Jun 14

Struggling With WordPress? Try This in 2026 ⚡ elegantthemes.com/affiliates… #WordPressTips #EasyWebDesign #AIAssistant #OnlineBusiness #ContentTools #WebHelp

2

Jun 11

Merchants SA I hope you're taking notes sana lwam same applies to you Concentrix (Webhelp) babygirl.

2

189

Jun 8

Struggling With WordPress? Try This in 2026 ⚡ elegantthemes.com/affiliates… #WordPressTips #EasyWebDesign #AIAssistant #OnlineBusiness #ContentTools #WebHelp

5

May 25

par Allah jai commencer la toiture mon kho je goutte tellement y fait chaud jregrette webhelp et la clime

1

2

78

Tiens il ressort du bois celui-ci.

- Organisateur de cocktails dinatoires de Macron pour récupérer du blé

- Se créer un montage fiscale pour rapatrier son pognon à Londres

- Tout fier d'avoir tanner Macron pour supprimer l'ISF

- Corédige le rapport Webhelp

13 Jun 2019

THREAD sur le rapport @Webhelp_FR /@AltermindGroup remis à @GDarmanin fin Mars.

Il est présenté comme une généreuse contribution au "Grand débat national".

(on ne sait si ça été payé par le gouvernement, ça serait le pompon)

Le PDF ▶️static1.squarespace.com/stat…

1

12

37

1,787

Depuis webhelp tout le monde voyait ton taff même si y’avait aucune affinité !

Bonne chance Garçon 🔥

Connexion TRAP$HIT @Liims_pintero 🎱🤞🏾🩸🇨🇮 dans dos 🤫

1

1

27

1,817

En call centers bilingües tipo Teleperformance y Webhelp piden desde B2

1

2

353

Apr 13

Hiring manager was Unima Iqbal - For that matter ex #Webhelp n now #Concentrix - Vaseem Ahmad recruiting for WFM, asked HR to prioritise only Ms, n guess who told me - Salmaan Sheikh from South Africa - who sought action against this in 2022

1

2

182

Labour Court upholds dismissal of Webhelp worker for failing to notify manager of sick leave, ruling that even a medical certificate cannot excuse neglecting the duty to report ill health in advance.

#LabourLaw #SickLeave #WorkplaceDiscipline #CCMA

Read more here: tinyurl.com/3fy5bav5

2

4

1,443

Mar 15

Email us to have your flyer posted on our social media pages

webhelp@papalace.com

1

18

@qatarairways having the most ridiculous service during this period. Telling people to call the Qatar office for webhelp. So what is the use of in country offices?

4

202

Feb 9

C’est quand même admirable de voir qu’on a 3 champions mondiaux du service clients made in France:

👉 Teleperformance : env. 500.000 salariés monde

👉 Webhelp : env. 100.000 salariés (Concentrix)

