🏗️🏭🚛

Joined December 2015

- Tweets 3,091

- Following 575

- Followers 2,435

- Likes 6,315

503 Photos and videos

Pinned Tweet

8 Nov 2023

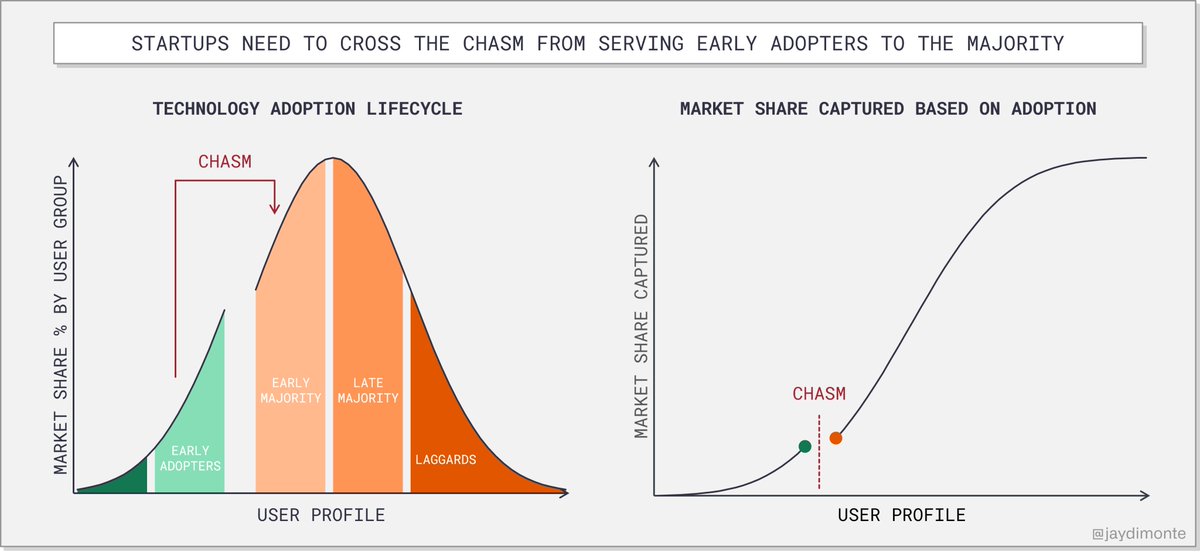

We all know about "crossing the chasm" when it comes to starting with early adopters and moving on to the majority

A necessary action for any startup pursuing scale

But, this framework isn't helpful for industrial startups...

3

1

14

1,914

Jackie DiMonte retweeted

Apr 19

A parasite that has been eating people for 3,500 years is about to be wiped off the planet. It infected 3.5 million people in 1986. Last year, it infected 10. And I have not seen it make a single front page.

It is called Guinea worm. You drink contaminated water from a pond in a poor village. A year later, a worm up to three feet long starts coming out of your leg through a burning blister. There is no pill that stops it and no surgery that works. You wrap the worm around a stick and pull it out slowly, over days or weeks, inch by inch. If you rush, the worm breaks inside you and causes a fresh infection.

Guinea worm is ancient. Preserved worms have been pulled out of Egyptian mummies from around 1000 BCE. The Ebers Papyrus, an Egyptian medical scroll from 1550 BCE, describes pulling the worm out with a stick. For three and a half thousand years, that was the best humans could do.

Then in 1986, public health workers decided to kill the parasite off. They had no vaccine and no drug. What they had was cheap cloth water filters and a small army of volunteers willing to walk from village to village for decades.

The plan was simple. Give everyone who drinks from a pond a cloth filter to strain out the tiny water fleas that spread the parasite. Then send volunteers walking house to house, year after year, teaching people how to use the filters and keeping anyone with an emerging worm out of the water.

It worked. From 3.5 million cases a year to 10. Four were in Chad, four in Ethiopia, two in South Sudan. The other four countries where the worm used to be common, Angola, Cameroon, the Central African Republic, and Mali, had zero human cases for the second year in a row. The World Health Organization has already certified 200 countries as Guinea worm free. Six are left.

The last hurdle is dogs. Cameroon had 445 infected animals last year and Chad had 147, so a lot of the remaining work is on animals, not humans. Strays get leashed, and crews treat ponds to kill any remaining worms. The campaign keeps watching until the number hits zero.

