COMPUTEX 2026 Recap! An amazing week filled with innovation, collaboration, and great conversations. Thank you to everyone who visited the DeepCool booth and joined us as we unveiled our latest products and future vision. See you next year, Taipei.🥰

#deepcool #computex #computex2026 #pccooler #gamingpc

22

カニ retweeted

Jun 12

デスク環境や手持ちのデバイス、COMPUTEXなどのイベント写真を投稿できるサイトを運営しています!

投稿数がまだまだ少なく、もしよければ投稿に協力していただけませんか😭

5

13

64

16,659

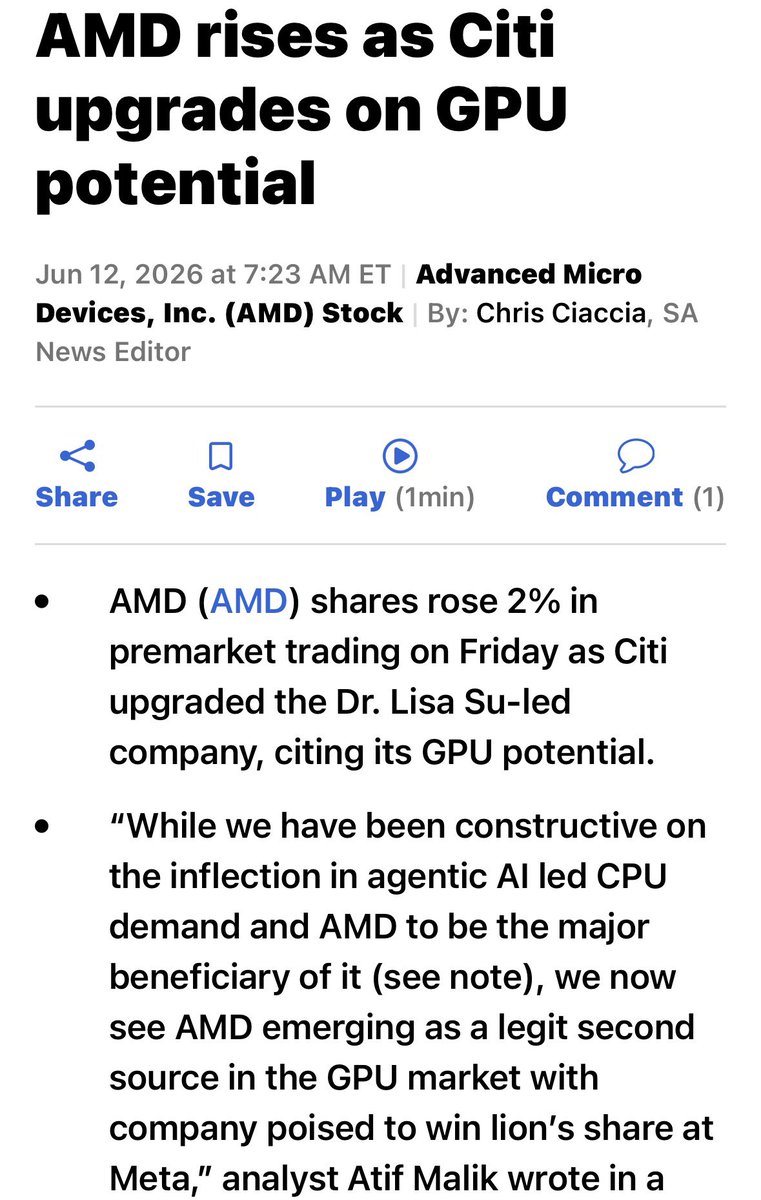

$AMD

Citi 將 $AMD 的投資評等從「中立」調升至「買進」,並將目標價從 460 美元大幅上調至 575 美元,調升評等主因是看好該公司在 GPU 市場的潛力,並由 Dr. Lisa Su 帶領團隊持續推進。

