Jun 4

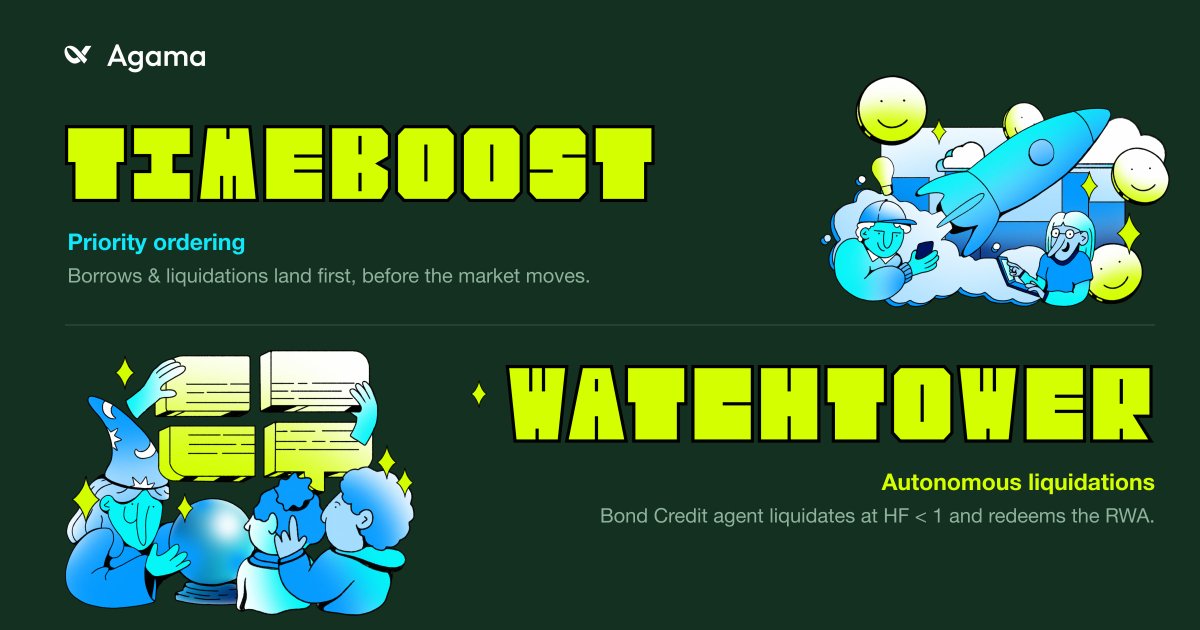

The fastest liquidation wins 💚

In RWA-backed lending, a late liquidation is bad debt. So we don't run a bot and hope, we run two layers built to win that race.

A @bondoncredit Watchtower agent watches every position onchain, 24/7. The instant one breaches its health factor, it fires, no human, no delay.

Then @arbitrum Timeboost carries that tx through the express lane, sequenced with priority while every other tx waits 200ms behind.

An AI that never blinks, on a lane built for speed. That's how real-world collateral should be protected.

2

2

14

441

May 29

This is what my AI says:

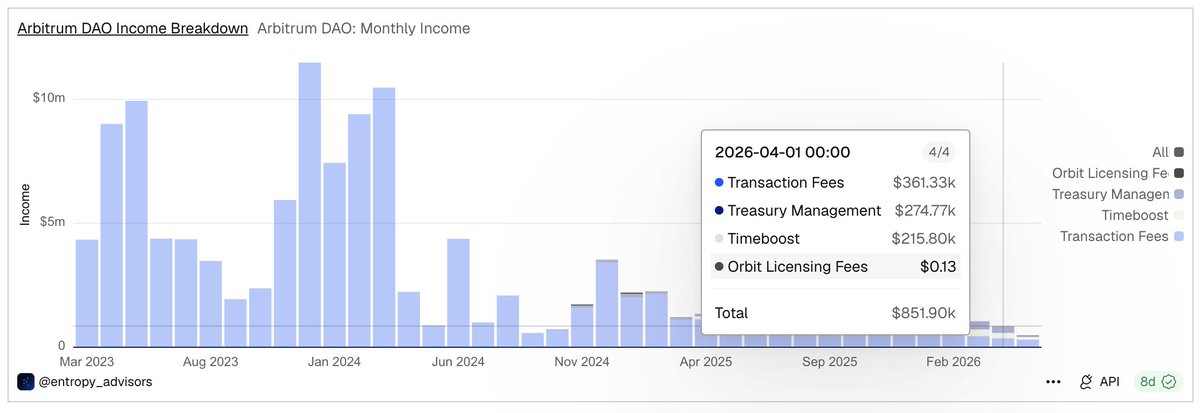

Four revenue lines into the DAO treasury.

