May 13

Provide owners and investors an unprecedented level of assurance on your next project.

With an official thumbs up from top independent engineer firms, Quintas Advisory and Luminate, our intelligent tracker control system, TrueCapture®, has become a proven option for validating and ensuring a utility-scale site’s production potential, before construction starts.

Currently deployed across 400 sites, it is helping unlock the full value of independent row architecture to deliver up to four percent more energy, faster and stronger ROI, lower LCOE, and millions in added revenue, per site, over 25 years.

Learn more about why TrueCapture is the go-to, bankable solution on five continents.

Download the Whitepaper: nextpower.com/post/whitepape…

#UtilityScaleSolar #SolarTracking #SolarPerformance #SolarROI #ValidatedResults #Bankability

3

141

May 13

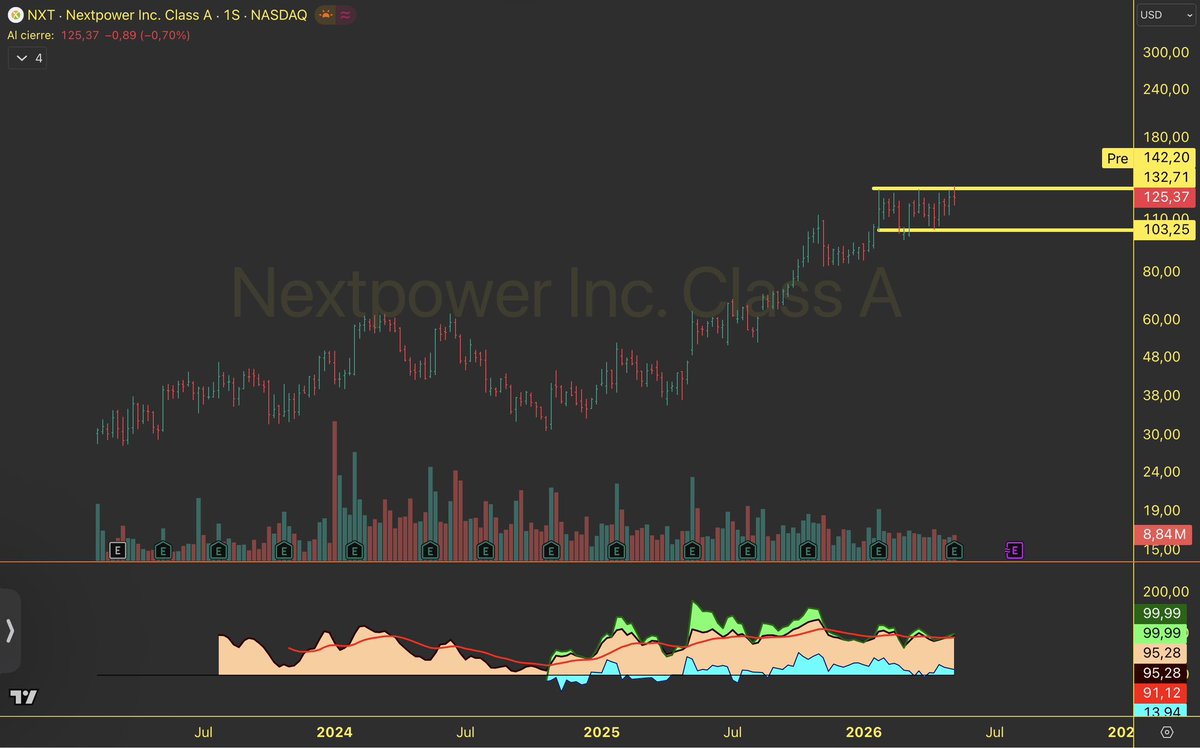

$NXT

Si nada se tuerce podemos tener otro buen tramo al alza

Calidad y gestionando toca la cadena de valor de las solares a excepción de los paneles 🧐. Ha dejado solo de ser “ seguidores solares”

