3,048 Photos and videos

8h

$MDA is my top space stock to DD

Love the V space basket names. Ones that I want more exposure to: $IRDM $MDA $SIRI $VSAT

Have been in/out of $IRDM getting too cute swing trading but conviction is already there for me. Really want to dig in deeper on $MDA and $SIRI in particular.

They will find out the hard way.

It’s only just recently (some) spacemob getting Viasat after it already 9xed. SES, OHB, AstroScale etc all over looked.

But really the US investors should be onto MDA, it’s listed. At least @JaguarAnalytics sees it! Called a $100 USD target!

1

2

824

Jun 13

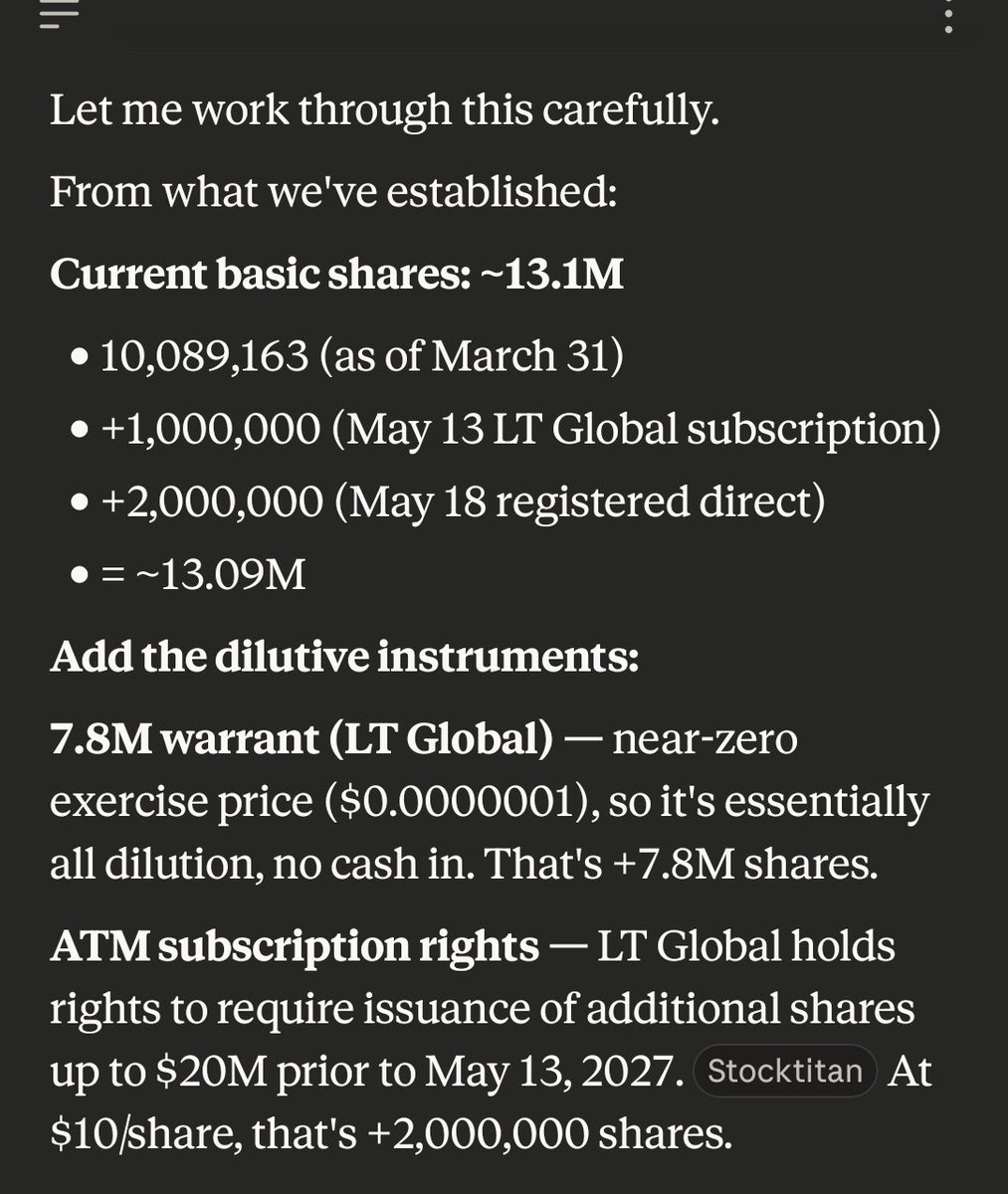

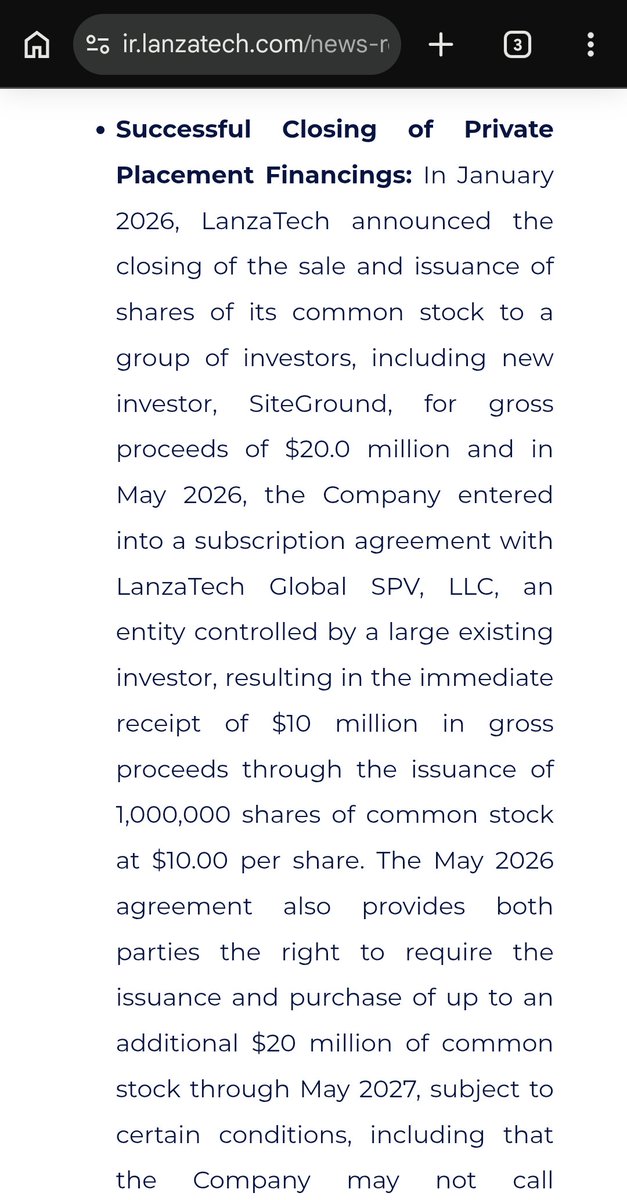

$LNZA volume really coming in lately, huh? I wonder if it has to do with the company likely getting options soon (see a prior post I shared yesterday).

We got a serious gap to fill imo. The offering was $10/share and frankly NOT that dilutive. The ATM is reasonable and has limits on when it can be used. Share issuance authorization is really not that crazy to worry about down here in MC.

