23 Oct 2025

His Holiness the @DalaiLama Congratulate #Japan's Prime Minister @takaichi_sanae, Country's first female PM, #Japan-#Tibet has historical relationship dalailama.com/news/congratul… #FreeTibet #XiJinping #China #3rdPlenum #ThirdPlenum #CTA #TPiE #Tokyo #US #India #EU #AUS #UN #TibetWillBeFree

2

4

242

Counsellor Huang Jingrui is the spokesman of the Commissioner’s Office of #China’s Foreign Ministry in #HongKong & has been posted in the city since September 2022.

In his first-ever public address, Counsellor Huang spoke at an #FCCClubLunch to outline China’s #ThirdPlenum & how it will affect #HK. He also used the opportunity to address the international community’s concerns about declining #freedoms in the city.

“China and Hong Kong’s reputation has been smeared over the years, and actually the media is part of it. Media itself has become a problem, especially Western media,” he said.

In full: fcchk.org/hk-press-not-above…

2

4

1,444

24 Sep 2024

China's latest economic stimulus package, announced today, marks a significant shift in the government's approach to reviving their economy. This package, the most recent in a series of measures following July's Third Plenum meeting - which focused on long-term economic reforms - is notably more direct and substantial, warranting close attention from India and the global community.

Unlike previous stimulus efforts (since the Third Plenum) that primarily targeted the property sector, this round casts a wider net. It directly intervenes in the stock market by allocating cheap funding for professional Chinese investors to purchase domestic stocks, with $70 billion set aside for this purpose. Simultaneously, it further bolsters the property sector with additional mortgage rate cuts of 50 bps on average, building upon the 80 bps reduction on over $5 trillion of outstanding mortgages announced earlier this month.

While earlier measures, such as these mortgage rate reductions, primarily benefited the end-consumers (homebuyers) with banks absorbing the financial impact, this new package takes a different approach. This round includes provisions to reduce banks' reserve requirement ratio (RRR) by 50 basis points and reverse repo rates by 0.2 percentage points. These measures should improve banks' liquidity positions, effectively making the Chinese government the primary sponsor of this stimulus round.

The Chinese stock markets responded positively, with the Hang Seng and Shanghai indices surging by approximately 4% in a single day. Brent crude oil also saw a 2% increase, reaching $75.5/bbl at the time of writing. This reaction is particularly noteworthy given the recent underperformance of the Chinese stock market, which currently trades at a PE ratio below 10. In fact, the total market capitalization of Chinese stocks stands at about $9 trillion, less than twice India's current market cap of $5.5 trillion, despite China's significantly larger GDP ($18 trillion vs India's $4 trillion).

The scheme to directly lend money to professional investors for purchasing stocks is an unusual approach, and its effects are challenging to predict. The government's lending of $70 billion seems modest compared to the total market cap of $9 trillion. It's unclear how this relatively small injection, even if leveraged through F&O routes, could significantly alter the valuation multiples of Chinese stocks. Such measures are typically reserved for extreme crises, reminiscent of the US government's $500 billion TARP program following the 2008 financial crisis. While these interventions can reinforce investor confidence in dire situations, their tangible benefits to China's current economic state remain uncertain.

The impending impact of US-imposed tariffs on Chinese goods, set to take effect later this year and into 2025, is a crucial factor driving these stimulus measures. With steel exports expected to be significantly affected, China is focusing on reviving its domestic property sector. Previous analyses* suggest that a 10% growth in their property market could absorb the excess steel accumulation resulting from higher US tariffs.

This stimulus package is likely to have a substantial effect on China's housing sector, potentially absorbing their excess steel production. For India's steel sector, this development presents a dual opportunity: reduced dumping of Chinese steel in India, and potential new export opportunities in the US and other Western markets.

