a girl scaling web3 brands through data, experimentation and storytelling.

Joined July 2020

- Tweets 10,956

- Following 942

- Followers 23,636

- Likes 153,864

777 Photos and videos

Jacy🌸 retweeted

May 26

Top important DeFi news to pay attention to this week 🧠👇

1. @solsticefi $SLX TGE and airdrop claim will be open on May 25.

2. @xmaquina, Physical AI and Humanoid robotics DAO, $DEUS TGE happens on May 27

3. @dropee_app TGE on May 27. Dropee hits 13M users, 4M MAU, 300K DAU, and $2.5M revenue in 8 mobile games before the token even exists.

4. @Cardano v11 hard fork is scheduled for May 29. This upgrade brings performance optimizations, state changes, and smart contract improvements to the network.

5. $NEAR is driven by a fresh wave of AI narrative hype and aggressive scaling roadmaps. @NEARProtocol is hinting at next-gen data availability and compute scaling frameworks designed specifically to handle high-throughput, onchain AI models.

6. @variational_io phase 2 is coming with more TradFi liquidity for 100 RWA markets.

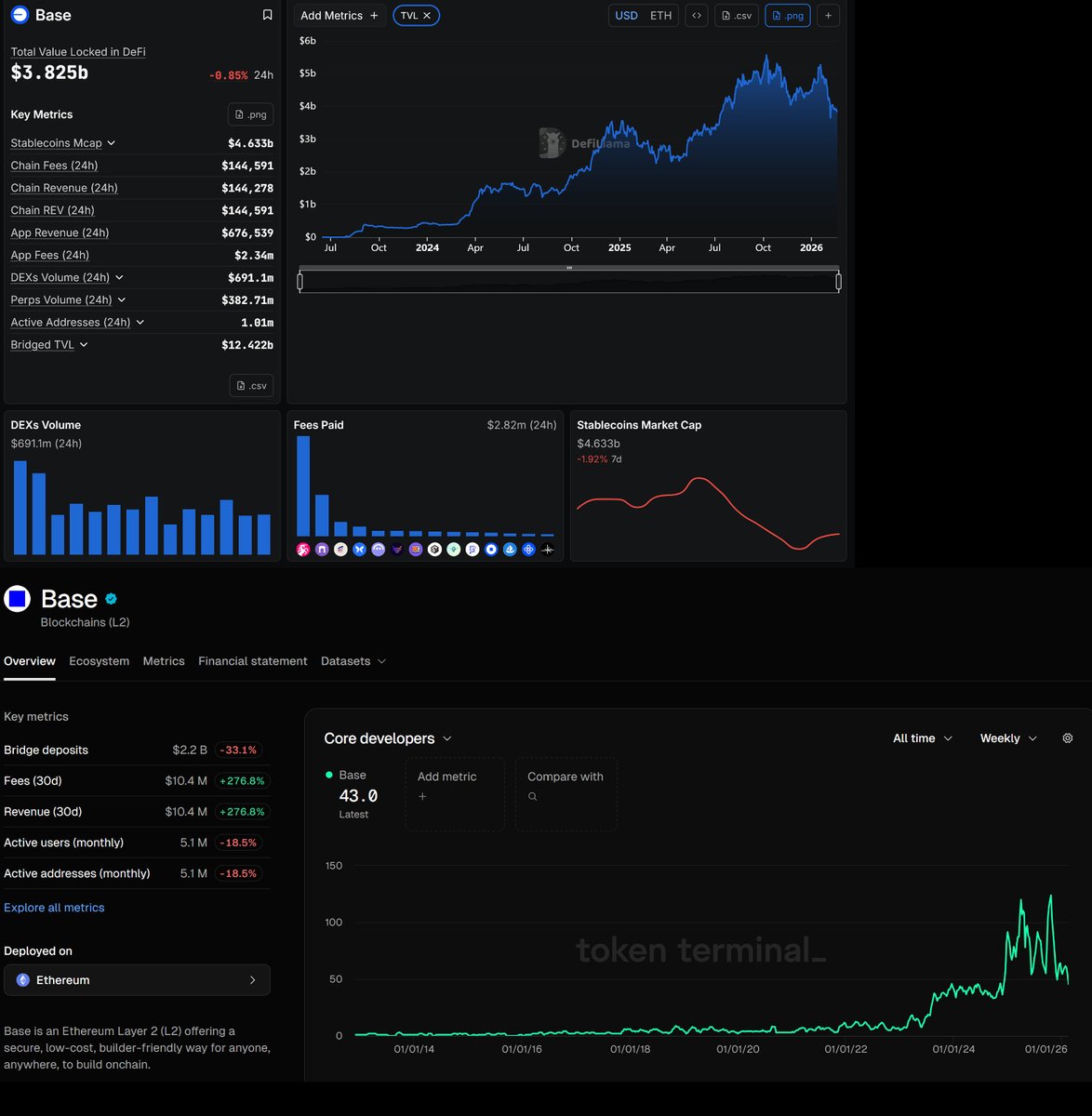

7. @base took the top spot in 24h DEX volume. Base AI ecosystem is heating up with $VVV, agentic payments, and decentralized AI.

8. @Polkadot OpenGov is voting on a major change to the network’s staking architecture, requiring a lock of a minimum of 10,000 $DOT

9. @prjx_hl is launching a new cashdrop program to replace point-based airdrops. $1m was sent out. $500k is committed in the next year.

4

2

21

1,263

Jacy🌸 retweeted

May 26

Hyperliquid just deployed a new HIP-4 market:

app.hyperliquid.xyz/trade/ju…

When worldcup?

16

8

135

14,747

May 21

Crypto still prices chains like it is 2021. Like every chain has a realistic shot at becoming the next Ethereum.

Then six months later you check the numbers and realize half of them are still fighting over the same rotating pool of incentives and airdrop farmers.

Meanwhile the actual economic activity keeps concentrating in a few ecosystems.

✦ @solana dominates retail attention because its apps actually generate demand, like @Pumpfun, @Backpack, @kamino, and @JupiterExchange. Some of them even pull more revenue than entire chains.

✦ @base quietly became one of the strongest distribution moats in crypto. Coinbase onboarding stablecoin flow consumer familiarity is an unfair advantage most chains simply cannot replicate.

✦ @trondao is quietly becoming the most underrated chain, averaging $800K in daily chain fees and supporting over 50% of all USDT transfers. Nobody calls it cool but it prints.

✦ @HyperliquidX was the second chain ranked by annual revenue in 2025. Proof that when there are real users and real revenue first, the chain becomes valuable because the app already matters.