⚡️ Nextpower: Eleva Perspectivas FY27 con un Backlog Récord de $5.25B

📊 Resultados Financieros

BPA (EPS) Ajustado: $1.05 (vs. $0.93 estimado) ✅

Ingresos: $881M (vs. $829.82M estimado) ✅

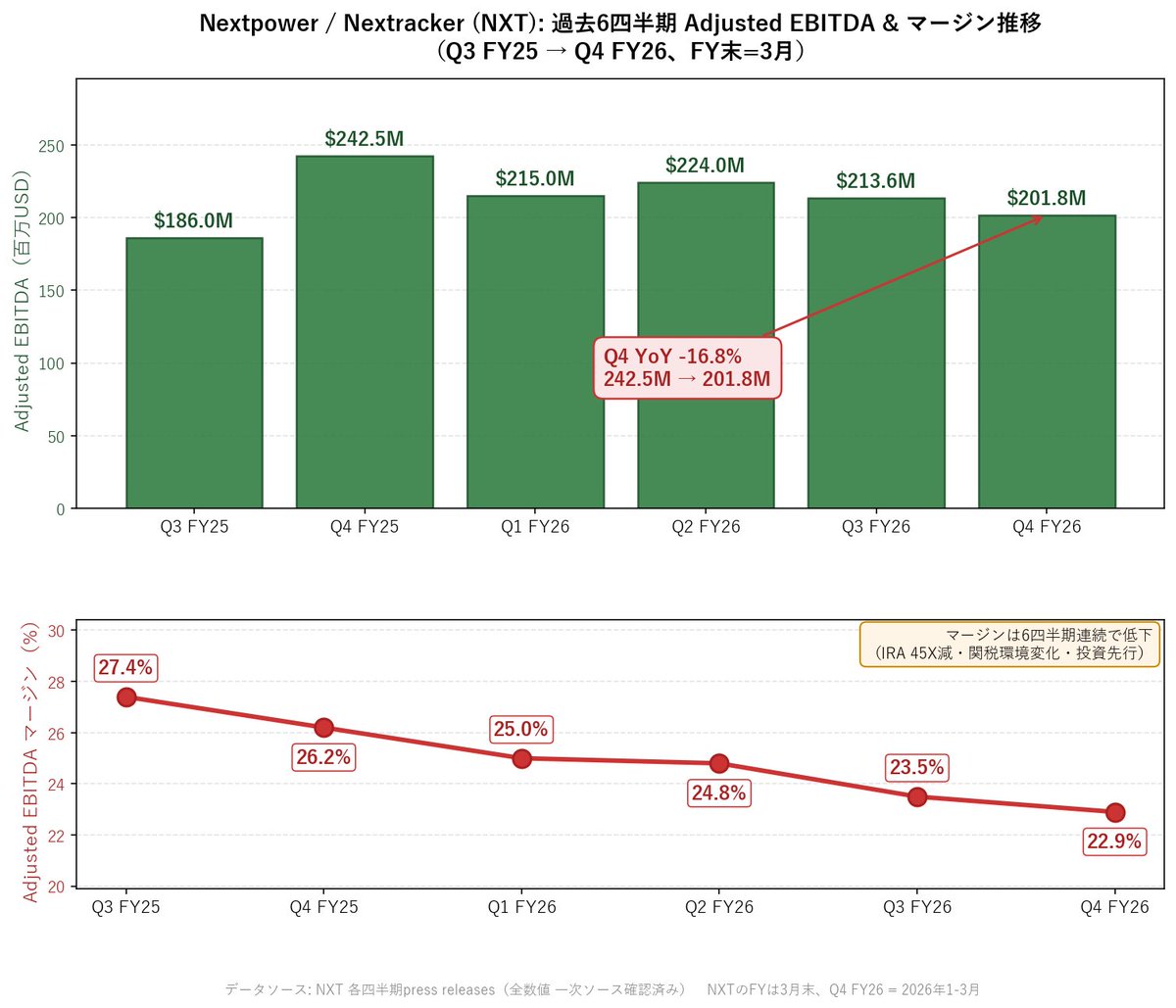

EBITDA Ajustado: $202M

Margen EBITDA Ajustado: 22.9%

Margen Bruto Ajustado: 34.5%

Backlog (Cartera de pedidos): >$5.25B 🚀

🔮 Guidance (Proyecciones FY27)

Ingresos FY27: $3.8B – $4.1B (vs. $3.93B estimado) ✅

BPA Ajustado FY27: $4.21 – $4.59 (vs. $4.79 estimado) ⚠️

EBITDA Ajustado FY27: $825M – $900M

🔑 Puntos Clave del Negocio

Los ingresos del FY26 alcanzaron un récord de $3.56B, marcando un crecimiento del 20% interanual.

Momentum histórico en reservas (bookings) a través de eBOS, robótica y soluciones combinadas.

Han superado los 160 GW en envíos acumulados de seguidores solares a nivel global.

Ingresos récord trimestrales y anuales en su plataforma de software TrueCapture.

Expansión estratégica hacia nuevos verticales: conversión de energía, almacenamiento en baterías (BESS) y centros de datos.

🗣 Comentario de la Directiva

El CEO, Dan Shugar, enfatizó que el FY26 marca un "punto de inflexión" definitivo. La compañía está dejando de ser simplemente un líder en seguidores solares para transformarse en una plataforma tecnológica integrada de energía a escala utility.

Visibilidad de ingresos blindada

El dato más crítico de este reporte es el backlog récord de $5.25B. En el sector de infraestructura, esta métrica funciona como un foso defensivo (moat) a corto plazo, otorgando a la directiva una visibilidad de flujos de caja envidiable para los próximos 18-24 meses, independientemente del ruido macroeconómico o de los tipos de interés.

Márgenes de software en un modelo de hardware

Un margen bruto del 34.5% es sencillamente espectacular para lo que tradicionalmente se consideraba una empresa de equipamiento. Esto confirma el éxito de su estrategia land-and-expand: usan el hardware para ganar cuota y luego monetizan a través de su software TrueCapture, el cual genera ingresos recurrentes de altísimo margen.

Interpretando el "miss" en la guía de BPA

La guía de ingresos supera las estimaciones, pero el midpoint del BPA para FY27 ($4.40 vs $4.79 esperado) se queda corto. Lejos de ser una señal de debilidad operativa, esto apunta a un ciclo intensivo de reinversión. La agresiva expansión hacia los centros de datos (para alimentar la megatendencia de la IA) y el almacenamiento de baterías requiere gasto operativo inicial, pero multiplica su mercado total direccionable (TAM).

El catalizador: Re-rating del múltiplo

La frase de Shugar sobre el "punto de inflexión" es un mensaje directo a Wall Street. Al redefinirse como una "plataforma tecnológica integrada" en lugar de un fabricante solar puro, Nextpower está pidiendo un re-rating. Si logran penetrar el mercado de infraestructura de energía para Data Centers, las acciones dejarán de valorarse bajo los múltiplos cíclicos del sector solar y comenzarán a cotizar con la prima propia de las empresas de tecnología industrial.

7

893

May 12

$NXT Q4 FY26 決算(FY3末)

⭕EPS Adj: 1.05 vs 予0.93

(-18.6% YoY / Beat 12.9%)

⭕売上: 880.52M vs 予829.82M

(-4.7% YoY / Beat 6.1%)

Adj EBITDA: 201.8M (-16.8% YoY)

EBITDAマージン: 22.9% (-330bps)

Adj粗利率: 34.5% ( 110bps)

※IRA 45X credits 47M含む(前年67M)

✅FY26通期売上 3.56B ( 20.3% YoY、過去最高)

vs 予3.51B (Beat 1.4%)

✅FY26通期Adj EPS 4.50 ( 6.6% YoY)

vs 予4.38 (Beat 2.7%)

✅バックログ 5.25B超、過去最高

✅累計トラッカー出荷 160GW突破

✅eBOS四半期受注、過去最高

✅NX PowerMerge 100MW超受注

✅Jinko Solar U.S.と複数年GW級鉄骨供給契約

✅Power Conversion事業買収発表 (Spain、FDI待ち)

✅投資適格信用格付け取得

⚠️ Q4売上・EBITDA・EPS全YoYマイナス

⚠️ 通期Adj FCF -17.4% YoY

⚠️ Power Conversion参入でFY27 50M増分コスト計画

FY27ガイダンス(売上引上げ・EPSは投資コスト織込み)

⭕売上 3.80-4.10B (予3.67B、前回3.6-3.8B)

(中間3.95B: Beat 7.6%、引上げ 250M)

❌Adj EPS 4.21-4.59 (予4.79)

(中間4.40: Miss-8.1%、 50M投資コスト影響)

Adj EBITDA 825-900M (中間862.5M、前回800-900M)

GAAP EPS 3.19-3.56 (中間3.375)

GAAP Net Income 501-559M (中間530M)

※Q1 FY27/FY28ガイダンス提示なし

🏷️ セクター: 再生可能エネルギー / ソーラーPVプラント

📝 事業内容: 太陽光発電所向け「インテリジェント電力生成プラットフォーム」。

ソーラートラッカー(追尾架台)の世界リーダーで累計出荷160GW超。

eBOS、基礎工事(NX Anchor)、ロボティクス、TrueCaptureを統合した

プラットフォーム企業へ進化中。Power Conversion参入でバッテリー

ストレージ/データセンター垂直市場へ拡大予定。本社フリーモント。

1

2

4,108

May 12

$NXT Q4 2026 earnings: Record Backlog and Annual Sales Mask Q4 Revenue Contraction and Margin Decay