👉 Foundever : 170.000 salariés monde

Bravo aux fondateurs et salariés - BPO

2

1

5

1,562

Jan 13

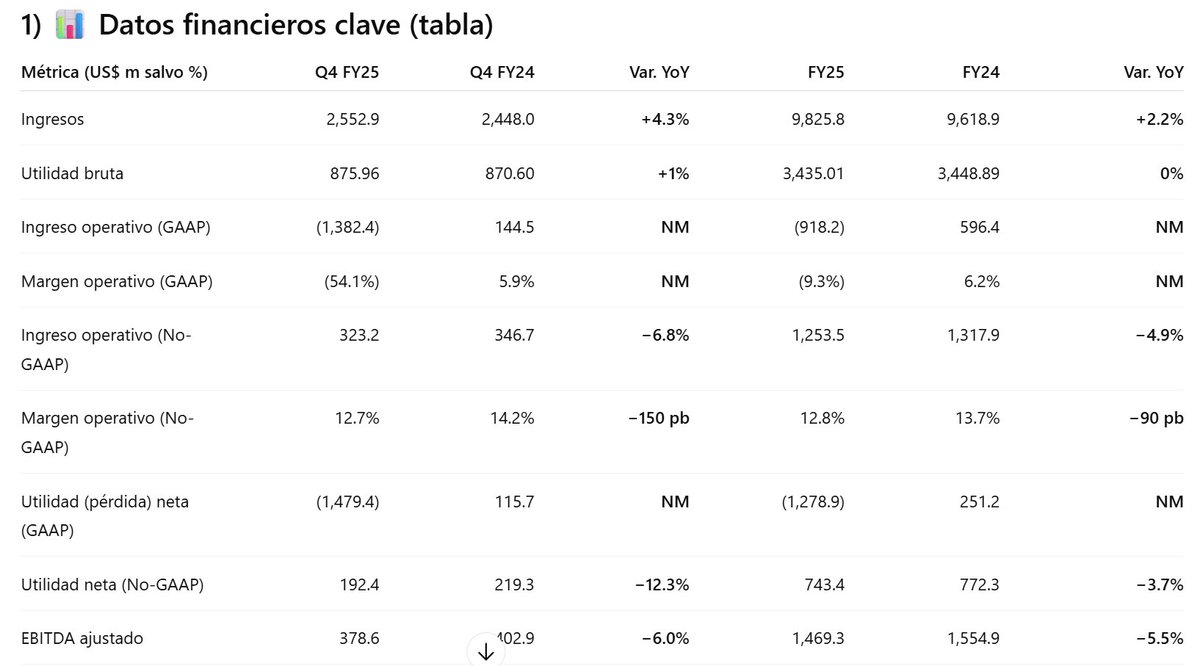

📈 Concentrix $CNXC

💰Resultados💰

💲Beneficios por Acción:

2,95 dólares Vs 2,91 dólares esperados. ✅

💵 Ingresos:

2,55 B Vs 2,54 B esperados. ✅

2) 🚀 Operaciones y estrategias de crecimiento

La compañía señala avances en soluciones de transformación inteligente y afirma entrar a 2026 con “la estrategia y el modelo adecuados para impulsar crecimiento y FCF” (CEO) .

Cartera diversificada por verticales: crecimiento en BFSI ( 12% YoY en Q4), Comunicaciones y media ( 8%) y Retail/Travel/e-commerce ( 4%); presión en Tecnología & electrónica (−2%) y Healthcare (−1%) .

3) 🧾 Análisis de costos y gastos

Impairment de goodwill (no caja) por US$1,527.7m en Q4, ligado al rango reciente de cotización y capitalización bursátil, afecta el resultado GAAP y márgenes reportados .

SG&A prácticamente plano en Q4 ( 1%), y −1% en el año; costo de ventas 6% en Q4 y 4% en FY, dejando utilidad bruta estable (Q4 1%) .

4) 📈 KPIs sectoriales

Ingresos por vertical (Q4 YoY): BFSI 12%, Comms & media 8%, Retail/Travel/e-comm 4%; Tech & consumer electronics −2%; Healthcare −1%; Otros 8% .

Concentración por vertical (FY): Tech & CE US$2.67bn, Retail/Travel/e-comm US$2.43bn, Comms & media US$1.59bn, BFSI US$1.54bn, Healthcare US$0.73bn, Otros US$0.87bn .

5) 💧 Liquidez y apalancamiento

Flujo de caja operativo récord FY25: US$807m; FCL ajustado US$626m; ambos por encima de FY24 según tablas de conciliación .

Efectivo al cierre: US$327m; deuda LP neta: US$4,573m; patrimonio: US$2,744m (descenso por el impairment contable) .

Deuda/finanzas: reducción de deuda neta en US$184m en FY25, manteniendo retornos al accionista en paralelo .

6) 🧭 Narrativa estratégica (cita traducida)

Chris Caldwell (Presidente y CEO): “Nuestros resultados del cuarto trimestre y del año reflejan el compromiso de avanzar el negocio para satisfacer la demanda cambiante de los clientes mientras entregamos valor a los accionistas… Entramos en 2026 bien posicionados para impulsar crecimiento y flujo de caja libre” .