- Sequencer fees. Users pay gas in ETH on Arbitrum One. The sequencer collects gas, pays Ethereum L1 for data availability (cheap since Dencun blobs went live March 2024), and the net flows to the DAO. Biggest line by far.

- Timeboost. Arbitrum's MEV auction, live since 2025. Searchers bid ETH every 60 seconds for the right to a 200ms 'express lane' that orders their transactions first. Auction proceeds to the DAO. Real but smaller than sequencer fees.

- Arbitrum Expansion Program (AEP). When other chains use Arbitrum's stack under the BSL license (Apechain, XAI, Treasure, Orbit chains), they pay a percentage of their sequencer revenue back to ArbitrumDAO. The chain-as-a-service line, growing as more L3s launch.

- Treasury yield (ATMC). ETH staking and OTC operations on treasury holdings. Not chain revenue strictly, but the treasury earns on its own balance.

The $23.49M 2025 revenue is mostly sequencer fees with contributions from Timeboost and AEP.

ARB holders never receive a direct fee share.

3

15

2,335

Thrilled to have our researcher @kakia1989 speaking in Munich about transaction ordering policies, with Timeboost as a leading example.

Timeboost emerged from the deep R&D and we’re excited to share how research-driven innovation is advancing blockchain infrastructure today.

May 28

Looking forward to speaking at TU Munich Blockchain & Cybersecurity Salon, at MEV, DeFi & Mechanism Design session, next week. The talk is about ahead-of-time auctions for transaction ordering, TimeBoost being the example. The program is available here: blockchain.salon.net.cit.tum….

1

14

2,652

May 28

Looking forward to speaking at TU Munich Blockchain & Cybersecurity Salon, at MEV, DeFi & Mechanism Design session, next week. The talk is about ahead-of-time auctions for transaction ordering, TimeBoost being the example. The program is available here: blockchain.salon.net.cit.tum….

13

3,279

May 25

ARB at $681m market cap sitting on $15.5b TVL. token captures 4.4% of its own TVL vs the L2 average of 32%. timeboost launched april 2025 projecting 50,000 ETH/year in MEV revenue but day 1 pulled $2.4k because major market makers haven't participated yet. $73.8m in Q1 fees, 97% margins, 800 protocols, blackrock BUIDL integration. and yet $3b in net outflows YTD, base doing more DEX volume in a day than arbitrum does in a week, and someone just bought $6.5m worth of governance votes for $10k. this is the cleanest binary setup in L2s right now. if timeboost monthly revenue crosses $8m by Q3 and the DAO doesn't implode, the value gap closes hard. if it doesn't, $15.5b in TVL is just parked capital generating nothing for token holders.