#ChinaStimulus #GlobalEconomy #IndianEconomy #SteelSector #EconomicOpportunity #GlobalTrade #ThirdPlenum #StockMarket #China #Exports #Tariffs #RealEstate #Housing #MortgageRates #Hangseng

*Also see x.com/swaminathankp/status/1…

13 Sep 2024

Recent developments in global trade, especially the imposition of higher tariffs on Chinese goods by Western economies, have increased pressure on China, potentially contributing to its changing posture and willingness to ease tensions with India. This shift is evidenced by the recent statement from India's External Affairs Ministry, indicating that approximately 75% of disengagement issues with China, including those relating to the border, have been resolved, with negotiations in progress for the remaining concerns.

This is reflective of China's increasing economic dependency on India, not only as a market for Chinese goods but also as a strategic partner in global supply chains. India's emergence as a manufacturing hub provides investment opportunities for Chinese firms seeking to diversify their manufacturing bases and mitigate the impact of Western sanctions.

India's stock markets surged by nearly 1.5% in yesterday's final trading hour, responding to China's decision to cut home mortgage rates by 80 basis points on over $5 trillion of outstanding mortgages. This move, potentially freeing up $42 billion in annual interest expenses, helps to revive their property sector and therefore significantly reduces the likelihood of Chinese dumping of metals and other commodities into India. Additional stimulus packages directed towards their housing market are possible this year, potentially emerging from China's Third Plenum held in July this year - a crucial meeting that occurs once every five years and has historically been a platform for introducing major economic reforms.

This revival in China's property sector may absorb the export volumes impacted by Western tariffs. For instance, China's iron and steel consumption in the property sector dropped from 350 million metric tons in 2020 to around 260 million metric tons in 2024. A 10% boost in this sector due to government stimulus could compensate for the expected $3-4 billion fall in steel exports to the US.

While these developments present opportunities, India must navigate this emerging scenario with caution to ensure long-term, sustainable economic growth. Two key priorities emerge:

1. Protecting domestic industries from the potential redirection of Chinese exports. With US tariffs on select Chinese goods expected to rise from ~7.5% to 25% this year, there's a risk of these goods being redirected to markets like India. The steel sector is particularly vulnerable. In 2023, China exported $3 billion worth of steel materials to India, along with $2.5 billion in finished steel products. With reduced access to the US market, there's a risk of increased steel dumping in India, which could adversely impact domestic producers and disrupt local market dynamics. In response to this concern raised by the steel industry, India will impose tariffs of between 12% and 30% on some steel products imported from China and Vietnam in a bid to safeguard and boost local industry.

2. Selectively allowing Chinese FDI in areas where India currently lacks technical expertise or faces a steep learning curve. This approach will enable India to swiftly position itself as a global manufacturing hub and establish a firm foothold in international supply chains. However, this reform must be implemented judiciously to prevent excessive Chinese control over Indian startups in critical sectors. The focus should be on enabling the selective establishment of Chinese manufacturing subsidiaries in India and facilitating the movement of Chinese experts. This approach aims to ensure knowledge transfer and upskilling of Indian workers, potentially catalyzing a new wave of Indian manufacturing startups.

In conclusion, while China's recent economic posture presents immediate opportunities for India, we must tread cautiously to ensure that these engagements contribute to long-term, sustainable economic growth.

#GlobalTrade #IndiaChinaStandoff #Manufacturing #IndianEconomy #Steel #FDI #EconomicGrowth #StockMarket #ChinaNews #MakeInIndia #AtmanirbharBharat #ManufacturingHub #SkillDevelopment #Diplomacy #GreenSteelIndia

*Also see x.com/swaminathankp/status/1…

11

38

328

65,189

13 Sep 2024

✍️ #China🇨🇳's #economy grew 4.7% in Q2 2024, down from 5.3% in Q1. With real #estate no longer a key #growth driver, what policies from the recent #ThirdPlenum will address these challenges?

policycenter.ma/publications…

3

131

11 Sep 2024

"the incoming EU leadership should put as a priority the redefinition of its 'China policy'", argues @laia_comerma in the latest CSDS Policy Brief.

