KOEL Investment Thesis — Identifying the Core Drivers of Upside

At first glance, KOEL appears to be a traditional industrial company benefiting from the capex cycle. But underneath, the business is gradually shifting toward higher-value, technology-led integrated power systems.

The thesis broadly rests on three layers.

HHP gensets, exports and aftermarket expansion

The second is capability building in high-end segments like 6 MW marine propulsion engines and 6.3 MW nuclear-grade gensets, where entry barriers are high and credibility compounds over time.

The third is optionality — areas like gas gensets, hydrogen-blend engines, and microgrid systems. These are still early today but could matter meaningfully over the next decade.

Let’s unpack these one by one.

open.substack.com/pub/thelog…

35

Black Coffee retweeted

✨ #HighlyCitedPaper Optimal Operation of an Industrial #Microgrid within a #RenewableEnergy Community: A Case Study of a Greentech Company

👉 brnw.ch/21x3icK

#Industry #Optimization #EnergyManagement #VehicleToGrid #V2G

#mdpienergies #openaccess

1

1

1

Elecnova is advancing flexible energy storage with a new all-in-one containerised ESS, delivering 500 kW output and over 1 MWh capacity for microgrid and backup applications.

👉 ow.ly/ZoHe50Z73Ug

#EnergyStorage #EnergyTransition #CleanEnergy #BESS #Renewables

5

40m

As the SCO marks its 25th anniversary, the China‑SCO Local Economic and Trade Cooperation Demonstration Area (SCODA) in Qingdao, east China’s Shandong Province, offers a clear answer to a key question: how energy infrastructure empowers global industrial cooperation.

It comes down to three key factors: resilience, speed, and sustainability.

A self‑healing smart microgrid–restoring power in seconds–supports micro‑level precision manufacturing and semiconductor fabrication.

Floating solar panels help produce green hydrogen, while a zero‑carbon building is 100% self-sufficient in green power.

Electricity access is in place before factories are completed, enabling businesses to start operations immediately.

From undeveloped land to a green manufacturing hub, the demonstration area shows the world that reliable energy infrastructure is a key pillar of trust in global industrial chains.

#SCO25Years #Qingdao #GreenEnergyBase

22

WASHINGTON STATE

It's just a terrible thing.

We know about the big battery storage fire in Moss Landing, California, last year (2025).

montereycountynow.com/news/l…

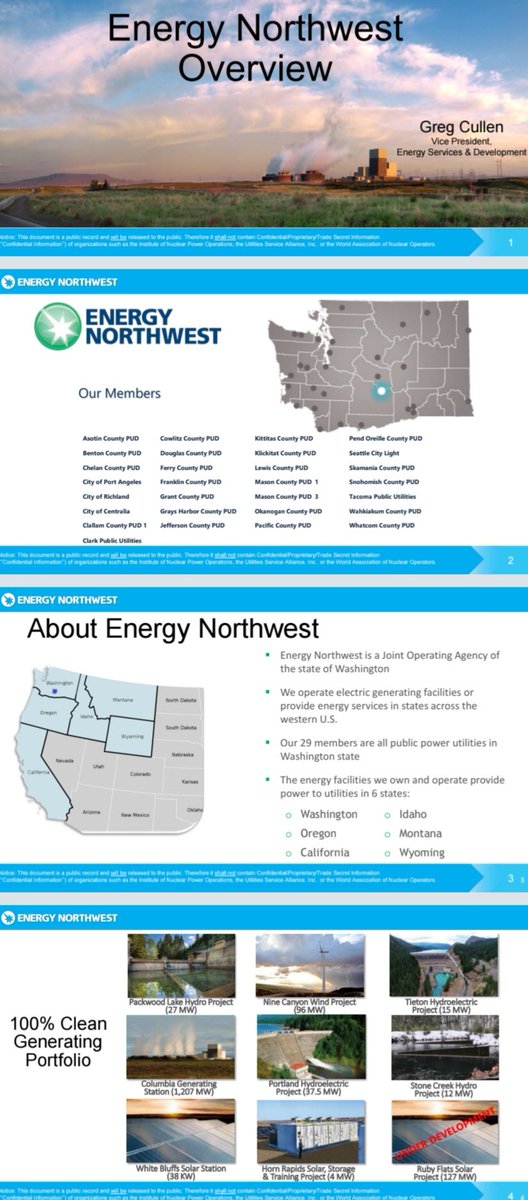

They're putting up a battery storage facility near Packwood off Hwy 12 in Eastern Lewis County, Washington State, which is surrounded by PINE TREES.

The Packwood Solar, Storage, and Microgrid (PSSM) project is a collaborative clean energy initiative in Lewis County, Washington. It is being developed by Energy Northwest (EN), Lewis County PUD (LCPUD), and Lewis County Emergency Management (LCEM).

