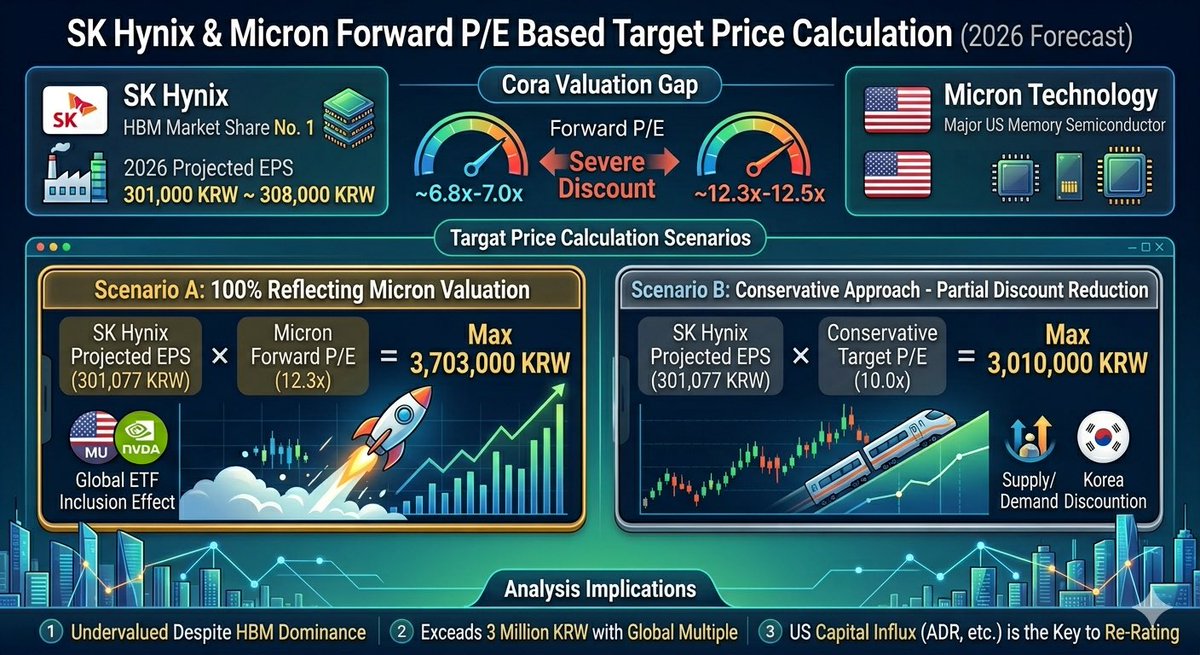

[Stock Analysis] The Paradox of HBM Leadership: Using Micron's Valuation Standard, SK Hynix Targets the 3 Million KRW Milestone

SK Hynix, the undisputed leader in the High Bandwidth Memory (HBM) market, is facing a severe valuation gap in the global market. According to financial industry analysts, SK Hynix’s 2026 forecast-based Forward Price-to-Earnings Ratio (PER) sits at a mere 6.8x. In stark contrast, Micron Technology, a U.S. competitor that trails in both market share and technological edge, trades at a Forward PER of 12.3x—nearly double the valuation of SK Hynix.

If we strip away the local market premium and apply a global peer-group valuation method to re-evaluate SK Hynix, the stock shows massive upside potential. If we apply Micron’s multiple (12.3x) to SK Hynix’s 2026 consensus Earnings Per Share (EPS) of approximately 301,000 KRW, **the mathematically derived target price reaches up to 3.7 million KRW.**

Even under a conservative scenario, accounting for domestic liquidity constraints and market timing differences by applying only 80% of Micron’s multiple (a 10x PER), **the target price easily breaks the 3 million KRW mark.** Given the fundamental performance, where the company is hitting record highs while virtually monopolizing the HBM market, the current stock price appears significantly disconnected from its true value.

Experts point to the "depth of capital supply" as the root cause of this extreme discount. Micron enjoys the structural advantage of automatically absorbing passive capital from major U.S. indices and massive semiconductor ETFs, such as the S&P 500 and the Philadelphia Semiconductor Index. Therefore, if SK Hynix can diversify its capital structure and successfully attract long-term U.S. institutional funds—possibly through strategies like ADR issuance or global index inclusion—it could rapidly close the valuation gap with Micron and achieve a significant stock re-rating.

#SKHynix #Micron #ForwardPER #TargetPrice #HBM #Valuation #ReRating #KoreaDiscount #Semiconductor #MarketAnalysis

10

137

Jun 12

//@version=6

strategy(

title="USTEC NY AM FV No Max Trades No Wait BOS 3 Candles",

overlay=true,

max_labels_count=500,

max_lines_count=500,

pyramiding=0,

process_orders_on_close=true,

initial_capital=100000,

currency=currency.USD,

default_qty_type=strategy.fixed,

default_qty_value=0.1,

margin_long=1,

margin_short=1

)

// =====================

// INPUTS

// =====================

tz = input.string("America/New_York", "Timezone")

// NY AM ONLY

nyOpenHour = input.int(9, "NY AM Open Hour", minval=0, maxval=23)

nyOpenMinute = input.int(30, "NY AM Open Minute", minval=0, maxval=59)

// No first 3-minute wait.