Read🔸 csds.vub.be/publication/is-x… #China #Xi #ThirdPlenum

3

364

4 Sep 2024

✍️ #China🇨🇳's #economy grew 4.7% in Q2 2024, down from 5.3% in Q1. With real #estate no longer a key #growth driver, what policies from the recent #ThirdPlenum will address these challenges?

policycenter.ma/publications…

4

149

2 Sep 2024

Ever since the #ThirdPlenum on 15 Jul, #XiJinping has been out of the spotlight. Clear indications are that there is a pushback internally against him in the #CCP. Is he being deliberately sidelined? IS XI A LAME DUCK?gunnersshot.com/2024/09/02/i… via @palepurshankar @gunners_shot1

2

5

247

29 Aug 2024

📰 #China🇨🇳's #economy grew 4.7% in Q2 2024, down from 5.3% in Q1. With real #estate no longer a key #growth driver, what policies from the recent #ThirdPlenum will address these challenges?

policycenter.ma/publications…

4

138

24 Aug 2024

#ChinaPolicies /20-7

#ChinaPolicy

Third Plenum/Plenary Session

#ThirdPlenum #3rdPlenum

#ThirdPlenarySession

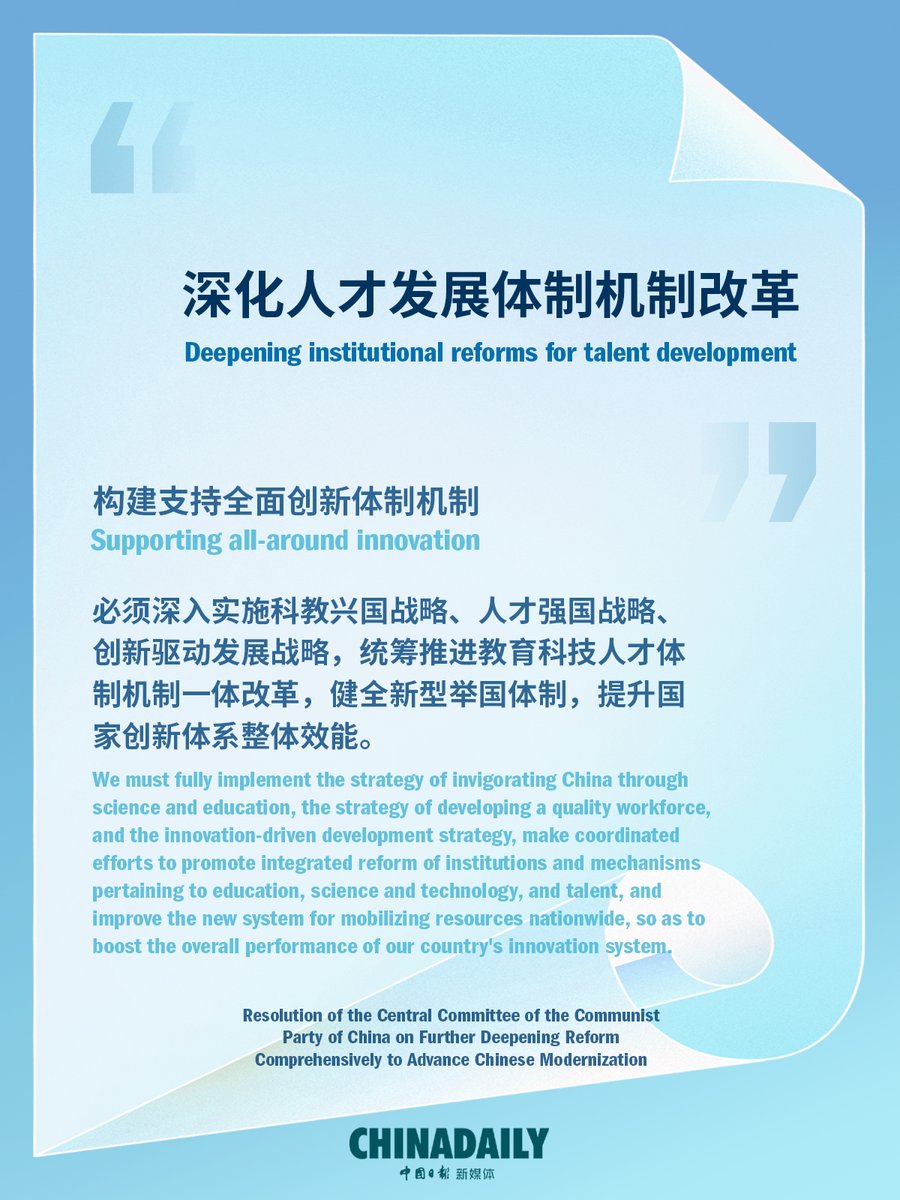

📍深化人才发展

体制机制改革 Deepening

Institutional Reforms

For Talent Development

🔸构建支持

全面创新体制机制

Supporting

All-around Innovation

24 Aug 2024

The Communist Party of China's resolution after the third plenary session of its 20th Central Committee lists three major areas on how to support all-around innovation. (3/3) #3rdplenum #XiJinping #XiSays @XisMoments

1

3

8

90

22 Aug 2024

The #ThirdPlenum highlights China's comprehensive strategy to boost its economic and military might, posing significant challenges for global dynamics and regional security, notes @kalpitm or-f.org/30274

442

22 Aug 2024

✍️ #China🇨🇳's #economy grew 4.7% in Q2 2024, down from 5.3% in Q1. With real #estate no longer a key #growth driver, what policies from the recent #ThirdPlenum will address these challenges?

policycenter.ma/publications…

1

4

203

21 Aug 2024

The #ThirdPlenum highlights China's comprehensive strategy to boost its economic and military might, posing significant challenges for global dynamics and regional security, notes @kalpitm or-f.org/30274

