Jun 14

I always admired to learn a lot of about my 2 Guru from equity market since initial days of my learning to till today, a highly recommended podcast to watch and learn about most successful investing style.@hiddengemsindia sir , @valuepick sir

youtu.be/_W-CNN3rcvY?si=RT1k…

1

64

R R Kabel Limited: Value Pick Stock June 2026

Read More - bit.ly/4e0rOPL

#finblab

#RRKABEL #valuepick

1

140

R R Kabel Limited: Value Pick Stock June 2026

Read More - bit.ly/4e0rOPL

#finblab #RRKABEL #valuepick

1

83

May 12

🛡️ #Havells India (HAVELLS) at 52-week low valuation – a cash generating machine with iconic brand power!

Current Snapshot (as of May 2026):

• Trading near 52W low (~₹1,190 levels)

• Trailing PE: ~43x (well below 10-year median of ~68x)

• Forward PE: ~36x (attractive for a premium FMEG player) 🔥

Why Havells stands out:

• Iconic brand in fans, lighting, wires & cables, switchgears, and consumer durables – trusted household name with strong pricing power and market leadership.

• Cash generating machine – consistent strong operating cash flows (₹1,572 Cr in last 12 months), net cash rich balance sheet, negligible debt, and healthy free cash flow generation.

Brokerage & Analyst Views (latest):

• Consensus 12-month target: ₹1,480–₹1,570 (25-35% upside) 🔥

• Bullish calls: ICICI Securities (₹1,615 Buy), Nomura (₹1,620 Buy), LKP Research (₹1,450 Buy), JM Financial (₹1,750)

• Average analyst upside potential: ~28% with stable long-term growth outlook in wires, cables & premium appliances.

Defensive play undervalued growth story = perfect setup for long-term compounding!

Strong brand moat cash flow discipline = ready to rebound.

#Havells #Stocks #Investing #FMEG #ValuePick

2

433

Apr 25

Jermod McCoy waiting 3 rounds to hear his name called. Raiders fans waiting 20 years to hear "shutdown corner" and "Las Vegas" in the same sentence.

Mel Kiper's draft board just filed a missing persons report. Meanwhile Vegas books already moved Jermod McCoy Defensive Rookie of the Year odds from 100/1 to 25/1.

#RaiderNation #NFLDraft #ValuePick #JustWinBaby

1

2

6

2,798

WTA 100 MADRID SPAIN

BONDAR VS SVITOLINA

OUR PICK SVITOLINA FROM HERE @2.20 🏆

I SEE HER LAST FEW MATCH AND SHE DOING VERY GOOD ON CLAY AND SVITOLINA GOING TO WIN FROM HERE #MMOPEN #tennislive #tennis #wta1000 #svitolina #bondar #underdog #valuepick