7) 🔭 Proyecciones y orientación

Q1 FY26: ingresos US$2.475–2.500bn (crec. c/c 1.5%–2.5%), OI GAAP US$140–150m, OI No-GAAP US$290–300m, EPS No-GAAP US$2.57–2.69, tasa efectiva ~25% .

FY26: ingresos US$10.035–10.180bn (c/c 1.5%–3.0%), OI GAAP US$688–738m, OI No-GAAP US$1.24–1.29bn, EPS No-GAAP US$11.48–12.07, FCL ajustado ~US$630–650m; acciones diluidas asumidas ~60.6m; tasa efectiva ~25% .

8) 💸 Dividendo y retorno al accionista

Dividendo trimestral: US$0.36/acción (pagado el 4-nov-2025 y declarado para pago el 10-feb-2026) .

Recompras Q4: 1.3m de acciones por US$56.4m; remanente de autorización US$438.6m al 30-nov-2025. Retorno total FY25: US$258m entre dividendos y recompras; además, deuda neta −US$184m en el año .

9) ⚖️ Puntos positivos y negativos del trimestre

Positivos

Ingresos 4.3% en Q4 y 2.2% en FY, superando la guía de crecimiento c/c; CFO récord US$807m y FCL ajustado US$626m en el año .

Diversificación sectorial con fortaleza en BFSI y Comms & media; disciplina en costos operativos No-GAAP (márgenes todavía de doble dígito) .

Negativos

Impairment de goodwill US$1.52bn en Q4 provoca pérdidas GAAP y caída del patrimonio; margen No-GAAP se contrae 150–90 pb (Q4/FY) por mix/entorno de demanda .

Tecnología y Healthcare rezagados en Q4; sensibilidad a FX y a ejecución de integración (Webhelp) señalada en notas de No-GAAP y “safe harbor” .

10) 🧮 Opinión o calificación del desempeño

Lectura mixta-constructiva: crecimiento moderado y caja muy sólida, pero presión en márgenes No-GAAP y fuerte ajuste contable por goodwill. Con guía 2026 de crecimiento c/c y FCL al alza, asigno 7/10 (fundamentos operativos estables; foco en expansión rentable y desapalancamiento) .

11) 🧠 Resumen conciso y puntos clave

Concentrix cerró 2025 con ingresos US$9.83bn ( 2.2%), No-GAAP OI US$1.25bn (12.8% margen) y FCL ajustado récord US$626m, mientras que un impairment de goodwill (US$1.52bn) llevó a pérdida GAAP. En Q4, ingresos 4.3% y No-GAAP EPS US$2.95. La demanda repunta en BFSI y Comms, se mantiene más débil en Tech y Healthcare. Para 2026, guía de ingresos US$10.0–10.2bn, No-GAAP EPS US$11.48–12.07 y FCL ajustado ~US$630–650m, con continuidad de dividendos y recompras selectivas mientras reducen deuda neta .

12) ✅ Cierre

No olvides seguirme en mi cuenta X para mantenerte al tanto de los mercados financieros 👉 x.com/IngJuanPa7

1

2

19

3,465

Jan 13

$CNXC Q4 2025 earnings: Top-Line Acceleration Overshadowed by $1.5B Impairment

Concentrix delivered its strongest revenue growth of the fiscal year in Q4 ( 4.3% reported, 3.1% constant currency), beating the top end of its guidance. However, the report is dominated by a massive $1.52 billion non-cash goodwill impairment charge, driven by the company's depressed stock valuation, which swung GAAP results to a $1.48 billion loss. Operationally, profitability deteriorated: Non-GAAP operating margin compressed 150 basis points YoY to 12.7%, and Non-GAAP EPS fell 9.5%. While the FY26 outlook promises continued growth, the divergence between rising sales and shrinking margins remains a key friction point.

🐂 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗠𝗼𝗺𝗲𝗻𝘁𝘂𝗺 𝗕𝘂𝗶𝗹𝗱𝗶𝗻𝗴: Top-line growth has accelerated for three consecutive quarters, moving from 1.3% (CC) in Q1 to 3.1% in Q4. FY26 guidance calls for continued expansion ( 1.5% to 3.0% CC), suggesting the demand environment is stabilizing.