When Guinea worm hits zero, it becomes the second human disease ever erased from the planet. The first was smallpox. It will also be the first parasite humans have ever wiped out, and the first disease ever ended without a single dose of medicine. Volunteers walked village to village with cloth filters for 40 years. Now a plague from the age of the pharaohs is about to be gone.

Apr 17

Give me the kind of good news from around the world that nobody ever talks about... but should.

730

20,536

128,624

7,913,031

Jackie DiMonte retweeted

Apr 6

In hardtech, engineering innovation is what gets you started but supply chain is how you win.

9

24

195

77,959

Jackie DiMonte retweeted

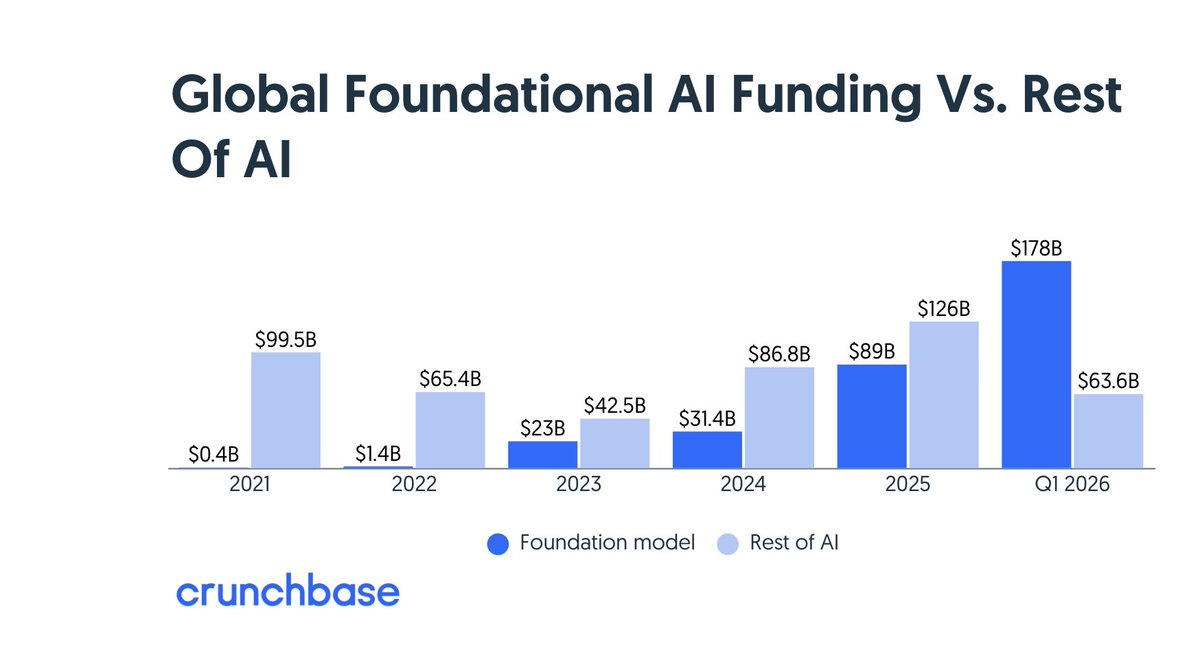

NEW: As of March 31, foundational AI startups had raised $178B across 24 deals, compared with $88.9B across 66 deals in all of 2025, a 100% increase, per @Crunchbase data. That’s also significantly higher — 466.9% higher to be exact — than the $31.4B raised across 52 deals in 2024.

By contrast, funding to foundational AI companies totaled just $23.2B in 2023 (a fraction of the size of OpenAI’s latest round) and a mere $1.4B in 2022