1

455

19 Aug 2024

#ChinaPolicies /20-5-1

#ChinaPolicy #中国政策

3rd Plenum/Plenary Session

#ThirdPlenum #3rdPlenum

#ThirdPlenarySession

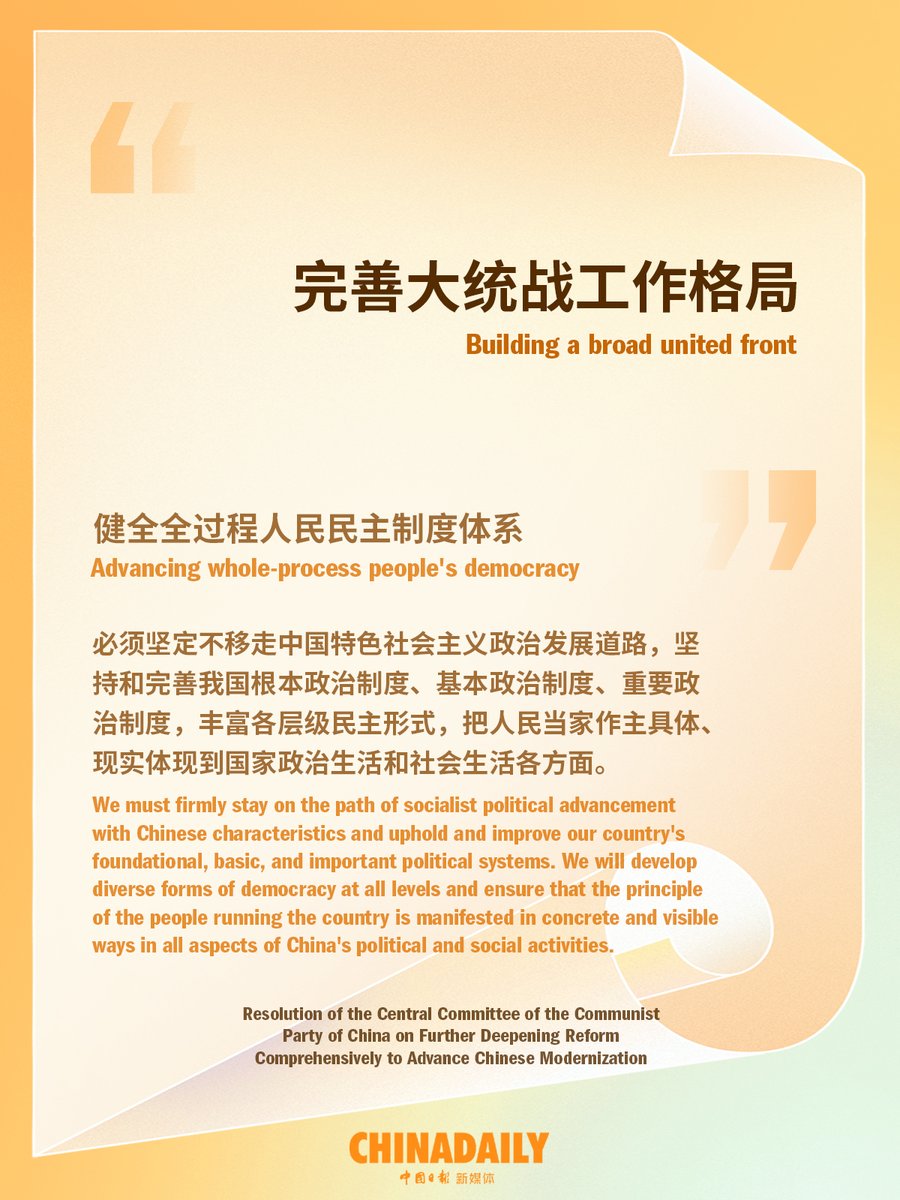

📍完善大统战工作格局

Building A Broad

United Front #UnitedFront

cpc.people.com.cn/BIG5/n1/20…

qstheory.cn/qshyjx/2024-08/0…

cppcc.gov.cn/zxww/2024/08/16…

18 Aug 2024

The Communist Party of China's resolution after the third plenary session of its 20th Central Committee lists four major areas on how to advance whole-process people's democracy. (4/4) #3rdplenum #XiJinping #XiSays @XisMoments