𝗦𝘁𝗿𝗼𝗻𝗴 𝗕𝗙𝗦𝗜 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲: The Banking, Financial Services, and Insurance segment surged 12% YoY, a significant acceleration that offset weakness in Tech. This vertical mix shift suggests Concentrix is winning in complex, high-value regulatory environments.

🐻 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

𝗣𝗿𝗼𝗳𝗶𝘁𝗮𝗯𝗶𝗹𝗶𝘁𝘆 𝗗𝗲𝘁𝗲𝗿𝗶𝗼𝗿𝗮𝘁𝗶𝗼𝗻: Non-GAAP operating margins fell 150bps YoY in Q4. More concerning is the FY26 guidance: the midpoint implies an operating margin of ~12.5%, down from FY25's 12.8% and FY24's 13.7%. Operating leverage is moving in the wrong direction.

𝗠𝗮𝘀𝘀𝗶𝘃𝗲 𝗚𝗼𝗼𝗱𝘄𝗶𝗹𝗹 𝗜𝗺𝗽𝗮𝗶𝗿𝗺𝗲𝗻𝘁: Management booked a $1.52B impairment charge, admitting the market capitalization does not support the carrying value of past acquisitions (likely Webhelp). While non-cash, it is a severe admission of value destruction.

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

🔴 Bearish. While revenue acceleration is a positive signal, the substantial margin degradation and the $1.5B impairment charge indicate structural issues. The company is growing sales but becoming less profitable per dollar earned, and FY26 guidance does not forecast a return to margin expansion.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀

New: 🔴🔴 $𝟭.𝟱𝟮 𝗕𝗶𝗹𝗹𝗶𝗼𝗻 𝗚𝗼𝗼𝗱𝘄𝗶𝗹𝗹 𝗜𝗺𝗽𝗮𝗶𝗿𝗺𝗲𝗻𝘁

Concentrix recorded a $1.52 billion non-cash goodwill impairment charge in Q4. Management explicitly cited the 'trading range for the Company’s stock price and market capitalization' as the primary trigger. This wiped out full-year GAAP earnings, resulting in a $1.28 billion net loss for FY25. This signals that the premiums paid for past acquisitions (Webhelp) are not being recognized by the public market.

🔴 𝗠𝗮𝗿𝗴𝗶𝗻 𝗖𝗼𝗺𝗽𝗿𝗲𝘀𝘀𝗶𝗼𝗻 𝗧𝗿𝗲𝗻𝗱

Profitability metrics are deteriorating. Non-GAAP operating margin dropped from 14.2% in 24Q4 to 12.7% in 25Q4. Adjusted EBITDA margin similarly compressed from 16.5% to 14.8%. The company faces negative operating leverage, likely due to competitive pricing pressures, mix shift, or elevated investment costs that are not yet yielding efficiency gains.

🟢 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗦𝗲𝗿𝘃𝗶𝗰𝗲𝘀 (𝗕𝗙𝗦𝗜) 𝗣𝗼𝘄𝗲𝗿𝗶𝗻𝗴 𝗚𝗿𝗼𝘄𝘁𝗵

The BFSI vertical is the standout performer, accelerating to 12% YoY growth in Q4 (up from flat/low growth earlier in the year). Comms & Media also posted strong 8% growth. These segments are successfully offsetting declines in the tech sector.

⚪ 𝗧𝗲𝗰𝗵 & 𝗛𝗲𝗮𝗹𝘁𝗵𝗰𝗮𝗿𝗲 𝗟𝗮𝗴𝗴𝗶𝗻𝗴

Two key high-value verticals remain in contraction. Technology and Consumer Electronics revenue fell 2% YoY, and Healthcare declined 1%. Since these are typically higher-margin segments than Retail or Media, their underperformance likely contributes to the overall margin compression.

