Joined September 2024

- Tweets 1,152

- Following 363

- Followers 140

- Likes 937

1 Photos and videos

Jay retweeted

May 29

Hi Fellow FinX investors,

I know European semiconductor stocks are absolutely exploding across retail X lately. Many “AI bottleneck” names are already up 5-10x.

But here’s the uncomfortable reality check:

Ex-China, East Asia (Taiwan, Japan, Korea) still completely dominates global semiconductor manufacturing, packaging, and scaling capacity. Europe largely gave up advanced semiconductor manufacturing decades ago.

Some of these European companies genuinely have elite technology. I’m not debating that.

What I am questioning is:

How many of them actually have deep Asian manufacturing integration?

Because in semis, superior technology alone is NOT enough. Capacity scaling is everything.

$SIVE understood this early. Management outsourced production to WIN SEMI in Taiwan and is actively securing additional capacity. That’s one reason I’m invested.

Meanwhile, several hyped European semi names look more like isolated islands — great technology, but without serious Asian supply-chain support. In my opinion, expecting rapid revenue ramps or mass-production scale-ups from these companies is unrealistic.

Trading momentum is fine. Narrative pumps can absolutely continue. But investors should still maintain some market cap discipline.

My current framework:

• European AI semi small caps can run from narrative toward ~$1B–5B

• Above ~$5B becomes much harder to justify when your manufacturing capacity is effectively constrained by Asia

• ~$10B is probably the realistic upper ceiling for most — unless the company deeply integrates into the Asian ecosystem

For example: Ayar Labs opening operations in Taiwan makes far more strategic sense to me than trying to build a semiconductor empire.

Just my current view of the global semiconductor map. Hope this adds some perspective.

#Semiconductors #AI #Photonics #SupplyChain #CPO #EuropeanSemis #Taiwan

3

3

34

2,609

Jay retweeted

May 27

Do you guys see Shunsin (TWO:6451) in the photo? 👀👀

May 27

Having already driven massive shortages in memory chips and CPUs, the global AI boom is now disrupting a more obscure part of the supply chain: optical communications.

s.nikkei.com/4wZQtgf

3

4

61

9,042

Jay retweeted

May 27

x.com/aleabitoreddit/status/…

Serenity says NVDA’s groq rack is made exclusively by Shunsin (6451)

Apr 29

Just an FYI: I don't need to post something every day about the names I own.

However, I did miss this with Shunsin (6451):

Foxconn picked by $NVDA as exclusive rack-scale supplier for Groq accelerator.

This is highly positive for Shunsin (Foxconn's optical packing arm).

So ShunSin's CPO and optical packaging basically backdoored Nvidia's next-gen supply chain with this news.

Markets just haven't realized this connection yet (and it's on disposition, so frozen for most).

The article explicitly notes that Foxconn is integrating these systems "including ... networking."

Bc Foxconn is the exclusive assembler, they'll vertically integrate and likely use ShunSin's optical packaging solutions into the design, bypassing ShunSin's need for networking contract directly from Nvidia.

This is what I meant by Shunsin is literally a free piggy back ride to $NVDA CPO ecosystem. Foxconn is massive.

And you're getting the leading player in Nvidia's optical supply chain for a lower valuation than $LWLG lol.

2

1

7

4,504

Jay retweeted

May 27

$NVDA to spend 150 billion in Taiwan per year, do you have any idea how much liquidity it can contribute to Taiwan Stock market?

#Taiwanstock #TaiwanSemi

reuters.com/world/asia-pacif…

May 27

Nvidia to spend $150 billion a year in Taiwan, 'epicentre' of AI revolution- CEO

2

2

21

2,731

Jay retweeted

May 26

MssCorp (6830.TW) 汎銓科技Capacity Allocation: How Much Has Been “Booked” by NVIDIA and TSMC?

— Taiwan Investor Consensus Breakdown

Discussions in Taiwanese forums (CMoney and 股市同學會) have been active about how much of MSS’s Zhubei plant capacity has been secured by its two biggest clients: NVIDIA and TSMC.

Here is a clear, logic-driven summary separating official facts from market consensus:

Official Facts (from 2025–2026 earnings presentations & MOPS filings):

• Zhubei Plant 1 has been expanded into a dedicated “AI Client Zone” offering the highest confidentiality standards and priority capacity allocation for a major US Tier-1 AI chip customer (widely understood to be NVIDIA), with strong emphasis on CPO and Silicon Photonics testing.

• Zhubei Plant 2, the main Material Analysis headquarters, and the SAC-TEM Center primarily support Angstrom-era (sub-1.4 nm) material and failure analysis for leading foundry customers.