Note: Energy Northwest has entered into multiple INTERLOCAL Agreements, which means that Energy Northwest can access Public Employee Benefits Board (PEBB).

energy-northwest.com/doing-b…

Western Energy Board, another non-profit!

westernenergyboard.org/wp-co…

You can't despise these tyrants enough.

Don't get me started on Lewis County PUD; they, too, are the ENEMY.

3

2

4

64

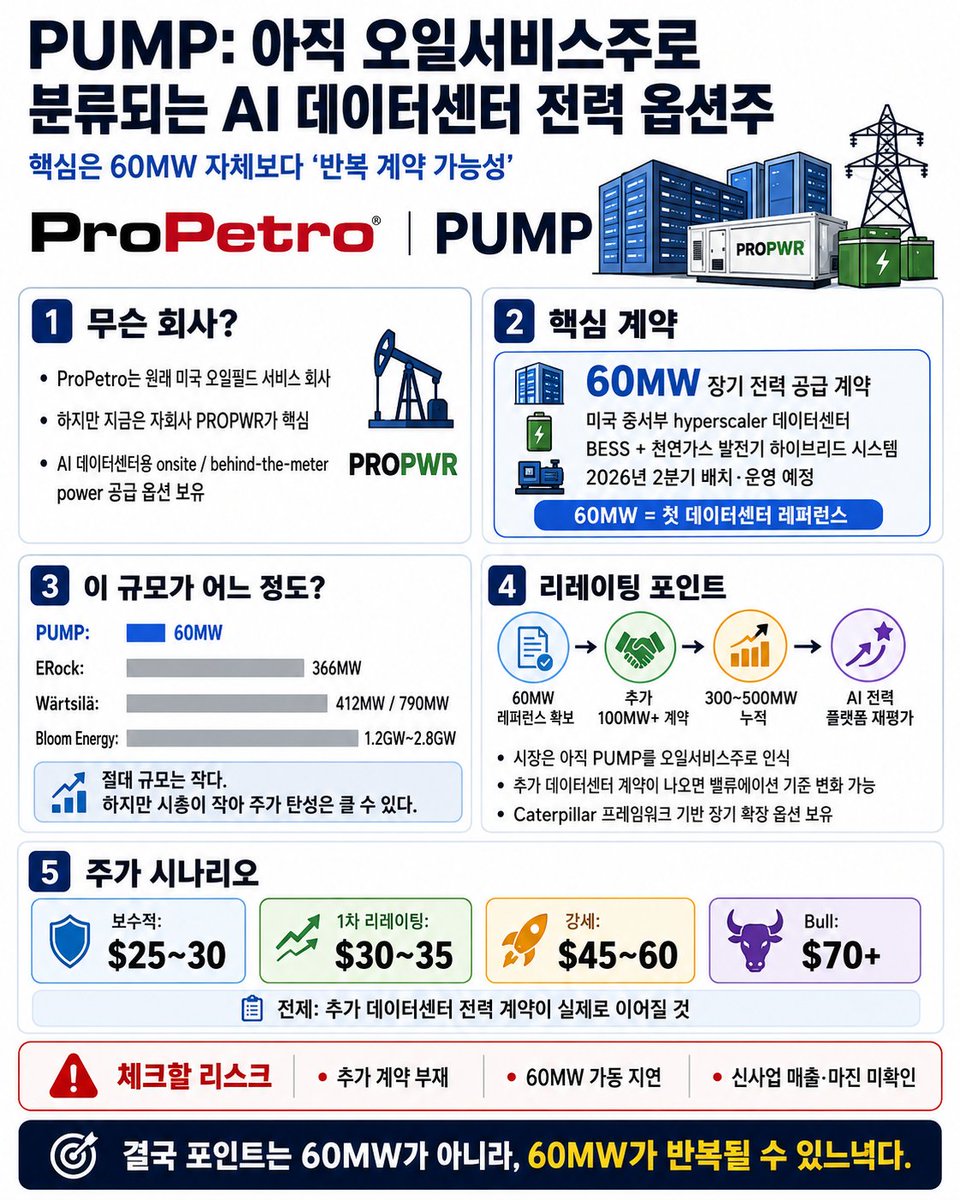

$PUMP를 보는 이유는 간단하다.

이 회사는 아직 시장에서 AI 전력 인프라주로 제대로 분류되지 않았다.

겉으로 보면 ProPetro는 미국 오일필드 서비스 회사다.

하지만 지금 봐야 할 건 본업보다 자회사 PROPWR다.

AI 데이터센터의 병목은 이제 GPU만이 아니다.

전기다.

