Jun 11

📊⚡ Pillar: Options Mechanics

Theta in Plain English

🧊 An option is a melting ice cube.

Every minute the market is open ⏳ — and many when it isn't 🌙 — your option is losing time value.

The closer you get to expiry...

🔥 The faster it melts.

Especially for:

🎯 ATM (At-The-Money) Options

These carry the highest time value and therefore experience the fastest theta decay.

⚠️ The math is brutal:

An ATM weekly option can lose 40–60% of its value in the final 2 days even if the underlying barely moves. 📉🧊

Many retail option buyers focus on:

📈 Direction

📊 Breakouts

🚀 Targets

But ignore the hidden cost:

⏳ Time Decay

A correct market view can still lose money if the move isn't fast enough.

💡 Before buying any option, ask:

🎯 "How much movement do I need?"

🎯 "How fast do I need it?"

🎯 "Is theta working against me?"

Direction matters.

But speed matters too. ⚡

#OptionsTrading #ThetaDecay #OptionBuying #OptionsMechanics #NiftyOptions #BankNifty #TradingPsychology #ImpliedVolatility #RiskManagement #TraderMindset #WeeklyExpiry #MarketEducation 📊🧊⚡🚀

44

$SOXL $MU $SPY 📡 IV Radar

🔴 SOXL — IV Rank 100 | ATM IV 251% | RR -23.5% | Bearish skew

🔴 MU — IV Rank 97 | ATM IV 116% | RR -17.8% | Bearish skew

🔴 SPY — IV Rank 86 | ATM IV 18.4% | RR -37.4% |

#Options #ImpliedVolatility #OptionsFlow #IV

hpsilab.com

215

Jun 10

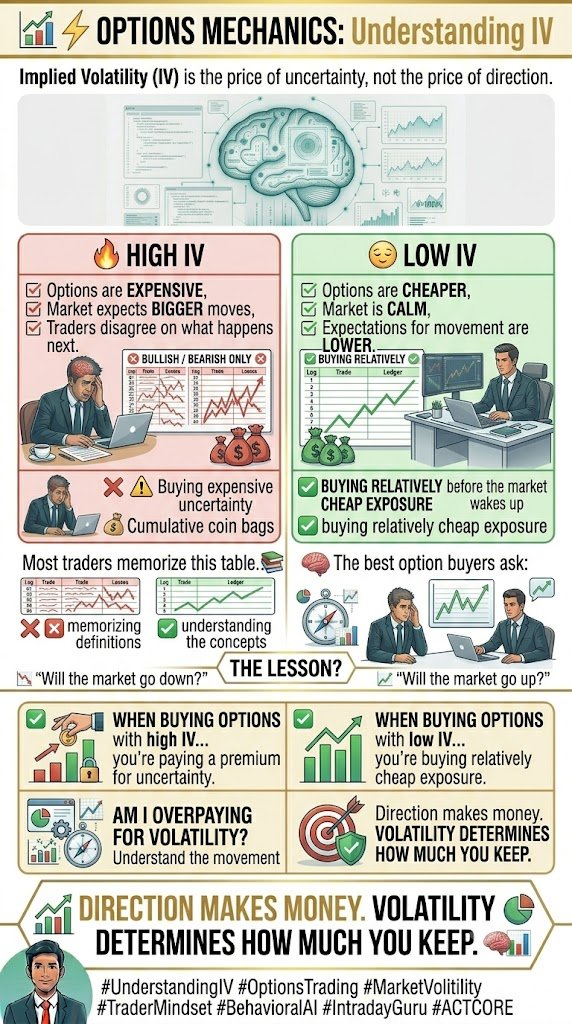

📊⚡ Options Mechanics: Understanding IV

Implied Volatility (IV) is the price of uncertainty, not the price of direction.

🔥 High IV

= Options are expensive

= The market expects bigger moves

= Traders disagree on what happens next

😌 Low IV

= Options are cheaper

= The market is calm

= Expectations for movement are lower

Many traders make a critical mistake:

❌ They buy options simply because they're bullish or bearish.

But direction alone isn't enough.

💡 When you buy options with high IV, you're paying a premium for uncertainty.

