Joined March 2021

- Tweets 5,629

- Following 465

- Followers 768

- Likes 16,060

958 Photos and videos

Murrieta retweeted

Jun 8

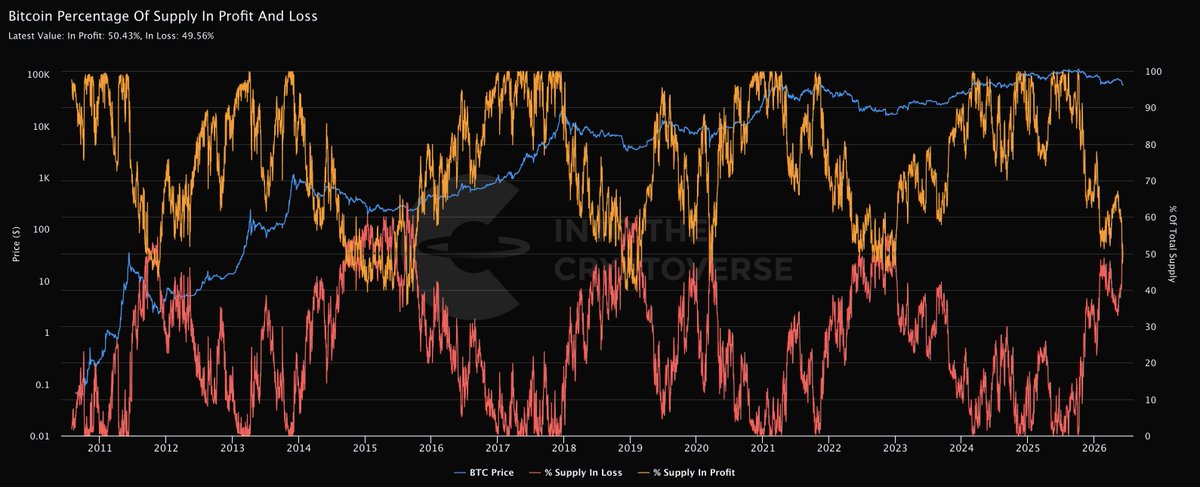

I love the cadence of this chart

Bitcoin % of Supply in Profit/Loss

As I said previously, you start looking for major market cycle bottoms *after* they cross, not before.

They just crossed.

Such a great chart for keeping people on the right side of the market in midterm years

226

583

5,821

374,025

Murrieta retweeted

Jun 5

CEOs walking into work after realizing that the AI tokens are going to cost more than the employees they fired