• Zhubei Plant 3 (≈2,200 ping, expected completion late 2026–early 2027) is being developed as an additional AI / Silicon Photonics specialized zone under a client co-location model.

MSS emphasizes a “dedicated zone priority capacity” strategy rather than publicly announcing full-plant exclusivity contracts.

Taiwan Investor Consensus (mainstream view across forums):

• NVIDIA is believed to have already secured the majority of Zhubei Plant 1 and is expected to take ~70–75% of the new capacity in Zhubei Plant 3 for its CPO/SiPh roadmap.

• TSMC continues to utilize substantial capacity in Zhubei Plant 2, headquarters, and SAC-TEM for advanced process development.

• Overall view: Future incremental capacity (especially from Plant 3) is largely pre-allocated to these two strategic anchor clients, pointing to very high utilization rates once the new space comes online.

Investment Logic:

1. Both NVIDIA (CPO/SiPh) and TSMC (leading-edge nodes) face extremely high and growing demand for advanced material/failure analysis during the Angstrom era.

2. The dedicated-zone model delivers security, customization, and priority — creating high switching costs for clients.

3. This dual-engine structure (NVIDIA TSMC) provides strong order visibility while mitigating single-client concentration risk.

Although no official “full-plant booking” contract has been disclosed, the strategic alignment and consistent forum consensus suggest MSS’s capacity expansion is not subject to open-market competition — it is largely pre-positioned for its two most important long-term partners.

This dynamic is a core reason many Taiwanese investors remain optimistic about MSS’s growth trajectory heading into 2027 and beyond.

Will the upcoming 5/27 earnings presentation provide more details?

Sources & References:

• MSS (6830.TW) Earnings Presentations (April 2026 & May 2026)

• Official MOPS filings: mopsov.twse.com.tw/nas/STR/6…

• Market consensus discussions: CMoney and 股市同學會 (Taiwan stock forums)

$6830 #SiliconPhotonics #CPO #AI #MSS

8

11

70

24,177

Jay retweeted

May 25

MssCorp (6830.TW) 2026/5/27 earnings presentation leak :

-Self-developed MSS HG (Helmet Gecko) Silicon Photonics tester:

• Three HG units have been assembled and are now operational, providing silicon photonics R&D analysis and engineering validation services to multiple clients.

• The core optical loss detection technology has received patents in Taiwan, Japan, and the United States.

• The system has successfully completed certification by major US AI chip manufacturers.

• PD and QA production versions are scheduled for launch in 2026.

• High-volume commercial ramp-up is expected in 2027.

This development represents one of the company’s four key growth engines, advancing the transition from analysis services to a higher-margin business model encompassing equipment sales, IP licensing, and integrated measurement services in the expanding CPO/silicon photonics market.

Full presentation deck: mopsov.twse.com.tw/nas/STR/6…

#6830 #SiliconPhotonics #CPO #AI #NVDA

5

5

56

26,366

Jay retweeted

May 25

Market Insight: Huawei's Tau (τ) Scaling Law

Huawei just unveiled the Tau (τ) Scaling Law at IEEE ISCAS 2026 — a paradigm shift from traditional Moore’s geometric scaling (shrinking transistors) to time-constant (τ) scaling that compresses signal propagation delays.

1. Advanced Packaging Closes the Density Gap: Via LogicFolding (hybrid bonding ultra-dense 3D TSV stacking), logic gates, analog circuits, and memory are vertically “folded.” On Kirin 2026, transistor density jumps 53.5% to 238 MTr/mm² — without node shrink — with 41% CPU efficiency, 13% peak frequency, and 40% SRAM speed. Target: 1.4 nm-equivalent density by 2031.

2. AI Scale-Up Has Only One Path: Full Optical Interconnect Advanced packaging exposes copper’s hard physical limit on bandwidth density, power, and signal integrity in massive GPU clusters. Industry consensus (Huawei, Alibaba, Google TPU): copper must retreat — only CPO (Co-Packaged Optics) silicon photonics enables true full-optical scale-up by co-packaging optical engines directly with ASICs.

3. Why NVIDIA, Broadcom & the Industry Are Racing?

Huawei’s paper publicly confirms what NVIDIA has acted on since 2025 GTC: copper cannot support million-GPU AI factories. NVIDIA’s Quantum-X 1.6T / Spectrum-X 3.2T CPO switches TSMC silicon photonics are now accelerating precisely because the “no-alternative” reality is out in the open.