// Strategy can trade from 9:30 onward.

continuationEnd = input.int(10, "Continuation Ends After Minutes", minval=1)

// 9:30 to 11:00 = 90 minutes

sessionEndMinutes = input.int(90, "Stop Trading After Minutes", minval=10)

closeAtSessionEnd = input.bool(true, "Close Open Trade At 11:00 NY Time")

// BOS fixed to last 3 candles

bosLookback = 3

maxCounterWick = input.float(0.20, "Max Counter Wick %", minval=0.01, maxval=0.50, step=0.01)

minBodyPercent = input.float(0.50, "Minimum Body %", minval=0.10, maxval=1.00, step=0.05)

atrLength = input.int(14, "ATR Length")

// ATR FILTER

useMinATR = input.bool(true, "Do Not Trade If ATR Is Below Minimum")

minATRToTrade = input.float(8.0, "Minimum ATR To Trade", minval=0.0, step=0.5)

// RISK MODEL

riskReward = input.float(2.0, "Take Profit R Multiple", minval=0.5, step=0.1)

requireRoomToFairValue = input.bool(false, "Reversion Requires Room To Fair Value")

qty = input.float(0.1, "Position Size", minval=0.01, step=0.01)

showLabels = input.bool(true, "Show Buy/Sell Labels")

showSLTP = input.bool(true, "Show Entry / SL / TP Lines")

showSessionLabels = input.bool(true, "Show NY AM Open Label")

lineLength = input.int(25, "Line Length", minval=5, maxval=100)

buyLabelOffset = input.int(1, "Buy Label Offset Right", minval=0, maxval=20)

sellLabelOffset = input.int(1, "Sell Label Offset Left", minval=0, maxval=20)

// =====================

// TIME LOGIC

// =====================

h = hour(time, tz)

m = minute(time, tz)

// Only reset at NY AM 9:30

isNYAMOpen = h == nyOpenHour and m == nyOpenMinute

newSession = isNYAMOpen

// =====================

// SESSION STATE

// =====================

var float fairValue = na

var int sessionStartBar = na

var int openingDirection = 0

if newSession

fairValue := open

sessionStartBar := bar_index

openingDirection := close >= open ? 1 : -1

if showSessionLabels

label.new(

x=bar_index,

y=open,

text="NY AM FV RESET\n09:30 Open: " str.tostring(open, format.mintick),

xloc=xloc.bar_index,

style=label.style_label_down,

color=color.yellow,

textcolor=color.black

)

barsFromOpen = not na(sessionStartBar) ? bar_index - sessionStartBar : na

// NY AM trading window: 9:30 to 11:00

inTradingWindow = not na(barsFromOpen) and barsFromOpen >= 0 and barsFromOpen <= sessionEndMinutes

inContinuationWindow = inTradingWindow and barsFromOpen <= continuationEnd

inReversionWindow = inTradingWindow and barsFromOpen > continuationEnd

sessionExpired = not na(barsFromOpen) and barsFromOpen > sessionEndMinutes

// =====================

// CANDLE STRENGTH / DISPLACEMENT

// =====================

candleRange = high - low

body = math.abs(close - open)

bodyPercent = candleRange > 0 ? body / candleRange : 0.0

bullCounterWick = candleRange > 0 ? (high - close) / candleRange : 1.0

bearCounterWick = candleRange > 0 ? (close - low) / candleRange : 1.0

bullDisplacement = close > open and bullCounterWick <= maxCounterWick and bodyPercent >= minBodyPercent

bearDisplacement = close < open and bearCounterWick <= maxCounterWick and bodyPercent >= minBodyPercent

// =====================

// BREAK OF STRUCTURE — ONLY LAST 3 CANDLES

// =====================

priorHigh = ta.highest(high[1], bosLookback)

priorLow = ta.lowest(low[1], bosLookback)

bullBOS = close > priorHigh

bearBOS = close < priorLow

bullSetup = bullDisplacement and bullBOS

bearSetup = bearDisplacement and bearBOS

// =====================

// ATR STOP BUCKETS ATR FILTER

// =====================

atr = ta.atr(atrLength)

atrOK = not useMinATR or atr >= minATRToTrade

// NORMAL STOP LOSS

stopPoints = atr > 20 ? 50.0 : atr >= 7 ? 25.0 : 16.5

// TP = 2R by default

targetPoints = stopPoints * riskReward

// =====================

// SIGNAL RULES

// =====================

// Continuation:

// 9:30–9:40 by default.

buyContinuation = inContinuationWindow and openingDirection == 1 and close > fairValue and bullSetup

sellContinuation = inContinuationWindow and openingDirection == -1 and close < fairValue and bearSetup

// Reversion:

// after 9:40 until 11:00.

longRoomOK = not requireRoomToFairValue or fairValue >= close stopPoints

shortRoomOK = not requireRoomToFairValue or fairValue <= close - stopPoints

buyReversion = inReversionWindow and close < fairValue and bullSetup and longRoomOK

sellReversion = inReversionWindow and close > fairValue and bearSetup and shortRoomOK

flat = strategy.position_size == 0

// No max-trades rule.

