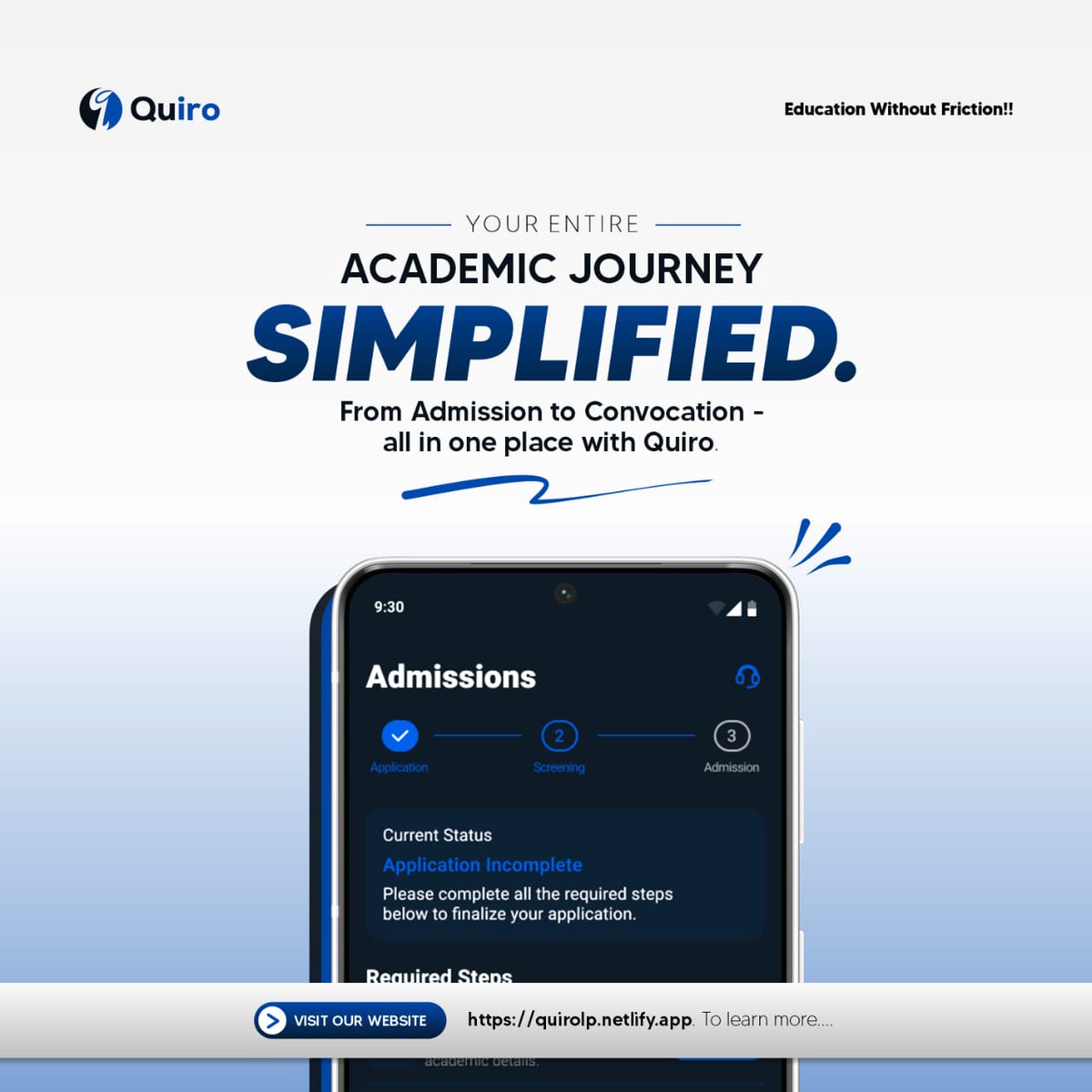

Introducing seamless interactions across all stages in all locations. From admission to convocation all with ease on one app.

#edtech

#embeddedfintech

#ai

#UMS

#mobile

#saas

#infrastructure

2

2

34

Clover knew their merchants needed payroll built into their platform, but payroll isn’t their specialty. So, they turned to ADP® Embedded Payroll, letting ADP handle the payroll compliance and expertise while Clover delivers a seamless experience for business owners.

Learn more from Clover’s executive on how the partnership enables merchants to run payroll where they already run their business: bit.ly/460RKHK

#EmbeddedPayroll #CloverPayrollByADP #Payroll #EmbeddedFinTech #EmbeddedFinancialTechnology

1

2

340

🚨 $SURG The Bigger Picture - Infrastructure platform economics - SmallCap Stocks to 👀 Now: $ACON $ONDS $PRSO $JTAI thestreetreports.com/the-big… #SurgePays #SURG #Wireless #Fintech #EmbeddedFintech #DigitalPayments #MVNE #RetailTech #PlatformPlay #SmallCapStocks #StocksToWatch #GrowthStocks #Underbanked #Connectivity #TechStocks

1

3

3

825

30 Jun 2025

Rates don’t create loyalty. Relevance does. 💥

Q2 and @BankDirector reveal how leading banks are using segmentation #EmbeddedFintech to build durable, strategic deposit bases. 🤝

It’s not a tech trend—it’s a liquidity strategy.

🔗 bit.ly/4eqH3RP

2

108

6 Aug 2024

Unlocking #SMB Potential 🔓

Join Q2’s Jody McCrary and @First_Financial’s Andrea Smiddy-Schlagel at 1 p.m. CT on August 20 as they explore how #EmbeddedFintech solutions can transform relationships with small to mid-sized business customers. ⬇️

bit.ly/3SHksae

1

2

2

202

finmid (@wearefinmid) has successfully closed a €23M Series A Round, bolstering its mission to revolutionize the #financial services industry with innovative embedded #fintech solutions.