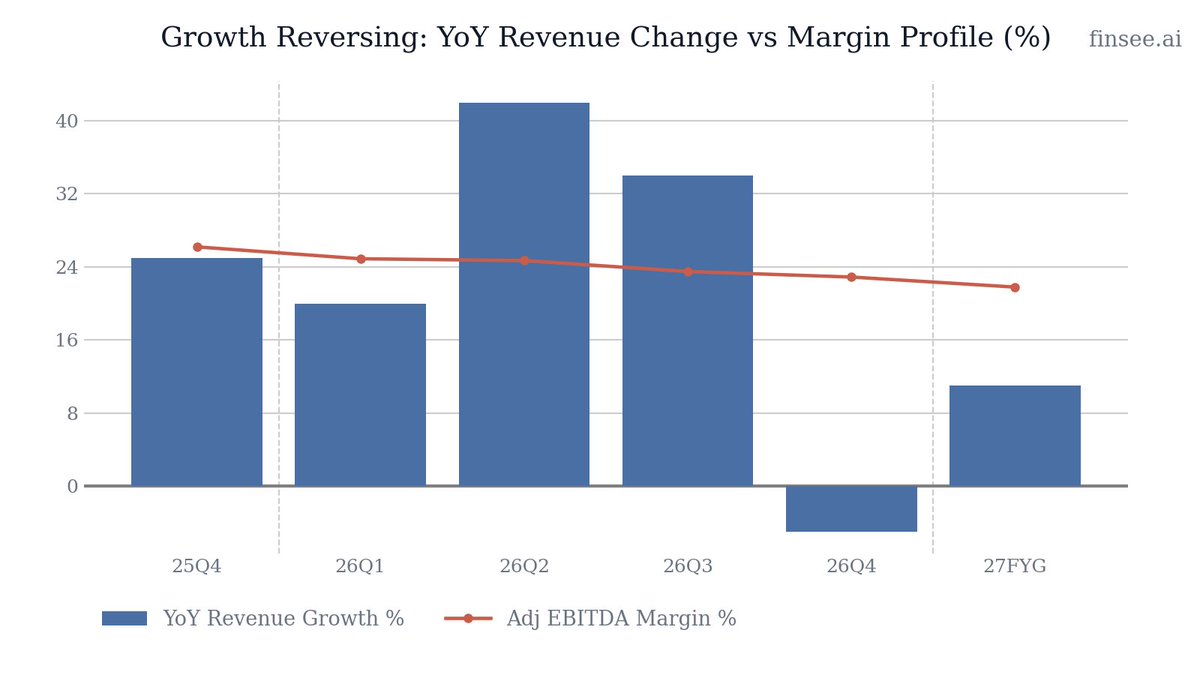

Nextpower's headlines tout a record $3.56B in FY26 revenue ( 20% YoY) and a raised FY27 outlook, but the Q4 data reveals a sudden break in the growth trend. Q4 revenue actually reversed to a 5% YoY decline ($881M vs $924M last year), and Adjusted EBITDA fell 16% YoY. Profitability is steadily eroding—Adjusted EBITDA margins compressed from 26.2% in 25Q4 to 22.9% this quarter, driven by heavy R&D investments, M&A integrations, and tariff impacts. However, the company is successfully executing its pivot from a tracker hardware supplier to an integrated solar platform. With a record $5.25B backlog and raised guidance implying a return to double-digit growth in FY27, management is trading near-term margins for long-term wallet share.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲 𝐢𝐬 𝐖𝐨𝐫𝐤𝐢𝐧𝐠 — The transition beyond pure-play trackers is yielding results. The company secured record bookings for eBOS (NX PowerMerge), foundations, and TrueCapture software, effectively increasing the revenue opportunity per solar project.

• 𝐌𝐚𝐬𝐬𝐢𝐯𝐞 𝐁𝐚𝐜𝐤𝐥𝐨𝐠 𝐏𝐫𝐨𝐯𝐢𝐝𝐞𝐬 𝐕𝐢𝐬𝐢𝐛𝐢𝐥𝐢𝐭𝐲 — Backlog swelled to a record $5.25 billion. Combined with strong US domestic content capabilities (over 25 partner facilities) and the new Nextpower Arabia JV, demand remains highly insulated from isolated regional downturns.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐐𝟒 𝐆𝐫𝐨𝐰𝐭𝐡 𝐖𝐚𝐥𝐥 — Despite massive backlogs, Q4 revenue unexpectedly shrank 5% YoY. If this is a project timing issue, it's manageable; if it signals a slowdown in deployment cadence or permitting bottlenecks, the FY27 guidance carries higher risk.

• 𝐔𝐧𝐫𝐞𝐥𝐞𝐧𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧 — Operating expenses are surging as the company funds its platform transition. Adjusted EBITDA margins have dropped sequentially for four straight quarters, and FY27 guidance implies further decay down to ~21.8%.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The strategic pivot to an integrated platform is clearly winning customer orders (record backlog), but investors must accept lower structural margins and elevated OpEx to fund this growth phase.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐞𝐝 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐒𝐮𝐜𝐜𝐞𝐞𝐝𝐢𝐧𝐠 [NEW]

Nextpower is successfully expanding wallet share per project. The rollout of NX PowerMerge (eBOS trunk connector) achieved record bookings of over 100 MW. The integration of NX Anchor foundations with NX Earth Truss enables deployment across all soil conditions, marking a clear evolution from a component supplier to a comprehensive plant ecosystem provider.

🟢 𝐃𝐨𝐦𝐞𝐬𝐭𝐢𝐜 𝐂𝐨𝐧𝐭𝐞𝐧𝐭 𝐚𝐬 𝐚 𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐌𝐨𝐚𝐭

The company's localized supply chain continues to win deals amid tariff uncertainty. Nextpower cemented a multi-year, gigawatt-scale US steel frame supply agreement with Jinko Solar. By enabling customers to hit IRA domestic content thresholds, Nextpower drives a 'flight to quality' away from heavily imported competitors.

⚪ 𝐃𝐚𝐭𝐚𝐜𝐞𝐧𝐭𝐞𝐫 𝐌𝐚𝐜𝐫𝐨 𝐓𝐫𝐞𝐧𝐝 & 𝐏𝐨𝐰𝐞𝐫 𝐂𝐨𝐧𝐯𝐞𝐫𝐬𝐢𝐨𝐧 [NEW]

To capture the 'bring your own power' trend driven by hyperscalers and AI data centers, Nextpower announced an agreement to acquire key power conversion product lines (subject to Spanish FDI approval). This accelerates their entry into the battery storage and data center verticals, making solar output dispatchable to match 24/7 compute loads.

🔴 𝐑&𝐃 𝐚𝐧𝐝 𝐒𝐆&𝐀 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬 𝐄𝐱𝐩𝐥𝐨𝐝𝐢𝐧𝐠 [NEW]

The cost of building this technology platform is steep. In Q4 alone, R&D expense nearly doubled YoY to $43.1M (from $23.5M). SG&A jumped to $100.6M (from $86.7M). This operating leverage reversal is the primary driver dragging down operating margins from 21.1% in 25Q4 to 17.4% in 26Q4.