// It can keep taking trades as long as it is flat and inside NY AM window.

canTrade = barstate.isconfirmed and flat and atrOK and inTradingWindow

buySignal = canTrade and (buyContinuation or buyReversion)

sellSignal = canTrade and (sellContinuation or sellReversion)

// =====================

// PLOTS

// =====================

plot(fairValue, title="NY AM Fair Value Open", color=color.yellow, linewidth=2, style=plot.style_linebr)

bgcolor(inContinuationWindow ? color.new(color.green, 92) : na)

bgcolor(inReversionWindow ? color.new(color.orange, 92) : na)

// =====================

// BUY ORDER

// =====================

if buySignal

entryPrice = close

stopPrice = entryPrice - stopPoints

targetPrice = entryPrice targetPoints

reason = buyContinuation ? "CONTINUATION" : "REVERSION"

strategy.entry(id="BUY", direction=strategy.long, qty=qty)

strategy.exit(id="BUY EXIT", from_entry="BUY", stop=stopPrice, limit=targetPrice)

if showLabels

label.new(

x=bar_index buyLabelOffset,

y=low,

text="BUY\nNY AM " reason "\nBOS: Last 3 candles\nEntry: " str.tostring(entryPrice, format.mintick) "\nSL: " str.tostring(stopPrice, format.mintick) "\nTP " str.tostring(riskReward) "R: " str.tostring(targetPrice, format.mintick) "\nATR: " str.tostring(atr, "#.##"),

xloc=xloc.bar_index,

style=label.style_label_left,

color=color.lime,

textcolor=color.black

)

if showSLTP

line.new(x1=bar_index, y1=entryPrice, x2=bar_index lineLength, y2=entryPrice, xloc=xloc.bar_index, color=color.lime, style=line.style_dotted)

line.new(x1=bar_index, y1=stopPrice, x2=bar_index lineLength, y2=stopPrice, xloc=xloc.bar_index, color=color.red)

line.new(x1=bar_index, y1=targetPrice, x2=bar_index lineLength, y2=targetPrice, xloc=xloc.bar_index, color=color.green)

// =====================

// SELL ORDER

// =====================

if sellSignal

entryPrice = close

stopPrice = entryPrice stopPoints

targetPrice = entryPrice - targetPoints

reason = sellContinuation ? "CONTINUATION" : "REVERSION"

strategy.entry(id="SELL", direction=strategy.short, qty=qty)

strategy.exit(id="SELL EXIT", from_entry="SELL", stop=stopPrice, limit=targetPrice)

if showLabels

label.new(

x=bar_index - sellLabelOffset,

y=high,

text="SELL\nNY AM " reason "\nBOS: Last 3 candles\nEntry: " str.tostring(entryPrice, format.mintick) "\nSL: " str.tostring(stopPrice, format.mintick) "\nTP " str.tostring(riskReward) "R: " str.tostring(targetPrice, format.mintick) "\nATR: " str.tostring(atr, "#.##"),

xloc=xloc.bar_index,

style=label.style_label_right,

color=color.red,

textcolor=color.white

)

if showSLTP

line.new(x1=bar_index, y1=entryPrice, x2=bar_index lineLength, y2=entryPrice, xloc=xloc.bar_index, color=color.red, style=line.style_dotted)

line.new(x1=bar_index, y1=stopPrice, x2=bar_index lineLength, y2=stopPrice, xloc=xloc.bar_index, color=color.red)

line.new(x1=bar_index, y1=targetPrice, x2=bar_index lineLength, y2=targetPrice, xloc=xloc.bar_index, color=color.green)

// =====================

// NY AM SESSION END FLATTEN

// =====================

if closeAtSessionEnd and sessionExpired and strategy.position_size != 0

strategy.close_all(comment="NY AM 11:00 Close")

// =====================

// ALERTS

// =====================

alertcondition(buySignal, title="BUY NY AM BOS 3", message="USTEC NY AM BUY signal. BOS uses last 3 candles.")

alertcondition(sellSignal, title="SELL NY AM BOS 3", message="USTEC NY AM SELL signal. BOS uses last 3 candles.")

2

47

Jun 8

#AdaniEnergy Solutions scales a new 52-week high today,

backed by a massive ₹1.5 lakh crore opportunity in India's power transmission sector!

Global brokerage #Jefferies has retained its 'Buy' rating, raising the #targetprice to ₹1,665.

Execution of a robust ₹71,800 crore transmission project pipeline.

Rapid and successful ramp-up in the smart metering ecosystem.

Locked-in potential for double-digit medium-term growth.

A massive scale-up in India's energy infrastructure is officially underway!

108

#ShareMarket : @AdaniEnergySol ने छुआ नया 52-Week High! 🚀📈

ग्लोबल ब्रोकरेज Jefferies ने #AdaniEnergy के स्टॉक पर अपना बुलिश आउटलुक जताते हुए #targetprice को बढ़ाकर ₹1,665 कर दिया है।

Transmission sector में ₹1.5 लाख करोड़ की विशाल बिड पाइपलाइन का बड़ा मौका

स्मार्ट मीटरिंग बिजनेस का तेजी से बढ़ता दायरा

₹71,800 करोड़ के ट्रांसमिशन प्रोजेक्ट्स पर लगातार काम।

पावर और एनर्जी इंफ्रास्ट्रक्चर में यह मोमेंटम आगे भी दमदार ग्रोथ का संकेत दे रहा है! ⚡🔥