This infusion of capital will accelerate finmid's development of seamless financial solutions that can be integrated into various business models, enhancing customer experiences and expanding financial accessibility.

By embedding sophisticated financial technology directly into everyday business platforms, FinMID is setting new standards for convenience and efficiency in financial transactions.

Read the full article here: newzchain.com/finmids-series…

#Fintech #Funding #TechInnovation #EmbeddedFintech

3

89

19 Mar 2024

Get in touch with the @BladeLabs_ team for tailored, seamless, and secure embedded tech solutions. bladelabs.io/contact-us/

#ASAPModel #DigitalAssets #EmbeddedFintech #BladeLabs

19 Mar 2024

Tailored embedded fintech that aligns seamlessly with the ASAP model proposed by the IMF

From versatile Access Layer solutions to robust Platform Layer, we provide a comprehensive framework for digital asset management.

bladelabs.io/digital-asset-p…

#DigitalAssets #IMFFramework

2

6

141

26 Jan 2024

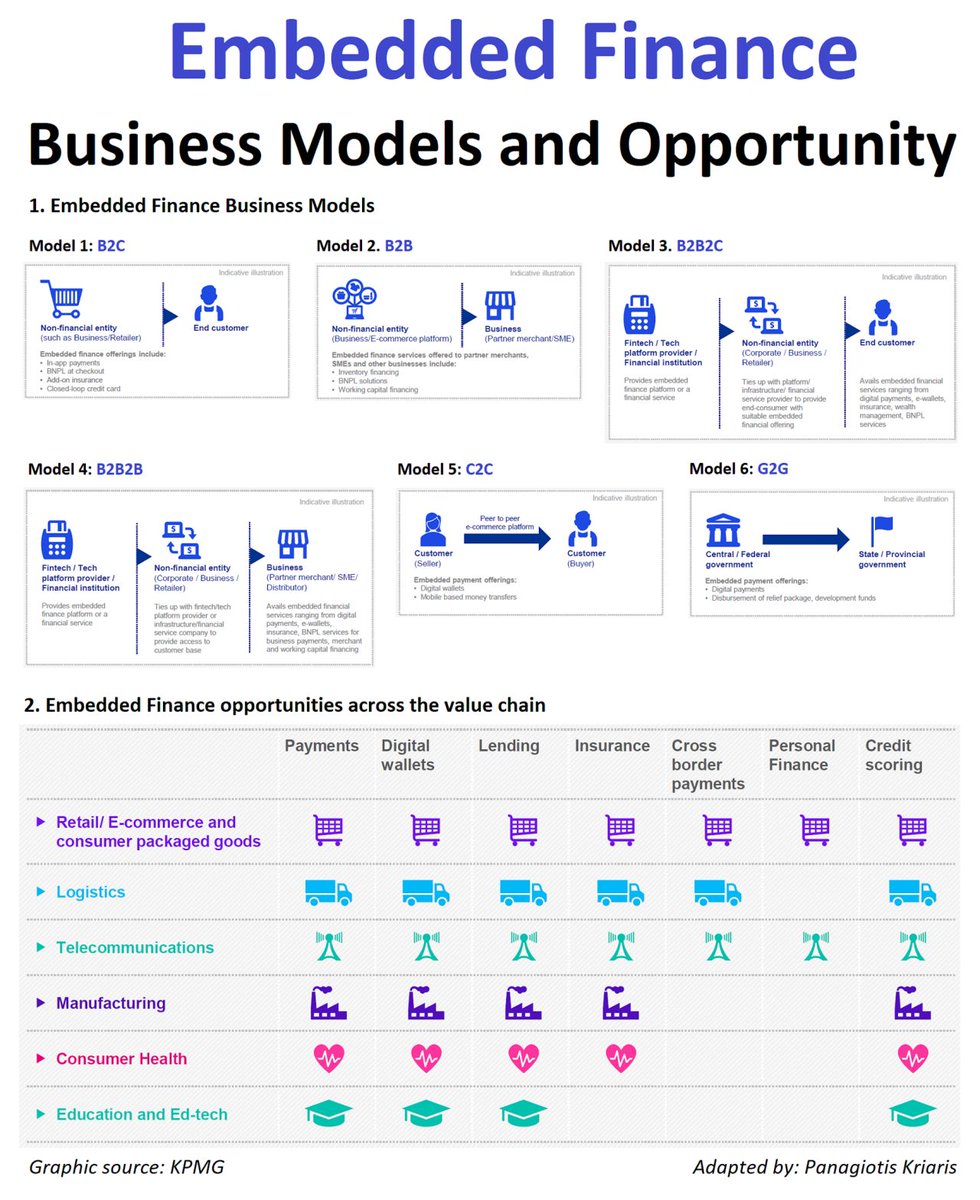

Business Models in Embedded Finance👇

KPMG mapped them out in 6️⃣ categories:

1️⃣ B2C: The so-called retail business model with consumers at the receiving end and marketplaces, e-commerce platforms, and other apps on the distribution side.

2️⃣ B2B: Non-FS players offer financial services (e.g., payments, lending, inventory financing, working capital financing, insurance) to other businesses or merchant platforms.

3️⃣ B2B2C: Here we have the introduction of an additional business layer in the value chain in the form of a fintech or technology provider. Example: an insurtech working with a furniture retailer to offer product insurance to the retailer’s customers.

4️⃣ B2B2B: similar to the B2C side a technology provider is integrated into the model

5️⃣ C2C: This model involves embedding financial services (i.e. payment options) into C2C marketplaces or P2P platforms.

