Your outdoor patio deserves to be loved all summer long. No more waiting for the "perfect day", make it every day! Rain or shine!

#motorizedshades #homeimprovement #suncontrol #outdoorliving #outdoorscreen #backyardgoals

2

Let the view shine through while keeping the heat out

#SunscreenRollerBlinds #OfficeBlinds #WindowPlusEA #SunControl #ModernOffice

5

Mar 1

Hi @volklub,

Can you guide if PPF is a must? Have a Hycross exclusive edition., got suncontrol, dashcam,7d matt done. Xpel PPF is 1.7-2lacs. Is that normal or needed? Painting is easier 5-7yrs down. I have open parking.

1

4

3,139

10 Sep 2025

#GRWRHITECH Garware Hi-Tech Films Ltd. (GHTFL) – Q1 FY26 Concall (Aug 2025) highlights:

---

Revenue/Geo Mix (Q1 FY26)

•Exports: 72.5% of total revenue

•Domestic: 27.5%

•Geography split:

o US: ~45%

o Europe: ~12-13%

o Middle East: ~3-5% (fastest growing)

o Asia ex-India: ~12-13%

o India: ~23.5-27.5%

Segmental Insights

•SunControl Films: Revenue down ~7% YoY (monsoon disruption, auto slowdown, US tariffs).

•Paint Protection Films (PPF): ~28% YoY growth, strong in North America, Middle East, and India (via Garware Application Studios).

•Industrial Products Division (IPD): Revenue down ~3% YoY; shrink films fell 29% (beverages US tariffs).

---

Capacity Position

o PPF line expansion new TPU plant underway.

o Studios: 250 operational, targeting 300 by Mar 2026.

o High utilization in PPF and SunControl; volumes can be shifted to Middle East/Europe if US tariffs worsen (though smaller markets).

---

Future Guidance / Outlook

•Guidance withdrawn (earlier INR 2,500 Cr revenue FY26 target now suspended due to tariff uncertainty).

•Tariff impact outlook:

o Manageable up to ~16%.

o Latest 25% tariff hike described as “very difficult”; if tariffs hit ~50%, profitability and market share in US will be severely challenged.

•Growth priorities:

o Middle East (esp. Saudi Arabia; targeting 30-40% growth in FY26).

o Europe (~20% growth expected).

o India PPF expansion via franchise studio model.

•Strategic initiatives:

o Cost reduction, supply chain re-negotiation, selective price hikes.

o Ongoing capex in new TPU plant second PPF line.

o Brand/channel expansion in Europe, Middle East, and India.

•Management stance: Cautiously optimistic, but near-term highly dependent on US-India tariff developments.

---

10 Sep 2025

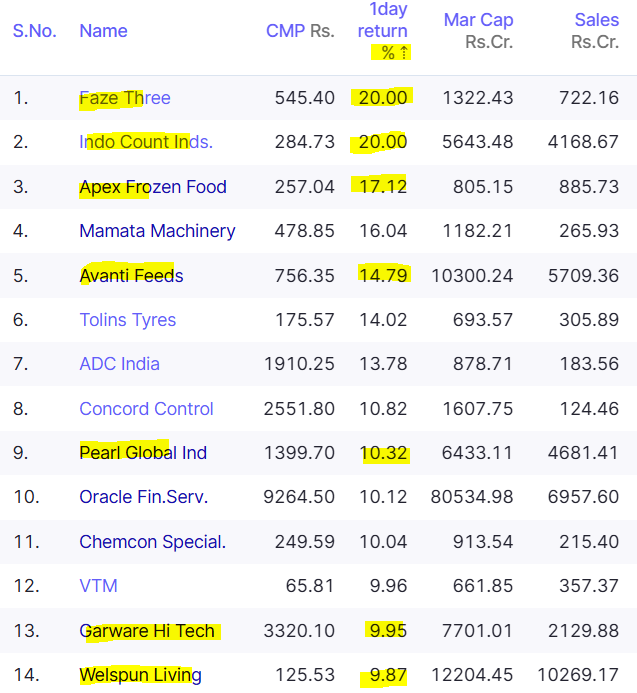

All export theme stocks done very well today:

Faze Three 20%

Indo Count Inds 20%

Apex Frozen Food 17%

Avanti Feeds 15%

Pearl Global Ind 10%

Garware Hi Tech 10%

Welspun Living 10%

GHCL Textiles 10%

Vardhman Textiles 8%

Pokarna 7%

IGIL 7%

#exports #tariffs #trump

3

339

10 Sep 2025

🚨 Garware Hi-Tech Films Q1 FY26

📊 Revenue ₹495 Cr

( 4.3% YoY; missed ₹550 Cr est. due to tariffs & early monsoon)

💰 PAT ₹83 Cr (vs ₹88 Cr YoY)

📉 EBITDA ₹123 Cr; margin 24.8% (vs 27.4%)

✅ Debt-free, ₹700 Cr cash

🌍 Segment performance:

🚗 PPF 28% YoY

(domestic exports; 20–23% share in India, expanding via 250 studios → target 300 by FY26)

☀️ SunControl Films -7% YoY

(auto slowdown, weak demand in developed mkts)

📦 Shrink Films -29% YoY

(early rains, beverage demand hit)

🏭 Industrial Products -3% YoY

🌐 Geographies:

US ~45% revenue; facing tariff hikes

(6.25% → 16.25% → 25%)

India 27.5% revenue

Europe ~12–13% (growing ~20%)

Middle East ~3–5% (growing 30–40%)

Asia ex-India ~12–13% (Japan negligible)

Exports = 72.5% of revenue

⚠️ Risks:

Tariffs may cut ₹100 Cr from bottom line (absorbed so far via supply chain & cost efficiencies)

Seasonal demand disruptions (early monsoon)

📈 Growth drivers:

2nd PPF line & new TPU plant coming up

Premium PPF & SunControl range via franchisee studios

(10–15% higher margins)

Strong global presence & brand loyalty

(esp. in auto aftermarket & architectural films)

🌟Management outlook:

FY26 will be tough (tariffs, geopolitics),

Diversification New Capacity Middle East/Europe growth should offset,

1

6

551

13 Aug 2025

CON CALL

Q1 FY26 GARWARE HITECH FILMS

•Macro: Early monsoon & US tariff hikes (6.25%→16.25%→31.25% 25% announced) hit demand.

•Financials: Revenue ₹495 Cr ( 4% YoY), EBITDA ₹123 Cr (−5%), PAT ₹83 Cr (−6%). Debt-free, ₹700 Cr cash.

•Segments:

•SunControl: −7% YoY; tariff impact limited to ₹3–4 Cr in Q1.

•PPF: 28% YoY; 250 Garware Studios, targeting 300 by Mar’26, higher margins.

•IPD: −3% YoY; shrink films −29%.

•Geography: US 45% (tariff headwinds), Europe 20% growth expected, ME fastest-growing (30–40%).

•Guidance:

FY26 revenue target withdrawn due to tariff uncertainty.

•Capex:

2nd PPF line, new TPU plant underway.

Very Well Curated by @Dixitagg

3

7

78

8,035

8 Aug 2025

Garware Hi-Tech Films: Strong Growth & Strategic Expansion 🚀 | MCap 7,364.2 Cr

- Revenue from operations for Q1 FY26: ₹495 Cr.

- Cash surplus as of June 30, 2025: ₹704 Cr, with zero net debt.

- Revenue growth: ₹874 Cr (FY17) to ₹2,109 Cr (FY25).

- EBITDA margin improved from 9.0% (FY17) to 23.5% (FY25).

- PAT margin increased from 2.5% (FY17) to 15.7% (FY25).

- Diversified portfolio: 3,000 SKUs, 85% value-added products in Q1 FY26.