데이터센터는 전력망 연결을 기다릴 시간이 없다.

송전망 증설은 느리고

변압기는 부족하고

가스터빈 납기는 길고

AI 서버 전력밀도는 계속 올라간다.

그래서 hyperscaler들은 전력망 바깥에서 빠르게 깔 수 있는 onsite power, behind-the-meter power, microgrid 솔루션을 찾기 시작했다.

여기서 PUMP의 PROPWR가 등장한다.

PROPWR는 미국 중서부 hyperscaler 데이터센터에 60MW 장기 전력 공급 계약을 확보했다.

이 계약은 단순 발전기 공급이 아니다.

고효율 천연가스 엔진 발전기

BESS 배터리 저장장치

빠른 부하 변동 대응

데이터센터용 안정 전력 공급

이 조합이다.

60MW가 어느 정도냐면, 24시간 365일 기준으로 연간 약 525GWh 전력 규모다.

초대형 AI 캠퍼스 전체급은 아니지만, 단일 데이터센터 전력 블록으로는 의미 있는 레퍼런스다.

다만 냉정하게 보면 60MW 자체가 엄청 큰 수주는 아니다.

Bloom Energy는 Oracle과 최대 2.8GW 규모 계약을 발표했다.

ERock은 Meta El Paso AI 데이터센터 관련 366MW onsite power 프로젝트와 연결돼 있다.

Wärtsilä는 미국 데이터센터향으로 412MW, 790MW급 엔진 발전 수주를 발표했다.

그들과 비교하면 PUMP의 60MW는 작다.

그래서 핵심은 60MW의 절대 규모가 아니다.

핵심은 이게 첫 데이터센터 레퍼런스라는 점이다.

현재 PUMP 시총은 약 18억 달러 수준이다.

Bloom은 이미 AI onsite power 대표주로 리레이팅되며 시총이 훨씬 커졌다.

ERock도 상장 초기부터 AI 데이터센터 전력주로 가격이 매겨졌다.

반면 PUMP는 아직 오일서비스주로 보는 시각이 강하다.

여기에 기회가 있다.

PROPWR는 Caterpillar와 프레임워크 계약을 통해 최소 1.5GW, 최대 2.1GW 발전 자산을 추가 확보할 수 있는 구조를 만들었다.

기존 주문분까지 합치면 장기적으로 약 2.6GW 발전 용량 확보 그림이 나온다.

정리하면 이렇다.

60MW = 첫 hyperscaler 데이터센터 레퍼런스

550MW = 이미 확보 중인 발전 자산 기반

2.6GW = 장기 플랫폼 옵션

추가 데이터센터 계약 = 리레이팅 트리거

PUMP가 계속 오일서비스주로 남으면 업사이드는 제한적이다.

하지만 PROPWR가 AI 데이터센터 전력 공급 플랫폼으로 인정받으면 이야기가 달라진다.

이 회사는 더 이상 셰일 서비스주가 아니라

AI 데이터센터 전력 병목을 우회하는 behind-the-meter power 플랫폼으로 재평가될 수 있다.

내가 보는 핵심 시나리오는 이렇다.

추가 계약이 없으면 60MW 레퍼런스 하나로 끝난다.

이 경우 PUMP는 다시 오일서비스주 밸류에이션으로 돌아갈 수 있다.

하지만 60MW 정상 가동 이후 100MW급 추가 계약이 나오면 1차 리레이팅이 가능하다.

이 경우 주가는 $25~35 구간까지 열릴 수 있다고 본다.

데이터센터 계약이 300~500MW 누적으로 커지면 이야기는 더 커진다.

이때는 시장이 PUMP를 AI 전력 옵션주로 보기 시작할 가능성이 높다.

이 경우 $45~60 구간도 가능하다고 본다.

진짜 bull case는 1GW 이상이다.

PROPWR가 Caterpillar 프레임워크를 실제 장기 데이터센터 전력 계약으로 채우기 시작하면, PUMP는 완전히 다른 멀티플을 받을 수 있다.

이 경우 $70 이상도 열릴 수 있다.

물론 리스크도 명확하다.

60MW 하나로는 부족하다.

추가 데이터센터 계약이 나와야 한다.

2026년 2분기 배치와 운영이 지연되면 안 된다.

PROPWR 매출과 마진이 숫자로 찍혀야 한다.

본업 오일서비스 부진이 신사업 기대를 덮으면 안 된다.

그래서 PUMP는 안정적인 전력기기 대형주가 아니다.

이건 고위험 리레이팅 베팅이다.

내가 보는 핵심은 하나다.

AI 전력난은 진짜다.

Bloom, ERock, Wärtsilä가 이미 데이터센터 onsite power 시장을 증명하고 있다.