✦ @ethereum still captures the highest quality liquidity despite everyone calling it “too expensive” every cycle.

✦ @BNBChain’s app revenue went up 3x in Q4 2025 alone, hitting $55M. Real throughput gains, actual users.

✦ Stablecoin giants like @tether and @circle are raking in millions daily in fees, dwarfing most L1s.

✦ Even @SuiNetwork has managed to carve out stronger activity than we expected because there is visible user engagement and ecosystem momentum behind it.

Then you compare that with how aggressively some other chains were valued.

✦ @Sei_Network TVL collapsed from a $628M peak to $41M, now at ~$64M. App fees sit at $11K/day, revenue at $2.8K, and chain fees below $100/day. There is activity, but zero economic density.

✦ @Cardano’s TVL fell 81% from ATH. Solid roadmap, but the users are just not showing up.

✦ @avax is annualizing $8M in 2025 chain revenue against a $600M TVL and billions in FDV. The subnet thesis is superb, but the fee capture isn’t.

✦ @Aptos P/F ratio is sitting at ~327x. Still trading at high FDV with daily chain revenue often in the low thousands. Funded, fast, but still waiting for the moment.

✦ @berachain hit $3B TVL on incentives, then cooled hard once the taps slowed.

✦ @StoryProtocol has a huge IP narrative but the actual onchain economic activity looks whack. They barely even see meaningful fees.

✦ EclipseFND raised big but hovering at tiny daily fees. TVL is down from $48M last year to $1.2M now.

✦ Others like @movement_xyz launched at crazy valuations and are still waiting for demand. How about @SonicLabs? @Scroll_ZKP? The list is endless.

The app layer is clearly eating the infrastructure layer’s lunch, yes most new chains are still trying to win by building more infrastructure.

The truth is, crypto has more infrastructure than users.

Most new chains are not competing against top chains alone, but also the apps already owning user attention.

So the question is no longer if you can build a faster chain. It is if you can attract users that stay.

Can you build distribution strong enough that apps actually choose your ecosystem over the dozens of alternatives offering the same technical promises?

Network effects are way harder now. Liquidity is sticky and capital eventually flows toward places already generating revenue.

So build for usage, not just tech flex. The market eventually catches up to the numbers that matter.

15

1

21

7,053

Jacy🌸 retweeted

May 18

Top important DeFi news to pay attention to this week 🧠👇

1. @aave has restored WETH LTV to its pre-incident level. Users can now once again borrow against WETH, including through collateral and debt swaps.

2. @solsticefi will launch its token, $SLX, on May 21.

3. @trepa_io - a precision-based prediction market on Solana - will launch early access on May 20.

4. @PhoenixTrade is making new waves in onchain RWA perpetual trading on Solana with a fully onchain matching and risk engine.

5. @jito_sol’s Q1 Quarterly Call takes place on May 20. Key updates on staking, MEV, and ecosystem metrics are expected.

6. Raydium may introduce a major DEX upgrade featuring limit orders, dynamic fees, single-sided liquidity, and improved capital efficiency.

7. @LidoFinance DAO’s vote on NEST - an onchain LDO buyback engine - will conclude on May 18.

8. @ALEXLabBTC’s proposal to end $ALEX emissions, discontinue grant programs, and begin protocol-driven token buybacks and burns is open for voting until May 31.

9. @FlareNetworks FAssets v1.3 is now live on mainnet, allowing users to mint $FXRP directly from $XRP on CEXs and use it in DeFi on Flare.

7

7

33

1,745

May 14

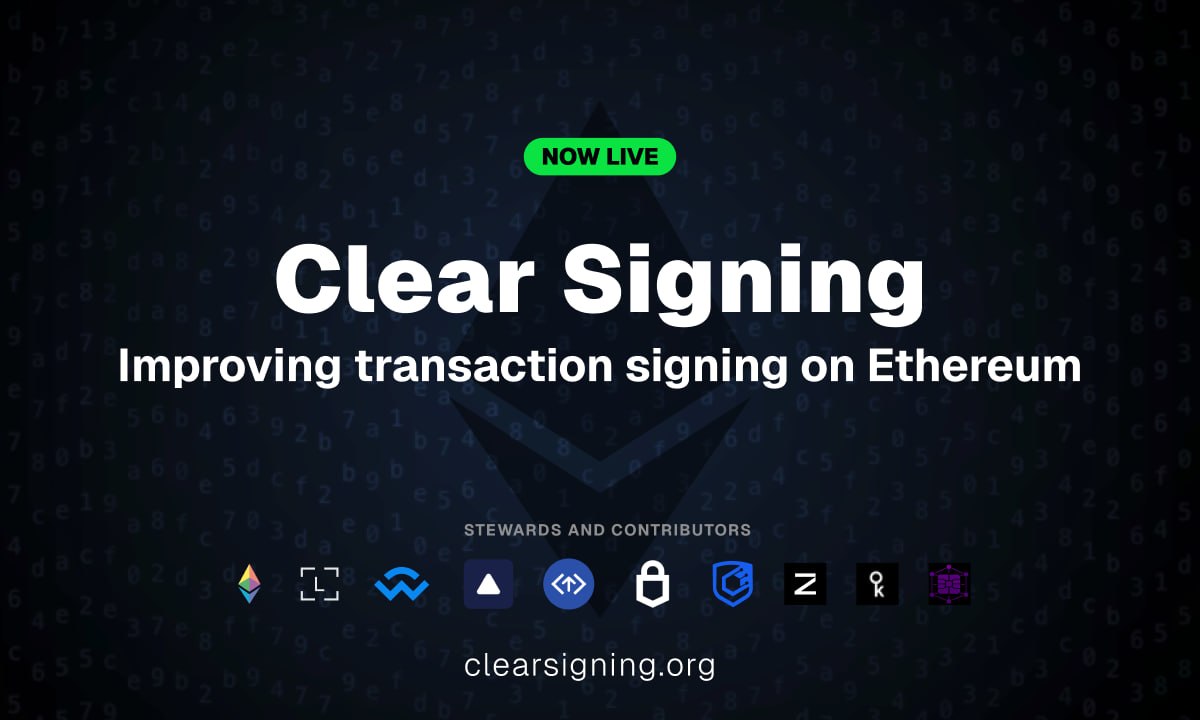

One of the biggest barriers to mainstream crypto adoption is trust.

Imagine approving things you literally cannot read and just hoping nothing goes wrong.

Security mostly depends on users being highly technical, extremely careful, or constantly paranoid just to interact safely on-chain.

That was never sustainable for mass adoption, and clear signing changes that dynamic completely.