179

1,235

16,872

789,888

Murrieta retweeted

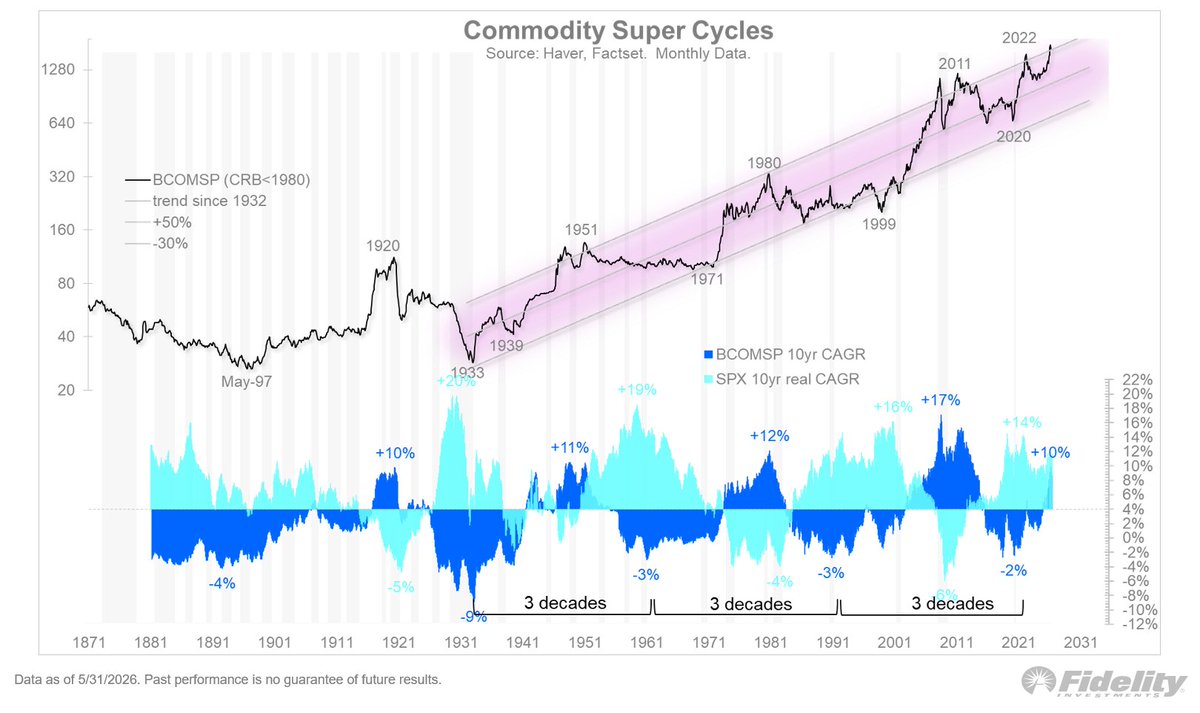

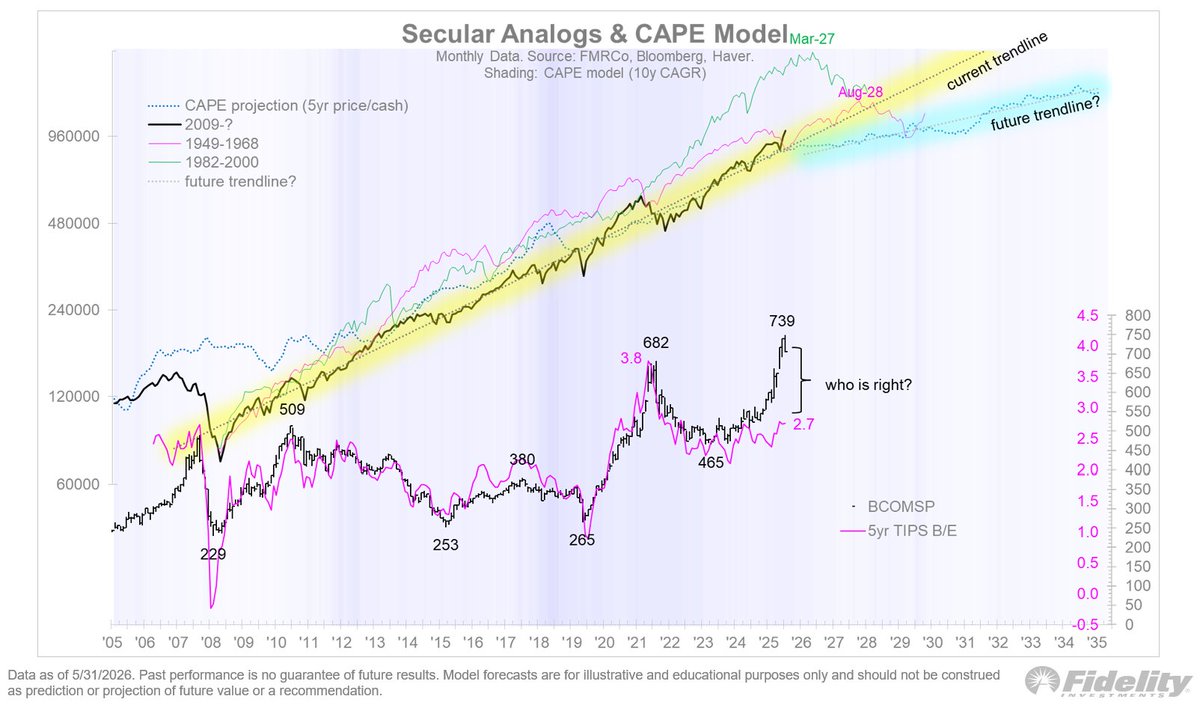

A boom-turned-bubble is one scenario for an end to the secular trend, but an inflation bust is another. Below in the Commodity Super Cycles chart we see that commodities appear to have entered another secular bull market of their own. What’s interesting about this is that super-cycles for commodities and equities tend to be mirror images of each other (illustrated by the 10-year CAGRs below). So perhaps the strength in commodities is a subtle early warning sign for the secular trend in equities.