1

3

499

Jun 13

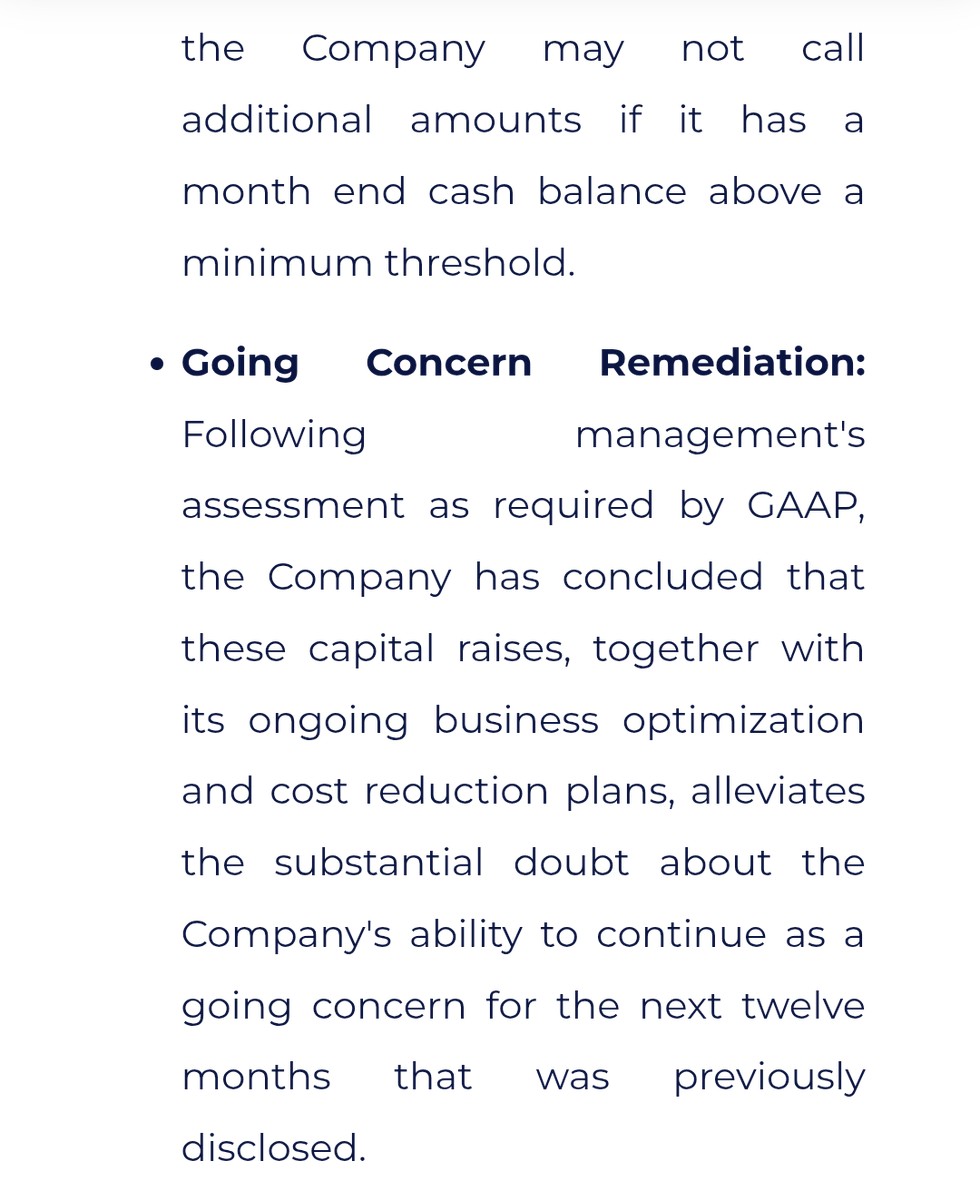

I have done some light further review and am leery of this presentation's guidance that no further raise is needed. It seems to imply a steep revenue ramp need within 18 months. Not sure I see how to thread that needle on my own, so I reached out to IR. Will share what I hear back.

1

1

85

Jun 13

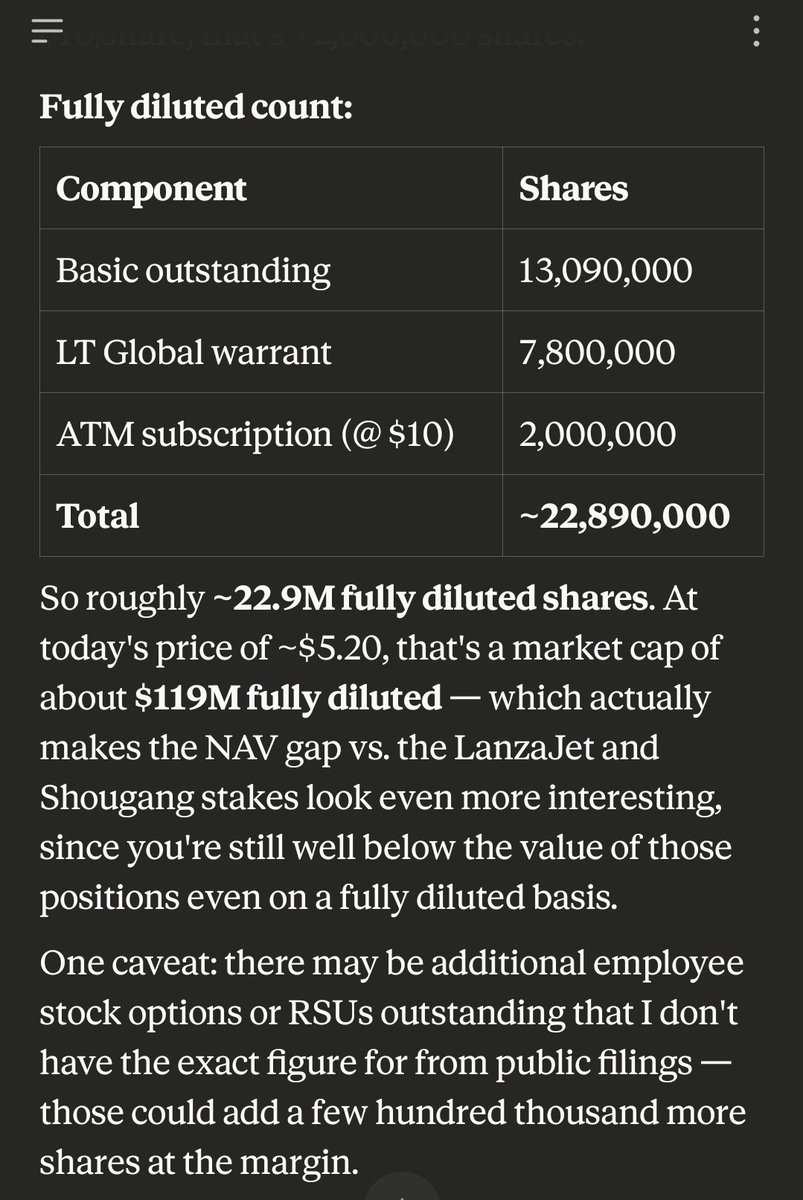

$LNZA quick cap analysis (likely flawed as I have not combed thru filings, would love feedback)