And while the tech is great, it is also impressive to see wallets, infrastructure providers, security teams, tooling projects, and the Ethereum Foundation aligning around an open standard instead of fragmented solutions.

Honestly, this is one of the most important infrastructure upgrades Ethereum could push right now. Curious to see how it pans out.

May 12

0/ Clear signing is now live.

An open standard to end blind signing, making human-readable transactions default.

This effort brings a major UX and Security upgrade to transaction signing on Ethereum.

10

1

19

3,336

May 13

If someone receives USDT for freelance work every month, are they really a crypto user or just a worker using better money rails?

Truth is, the most important crypto users today do not even call themselves crypto users.

For the longest time, we measured adoption wrongly.

We looked at wallet downloads, trading volume, memecoin activity, TVL rankings, NFT cycles and other surface metrics.

But the real adoption was happening quietly in the background.

Crypto stopped being a niche financial experiment and started becoming invisible infrastructure.

Most people using the internet today do not think about TCP/IP protocols, cloud servers, or payment routing layers. They just open apps and expect things to work.

Crypto is slowly entering that phase too.

People are no longer using crypto because they are “into crypto”, but because alternative systems are slower, more expensive, or simply broken.

➺ A remote worker in country A saves in stablecoins because inflation destroys purchasing power.

➺ A startup pays international contractors through crypto rails because traditional wires are expensive.

➺ A merchant accepts stablecoins because settlement is faster than local banking systems.

None of these people wake up excited about blockchains. They have just come to terms with the reality of crypto rails outperforming traditional rails in specific use cases.

Especially for cross-border payments, in unstable economies, and for internet-native work.

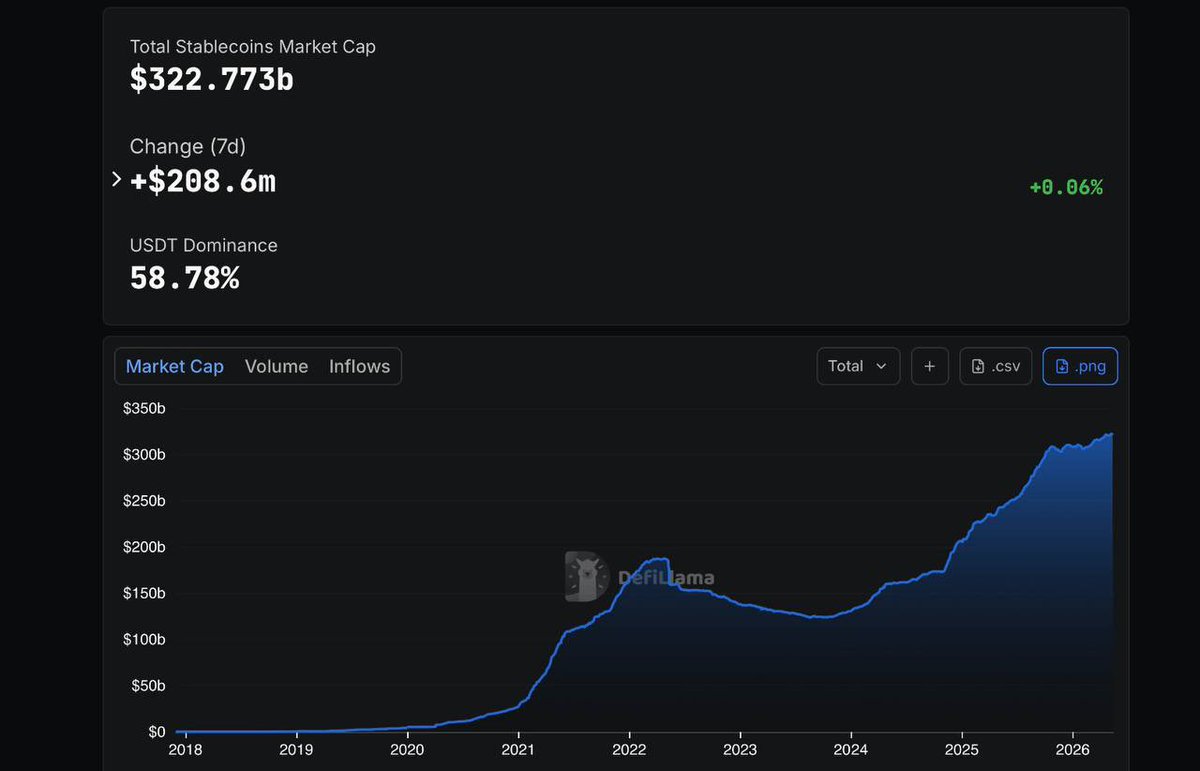

This is why stablecoins are currently experiencing significant growth, hitting new ATHs every other day.

They are clearly becoming one of the most important crypto products, not because they are exciting, but because they remove friction.

Based on current trends, mass adoption is starting to look less like millions of people becoming crypto natives, and more like millions of people never realizing they are using crypto at all.

Eventually, most people sending stablecoins may not care which chain processes the transaction. They only care that it is fast, cheap, and it works.

16

3

16

4,544

Jacy🌸 retweeted

May 8

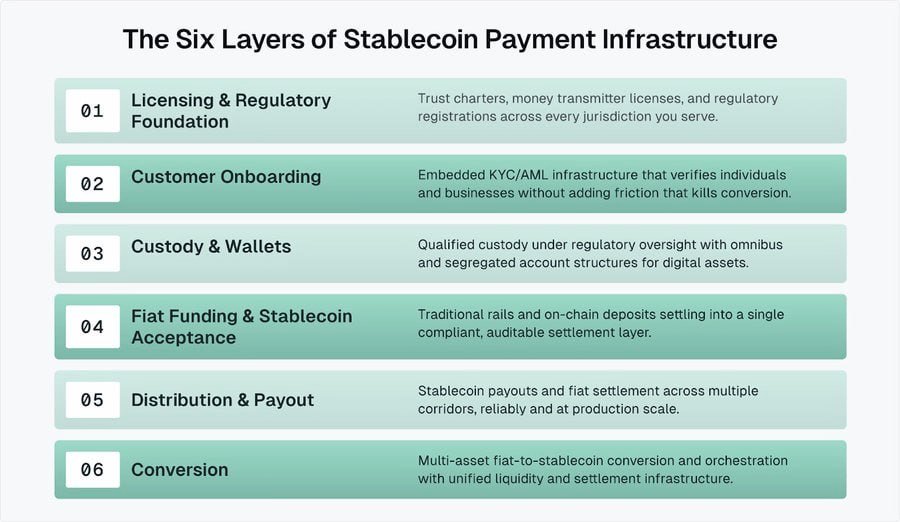

Stablecoins are no longer just “crypto dollars.”