雖然我們此前一直對代理型 AI(Agentic AI)所帶動的 CPU 需求拐點持建設性看法,並預期 $AMD 將成為主要受益者,但我們現在更看到 $AMD 正崛起成為 GPU 市場中極具競爭力的第二供應來源,且該公司有望贏得 Meta 的絕大部分訂單。

在我們看來,大多數投資人目前仍將 $AMD 視為單純的 CPU 股票,且現階段股價僅反映了 $AMD 在 2028 年前實現超過 500 億美元 GPU 銷售額約 60% 的可能性。

此外,在 Computex 結束後,我們將 2030 年 CPU 的TAM 模型從先前的 1,320 億美元上調至 1,370 億美元。

憑藉其效能領先優勢、更多核心數、X86 架構、更廣泛的產品線,以及對多執行緒與單執行緒的全面支援,我們依然預期 $AMD 將成為這波 CPU 復興浪潮中的核心受益者。

1

190

Wildcat Lake-laptops op Computex: Wie kan op tegen de MacBook Neo? tweakers.net/reviews/14830/w… 😍 ASUS Vivobook S14 ✅️ 😍

12

The ASUS booth at Computex 2026 created quite the media buzz. The star attraction? The new NVIDIA processor-powered ProArt P16 and P14 creator workstations! Visit the ASUS Blog to learn more!

22

72

515

8,328,766

59m

📈US markets stage violent V-bottom as tech repairs early losses and the Russell 2000 surges 3.93% ahead of a major Fed policy regime shift. $SPY $IWM $SPCX youtu.be/GpKqD_1ubzI

The trading week ending June 12, 2026, delivered a classic dip-and-repair profile. Early-week turbulence evaporated on Trump-Iran peace signals and a resilient return to tech duration assets, absorbing a mid-week semiconductor correction. The Nasdaq Composite led the charge with a 2.50% gain, reclaiming its baseline with a steep recovery slope. More impressively, the Russell 2000 surged 3.93%, indicating that small-cap, high-leverage equities are pricing in a economic soft landing. This technical repair establishes a robust risk-on foundation, though the market enters the new week in a state of high alert regarding terminal interest rate expectations.

What stands out here is a sharp thematic divergence in sector capital flows. While the AI Infrastructure trade regained its footing, Energy plummeted 3.75% as geopolitical risk premiums were priced out. Large-cap tech experienced a temporary technical vacuum as institutional desks likely trimmed Magnificent 7 positions to fund allocations for the historic SpaceX IPO mega-listing. However, the AI Trinity of Nvidia, TSMC, and ARM quickly resumed leadership, fueled by massive capital expenditure cycles reaffirmed at Computex.

Digging deeper into Q1 2026 13F filings, the world's most sophisticated desks are abandoning broad indices in favor of hyper-concentration within the AI physical layer. Berkshire Hathaway nearly tripled its stake in Alphabet to 16.6 billion, while Bill Ackman executed a violent pivot, exiting Alphabet entirely to deploy 2.1 billion into Microsoft. Altimeter Capital shifted aggressively from consumer software to double down on Nvidia and initiate positions in ARM. Translation for investors: institutions are securing the hardware and infrastructure of the next industrial revolution, moving beyond speculative software applications.

The real implication is that the Federal Reserve stands at a complex crossroads. May data prints revealed sticky inflation with CPI at 4.2% and PPI climbing 6.5%, even as initial jobless claims hit a three-month high of 229,000. Commodities saw extreme volatility, with WTI crude plunging to 86.41 per barrel, while gold surged near 4205 per ounce. This late-week rally in precious metals suggests that professional desks are actively hedging against an inflation shock or a hawkish policy error ahead of the June 17 FOMC meeting.

Key takeaway: the upcoming FOMC decision marks a definitive policy regime shift with the debut of Kevin Warsh as Fed Chair. With 2026 GDP forecasts revised up to 2.25%, there is zero incentive for an easing bias. The market is bracing for a hawkish pivot toward a formal higher-for-longer stance that could keep rates elevated through 2026. This week's chronological watchlist includes the NY Fed Manufacturing Index on Monday, Retail Sales and the pivotal FOMC Dot Plot on Wednesday, followed by Micron earnings. U.S. markets will be closed on Friday for Juneteenth.