If commodities continue to rally, the “open jaw” below between the Bloomberg Commodity Spot Index and the 5-year TIPS break-even will be a challenge for the bond bulls. One of those lines is wrong, I think, and if it’s the inflation break-evens, then it has implications for the Fed and therefore for bonds and therefore for equities via the Fed model.

The Fed model returned to relevance in 2022 after being dormant for several decades. The Fed model simply holds that if the risk-free asset is competitively priced against the risk asset (equities), and its valuation derates, then so must equities. Hence, per the above chart, if inflation remains sticky in the 3-4% area and pushes up the TIPS breaks, then bond yields may well rise into that danger zone of 5% or above, which per the Fed model could force the stock market to derate.

12

52

262

51,827

Murrieta retweeted

Jun 5

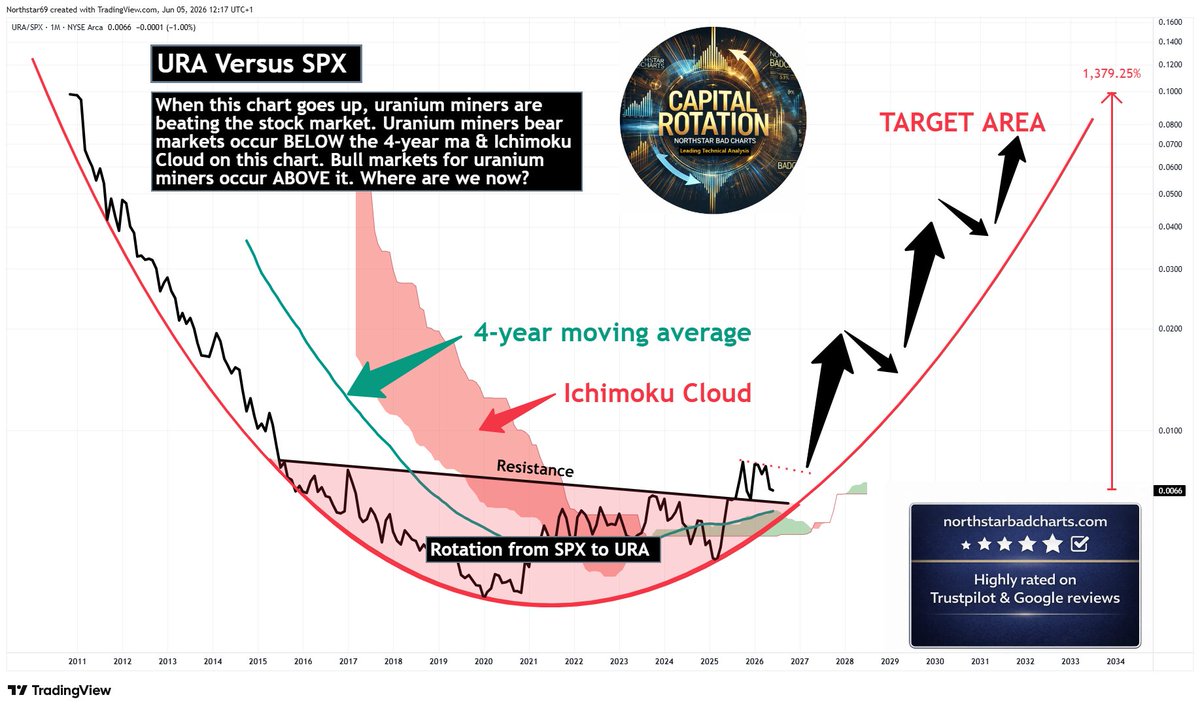

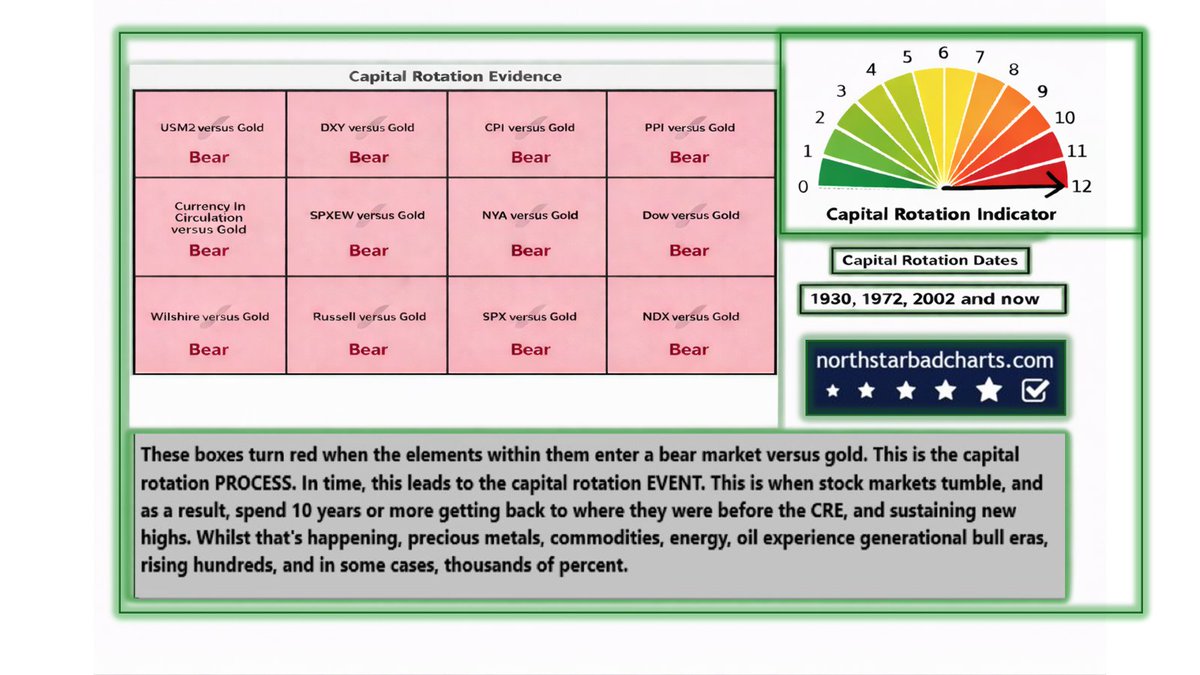

U-R-A-N-I-U-M: Capital is quietly rotating away from stock markets 👇

31 Dec 2025

It hit us between the eyes in 2025 - Gold & silver soared. Crypto stagnated. Golds capital rotation evidence is complete. This is a new era. Now we wait. The clock is ticking. The CRE may be days, weeks, or many, many months away. It is coming though. Be ready.

22

71

644

56,541

Murrieta retweeted

Jun 5

Weak af

Jun 4

$BTC The inability for price to bounce higher after touching the 200-week implies it wants to explore below. Blue squiggle is the last place structurally speaking I would think to see a reversal. But this looks bidless at the moment.

8

1

74

9,508

Murrieta retweeted

Jun 4

COSMIC 1.0.15 has been released. This update significantly levels up COSMIC gaming.