Bottom line: There is no second path. Miss the full-optical scale-up transition and you face existential risk in the AI era.#CPO #SiliconPhotonics #AIScaleUp #TauScalingLaw

May 25

看了华为相关定律,以及其Atlas实现, 最核心的本质仍然是使用高级封装来弥补工艺差距, 使用高级架构来弥补性能差距:

这仍然是可行的: 早先的AMD面对intel就是这样.

然而这样:

1. 高功耗是无法避免的: 液冷是一定的. => 投资对象:液冷

2. 使用光纤而非铜线. 铜线限制了高级架构的scale up 能力, 因为性能密度不足, 只能扩大scale-up的范围. => 投资对象, 光模块, 光纤.

3. 高级封装RDL和 类似于APPLE的InFo-OS相对简单: APPLE MAX系列直接把PC的DDR带宽提升到服务器级别. => 投资对象, 蚀刻, 测试.

Google TPU是全光scale-up. 这就是面对NVDA这高性能密度的选择.

目前Huawei , ALI 都是全光scale-up (LPO based).

2

4

21

5,606

Jay retweeted

May 24

With NVIDIA GTC Taipei 2026 fast approaching, the spotlight is once again on AI infrastructure and next-generation interconnects, Taiwanese CPO (Co-Packaged Optics) concept stocks are expected to draw significant attention from global investors in the coming week.

As a Taiwanese investor who actively follows the local supply chain and has these names in my watchlist , I’d like to give international audiences a clear, ground-level introduction to the key Taiwanese CPO players I’m tracking.

Here’s a categorized overview based on the companies appearing in my TW Phontonics self-selected list:

Upstream – Epitaxy & Wafer Materials

-Episil-Precision Inc. (3016.TW): Silicon and compound semiconductor epitaxial wafers with increasing exposure to silicon photonics and CPO.

(recommended by @ParadisLabs )

-WIN Semiconductors Corp. (3105.TW): Leading GaAs/InP foundry, essential for CPO laser diodes and photodetectors. (recommended by serenity)

-Landmark Optoelectronics (3081.TW): Specialized InP epitaxy supplier and one of the key light-source providers for 800G/1.6T CPO modules. (recommended by serenity)(Directly listed in NVIDIA CPO ecosystem per Goldman Sachs Exhibit 21 — high likelihood of being mentioned at GTC)

-IntelliEPI Inc. (IET-KY, 4971.TW): High-end MBE epitaxy player focused on compound semiconductor wafers for advanced optical and RF applications.

Midstream – Optical Components, FAU & Modules

FOCI Fiber Optic Communications, Inc. (3363.TW): Leading FAU manufacturer and important TSMC COUPE ecosystem partner with direct exposure to NVIDIA’s CPO supply chain. (recommended by serenity) (Directly listed in NVIDIA CPO ecosystem per Goldman Sachs Exhibit 21 — high likelihood of being mentioned at GTC)

-Browave Corporation (3163.TW): Major supplier of passive optical components and high-density FAU solutions for CPO interconnects. (Directly listed in NVIDIA CPO ecosystem per Goldman Sachs Exhibit 21 — high likelihood of being mentioned at GTC)

-PCL Technologies Inc. (4977.TW): High-speed optical transceiver and CPO module specialist closely tied to Broadcom’s platforms.

-EZconn Corporation (6442.TW): Optical communication passive components and high-frequency RF connectors, benefiting from data center and 5G/AI demand. (光聖)

-Luxnet Corporation (4979.TW): Active optical components supplier, particularly to Marvell’s high-speed module ecosystem. (華星光)

-Shunsin Technology (Shunsin-KY, 6451.TW): Foxconn-affiliated SiP and optical module packaging leader actively ramping CPO solutions. (recommended by serenity)(Notable NVIDIA CPO supply chain exposure via Foxconn — potential GTC mention)

-GCS Holdings / GCS (4991.TW): Compound semiconductor epitaxy and foundry services supporting optical and RF applications in the CPO chain.

Downstream – Packaging, Testing & Systems

Msscorps Co., Ltd. (6830.TW): Leader in advanced materials analysis and specialized testing equipment for silicon photonics and CPO qualification. (recommended by serenity) (Direct NVIDIA CPO-related orders — potential GTC mention)

Nextronics Precision Industrial Co., Ltd. (8147.TW): Precision connector and interconnect solutions supporting high-speed optical and CPO systems. (正淩, recommended by serenity) (Direct NVIDIA CPO supply chain exposure — potential GTC mention)

Accton Technology Corp. (2345.TW): High-performance networking switch provider positioned for CPO-enabled AI switches and scale-out infrastructure.

Elite Advanced Laser Corporation (3450.TW): Advanced packaging and testing player supporting the broader CPO assembly chain.