6️⃣ G2G: This involves embedding FS between government relationships, i.e. tax payments between levels of government.

Source Graphic: Panagiotis Kriaris

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#embeddedfinance #embeddedbanking #embeddedfintech #openbanking #fintech #financialtechnology #fintechindustry #payments #paytech #digitalbanking

1

5

407

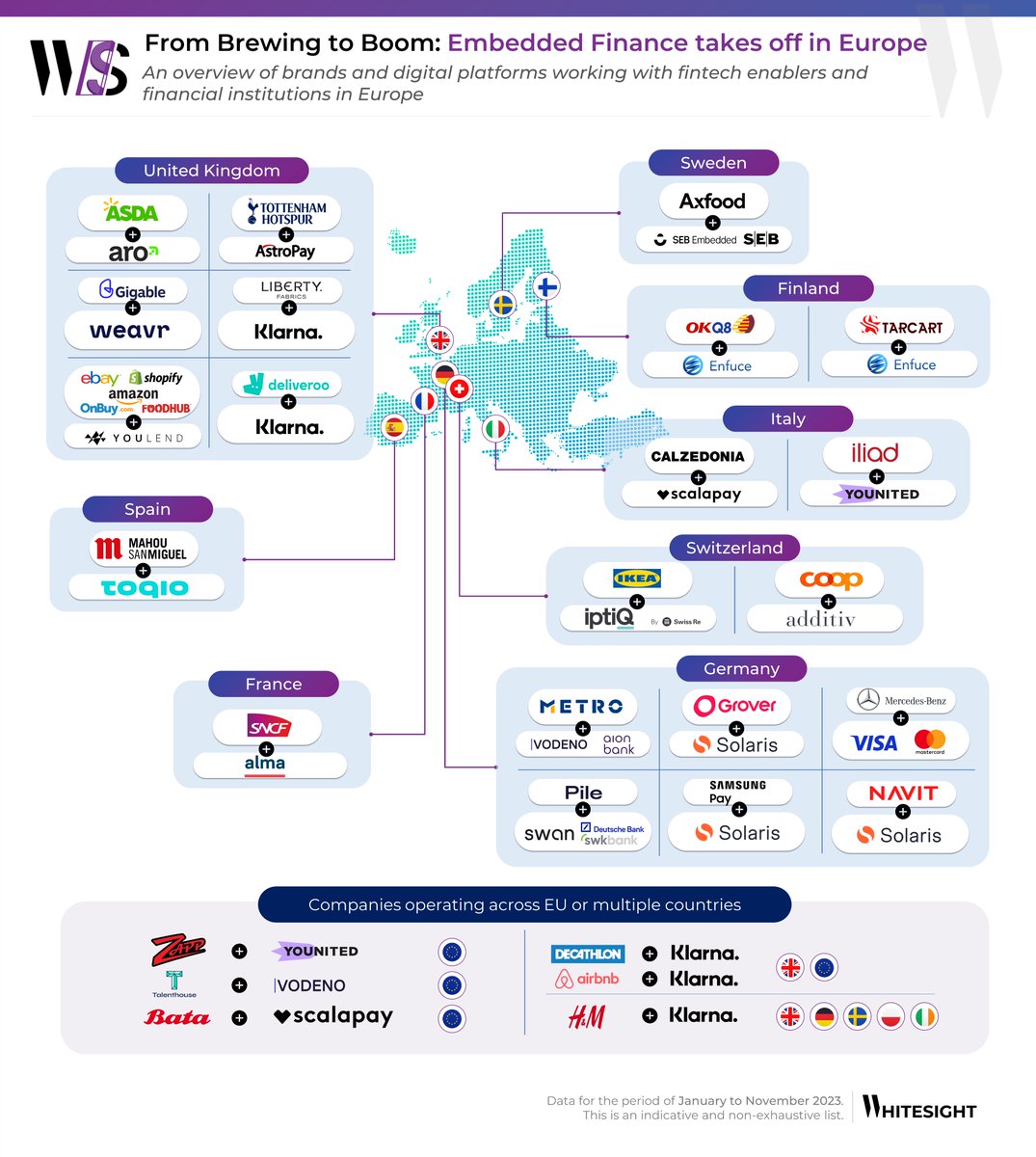

9 Jan 2024

Embedded Finance takes off in Europe: Germany and the UK lead embedded finance innovation.

Progressive regulations and policies in the UK and Europe, such as open banking, PSD2, and FinTech licences (electronic money institutions, digital or startup banks, etc.), have led to the creation of an abundant playground for innovation.

Non-banks across the UK and EU are experimenting with contextual embedded financial products for captive users. Varying from individuals to freelance professionals and small businesses, the audience for these offerings is quite diverse.

Read the complete @WhiteSight_ source article for more info: lnkd.in/eW-37Q98

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#embeddedfinance #embeddedbanking #embeddedfintech #fintech #fintechindustry #financialtechnology #openbanking #paytech #financialservices