1

1

3

103

18 Aug 2024

#ChinaPolicies /20-5

Third Plenum

Plenary Session

#ThirdPlenum #3rdPlenum

#ThirdPlenarySession

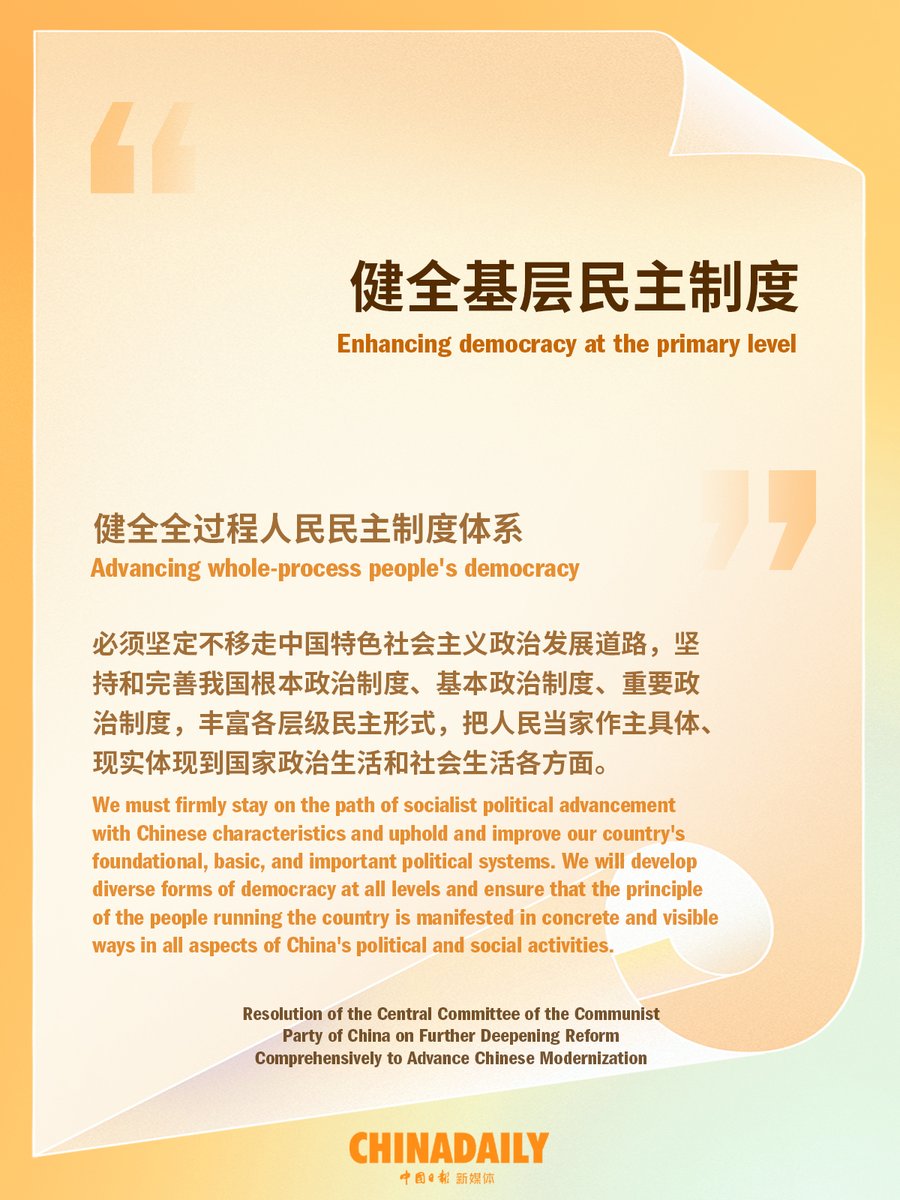

📍Enhancing Democracy

At The Primary Level

📍健全全过程人民民主制度

Advancing Whole-process

People's Democracy

npc.gov.cn/c2/kgfb/202408/t2…

qizhiwang.org.cn/BIG5/n1/202…

17 Aug 2024

The Communist Party of China's resolution after the third plenary session of its 20th Central Committee lists four major areas on how to advance whole-process people's democracy. (3/4) #3rdplenum #XiJinping #XiSays @XisMoments

1

1

6

83

13 Aug 2024

Reported upcoming financial talks between #China and #US come after the #thirdplenum drew up a sweeping reform agenda for high-quality development, while the US is facing increasing economic woes, including recession fears. globaltimes.cn/page/202408/1…

1

1

3

3,175

13 Aug 2024

The NDRC, #China’s top economic planning agency, has been accelerating the study of a batch of reform plans, which will be rolled out soon as the country steps up efforts to foster new quality productive forces following the #thirdplenum.

globaltimes.cn/page/202408/1…

1

1

5

3,518

9 Aug 2024

The #ThirdPlenum highlights China's comprehensive strategy to boost its economic and military might, posing significant challenges for global dynamics and regional security, notes @kalpitm or-f.org/30274

454

8 Aug 2024

The #ThirdPlenum highlights China's comprehensive strategy to boost its economic and military might, posing significant challenges for global dynamics and regional security, notes @kalpitm or-f.org/30274

449

5 Aug 2024

One of the most thoughtful commentators on China tech policy/strategy, @EvanFeigenbaum provides some context for recent events, #ThirdPlenum, #NQPF, etc...