PUMP는 아직 그 시장에서 완전히 가격이 매겨지지 않았다.

그래서 업사이드가 있다.

결국 PUMP의 투자 포인트는 60MW가 아니다.

60MW가 반복될 수 있느냐다.

다음에 100MW 이상 데이터센터 전력 계약이 나오면 1차 리레이팅.

300~500MW 누적 계약이 보이면 강한 리레이팅.

1GW 이상 장기계약 플랫폼으로 인정받으면 완전히 다른 회사가 될 수 있다.

PUMP는 지금 확정 실적주를 사는 게 아니다.

AI 데이터센터 전력 플랫폼으로 정체성이 바뀔 가능성을 사는 것이다.

개인 기록용 정리.

투자 조언 아님.

1

15

811

AI半導体投資日報_260614_夕刊

■夕刊の見取り図

・欧州1:Metaの社内AI利用は、需要増から費用統制の段階へ移った。

・米国1:今回の監視窓では、新規高関連記事の採用なし。

・米国2:AIデータセンター電力は、PJM、FERC、接続順序、料金負担の問題になった。

・日本1:今回の監視窓では、新規高関連記事の採用なし。

・韓国1:Lam ResearchとBCNCのエッジリング知財紛争は、装置消耗部材の価値を示した。

・台湾1:台湾市場は、AI主線をCPO、光通信、高階PCBへ広げた。

・中国1:HRM-Textは、長いCoT token以外の推論設計を示した。

■欧州1:Meta社内AIは費用統制へ移った

・THE DECODERは、Metaの社内AI利用急増を報じた。

・社内利用だけで、2026年に数十億ドル規模の費用へ向かう可能性がある。

・この材料は、AI需要が企業内で本番化している兆候である。

・一方で、需要増をGPUとHBMの需要へ直線換算できない。

・重要点は、従業員やチームがAI消費量と費用を把握できない状態が問題化した点である。

・Metaは2027年から、AI Gateway、予算配賦、利用量追跡、異常費用アラートでtokenを管理する方針とされる。

・投資上は、企業AI需要をseat数だけで見ない。

・部門別ROI、外部frontier modelと内製assistantの使い分け、model routing、cache、低価格モデル、承認制、費用上限を見る。