🟢 𝗦𝗼𝗹𝗶𝗱 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 𝗖𝗼𝗻𝘃𝗲𝗿𝘀𝗶𝗼𝗻

Despite the GAAP loss, cash generation remains a bright spot. FY25 Adjusted Free Cash Flow reached $626 million, landing within the guidance range ($625-650M). FY26 guidance projects further growth to $630-650M, ensuring the dividend and buyback programs remain funded.

— • — • —

𝗢𝘁𝗵𝗲𝗿 𝗞𝗣𝗜𝘀

𝗡𝗼𝗻-𝗚𝗔𝗔𝗣 𝗘𝗣𝗦 (𝟮𝟱𝗤𝟰): $𝟮.𝟵𝟱

Decelerating. Decreased 9.5% YoY from $3.26 in 24Q4. Despite revenue growing 4.3%, earnings power declined significantly due to margin compression and higher tax/interest implications relative to operating income.

𝗥𝗲𝘃𝗲𝗻𝘂𝗲 (𝟮𝟱𝗤𝟰): $𝟮,𝟱𝟱𝟯 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Accelerating. Up 4.3% reported and 3.1% constant currency. This beat the company's previous guidance range ($2,525-2,550M) and marks the highest quarterly growth rate of FY25.

𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗥𝗲𝘁𝘂𝗿𝗻𝘀 (𝗙𝗬𝟮𝟱): $𝟮𝟱𝟴 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Stable. The company returned $258M to shareholders via dividends ($90M estimated) and buybacks ($168M estimated), while reducing net debt by $184M. Buyback authorization has $438.6M remaining.

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

𝟮𝟲𝗤𝟭 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $𝟮.𝟰𝟳𝟱 - $𝟮.𝟱𝟬𝟬 𝗯𝗶𝗹𝗹𝗶𝗼𝗻

Decelerating. Implies 1.5% to 2.5% constant currency growth, slightly lower than the 3.1% CC growth achieved in 25Q4. Includes a ~290bps positive FX impact.

𝟮𝟲𝗤𝟭 𝗡𝗼𝗻-𝗚𝗔𝗔𝗣 𝗘𝗣𝗦: $𝟮.𝟱𝟳 - $𝟮.𝟲𝟵

Decelerating. The midpoint ($2.63) represents a ~10% decline YoY vs 25Q1 ($2.79) and a 4% decline vs 24Q1 ($2.75). Profitability continues to face headwinds.

𝟮𝟲𝗙𝗬 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $𝟭𝟬.𝟬𝟯𝟱 - $𝟭𝟬.𝟭𝟴𝟬 𝗯𝗶𝗹𝗹𝗶𝗼𝗻

Stable. Implies 1.5% to 3.0% constant currency growth, generally consistent with the exit rate of FY25. Shows continued modest organic expansion.

𝟮𝟲𝗙𝗬 𝗡𝗼𝗻-𝗚𝗔𝗔𝗣 𝗘𝗣𝗦: $𝟭𝟭.𝟰𝟴 - $𝟭𝟮.𝟬𝟳

Accelerating. Midpoint ($11.78) implies ~5% growth over FY25 ($11.22), though this is primarily driven by revenue scale rather than margin expansion, as implied operating margins remain flat/down.

— • — • —

𝗞𝗲𝘆 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀

𝗜𝗺𝗽𝗮𝗶𝗿𝗺𝗲𝗻𝘁 𝗧𝗿𝗶𝗴𝗴𝗲𝗿 𝗗𝗲𝘁𝗮𝗶𝗹𝘀

The $1.52B impairment is massive. Beyond the stock price, has there been a fundamental change in the long-term cash flow assumptions for the legacy Webhelp business or other reporting units?

𝗠𝗮𝗿𝗴𝗶𝗻 𝗖𝗼𝗺𝗽𝗿𝗲𝘀𝘀𝗶𝗼𝗻 𝗥𝗼𝗼𝘁 𝗖𝗮𝘂𝘀𝗲

Non-GAAP operating margins compressed 150bps YoY in Q4. Is this primarily pricing pressure in the Tech vertical, or are there one-time integration/AI investment costs that will roll off in FY26?