Bottom line: corporate guidance will serve as the ultimate reality check for AI valuations. Oracle's strong earnings set a high bar, and next week all eyes turn to Micron as the definitive barometer for High Bandwidth Memory demand, alongside Accenture and FedEx. For professional investors, the current environment necessitates a barbell approach. While core AI infrastructure positions should be held for secular growth, a tactical rotation into defensive staples and precious metals is advised to hedge against a potential Warsh shock.

stock.gl

Disclaimer: Market involves risk; invest with caution. This is based on public information and is not investment advice.

1

230

いまこのネタについて語っています

「iPhone Foldはこれなのか?COMPUTEXで謎のモックを発見(山根康宏) | テクノエッジ TechnoEdge」

YouTubeライブ配信中: youtube.com/live/HU7ZzSKavho…

2

1,093

mip retweeted

lots of vendors showcased their solutions to the 16pin melting problem at computex 2026.

off the top of my head:

- msi psu gpu(current per pin sensing ciruit)

- adata psu

- coolermaster psu cable

- gigabyte psu cable

- asrock psu cable

- asus psu cable gpu(48v)

- superflower psu cable

- thermal grizzly adapter

- ezdiyfab adapter

- corsair psu cable

- seasonic psu cable

- colorful/segotep btf3.0 (my biggest regret this year not visiting their booth)

let me add this:

i think we should not mock the brands that put in the effort to address the 16pin melting problem.

i have huge respect for cablemod despite their 16pin adapter melted like shit years ago, because cablemod actually take care of their customers.

I cut 3 wires while the card was running... Here is what happened next... youtu.be/aYZsOrdGTug?si=NM1K…

7

8

31

8,277

Taiwan is love.

Computex was my first tech event in life and I enjoyed it. Learned new things, explored tech. Had a chat with good and knowledgable people around.

2

1

13

ジェンセン・フアンCEOが今回のアジア歴訪(台湾Computex後、韓国訪問)で日本を素通りした主な理由は、AIサプライチェーンの即時強化に焦点を当てたツアーだったからです。台湾はTSMCによる先端製造の要、韓国はHBMメモリなどでNVIDIAのGPU生産に不可欠なパートナー。両国の深いエコシステムと迅速な連携が魅力です。

日本の半導体戦略の課題:Rapidusの先端プロセス(2nm)量産に向けた資金・人材不足と歩留まり向上、台湾・韓国の集中投資・実行力に追いつく難しさ。材料・装置では世界トップですが、先端ロジックやAI即戦力で後れています。