These companies collectively cover the full CPO value chain that Taiwan offers. Several have confirmed or publicly discussed exposure to NVIDIA’s CPO programs (either directly or through key partners like Foxconn and TSMC), making them more likely to appear in supply-chain discussions around NVIDIA GTC events. Just some ideas from me for an event speculation. DYOR!

$NVDA $TSM #CPO #GTC #Taiwanstocks

8

23

120

32,158

Jay retweeted

May 24

War ending Lisa su Jensen Huang NVIDIA Taipei GTC/Computex = Wonder Week ahead!😁

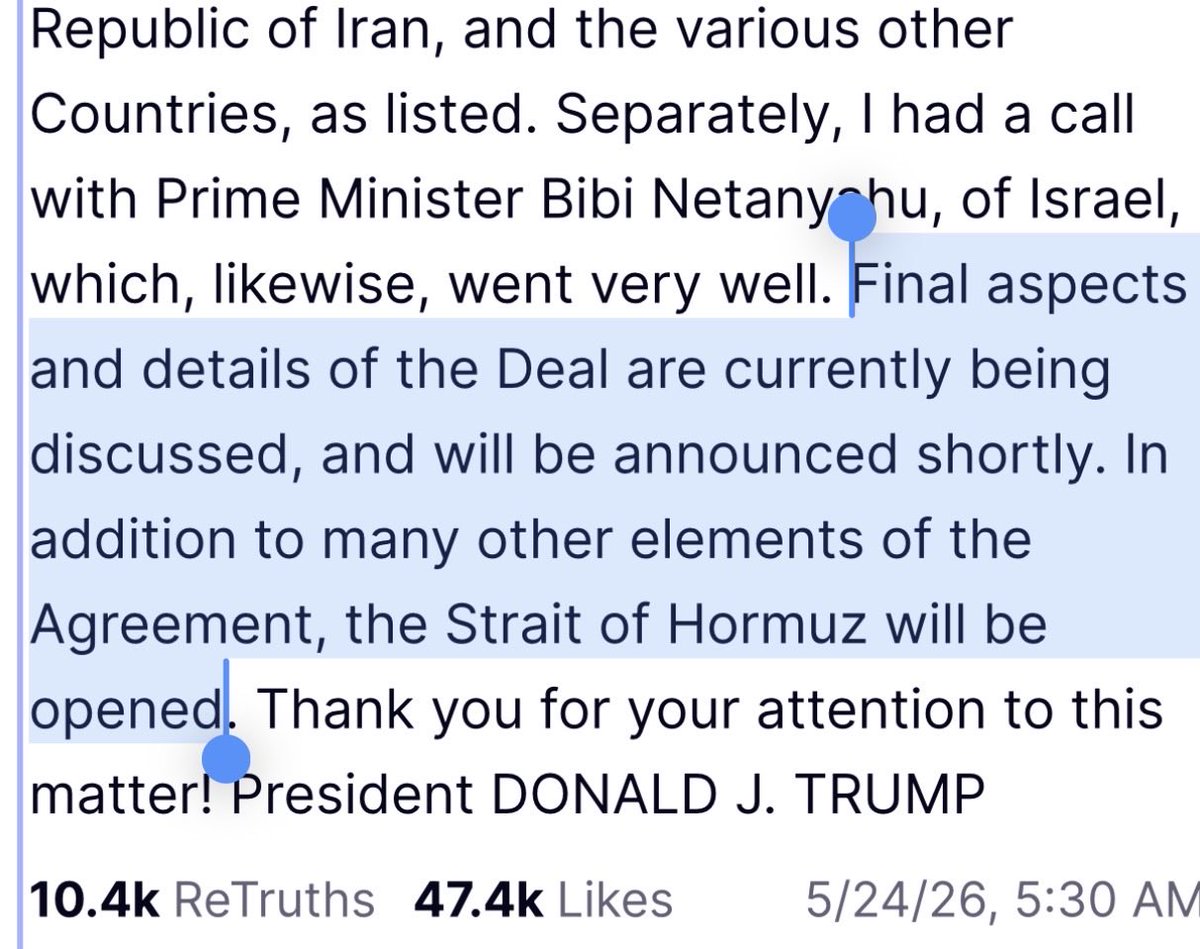

May 24

Well, looks like Iran War is about to end.

Markets/Indexes are probably going like this Monday.

Probably even better for Europe/Taiwan/Korean equities that were dragged down more from oil fears.

If something goes up during this time… probably goes higher in better macro.

2

1

20

2,898

Jay retweeted

May 17

🚨🚨 Restablecer el sistema linfático...