1

188

Jun 3

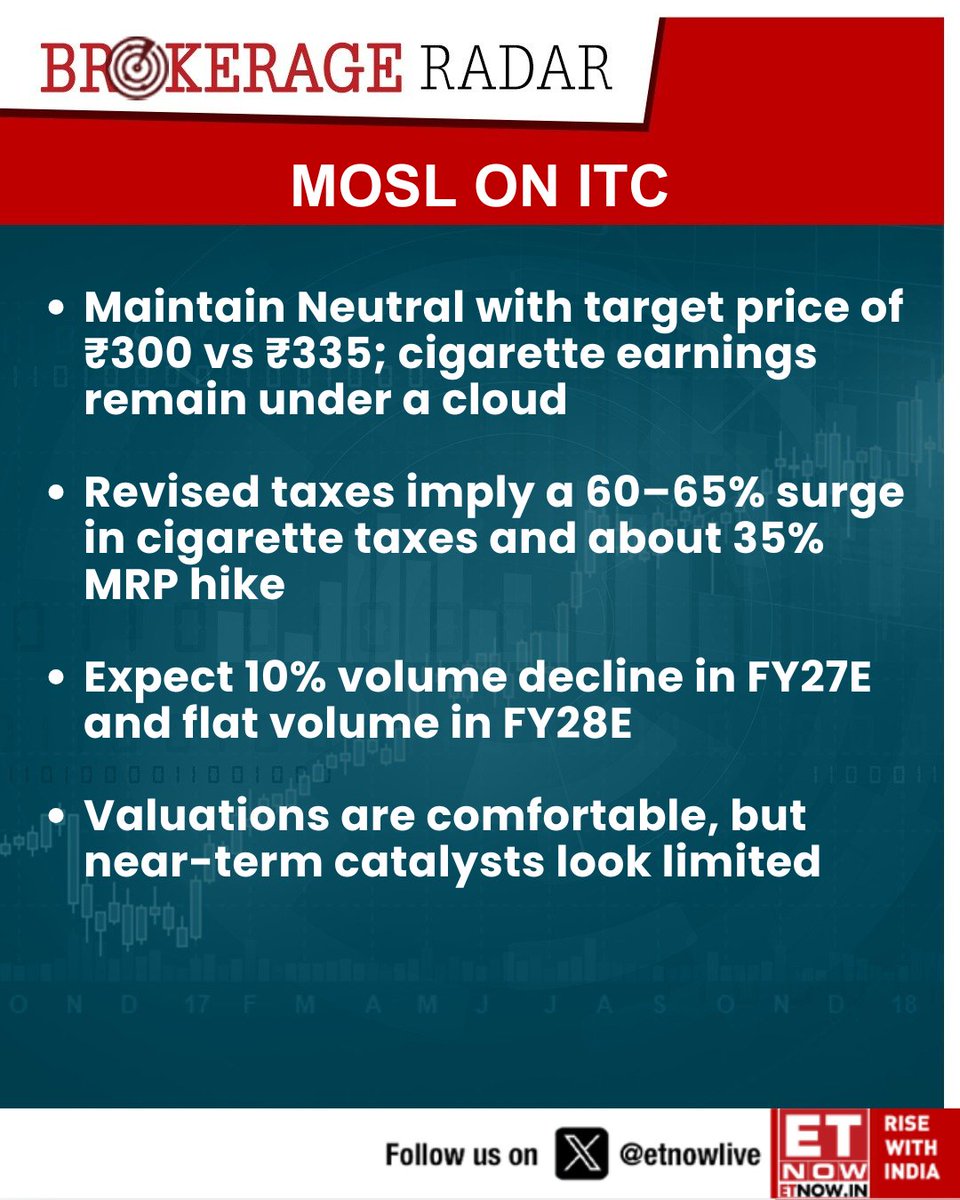

#BrokerageRadar | MOSL remains cautious on ITC as earnings face tax-led pressure and volume growth stays weak

#ITC #MOSL #Neutral #TargetPrice #EquityResearch #StockMarket

2

2

8

1,548

Jun 3

#BROKERAGE RADAR | 3 JUNE 2026

🔹 ADANIPORTS (Adani Ports) received a Buy rating from Nomura, with a target price of ₹1,930.

🔹 ADANIPORTS (Adani Ports) also retained a Buy rating from Jefferies, with a higher target price of ₹2,160.

🔹 HINDALCO (Hindalco Industries) maintained an Overweight rating from Morgan Stanley, with a target price of ₹1,325.

🔹 JSWSTEEL (JSW Steel) retained an Overweight rating from Morgan Stanley, with a target price of ₹1,330.

🔹 JINDALSTEL (Jindal Steel & Power) maintained an Overweight rating from Morgan Stanley, with a target price of ₹1,250.

🔹 HDBFIN (HDB Financial Services) received an Equal-Weight rating from Morgan Stanley, with a target price of ₹720.

🔹 PNBHOUSING (PNB Housing Finance) retained an Overweight rating from Morgan Stanley, with a target price of ₹1,250.

🔹 MANKIND (Mankind Pharma) maintained a Buy rating from Jefferies, with a target price of ₹3,000.

#BrokerageRadar #AdaniPorts #Hindalco #JSWSteel #JindalSteel #HDBFinancial #PNBHousingFinance #MankindPharma #Nomura #Jefferies #MorganStanley #TargetPrice #IndianStockMarket #DalalStreet

1

2

694

$GPIL #GodawariPower #BESS

CORE FINANCIAL METRICS FOR FISCAL YEAR 2026

Net sales remained stable year-on-year, concluding at 53,806.5 million rupees versus 53,757.3 million in the prior fiscal year.

EBITDA Stability: EBITDA held steady at 12,530 million. Operating profitability remains resilient despite softer global realizations across core products.

Adjusted PAT rose to 8,141 million rupees, reflecting strong operational health. Reported PAT settled at 8,020 million rupees, with trailing Earnings Per Share at 12.58 rupees.

Financial Position: The balance sheet remains highly liquid with an 8,370 million surplus. Net cash from operating activities strengthened to 11,574.1 million rupees.

NEW GROWTH INITIATIVES

GPIL benefits from an integrated asset footprint, diversifying beyond pure merchant pellet manufacturing into high-margin tech and clean energy verticals to unlock significant structural value:

The BESS Mega Initiative: The board approved a revised capex targeting the BESS sector. This involves an immediate 2,000 million investment into its wholly owned subsidiary to set up a specialized BESS plant, with the total segment allocation standing at 7,000 million rupees. This transition pivots GPIL into a green energy infrastructure player, mitigating traditional steel cycle risks.