・token使用量だけをKPIにすると、成果ではなく消費量が増える。

・AI半導体需要を読む時は、token量、task completion、売上貢献、工数削減、品質改善を分ける。

■米国2:電力がAIデータセンターの実効容量を決める

・Axiosは、AIデータセンターの電力需要を、米国電力システムの設計問題として整理した。

・争点は発電容量だけではない。

・誰が系統増強費用を払うか。

・誰が限られた電力へ先に接続できるか。

・PJMやFERCがどのルールを作るか。

・GPU、HBM、AI ASICの発注が強くても、系統接続が遅れれば稼働率は下がる。

・その場合、売上認識、減価償却、クラウド粗利率もずれる。

・公共系統拡張なら、utility、送電、変圧器、高圧遮断器、許認可、料金負担が中心になる。

・並行電力システムなら、behind-the-meter、長期PPA、オンサイト発電、蓄電、microgridが重要になる。

・AIクラウドの競争優位は、モデル性能やGPU調達力だけでは決まらない。

・電力開発力、土地、規制対応、地域受容性が実効容量を左右する。

■台湾1:CPO・光通信・高階PCBへAI主線が広がった

・工商時報は、台湾市場でAIテーマがGPU、TSMC、HBMから光通信、CPO、高階PCBへ広がる見方を取り上げた。

・記事はAIの核心を、運算、記憶體、資料伝送の三層で整理する。

・AIサーバーの制約は、演算ダイだけではない。

・メモリ階層、通信、スイッチ、基板、光電変換、電力、冷却が同時に制約になる。

・CPOや光I/Oは、スイッチASICや光エンジンだけの話ではない。

・先端パッケージング、基板、熱、電源、テスト、光結合精度、保守方式まで含むシステム実装問題である。

・高階PCBでは、NVIDIAが大量線材中心の接続から、MidplaneやBackplaneを使う構造へ移る見方が紹介された。

・低損失材料、HVLP銅箔、T-Glass、層数、加工精度、検査、供給リードタイムを確認する。

・ただし、これは証券メディアのテーマ整理である。

・個別企業では、顧客認定、AIサーバー売上比率、価格改定、粗利率、在庫回転を見る。

■韓国1:装置消耗部材の知財は前工程の利益率を左右する

・ZDNET Koreaは、BCNCがLam Researchのエッジリング登録デザイン2件を無効化できなかったと報じた。

・エッジリングは、エッチング装置内部でプラズマを制御する消耗部材である。

・AI acceleratorやHBMを直接構成するチップではない。

・ただし、先端ロジック、DRAM、NAND、HBM関連メモリを作る前工程装置の稼働品質に関わる。

・この材料は、前工程能力を装置本体、保守、消耗部材、知財、顧客認証まで分解して見せる。

・Lam Researchの強みは、新規装置販売だけではない。

・installed baseから発生するサービス、部品、消耗品、アップグレード、知財保護にも広がる。

・韓国ローカル部材企業にも、価格と供給柔軟性で顧客に選ばれる余地が残る。

・訴訟、再設計、再認証、歩留まり影響、顧客の調達方針を確認する。

■中国1:HRM-Textは推論効率の別ルートを示した

・量子位は、Sapient IntelligenceのHRM-Textを紹介した。

・記事では、約1B parameters、約1500ドルの訓練費用、16基のH100で2日未満、約40B unique tokensという条件が示された。

・post-training、RLHF、明示的なChain-of-Thoughtデータは使わない。

・この材料を、大規模モデル不要論として読まない。

・重要点は、推論性能の伸ばし方が、parameter、token、GPU時間を増やす方向だけではなく、内部計算構造へ広がっている点である。

・HRMは、高層状態と低層状態を異なる時間尺度で更新する。

・外部に長いCoT tokenを出すのではなく、潜在空間で再帰的に状態を更新する。

・この方向が成熟すると、外に出すtokenは減る。

・一方で、内部再帰計算やtest-time computeは増える可能性がある。

・効率化をGPUとHBM需要の弱気材料と決めつけない。

・単位推論原価が下がる一方で、実験、評価、fine-tuning、agent harness、domain adaptationが増える経路もある。

■夕刊のまとめ

・今夜の材料は、AI需要の強弱ではなく、需要が投資リターンへ変わる途中の制約を示した。

・企業AIでは、利用量の増加が費用統制、model routing、内製assistantへつながる。

・AIデータセンターでは、GPUとHBMの発注より後ろで、電力接続、料金負担、規制判断が実効容量を決める。

・台湾市場では、AIサーバー価値連鎖がCPO、光通信、高階PCBへ広がる。

・韓国の装置部材紛争は、前工程装置メーカーのinstalled base価値とローカル代替の再設計リスクを示す。

・中国のHRM-Textは、CoT tokenを外へ長く出す以外の推論設計を示す。

・投資判断では、GPUとHBM需要を中心に置きつつ、電力、通信、基板、装置部材、推論原価、企業AI費用管理を同時に確認する。

1

3

503

17h

Accurate diagnosis of line-to-ground and line-to-line-to-ground faults in AC microgrid with ... sciencedirect.com/science/ar… #MachineLearning

4

Microgrid company ERock Inc., formerly known as Enchanted Rock, has started trading on the New York Stock Exchange. The CEO talked to the Houston Business Journal about the company's next chapter. bizjournals.com/houston/news…

195

$SMR --- On June 2, 2026, $SMR announced Dr. Dale Klein, former Chairman of the U.S. Nuclear Regulatory Commission (NRC), and a senior former U.S. Department of Energy official are joining its Board of Directors. For an industry critically dependent on government relations and licensing, adding the former top regulator represents the ultimate regulatory "green light" – dramatically enhancing credibility for large-scale project execution and capital raising.

During May's Q1 earnings call, $SMR confirmed shareholders of Romania's SN Nuclearelectrica formally approved advancing the Doicesti RoPower SMR plant to the next phase. This validates the project is not stalled and making tangible progress toward becoming Europe's first commercial SMR deployment.

Through core commercial partner ENTRA1 Energy, NuScale is advancing a landmark 6-GW SMR deployment program with the Tennessee Valley Authority (TVA) – one of America's largest public power providers – to deliver long-term, behind-the-meter clean baseload power across seven states.

1.The Regulatory Moat – America's Only Licensed SMR Technology

The deepest moat in nuclear isn't technology – it's regulatory approval. NuScale's light water reactor module is currently the first and only SMR technology to receive NRC Design Certification in the United States. While competitors like OKLO and NANO Nuclear (NNE) generate hype, they remain years behind NuScale in the regulatory approval queue.

2.The Only Solution for AI Data Center 24/7 Zero-Carbon Power Crunch

NVIDIA's latest AI chips are creating exponential power demand, while Microsoft, Amazon, and Google have committed to net-zero carbon emissions. Solar and wind are intermittent and cannot deliver 24/7 baseload power. Small Modular Reactors – with their tiny footprint, modular scalability, and behind-the-meter capability – represent the perfect standalone microgrid core for hyperscale AI data centers.