1

3

359

7 Jan 2024

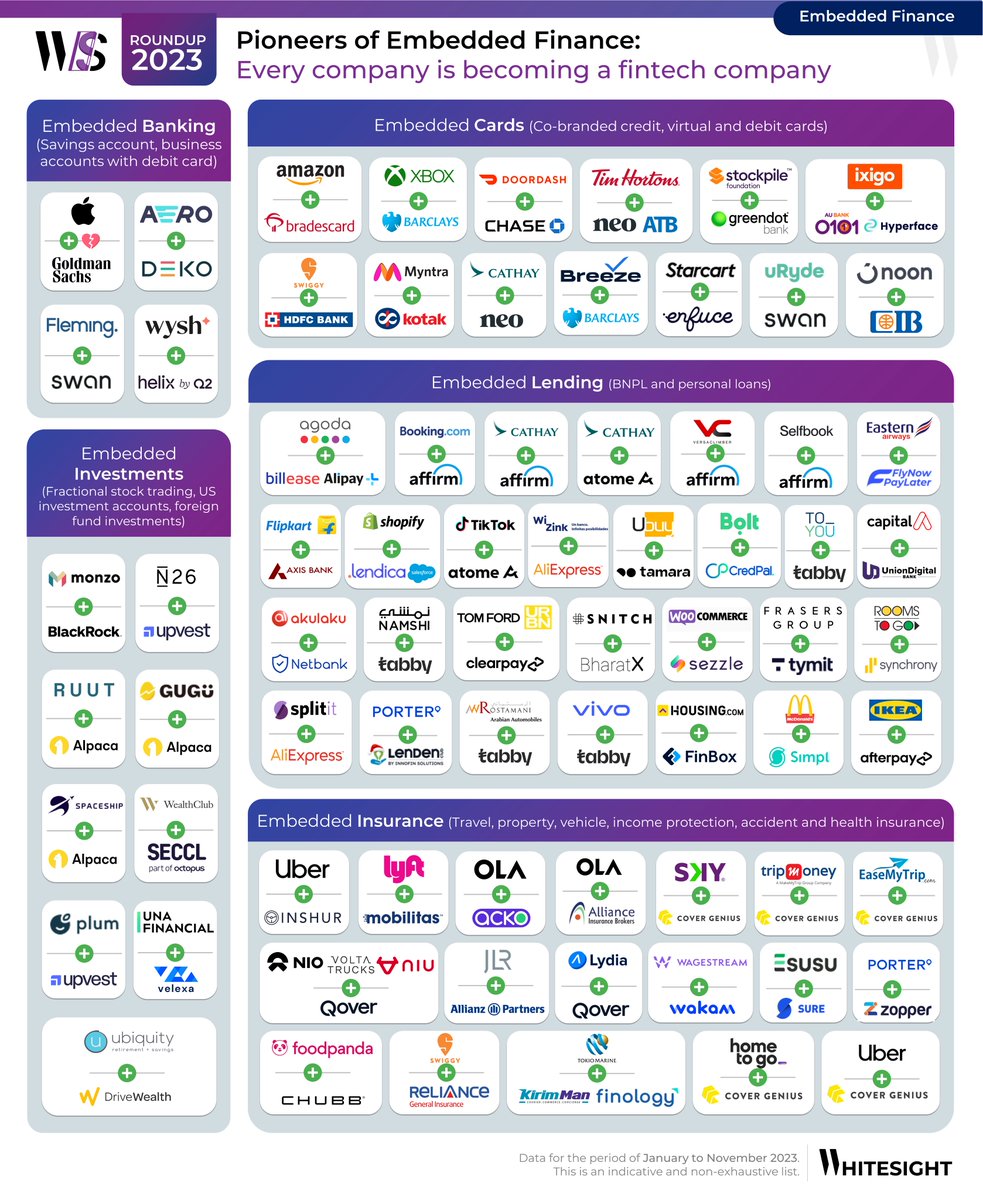

The State of Embedded Finance by @WhiteSight_

Let’s dive into the evolution of embedded finance in 2023:

According to Bain & Company, financial services integrated into e-commerce and various software platforms represented $2.6 trillion, equivalent to almost 5% of the total US financial transactions in 2021.

It is projected that by 2026, this figure will surpass $7 trillion, representing a massive economic opportunity for the non-banks. Embedded finance has been initially driven by integrating embedded payments by non-banking entities.

In 2023, it grew massively in both scope and scale with almost every financial service such as bank accounts, cards, credit products, investments, and insurance coming into the mix.

I highly recommend reading the complete source article for more info: lnkd.in/eHq-bYs5

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#embeddedfinance #embeddedbanking #fintech #financialtechnology #fintechindustry #embeddedfintech #payments #paytech #digitalbanking #openbanking #fintechnews

1

4

380

11 Dec 2023

#payments #treasurymanagement #embeddedfintech @treasure_hq @PriorityCommrce

Priority Announces Strategic Technology Partnership with Treasure Financial

buff.ly/48bIRtL

2

46

25 Nov 2023

In 2023, we’ve witnessed a surge in e-commerce-BNPL collaborations across different regions, with several e-commerce platforms working their magic to seamlessly integrate BNPL options into online checkouts:

What’s spurring this BNPL uproar in the e-commerce and retail world is the hunger for flexible payment options, an improved shopping experience, and its role in promoting financial inclusion through informal credit channels, such as online marketplaces – all without the hassle of those lengthy and often dreary bank and credit card paperwork rituals.

Here are a few partnerships that certainly stand out:

⚫️ Ikea teaming up with @AfterpayUSA to make furniture purchases a breeze with no-interest credit.

⚫️ Amazon joining forces with @Affirm , offering the luxury of next-day delivery with a convenient three-week payment plan.

⚫️ Namshi collaborating with Tabby in Saudi Arabia for a unique shopping experience that divides the purchase into four interest-free instalments at checkout.

⚫️ Liberty teaming up with @Klarna to elevate the luxury shopping experience through no-interest instalment plans.

⚫️ Walmart and Klarna joining forces to sprinkle Pay in 4 magic on grocery shopping, personal must-haves and others.

I highly recommend reading the complete source article by @WhiteSight_ for more info and examples: whitesight.net/2023-emfi-rou…

❓Now over to you: which FinTech partnership stands out for you in 2023?