🔴 𝐈𝐑𝐀 𝟒𝟓𝐗 𝐚𝐧𝐝 𝐓𝐚𝐫𝐢𝐟𝐟 𝐁𝐞𝐧𝐞𝐟𝐢𝐭𝐬 𝐍𝐨𝐫𝐦𝐚𝐥𝐢𝐳𝐢𝐧𝐠

A crucial prop to gross margins is diminishing. Q4 results included roughly $47M of net IRA 45X advanced manufacturing tax credit vendor rebates and tariffs, a sharp deceleration from $67M in the same quarter last year and $53M in Q3. As these benefits thin against rising base revenue, gross margins face mathematical headwinds.

🔴🔴 𝐐𝟒 𝐕𝐨𝐥𝐮𝐦𝐞 𝐑𝐞𝐯𝐞𝐫𝐬𝐚𝐥 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐃𝐞𝐦𝐚𝐧𝐝 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 [NEW]

Management highlights 'record FY26 revenue,' but conveniently buries that Q4 revenue dropped 5% YoY. If demand is truly accelerating and backlog is at record highs, a sudden top-line contraction suggests severe project push-outs, permitting delays, or supply chain bottlenecks at the developer level.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝐅𝐘𝟐𝟔): $513.6 million

Decelerating. Dropped from $621.8 million in FY25. The decline was largely driven by working capital investments to support the growing backlog, including higher inventory and contract assets, alongside an uptick in CapEx ($44.8M vs $33.9M) to build out new business lines.

𝐂𝐚𝐬𝐡 𝐚𝐧𝐝 𝐄𝐪𝐮𝐢𝐯𝐚𝐥𝐞𝐧𝐭𝐬: $1.09 billion

Stable and highly liquid. Increased from $766M a year ago. The company maintains an investment-grade credit rating with zero drawn debt, providing massive flexibility for the newly announced $500M buyback program and future cash-based M&A.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟕 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $3.8 - $4.1 billion

Accelerating vs Q4, but decelerating on a full-year basis. The midpoint ($3.95B) implies an 11% YoY growth rate compared to FY26's 20% growth. Represents an upgrade from the prior $3.6 - $3.8B outlook, reflecting confidence in converting the $5.25B backlog.

𝐅𝐘𝟐𝟕 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $825 - $900 million

Decelerating margin profile. While the absolute dollar range was raised from a prior $800-$900M view, the implied midpoint margin of 21.8% continues the steady multi-quarter drift downward from the company's historical 25-26% level. Guidance explicitly includes $50M in incremental costs to accelerate entry into the power conversion market.

𝐅𝐘𝟐𝟕 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐃𝐢𝐥𝐮𝐭𝐞𝐝 𝐄𝐏𝐒: $4.21 - $4.59

Decelerating. The $4.40 midpoint implies an outright decline from the $4.50 delivered in FY26. This reflects heavier planned integration costs, increased R&D for the NX platform, and potential normalization of tax rates.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐐𝟒 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐢𝐨𝐧

With backlog at a record $5.25B, what specifically drove the 5% YoY decline in Q4 revenue? Are you seeing structural permitting delays or developer push-outs?

𝐌𝐚𝐫𝐠𝐢𝐧 𝐅𝐥𝐨𝐨𝐫 𝐄𝐱𝐩𝐞𝐜𝐭𝐚𝐭𝐢𝐨𝐧𝐬

Adjusted EBITDA margins have compressed sequentially for four straight quarters down to 22.9%, and FY27 guidance implies ~21.8%. At what point does the operating leverage from new platform products kick in and establish a margin floor?

𝐌&𝐀 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐂𝐨𝐧𝐭𝐫𝐢𝐛𝐮𝐭𝐢𝐨𝐧

How much of the $200-$300 million raise in FY27 revenue guidance is purely organic tracker volume versus inorganic contribution from power conversion, robotics, and eBOS acquisitions?

𝐏𝐨𝐰𝐞𝐫 𝐂𝐨𝐧𝐯𝐞𝐫𝐬𝐢𝐨𝐧 𝐓𝐢𝐦𝐞𝐥𝐢𝐧𝐞

You noted $50M in incremental costs to accelerate entry into the power conversion market. What is the timeline to commercialize these products, and how dilutive will this be to gross margins in the near term?

3

1,053

May 12

$NXT Q4 FY26 EARNINGS HIGHLIGHTS

🔹 Revenue: $880.5M (Est. $828.9M) 🟢; -4.7% YoY

🔹 Adj. EPS: $1.05 (Est. $0.90) 🟢

🔹 Adj. Net Income: $161.7M (Est. $137M) 🟢; -16% YoY

🔹 Adj. EBITDA: $202M

🔹 Backlog: Over $5.25B, record level

FY27 Guide:

🔹 Revenue: $3.8B-$4.1B, raised from $3.6B-$3.8B

🔹 GAAP Net Income: $501M-$559M

🔹 EPS: $3.19-$3.56

🔹 Adj. EBITDA: $825M-$900M, raised from $800M-$900M

🔹 Adj. EPS: $4.21-$4.59

🔹 Incremental Costs: Approx. $50M related to power conversion market entry

Other Metrics:

🔹 Cumulative Tracker Shipments: Surpassed 160 GW globally

🔹 Backlog: Over $5.25B, record level

🔹 NX Horizon-XTR Sales: Exceeded 50 GW cumulative

🔹 Tracker Systems Sales: Surpassed 25 GW to date in each of Latam and MEIAT

🔹 Q4 New Product & Bundled Solution Bookings: Increased QoQ

🔹 eBOS Bookings: Record quarter

🔹 NX PowerMerge Bookings: Over 100 MW

🔹 TrueCapture Revenue: Record quarterly and annual revenue

🔹 First Bundled VCA Project Incorporating Robotics: Booked

M&A:

🔸 Zigor Power Conversion Assets Acquisition: Approx. $80.5M in cash

🔹 Closing Payment: $46M

🔹 Potential Earnouts: Up to $34.5M

🔹 Additional Growth Investment: $50M

🔹 Production Ramp: Expected to begin in 2027

🔹 Deal Requires Spanish FDI Approval

Commentary:

🔸 “Fiscal 2026 marked a defining inflection point for Nextpower as we accelerated our evolution from the solar tracker leader over the last decade to an integrated utility-scale energy technology platform.”

🔸 “Our core tracker business remains very strong, supported by one of the highest booking quarters in our history and expanding market leadership.”

🔸 “We are now seeing clear, measurable traction around our platform strategy, reflected in rising adoption across eBOS, foundations, and robotics solutions, early success in bundled deployments, and growing demand for new products such as NX PowerMerge.”

🔸 “Supported by our growing backlog and strong bookings momentum, we are raising our fiscal 2027 outlook and remain focused on disciplined capital allocation, investing in a balance of organic growth and strategic acquisitions, returning capital to shareholders, while maintaining a strong balance sheet and delivering consistent, long-term shareholder value.”