They’re becoming the payment rails for internet-native finance.

But the real moat won’t be who issues the stablecoin.

It’ll be who can coordinate the full stack:

• regulation

• onboarding

• custody

• fiat rails

• payouts

• FX and liquidity.

That’s the hard part most people underestimate.

Sending stablecoins is easy but building compliant, reliable, global money movement around them is the real infrastructure race.

29

5

63

4,828

May 8

Remember this post?

Well, the selectiveness I talked about becomes even more obvious when you look at where VC funding is actually flowing currently.

Investors are betting on sectors they believe can survive tighter liquidity conditions and generate long-term value.

So while overall funding is in decline, some sectors are still attracting heavy conviction and absorbing a disproportionate share of the capital left in the market.

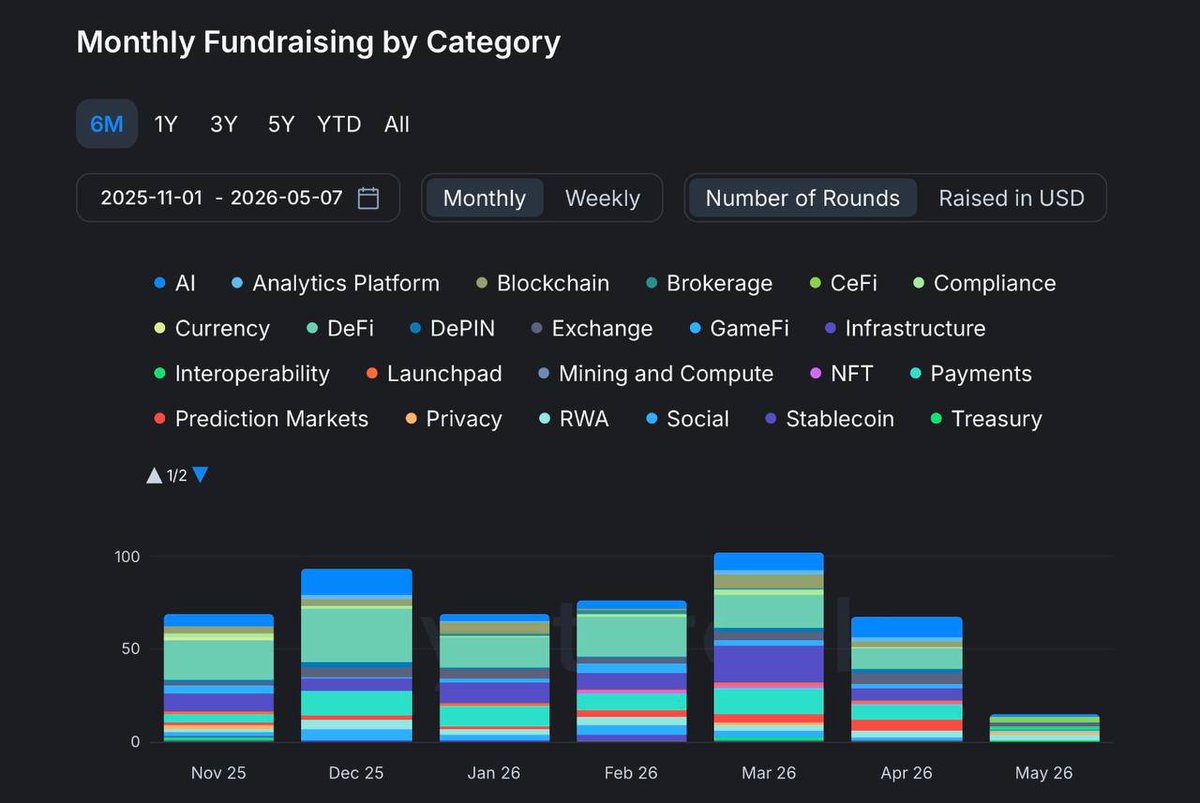

March 2026 was a good example of this shift. Despite crypto VC funding hitting $2.6B in March, the capital was not distributed evenly across sectors.

In other words, the market is not simply reducing capital deployment, it is repricing what deserves to be funded. And lately, the strongest conviction areas have been:

➣ Stablecoin and payment infrastructure

Stablecoins are increasingly being viewed as the most viable crypto product category. As a result, payment infrastructure and settlement rails are receiving stronger institutional attention.

➣ DeFi protocols with real revenue generation

Investors are still willing to bet on DeFi, but the focus has shifted towards protocols with sustainable revenue models, institutional integrations, stablecoin utility, and liquidity efficiency.

➣ On-chain financial infrastructure

If blockchain is going to power global finance, then the infrastructure layer enabling that transition becomes incredibly valuable to investors.

➣ AI x crypto infrastructure

AI is currently one of the strongest funding magnets, but investors are not just funding “AI tokens”. They are backing infrastructure that enables autonomous agents, decentralized compute, data marketplaces, AI coordination layers, and M2M economic systems.

➣ Blockchain services and middleware

Middleware has quietly become one of the safest bets for VCs. These include developer tooling, indexing systems, data infrastructure, interoperability layers, compliance tooling, analytics platforms, and backend systems that support the broader ecosystem.

➣ RWA tokenization

Investors see tokenization as one of the clearest bridges between TradFi and blockchain infrastructure, so the market is moving beyond theory into actual deployment of tokenized treasuries, private credits, and real-world financial assets.

Infrastructure has become the dominant theme because investors now care more about durability than narrative. Even broader VC sentiment outside crypto reflects the same pattern.

Across tech markets, VCs are aggressively prioritizing AI infrastructure, fintech, deep tech, enterprise software, cybersecurity, healthcare, and systems-level platforms instead of consumer speculation.

While overall deal counts are declining, average check sizes are increasing. Meaning investors are making fewer bets, but betting big on high-conviction projects.

This is a very different situation from the 2021 cycle. The easy money era is fading, and only projects that plug into the new reality will survive this downturn.