𝗧𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝘆 𝗩𝗲𝗿𝘁𝗶𝗰𝗮𝗹 𝗧𝘂𝗿𝗻𝗮𝗿𝗼𝘂𝗻𝗱

The Technology segment remains negative (-2%). When do you expect this vertical to stabilize, and are AI-agent headwinds impacting volumes in this specific cohort?

𝗙𝗬𝟮𝟲 𝗠𝗮𝗿𝗴𝗶𝗻 𝗕𝗿𝗶𝗱𝗴𝗲

Guidance implies FY26 operating margins of ~12.5%, which is below FY25's 12.8%. Why is operating leverage negative despite projected revenue growth of up to 3%?

3

897

Jan 11

kızlar bir yıl webhelp diye bir şirkette çalıştım başımdaki cadaloz hamileyken hakkım olan şeyler yaptım diye içerlemiş. başıma bela oldu istifa edene kdr. yani bence ayrıcalıklardan dolayı gevşetilen kuralların hepsi sindirilebiliyor.

2

92

15 Dec 2025

Funny enough my first job was a post you made somewhere around 2023 applied got an interview passed worked there for 1 and half years before exploring other opportunities. One of the best companies I have worked with. Webhelp Ghana now Concentrix Ghana. Big ups✌️😊

1

2

18

1,475

15 Dec 2025

🏭 Manufacturing & FMCG

1. Tiger Brands

tigerbrands.com/careers/

2. Pioneer Foods

pioneerfoods.co.za/careers/

3. AVI Limited

avi.co.za/careers/

4. Unilever South Africa

unilever.co.za/careers/

5. Clover South Africa

clover.co.za/Careers

---

🧹 Waste, Cleaning & Municipal Services

6. Pikitup Johannesburg

johannesburg.gov.za/about_/P…

7. Averda South Africa

averda.com/careers

8. EnviroServ

enviroserv.co.za/careers/

9. WastePlan

wasteplan.co.za/careers/

10. Interwaste

interwaste.co.za/careers/

---

🧾 Call Centres & BPO

11. Teleperformance South Africa

jobs.teleperformance.com/en-…

12. Webhelp South Africa

jobs.webhelp.com/

13. CCI South Africa

cci-global.com/careers/

14. Merchants (BPO)

merchants.co.za/careers/

15. iContact BPO

icontactbpo.com/careers/

---

🚜 Agriculture & Food Production

16. Astral Foods

astralfoods.com/careers/

17. RCL Foods

rclfoods.com/careers/

18. ZZ2 Farming

zz2.co.za/careers/

19. Westfalia Fruit

westfaliafruit.com/careers

20. TWK Agri

twkagri.com/careers

---

🏪 Franchises & Fast Food

21. KFC South Africa

kfc.co.za/careers

22. McDonald’s South Africa

mcdonalds.co.za/careers

23. Debonairs Pizza

debonairspizza.co.za/careers

24. Pizza Hut South Africa

jobs.pizzahut.co.za/

25. Steers / Famous Brands

famousbrands.co.za/careers/

---

🧑🔧 General Labour, Staffing & Learnerships

26. Adcorp Group

adcorp.co.za/careers/

27. Workforce Staffing

workforcestaffing.co.za/care…

28. Quest Staffing Solutions

quest.co.za/careers/

29. Kelly South Africa

kelly.co.za/careers/

30. ManpowerGroup South Africa

manpowergroup.co.za/careers/

---

🏢 Property, Malls & Real Estate

31. Growthpoint Properties

growthpoint.co.za/careers/

32. Redefine Properties

redefine.co.za/careers/

33. Hyprop Investments

hyprop.co.za/careers/

34. Excellerate JHI

excelleratejhi.com/careers/

35. Broll Property Group

broll.com/careers/

2

3

1,202

29 Nov 2025

QSALES – Ett av de mest spännande early-tech casen i sales-AI just nu🔥

Säljvärlden står inför sin största revolution på 20 år. Säljare globalt sitter fast i gamla arbetssätt: dyra coacher, kurser och metoder som inte skalar.