3

2

568

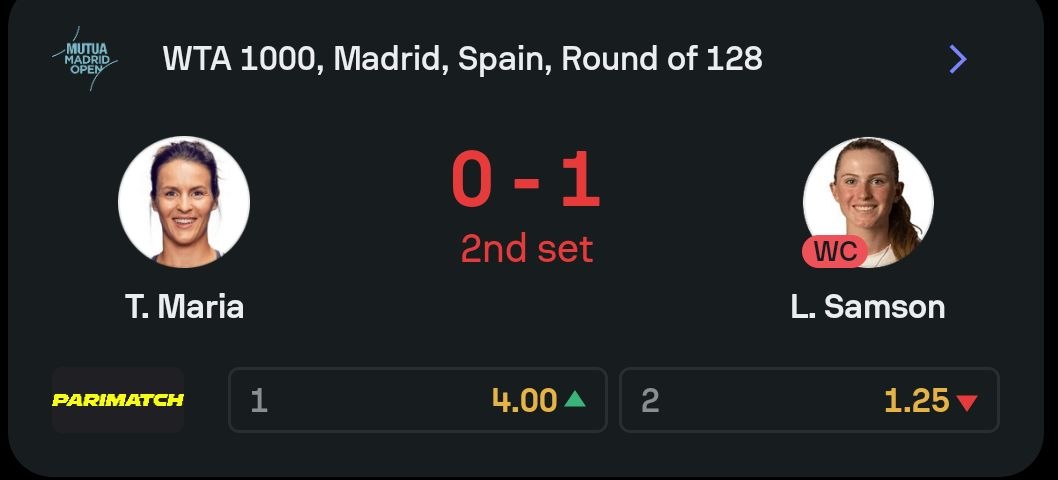

Guys Found A IN-PLAY Tennis pick

WTA 1000 MADRID 🇪🇸

MARIA VS SAMSON

OUR PICK MARIA FROM HERE ODDS 4.00 🏆

WE CAN TAKE SOME CHANE ON MARIA ON THESE ODDS OR YOU CAN PICK HER FOR OVER 23.5 GAMES

#MMOPEN #wtamadrid #maria #samson #tennis #tennislive #valuepick

2

222

Apr 14

SPML Infra may be the one ....

VP sir had posotive Outlook on this comoany earlier......waiting eagrly for updates on this company from Sir....

1

1,710

#Tatapower EV Charging station rapidly growing n chart cooked first.Lokesh Machine also showing strength @drprashantmish6 @AdeParimal @valuepick @AnyBodyCanFly @AnilSinghvi_ @akshaykumar @CNBC_Awaaz @MotilalOswalLtd @MotilalOswalPW @ARWealth @shareindiasec @iam_juhi #moneymaking

12

1,261

Mar 23

Stock to Study : eClerx Services Ltd (ECLERX) - Promoter nibbling from open market.

Company Snapshot

eClerx Services Ltd is a leading Indian digital operations and analytics firm providing specialized business process management, data analytics, automation (including AI-driven solutions), financial crime compliance, customer experience transformation, and insights services. It serves Fortune 2000 clients primarily in financial services, retail, high-tech, telecom, media/entertainment, and manufacturing. Strong focus on intelligent operations, Agentic AI adoption, analytics & automation growth, and global delivery centers (India-heavy with international presence).

Guidance & Outlook from Q3 FY26 Concall (Jan/Feb 2026)

Management commentary positive on robust revenue/margin performance, deal wins, and AI momentum; reaffirmed margin guidance with top-quartile growth commitment:

- FY26 Revenue Outlook: No explicit full-year number; strong 9M momentum (USD operating revenue 18% YoY to $346.5 Mn; INR 22% to ₹30,097 Cr); Q4 expected softer sequentially but overall healthy trajectory.

- EBITDA Margin Guidance: Reaffirmed 24–28% (sustainable; Q3 actual ~28% with strong leverage).

- Deal Wins: Q3 $45 Mn (healthy pipeline; analytics & automation 10%).

- Headcount: 21,847 (up 18% YoY); focus on utilization, productivity, and AI investments.

- Key Drivers: Client expansions, AI adoption (Agentic AI), high-value services in financial markets/digital; Q3 strong sequential growth (USD rev 5.4% QoQ to $121.7 Mn; INR 6.5% QoQ to ₹10,703 Cr).

- Q4 FY26: Softer QoQ expected (typical seasonality) but positive on execution and pipeline.

- Medium-term: Top-quartile peer growth; margin discipline (24–28%); cash generation strong (EBITDA conversion ~82%); bonus issue 1:1 approved (subject to approval); focus on AI/automation scale-up.

Valuation Analysis & Projections

FY26 Estimates (conservative, based on 9M Q3 strength):

- Revenue: ~₹40,000–42,000 Cr (strong ~20–25% YoY implied).

- EBITDA: ~₹10,000–11,000 Cr (margin ~25–27%).

- PAT: ~₹6,500–7,000 Cr (implied EPS ~₹140–150).

Implied Multiples at ~₹1,442–1,469 (as of 23 Mar 2026 close; recent range ₹1,428–1,458):

- FY26 P/E: ~9.5–10.5x (attractive on growth).

- FY26 EV/EBITDA: ~7–8x.