May 4

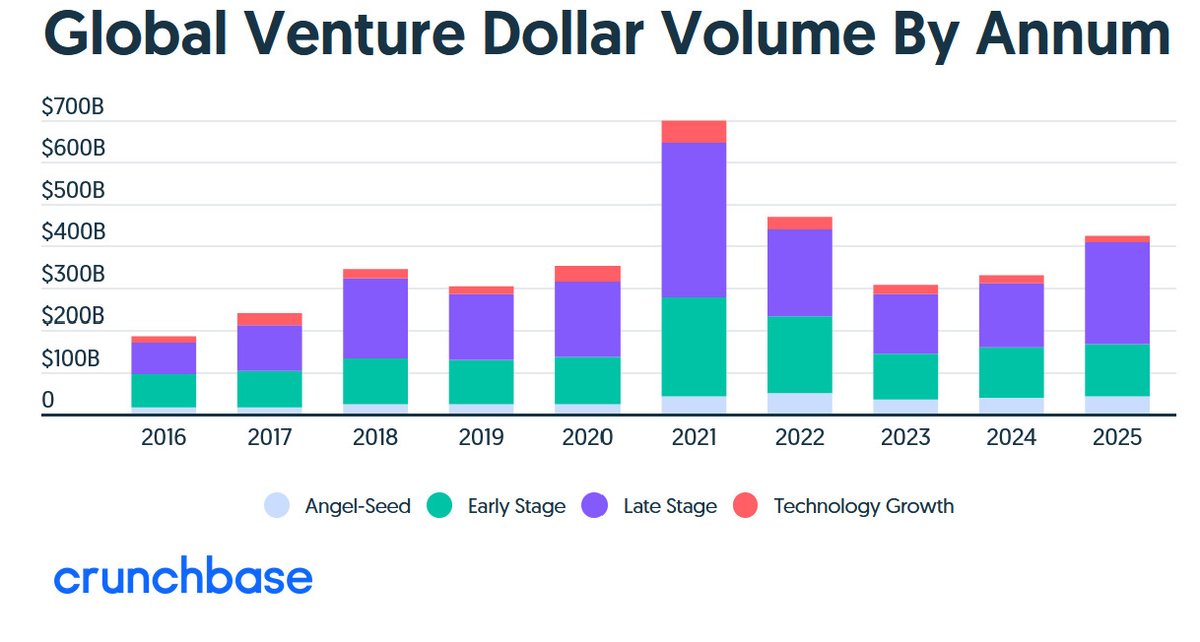

Venture capital (VC) funding has been in decline since reaching its peak in 2021. But it is not simply about less money being available in the market.

Some sectors are seeing more decrease than others. Crypto, for example, dropped significantly as VC funding in April 2026 fell from $2.6B to $659M. This marked a 74% decline from March’s figures and the lowest monthly level since July 2024.

In 2021, global VC funding reached well over $600B. By 2023, funding dropped largely ($285B) and even with a rebound in 2025 ($425B), it still has not bounced back.

However, let us look beyond the total funding. The real issue is how capital is distributed.

Deal activity has been falling even when funding rises. In 2024, deal count was down 17% YoY, while larger deals took a bigger share of the total capital. At the same time, average deal sizes increased.

Fewer startups are getting funded, but those that do are raising more capital. It is a pattern that shows up consistently across sectors and there are several factors causing this move:

➤ Higher interest rates and less appetite for risk

➤ Weak IPO market, slower exits and less recycled capital

➤ AI is pulling in a huge share of funding

When you compare yearly and quarterly data, the instability is clearly visible:

➤ Q1 2025 funding rose to around $80B, partly driven by a single large AI deal

➤ Q2 2025 dropped from around $114B to $91B quarter-to-quarter

➤ Overall, 2025 rebounded compared to 2024, but still remained below the 2021 high

It creates a misleading picture. Funding appears to recover, but most of it is driven by a small number of large deals. Remove those and the underlying market still looks weak.

If this downtrend continues:

➤ Fewer startups get funded

➤ Investors gain more power

➤ More acquisitions happen, resulting in fewer independent companies

➤ Funding inequality expands

➤ Innovation becomes more selective

So the bottom line is this: VC funding is not just declining, it is becoming more selective. It shows in the numbers, deal structures and how the market is inching toward funding what is proven instead of funding everything.

18

3

40

6,303

May 6

Most chains say they are “institution-ready”, but @avax is one of the few chains actually building like institutions are already here.

To position a chain as a hub for institutionalization, you have to go deeper than speed and low fees.

The real focus is on infrastructure design that mirrors how institutions already operate.

While Avalanche is not the loudest ecosystem, here is why I think it is the next big thing for institutions:

~❉᯽❉~

◈ Avalanche L1s (subnets):

Institutions do not want to share execution environments with meme coins, random DeFi experiments, or unpredictable congestion.

Avalanche lets them deploy dedicated blockchains with:

➸ Custom validator sets (including permissioned validators)

➸ Built-in compliance logic (KYC/AML at the protocol level)

➸ Jurisdiction-specific controls

➸ Defined fee structures and predictable economics

That means institutions do not need to “adapt” to crypto. They can replicate their existing regulatory and operational environment onchain, then extend it.

◈ Deterministic performance:

Avalanche’s consensus gives near-instant finality, typically under a second.

Institutions care about:

➸ Settlement certainty

➸ Reduced counterparty risk

➸ Real-time reconciliation

Compare that to probabilistic finality on networks like Ethereum, where final settlement assumptions can still introduce operational complexity.

Avalanche aligns much closer to TradFi settlement expectations, but with blockchain efficiency.

◈ Cost structure control:

On shared L1s, fees are volatile. For institutions running large-scale operations, that is a budgeting nightmare.

Avalanche L1s allow:

➸ Fixed or predictable fee models

➸ Custom gas tokens

➸ Isolation from network-wide congestion

This makes it perfect for high-volume use cases like payments, trading infrastructure, and tokenized asset issuance.

◈ Modular interoperability without forced exposure:

Avalanche’s architecture enables communication across L1s and with the broader ecosystem, but on controlled terms.

Institutions can choose:

➸ What assets move across chains

➸ What counterparties they interact with

➸ What level of openness they allow

This is important for tokenized RWAs, where compliance, privacy, and access control are not optional.

◈ Institution-grade privacy and compliance pathways:

Public blockchains are transparent by default, which clashes with institutional requirements.

Avalanche’s design allows:

➸ Permissioned environments

➸ Selective data visibility

➸ Integration with identity layers

So instead of forcing full transparency, it enables configurable transparency, which is far more aligned with financial regulations.

◈ Operational familiarity:

Avalanche does not force institutions into entirely new territories. With EVM compatibility, institutions can:

➸ Reuse existing tooling

➸ Port smart contracts

➸ Leverage established developer ecosystems

This lowers the barrier to entry significantly compared to building from scratch on non-EVM systems.

◈ Institutional onboarding strategy:

Avalanche has leaned into real-world collaboration, from tokenized funds to pilot programs involving financial institutions.

These partnerships are not just for headlines, they are shaping how institutions actually use blockchain infrastructure.

Here is raw proof of its real-world adoption:

➸ RWA tokenization:

@BlackRock, @Securitize, and @apolloglobal have tokenized funds on Avalanche.