💡 When you buy options with low IV, you're buying relatively cheap exposure before the market wakes up.

The best option buyers don't just ask:

📈 "Will the market go up?"

📉 "Will the market go down?"

They also ask:

🎯 "Am I overpaying for volatility?"

Direction makes money.

Volatility determines how much you keep. 🧠📊

#OptionsTrading #ImpliedVolatility #IV #OptionBuying #NiftyOptions #BankNifty #TradingEducation #OptionsMechanics #Volatility #TraderMindset #RiskManagement #MarketWisdom 📊⚡🚀

25

Jun 9

You can be 100% right on direction and still lose money. That's Vega - the Greek nobody warns you about.

Vega measures how much your option's price moves when implied volatility shifts by one percentage point. Not the stock. The market's expectation of how much the stock will move.

Here's the trap that catches new buyers every earnings season:

Stock sits at $100. You buy the $100 call, 30 days out. IV is 80% because earnings are tomorrow - the option is loaded with fear premium. Earnings hit. The stock... stays at $100. You were dead right on direction. But IV collapses from 80% to 30%, and your call loses most of its value anyway.

That's IV crush. Vega is the dial that does the damage.

In OptionsLabPro's Greeks Explorer, the "Vega vs IV" chart shows exactly how much price you're exposed to per IV point. Then open the IV Crush simulator: pin the spot at $100, drag the IV slider from 80 down to 30, and watch the option value bleed out without the stock moving a single cent.

Feel that one drop and you'll never buy a naked call into earnings the same way again.

Try it yourself: optionslabpro.com

$TSLA #ImpliedVolatility #FeelTheMarket

31

Ever heard of implied volatility? It’s the market's fear gauge! 📉

This number reflects what traders expect for future price swings based on current options prices. Unlike historical volatility, which looks back, implied volatility gives insight into potential market uncertainties ahead. When fear rises, so does this figure!

Understanding it can sharpen your trading decisions.

#ImpliedVolatility #MarketTrends #TradingTips #Finance #Investing #StockMarket

9

Ever wondered how implied volatility can shift an option's price? 🤔 Meet Vega!

Vega shows us how sensitive an option is to changes in implied volatility. And here's the kicker: longer-dated options are even more sensitive! Understanding this can enhance your trading strategy.

#Options #Vega #TradingTips #ImpliedVolatility #MarketInsights

16

In October 1997, two men won the Nobel Prize in Economics.

Their formula, they said, could price any option in the world with perfect mathematical precision. The committee called it one of the greatest discoveries in modern finance.

Twelve months later, the Federal Reserve had to call an emergency meeting to prevent their hedge fund from collapsing the global financial system.

This is the story of Implied Volatility , and the most expensive lesson in the history of options trading.

Their names were Myron Scholes and Robert Merton. Together with John Meriwether, they ran Long-Term Capital Management " LTCM " out of Greenwich, Connecticut.

The strategy was elegant. Their models showed that volatility in financial markets always reverts to normal. When fear spikes, it eventually calms. So they did something simple: they sold that fear.

Every time the market priced options expensively , because traders were scared , LTCM sold those options. They collected the premium. Then waited for calm to return.

For four years, they were right.

1994: 21%. 1995: 43%. 1996: 41%.

At their peak, they controlled $126 billion in positions with just $7.5 billion in equity. A leverage ratio of 25 to 1. The best minds on Wall Street sent them money. The models were perfect.

Then in August 1998, Russia defaulted on its debt.

The market didn't calm down. Volatility didn't revert. Fear didn't fade. It exploded , and kept exploding. Their models had never seen anything like it. Because their models assumed the world was normal.

The world was not normal.

LTCM lost $4.6 billion in five weeks. 90% of their equity — gone. The Federal Reserve called the 14 largest banks on Wall Street into a room and told them to write a $3.6 billion check. Not a request. A warning.

Because if LTCM unwound their positions , markets worldwide would collapse.

So what is Implied Volatility?

IV is not the price of an option. IV is the fear the market has baked into that price.