- Investing in new PPF production lines & TPU facilities for future growth.

- Market leader in SunControl Films (SCF) & Paint Protection Films (PPF), backed by proprietary tech & R&D.

- Expanded Garware Application Studios (GAS) network to 300 touchpoints, targeting 250 more.

- ESG initiatives: GreenPro certification, 30% PCR usage, community programs.

- Navigating tariff & geopolitical challenges with cost optimization & strategic adaptations.

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 18 pages)

1

1

564

15 May 2025

Garware Hi-Tech Films' shift to value-added products like SunControl and Shrink Films is a textbook example of strategic differentiation in a commodity market

1

9

640

14 May 2025

🚀 Garware Hi-Tech Films Hits Record ₹2,000 Cr Revenue in FY25 – Key Growth & Sustainability Wins | MCap 8,282.35 Cr

- Record annual revenue exceeding ₹2,000 crore in FY25.

- Highest-ever yearly profit at ₹331.2 crores (PAT).

- Value-added products (VAP) contributed 87% to FY25 revenue, led by SunControl Films, Paint Protection Film (PPF), and Shrink Film.

- New PPF production line (300 LSF) to be operational by Q2 FY26.

- TPU Extrusion Line (360 LSF) to be operational by Q2 FY27.

- Expansion of Garware Application Studios (GAS) and PPF distributors to 200 across Tier 1 & Tier 2 cities in India.

- Industrial products division holds ~70% market share in India's shrink film market.

- Digital marketing success: 50,000 LinkedIn followers and 200 million digital impressions.

- Sustainability initiatives: zero liquid discharge, 100% water recycling, and 30% PCR materials in shrink films.

- Architectural films growth with new launches like SpectraPro and DecoVista series.

- PPF business expansion in India, supported by applicator training programs.

- Over 10 registered/pending patents and 168 trademarks globally.

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 44 pages)

2

190

14 May 2025

🚨 GARWARE HI-TECH FILMS (GRWRHITECH) RELEASES FY25 & Q4 RESULTS – STRONG PERFORMANCE, STRATEGIC GROWTH, AND ROBUST FINANCIALS!

■ FY25 REVENUE FROM OPERATIONS STOOD AT ₹2,109.4 CR, MARKING A 25.8% YOY SURGE, WHILE EBITDA ROSE BY 54.3% TO ₹495.5 CR.

■ PAT JUMPED TO ₹331.2 CR (UP 62.9% YOY) AND PBT TO ₹445.5 CR (UP 64.8% YOY), SHOWCASING STRONG PROFITABILITY.

■ Q4 FY25 PERFORMANCE WAS EQUALLY IMPRESSIVE WITH ₹547.9 CR IN REVENUE (UP 22.7% YOY) AND ₹121.4 CR IN EBITDA (UP 35.3% YOY).

■ PAT FOR THE QUARTER CAME IN AT ₹77.8 CR AND PBT AT ₹108.8 CR, INDICATING STABLE QUARTERLY GROWTH.

■ KEY STRATEGIC INITIATIVES INCLUDE NEW INVESTMENTS IN TPU & PPF LINES, TECHNICAL CAPABILITY ENHANCEMENT, AND MARKET EXPANSION.

■ PRODUCT LINE STRENGTH CONTINUES WITH SUNCONTROL FILMS, PAINT PROTECTION FILMS, AND INDUSTRIAL PRODUCTS DRIVING GROWTH.

■ RECENT DEVELOPMENTS INCLUDE GREENPRO CERTIFICATION, USA D2C E-PORTAL LAUNCH, GARWARE HOME SOLUTIONS EXPANSION, AND DIGITAL OUTREACH.

■ COMPANY MAINTAINS A HEALTHY BALANCE SHEET WITH ₹650 CR CASH SURPLUS AS OF MARCH 31, 2025.

■ MANUFACTURING BASE EXPANDS WITH TWO EXISTING LOCATIONS AND UPCOMING PRODUCTION LINES TO SUPPORT FUTURE GROWTH.