MC still at just $120m if fully diluted out. That includes real cash, low burn rate, real revenue, real growth, real value from public JV in China and inflecting LanzaJet business.

Feels like a no-brainer long-term hold. Going to grab some more next week. Hope we stay down below 6 a bit longer.

1

278

Jun 13

We were above $250m MC even with dilution likely in the pipeline back in May 2026. That was with the jet fuel surge lifting illiquid SAF basket plays.

Likely helped to nudge LanzaTech over the finish line with getting the final cash they needed after severe dilution/split and bankruptcy scare last year.

I gotta think not unreasonable to see $250m MC again. Even if you take a fully diluted view, that's a 2x from here. And that's conservative imo.

1

1

117

Kevin retweeted

Jun 13

Wonderfully ironic that the abvx cancer panic is uno reversed in that its probably lowering the incidence of dysplasia in uc ergo normal cancer rates.

I'd respond to @meremrtl in his post directly, but he blocked me for politely disagreeing with him on $NKTR. There's something VERY important that he is VERY wrong about that I'd like to highlight.

It's funny that he recognizes that the 2 solid tumor cases in the $ABVX trial are mere bad luck/noise. I agree with him that the latency argument for solid tumors argues that these cancers pre-dated the $ABVX study given that they were slow-growing cancer types identified far too early (6-8 months) to be due to $ABVX's drug. These are the cases the market has been freaking out about, so...good to see you're an $ABVX bull, Stephen!

Now the point he is making about colonic dysplasia is very, very (very very very) stupid. He is trying to say that the single case of colonic dysplasia is the worrisome finding in the $ABVX study. I'll provide data to show you that his take is objectively stupid, so that he doesn't whine about me saying so. I'm not being mean - I'm calling a spade a spade, and of course very smart people can make very stupid points sometimes😉

There was 1 case of colonic dysplasia in the entire P2-P3 program for $ABVX.

In P3 we have ~310 patient years of exposure across arms (388 patients x ~80% 1 year completion rate). In reality 310 is a slight underestimate as we don't know when the other 20% discontinued, but it wasn't day 0. Still, let's be conservative.

In P2, we have ~130 patients treated across 5-7 years in the long term open label extension. Let's be overly conservative here too, and say 100 patients for 5 years = 500 more patient years.

So, very conservatively, we have ~810 patient years of obefazimod exposure.

1 case of colonic dysplasia. 810PY. That makes the colonic dysplasia event rate 0.12/100 Patient-Years on Obefazimod so far.

What Stephen (very very stupidly) fails to ask is: "What is the expected rate of colonic dysplasia in this patient population at baseline?".

The answer is ~1.77/100PY. ~15x higher than what $ABVX is showing.

Yeah, the expected background rate of colonic dysplasia in this population (long-term UC patients with median age in the 40s) is ~1.77/100PY, FIFTEEN TIMES HIGHER THAN WHAT IS BEING SEEN IN THE $ABVX TRIALS.

Colonic dysplasia is actually a relatively common (nonmalignant) event in general, but it is especially common in ulcerative colitis patients because their chronically inflamed colons are at a high risk of accumulating DNA mutations and immune dysfunction that leads to carcinogenesis.

What we are seeing in the $ABVX trials is actually a DRAMATICALLY lower than expected rate of colonic dysplasia, which is suggestive of A DECREASED RISK OF COLONIC DYSPLASIA AND COLON CANCER due to high levels of disease control.

Really, it's very simple...UC patients have a high risk of colon dysplasia/cancer because their colons are so severely inflamed...$ABVX's obefazimod stops that inflammation, LOWERING their risk of developing it. Not only is this mechanistically supported...the DATA support it as well.

What Stephen is highlighting as the big scary AE for $ABVX is actually an objective POSITIVE for the company if you have the brain and objectivity to analyze the data. However, some people (like Stephen) are just here to stir the pot! Oh well. The data are very clear, and they are bullish for $ABVX.