Dr. Alan Mandell ayudó a las personas con diversos problemas durante más de 20 años...

Obtuvo su B.A. y M.D. y muchos otros premios...

Él no usa ninguna basura de farmacia, solo usa remedios populares probados a lo largo de los años.

► ¿Dormirse en 2 minutos?

► Un vaso al día durante 1 semana para un estómago plano.

► Presione 1 punto para dolor de estómago, náuseas, hinchazón o gases.

► Una técnica de dos minutos eliminará la secreción nasal y la congestión nasal.

1

90

202

5,972

$PENG

펭귄 솔루션

펭귄 솔루션 리서치 하다 찾은 아티클 공유합니다.

투자자분들께서 참고 하시기 좋은 내용이라 생각합니다.

Penguin Solutions, Inc.는 AI 추론에서 중요한 “메모리 장벽(memory wall)” 문제를 해결하기 위해 CXL 메모리 기술을 활용한 업계 최초의 상용화-ready KV 캐시 서버인 Penguin Solutions MemoryAI KV 캐시 서버를 발표했습니다. 이 혁신적인 솔루션은 최대 11TB의 CXL 기반 메모리를 제공하여 엔터프라이즈 규모의 추론(에이전틱 AI 포함) 성능을 최적화하도록 설계되었습니다. 그 결과, 지연 시간 감소, 처리량 증가, GPU 클러스터 효율 향상, 엄격한 SLA 달성, 그리고 더 빠른 TTFT(Time-to-First-Token)를 실현합니다.

Penguin Solutions MemoryAI KV 캐시 서버는 AI 추론에서의 메모리 병목 문제를 해결하기 위해 CXL 메모리를 활용한 업계 최초의 상용 제품입니다. 이 솔루션은 최대 11TB의 CXL 기반 메모리를 제공하여 엔터프라이즈급 추론 성능을 극대화하도록 설계되었습니다.

모델 학습과 튜닝이 주로 컴퓨팅 중심(Compute-bound)이며 간헐적으로 이루어지는 반면, 실제 서비스 환경에서의 추론 및 에이전틱 AI 워크로드는 지속적이고 메모리 중심(memory-bound)이며 지연에 매우 민감한 특성을 가집니다. 일반적으로 추론은 약 30%가 GPU 연산, 70%가 메모리 의존적이기 때문에 더 큰 메모리 용량이 요구되며 이는 성능 병목과 GPU 유휴 시간 증가를 초래합니다. Penguin의 MemoryAI KV 캐시 서버는 3TB DDR5 메인 메모리와 최대 8개의 1TB CXL 추가 카드(AIC)를 통합하여 이러한 메모리 의존 프로세스를 가속화합니다.

Penguin Solutions의 CTO Phil Pokorny는 “CXL 기반 KV 캐시 기술은 TTFT를 단축하고, 토큰당 처리 시간을 줄이며, 전체 토큰 처리량을 향상시킨다”고 말했습니다. 그는 이어 “이러한 성능 개선은 낮은 지연과 빠른 응답을 요구하는 다수 사용자 환경에서의 엔터프라이즈급 추론을 가능하게 하며, 모델 크기, 컨텍스트 윈도우, 정밀도, 동시성 요구가 계속 증가하는 상황에서도 일관된 서비스 수준을 유지할 수 있도록 한다”고 덧붙였습니다.

GPU에 사용 가능한 메모리를 크게 확장함으로써 이 서버는 GPU 메모리 대역폭 제한을 완화하고, 중복 계산을 줄이며, 추론 성능 중심으로 클러스터를 최적화할 수 있게 합니다. 또한 시스템 효율이 향상되어 더 큰 모델 학습과 대규모 데이터 처리 속도도 개선됩니다.

6

29

155

49,317

Jay retweeted

May 16

If someone told you there was a $2.5 billion company partnered with $NVDA, $AMD, $INTC, $DELL, and SK Hynix you would think the market cap would be crazy high, but it’s not.

That company is $PENG. And the more I sit with it the more comfortable I get.

Here is why the risk feels so low to me.

AI infrastructure spending is not slowing down. Every hyperscaler just raised capex guidance again.

$NVDA is supply constrained not demand constrained. Every GPU cluster being deployed needs memory systems, networking, and compute infrastructure built around it.

That is exactly what $PENG builds and integrates. The demand tailwind behind this company is not a 2026 story. It is a decade long story.

When the macro gets choppy and people start asking which AI stocks are actually safe the answer is the ones with real revenue, real customers, and real partnerships with the companies that are guaranteed to win regardless of which chip architecture prevails.