Multiple fullscreen windows on a single workspace has been implemented meaning transitioning from Steam Big Picture to a game and back is smooth. Games launch fullscreen as intended. Wayland pointer constraints protocol fixes the FPS games experience. And in-game menus are working well.

Available in Pop!_OS now and your favorite distro soon (if not already!)

6

6

177

6,032

Murrieta retweeted

Jun 2

RISK MANAGEMENT: Anthropic pulling forward its IPO and Alphabet $GOOGL issuing $80bn in stock are examples that signal to you what the AI companies themselves think the answer to this question is.

Jun 2

The Macro Minute | June 2, 2026

In today’s video, we answer the following questions:

- Are we in an AI stock market bubble?

- How would @DariusDale42 solve income inequality if given the opportunity?

For daily updates, follow listen to The Macro Minute on your favorite podcast platform.

6

6

95

13,743

Murrieta retweeted

May 29

BOOM! Our revamped complimentary Education resource has been deployed: 42macro.com/education.

If you suspect that you have any blind spots in your investment process, this TLDR-friendly tool will help you quickly get up to speed on what you NEED to know.

Enjoy the learning!

5

4

69

5,516

Murrieta retweeted

May 29

MARKETS: I guarantee this episode would have 3-4x more engagement if our friend @adamtaggart replaced the word “bubble” with “crash,” “collapse,” “meltdown,” or any of the other buzzwords that bear porn purveyors use to trigger emotional responses from their victims.

Reminder: the stock market only goes up BECAUSE OF bear porn victims capitulating, one by one, and panic-buying at higher and higher prices. This dynamic is exacerbated by the proliferation of options and the rally fuel that charm and vanna flows provide.