But hey, even Stephen signed off on the "real cancers" as not being a concern! Maybe he is coming around to be an $ABVX bull himself!

Source data: journals.lww.com/ajg/fulltex…

1

2

20

2,605

Kevin retweeted

Jun 12

*IRAN CIVILIAN NUCLEAR POWER PLANTS ACCEPTABLE: US OFFICIAL

1

5

395

Jun 11

Just presented at Future Tech Conference:

LanzaTech Global $LNZA — CEO Dr. Jennifer Holmgren

Waste carbon → sustainable aviation fuel and specialty chemicals. Europe's first commercial SAF facility site selected. DRAGON II UK project advancing. Commercial plants operating across Asia and Europe.

Full replay: redchip.news/3RfnDbf

#LNZA #SAF #CarbonRecycling #CleanEnergy

1

1

728

Jun 12

I just watched and some top of mind highlights:

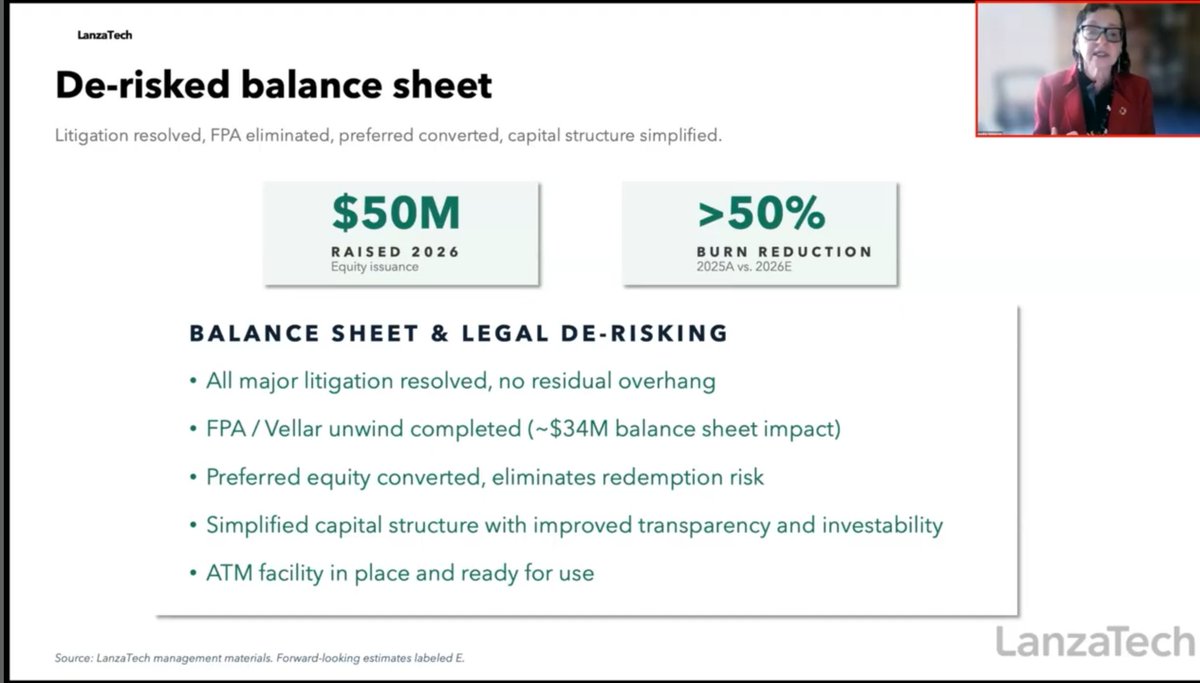

- I trust Jennifer Holmgren. This is one of the most thoughtful CEO readouts I have ever seen. She is confident in the turnaround.

- On no unclear terms, no more raises are expected. An ATM facility is in place if needed, but it was CLEARLY stated there is no more need after recent raises and restructuring.

- No gross capital structure with preferred equity: all commons now.

- They have proven their licensing model and are ready to progress toward a debtco blended model where they capture the ethanol fuel upside themselves.

- They have 5-10 years of biotech AI experience. "Large science models".

I'm legitimately pumped. I have gone max spec on this but am upgrading to "real boy" status. I think this could be like catching Velo3D (who, funny enough, presented right before LanzaTech during the conference and also uses a licensing approach).

2

1

376

Jun 13

$LNZA watched it again with the slides on YouTube. Some bangers attached.

Not a lot of us talking LanzaTech these days after some big names discovered it and (rightfully) moved on early last year. Would love any pushback on what I might not be seeing with this company. Planning to do some deeper DD and actually (gulp) read SEC filings to understand cap structure / etc. Will likely dig in on the Chinese public JV as well. Just weirdly tickled by this one, kind of a pet project. I see the real opportunity to get a 20x type return here and want to see if that's just a mirage.