8

7

66

16,369

$NXT 𝐍𝐞𝐱𝐭𝐩𝐨𝐰𝐞𝐫: 𝐑𝐚𝐢𝐬𝐞𝐬 𝐅𝐘𝟐𝟕 𝐎𝐮𝐭𝐥𝐨𝐨𝐤 𝐀𝐬 𝐁𝐚𝐜𝐤𝐥𝐨𝐠 𝐇𝐢𝐭𝐬 𝐑𝐞𝐜𝐨𝐫𝐝 $𝟓.𝟐𝟓𝐁

📊 𝐑𝐞𝐬𝐮𝐥𝐭𝐬

• Adj. EPS: $1.05 (Est. $0.93) ✅

• Revenue: $881M (Est. $829.82M) ✅

• Adj. EBITDA: $202M

• Adj. EBITDA margin: 22.9%

• Adj. gross margin: 34.5%

• Backlog: >$5.25B

⠀

🎯 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

• FY27 Revenue: $3.8B–$4.1B (Est. $3.93B) 🟰

• FY27 Adj. EPS: $4.21–$4.59 (Est. $4.79) ❌

• FY27 Adj. EBITDA: $825M–$900M

⠀

📌 𝐊𝐞𝐲 𝐓𝐚𝐤𝐞𝐚𝐰𝐚𝐲𝐬

• FY26 revenue reached record $3.56B, up 20% YoY

• Record bookings momentum across eBOS, robotics and bundled solutions

• Surpassed 160 GW cumulative tracker shipments globally

• Expanding into power conversion, battery storage and data center verticals

• Record quarterly and annual TrueCapture revenue

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 𝐂𝐨𝐦𝐦𝐞𝐧𝐭𝐚𝐫𝐲

• CEO Dan Shugar said FY26 marked an “inflection point” as the company evolves from a solar tracker leader into an integrated utility-scale energy technology platform

1

2

564

Nuestro parque fotovoltaico Tepezalá Solar cumple siete años generando energía limpia y renovable, contribuyendo así a la transición energética.

Con un enfoque en eficiencia operativa, cuenta con la tecnología TrueCapture, una herramienta automatizada de monitoreo que utiliza algoritmos de optimización para ajustar la orientación de los paneles solares según las condiciones ambientales, maximizando la captación de luz y la producción energética.

Descubre más sobre nuestras #SolucionesBajasEnCarbono en: bit.ly/3XfdoTP

5

6

499

Feb 1

Competitive Moat & Strategic Positioning

The company maintains the #1 global tracker market share for ten consecutive years

Technical Advantage: The NX Horizon-XTR eliminates the need for extensive land grading, which reduces site preparation costs for developers and simplifies the permitting process.

Software Moat: The TrueCapture system maximizes energy production by adjusting individual rows in real-time to avoid shading and optimize for diffuse light.

2$-6% additional capability.

Switching Costs: Nextpower serves 90% of the top owners and developers in the U.S.. Its integrated "Connected Plant" model (software structural electrical) creates high stickiness through a single-vendor ecosystem.

Global Scale: Nextpower operates through over 100 global manufacturing sites in 45 countries, providing supply chain resilience against localized trade regulations

While no single "Moat" exist for $NXT they have numerous mini moats we can call them. Replicating their business model is extremely difficult to do in a short period of time.

1

2

82

NextPower $NXT – earnings call insights.

As you know, AI will drive an unprecedented explosion in electricity demand throughout the coming decade.

Solar, with its plunging LCOE (~$20–30/MWh in optimal sites), zero marginal cost, and modular deployability, is physically destined to become the default baseload for compute infrastructure.

In this context, $NXT has evolved from a pure-play tracker supplier to a vertically integrated, end-to-end utility-scale solar platform: AI-optimized trackers, software (TrueCapture), adaptive foundations (NX Earth Truss), domestic EBOS, robotics for installation/maintenance, and emerging power conversion for solar-storage hybrids.

This bundling materially reduces system LCOE by 5–10% via higher yields (20–30% from trackers over fixed-tilt 2–6% from TrueCapture's ML-driven shading mitigation and diffuse light tracking), 30% faster installation with Earth Truss (adapting to soil mechanics, cutting material use 20–30%), and minimized losses (e.g., optimized EBOS cabling to curb I²R heating).

Moats compound deeply:

Tech leadership

- NX horizon hail pro:

Withstands 2-inch hail at 100 mph via torque-tube reinforcements and AI-stow algorithms (integrating Doppler radar for storm prediction). Empirical data across 2,170 hailstorms in 2025 shows module breakage <0.007%, orders of magnitude below industry 1-5% averages. This slashes insurance premiums (up 50% post-2024 Texas events) and unlocks hail-prone US Midwest amid IPCC-projected 20% severe weather by 2050.

- TrueCapture: ML models (neural nets on terabytes of irradiance data) simulate photon paths, minimizing cosine losses with sub-1% yield prediction error, transforming intermittent solar into near-dispatchable power for data center co-location, syncing with GPU spikes.

- Power conversion pilots (2026): >98% efficient SiC inverters for hybrids, AI-forecasting storage dispatch. Critical as 80% new US solar pairs with batteries (<$100/kWh costs by 2030), enabling "bring your own power" for hyperscalers.

Policy-aligned domestic manufacturing

IRA ramps and tariffs (25-50% on foreign trackers) accelerate localization: $NXT's 100% domestic-content trackers, expanding US EBOS (25 partners), and 81% US-weighted revenue ( 63% YoY) yield structural advantages over Chinese rivals (70% global market). Q3 tariffs hit $44M but are offset via diversified supply; long-term, they entrench ecosystem lock-in as AI software ingests proprietary data, raising switching barriers.

Global scaling

NextPower Arabia JV: 2.25 GW initial supply (delivering now), 12 GW local manufacturing capacity, tech royalties (likely 5-10%), and equity shares without consolidation, de-risking exposure. Taps MENA's unmatched irradiance (up to 2,500 kWh/m² annually) and Saudi's 130 GW renewables target by 2030, transforming petrostates into solar exporters while countering Chinese dominance and aligning with UAE's 5 GW round-the-clock projects.

Europe: record bookings via REPowerEU. Overall, >$5B backlog (implying 5-10 GW at $0.5-1/W) provides 1-2 years visibility.

Financial execution pristine

- Q3 Revenue: $909M ( 34% YoY, 81% US-driven)

- Adj. EBITDA: $214M ( 15% YoY, 23% margin)

- YTD Revenue: $2.68B ( 32% YoY)

- YTD GAAP Net Income: $435M

- Operating Cash: $123M Q3 ($391M YTD)

- Adj. Free Cash Flow: $119M Q3 ($360M YTD)

- Balance sheet: $953M cash, zero debt, new investment-grade rating

- Capital alloc: Modest CapEx, implied M&A (power tech), $500M 3-year buyback

Raised FY2026 guidance: Revenue $3.425-3.5B, EBITDA $810–830M, EPS $4.26-4.36, assuming stable policy, implying 20-30% FY2027 growth.

Risks are real but manageable: tariffs, permitting delays, and project timing variability.

If they capture 10-15% of global utility-scale additions (~500 GW cumulative 2026–2030), revenues triple by 2030, with software/royalties expanding margins to 50% .