1

38

7,487

May 22

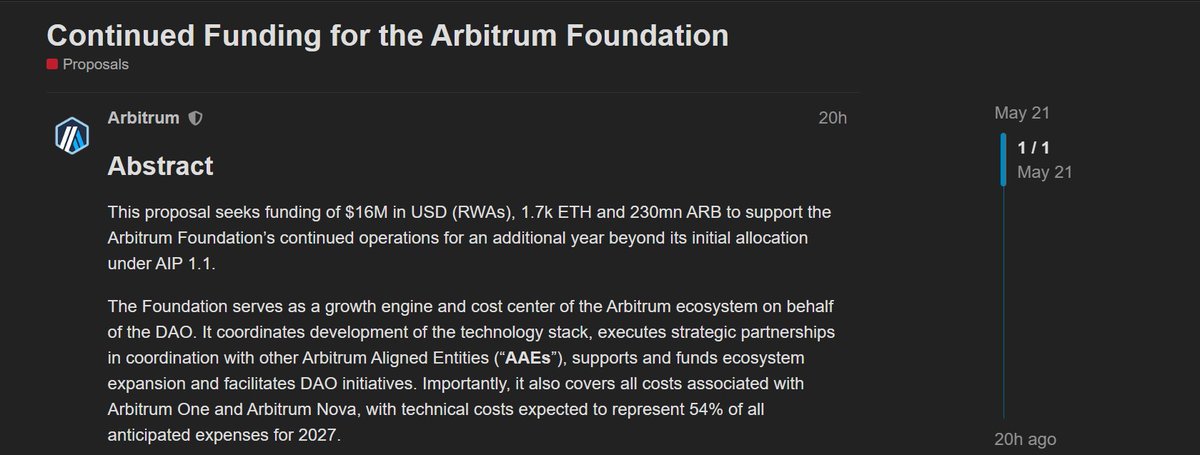

A new proposal in the ArbitrumDAO requests continued funding for the @arbitrum Foundation beyond its initial allocation under AIP 1.1.

The Foundation is positioned as a cost center for the ecosystem: while revenue from Arbitrum One, Timeboost, the Arbitrum Expansion Program, and other sources accrues to the DAO treasury, the Foundation covers many of the operational costs behind Arbitrum’s growth and continuity.

The proposal points to the ecosystem’s growth as context: by February 2026, Arbitrum had 4.7M daily transactions, $8.6B in stablecoin supply, ~$800M in RWAs, and $23.49M in gross profit generated in 2025 across transaction fees, Timeboost, and AEP.

For 2027, the Foundation projects $27.6M in operating expenses and 244.9M ARB for ecosystem growth expenses and investments, with technical costs representing around 54% of expected expenses.

The current request is lower than the full projected need, with the Foundation asking the DAO for $16M in RWAs/stablecoins, 1,740 ETH, and 230M ARB.

As delegates in the Arbitrum ecosystem, we’ll follow the discussion closely and share our vote as the proposal moves through governance.

Read more: forum.arbitrum.foundation/t/…

1

8

166

May 20

Stylus is objectively impressive tech.

RedStone's November 2025 benchmarks showed:

→ ~10-100x faster execution for crypto/big-int operations

→ ~30% gas savings on complex workloads

→ Native support for Rust, C, C (anything that compiles to WASM)

It's the most powerful EVM-compatible execution environment shipped to date.

And the capital backing is real:

→ ~5M ARB committed to Stylus Sprint grants

→ Timeboost generated ~$2M in revenue

→ US Commerce Department started publishing GDP data on Arbitrum One in July 2025

This isn't a forgotten project. It's an actively funded category-defining primitive.

1

2

21

BONUS: ARBITRUM-NATIVE TECH

Stylus, Timeboost and Arbitrum Chains unlock new business models on the Arbitrum Platform.

Here’s some exciting ideas we’re looking to see:

- Stylus-powered applications

- Timeboost trading systems

- WASM-native financial tooling

- Crosschain liquidity apps

3

3

15

3,059

May 11

🔵 Arbitrum

➡️ Timeboost reserve prices are shifting from fixed values to dynamic pricing based on real-time market conditions.

➡️ Firestarters officially concludes, with final grants focused on DeFi transparency dashboards and stablecoin research.

1

2

27

May 10

Brick from @EntropyAdvisors giving a talk about the ArbitrumDAO and interestingly — the treasury management efforts by them is now earning more revenue than Arbitrum’s Timeboost.

I didn’t know this — very cool.

3

36

7,392

MEV Bot Raih Profit $1 juta Setelah Front Run Transaski Vitalik Buterin.

FYI, setiap kali kita melakukan transaksi di blockchain, selalu ada jeda antara “transaksi dikirim” dan “transaksi dikonfirmasi”, termasuk saat swap atau trading di DEX. Dan biasanya, di jeda waktu itulah MEV bekerja.

MEV (Maximal Extractable Value) adalah profit tambahan yang bisa diekstrak dengan cara memanipulasi urutan transaksi dalam satu block.