2

150

Jun 12

Jun 12

🚨 TIME IS MONEY 🚢

The American Supply Chain Soverienty Initiative will make sure products can move faster through the Port of Los Angeles... which handles $1 BILLION of cargo EVERY DAY!

That means things get to the AMERICAN PEOPLE quicker and at a cheaper price.

Now I need Congress to make it easier for @USDOT to secure and streamline the supply chain so we can move at TRUMP SPEED🇺🇸

3

282

$ABVX seems to have (in the last hour or so?) quietly released a new corporate deck with 3 important slides at the end. All, in my opinion, providing strong new information showing that these cancer cases were unrelated to drug and equivalent to expected background noise.

Most important is the slide on the 2 non-nonmelanoma skin cancers. BOTH of these were more indolent, low/intermediate subtypes of their respective cancer (prostate and breast). Not only does this mean that the cancers are less threatening, it also means that THEY ARE SLOWER GROWING CANCERS. Why is this particularly important? Because it means that the development of the cancers very (very) likely PREDATES THEIR ENROLLMENT IN THE TRIAL. Look into the doubling times of grade 2 (Gleason 7) prostate cancer and grade 2 NST breast carcinoma. These are slow-growing tumors that very likely existed before these patients ever even had a dose of obefazimod.

That relates to another key finding on this slide - the prostate cancer case was identified via PSA screening at 8.5 months into the study (remember earlier is better). In the Guggenheim conference they had said it was confirmed at day 367...they must have been referring to the biopsy confirmation of the subtype, not PSA confirmation of the prostate cancer diagnosis. This new information speaks to an earlier diagnosis. The breast cancer patient was diagnosed even earlier than that! Only 6.8 months of Obe exposure.

Also, these new slides give us actual information on the prior drug exposures - before this afternoon we knew that they were on some prior treatments, but we didn't know what...THE PROSTATE CANCER WAS PREVIOUSLY EXPOSED TO ***5*** DRUGS WITH LABELED CANCER WARNINGS BEFORE ENROLLING IN THE STUDY! 3 OF THEM HAD ***BLACK BOX WARNINGS*** FOR CANCER RISK!

-Humira (black box)

-Infliximab (black box)

-Rinvoq (black box)

-Entyvio (warnings and precautions)

-Stelara (warnings and precautions)

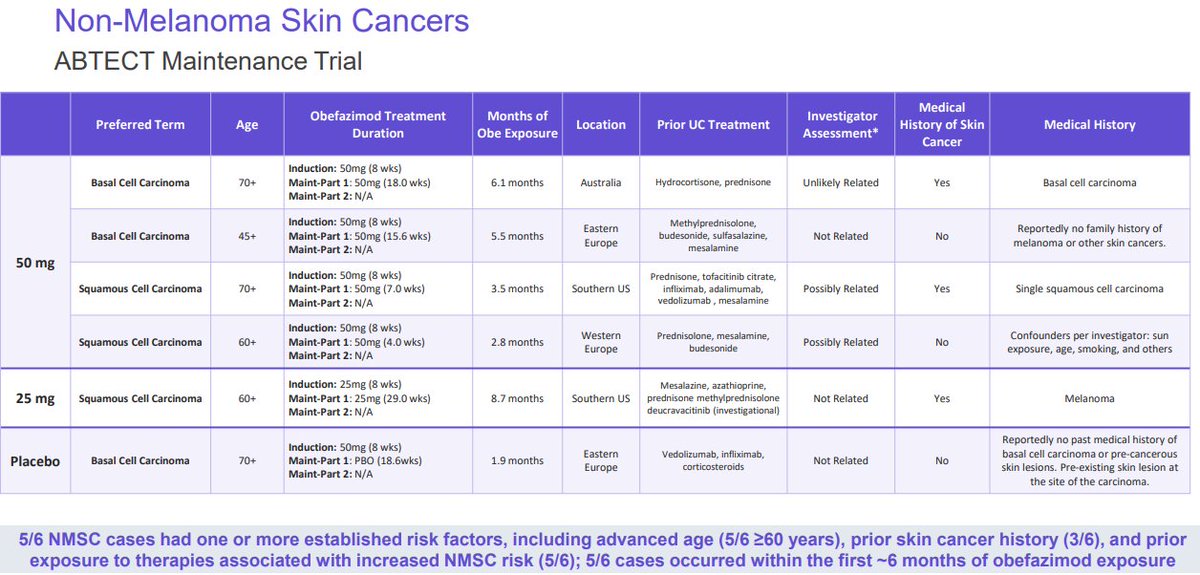

We also just got new info on the NMSC cases (which matter far less but which spooked the market anyway).