Thank you, bear porn purveyors, for maintaining the wall of worry that allows those of us participating in raging bull markets to compound wealth! We appreciate you. 🤣

Despite stocks being at rich valuations, there's a risk of them bubbling sharply higher from here if the Federal Reserve under Kevin Warsh choses to "look past" the current inflation concerns, warns @DariusDale42

So, how to position?

WATCH: youtu.be/AaVjxiFROOU

15

11

121

11,809

Murrieta retweeted

May 20

MARKETS: Friendly reminder that I don't make market calls. Our quantitative risk management overlays KISS (for retail; since Jan-23) and Dr. Mo (for institutions & sophisticated retail; since Oct-23) are responsible for signaling to members of our global investor community what to do in their portfolios, not me.

My sole job as CIO is to narrate the evolution of the distribution of probable economic, policy, and market outcomes so that when KISS and Dr. Mo instruct our global investor community to do something different in their portfolios, they understand the fundamental reasons why and can dispassionately execute the signals.

Most investors struggle to execute systematic processes in isolation because most people suffer from narrative fallacy and need to assign cause and effect to market movements. I don’t. To Druckenmiller and me, markets are simply squiggly lines that make us richer or poorer. But since this is admittedly a highly unusual method for approaching capital markets, I am happy to meet our members halfway with high-quality fundamental research.

Plus, as a former member of the bottom 0.001% of our K-shaped society, I derive personal satisfaction from piecing the macro puzzle together faster than Wall Street consensus.

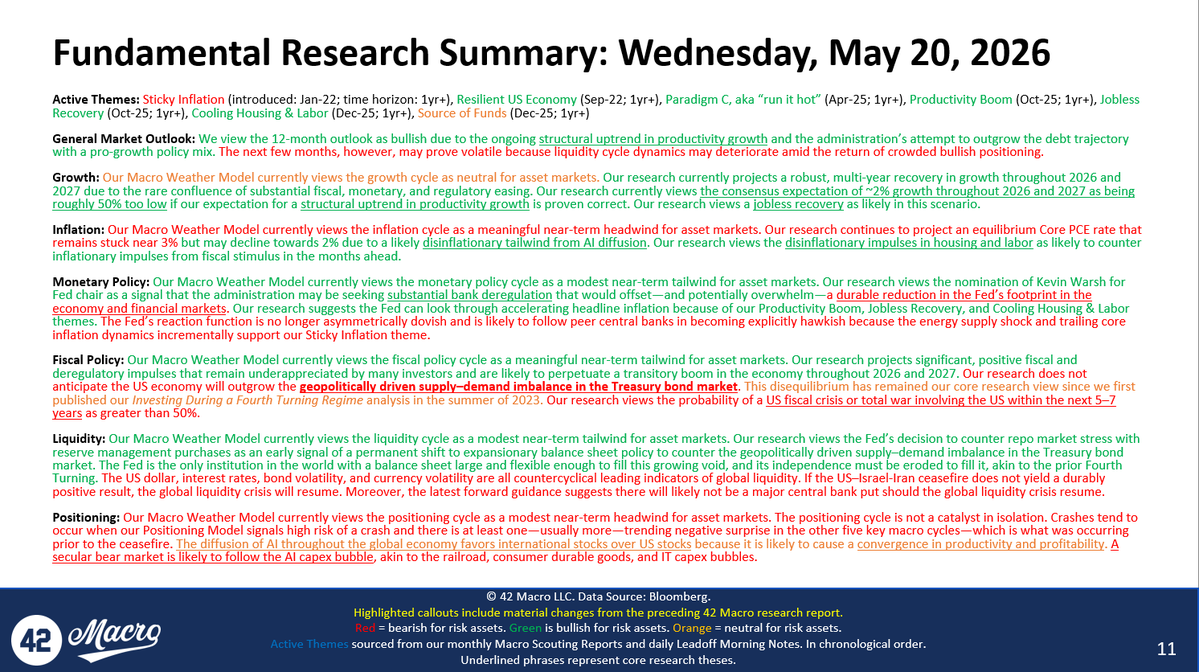

At any rate, here is our latest Fundamental Research Summary, which we feature in every @42Macro research report and incrementally revise as the data and our themes evolve:

May 20

OK max confused, I thought it was time to be defensive/short now

12

10

140

31,155

Murrieta retweeted

May 14

MARKETS: The key takeaways from the discussion below are twofold:

1. The backward-looking Fed is once again falling behind the curve relative to US core inflation dynamics and peer central banks; and

2. Any attempt by the Fed to catch up will likely cause a destabilizing-but-likely-transitory unwind of the crowded AI trade.