#GRWRHITECH #GARWARE #RESULTS #Q4FY25 #INVESTING #EARNINGS #STOCKMARKET #AUTOMOTIVE #PPF #TPU #SUNCONTROL #MADEININDIA #GREENBUILDING #FINANCIALS

1

2

173

14 May 2025

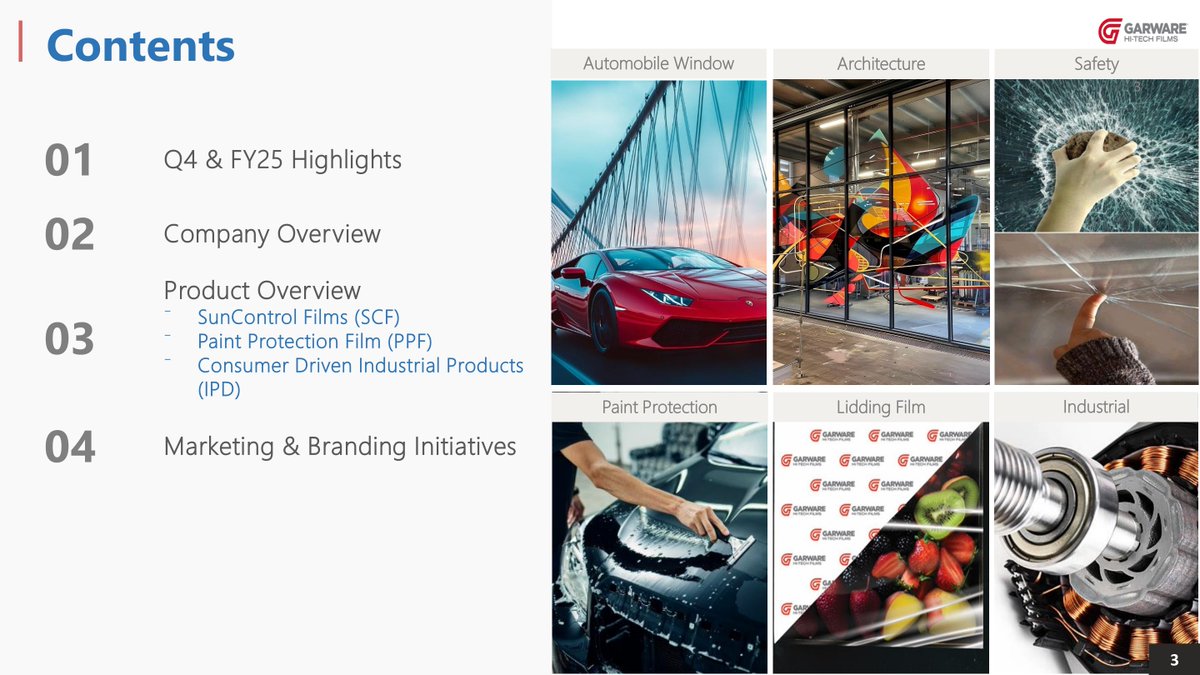

Garware Hi-Tech Films (GRWRHITECH) released its Investor Presentation for the Audited Financial Results for the Quarter and Year Ended March 31, 2025.

Key Highlights:

- 𝗙𝗬𝟮𝟱 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

▪ Revenue from Operations: ₹2,109.4 Cr, a 25.8% YoY increase. 🚀

▪ EBITDA: ₹495.5 Cr, a 54.3% YoY increase.

▪ PAT: ₹331.2 Cr, a 62.9% YoY increase. 💰

▪ PBT: ₹445.5 Cr, a 64.8% YoY increase.

- 𝗤𝟰 𝗙𝗬𝟮𝟱 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

▪ Revenue from Operations: ₹547.9 Cr, a 22.7% YoY increase.

▪ EBITDA: ₹121.4 Cr, a 35.3% YoY increase.