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#fintech #buynowpaylater #embeddedfintech #bnpl #payments #paytech #digitalpayments #embeddedfinance #financialtechnology #fintechindustry

1

5

1,224

22 Nov 2023

Colendi took part in the Singapore Fintech Festival, with Invest in Türkiye team as the fastest growing member of the outstanding Turkish fintech ecosystem. We had an amazing journey breaking down interesting facts about Türkiye and us to our audience. Our CEO Bulent Tekmen @tekmen captivated the audience at the SFF, delving into the ongoing fintech revolution. Tekmen illuminated the entrepreneurial journey with unparalleled realism. Shoutout to everyone who shared this experience with us, also Navin Suri, Sagari White and rest of the SFF team for their great hospitality.

@sgfintechfest

We present our admirations to Investment Office of the Presidency of the Republic of Türkiye and A. Burak Dağlıoğlu @aburakdaglioglu and team for spotlighting the immense growth and development on fact-pacing Turkish fintech sector.

Gratitude also goes to the Ambassador of Turkey in Singapore Mehmet Burçin Gönenli @MehmetBGonenli for his warm welcome.

@necipfazl

#SFF23 #EmbeddedFintech #FutureofFinance

1

5

17

1,836

16 Nov 2023

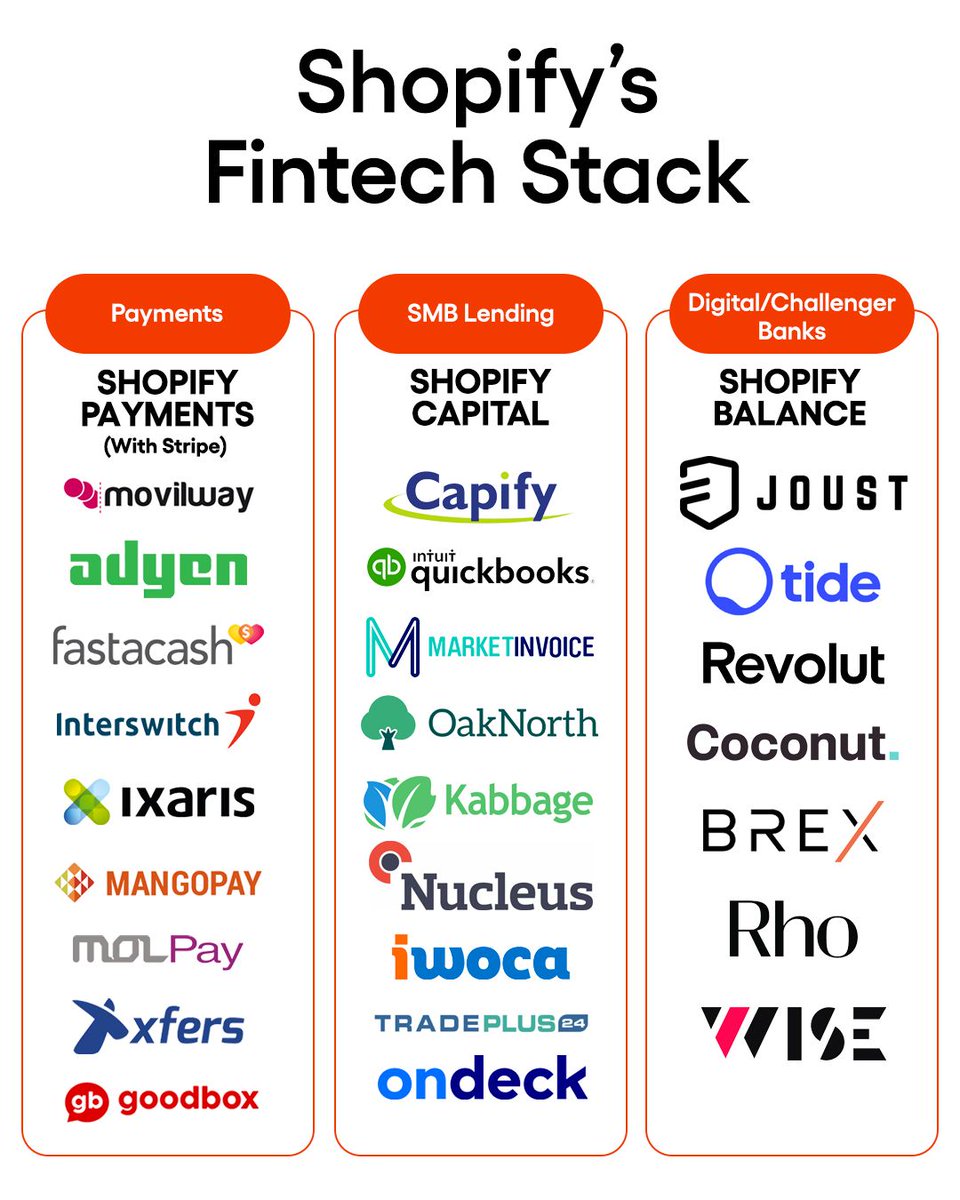

How Embedded Finance Makes Shopify a FinTech Business

Shopify’s FinTech stack includes the following products:

Shopify, often seen as an e-commerce platform, is actually a significant player in the fintech industry, with over 50% of its revenue coming from financial services.

Let's dive in:

𝗦𝗵𝗼𝗽𝗶𝗳𝘆 𝗣𝗮𝘆

This is Shopify’s checkout button for online stores. It offers an accelerated checkout option for customers by allowing customers to save credit card information, along with other data. Shop Pay is remarkably similar to Amazon Pay and Apple Pay.

Sellers can enable Shop Pay just like you would any other options for third-party providers on your Shopify website.

Shopify also added Shopify POS hardware integrated with Shopify payments to 14 countries.