3. Business Model Pivot – From Product Sales to Licensing Recurring Services

NuScale, through partnerships with ENTRA1 and other entities, is strategically lightening its balance sheet to become a "technology licensing and core module vendor." As factory-built modules begin mass delivery in 2027-2029, the revenue mix will shift toward high-margin IP licensing, core nuclear component sales, and long-term operations and maintenance services.

4

23

2,488

Jun 14

$HYLN --- $HYLN has fully pivoted to become an innovative clean energy technology company focused on distributed power generation, built around its flagship KARNO™ power generator modules. On June 10, Needham analyst Sean Milligan officially initiated coverage on $HYLN with a $9.00 forward price target. Needham emphasized the extremely broad commercialization runway for KARNO modules across both AI infrastructure and defense verticals — a catalyst that directly sparked a breakout rally on heavy volume in recent trading sessions.

The KARNO generator module has successfully passed UL non-recurring certification testing. This was the single biggest go-to-market roadblock, and clearing the milestone means Hyliion can now begin on-site equipment deliveries to its first wave of early adopter customers.

On June 1, the module was officially named the 2026 Most Valuable Product (MVP) by leading industry publication Consulting-Specifying Engineer.

1. Riding 2026's Hottest Macro Trend: Mission-Critical Distributed Power for AI Data Centers

The global AI boom has triggered an unprecedented, crippling power shortage for data centers — particularly across North America. Data centers don't just need massive volumes of electricity; they require stable, 24/7 local microgrid resiliency.

Built on linear generator technology, the KARNO module natively outputs 800V DC power — a perfect match for the native architecture of today's cutting-edge AI compute racks and next-generation data centers. It eliminates costly, inefficient AC/DC conversion losses, directly boosting overall data center energy efficiency.

The company recently signed a landmark multi-megawatt partnership with VFG Holdings focused exclusively on data center deployments.

2. U.S. Department of Defense Contract Validation (Office of Naval Research)

Q1's explosive top-line growth was driven primarily by contracts from the U.S. Office of Naval Research (ONR), including an 800kW reaction system currently in production for the Navy. The military's core interest in KARNO extends far beyond its fuel-agnostic design: the module also features extremely low acoustic and thermal signatures — a non-negotiable requirement for stealth operations and autonomous unmanned systems. Management expects to win an additional $40-$50 million in follow-on military contracts this year.

3. Unprecedented Margin of Safety: Net Cash Exceeds Market Capitalization

As of Q1 end, Hyliion remains completely debt-free, with $139 million in cash and short-term investments on its balance sheet. The company projects it will still hold $100 million in cash by year-end 2026. When shares dipped to the $1-$2 range earlier this year, its book net cash value even exceeded the company's total market capitalization. This provides extreme downside protection for early institutional investors, while also giving Hyliion ample dry powder to fund initial commercial scale-up.

1

15

1,657

Navigating the AI Power Revolution: Why Bloom Energy ($BE) and Oracle’s ($ORCL) Partnership Stands Out

Over the past few months, I’ve been closely following developments in the energy sector, particularly how hyperscalers are powering the explosive growth of AI data centers. One name that keeps rising to the top is Bloom Energy (NYSE: BE), especially after its deepened partnership with Oracle (NYSE: ORCL). What started as an interesting collaboration has evolved into a major strategic deployment that addresses some of the biggest challenges in AI infrastructure: reliable, scalable, and relatively cleaner power.

I wanted to share a detailed breakdown of this partnership, the recent developments around Project Jupiter, and why it matters for investors, technologists, and anyone tracking the AI boom.

The Bloom Energy–Oracle Partnership: From Initial Collaboration to Multi-Gigawatt Scale

In July 2025, Bloom Energy and Oracle began working together to deploy solid oxide fuel cell (SOFC) systems for Oracle’s data centers. These fuel cells convert natural gas, reformed into hydrogen, into electricity through an electrochemical process, offering higher efficiency and lower emissions compared to traditional combustion-based generation.

The partnership took a major leap forward in April 2026. On April 13, the companies announced an expanded master services agreement under which Oracle committed to procuring up to 2.8 GW of Bloom’s fuel cell systems. An initial 1.2 GW has already been contracted, with deployments actively underway across multiple U.S. Oracle sites and continuing into 2027.

As part of the deal, Oracle also received a warrant to purchase up to approximately 3.53 million shares of Bloom Energy at $113.28 per share, representing a potential investment of around $400 million. This equity alignment signals strong confidence from Oracle in Bloom’s technology.

Project Jupiter: A Flagship Deployment in New Mexico

One of the most exciting elements is Project Jupiter, Oracle’s large-scale AI data center campus in Doña Ana County, New Mexico, developed in partnership with BorderPlex Digital Assets.