$PENG has all of that.

$NVDA validates your GPU thesis. $AMD validates your CPU thesis. SK Hynix validates your memory thesis. $PENG sits at the intersection of all three and captures systems revenue on every single deployment.

And then the $MRVL photonic memory partnership is still sitting completely unpriced. The Photonic Memory Appliance being built right now.

$MRVL guiding $1 billion on the Photonic Fabric platform by FY29. $PENG builds the box. Zero dollars of that in any model today.

$2.5 billion market cap. Partnered with the most important names in compute. Real revenue. Real customers. Demand that is going nowhere.

The risk profile on this one is a lot lower than people think.

16

33

277

22,950

Jay retweeted

May 16

FII Vera Rubin Rumor & CPO Order Upgrade for Shunsin (TWE:6451):

• Unofficial source (FII Earnings Call’s lunch gathering ) claim FII has secured major involvement in NVIDIA’s Vera Rubin platform (August mass production, ~60% share on key components, doubled GB server shipments to ~60k units, and >10k racks). money.udn.com

• Taiwanese media (Economic Daily News, May 13) reports Foxconn has begun early CPO full-optical switch shipments to NVIDIA, with targets sharply upgraded to over 50,000 units combined for 2026–2027 (from original ~10k estimate). money.udn.com

• Shunsin (TWE:6451), Foxconn group’s key subsidiary for high-speed optical transceiver modules and CPO technology, is positioned in the “optics” segment that FII is reportedly sourcing externally while integrating most other components in-house.

• If realized, the elevated CPO volumes could drive increased intra-group demand for Shunsin’s optical interconnect solutions.

Conclusion: This combination points to another potential positive development for Shunsin (TWE:6451) within the Foxconn AI supply chain..

#市場小作文 #RUMOR

工业富联午餐交流反馈

业绩:4月单月营收突破1000亿,上半年突破5000亿

Vera Rubin交货进展

-Vera Rubin没有延期,为了做得更好,组装有一些改样,8月量产,9月出货

-富联做了6成份额,做了两个大客户,都是独供

-Switch 和 compute tray都是富联做的,midplane 也是富联做的,就剩一个光

-Compute tray midplane 已经开始生产,用的胜宏板子,44层,这是个标准品,所有CSP代工厂都要跟富联买

-VR现在一个柜子1800公斤,单价700-800万美金

-存储柜子富联做的比较多

英伟达服务器出货量

-GB 今年出货量翻倍,达到6万台;VR今年出货量会远超1万台

英伟达服务器零部件

-富联增加垂直整合能力,富联自己可以做冷却系统,电源系统,增加获利能力,不会是富联独供,也会分出去

-英伟达服务器内部60-65%零部件可以自己做,但其中一半会从外面买,争取剩下30%多自己做,现在已经有20%多是自己做了,后面还有10个点提升空间,这些产品毛利率通常高过15%