➸ Financial institutions:

Some of Avalanche’s partners include @jpmorgan (Onyx platform), @Citi, @WisdomTreeFunds, and @FTI_US.

➸ Enterprise Applications:

@Deloitte uses Avalanche for FEMA disaster reimbursement, and @Togg2022 (Turkish EV manufacturer) uses it for smart vehicle mobility initiatives.

~❉᯽❉~

Avalanche is not trying to be the loudest ecosystem. It is building a financial infrastructure where:

➸ Institutions get control

➸ Compliance is native

➸ Performance matches real-world financial demands

➸ Interoperability exists without sacrificing boundaries

Other chains are optimizing for open participation first, then trying to retrofit institutional features later.

Avalanche is building for institutions first, and letting everything else plug in around that.

If institutional adoption is what takes this space to the next phase, @avax is not waiting around for it. It is already building for it.

16

27

5,399

Jacy🌸 retweeted

May 5

Telegram becoming TON’s largest validator strengthens decentralization.

It lets other major players join the validator pool without centralizing the network — with Telegram as the counterbalance.

📈 More and more TON gets locked in validation as everyone competes for 20% APR.

687

672

5,090

339,502

May 5

Imposing conditions on recovery is unacceptable.

We are talking about people’s life savings being lost in this exploit. The team should be prioritizing unconditional support rather than creating hurdles.

I feel so bad for the victims.

May 5

We told our community we would find a path to recovery. This is that path.

Today’s update covers: how users will be compensated and how the exchange is being rebuilt.

4

17

1,966

May 5

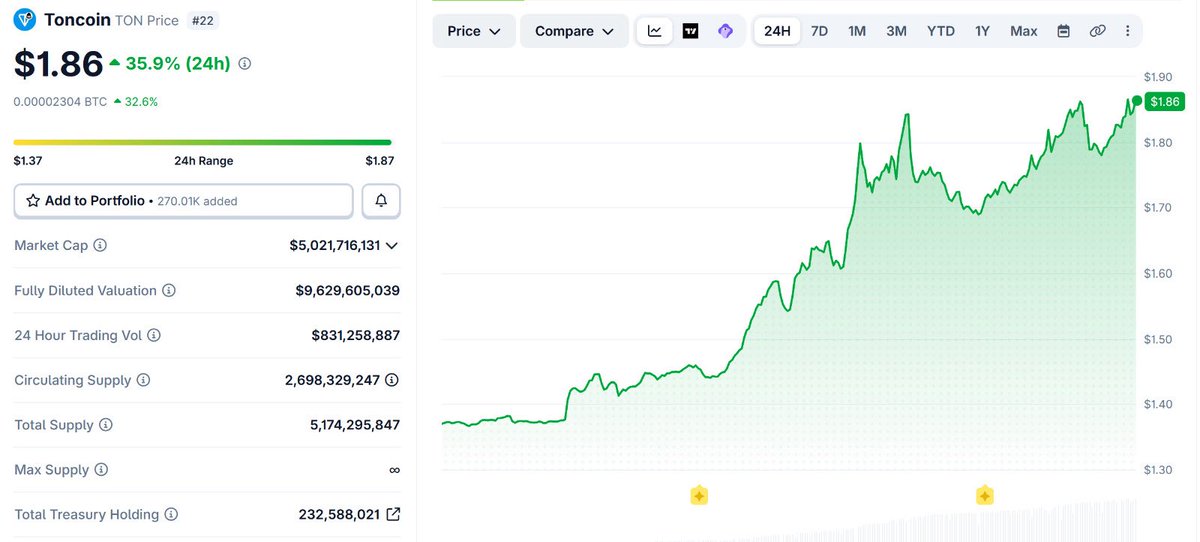

TON blockchain has shared another update, following its 6x fees reduction.

On May 4th, Telegram CEO @durov, announced that Telegram will replace the TON foundation as the driving force behind the blockchain and become its largest validator.

TON reacted immediately, as its price went from $1.37 to $1.84, resulting in around a 30% growth within 24 hours. Trading volume also increased by 600%, while its Mcap rose to $4.5B.

Memecoins built on $TON, @notcoin and @realDogsHouse also experienced price surges of 26% and 90% respectively, after the announcement.

Until now, @ton_blockchain has been more community driven. Telegram is now stepping in and connecting its 950M user app to a single blockchain that helps it run.

Telegram becoming the largest validator means;

➸ It helps validate transactions

➸ It has real say in how the network evolves

➸ Its business incentives will be tied directly to $TON

Telegram is not just supporting $TON anymore, its revenue flow will be built around it as well. Take the Telegram ad platform for example, advertisers pay for ad placements using $TON and channel owners receive 50% of that revenue in $TON also.

Every ad purchase creates buying pressure and every payout pushes that value back into the ecosystem. The network is already active, with 1.5B transactions in Q1 2026 alone and $1.2B TVL by April 2026.

Telegram becoming the largest validator also means that it becomes the most powerful player on the network. However, it is great for growth, but not so much for shared control.

🎯So the real question this move raises is; Can $TON grow without losing what makes it valuable in the first place?

Definitely a situation worth watching closely.

9

1

14

4,379

May 4

Venture capital (VC) funding has been in decline since reaching its peak in 2021. But it is not simply about less money being available in the market.

Some sectors are seeing more decrease than others. Crypto, for example, dropped significantly as VC funding in April 2026 fell from $2.6B to $659M. This marked a 74% decline from March’s figures and the lowest monthly level since July 2024.

In 2021, global VC funding reached well over $600B. By 2023, funding dropped largely ($285B) and even with a rebound in 2025 ($425B), it still has not bounced back.

However, let us look beyond the total funding. The real issue is how capital is distributed.

Deal activity has been falling even when funding rises. In 2024, deal count was down 17% YoY, while larger deals took a bigger share of the total capital. At the same time, average deal sizes increased.

Fewer startups are getting funded, but those that do are raising more capital. It is a pattern that shows up consistently across sectors and there are several factors causing this move:

➤ Higher interest rates and less appetite for risk

➤ Weak IPO market, slower exits and less recycled capital

➤ AI is pulling in a huge share of funding

When you compare yearly and quarterly data, the instability is clearly visible:

➤ Q1 2025 funding rose to around $80B, partly driven by a single large AI deal

➤ Q2 2025 dropped from around $114B to $91B quarter-to-quarter

➤ Overall, 2025 rebounded compared to 2024, but still remained below the 2021 high

It creates a misleading picture. Funding appears to recover, but most of it is driven by a small number of large deals. Remove those and the underlying market still looks weak.