Bukan exploit. Bukan bug. Ini konsekuensi langsung dari dua properti blockchain yang bertabrakan: transparansi mempool dan otoritas validator atas ordering.

─────────────────────────

BAGAIMANA CARA KERJANYA

Setiap transaksi yang lakukan pengguna, baik simple transaksi seperti kirim atau complex transaction seperti swap akan masuk dulu ke mempool sebelum dikonfirmasi dan di tambahkan ke block.

Mempool ini bersifat publik. Siapa pun bisa membaca dan mengawasi isinya secara real-time, termasuk bot.

Ekosistemnya MEV pun sudah cukup terstruktur:

→ Searcher: Bot yang memantau mempool, mencari peluang, lalu mengirim bundle transaksi yang sudah dioptimasi.

→ Builder: Pihak yang menyusun block paling profitable dari bundle transaksi yang masuk.

→ Validator: Memilih block dengan bid tertinggi dan menerima sebagian profitnya.

Infrastruktur seperti MEV-Boost di Ethereum memfasilitasi seluruh alur ini

─────────────────────────

MEKANISME YANG PALING UMUM

Sandwich Attack: Mekanisme di mana bot memanfaatkan transaksi user yang masih pending di mempool untuk mengambil profit dari perubahan harga.

Biasanya prosesnya seperti ini: pengguna submit swap token A ke B di DEX, lalu bot mendeteksi transaksi tersebut di mempool dan mensimulasikan potensi profitnya. Jika dianggap menguntungkan, bot akan membeli token B terlebih dahulu sebelum transaksi pengguna diproses (frontrun), sehingga harga naik.

Akibatnya, transaksi pengguna dieksekusi di harga yang lebih tinggi. Setelah transaksi selesai, bot langsung menjual kembali token tersebut (backrun) dan mengambil profit dari selisih harga.

Pengguna tetap menerima token-nya, tetapi di harga yang sudah di-markup. Selisih harga itulah yang menjadi keuntungan bot.

Dan baru baru ini, bahkan Vitalik Buterin juga menjadi korban mekanisme ini.

Tx hash simulation:

Vitalik Txsn: app.blocksec.com/phalcon/exp…

Mev Txsn: app.blocksec.com/phalcon/exp…

Arbitrage: MEVs bot memanfaatkan perbedaan harga token yang sama di beberapa DEX untuk mencari profit instan. Misalnya, bot membeli token di pool yang harganya lebih murah lalu langsung menjualnya di pool lain dengan harga lebih tinggi. Semua proses ini biasanya dilakukan dalam satu atomic transaction, sehingga jika salah satu langkah gagal, seluruh transaksi otomatis dibatalkan.

Berbeda dengan sandwich attack yang merugikan user retail, arbitrage justru sering dianggap sebagai bentuk MEV yang “sehat” karena membantu menstabilkan harga antar liquidity pool dan mengurangi gap harga di market.

─────────────────────────

MITIGASI YANG SEDANG DIKEMBANGKAN

→ Shutterized mempool: transaksi dienkripsi sebelum masuk mempool. Bot tidak bisa baca intent lebih awal → Timeboost: Membuat marketplace untuk priority access. Lebih transparan dibanding sistem yang tidak terstruktur.

Tertarik untuk membuat MEV Bots?

3

20

814

If Vitalik can get sandwiched, so can you.

Good excuse to learn a bit about MEV, mempools, and how to stop donating money to bots.

This is not just about one funny tx.

Although, yes, it is funny.

It is about the fact that Ethereum trading happens inside an adversarial ordering market.

When you send a public swap, your intent is visible before it becomes final.

Bots see it.

Bots simulate it.

Bots check if your slippage is worth extracting.

A sandwich is basically:

1. Bot sees your pending swap

2. Bot buys before you

3. Your swap executes at a worse price

4. Bot sells after you

5. Your slippage becomes their profit

You still receive the token, so it does not look like a hack.

But you got worse execution because someone inserted themselves into your transaction ordering.

That is MEV.

Not magic.

Not “the protocol got hacked.”

Just the mempool doing mempool things.

And MEV does not care who you are.