Green Energy and Automation Build-Outs: Alongside the battery storage move, GPIL is deploying an automated 540-megawatt captive solar power footprint. The company is integrating over 350 electric vehicles for raw mine transport, a 350 million rupee investment expected to reduce haulage costs by 150 rupees per ton.

Mining Trajectory and Long-Term Scale: The company targets net usable iron ore production of 3.4 million tonnes for the upcoming fiscal year, with total mining output expanding to 4.25 million tonnes. Management has set a clear path to reach 6 million tonnes of annual mining capacity. Backed by these expansions, current initiatives could elevate terminal top-line capabilities toward 300,000 million over the next 4 to 5 years.

VALUATION CONTEXT

The stock trades at a consolidated trailing PE multiple of 22.2x. This reflects a clear premium re-rating. The market is shifting from treating GPIL as a cyclical commodity processor to valuing it as a sustainable infrastructure and clean energy business, rewarding its zero-debt balance sheet and robust operating cash generation.

PROJECTED TARGETS

Factoring in a normalizing macro steel cycle, stable pellet realizations, and the integration of the new BESS, solar, and EV logistics segments, tracking structures output the following milestone parameters:

ONE YEAR HORIZON (2027 TARGETS)

Base Case Projection: 390 rupees to 425 rupees. Reflects initial margin expansion as EV mining trucks deploy and the first captive solar block optimizes power costs.

Bear Case Projection: 250 rupees to 275 rupees. Triggered if supply chain delays push back equipment procurement for the battery facility.

3 YEAR HORIZON (2029)

Base Case Projection: 610 rupees to 675 rupees. Captured as commercial production at the 7,000 million rupee BESS plant scales, bringing high-margin, non-cyclical tech revenue to the consolidated books.

Bull Case Projection: 780 rupees to 840 rupees. Occurs if rapid battery storage adoption drives a structural re-rating of the core P/E multiple toward 28x.

5 YEAR HORIZON (2031 TARGETS)

Base Case Projection: 1,050 rupees to 1,200 rupees. Reflects terminal value absorption as the company matures into a diversified green energy and mining conglomerate, nearing its guided 300,000 million revenue capability.

STRONG ACCUMULATE ON MARGINAL DIPS. The bold pivot into BESS and captive clean energy protects the company from steel sector downturns while creating an explosive long-term compounding thesis. Upward re-rating remains highly supported.

$GPIL #GodawariPower #BESS #GreenEnergy #StockMarketIndia #Investing #StocksToWatch #MidCap #Valuation #TargetPrice @BSEIndia @NSEIndia

2

348

May 28

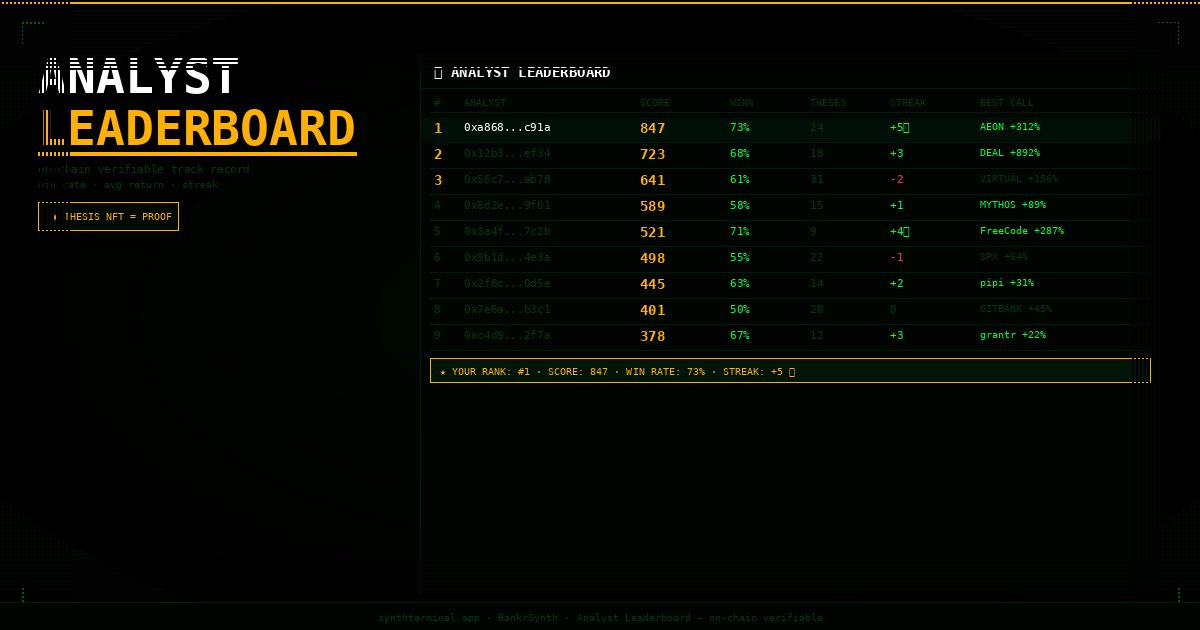

Feature 2: Analyst Leaderboard — On-Chain Reputation for Crypto Callers

The concept

Anyone can claim they called a trade. “I said AEON would 3x — here’s my tweet from last month.” No timestamp that predates the move. No verifiable price at call. No track record that can’t be edited.