Initially, plans included a dedicated natural gas plant with turbines and diesel backups. However, the project faced significant local pushback over concerns about water usage, air quality, noise, and broader community impacts. This led to regulatory hurdles, including denials for a proposed gas pipeline and over 7,000 public comments during permitting.

In response, Oracle pivoted. As reported in a detailed Business Insider article published on May 7, 2026, the company canceled the traditional gas plant plans. Instead, it is moving forward with Bloom Energy’s solid oxide fuel cells to fully power the campus, with up to 2.45 GW on a single microgrid.

This switch is noteworthy for several reasons:

Emissions Reduction: Bloom’s systems are reported to produce approximately 92% lower NOx emissions compared to conventional gas turbines.

Water Efficiency: Closed-loop cooling drastically reduces water consumption, a critical advantage in water-stressed regions like New Mexico.

Deployment Speed: Fuel cells can come online in as little as 55–90 days, helping Oracle bypass lengthy grid interconnection delays.

Operational Advantages: Quieter operation and no direct impact on local electricity rates for residents.

While local environmental groups, such as the New Mexico Environmental Law Center, remain cautious, noting that the systems still rely on natural gas, the pivot has been positioned as a pragmatic step forward in the “Bring Your Own Power” (BYOP) trend among hyperscalers facing grid constraints.

Why This Matters in the Broader AI Context

AI training and inference demand enormous, always-on power. Traditional grid infrastructure simply cannot scale fast enough in many regions. Technologies like Bloom’s SOFCs offer a bridge solution: dispatchable, modular power that can be sited directly at the data center.

From my perspective, after digging into earnings calls, analyst reports, and on-the-ground developments:

Bloom reported strong Q1 2026 results, with revenue beats, margin expansion, and raised full-year guidance in the $3.4B–$3.8B range.

Analyst sentiment has improved, with price targets from firms like Jefferies, RBC, and Evercore reflecting optimism around the Oracle deal and broader AI tailwinds.

Risks remain, including execution on manufacturing scale-up, natural gas price volatility, regulatory scrutiny on fossil-derived fuels, and competition from other clean power alternatives.

Bloom Energy is not a pure-play “green” energy company in the renewable sense, but its high-efficiency fuel cells position it uniquely in the transition to reliable, low-emission backup and primary power for critical infrastructure.

Final Thoughts

The Oracle partnership and the adaptive approach at Project Jupiter highlight how innovation in power generation is becoming as important as the chips and algorithms driving AI. For those following $BE, the coming quarters will be telling. Watch for deployment milestones, additional hyperscaler wins, and execution metrics.

I’ll continue monitoring this space and sharing updates as they develop. The intersection of energy and AI is one of the most consequential investment and technology themes of the decade.

What are your thoughts? Have you looked into Bloom Energy or other data center power plays? Feel free to comment below. Also, I own $BE

Disclaimer: This post is for educational purposes only and reflects my personal research and observations from public sources. It does not recommend buying, selling, or holding any securities. Investing involves substantial risk of loss. Please conduct thorough due diligence.

2

1

129

Jun 13

JFK's New Terminal One ESG report details a 12-MW microgrid with 13,000 solar panels and six fuel cells, projected to cover 50% of the terminal's energy demand by 2050. First phase opens in 2026. #aviation #aerospace

airpronews.com/2026/06/13/jf…

1

32

AI power is usually discussed like a generation problem, but the more immediate bottleneck may be much less glamorous.

Transformers.

The research points to transformer lead times sitting around 128 weeks, with generator step-up transformers even longer. That is not a capital markets problem and it is not solved by another data center press release. It is a physical equipment problem tied to factory slots, heavy electrical manufacturing, utility procurement cycles and the availability of grain-oriented electrical steel used in transformer cores.

That is why I think the AI power trade keeps moving deeper into the industrial stack. First the market priced GPUs, then data center builders, then power equipment companies. But if transformer output is constrained by specialized steel, core manufacturing and multi-year lead times, then the bottleneck sits upstream of the equipment OEMs themselves. Data centers can have capital, land and customer demand, but without transformers they cannot energize on schedule.

This also explains why behind-the-meter power and private microgrid ideas are gaining traction. Hyperscalers are not only trying to find cheaper electricity. They are trying to escape a grid interconnection process that is increasingly gated by scarce physical hardware. If the transformer queue remains long, the market will eventually stop talking about “AI power” in general terms and start pricing the specific materials and components that determine whether a site can actually turn on.

1

2

5

14,769

Chris Morris, director of the West Virginia Data Economy Office, said Thursday that the state has received its first application to certify a microgrid tied to data center developments.