Read more in the @CrunchbaseNews article in the comments

2

4

5

647

Mar 31

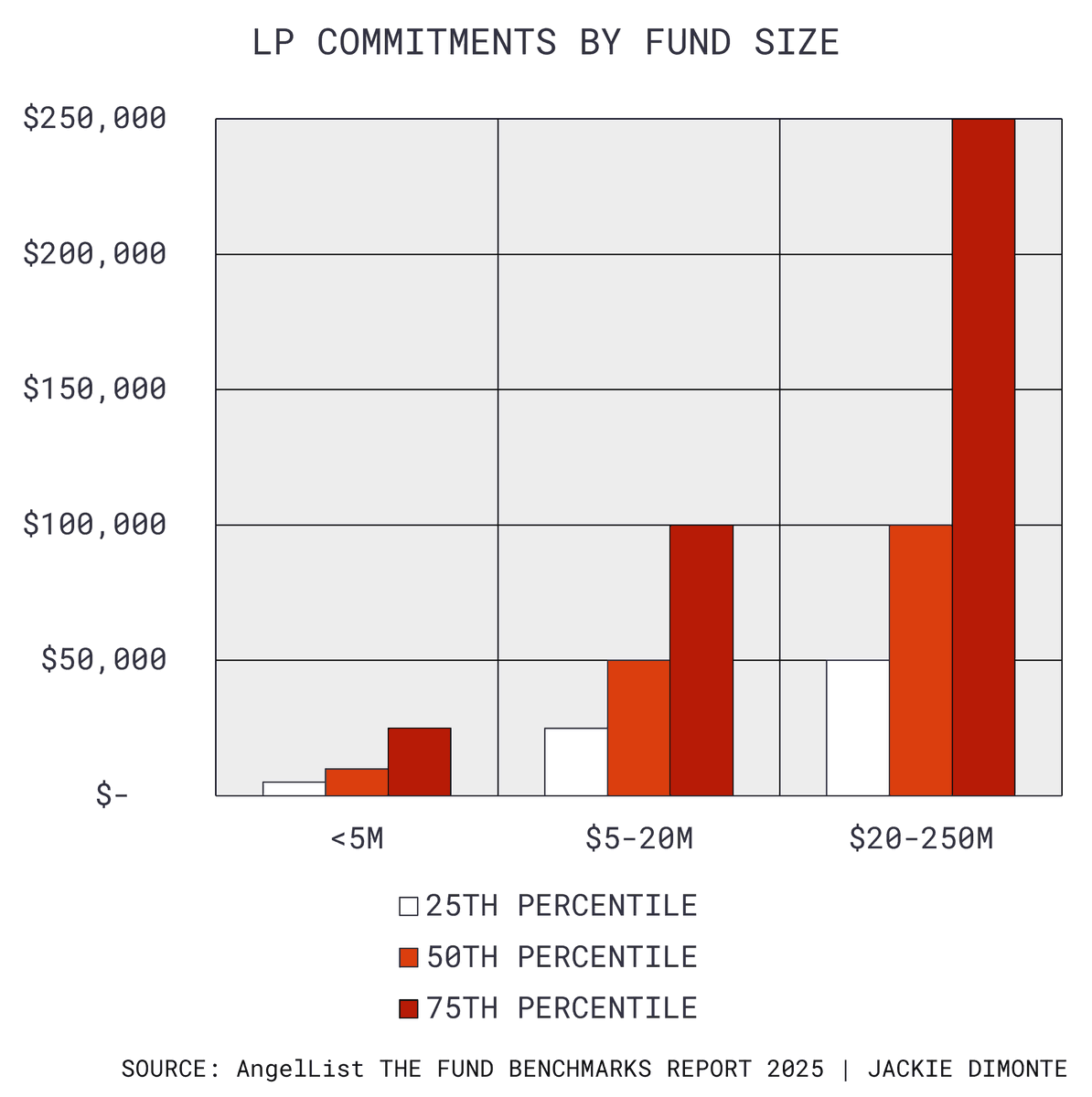

Angels make the world go round.

😇 Per AngelList, the median commitment size for a...

<$5M fund is $10K.

$5–20M fund: $50K.

$20–250M fund: $100K.

Fund commitments at these check sizes are overwhelmingly coming from HNW individuals… and likely a lot of overlap with folks that are (or would be) angel investors.

This shows up in the data: 50% of dollars going to <$20M funds come from individuals (vs. family offices and institutions).

But that participation is slowing, and that’s meaningful. I've written before about the decline of angel-led rounds in the last few years. The slowing of small fund fundraising might trace back to the same pullback.

All to say, just like angels in early companies, those first LPs into emerging funds are special. At Grid, a number of those folks backed us fast and early. Forever grateful for their partnership.