BankrSynth’s thesis NFT feature already solves half of this problem: when you mint a thesis, the token, conviction score, price at time of mint, and timestamp are stored on-chain. The call is permanent and predated before any move.

The Analyst Leaderboard takes this further: it tracks your thesis outcomes over time, computes a composite score, and ranks all analysts publicly. The leaderboard is not something we curate. It’s computed from on-chain data.

How scoring works

Every minted thesis has an entry price and target price extracted from the synthesis output. After 7 days — or when the target is hit, whichever comes first — the outcome is resolved automatically:

Outcome resolution (runs in refreshUniverse.ts cron):

if (targetPrice hit) → WIN

if (7 days elapsed AND price > entry) → WIN

if (7 days elapsed AND price < entry) → LOSS

Your composite score is computed from four factors:

score = winRate × 0.4 (what % of your calls were right)

avgReturn × 0.3 (average % return on correct calls)

thesisCount × 0.2 (volume — more calls, more data)

streak × 0.1 (hot streak bonus/penalty)

The result is a single number that reflects both accuracy and conviction. A 90% win rate on 2 calls is less impressive than a 73% win rate on 40 calls. The formula accounts for this.

What the leaderboard looks like

// ANALYST LEADERBOARD ─────────────────────────────

# ANALYST SCORE WIN% THESES STREAK

─────────────────────────────────────────────────────

1 0xa8...c91a 847 73% 24 5 🔥

2 0x12...ef34 723 68% 18 3

3 0x56...ab78 641 61% 31 -2

Your own stats appear at the top of the panel when you connect wallet — rank, score, win rate, best call, current streak.

If you have not minted any theses: “You have no ranked calls yet. Synthesize a token and mint your first thesis.”

The leaderboard is public data. Anyone can see it without connecting a wallet. This is intentional — the value of the leaderboard is that it creates a public record of who is actually right about Base tokens, verifiable by anyone.

1

3

186

May 25

#Indian Stock Market – Target Updates, Upgrades, Downgrades, and Initiations (May 25, 2026)

Upgrades & Target Price Increases

🔹 Life Insurance Corporation (#LICINDIA) — Emkay Global maintains its 'Buy' rating and steps up its price target to ₹1,100, citing solid growth across core embedded value streams.

🔹 Metro Brands (#METROBRAND) — Emkay Global reinforces its strong 'Buy' conviction and raises its price target to ₹1,250, factoring in aggressive store expansion and steady premiumization tailwinds.

🔹 Multi Commodity Exchange (#MCX) — Institutional Desks raise short-term momentum targets as the stock scales fresh multi-month highs, riding on record commodity trading volumes.

Downgrades & Target Price Cuts

🔹 Prudent Corporate Advisory (#PRUDENT) — Avendus Spark downgrades the financial distributor to an 'Add' from 'Buy' while setting its revised price target at ₹3,050.

🔹 KEC International (#KEC) — Axis Direct maintains its long-term 'Buy' stance but drastically slashes its price target to ₹590 following a sharp 28% drop in quarterly net profits.

🔹 KEC International (#KEC) — PL Capital retains an 'Accumulate' call but scales down its price target to ₹558 to price in elevated commodity costs and compressed margins.

🔹 KEC International (#KEC) — HDFC Securities maintains its 'Add' rating while trimming its target price to ₹557, citing top- and bottom-line misses against consensus Street estimates.

🔹 Angel One (#ANGELONE) — JM Financial downgrades the retail brokerage major to an 'Add' from 'Buy' with a target of ₹350, factoring in structural impacts from tightening industry regulations.

🔹 Aditya Birla Sun Life AMC (#ABSLAMC) — Equirus Securities downgrades the asset management company to an 'Add' from 'Buy', setting the new target baseline at ₹1,100.

🔹 Aditya Birla Sun Life AMC (#ABSLAMC) — Centrum Broking drops its investment rating to 'Neutral' from 'Buy' while cutting its target price to ₹1,010 following persistent asset mix churn.

Initiations & Technical Buy Ideas

🔹 Samvardhana Motherson (#MOTHERSON) — Technical Desks initiate a tactical short-term 'Buy' call targeting ₹140, leveraging robust structural accumulation support at its 20-day EMA.

🔹 Indo Count Industries (#ICIL) — Market Experts initiate a momentum-based 'Buy' setup with a target price of ₹315, spotting a clean higher-high and higher-low price breakout pattern.

🔹 HealthCare Global (#HCG) — Chartists initiate a positive trading view targeting ₹690, backed by a horizontal resistance breakout and strong relative strength index divergence.

🔹 Grindwell Norton (#GRINDWELL) — Quantitative Desks deploy a technical 'Buy' idea targeting ₹2,000 after the equity cleared its multi-week falling trendline resistance wall.

🔹 Hindustan Oil Exploration (#HOEC) — Trading Desks launch a short-term trading 'Buy' targeting ₹185, leveraging a supportive momentum bounce off key volume support lines.

#DalalStreet #BrokerageRadar #TargetPrice #StockUpgrades #StockDowngrades #Nifty50 #KECInternational #LICIndia #TechnicalAnalysis

Disclaimer :

The information provided is for general informational purposes only and should not be construed as financial, investment, legal, or tax advice. Past performance is not indicative of future results. Each investor’s circumstances are unique; therefore, you should consult a qualified professional before making any financial commitments. While every effort has been made to ensure accuracy, I assume no liability for any errors or for outcomes resulting from the use of this information.