The bad side is obvious:

sandwiches, frontrunning, toxic orderflow, users getting silently taxed by bots.

But MEV is not only bad.

There is also defensive MEV.

The same infrastructure that lets bots monitor pending transactions, simulate outcomes, and race for priority can also be used by whitehats to intercept exploits, rescue funds, or backrun attackers before stolen assets fully move away.

Same transaction-ordering power.

Different use.

Bad MEV extracts from users.

Good MEV can protect users, stabilize protocols, execute liquidations, close arbitrage gaps, or race attackers during live exploits.

So I do not think the right question is:

“Is MEV good or bad?”

The better question is:

“Who controls transaction ordering, under what rules, and who receives the value?”

Different ecosystems are trying different answers.

Gnosis is working with Shutterized mempools.

The simple idea: transactions are encrypted before entering the mempool, ordered while still unreadable, and decrypted later.

So validators, builders, and searchers do not get to read your trade early enough to sandwich it.

Arbitrum is going in another direction with Timeboost.

Instead of pretending ordering has no value, it creates a market around a limited time advantage and routes part of that value back through the chain/DAO structure.

Different designs.

Same premise.

MEV is not an edge case.

It is part of blockchain market structure.

For users, the practical advice is boring but useful:

Do not use high slippage unless you know why.

Avoid large public swaps in illiquid pools.

Use CoW Swap or solver-based execution when possible.

Use private RPCs like MEV Blocker or Flashbots Protect.

Assume public mempool trading is adversarial by default.

The deeper point:

The mempool is where user intent becomes exposed.

The block is where that intent becomes final.

MEV lives in the gap between those two moments.

And that gap is one of the most important design spaces in crypto.

May 6

Jared from subway just sandwiched @VitalikButerin: etherscan.io/tx/0x7f8849543f…

this is the most Ethereum thing that has ever happened, MEV doesn't care who you are🥪

10

19

132

27,033

I want to share my thoughts on hyperliquid’s latest priority fees update. I think it’s going to significantly change the market structure there going forwards longer term.

A lot of the best market makers on HL - Alber Blanc, Pinely etc. are latency edge guys. They’ve already invested significant resources into trying to simulate what the next TOB is going to look like from pre-validated transactions, like by emitting raw mempool transactions from the node or by reverse engineering the binary to listen to the gossip data. Infra like this is all useless now, because you can literally just pay for it. There's a Dutch auction for the slot, you send your IP with your bid, and if you win, the IP gets whitelisted and prioritised, so the gossip data comes 10ms before everyone else.

The change to order priority fees is also interesting - you pay up to 8 bps to reduce the latency of your order. They say it’s empirically 45ms of latency reduced per bp paid, so max of 360ms faster - I haven’t tested this. Under the new system, if a maker cancels their order, that still gets processed first, but for the remaining executable orders, whoever paid more is matched first. Currently it looks like there aren’t that many people bidding for the market data, and even fewer (if any) bidding for the order priority. I think this is because Hyperliquid already implements a speedbump on taker orders which is roughly 250ms but can spike up to half a second so it’s already harder to take - the block time is ~70ms so this is ~4 blocks as it is, and makers have plenty of time to cancel their liquidity.

These fees are paid in HYPE and burned. This isn’t really new - when protocols see trading firms making money they often want to extract more of a cut. Arbitrum did a similar thing with the timeboost auctions, and I’d say this was pretty successful, in that roughly 20-30% of the latency sensitive dex flow moved onto timeboost, and volumes didn’t meaningfully change. We’re sitting at around a year since they shipped this, and timeboost brought in around $7mn in revenue in this time. This is on (roughly) $300bn in volume, so with Hyperliquid at approx. 10x this, I can see the bull case for them to move to this kind of model.

Objectively, I think it’s a smarter version of Lighter’s design - Jeff basically just waited to see what Lighter’s business model would look like, improved it, shipped it to testnet on April 10th, and rolled it out to mainnet within a week. I don’t think any firm has had time to think about the game theory of how to bid yet and optimise this, but it should basically completely collapse the gap between the top MMs.

Disclaimers - I’m long some HYPE and haven’t sold LIT airdrop (yet).

27

41

600

111,612