If this downtrend continues:

➤ Fewer startups get funded

➤ Investors gain more power

➤ More acquisitions happen, resulting in fewer independent companies

➤ Funding inequality expands

➤ Innovation becomes more selective

So the bottom line is this: VC funding is not just declining, it is becoming more selective. It shows in the numbers, deal structures and how the market is inching toward funding what is proven instead of funding everything.

13

58

7,407

May 3

Not a day goes by where we don’t see any drama 😂😂

May 3

MegaETH vs Monad (Context so far)

Timeline so far:

1. Zayn (Monad) asks publicly whether MegaETH has any agreement with Binance for the listing, or if it was a unilateral Binance decision.

2. Bread (MegaETH) replies (now-deleted tweet): roughly in these words "Binance bought MEGA on the open market."

3. James (Monad) follows up: "are you asserting that neither MEGA nor any person/entity associated with MEGA signed any legal contract with Binance?"

4. Shuyao (MegaETH) responds: "No MEGA has been provided as airdrop or marketing fees to CEXs for listing purposes. I had Bread delete his tweet because, as an ecosystem lead, he did not understand how asset listing works and misspoke."

5. James replies: it's possible Binance just woke up and listed MEGA out of goodwill, but that's extremely unlikely, it would set a bad precedent for future listings. More likely there's a side agreement giving Binance, its team, or its investors a way to make money via some other route.

6. Abdul (ex-Monad) digs into what MegaETH actually paid Binance in the QT

The unanswered question is, if not tokens, then what?

9

20

1,362

May 2

Last month should have been a wake up call for anyone still underestimating crypto risk.

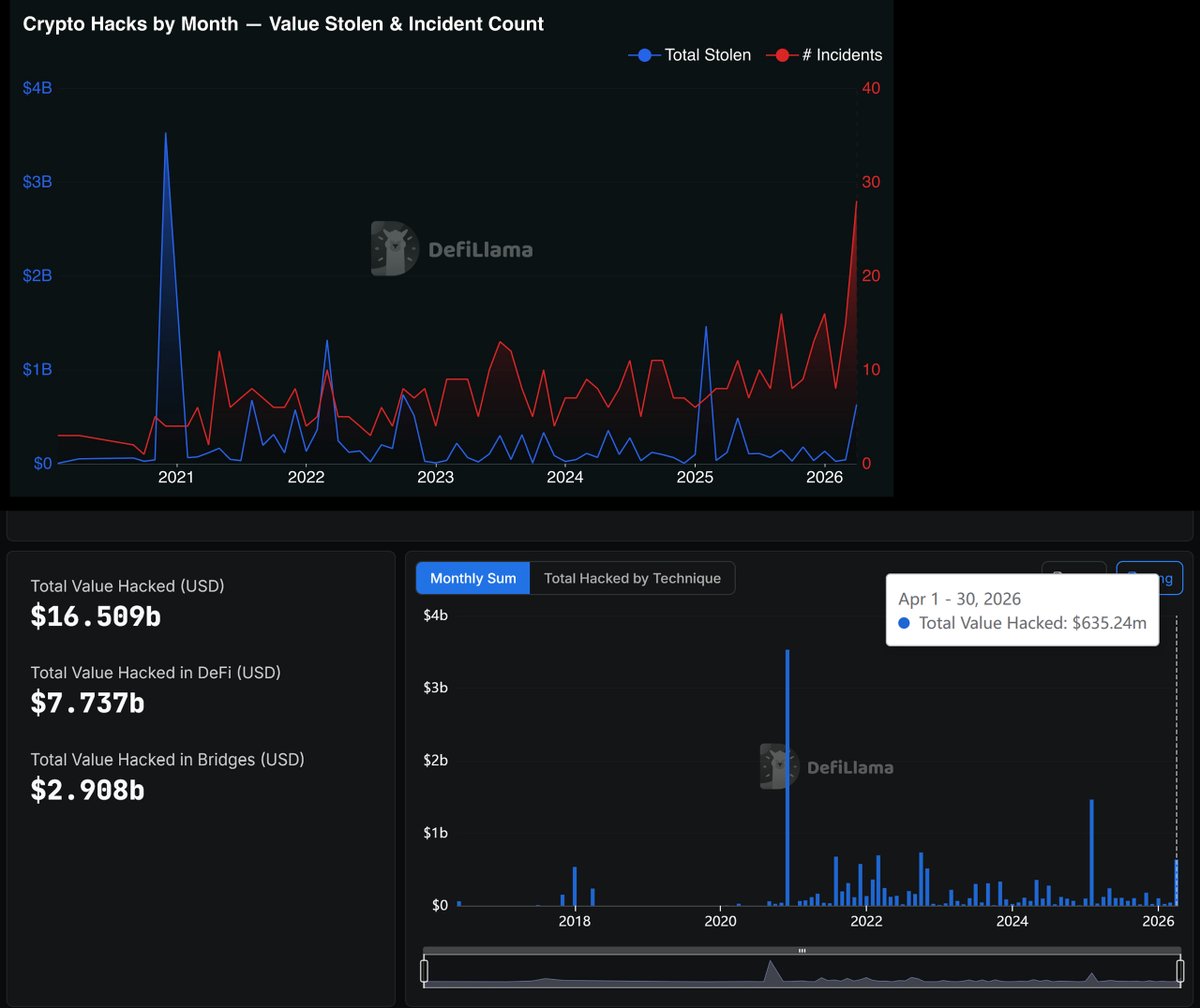

The various hacks that occurred proved that security is not keeping up. In April 2026 alone, DeFi exploits crossed over $630M in losses across 26 different hacks (according to CoinMarketCap - x.com/coinmarketcap/status/2…).

Let's break it down 👇

Most people will focus on the bigger numbers like;

➸ @KelpDAO ($290M drained)

➸ @DriftProtocol ($280M exploited)

That is just two incidents and over half a billion dollars gone.

But it was not just two hacks. The entire ecosystem seemed to be under pressure at the same time;

➸ @purrlend ($1.5M exploited)

➸ @wasabi_protocol ($4.5M lost)

➸ @volo_sui ($3.5M drained)

Along with dozens of other attacks most people will not even hear about.

So in a single month, we’ve had;

➸ Massive protocol breaking exploits

➸ Smaller, constant drains happening in the background

➸ Retail users getting hit through indirect exposure

It goes to show just how fragile the security culture really is.

With the rise in AI assisted exploits, these attacks are getting smarter. It points to faster vulnerability discovery, more scalable attack strategies and more convincing social engineering with fake identities posing as trusted insiders.