Looking forward to $NXT evolving into a behemoth in the AI era.

3

435

22 Dec 2025

$FSLR と $NXT が上昇。理由はこれ。

Intersectが両社の顧客だと再確認。

・$FSLR:First Solarの太陽光モジュール

・$NXT:Nextrackerのトラッカー+TrueCapture

大型案件=実需が株価を押し上げた。

22 Dec 2025

$GOOGL

Intersect Powerを48億ドルで買収。

電力先行型キャンパスで

AI向け計算需要の稼働率・コスト・拡張時期を自社でコントロール。

送電網増強を何年も待たずに済む。

📖 Intersect Power

再エネ発電と蓄電を開発する米国企業。

AIデータセンター向けに電力先行インフラを提供。

2

811

$NXT

오늘은 태양광 발전 효율을 더 극대화하는 태양광 트래커(추적장치) 및 관련 소프트웨어를 제조, 공급하는 기업 넥스트래커(티커 : NXT)에 대해서 알아보겠습니다.

1. 기업 개요 (무엇을 하는 회사인가?)

주요 제품 (하드웨어):

NX Horizon™ : 주력 제품입니다. 태양광 패널이 태양의 움직임을 따라 동쪽에서 서쪽으로 함께 움직이도록 하여(최대 120°), 고정식 대비 발전 효율을 최대 25%까지 높입니다. 또한 설치가 빠르고 쉬우며 탄소배출을 35%까지 줄입니다.

NX Gemini™ : 2개의 패널을 세로로 장착하는 양면형 트래커로, 지형 활용도를 높이고 발전량을 더욱 극대화합니다.

NX Horizon Low carbon™ : 최대 42%의 탄소 배출을 줄인 제품입니다.

NX Horizon – XTR™ : 이 제품은 한마디로 '험지(All-Terrain) 정복용'트래커입니다. NX Horizon 기반 평지 외의 지형에 설치할 수 있도록 특화시킨 모델

**XTR 모델의 가치**

기존 태양광 트래커는 완벽한 ‘일직선’으로 설치되어야 합니다. 따라서 평지가 아니면 대규모 토목 공사를 통해서 땅을 평지로 만들어야 하는 비용과 시간이 발생하고, 환경을 훼손하며, 프로젝트 허가를 어렵게 만듭니다.

그러나 XTR 모델의 Terrain-Following기술을 통해 자연적인 지형 굴곡을 그대로 따라가며 설치할 수 있습니다.

즉, 이 모델 하나로 CAPEX 절감, 프로젝트 리스크 감소, 환경 보호를 얻어 낸 셈입니다.

주요 제품 (소프트웨어):

TrueCapture™ : AI와 머신러닝을 기반으로 개별 트래커를 최적으로 제어하는 소프트웨어입니다. 지형의 그림자나 구름 등으로 인한 발전 손실을 최소화하여 발전량을 추가로 2~6%가량 향상시킵니다.

**TrueCapture™의 가치**

① 음영 회피 (Row-to-Row Optimization)

문제점 : 아침과 저녁 시간에는 앞줄의 패널이 뒷줄에 그림자(음영)를 만듭니다.또한,부지가 평평하지 않

고 울퉁불퉁하거나 경사진 경우(NX Horizon-XTR™이 설치된 곳)에도 패널 간에 그림자가 생겨 발전 효율이 떨어집니다.

TrueCapture™의 해결책 : 각 열의 각도를 개별적으로 미세하게 조정(Backtracking)하여,앞줄이 뒷줄에 그림자를 드리우는 것을 실시간으로 피하게 만듭니다. 이를 통해 기존 트래커라면 손실되었을 아침/저녁 시간의 발전량을 확보합니다.

② 확산광 최적화 (Diffuse Light Optimization)

문제점 : 날씨가 흐리거나 안개가 낀 날에는 태양의 직사광선은 거의 없고 하늘 전체에서 비추는 '확산광'만 존재합니다.이런 날에도 일반 트래커는 해의 위치를 따라가느라 비효율적인 각도를 유지합니다.

TrueCapture™의 해결책 : TrueCapture™는 날씨 데이터를 통해 확산광 조건임을 인지합니다.이때,패널을하늘을 향해 더 평평하게(수평에 가깝게) 눕혀분산된 빛을 최대한 많이 받아들일 수 있도록 각도를 최적화합니다.

NX Navigator™ : 발전소 운영 및 유지보수(O&M)를 원격으로 모니터링하고 제어하는 플랫폼입니다.

1

6

303

23 Oct 2025

$NXT | Nextracker 2. Çeyrek 2026 Kazanç Özetleri

🔹 Düzeltilmiş Hisse Başına Kazanç: 1,19 $ (Tahmini 0,63 $) 🟢; Yıllık # artış

🔹 Gelir: 905 milyon $ (Tahmini 679 milyon $) 🟢; Yıllık B artış

🔹 Düzeltilmiş FAVÖK: 224 milyon $; Yıllık ) artış

🔹 Düzeltilmiş Brüt Kar Marjı: 3,1 (yıllık 5,9'a kıyasla)

2026 Mali Yılı Beklentisi (Arttırıldı)

🔹 Gelir: 3,275 milyar $ - 3,475 milyar $ (Tahmini 3,39 milyar $) 🟢

🔹 Düzeltilmiş EPS: 4,04-4,25 ABD Doları (Tahmini 4,20 ABD Doları) 🟡

🔹 Düzeltilmiş FAVÖK: 775 Milyon ABD Doları-815 Milyon ABD Doları

🔹 GAAP EPS: 3,26-3,46 ABD Doları

Operasyonel Öne Çıkanlar

🔹 Rekor Birikmiş İş: >5 Milyar ABD Doları (şimdiye kadarki en yüksek)

🔹 Lansman: NX PowerMerge™ (eBOS ana hat konnektörü) — Bentek'te rekor siparişler

🔹 Satın Alma: Gelişmiş modül çerçeve teknolojisi için Origami Solar; çoklu GW tedarik anlaşması imzalandı

🔹 Yeni Ortak Girişim: Abunayyan Holding ile Nextracker Arabia (MENA'da genişliyor)

🔹 Rekor Sipariş Sayısı: Avrupa'da, temel çözümleri ve TrueCapture® verim sistemi

CEO Yorumu (Dan Shugar)

🔸 "İzleme sistemlerimize yönelik küresel talep güçlü kalmaya devam ediyor ve rekor birikmiş iş ve büyümeyi destekliyor."

🔸 "Bugüne kadar 150 GW'ın üzerinde sevkiyat gerçekleştirdik ve Avrupa ve Orta Doğu genelinde büyümeye devam ediyoruz."

CFO Yorumu (Chuck Boynton)

🔸 "Bilançomuz oldukça sağlam: 845 milyon dolar nakit, sıfır borç ve büyümeyi desteklemek için 1 milyar dolarlık yeni bir kredi imkanı."