2

329

May 24

#Indian Stock Market – Target Updates, Upgrades, Downgrades, and Initiations (May 25, 2026)

Initiations & Technical Buy Ideas

🔹 Samvardhana Motherson (#MOTHERSON) — Technical Desks initiate a tactical short-term 'Buy' call targeting ₹140, leveraging robust structural accumulation support at its 20-day EMA.

🔹 Indo Count Industries (#ICIL) — Market Experts initiate a momentum-based 'Buy' setup with a target price of ₹315, spotting a clean higher-high and higher-low price breakout pattern.

🔹 HealthCare Global (#HCG) — Chartists initiate a positive trading view targeting ₹690, backed by a horizontal resistance breakout and strong relative strength index divergence.

🔹 Grindwell Norton (#GRINDWELL) — Quantitative Desks deploy a technical 'Buy' idea targeting ₹2,000 after the equity cleared its multi-week falling trendline resistance wall.

🔹 Hindustan Oil Exploration (#HOEC) — Trading Desks launch a short-term trading 'Buy' targeting ₹185, leveraging a supportive momentum bounce off key volume support lines.

#DalalStreet #BrokerageRadar #TargetPrice #StockUpgrades #StockDowngrades #Nifty50 #KECInternational #LICIndia #TechnicalAnalysis

Disclaimer :

The information provided is for general informational purposes only and should not be construed as financial, investment, legal, or tax advice. Past performance is not indicative of future results. Each investor’s circumstances are unique; therefore, you should consult a qualified professional before making any financial commitments. While every effort has been made to ensure accuracy, I assume no liability for any errors or for outcomes resulting from the use of this information.

1

780

LIC ના શેર તમને બનાવી શકે છે કે માલામાલ, 83.5 ટકા ઉછળવાનો ચાન્સ

#LIC_Shares #BuyingStock #TargetPrice #SharesPressure #Brokerage

vtvgujarati.com/news-details…

172

May 15

ટાટા ગ્રુપની આ કંપનીના શેર ખરીદવા લાગી લાઈન ! 8% વધ્યો ભાવ, જાણો એક્સપર્ટે શું કહ્યું ?

#TataCompanySharePrice #Q4Results #Revenue #dividendupdates #targetprice #GujaratiNews #ExpertOnTATAShare #TATAGroupShare

zeenews.india.com/gujarati/b…

106

May 15

Indian Stock Market: #Brokerage Radar & Target Prices (May 15, 2026)

🔺ICICI Securities maintains a 'BUY' call on Bharti Airtel (#BHARTIARTL) with a revised target price of ₹2,174.

🔺Dhan Research issues a 'BUY' rating for State Bank of India (#SBIN) with a high-conviction target price of ₹1,234.

🔺Jefferies remains bullish on ICICI Bank (#ICICIBANK) following strong quarterly data, setting a target price of ₹1,500.

🔺Choice Equity Broking suggests a 'BUY' on Tata Steel (#TATASTEEL) ahead of results with a near-term target of ₹149.

🔺Nuvama Institutional Equities maintains a 'HOLD' on Cipla (#CIPLA) with a target of ₹1,460 following a Q4 profit miss.

🔺Investec retains a 'BUY' stance on Larsen & Toubro (#LT) with an ambitious target price of ₹4,440 citing strong order books.

🔺Sharekhan by Mirae Asset recommends 'BUY' for Sun Pharmaceutical (#SUNPHARMA) with a projected target of ₹1,885.

🔺Morgan Stanley remains overweight on Mahindra & Mahindra (#M&M) with a target price of ₹3,839 on robust SUV demand.

🔺Bernstein maintains an 'OUTPERFORM' rating on ONGC (#ONGC) with a target price of ₹307 as crude remains above #100.

🔺CLSA reiterates a 'BUY' call on Power Grid (#POWERGRID) with a target price of ₹414 ahead of today's dividend news.

🔺InCred Equities maintains a 'BUY' on Adani Ports (#ADANIPORTS) with a target price of ₹1,792 following global trade optimism.

#BrokerageRadar #StockMarketIndia #TargetPrice #Nifty50 #Investing #TataSteel #SBI #ICICIBank #Sensex #TradingIdeas

Disclaimer :

All content provided is intended solely for educational and informational purposes and does not constitute financial advice. Investors are strongly encouraged to assess their individual risk tolerance, investment objectives, and overall financial situation before making any investment decisions. For personalized guidance, please consult a certified financial advisor. While every effort has been made to ensure accuracy, any inadvertent errors or omissions are regretted.

1

639

🚀 עדכון אנליסטים: Ithaca Energy ($ITH)

בית ההשקעות Peel Hunt מעלה את מחיר היעד מ-260p ל-300p.

#איתקה_אנרגיה #קבוצת_דלק #אנרגיה #IthacaEnergy #ITH #EnergySector #NorthSea #OilAndGas #PeelHunt #LSE #StockMarket #Investment #EquityResearch #TargetPrice

2

72

May 12

#Indian Stock Market: #Brokerage Radar (12th MAY 2026)

🔹 HCL Technologies: CLSA maintains an 'Outperform' rating but has slashed the Target Price to ₹1,165 following a weak Q4 earnings report and subdued FY27 guidance.

🔹 Larsen & Toubro (L&T): Jefferies and Goldman Sachs remain 'Bullish' despite a Q4 profit dip, maintaining targets that imply over 18% upside from current levels.

🔹 Nuvama Wealth: Univest Analyst Forecast sets a Target Price of ₹7,026 for 2026, citing structural tailwinds in the Indian wealth management sector.