重视自动化和电源

-富联今年CAPEX 超过500亿,光自动化设备就会有300亿(强瑞,安达,博众,汇川),强瑞和安达智能很快就会接到很多单子

-数据中心最大考验是电力,以前不能投资电力,现在开始自己投资电力

-新厂在建设800V(从400V变800V),要考虑能耗,比较省电,效率比较高,需要考虑SiC的变化

-存储一定会有问题,长鑫产能包出去了都不够,预计2-3年还会有挤压

ASIC服务器进展

-asic 机柜营收过去占比是20%,今年占比超过30%

-1Q26 asic机柜营收翻了三倍

-富联来自谷歌和AWS的收入今年都会翻倍

CPO

-今年努力做到1万台,好几个工厂在不同地区做这个;明年做几万柜。

#零級分

2

3

51

8,215

Jay retweeted

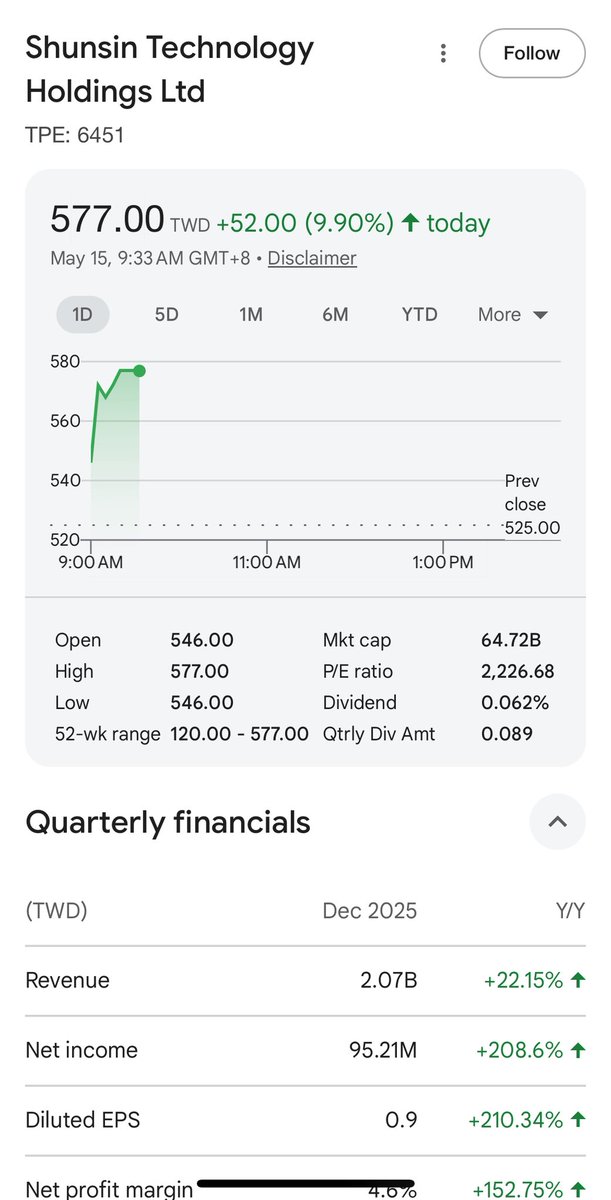

May 15

You guys should have listened…

May 14

Serenity’s High Conviction Bet: ShunSin (6451.TW) – Pre-Market Supplement:

I have a few quick points to add before the market opens. Hope everyone uses today’s earnings volatility as the perfect chance to get on board!

1. Earnings Loss Interpretation:

According to TWSE (Taiwan Stock Exchange) rules, stocks that enter “disposition” must publish monthly financial reports. ShunSin triggered disposition twice in the past two months, so the Q1 loss was already fully disclosed as known information. Even with the known loss, the stock still rose more than 200%. The reason is obvious. For the deeper context, check my earlier post on the subtle implications behind ShunSin’s material announcements clarifying earnings forecasts in the Taiwan market.

2. NVDA 50,000-unit Full-Optical CPO Switch Rerate:

Market rumors first claimed ShunSin landed a major Broadcom order that would drive 2026-2027 EPS up 1,200% (credibility of that news can be judged from the latent analysis above). That speculation alone pushed the stock to around NT$500. On top of that, fresh rumors of accelerated NVDA CPO timelines and Foxconn increasing its full-optical CPO switch orders to 50,000 units. Once you understand ShunSin’s critical role in the Foxconn ecosystem, it becomes clear they can essentially capture almost the entire order.

Here’s a simple forward EPS valuation model for this piece:

50,000 units× USD10k packaging value = USD500 million additional revenue

→ 25% gross margin contributes NT$3.925 billion gross profit

→ After deducting incremental operating expenses (conservative 10%) 20% tax → contributes approx. NT$1.88 billion after-tax net profit

→ EPS contribution ≈ NT$16.8 (for 2026-2027 combined, based on 112 million shares outstanding)

If we also factor in the existing 800G traditional optical modules plus the Broadcom major order, the overall 2026-2027 EPS outlook points to NT$25–30. Applying a typical 40–60x P/E multiple for Taiwan’s CPO sector, the reasonable target price has enormous upside imagination space.

Summary:

Earnings misses are often the best time to test real conviction in a stock. Once you truly understand ShunSin’s “full-capture” position for high-end orders in the Foxconn ecosystem, you’ll see why NT$500 is just the starting point of the speculation — not the end.

Today’s earnings shakeout is your last easy boarding opportunity before the CPO ramp truly begins! 🚀

#ShunSin #TWO.6451 #CPO #SiliconPhotonics #NVDA #Foxconn

3

1

17

4,183

Jay retweeted

May 15

Most foreign investors really didn’t realize this….

NVDA’s 50k-unit CPO full-optical switch order is a

50,000 Unit* 100,000 USD/per Unit=5 billion USD PO….

Yet Shunsin (6451.TW), the critical Foxconn CPO packaging player, has a market cap of only < $2B…

#foxconn, #NVDA

Taiwanese media reports that Foxconn has begun early shipments of all-optical CPO switch racks to NVIDIA, with shipment forecasts revised upward from the prior 10,000 units in 2026 to 50,000 units across 2026–2027.