3

132

Mar 26

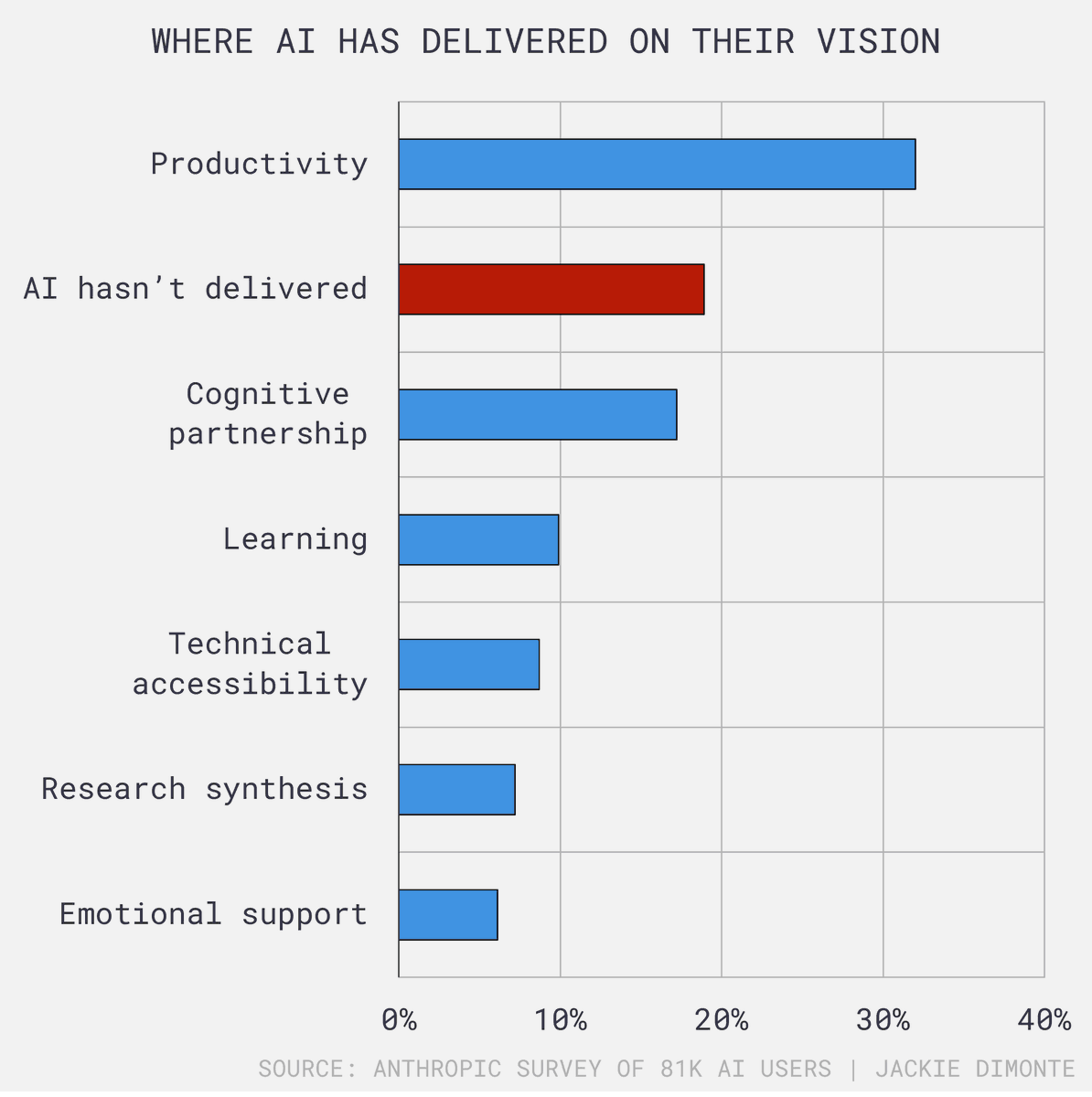

Is AI delivering real value?

The answer may surprise you.

Almost 20% of the 81K AI users Anthropic surveyed say AI has not delivered value to them.

That's more than people who say AI is a great thinking partner (17%), helps them learn new things (10%), or synthesizes research (7%).

The one exception is productivity, with 30% of users seeing gains.

For me, the biggest takeaway is that we're still experimenting with what AI is, how to use it, and where to extract value. And as models get better and more capable, they restart the experimentation process entirely.

What features were not helpful a month ago are dramatically more useful today.

Will be interesting to see the next time they publish data. Will "no value" still be among the top rankings?