4 Aug 2024

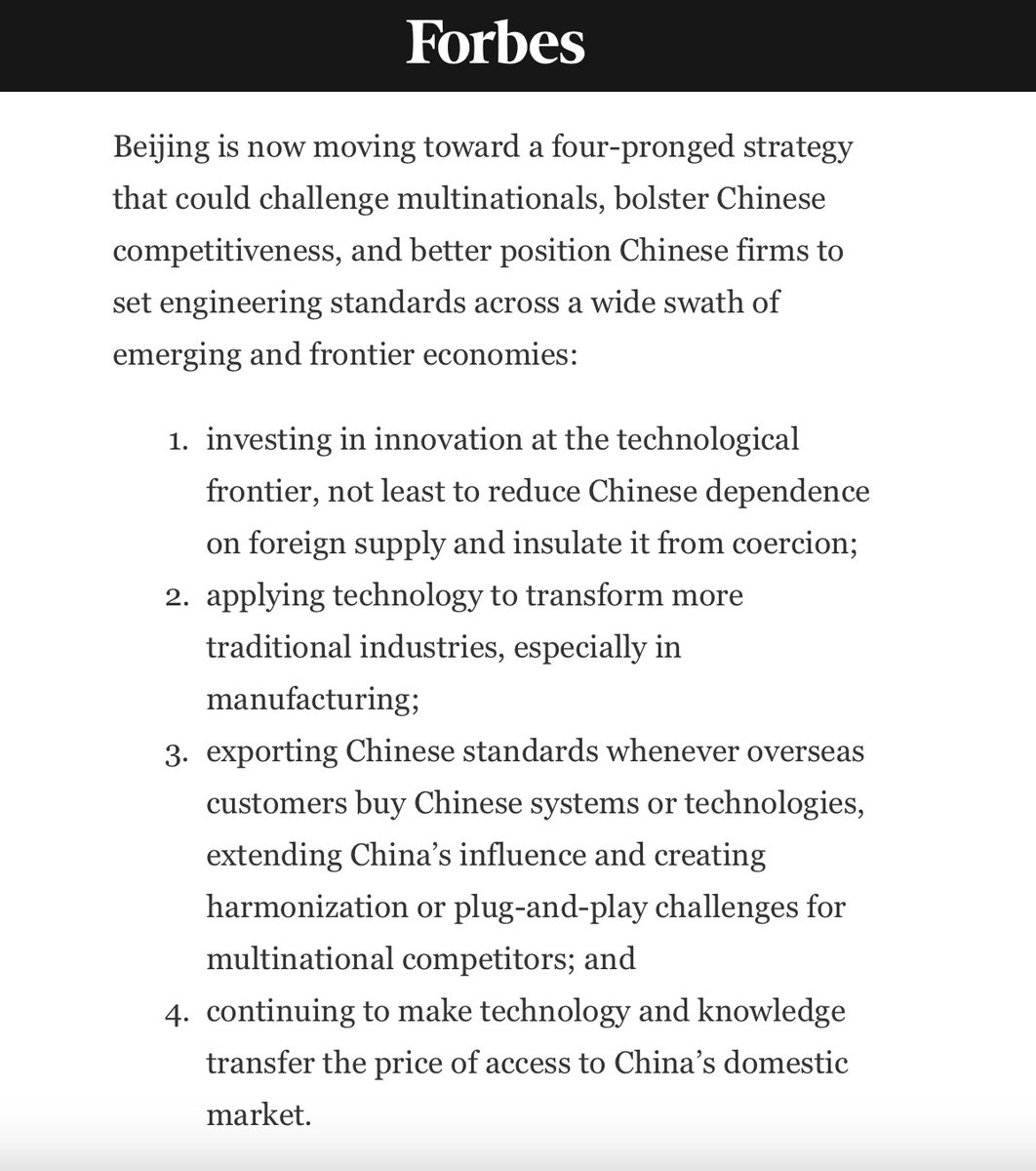

In @Forbes Markets, I explore four prongs of China's emerging #tech strategy. Taken together, and viewed through a long lens, they comprise a cohering effort to challenge foreign players, plug vulnerabilities, and bolster China’s competitive options: forbes.com/sites/evanfeigenb…

2

4

21

3,221

5 Aug 2024

📰 #China🇨🇳's #economy grew 4.7% in Q2 2024, down from 5.3% in Q1. With real #estate no longer a key #growth driver, what policies from the recent #ThirdPlenum will address these challenges?

policycenter.ma/publications…

1

4

232