→ When IV is low — options are cheap. The market is calm. Sellers collect premium. → When IV spikes options become expensive. The market is panicking. Sellers face ruin. → LTCM's fatal mistake: they assumed IV always comes back down. Russia proved it doesn't have to.

In $BTC options, IV explodes before every major move. When you see it spike , the market is pricing a storm. You can buy that storm. You can sell into it. But you cannot ignore it and call yourself a trader.

LTCM had two Nobel Prize winners and 125 PhD's.

They forgot one thing: the market does not care about your model.

Markets can stay irrational longer than you can stay solvent.

#Bitcoin #BTC #CryptoOptions #ImpliedVolatility #OptionsTrading #LTCM #CryptoEducation #Web3 #Crypto

103

Jun 3

Did you know? IV Rank and IV Percentile aren't the same thing — and the difference can wreck a "sell premium when IV is high" setup.

IV Rank asks: where is current IV in the 52-week high-low range?

IV Percentile asks: on what % of days over the past year was IV lower than today?

Sounds similar. They diverge fast when one outlier IV spike skews the range.

Example: a stock's IV ranged 20% – 80% over the year. Current IV = 50%.

- IV Rank = (50 − 20) / (80 − 20) = 50%. "Mid-range, neutral."

- But that 80% high was a 3-day earnings spike. Most days IV sat 25% – 40%. Current IV of 50% is actually higher than ~85% of trading days. IV Percentile = 85%.

So Rank says "meh, neutral" while Percentile screams "premium is rich."

That's the gap that catches premium sellers. You think you're getting average juice. You're actually selling when IV is expensive relative to how the stock usually trades.

The fix: check both before sizing a credit spread or iron condor. If they disagree by more than 30 points, the underlying has a fat-tail IV distribution — adjust width, take less risk.

Drag the IV slider in the Greeks Explorer and watch Vega reprice the chain. You feel the difference instantly: a 10-point IV move on a low-IV name swings premium more than you'd guess.

Try it yourself with virtual capital: optionslabpro.com

$TSLA #ImpliedVolatility #thetagang #FeelTheMarket

23

Jun 3

Options Trading Secrets: Using Implied Volatility Patterns To Understand Price Action Probabilities - Learn How You Can Spot Setups Before Retail Traders Get Trapped #Options #OptionsTrading #ImpliedVolatility #IV #Volatility #Trading #DayTrading #SwingTrading #OptionsStrategy