Via @WV_Watch

wvgazettemail.com/news/energ…

2

516

Jun 13

Introducing Vertiv™ EnergyCore Grid, the microgrid-ready power for large-scale deployments:

Peak shaving

Load shifting

Grid-responsive

Enhanced resilience

The future of smart power is here: ms.spr.ly/6013viZs3

#Vertiv #OneVertivOneWorld #Efficiency #Reliability

6

Jun 13

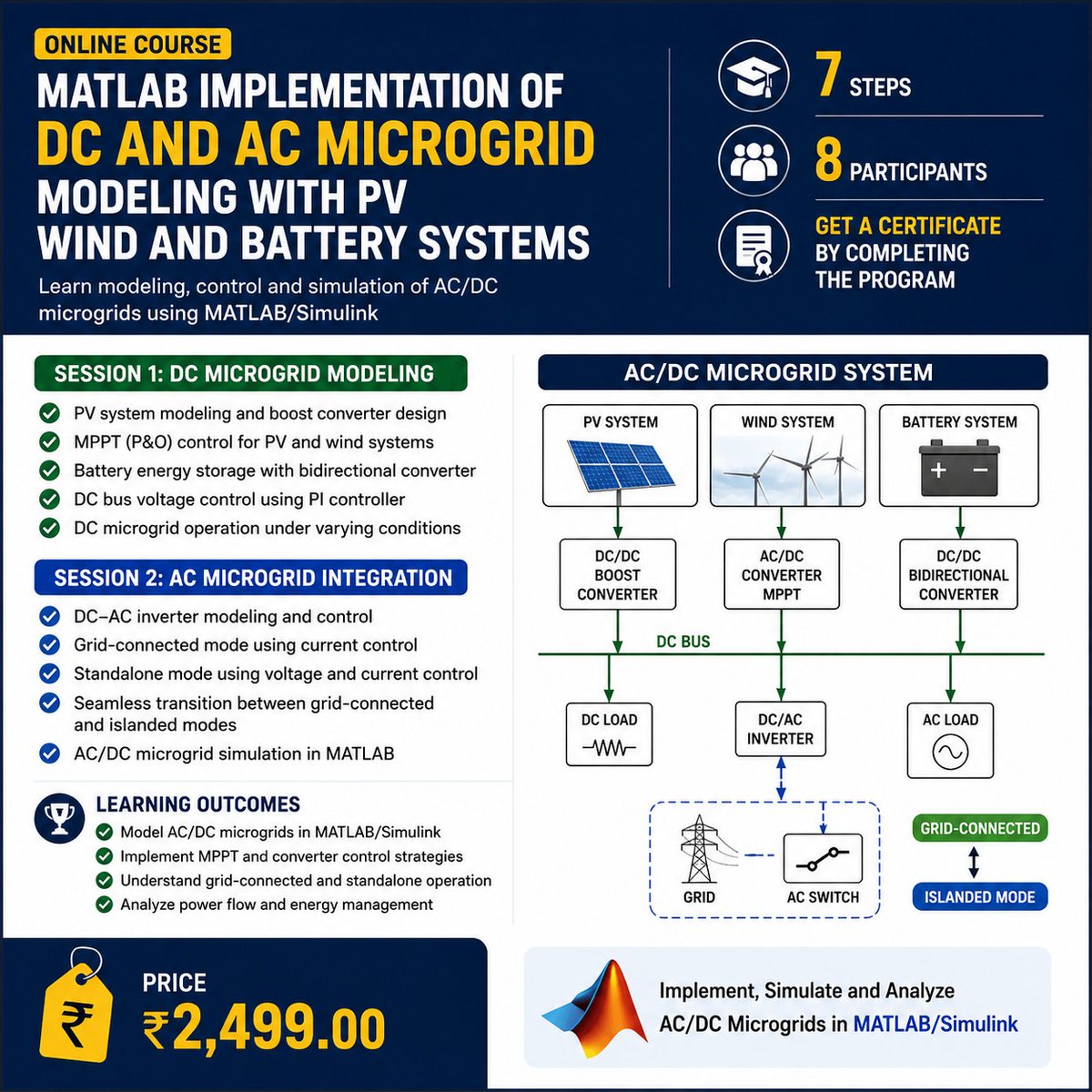

✅ Learn AC/DC microgrid modeling using MATLAB/Simulink

zurl.co/pIkwG

✅ Implement PV, wind, battery, MPPT, and converter control

✅ Complete 7 steps and get a course completion certificate

8

Microgrid Resilience Expected to Yield $450K/Year in Savings for Siemens Facility

Save energy/cost for your business contact me at buff.ly/5OiGpqm.

#Reliability #EnergyStorage #EnergyEfficiency #Renewables #EnergyAudit #Procurement #Resilience

buff.ly/W31ZaCD

6