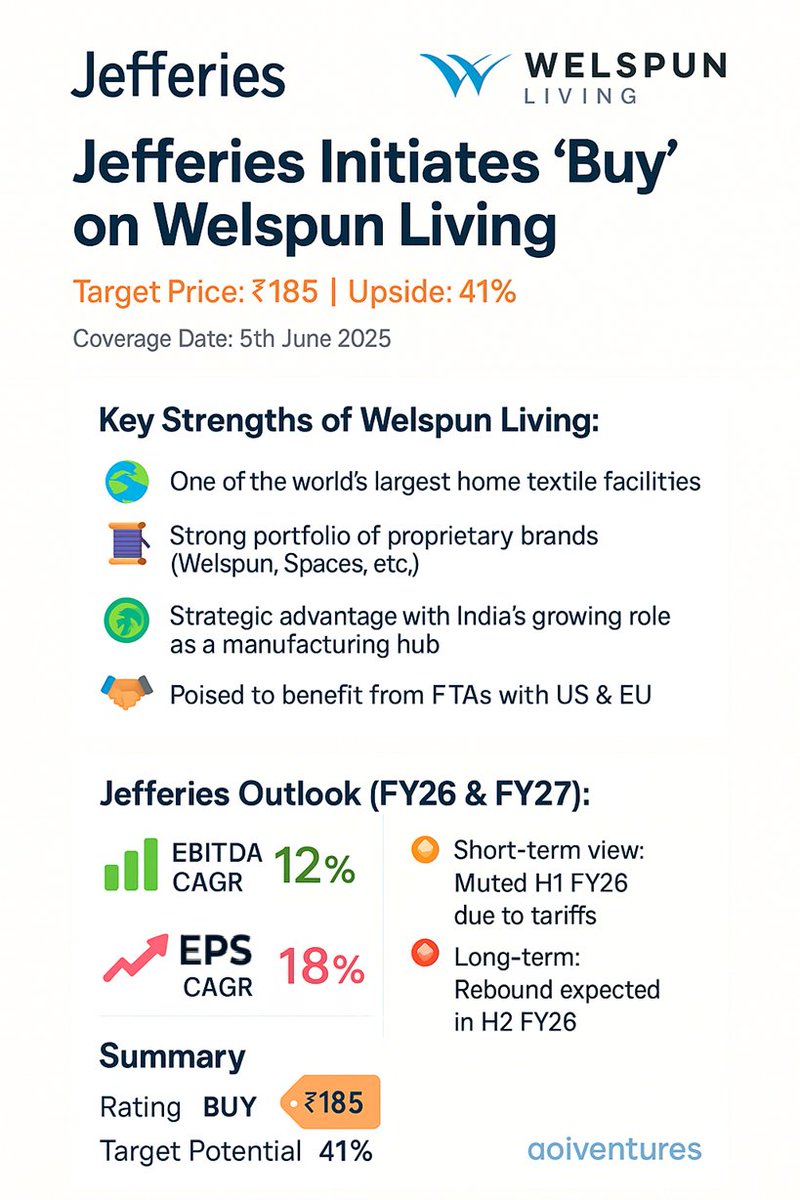

📢 Jefferies Initiates ‘Buy’ on Welspun Living; Sees 41% Upside

#WelspunLiving #Jefferies #StockCoverage #Textiles #Exports #WELSPUNLIV

1

1

4

1,380

20 Apr 2025

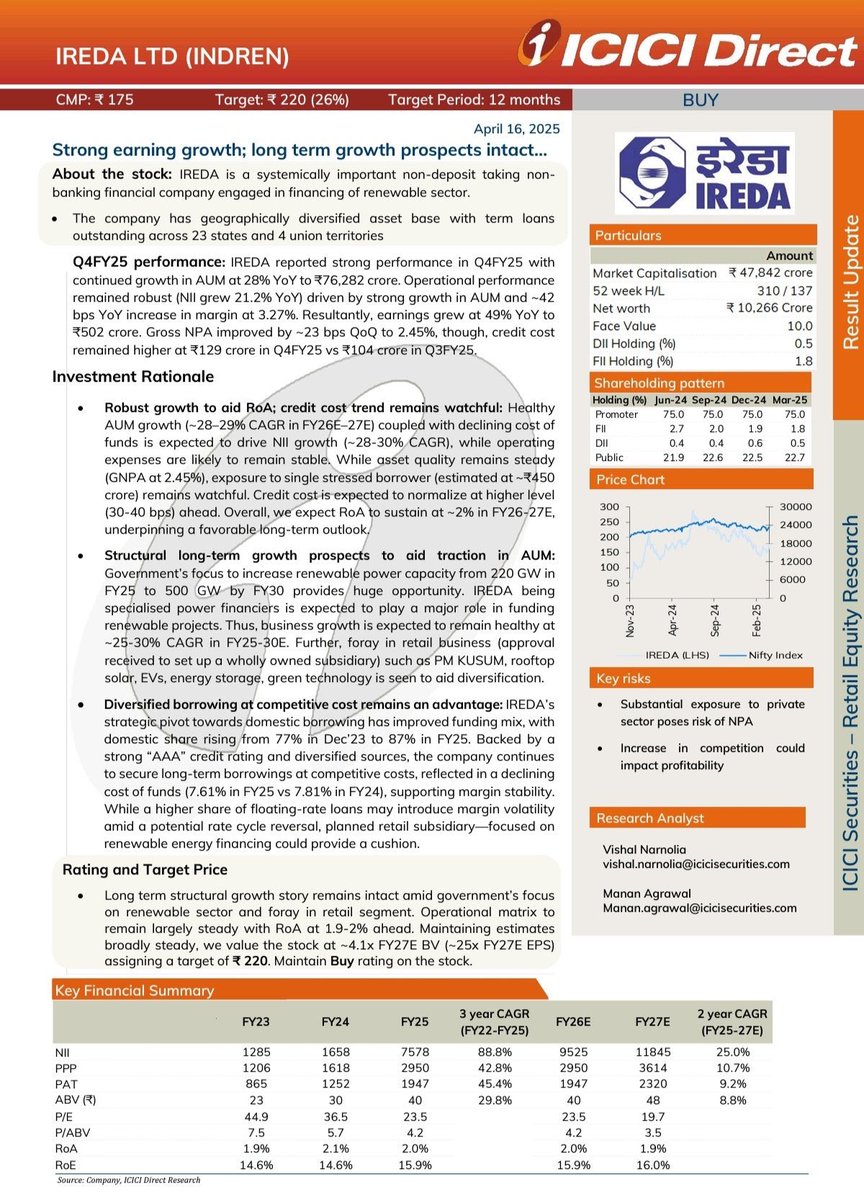

📢 ICICI Direct initiates coverage on IREDA with a BUY rating

CMP: ₹174 | Target: ₹220 | Upside: 26%

📊 ICICI Direct’s Investment Rationale:

▪️ AUM growth estimated at ~28–29% CAGR (FY26–FY27E)

▪️ RoA expected to normalize at ~2%

▪️ Government’s renewable energy push seen aiding loan growth

▪️ Diversified funding mix and AAA rating supporting low-cost borrowings

▪️ Retail expansion through new subsidiary also seen as a growth lever

⸻

📉 Key Risks (as per ICICI Direct):

▪️ Substantial exposure to private sector could impact NPAs

▪️ Rising competition may pressure margins

⸻

🔍 Key Highlights from Q4FY25:

📈 AUM up 28% YoY to ₹76,282 Cr

💰 Earnings up 49% YoY to ₹502 Cr

📉 Gross NPA improved 23 bps QoQ to 2.45%

⚙️ Credit cost steady at ₹129 Cr vs ₹104 Cr QoQ

⸻

📘 Valuation View:

Stock valued at ~4.1x FY27E BV (~25x FY27E EPS).

RoA estimated to remain in the 1.9–2% range in the near term.

⸻