2

5

745

23 Oct 2025

$NXT | Nextracker Q2’26 Earnings Highlights

🔹 Adj. EPS: $1.19 (Est. $0.63) 🟢; 23% YoY

🔹 Revenue: $905M (Est. $679M) 🟢; 42% YoY

🔹 Adj. EBITDA: $224M; UP 29% YoY

🔹 Adj. Gross Margin: 33.1% (vs. 35.9% LY)

FY26 Guidance (Raised)

🔹 Revenue: $3.275B–$3.475B (Est. $3.39B) 🟢

🔹 Adj. EPS: $4.04–$4.25 (Est. $4.20) 🟡

🔹 Adj. EBITDA: $775M–$815M

🔹 GAAP EPS: $3.26–$3.46

Operational Highlights

🔹 Record Backlog: >$5B (highest ever)

🔹 Launched: NX PowerMerge™ (eBOS trunk connector) — record bookings at Bentek

🔹 Acquisition: Origami Solar for advanced module frame tech; signed multi-GW supply deal

🔹 New JV: Nextracker Arabia with Abunayyan Holding (expanding in MENA)

🔹 Record Bookings: In Europe, foundation solutions, and TrueCapture® yield system

CEO Commentary (Dan Shugar)

🔸 “Global demand for our tracker systems remains strong, driving record backlog and growth.”

🔸 “We’ve shipped over 150GW to date and continue to expand across Europe and the Middle East.”

CFO Commentary (Chuck Boynton)

🔸 “Our balance sheet is rock solid — $845M cash, no debt, and a new $1B credit facility to support growth.”

2

8

50

12,592

15 Oct 2025

Stock Spotlight: $NXT (Nextracker Inc)

$NXT is up 153% YTD, hitting all-time highs and sits #1 in the Solar category on the Finvest Scorecard.

Why it stands out:

- Blowout earnings: Revenue and EPS both crushed estimates, backed by a $4.7B backlog and rising margins.

- IRA tailwinds: Capturing Advanced Manufacturing Tax Credits via its US onshoring strategy, boosting profitability.

- Global expansion: Secured a 1.5 GW project in Brazil and continues to scale its presence across emerging solar markets.

- Innovation edge: Integrating AI and robotics into its TrueCapture tracker system to maximize solar output.

- Analyst momentum: Upgraded to “Buy” by multiple firms and some see targets as high as $110.

With clean energy demand accelerating and policy tailwinds at its back, Nextracker is powering the next leg of the solar supercycle.

Is $NXT becoming the go-to name for investors betting on the global energy transition? Check out the scorecard on the Finvest app to discover such hidden gems.

2

463

13 Aug 2025

Via CleanTechnica: " Casa dos Ventos Selects Nextracker for 1.5 GW of Solar Projects in Brazil: NX Horizon-XTR™ solar tracking and TrueCapture® yield management and control system selected for performance and reliability in… dlvr.it/TMSNL2 " #Renewable #Energy

1

2

92

29 Jul 2025

Nextracker $NXT expands into AI and Robotics

Nextracker also announced two previously undisclosed complementary acquisitions:

🔹SenseHawk IP (Aug 2024): AI-powered drone tech that creates high-res 3D maps of solar sites to improve commissioning and optimize performance via tools like TrueCapture®.

🔹Amir Robotics (Mar 2025): Waterless robotic cleaning system for large-scale solar, designed to reduce soiling losses and integrate with Nextracker’s data platform—now in commercial trials.

8

549

28 Jul 2025

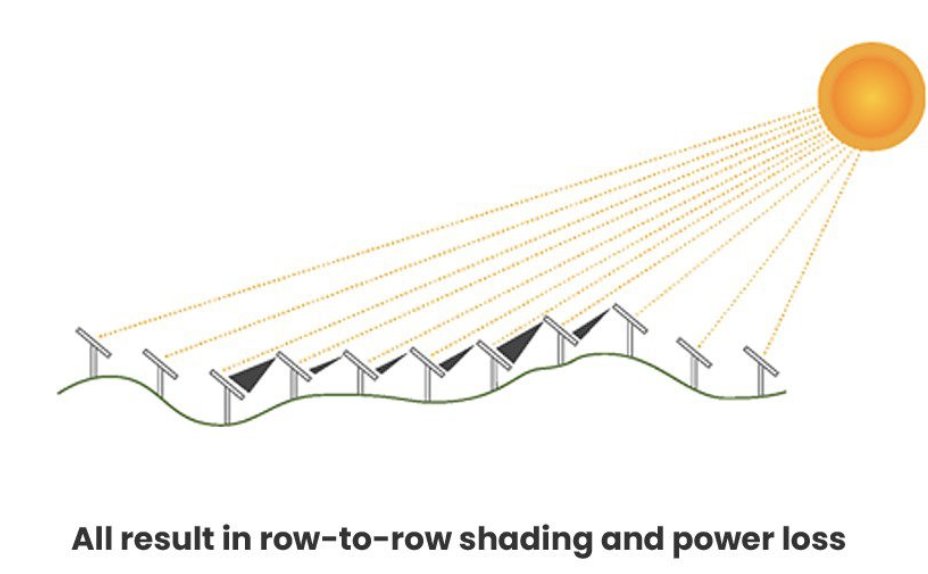

2. Nextracker- $NXT

A major issue in utility-scale solar projects is that many plants underperform expectations due to terrain-related shading. Hills, slopes, and nearby obstacles often reduced how much sunlight a panel can capture, leading to lower energy yields, and therefore, lost revenue. See the image below for an illustration on how the terrain can affect shading over the panels, which is where the Nextrackers’ optimization comes in.

Nextracker is solving this with its AI empowered software that adjusts each solar panel, in real time, based on the terrain and weather conditions. Their TrueCapture platform helps maximize output by optimizing panel angles across the entire field.

By addressing this issue, Nextracker is helping solar operators achieve higher energy yields, and maximizing profits. Their TrueCapture platform typically delivers up to 6% more energy output, a massive gain in efficiency for utility-scale projects.

1

3

1,550

6 Jul 2025

Bu hafta sonuna özel ABD borsalarında birkaç şirketten kısaca bahsedeceğim bunlar kendi çalışmalarım olup sadece şirketleri tanıma amaçlıdır...

Bakış açısı kazanma amaçlı;

Güncel yurtdışı portföyüm totalin u oranında zamanla artacaktır...

Güncel portföy hisselerim

$UNH

$NVO

Fırsat, analiz ve nakit buldukça yeni bir şeyler bakıyorum...