Enjoy!

May 14

Lagging Fed Raises Risk for the AI Trade schwabnetwork.com/video/lagg…

@DariusDale42 joined @sam_vadas on @SchwabNetwork to highlight why a lagging Federal Reserve and persistent inflation dynamics could spark significant market volatility in the near term.

This potential hawkish policy shift risks a sharp drawdown in global liquidity, specifically threatening the "aggressively crowded" AI trade that has dominated the recent risk-on environment.

6

6

77

15,646

Murrieta retweeted

May 12

The Macro Minute | May 12, 2026

In today’s video, we answer the following questions:

- Is the US economy being run too hot?

- Are markets at the start of a dealer-led unwind of the melt-up?

Subscribe to the Macro Minute on your favorite podcast platform:

Apple: podcasts.apple.com/us/podcas…

Spotify: open.spotify.com/show/1jYgzX…

YouTube: youtube.com/@42Macro

5

4

40

2,322

Murrieta retweeted

May 7

Howdy #Team42,

Join me and our friends @FerroTV, @lisaabramowicz1, and @annmarie on @BloombergTV today at 6:00 a.m. ET for a thoughtful and entertaining discussion regarding our outlook for the economy and asset markets.

Be sure to tune in to @BloombergRadio at 8:00 a.m. ET for another wonderful discussion with our friends @tomkeene and @ptsweeney as well.

Enjoy the content and thanks for tuning in. We appreciate you.

Have a great day!

—Skipper

4

4

38

4,377

Murrieta retweeted

May 1

MONETARY POLICY: The US–Israel–Iran conflict and the Strait of Hormuz are garnering the preponderance of headlines—and appropriately so given the associated sudden stop risk in the global liquidity cycle. Longer term, however, the most impactful battle in the world from the perspective of investors, business owners, and families on Main Street will transpire at the Eccles Building in Washington, D.C.

We hope these data-driven insights bless you on your journey to retiring on time and comfortably. 💜

May 1

Who’s right about regime change at the Fed: Kevin Warsh for pursuing it or Jay Powell for resisting it?

Enjoy this clip from our May 2026 Macro Scouting Report webcast, in which we detail key elements of our multi-year call for regime change at the Fed—most of which incoming Fed Chair Kevin Warsh, former Fed Chair candidate Rick Rieder, and current Fed Governor Stephen Miran have signaled agreement with.

At its core will be a shift away from backward-looking data dependency and a lack of accountability regarding adverse inflation outcomes toward forward-looking Bayesian inference and, most importantly, a shift away from Keynesian academic dogma toward incorporating supply-side economic principles.

5

4

75

20,517

Murrieta retweeted

Apr 24

GROWTH: Our Jobless Recovery theme continues to gather steam: latimes.com/business/story/2…. As I remarked on our friend @MariaBartiromo’s show last summer, this is incredibly bullish for stocks… until it isn’t.

The “smart money” bears will lament about it with cherry-picked data until the market peaks. Us “dumb money” bulls will make money off it until the market peaks. Choose wisely if you’re evaluating which camp to join.

3

2

32

12,869

We’ve had access to an engineering sample of the new Framework Laptop 13 Pro for about a month ahead of the announcement, and our biggest takeaway is this: it finally feels like a genuinely premium Framework.

The first thing that stood out to us was the build quality. We (1/8)

Apr 21

Our biggest breakthrough in efficiency yet, the Framework Laptop 13 Pro with 20 hours of battery life. In Graphite.

Linux-first with options for Ubuntu pre-installed. Featuring Intel® Core™ Ultra Series 3 processors, LPCAMM2 Memory, a new haptic touchpad, and a touchscreen display.

Pre-orders for the Framework Laptop 13 Pro open now: frame.work

37

199

4,656

372,316

Murrieta retweeted

Apr 21

Ugh, I’d skip Ubuntu tbh... Canonical keeps pushing snaps hard (even replacing apt packages), slower startup times, sandbox quirks, and yeah… the “ads” in apt didn’t help their image.

Fedora’s usually the better dev box: newer kernel/toolchains, clean upstream GNOME, Wayland-first, no weird vendor lock-in, and dnf is solid. Closer to “stock Linux” without Canonical’s opinionated layers.