QSALES förändrar allt – och det är $QBIM som ligger bakom revolutionen.

QSALES levererar långt mer än bara coaching. Det är säljarens AI-motor som ger personlig realtidscoaching, smarta scripts, förhandlingstips, lead-analys, retorikförbättring, CRM-stöd, auto-sammanfattningar, invändningshantering, closing-strategier och “next best action” i samma verktyg. Till och med AI-rollspel för att träna säljsamtal.

Men den verkliga kraften kommer över tid. QSALES bygger en datamotor som lär sig exakt vad som fungerar: vilka argument som konverterar, vad toppsäljarna gör annorlunda, hur pipen rör sig, vilka deals som riskerar att dö och hur man kan förutsäga intäkter med precision. Ramp-up-tiden för nya säljare sjunker drastiskt och kunskap stannar kvar i organisationen även när personal slutar.

För chefer och beslutsfattare innebär QSALES total överblick i realtid, objektiv performance-data, AI-genererade förbättringsplaner, bättre beslut, mindre magkänsla och en säljorganisation som äntligen går att skala utan att kostnaderna skenar.

AI tar nu över marknaden för:

✔️ Säljutbildning

✔️ Coaching

✔️ Performance

✔️ Lead scoring

✔️ Pipeline-optimering

Och QSALES är verktyget som driver hela skiftet — inte “ett steg före”, utan motorn som sätter standarden.

Vem kommer använda QSALES?

Alla med stora säljteam och konstant onboarding:

– Teleoperatörer (Telia, Tele2, Telenor, Tre...)

– Bilhandlargrupper (Hedin, Bilia, Kamux...)

– Fastighetsmäklare (MOHV, Bjurfors, Notar...)

– SaaS & techbolag (Upsales, Voyado, Pipedrive...)

– B2B-tech & åf (Siemens, Dustin, Atea, Advania)

– Industri & teknik (Schneider Electric, Siemens...)

– Logistik & transport (DHL, Schenker, PostNord...)

– Finans & försäkring (SEB, Nordea, Svedea...)

– Energi & elbolag (Fortum, E.ON, Skellefteå Kraft..)

– Mediebolag (Schibsted, Bonnier News...)

– Callcenter & kundtjänst (Webhelp, Transcom...)

– Bemanning & Rek (Academic Work, Manpower...)

Vi går mot en tid där varje säljare har en AI-partner.

Det här är CRM-revolutionen igen – men 10× större.

QSALES är tidigt men har potential att bli standardverktyget i hela säljbranschen.

Och bakom allt?

QBIM – fortfarande okänt för många investerare, men bygger teknologi som kan bli obligatorisk i framtidens säljorganisationer.

AI Sales = Ett av de hetaste områdena 2025.

QSALES är inte ännu ett AI-verktyg – det är säljarens nya motor.

#QBIM #QSALES @kalqyl @TradeVenue @MiljonarInnan30 #SpectrumOne

1

3

8

1,843

25 Nov 2025

🔄Grégoire Heuzé débauche une figure de l’investissement comme senior advisor

Altamoda, sa boutique, qui compte une petite vingtaine de banquiers, a déjà conseillé Webhelp, Ardian et Nissan. Révélations @aroun_benhaddou

▶️l.linforme.com/jpfu6nr6

2

511

16 Nov 2025

🤦♂️Ce qui a mal tourné : les signaux d’alerte ignorés

Au fil des mois, la thèse a été mise à mal par une série d’événements. D’abord, le management ne s’est jamais rendu à l’évidence que l’IA prenait des parts de marché à l’entreprise. Le PDG est le premier commercial de l’entreprise, et n’admettra probablement pas que son entreprise est en train d’être disruptée.

En 2023, Teleperformance a réagi à une consolidation du secteur. Leur concurrent principal, Concentrix (numéro 2 du marché), a racheté Webhelp pour devenir leader.

2

3

252