ただ、フアン氏は過去の訪日で「日本なくしてNVIDIAなし」と高く評価。長期的なAI・ロボット分野での協力は重要視されています。

1

2

4

11,211

4Roses retweeted

NVIDIAのジェンスン・ファンCEOが5月下旬から6月上旬にかけて台湾・韓国を歴訪しました。

日本への立ち寄りはありませんでした。

前回の来日は2024年11月です。

台湾では毎年恒例のCOMPUTEX 2026とNVIDIA主催のGTC Taiwanで基調講演を行いました。

NVIDIAのGPUを製造するTSMCの本拠地でもあるため、台湾訪問は供給網の確認作業を兼ねています。

韓国は6月5日から8日まで、4日間の公式訪問でした。

SK・現代自動車・LG・NAVER・Samsungの各トップと個別に面談し、

最終日の夜にはソウルのシラホテルで「Korea AI Ecosystem Reception」と呼ばれる夕食会を開催しました。

半導体からAIモデル、ロボティクス、自動運転まで、18社が1か所に集まりました。

この訪韓で最重要だったのは、SK hynixとの複数年にわたる技術協力協定の締結です。

ファン氏自身が、今回の訪韓の最大の成果として名指しで挙げました。

なぜSK hynixとの契約がそれほど重要なのか。

NVIDIAが2026年後半から出荷を始める次世代AIプラットフォーム「Vera Rubin」には、

HBM4と呼ばれる第6世代の高帯域幅メモリが搭載されます。

このHBM4は現行世代と比べてコストが約435%上昇しており、

Vera Rubinのシステム1台の中で最も高価な部品です。

AI推論コストそのものをBlackwellの10分の1に引き下げる性能を持ちながら、

肝心のメモリが足りなければラインが止まります。

「メモリ不足はあと数年は続く」とファン氏は公言しています。

HBM市場を握るのはSK hynix・Samsung・Micronの3社です。

日本企業の名前はここに入りません。

HBM3E世代でSK hynixはNVIDIA向けシェア50%超を獲得しており、

今回の複数年契約は、その関係をVera Rubin以降にも延長するものです。

翻って日本との関係を見ると、構図が見えやすくなります。

現在の日本とNVIDIAの関係は、主に購買者と売り手です。

マイクロソフトは2026年4月、日本に向こう4年で約1兆6000億円の投資を発表しました。

その投資の大半は、GPU搭載サーバーの調達費用です。

つまりこの1兆6000億円の多くは、最終的にNVIDIAの売上に計上されます。

日本は今、AIインフラの「建設現場」ではなく「顧客」の立場にいます。

2026年時点で稼働中のAI向けデータセンターは、米国が世界の約30%にあたる2528拠点です。

日本は210拠点で、世界シェアは3%程度です。

中国の483拠点の半分以下という位置づけです。

日本にも有力なAI関連産業は存在します。

東京エレクトロンやアドバンテストといった製造装置・テスト装置メーカーは、

TSMC・Samsung・SK hynixの製造ラインに欠かせない部品を供給しています。

ただしこれは「NVIDIAがCEOを派遣して直接交渉する相手」ではなく、

装置・材料の分野での間接的な存在感です。

Rapidusは2nmの先端半導体量産を北海道で目指していますが、

2026年現在、量産実績のある段階には至っていません。

設計会社NVIDIAの視点では「まだ取引できる段階にない」と判断するのが合理的です。

ファン氏が直接赴く先は、今NVIDIAの供給網を実際に動かしているか、

これから動かすことが確定している相手です。

台湾は製造、韓国はメモリ。

この2か所でNVIDIAの次世代製品の命運が決まる以上、CEOはそこへ行きます。

日本が「行かれる側」から「行かれる側」に移行するための条件は、

一言で言えば供給網への参入です。

顧客であり続けることと、パートナーとして設計に関与することは、

扱いが根本的に異なります。

「日本を素通りした」という事実は、失礼でも侮辱でもありません。

取引の優先順位が、そのまま動線に表れているだけです。

NVIDIAのCEO、日本を素通り 歴訪の韓台に劣るパートナーの魅力

nikkei.com/article/DGXZQOGN0…

5

21

3,474

#来年もいくぜCOMPUTEX

現地でしか体験出来ない体験は良いですね

#RP

Jun 9

🎁アスキーからプレゼントのお知らせ🎁

COMPUTEX2026スペシャル振り返りLIVEの配信を記念して

取材班が台湾で購入したお土産を1名様にプレゼント‼️

【応募方法】

① @asciijpeditors をフォロー

②「#キーワード」、「COMPUTEX2026スペシャル振り返りLIVEの感想」、「#PR」を添えて本投稿をリポスト📮

【応募期間】

6/9(火)~ 6/14(日)23:59まで

※当選発表はDMにてお送り致します✉️

☑️お得な情報盛りだくさんのASCII YouTubeチャンネルの登録も宜しくお願いします!!

🔻キーワードは生配信をチェック👀

youtube.com/live/Wy68sHMa8Es…

7

ليزر تكنولوجي📡 retweeted

Jun 12

We’re honored the new Dell XPS 13 has been awarded “Best in Show” by @XDADevelopers at Computex 2026.

Dell XPS 13 reflects our focus on thoughtful design and reliable performance - razor-thin, featherlight and featuring a smooth 120Hz display built for how you work and move.

2

6

37

2,510