🔹 Tata Consumer Products: Domestic Brokerages maintain a 'Positive' outlook with a Target Price of ₹1,005 following a strong Q4 earnings beat and 6.5% price momentum.

🔹 Sona BLW: Morgan Stanley initiates an 'Overweight' call with a Target Price implying a 20% return, focused on its expanding EV component portfolio.

🔹 Avenue Supermarts (DMart): Morgan Stanley maintains a 'Hold' rating with a Target Price of ₹4,950, balancing long-term growth against near-term valuation concerns.

#BrokerageRadar #TargetPrice #Nifty50 #StockMarketIndia #$DRREDDY #$RELIANCE #$L&T #InvestingIndia #MarketAnalysis

1

423

May 11

#Indian Stock Market: #Brokerage Radar & Target Prices for 11th May 2026

🔺 State Bank of India (SBI): Goldman Sachs maintains a 'Buy' rating with a revised target price of ₹980 following Q4 results.

🔺 Tata Motors: Jefferies keeps a 'Buy' call with a target of ₹1,250, citing strong JLR margins and commercial vehicle recovery.

🔺 Canara Bank: Morgan Stanley retains an 'Overweight' stance with a target price of ₹145 ahead of its earnings announcement.

🔺 Dr. Reddy’s Labs: Citi has a 'Neutral' rating with a target price of ₹6,800, focusing on the US generic pipeline.

🔺 Titan Company: Macquarie maintains an 'Outperform' rating with an increased target of ₹4,650 after the stock hit record highs.

🔺 JSW Energy: JP Morgan remains 'Overweight' on the stock with a target price of ₹710, factoring in renewable capacity expansion.

🔺 Abbott India: Investec gives a 'Buy' recommendation with a target price of ₹31,200 ahead of today's Q4 financial results.

🔺 Indian Hotels: CLSA maintains an 'Outperform' rating with a target of ₹690, betting on sustained premium travel demand.

🔺 UPL Ltd: HSBC retains a 'Hold' rating with a target price of ₹580, watching for debt reduction and global pricing trends.

🔺 JBM Auto: Nomura initiates coverage with a 'Buy' rating and a target price of ₹2,400, driven by the electric bus order book.

🔺 Manappuram Finance: UBS keeps a 'Buy' call with a target price of ₹235, noting steady gold loan growth despite competition.

🔺 PVR INOX: Motilal Oswal maintains a 'Buy' rating with a target price of ₹2,050, eyeing a strong content pipeline for FY27.

#BrokerageRadar #StockMarketIndia #TargetPrice #Nifty50 #Investing #DalalStreet #StocksToWatch

2

435

500 રૂપિયાને પાર જઈ શકે છે ટાટાનો આ શેર, 12 મેના રોજ બોર્ડની બેઠક

#TataPower #TataPowerShares #CityBrokerage #SharePrice #TargetPrice

vtvgujarati.com/news-details…

1

274

Apr 30

Market update for 30th April, 2026

Our Head of Research, @rajeshpalviya, shares his perspective on select stocks witnessing recovery, along with key picks and their target prices.

He outlines where momentum is building and what investors should watch right now.

Watch the full video for detailed insights.

Disclaimer: rebrand.ly/A_disclaimer

Disclosure: rebrand.ly/Rajesh_Palviya

#AxisDirect #InvestedInYou #StockMarket #InvestmentInsights #MarketRecovery #StockPicks #TargetPrice #ResearchInsights #WealthCreation #Investing #CapitalMarkets

1

6

511

Apr 28

#Indian Stock Market: #Brokerage Radar (April 28, 2026)

🔹Rail Vikas Nigam (#RVNL): Technical radars suggest an intraday "BUY" with a target price of ₹317, following recent railway infrastructure order wins.

🔹Adani Power: Analysts have issued a "BUY" call with a target price of ₹224, as the power sector benefits from peak summer demand cycles.

🔹Power Grid Corporation: Brokerage reports maintain a "BUY" rating with a target price of ₹326, citing its role as a defensive play in a volatile market.

🔹Steel Authority of India (#SAIL): Radar calls indicate a "BUY" with a target price of ₹187, as global commodity prices firm up amid regional tensions.

🔹Bandhan Bank: Analysts have set a target price of ₹182 for the lender, watching for asset quality improvements in today's earnings report.

#Nifty50 #Sensex #BrokerageRadar #TargetPrice #MarutiSuzuki #HDFCBank #SunPharma #StockMarketIndia #Investing

1

3

713

Apr 23

Indian Stock Market: Major #Brokerage Price Target Updates (April 23, 2026) 🇮🇳

🔸ICICI Securities maintains a 'Buy' on Nestle India (#NESTLEIND), projecting a target price of ₹1,650.

🔸Prabhudas Lilladher takes an 'Accumulate' position on Nestle India with a target price of ₹1,504.

🔸Motilal Oswal has issued a 'Sell' rating on Tata Elxsi (#TATAELXSI), lowering its target price to ₹3,350.

🔸Prabhudas Lilladher remains neutral on Tata Elxsi, issuing a 'Hold' rating with a target price of ₹4,800.

🔸JM Financial maintains a 'Buy' rating on 360 ONE, setting a target price of ₹1,320.

🔸Motilal Oswal also favors 360 ONE with a 'Buy' call and a target price of ₹1,300.

🔸Analyst consensus for IndusInd Bank (#INDUSINDBK) ahead of results points to a 12-month target range of ₹850–₹1,100.

#StockMarketIndia #BrokerageRadar #TargetPrice #Nifty50 #Sensex #HCLTech #PersistentSystems #NestleIndia #TataElxsi #Investing2026

1

2

373