İlk şirket $PRM

Perimeter Solutions (NYSE: PRM), iki güçlü segmentte yer alıyor:

Yangın önleme: Orman yangınlarına yönelik PHOS-CHEK® retardantlar, SOLBERG™ köpük ürünleri ve ekipmanlar. Devlet kurumları, hava tanker üsleri ve endüstriyel müşterilere kritik çözümler sunuyor

Özel ürünler: Fosfor pentasülfür tabanlı yağ katkıları (motor yağı, tarım, madencilik) ve yeni nesil batarya kimyasalları

Market Cap: ~1,5 milyar USD

Borç/Özkaynak oranı: ~0,55–0,57

Q1 2025 hasılat büyümesi: 22% YoY, gelir 72 m USD; EPS $0,38 (önceki -$0,57)

Brüt Marj: ~39% — sektörün oldukça üzerinde

P/E: ~15,8× (endüstri ortalamasının altında, potansiyel değer)

P/S: ~3,6× (nispeten yüksek satış değerlemesi)

Kurumsal Alım: hissedar WindAcre, 1 Temmuz’da 254,600 hisse ($3,56M) aldı – talep sinyali

Bilanço GüçlendiQ1 sonuçları, gelir büyümesi, kâra dönüş ve yüksek FAVÖK marjları hissede pozitif hava yarattı.

Analist Tavsiyeleri: @ZacksResearch Buy”, @UBS “Buy” gibi yükseltmeler öne çıktı

Teknik KırılımSon 3 gün içinde %8–8,5 yükselme, yeni rekor seviyeler test edildi

Q2 yakın takip edilecek

İnsider alış satışları yakın takip edilecek

Teknik bir kırılımla önümüzde olduğu için 14,4 altı kapanışlar riskli alan

İkinci şirket: $NXT

İş Modeli

Nextracker, utility–ölçekli güneş enerji santralleri için tek eksenli güneş takip sistemleri ve akıllı kontrol yazılımları geliştiriyor:

NX Horizon, NX Gemini gibi tracker’lar güneş panellerini gün içinde güneşin takip etmesini sağlıyor.

TrueCapture ve NX Navigator sistemleri ise enerji üretimini maksimize etmek amacıyla rüzgar ve hava durumu verisiyle panel açılarını dinamik olarak ayarlıyor

Piyasa Değeri & Finansal Güç

Market Cap: ~9,8 milyar USD

Borç: Yok (debt-to-equity = 0%)

Nakit: ~766 m USD, güçlü likidite

Senato yasasında vergi teşvikleri: Güneş paneli teknolojileri için uygulanan vergi cezası kaldırılınca, güneş hisselerine pozitif yansıdı; NXT haftalık yükselişle IBD "Stock of the Day" ilan edildi

Q2 FY25 net bilanço açıklamaları: Güçlü satış ve kâr büyümesi gözlemlendi; gross margin 35%, FAVÖK marjı ' civarı

Kurumsal güven: Insiderlar net $119M alım, $91.9M satış yaptı; ortalamada pozitif sinyal görülüyor .

Değerleme Oranları

P/E: ~19×, daha önce ~16–17× aralığındaydı .

EV/EBITDA: ~11.7×

ROE / ROA: 9 / ; endüstri liderliği gösteriyor .

Gelecek Vizyonu

Fırsatlar: Ultra düşük maliyetli, AI destekli low‑carbon tracker teknolojileri sayesinde enerji verimliliğinde lider pozisyon. Yeni ürünler (eBOS, Ojjo, Bentek) tedarik zincirine değer katıyor

Riskler: Hissedar satışları (startup liderleri); hızla yükselen fiyatlarda düzeltme riski; sektördeki teşvik yönetimleri etkileyici olabilir.

62 dolar seviyesinin altında kapanış almadıkça takipteyim.

Üçüncü şirket: $OLO

Olo Inc., restoran markalarına dijital sipariş, ödeme ve müşteri iletişim altyapısı sunan bir B2B SaaS platformudur.

750 restoran markasını, 88.000 lokasyonda destekliyor (Denny’s, P.F. Chang’s, Shake Shack, Cold Stone)

Restoranların kendi uygulama/website siparişlerini üçüncü taraf platformlardan bağımsız şekilde almalarını sağlar.

Ek hizmetler: Olo Pay, analytics, müşteri ilişkileri yönetimi, entegrasyon çözümleri

Market Cap: ~1,7 milyar USD

Enterprise Value (EV): ~1,35 milyar USD

EV/Revenue: ~4,5× – 4,7× (SaaS sektörü ortalamasının biraz üstünde)

EV/EBITDA: 57–73× (geçici düşük baz, EBITDA halen sınırlı)

P/E (TTM): ~518× (gelir yeni başlıyor), Forward P/E: ~32×

EV/FCF: ~40–51×

Thoma Bravo, Olo'yu ~2 milyar USD valuasyonla alacağını duyurdu

Potansiyeller:

Thoma Bravo'nun satın alma tamamlarsa, Olo “özel şirket” olarak büyümeye odaklanabilir.

SaaS pazarında güçlü konum: 88.000 lokasyon, global ölçek.

Analitik ve ödeme altyapısı gibi yan gelir alanları büyüme fırsatları sunuyor.

Riskler:

Satın alma gerçekleşmezse – piyasa değeri düzeltilebilir.

EBITDA halen düşük – kârlılık sürdürülmeli.

Rekabet: Third‑party delivery player’lar (DoorDash, UberEats) yeniden direkt altyap geliştirebilir.

9,2 dolar seviyesinin üzerinde kalmasını ve satın alım sürecini takip edeceğim.

Dördüncü ve son olarak $DDOG

Datadog, geliştiriciler ve BT ekipleri için bulut altyapı, uygulama performansı, güvenlik ve log analitiği sunan entegre bir SaaS platformudur.

Sunuculardan uygulamalara, veritabanlarından güvenliğe kadar altyapıyı tek bir panoda anlık izlemeyi sağlıyor.

Market Cap: Yaklaşık $47–52 milyar, bu değer S&P 500 girişini mümkün kılıyor !

S&P 500’e dahil ediliyor: 9 Temmuz’da Juniper Networks yerine alınacak

2024 Gelir: $2,7 milyar (Yıllık 26% büyüme) .

Şirket kârlı, GAAP net kâr açıklıyor — bunu yapabilen SaaS şirketi sayısı sınırlı .

Pasif fon girişleri: S&P 500 izleyen ETF ve fonların satın alma yapması bekleniyor .

Analist tepkileri: Wedbush, hedef fiyatı $170’a yükseltti ve “outperform” notunu korudu

P/S: ~6x, SaaS liderleri (Snowflake, CrowdStrike) ile karşılaştırıldığında hâlâ cazip

Net Marj: İlk çeyrekte %3.2 olarak yükseldi ve gross margin x seviyesinde

Gelişme Hızı: Yıllık 47% gelir büyümesi (Q1 bazında) .

9 temmuz tarihi ve pasif fon girişleri takip edilebilir.

Şu an için pahalı ancak bu iş modeli biraz yüksek çarpanlı fiyatlanıyor. burada bir düzeltme fırsat yaratabilir.

Investing pro AI de temmuz listesine ekledi.

Hisselerin haftalık grafiklerini aşağı bıraktım.

Arada sırada böyle yüzeysel analizler gelecek ama asıl $UNH gibi uzun vade portföyüne aldığım şirketlerde daha detaylı derin temel analizler gelecektir.

Okuyanların sabrına teşekkürler...

1

30

3,141