𝗦𝗵𝗼𝗽 𝗣𝗮𝘆 𝗜𝗻𝘀𝘁𝗮𝗹𝗹𝗺𝗲𝗻𝘁𝘀

Shopify integrated Pay with Affirm to offer Pay later option at check out, which will let merchants offer their customers more payment choice and flexibility at checkout, helping merchants boost sales through increased cart size and higher conversion.

𝗦𝗵𝗼𝗽𝗶𝗳𝘆 𝗕𝗮𝗹𝗮𝗻𝗰𝗲

Gives merchants access to critical financial products to start, run, and grow their business, including the Shopify Balance Account, Shopify Balance Card, and rewards such as cashback and discounts on everyday business spending like shipping and marketing.

The key hook is that as soon as a customer has paid on the e-commerce store a merchant would have that cash available immediately. This will be instant and without fees, unlike most business bank accounts that take days and charge fees.

𝗦𝗵𝗼𝗽𝗶𝗳𝘆 𝗖𝗮𝗽𝗶𝘁𝗮𝗹

Providing loans ranging from $200 to $1 million to merchants. Shopify Capital has grown to $4.7 billion in cumulative capital funded since its launch in April 2016, approximately $580.1 million of which was outstanding on December 31, 2022.

Since Shopify has access to all the sales (and subsequently CashFlow) data, their risk underwriting can be more accurate than traditional banking.

Recently, Amazon expanded the reach of "Buy With Prime" through a partnership after Shopify unloaded its logistics business in May.

Kudo’s to George Slawek for brining this to my attention in his LinkedIn post: lnkd.in/eBVzkpmB

And read a longer deep dive from Hardik Tiwari for more interesting info on this specific use case : lnkd.in/efgaXrWv

❓Now over to you: The picture is a bit dated so are there any new players in the FinTech Stack that are missing in the overview below?👇

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#shopify #embeddedfinance #embeddedfintech #embeddedbanking #payments #paytech #digitalpayments #fintech #financialtechnology #fintechindustry

4

924

12 Nov 2023

Embedded payments offer a way to integrate payment functionality directly into your software platform, creating a streamlined experience for your users – and more revenue for you. Learn more in this guide. bit.ly/46414YR

#embeddedpayments #embeddedfintech #b2b

2

77

28 Oct 2023

Starbucks' hugely popular rewards program held $1.8bn in customer cash as of April 2. If Starbucks was a bank, that would make it bigger than 90 percent of institutions covered by the US FDIC by deposit size.

Contrary to banks, which must maintain cash reserves to prepare for potential mass withdrawals, the coffeehouse chain only needs to stock up on coffee and snacks.

Could Starbucks be a hidden FinTech?

The Starbucks app boasts an impressive 31 million active users.

Customers can add funds to their accounts using Starbucks gift cards, or by connecting Apple Pay or payment cards to the app.

Each purchase made through the app earns users loyalty points (known as Stars), redeemable for benefits like free refills, beverages, or sandwiches.

A clever aspect of this strategy is that customers paying with funds deposited on the Starbucks app receive additional loyalty points.

Within the customer loyalty space, Starbucks has consistently been credited with having one of the best rewards programs with a loyal customer following.

Because of the company’s reputation, customers are not afraid to keep money in their Starbucks account, knowing that they can use it anytime.

The numbers speak for themselves:

The "stored value card liability and current portion of deferred revenue" – unspent money that coffee lovers have loaded onto the app – amounted to $1.8 billion in the previous quarter.

This unused cash has been compared to interest-free capital for Starbucks.

Furthermore, some gift card funds are never redeemed by customers, allowing Starbucks to retain the entire amount.

In its latest fiscal year, the company reported approximately $196 million in such "breakage revenue." Although it accounts for less than 1% of Starbucks' annual net revenue, it is essentially free money.

There is another benefit of encouraging users to pay for their purchases using the funds stored in their Starbucks accounts: fewer payment processing fees.

I highly recommend reading my complete source article for more info, stats and figures: connectingthedotsinfin.tech/…

Starbucks' rewards program is an innovative example of a non-banking entity using loyalty and trust to amass significant customer deposits. Is Starbucks a hidden FinTech giant? Their impressive numbers might suggest so.

❓What do you think?

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#fintech #embeddedfinance #embeddedbanking #embeddedfintech #bankingtech #financialtechnology #financialservices #starbucks #fintechindustry #bankingapp #banking #bankingindustry #digitalbanking #payments #paytech #digitalpayments