How you can look at the details of these skin cancer cases and think they are related to the drug is beyond me (but then again, these details just got released - quietly, for some reason).

First of all, ***ALL OF THE 4 50MG CASES OF NMSC OCCURED IN 6 MONTHS OR LESS!!! Again, too rapid to be reasonably assumed drug-related. The fact that they all happened in the first half of this study is actually extremely exculpating evidence for $ABVX.

Other details:

-4/5 were 60 years old (STRONGLY associated with skin cancer risk)

-3/5 had PRIOR SKIN CANCER ALREADY(!!!!!)

-4/5 had prior exposure to other drugs that are known to increase skin cancer risk.

Finally, they also added a slide discussing that some studies have shown the elevated risks of these cancers for UC patients at baseline.

-~5x higher risk of prostate cancer in IBD patients

-~2x higher risk of breast cancer in IBD patients

Why did $ABVX add these 3 slides to the corporate deck randomly, silently, on a Friday afternoon? IDK. Legitimately good news in those slides! I'd have pressed released this info as soon as I had it, because the details really help alleviate the (already statistically misguided) concern that these cancers could've been caused by Obefazimod.

Here's the link: ir.abivax.com/static-files/e…

30

32

272

68,054

Jun 12

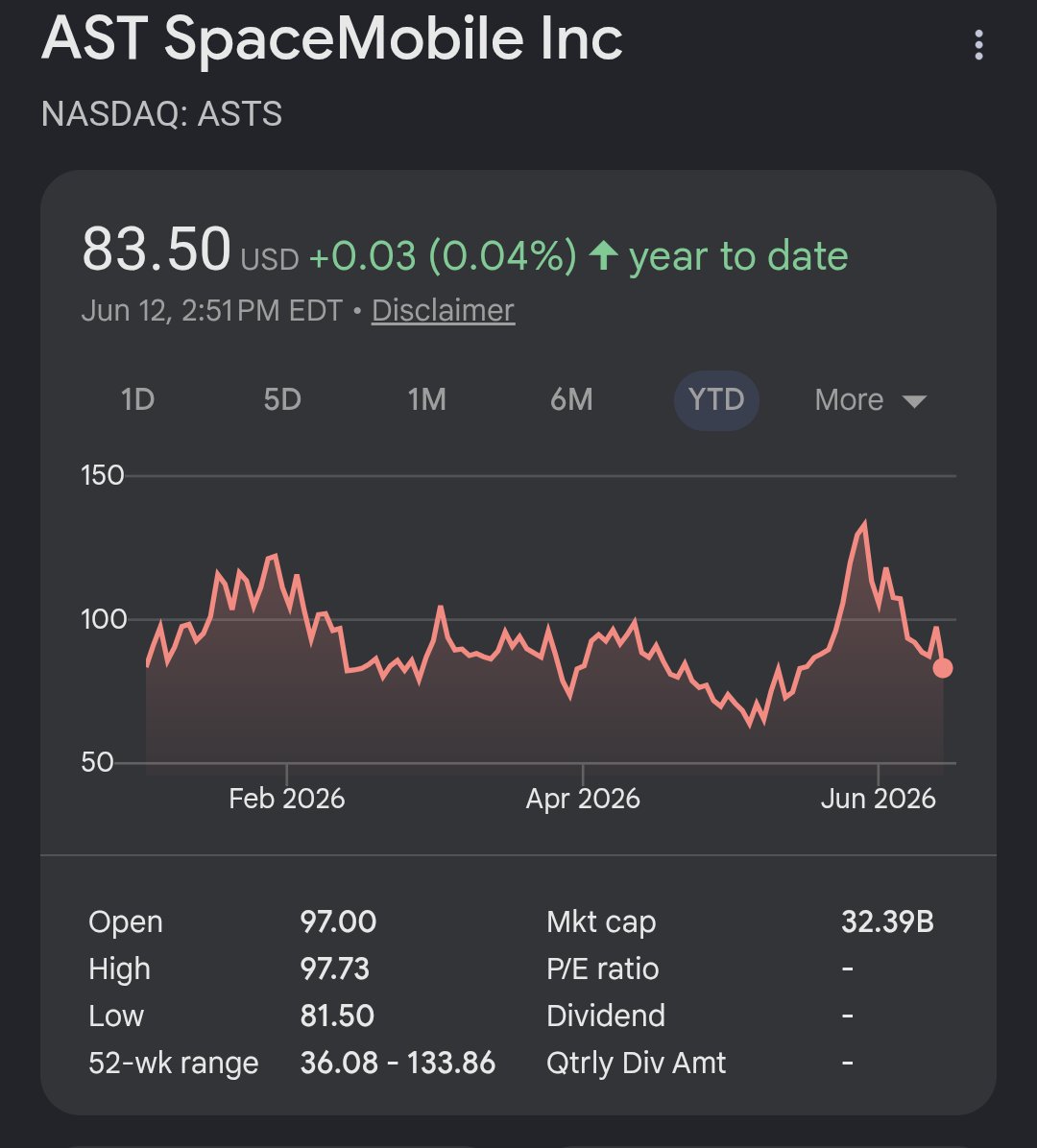

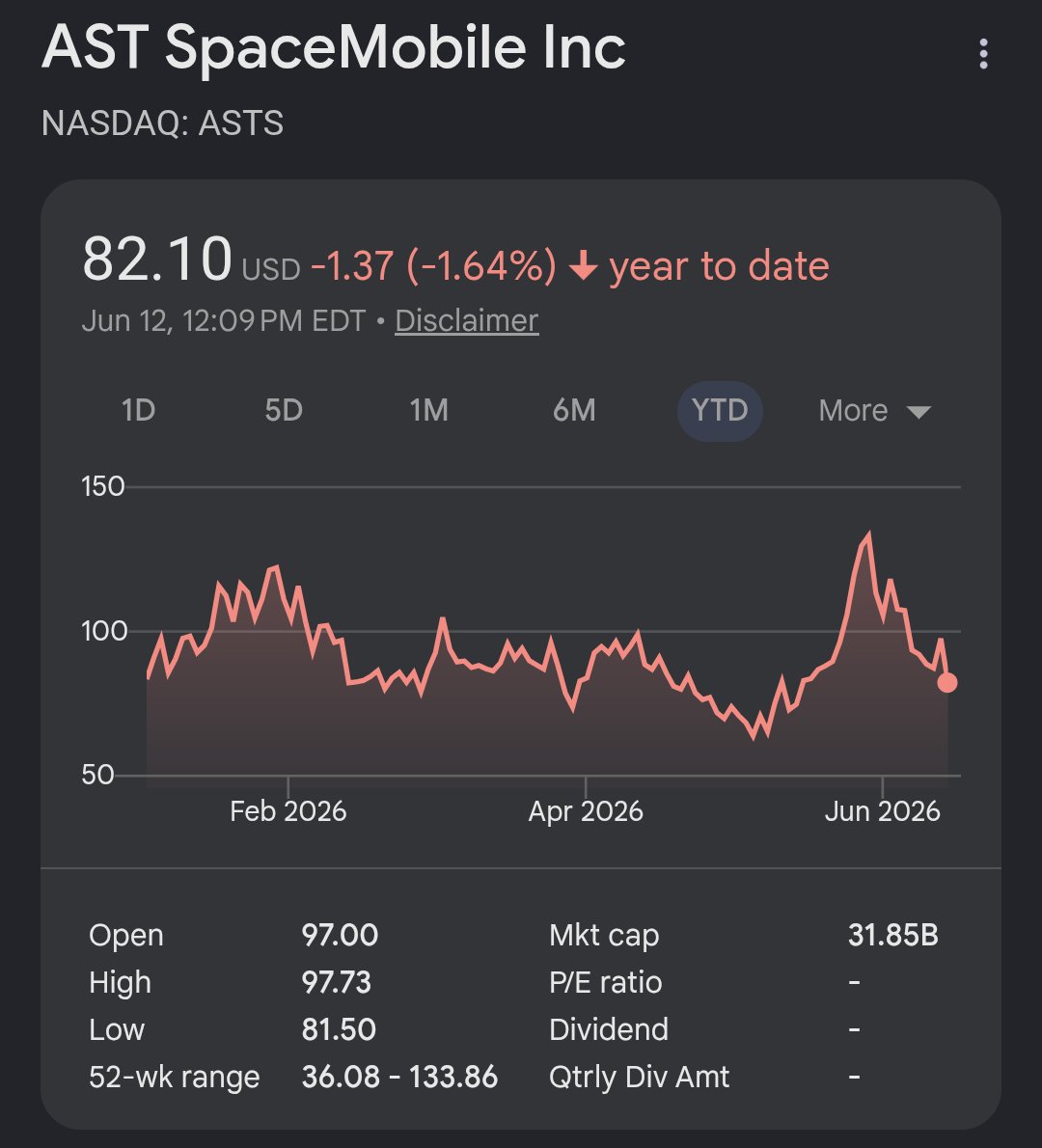

Raised a little dry powder to deploy next week if we sell more. Did add some $ASTS shares and calls (perhaps foolishly on the latter).

2

467