▪ PAT: ₹77.8 Cr, a 34.6% YoY increase.

▪ PBT: ₹108.8 Cr, a 39.4% YoY increase.

- 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝗶𝘁𝗶𝗮𝘁𝗶𝘃𝗲𝘀:

▪ Investments in TPU extrusion line and upcoming PPF line. 🏭

▪ Focus on strengthening technical capabilities and broadening product portfolio.

▪ Expansion into new markets.

- 𝗣𝗿𝗼𝗱𝘂𝗰𝘁 𝗢𝘃𝗲𝗿𝘃𝗶𝗲𝘄:

▪ SunControl Films (SCF)

▪ Paint Protection Film (PPF)

▪ Consumer Driven Industrial Products (IPD)

- 𝗥𝗲𝗰𝗲𝗻𝘁 𝗗𝗲𝘃𝗲𝗹𝗼𝗽𝗺𝗲𝗻𝘁𝘀:

▪ GreenPro Certification by CII & IGBC.

▪ Launched E-Portal for D2C PPF Sales for USA market.

▪ Expansion with 'Garware Home Solutions'.

▪ Continuous PPF network expansion.

▪ GHFL presence at Expos & Forums.

▪ Digital Marketing with significant engagement.

- 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗲𝗮𝗹𝘁𝗵:

▪ ₹650 Cr cash surplus as of March 31, 2025.

- 𝗠𝗮𝗻𝘂𝗳𝗮𝗰𝘁𝘂𝗿𝗶𝗻𝗴:

▪ Two manufacturing locations.

▪ Upcoming PPF and TPU Extrusion lines to drive growth.

📊 GARWARE HI-TECH FILMS LTD | 🏷️ Investor Presentation

🌐 Details: wegro.app/EqlRwN

⚡️AI-driven WhatsApp updates - Try FREE 👉 wegro.app/go

1

4

304

30 Jan 2025

Design with Light & Shadow: The Future of Architectural Sun Control 🌞

📩 Let's discuss your next project! Learn more at: vivarailings.com/products/su…

#Architecture #SunControl #ShadeStructures #SustainableDesign #ArchitecturalInnovation #VIVARailings

4

54

12 Nov 2024

Transform your high-ceilinged spaces with Marvel Roman Blinds - crafted for elegance and superior sun control. These heighted Roman Blinds enhance room architecture while adding a sophisticated touch.

#MarvelRomanBlinds #HighCeilingDecor #ElegantInteriors #SunControl #Luxury

2

22

13 Sep 2024

The term ‘nail-on’ in construction started with nails securing windows, but now it refers to using screws for a more durable attachment. This concept is also applied to modern sunshade installations! #ad #BOKModern #sunshade #suncontrol

architecturalrecord.com/arti…

1

939

29 Jul 2024

M-SCREEN ULTIMETAL® high-performance #RollerBlind fabric rejects up to 90% of solar energy - metallic side provides excellent visible transmission ow.ly/ATFs50Smiij #SolarProtection #WindowTreatments #SunControl

1

8

1,483

25 Apr 2024

Die gibt es bereits nicht mehr…

Pro-emit LED DIY-M-KIT COB SMD 300W

Dazu noch FarRed u uv-a Kit inkl suncontrol (für Steuerung ü App) hab zusätzlich aber noch 4 kleine boards a 36w m 5000k für Blüte xtra

1

5

111

27 Mar 2024

Suncontrol 😎🤝 🌱 noch jemand?

Gefühlt hab nur ick das Teil 😅

4

11

1,011

1 Mar 2024

Ja das stimmt. Nach und nach trudelt das Zeug erst ein. Bei grow technology oder grow Guru ist das in Deutschland gelistet.

Habe erstmal das Zelt die Autobewässerungsuntersetzter und den Controller.

Der Kleine Venti kommt im März mit der Version 2.

Xt308 mit Suncontrol bleibt.

1

3

80