By section:

ASTS

ASTX

NBIS

IREN

CIFR

SIVE/SIVEF

AXTI

AAOI

SLOIF

PURR

NOK

ORCX

MUU

MVLL

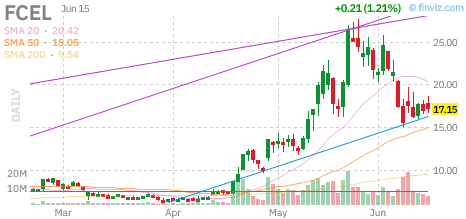

FCEL

BE

ASTS/ASTX by far my biggest (from price appreciation) and most bullish position. Long term hold. Over half of port. Then NBIS and SIVE biggest position for same reason price appreciation . Only adding to PURR NOK ORCX. Been taking profits on everything except ASTS and adding to these. Looking to add to robotics soon.

281

You still believe in FCEL thesis at this point? Do you have any calls or shares now ?

1

1

71

NIO to the moon retweeted

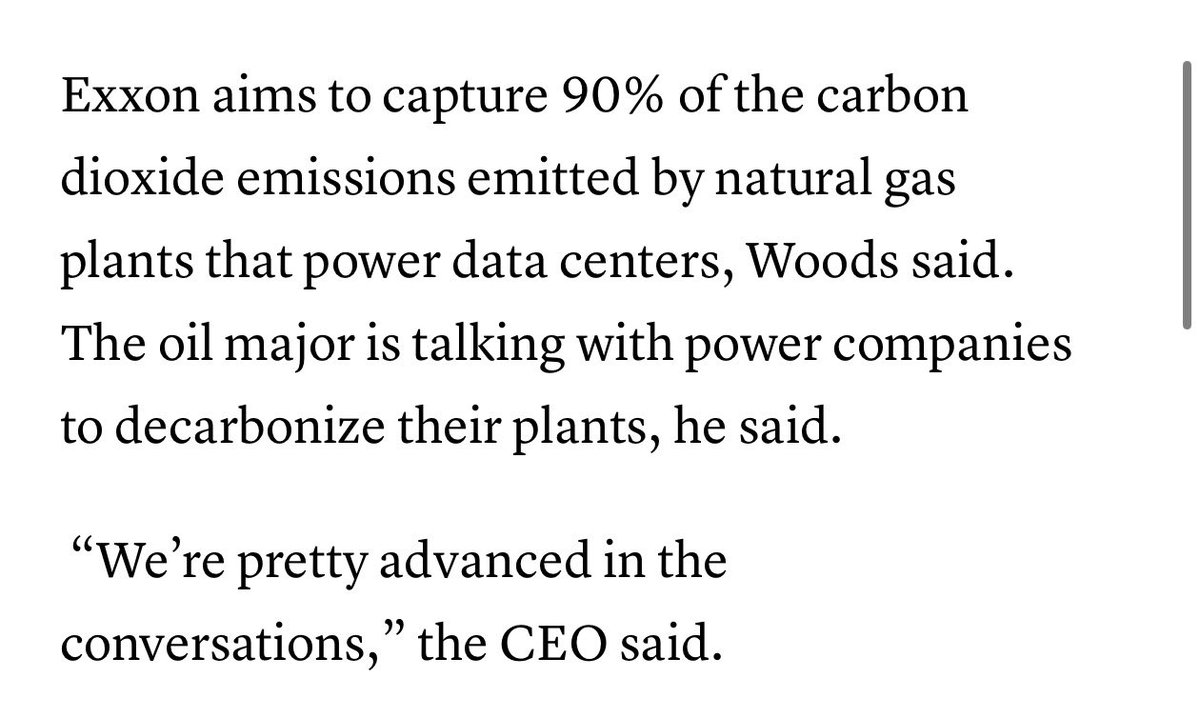

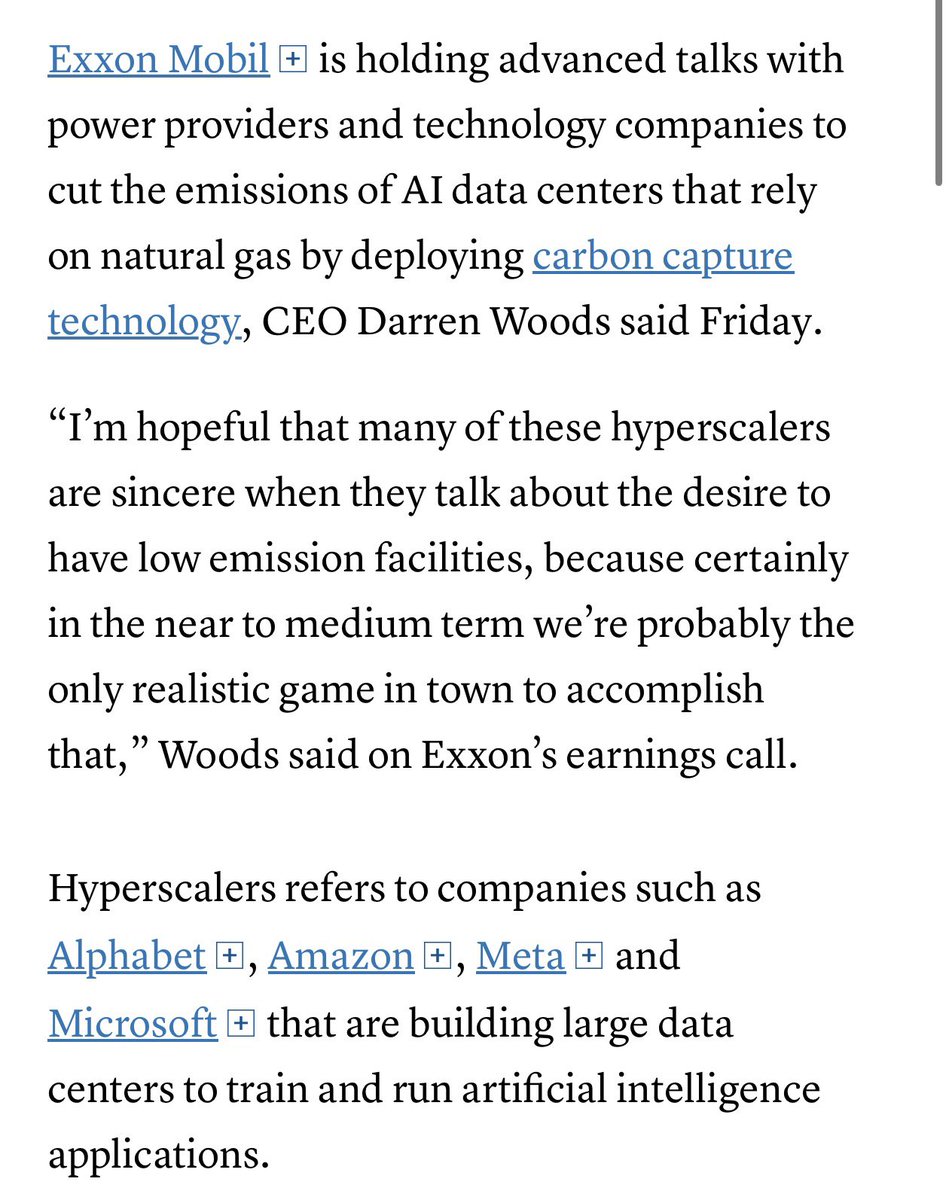

I expect $XOM to move aggressively to commercialize if the $FCEL Rotterdam Carbon Capture is a success. This technology cited below is the FuelCell MCFC Carbon Capture Solution. See the CNBC report attached from late 2025:

cnbc.com/2025/10/31/exxon-ai…

"We're pretty advanced in the conversations... I'm hopeful that many of these hyperscalers are sincere when they talk about the desire to have low emission facilities because certainly in the near to medium term we're probably the only realistic game in town to accomplish that."

When $XOM is this commercially motivated and confident in the $FCEL technology, you should probably be paying attention.

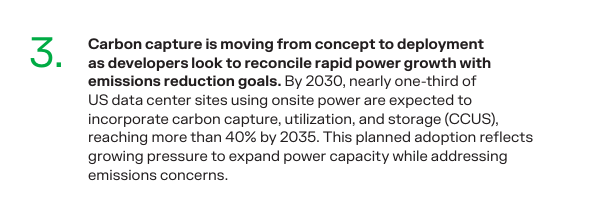

Bloom Energy $BE released their Mid-Year 2026 Data Center Power Report and look what they said:

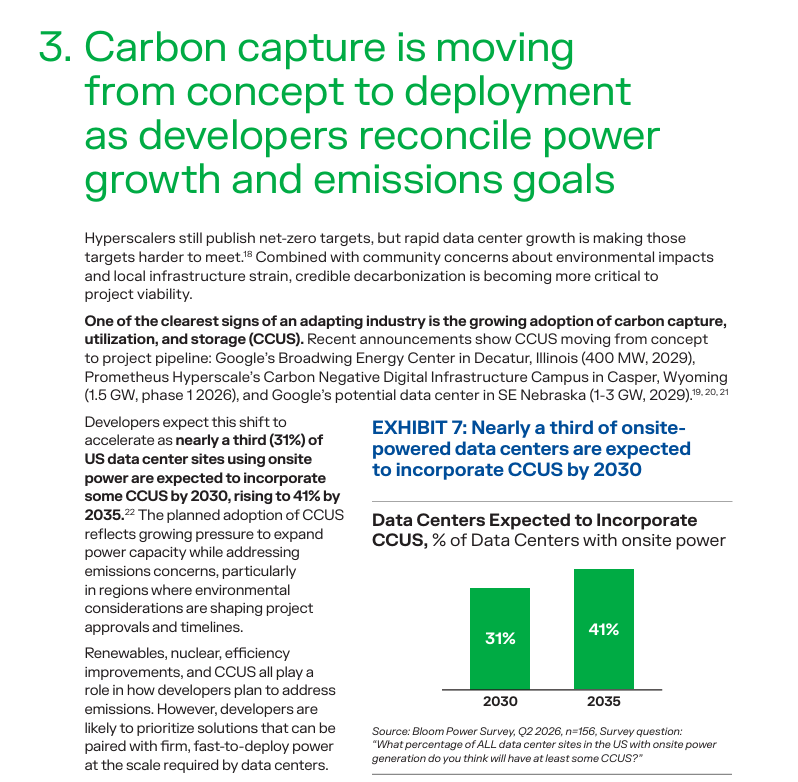

"By 2030, nearly 1/3 of US data center sites using onsite power are expected to incorporate carbon capture, utilization, and storage, reaching more than 40% by 2035. This planned adoption reflects growing pressure to expand power capacity while addressing emissions concerns."

This is your Carbon Capture moment. $FCEL has the industry leading carbon capture solution by a large margin. This means that hundreds of TWh will be deploying carbon capture technology by the end of the decade.

Read for yourself the AECOM Carbon Capture study. Look up "AECOM Next Generation Carbon Capture Technology"

6

3

26

6,598

Albert Jellema •|• Support retweeted

May 18

$FCEL taking a stab at calls here with all this volume

1

689

Company map from the 24h scan:

$MRVL: cleanest catalyst setup. S&P 500 inclusion on Jun 22 creates forced passive demand, while AI infra demand supports the core story: 800G/1.6T optics, AI switching, custom XPUs, and raised FY27/FY28 outlook.

$LITE/$AAOI: optical bottleneck trade. AI clusters need more lasers, transceivers, and interconnects as bandwidth demand scales. $LITE is the cleaner optics expression; $AAOI is the higher-beta version.

$NVDA/$SMH: broad “paid by capex” exposure. The video takeaway was to own the semiconductor/input layer where AI spend becomes revenue, not necessarily every company writing the capex checks.

$NVT/$CECO /#HPS.A.TO/$ORA /$VRT : power, grid, thermal, and always-on energy. Data centers are becoming a transformer, electrical distribution, cooling, ventilation, and power-generation problem. $VRT is obvious; the edge may be one layer below.

$FCEL : speculative carbon-capture angle. If onsite gas generation becomes part of AI data-center power, carbon capture can attach to that stack.

$OUST: Physical AI sensors/perception. If the next AI cycle moves into robots, autonomy, and industrial systems, perception hardware becomes a real infrastructure layer.

$SPCX/$RKLB: space-flow trade. $SPCX is driven by index/flow mechanics post-IPO; $RKLB is the more accessible public proxy if attention keeps moving into space infrastructure.

1

468

12h

Bloom Energy $BE released their Mid-Year 2026 Data Center Power Report and look what they said:

"By 2030, nearly 1/3 of US data center sites using onsite power are expected to incorporate carbon capture, utilization, and storage, reaching more than 40% by 2035. This planned adoption reflects growing pressure to expand power capacity while addressing emissions concerns."

This is your Carbon Capture moment. $FCEL has the industry leading carbon capture solution by a large margin. This means that hundreds of TWh will be deploying carbon capture technology by the end of the decade.

Read for yourself the AECOM Carbon Capture study. Look up "AECOM Next Generation Carbon Capture Technology"

272

12h

I expect $XOM to move aggressively to commercialize if the $FCEL Rotterdam Carbon Capture is a success. This technology cited below is the FuelCell MCFC Carbon Capture Solution. See the CNBC report attached from late 2025:

cnbc.com/2025/10/31/exxon-ai…

"We're pretty advanced in the conversations... I'm hopeful that many of these hyperscalers are sincere when they talk about the desire to have low emission facilities because certainly in the near to medium term we're probably the only realistic game in town to accomplish that."

When $XOM is this commercially motivated and confident in the $FCEL technology, you should probably be paying attention.

198

13h

Ce vert dans le portefeuille qui fait plaisir 🌿🚀

Journée exceptionnelle en bourse ! Tech, crypto et infrastructure ont tout cassé.

🚀 Explosions du jour :

• IQEPF 15,24 %

• ASST 10,03 %

• ASTS 6,27 %

• HIVE 6,17 %

🟢 IA & Énergie :

TE 4,76 % | SLNH 4,73 % | MARA 3,91 % | FCEL 3,36 % | BTDR 2,86 %

🛡️ Big Tech & FinTech :

AMZN 3,16 % | SOFI 3,20 % | OSCR 3,15 % | GOOG 2,48 % | NU 2,05 %

Momentum ultra positif !

#Bourse #Tech #Crypto

83

164

If Exxon is this interested $FCEL deserves more attention than it’s getting.

1

224