2

6

16

4,929

27 Oct 2023

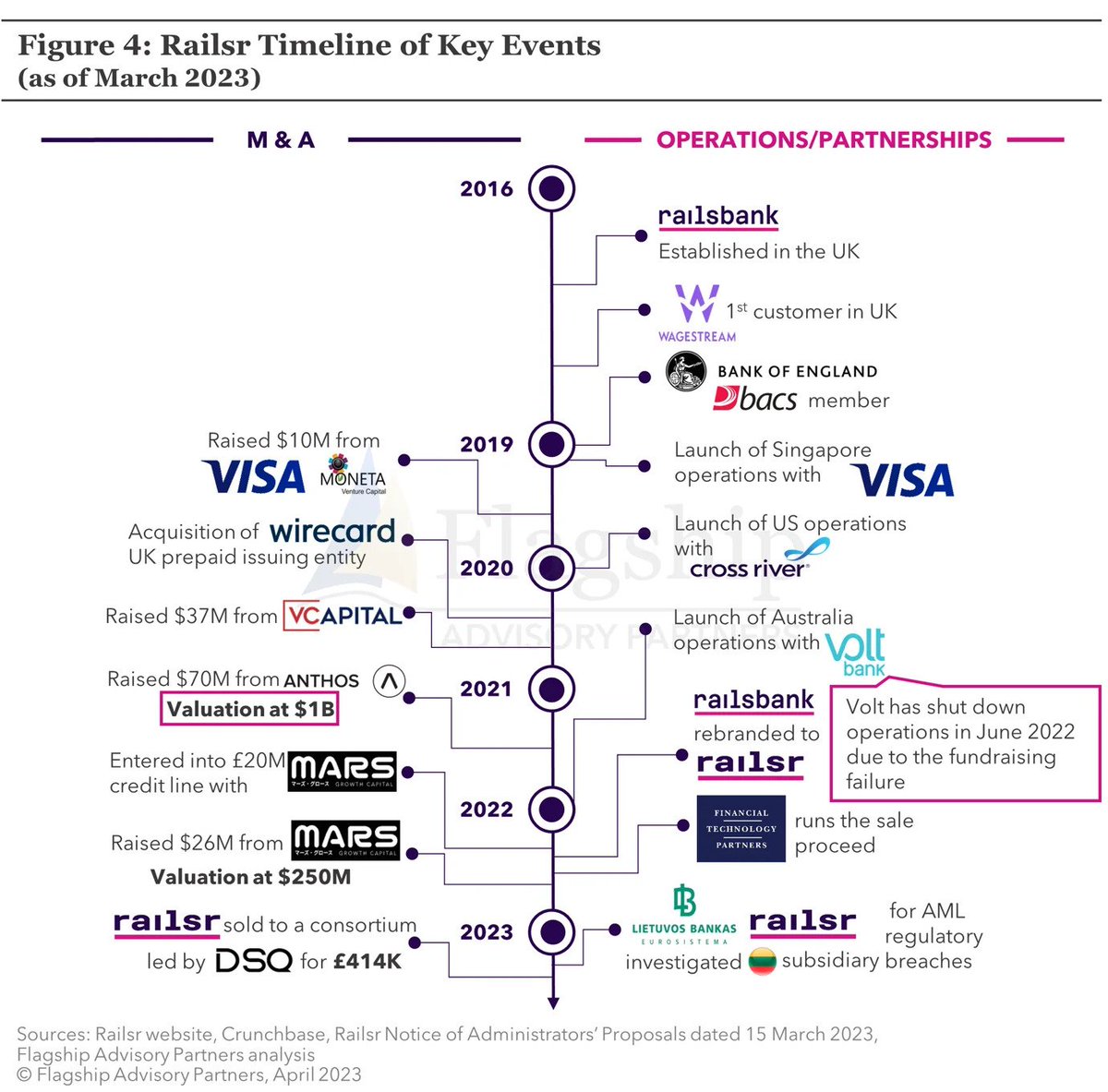

🚨 Embedded Finance, Railsr’s parent company, has secured $24m from existing investors just seven months after it was forced to undergo an insolvency process amid regulatory challenges.

Sky News understands that Railsr, the trading name of Embedded Finance, will announce in the coming days that it has struck a deal with investors to raise $24m (£19.8m).

The investment round is majorly backed by current stakeholders.

Railsr became a victim of aggressive over-expansion, running into serious regulatory issues just as funding markets for technology companies had dried up.

It has since appointed Philippe Morel, an experienced fintech executive, as its CEO - adding him to a leadership team that already included Rick Haythornthwaite, the former Mastercard chairman.

Read the complete source article for more info on this deal: lnkd.in/gP24xCKd

Picture Credit: Flagship Advisory Partners

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#donedeal #fintech #railsr #bankingasaservice #bankingtech #digitalbanking #banking #bankingindustry #financialtechnology #fintechindustry #fintechnews #embeddedfintech #embeddedfinance #embeddedbanking

1

4

13

1,606

7 Oct 2023

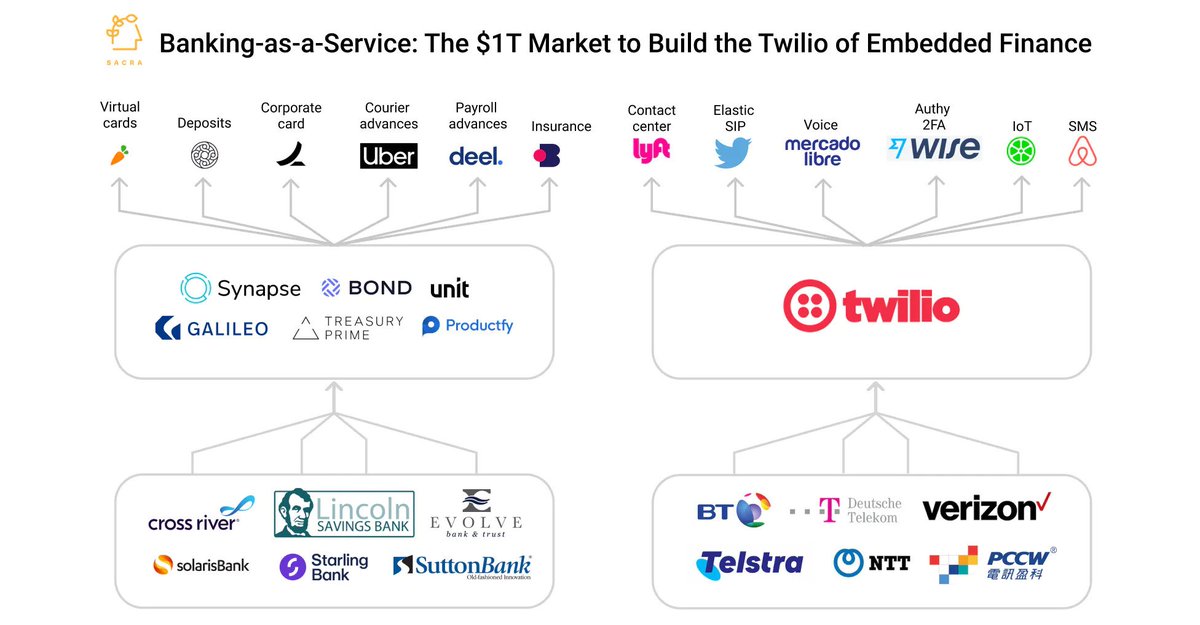

🏦 Banking-as-a-Service: The $1T Market to Build the Twilio of Embedded Finance:

Over the last several years, there has been an explosion of retail, travel, SaaS, and other companies expanding into financial services.