- P/B: ~4–5x (strong ROE/ROCE).

Order-book equivalent: Pipeline/deal wins strong ($45 Mn Q3); compared to BPM/KPO peers (often 15–25x P/E), eClerx trades at discount despite high margins (~28% EBITDA), AI tailwind, and cash flows. Analyst models (DCF/peer) point to ₹2,300–2,850 range (consensus average ~₹2,305–2,396; highs up to ₹2,850).

Key Positives

- Strong Q3: Operating rev ₹1,070 Cr ( 25.4% YoY), EBITDA ₹307.5 Cr (margin 28%, 190 bps YoY), PAT ₹192 Cr ( 40% YoY).

- 9M FY26: Rev 22% YoY, PAT 33% YoY; robust cash flows.

- AI/analytics momentum deal wins; margin guidance 24–28%.

- Bonus issue 1:1 dividend appeal; headcount growth supports scale.

Key Risks (mitigated but monitor)

- Q4 seasonal softness and macro/client spending caution.

- Margin pressures from variable payouts, travel/marketing, talent costs.

- Competition in BPM/analytics; forex volatility on exports.

- Execution on AI investments and client expansions.

Longer-term: AI adoption, analytics/automation growth, and client expansions will drive sustainable 15–20% CAGR in revenue/earnings. Position size accordingly; suitable for growth digital services portfolios. Monitor Q4 FY26 results, deal pipeline, and margin trajectory closely.

Stock Valuation and Projected Price Target :

At current valuations (~₹1,442–1,469), eClerx offers compelling risk-reward as a high-margin, AI-enabled BPM leader. The combination of strong Q3 growth ( 25% YoY rev, 40% PAT), reaffirmed 24–28% margin guidance, robust pipeline, and deep discount to peers justifies a re-rating toward 15–18x forward P/E (target price ₹2,100–2,700 over 12–18 months, 45–85% upside; analyst consensus ~₹2,305–2,396 implies ~60–65% potential, highs up to ₹2,850 suggest 95% ).

#valuepick #investment #stockpick

1

1

7

1,795

Feb 28

did a detailed valuation thread on Zappfresh around its IPO, incase you are interested in reading it :D

9 Oct 2025

DSM Fresh Foods/ Zappfresh IPO review

After a lukewarm response that forced an IPO extension, Zappfresh/DSM Fresh Foods finally listed today.

I find it to be a dark horse with strong potential. Based on that, sharing a detailed fundamental & Discounted cash flow valuation review. (1)

#Zappfresh #DSM #DSMFreshfoods

1

6

4,519

Feb 27

Sir, how’s your plant visit of Freshara Agro! What’s your view after meeting management and plant visit! Is it more positive or as it is? Also what’s your current view on Workmates?

1

2

1,626

Feb 23

💎 Anton Stach (£4.7m) delivering BIG for a promoted side!

⚽ 4 Goals

🎯 6 Assists

🔥 3 Double-Digit Hauls

📊 xG: 2.2

📊 xA: 3.6

Serious returns for a budget midfielder 💰📈

Is he the perfect 5th mid enabler for the run-in? 🤔

#FPL #BudgetBeast #Differential #FPLCommunity #ValuePick #GW27

#LUFC #PremierLeague #AVLLEE #FplPod #FplBangla

17

26

913

Feb 20

🚨 A-League Night = Goals Loading… ⚽🔥

I’m backing Adelaide United Over 1.5 Goals today.

They’ve been one of the most aggressive attacking sides at home, creating chances for fun. Perth Glory’s defence has been leaking goals, and if Adelaide start fast, this line can be cleared early.