Only real trade-offs: shorter release lifecycle and you’ll update more often, but if you’re deving, that’s usually a plus.

1

3

447

Apr 22

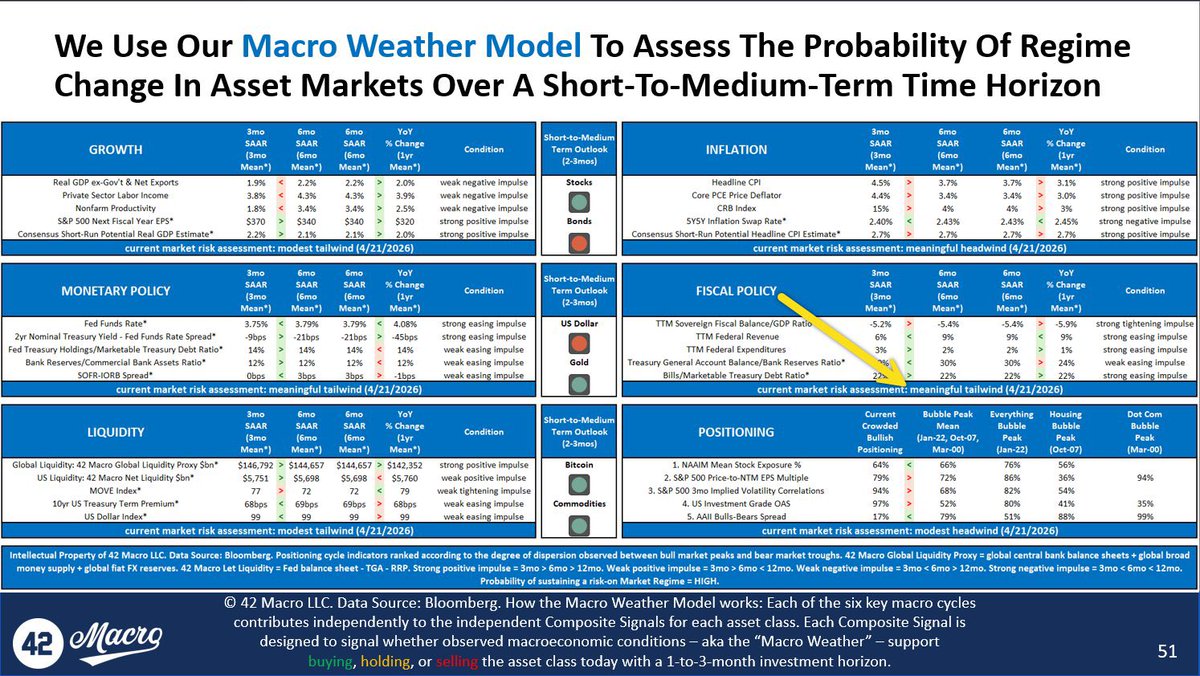

Modest tailwind on growth. Meaningful headwind on inflation. Meaningful tailwind on fiscal. Translation: the government is doing the Fed's job for it, badly, expensively, and somehow bullish for gold and Bitcoin. Paradigm C isn't a theme, it's a forecast. And it's aging like fine wine. 🍷

Apr 21

FISCAL POLICY: Agreed. The accelerating fiscal thrust that our friend Warren cites below is exactly what we called for when we introduced our year-old Paradigm C theme last April.

Paradigm C is what consensus calls "running the economy" hot. The following tweet contains a handy primer on our Fourth Turning (@HoweGeneration) and Five Big Forces (@RayDalio) inspired Paradigm A-E framework for those who may have missed it: x.com/DariusDale42/status/19….

1

68

Apr 21

Hyprland looks slick, but those animations/blur can definitely be a bit resource-heavy if you’re trying to keep overhead low. Massive props for the modern design and dynamic tiling, but sometimes it feels like you're trading cycles for eye candy.

If you like the Wayland/wlroots vibe without the bloat, you might want to look into Sway or a "barebones" Hyprland config with some of the transparency/shadow effects dialed back. Still hits that modern aesthetic without hitting the RAM quite as hard.

1

1

126

This Omacon keynote celebrates computers as more than just tools, but as beautiful, bespoke, and malleable objects. We have such a rich heritage to draw from in our industry, and we don't have to accept losing control over our machines or their aesthetics.

32

28

700

59,553