And this is where crypto has a real problem. From the outside looking in, people see;

➸ Platforms losing hundreds of millions overnight

➸ Users with no protection or recovery options

➸ A system where one mistake equals total loss

You cannot build the future of finance on systems that fail this often.

Security in crypto is still treated like a feature instead of infrastructure. At the moment, to a lot of protocols, throughput means more to them than safety.

People tend to only focus on security after something breaks, while hype gets way more attention than actually building strong, reliable systems. When that is the pattern, you can already guess how things will turn out.

If crypto wants to be taken seriously, three things need to happen:

✦ Prioritize security during development

✦ Better user protection layers such as insurance and other recovery mechanisms

✦ Accountability when protocols fail

Until then, every major hack will reinforce the narrative that says, “This space is not ready”. The technology and opportunities matter less if people do not feel safe. And right now, they don't.

May 1

📰 Narrative of the Week: DeFi Exploits Surge

📌 Purrlend exploited for $1.52M across MegaETH and HyperEVM.

📌 Wasabi Protocol loses over $4.5M across multiple EVM assets.

📌 Sui-based Volo exploited for $3.5M from Volo Vaults.

📌 April records 26 known hacks with losses exceeding $630M.

The rapid rise in AI-assisted attack sophistication is exposing major weaknesses across DeFi infrastructure.

3/6

17

4

54

5,571

Jacy🌸 retweeted

May 1

STREAM: Influencer Marketing for AI Product Launches x.com/i/broadcasts/1NGaraqmN…

13

6

69

3,872

Apr 30

Can’t believe I really went away for a month!! 😅

What did I miss??

Apr 2

We need to talk about perp DEX airdrops.

From a user experience angle, it feels like people are doing more just to earn less lately.

Once upon a time, airdrops worked differently. You interacted with a product early, took some risk and you got rewarded.

Now, most perp DEXs run on activity based systems:

➸ Trade more

➸ Deposit more

➸ Generate volume

➸ Stay active longer

In reality, its simply “pay-to-earn” rewards. The more you trade, the more you earn.

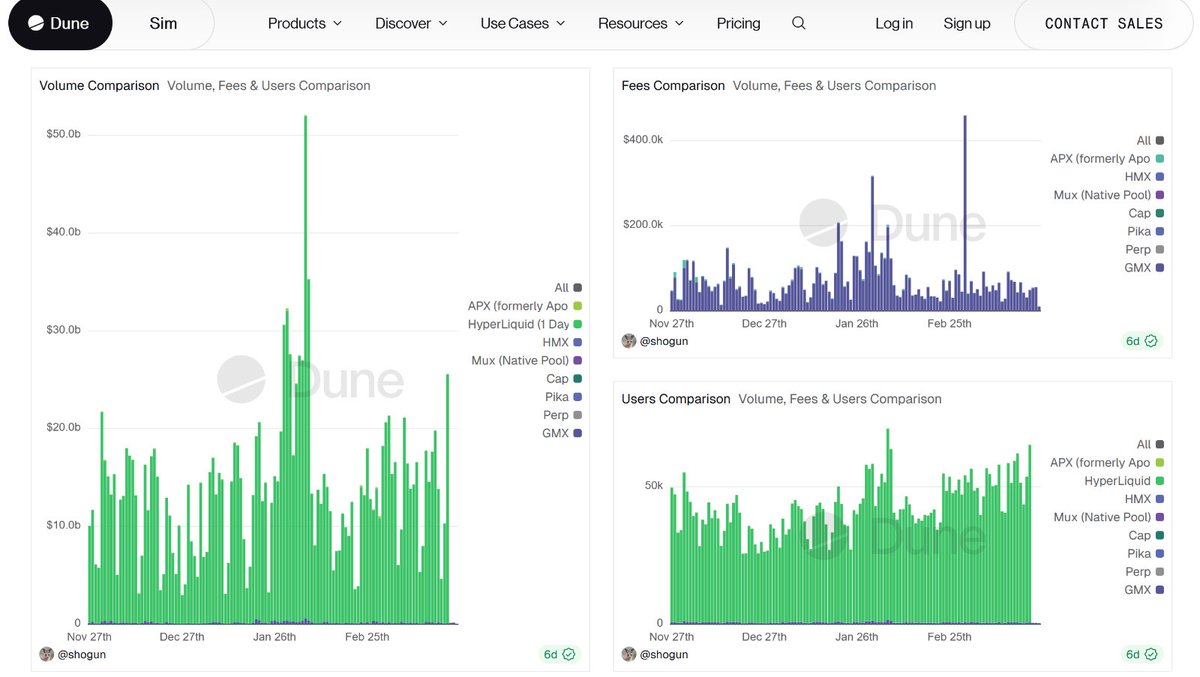

After @HyperliquidX massive airdrop, the entire market seemed to follow one model; points system, rankings and volume based rewards. This system showed some really impressive results.

Perp DEX volume exploded, crossing trillions in 2025 and daily volumes pushed past tens of billions. See aggregate perp DEX activity here: (dune.com/blocmatesresearch/p…).

Airdrops stopped being rewards and became growth engines while users became liquidity.

Look at how it plays out across protocols:

🎯 On @aevoxyz, rewards leaned heavily on options and perp activity. Users who ran higher volume strategies accumulated points significantly faster than casual traders.

🎯 Campaigns from @ZetaMarkets and @vertex_protocol follow the same pattern and since the structure is consistent, the outcome is too.

To even qualify meaningfully today, users are expected to:

➸ Trade regularly

➸ Pay fees repeatedly

➸ Take on market risk

➸ Commit capital over time

But after all that, results are still unpredictable because allocations are unclear, rewards are diluted across thousands of participants and payouts often do not match the effort.

At the same time, the playing field is not exactly level. Large traders dominate leaderboards, automated strategies optimize for everything and multi-wallet farming still finds ways to compete.

Protocols are trying to filter out low effort farming and reward meaningful usage. For this, volume and fees are the easiest metrics to track and by doing that, they have shifted airdrops away from early participation to capital efficiency.

Instead of being an upside for early users, they have become competitive systems where outcomes depend on how much you can put in but not when you showed up.

And that is what makes it unfair. Because the system asks everyone to play even when only a small group is positioned to win.

Airdrops used to reward early belief and participation, now they reward capital and efficiency. For the average user, that changes the game, not just in how much they earn, but whether it is even worth playing at all.

6

13

672

Jacy🌸 retweeted

Apr 17

Watch @IsdrsP break down Lido V3 & Lido Earn, and how both work to unlock institutional adoption of staking and DeFi across Ethereum.

youtube.com/watch?v=3Rpg8zxI…

24

16

58

8,285