Expect pressure. Expect chances. Expect goals. 🎯

Let’s cash this one 💰

#ALeague #AdelaideUnited #FootballTips #SoccerPicks #GoalFest #ValuePick #MatchDay #perthglory

1

3

356

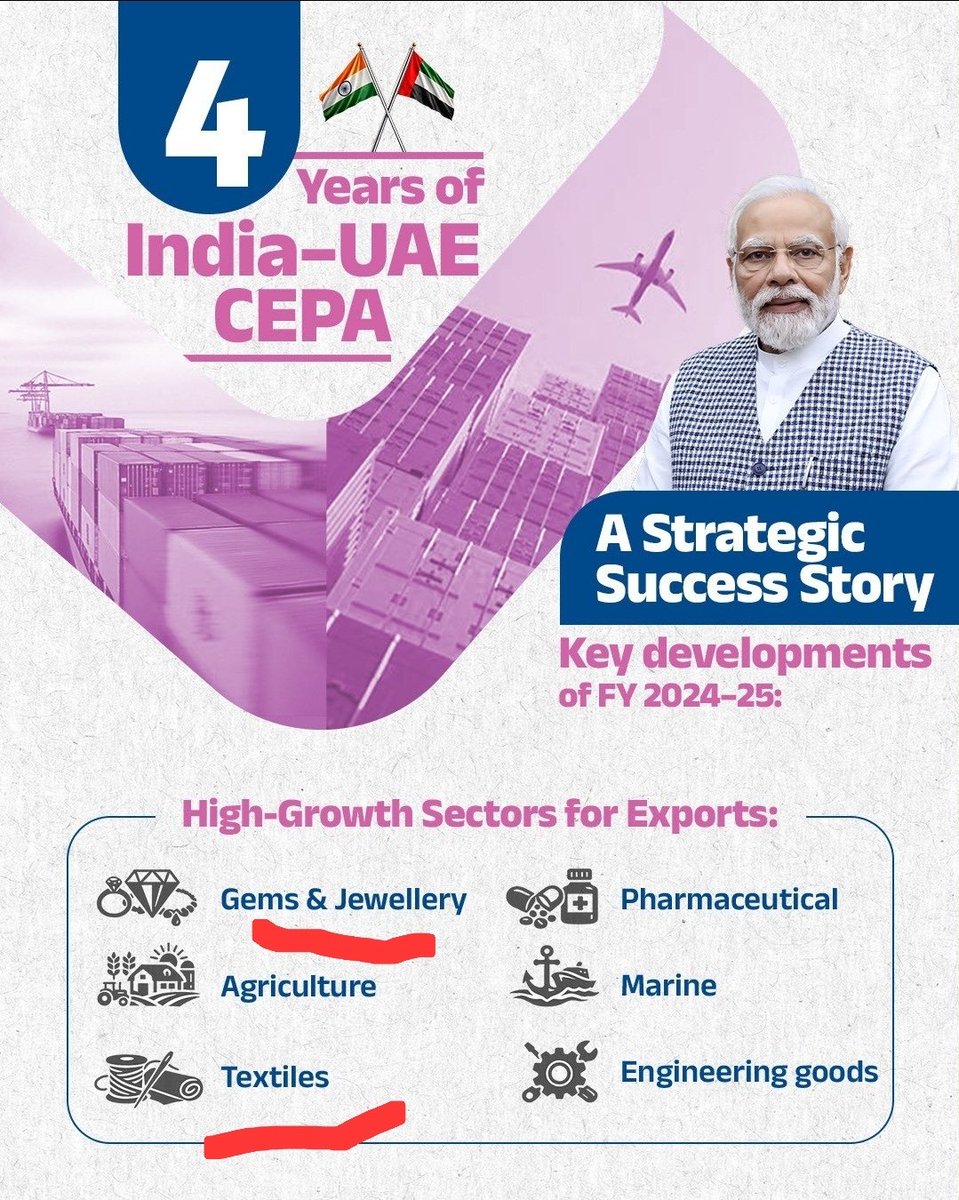

"Baar baar dekho-hazar baar dekho,ke dekhne kii chizz he" Q ke many companies having Textile & Gems n jewellery businesses only still lying at penny levels🤔 @NineColoursInd #investing #DealAlert #investors #textile #jewellery #India #penny #StocksToBuy #BuyTheDip @valuepick

ALT Ninecolor

1

1

8

896