Walmart, IKEA, ServiceTitan and Toast are just 4 of the companies that have launched products like underwriting, interest-free credit, payments and bank accounts in an effort to provide a better experience to their customers and get closer to their wallets.

Leveraging their reach and data, brands are able to do something with these products that traditional banks like JPMorgan Chase or Bank of America or Wells Fargo have never been able to: deliver personalized experiences at scale and at the point of sale.

Where banks provide a highly regulated and repeatable set of products, brands and FinTechs can harness demographic and behavioral data to build new kinds of product experiences that ultimately bring them closer to consumers.

Read the complete source article by Jan-Erik Asplund to learn all about this: sacra.com/research/banking-a…

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#banking #bankingasaservice #bankingtech #digitalbanking #fintech #embeddedfinance #embeddedbanking #embeddedfintech #financialtechnology #fintechindustry

3

9

46

5,603

5 Oct 2023

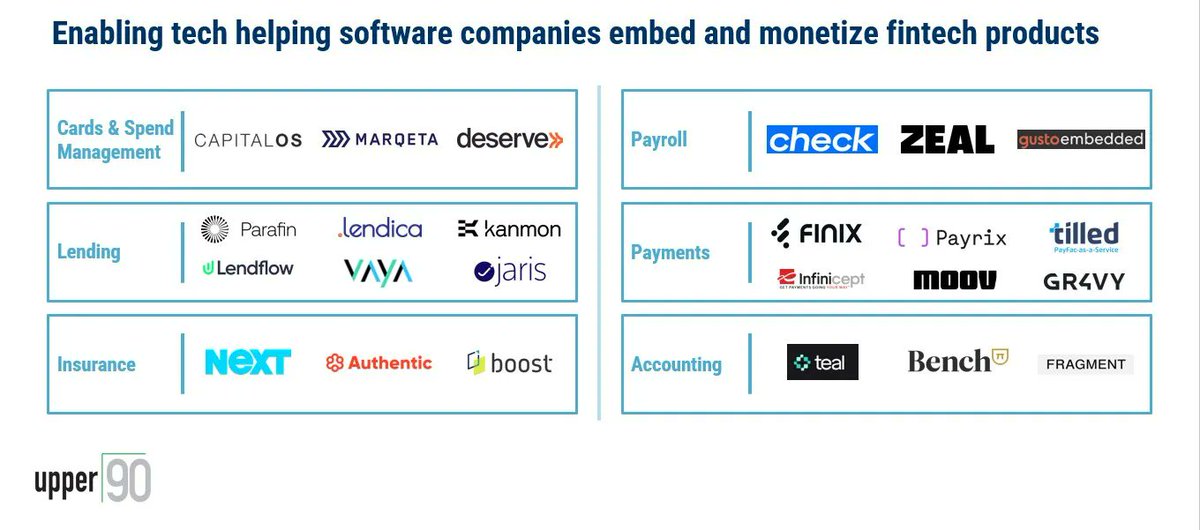

FinTech can play a pivotal role in escalating vertical software businesses by offering an additional avenue for revenue beyond the conventional subscription-based models, especially considering the financial constraints of SMBs in comparison to larger enterprises.

For instance, businesses like Toast and Shopify significantly amplify their revenue through fintech, primarily payments, and are extending their reach into facets like lending, invoice factoring, insurance, and payroll management.

Vertical software platforms, once established as the primary operating system for SMBs, can further deepen customer relationships and monetization via consistent product innovations, with fintech being a strikingly impactful medium.

Utilizing financial offerings not only expands revenue streams but also acts as catalysts for customer acquisition, retention, and offers expanded value propositions, fortifying the platform's integral role in businesses' operations.

Examples such as Authentic, which allows vertical software companies to provide SMB insurance coverage, showcase the potential of embedding financial platforms in vertical software.

This integration provides an assortment of opportunities like gauging customer intent for financial products, enabling pre-approvals based on existing platform data, reducing customer acquisition costs, diversifying revenue, and enhancing customer retention by creating a comprehensive one-stop solution.

I highly recommend reading the complete source article by @upper__90 for more info on this topic: upper90.medium.com/vertical-…

Find this helpful? [ 𝗿𝗲𝗽𝗼𝘀𝘁 ]

Anything to add about this subject? [ 𝗶𝗻𝘃𝗶𝘁𝗲𝗱 𝘁𝗼 𝗰𝗼𝗺𝗺𝗲𝗻𝘁 ]

Nice story, Marcel. Next! [ ❤️ ]

#fintech #embeddedfinance #embeddedbanking #embeddedfintech #financialtechnology #fintechindustry #fintechstartups #insurtech #paytech #banktech

1

4

545

EF is offering consumers products and capabilities they didn’t know existed, but ones they are happy to take advantage of now that they are available.

TY @retailvoices

#fintech #retail #embeddedfinance #embeddedfintech #paymentoptions #customerloyalty #personalpower

25 Sep 2023

How embedded finance is impacting the retail industry.

@Aazzur_

#RetailVoices #YourVoices

buff.ly/3LCFseu

2

29