74

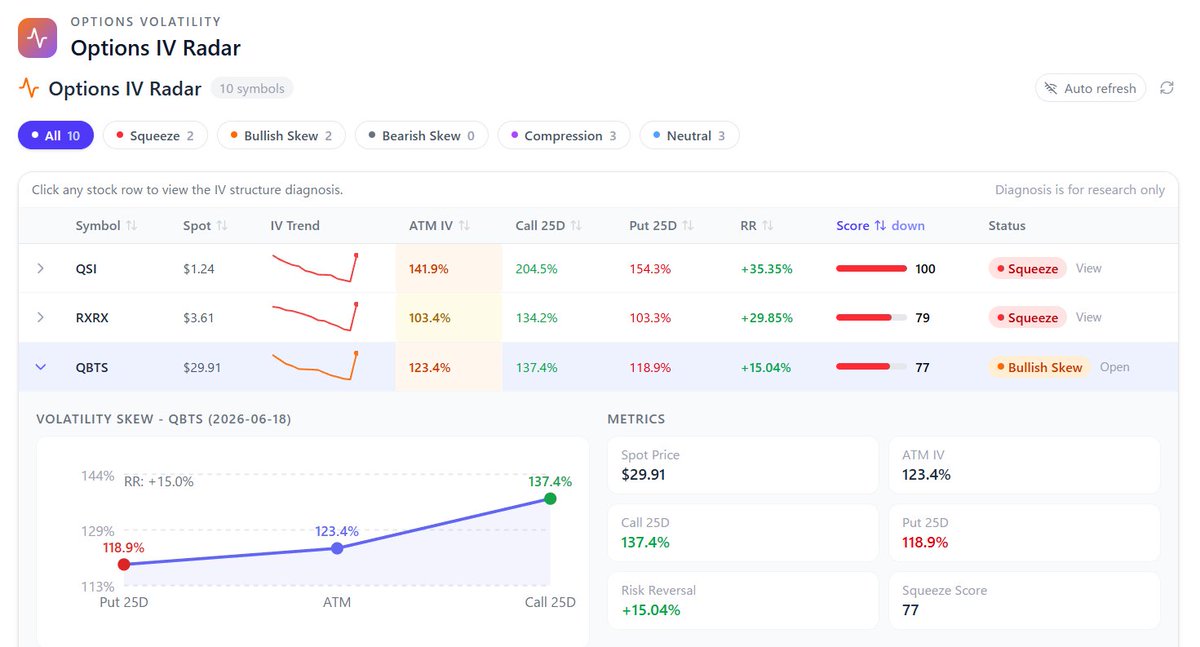

Options IV Radar.

Implied volatility = what the market fears. Risk reversal = which direction it's leaning. Squeeze Score = how coiled the tension is.

No noise. Just signal. 👉 hpsilab.com

#OptionsTrading #ImpliedVolatility #FinTech #BuildInPublic #QuantFinance

17

May 31

Implied volatility is a key concept in options trading that reflects the market’s expectation of how much an asset’s price may move in the future. It does not indicate direction but rather the expected level of uncertainty or movement in the market.

When implied volatility increases, option premiums tend to rise because traders expect larger price swings. When it decreases, option prices generally become cheaper due to lower expected movement. This makes volatility a major factor in determining option pricing and strategy selection.

Traders often use implied volatility to evaluate whether options are overpriced or underpriced and to decide which strategies fit current market conditions. High volatility environments may support premium-selling strategies, while low volatility conditions may favor premium buying approaches.

By combining implied volatility analysis with broader market research, traders can improve timing, manage risk more effectively, and make more informed trading decisions.

Volatility Index in Trading Strategy: youtu.be/Lz1x-EC_EMI

#ImpliedVolatility #OptionsTrading #TradingEducation #StockMarket #TradingStrategies

17

May 30

Avoid This Delta Trap — Master Implied Volatility & Win More Trades 🚨📈Are you an options trader struggling with weird Delta behavior and unpredictable IV? Learn some practical tips! #optionstrading #deltatrading #impliedvolatility #IV #optionsgreeks

48

World Markets are acting Thunderous.⛈️

#stock #stocks #sensex #finance #money #economy #impliedVolatility #IntrinsicValue #ExtrinsicValue #PCR #PutCallRatio

5

127

Most traders watch implied volatility. The real edge is in the spread between implied and realized vol.

When IV is running 15 points above realized on a name with no catalyst on the calendar, someone is paying for protection that the market doesn't justify. That positioning tells you more than the price action ever will.

Do you trade the vol spread or just the direction? 🤔

#OptionsFlow #ImpliedVolatility #Vesel

1

30

Bitcoin's implied volatility has fallen to its lowest point in a year, a development that market analysts say historically precedes a sharp price movement. #BITCOIN #CryptoOptions #DVOL #Glassnode #impliedvolatility

bitcoinworld.co.in/bitcoin-i…

34

Bitcoin's implied volatility has fallen to its lowest level in eight months, a development that typically signals market calm. #$BTC #BITCOIN #Derivatives #impliedvolatility #shortsqueeze

bitcoinworld.co.in/bitcoin-s…

24

May 25

Expected move vs actual move 👀⚡

That’s Implied vs Realized Volatility.

#ImpliedVolatility #RealizedVolatility #OptionsTrading #Volatility #OptionTrading #MarketVolatility #TradingEducation #StockMarketIndia #Derivatives #TradingStrategy #OptionsMarket #IV #FinanceTwitter

30

🔥 BULLISH

Bitcoin Implied Volatility Hits 7-Month Low as Institutional Demand Builds a Structural Floor!

Bitcoin's implied vol just hit a 7-month low — BVIV at 38% 📊 — as Strategy's 171K BTC in 2026 purchases build a structural floor, institutional call overwriters flood supply, and Iran risk fade…

$BTC #ImpliedVolatility #InstitutionalDemand

Read more 👇 zippfeed.com/uzj5dQuq/en-US

2

30