According to industry sources, Hon Hai Group is producing the all-optical CPO switch racks at its Vietnam plant and has already begun early shipments to NVIDIA. Supply is reportedly extremely tight — even the units originally allocated for demo purposes have been diverted to NVIDIA, leaving "not a single rack to spare."

6

4

60

15,696

Jay retweeted

May 14

Market rumors: Finisar optical modules price increase by 15-20%, mirroring the recent surge in memory prices. This once again confirms the logic of this chart. 🚀

‘’Finisar’’ is a subsidiary of $COHR (Coherent Corp.). The recent price increase in optical modules signals tight supply in the market, which has significantly enhanced the bargaining power of optical module suppliers

1

2

22

4,761

Jay retweeted

May 13

Shunsin (TWE:6451) Q1 2026 Earnings

Consolidated Revenue: NT$1.553 billion (YoY -21.4%)

Gross Profit: NT$186 million (Gross Margin ~11.96%, YoY improvement)

Operating Loss: Approximately NT$80 million (Operating Expenses NT$266 million, YoY 5%)

Pre-tax Net Loss: Approximately NT$85 million

Net Loss Attributable to Parent Company: Approximately NT$154 million (EPS: -NT$1.45)

Analysis of the Loss:

Shunsin is strategically shifting its focus from legacy consumer electronics applications — including mobile RF front-end modules, power amplifiers (PAs), and MEMS/biometric sensors — toward high-margin AI datacom solutions, next-generation Co-Packaged Optics (CPO), and Silicon Photonics (SiPh), leveraging its core System-in-Package (SiP) packaging capabilities.

This transition, combined with differences in customer ramp timing and shipment schedules during the early stages of high-speed optical deployment, has resulted in short-term consolidated revenue fluctuations.

Importantly, gross margin improved year-over-year despite the revenue decline, indicating that higher-value products are increasing in contribution. This suggests that the company’s product mix optimization is beginning to take effect.

Meanwhile, operating expenses increased modestly, reflecting continued investments in capacity expansion and organizational preparation to support future growth in AI-related optical communications.

Overall, the results are consistent with a transitional phase of strategic repositioning, characterized by short-term revenue pressure but improving product mix and long-term positioning in high-speed optical technologies.

Sourced from:

moneydj.com/kmdj/news/newsvi…

2

1

30

4,200

Jay retweeted

May 14

Serenity’s High Conviction Bet: ShunSin (6451.TW) – Pre-Market Supplement:

I have a few quick points to add before the market opens. Hope everyone uses today’s earnings volatility as the perfect chance to get on board!

1. Earnings Loss Interpretation:

According to TWSE (Taiwan Stock Exchange) rules, stocks that enter “disposition” must publish monthly financial reports. ShunSin triggered disposition twice in the past two months, so the Q1 loss was already fully disclosed as known information. Even with the known loss, the stock still rose more than 200%. The reason is obvious. For the deeper context, check my earlier post on the subtle implications behind ShunSin’s material announcements clarifying earnings forecasts in the Taiwan market.

2. NVDA 50,000-unit Full-Optical CPO Switch Rerate:

Market rumors first claimed ShunSin landed a major Broadcom order that would drive 2026-2027 EPS up 1,200% (credibility of that news can be judged from the latent analysis above). That speculation alone pushed the stock to around NT$500. On top of that, fresh rumors of accelerated NVDA CPO timelines and Foxconn increasing its full-optical CPO switch orders to 50,000 units. Once you understand ShunSin’s critical role in the Foxconn ecosystem, it becomes clear they can essentially capture almost the entire order.

Here’s a simple forward EPS valuation model for this piece:

50,000 units× USD10k packaging value = USD500 million additional revenue

→ 25% gross margin contributes NT$3.925 billion gross profit

→ After deducting incremental operating expenses (conservative 10%) 20% tax → contributes approx. NT$1.88 billion after-tax net profit

→ EPS contribution ≈ NT$16.8 (for 2026-2027 combined, based on 112 million shares outstanding)

If we also factor in the existing 800G traditional optical modules plus the Broadcom major order, the overall 2026-2027 EPS outlook points to NT$25–30. Applying a typical 40–60x P/E multiple for Taiwan’s CPO sector, the reasonable target price has enormous upside imagination space.

Summary:

Earnings misses are often the best time to test real conviction in a stock. Once you truly understand ShunSin’s “full-capture” position for high-end orders in the Foxconn ecosystem, you’ll see why NT$500 is just the starting point of the speculation — not the end.

Today’s earnings shakeout is your last easy boarding opportunity before the CPO ramp truly begins! 🚀

#ShunSin #TWO.6451 #CPO #SiliconPhotonics #NVDA #Foxconn

5

6

58

19,486