#IREDA #ICICIDirect #StockReport #GreenEnergy #NBFC #MarketUpdate #Renewables #StockCoverage #FinancialResults

✅ follow

@plus_trades

🚀join our free Telegram channel for daily stock updates, breakout ideas, and the latest crypto news!

t.me/plusstocks

1

4

630

4 Oct 2024

Bajaj Housing Finance: HSBC initiates coverage with a "Reduce" rating and sets a target price of ₹110/share.

🔹HSBC's target reflects a cautious outlook with a 27% downside potential from CMP

#BajajHousingFinance #HSBC #StockCoverage #TargetPrice #MarketUpdate

4

649

1 Oct 2024

4️⃣ straight months of new broker research coverage initiations!

Recent reports:

📊 Roth Capital – June

📊 Scotiabank – July

📊 National Bank – August

📊 CIBC – September

We now have 1️⃣2️⃣ brokerages providing independent research coverage of Denison, and all 1️⃣2️⃣ have given us “Buy,” “Sector Outperform,” or similar ratings! 👏

#DenisonMines #StockCoverage #Research #MiningIndustry #Uranium

16

69

6,297

IMV (#Nasdaq & #TSX) announced today that a 7th research #analyst has picked up coverage of its stock, namely Dr. Jim Birchenough @WellsFargo Securities.

According to @TipRanks , Jim is currently ranked 273 of 12,573 overall experts. Jim's #StockCoverage: bit.ly/2NfeXgk

2

2