1

2

353

Mar 25

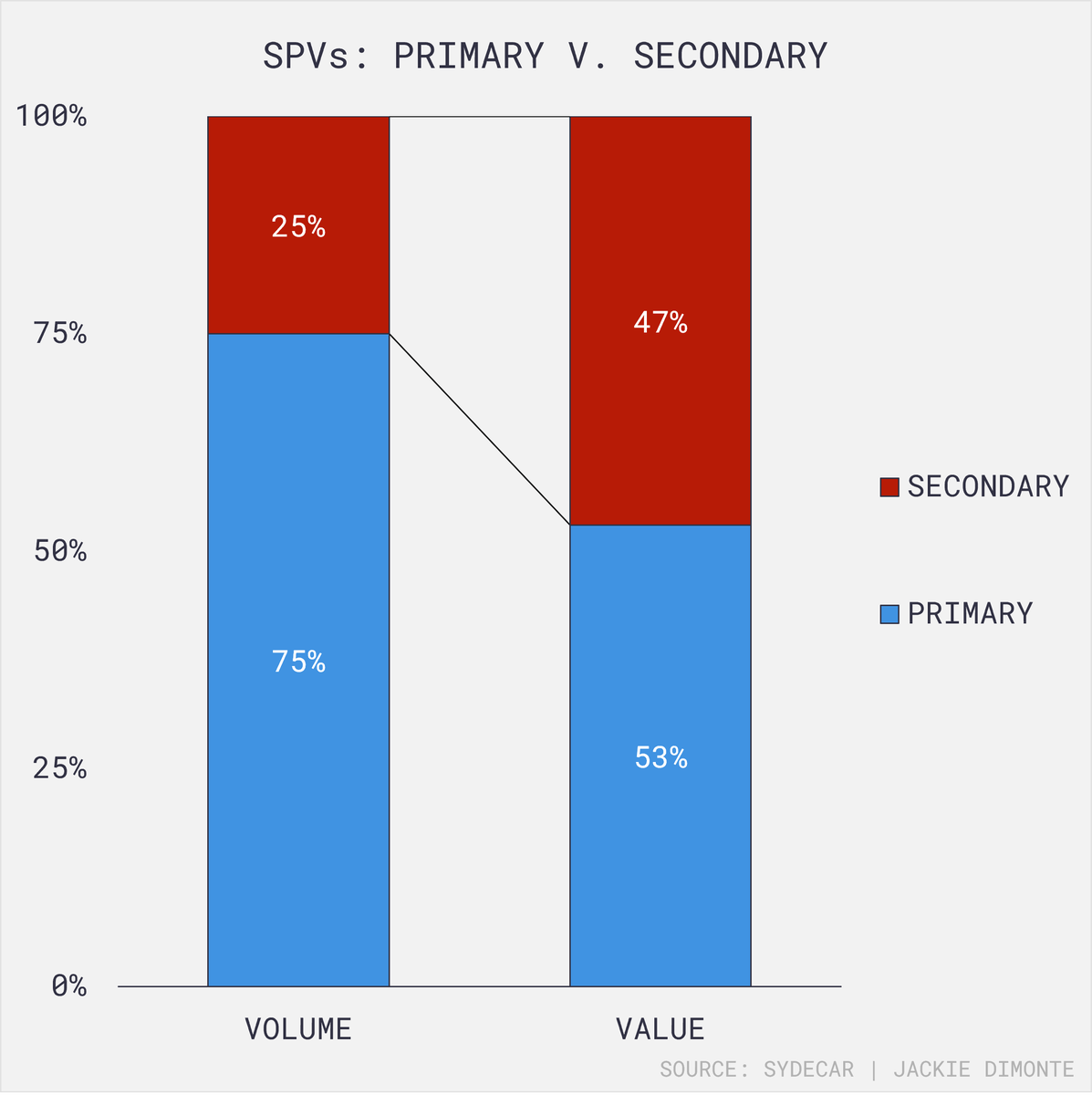

SPVs are booming. But where the money is going tells a different story than where the deals are.

Great data from Sydecar on SPV activity last year:

📈 SPV deal count 2x last year and capital invested 2.5x

But look at the split:

🔵 Primary SPVs account for 75% of deals but 54% of value

🔴 Secondary SPVs made up 25% of deals but 46% of value

In other words, secondary SPVs are fewer deals with much bigger checks:

🔵 Primary SPVs tend to be angel groups and smaller syndicates pooling capital into early rounds

🔴 Secondary SPVs are for accessing proven (hot?) opportunities

As the exit slump continues, my guess is secondary SPVs are becoming one of the primary tools for getting capital in (and out) of late-stage positions. Expect 2026 to be more of the same.

3

140

Mar 24

We’re in the early innings of AI, and no one really knows what comes next.

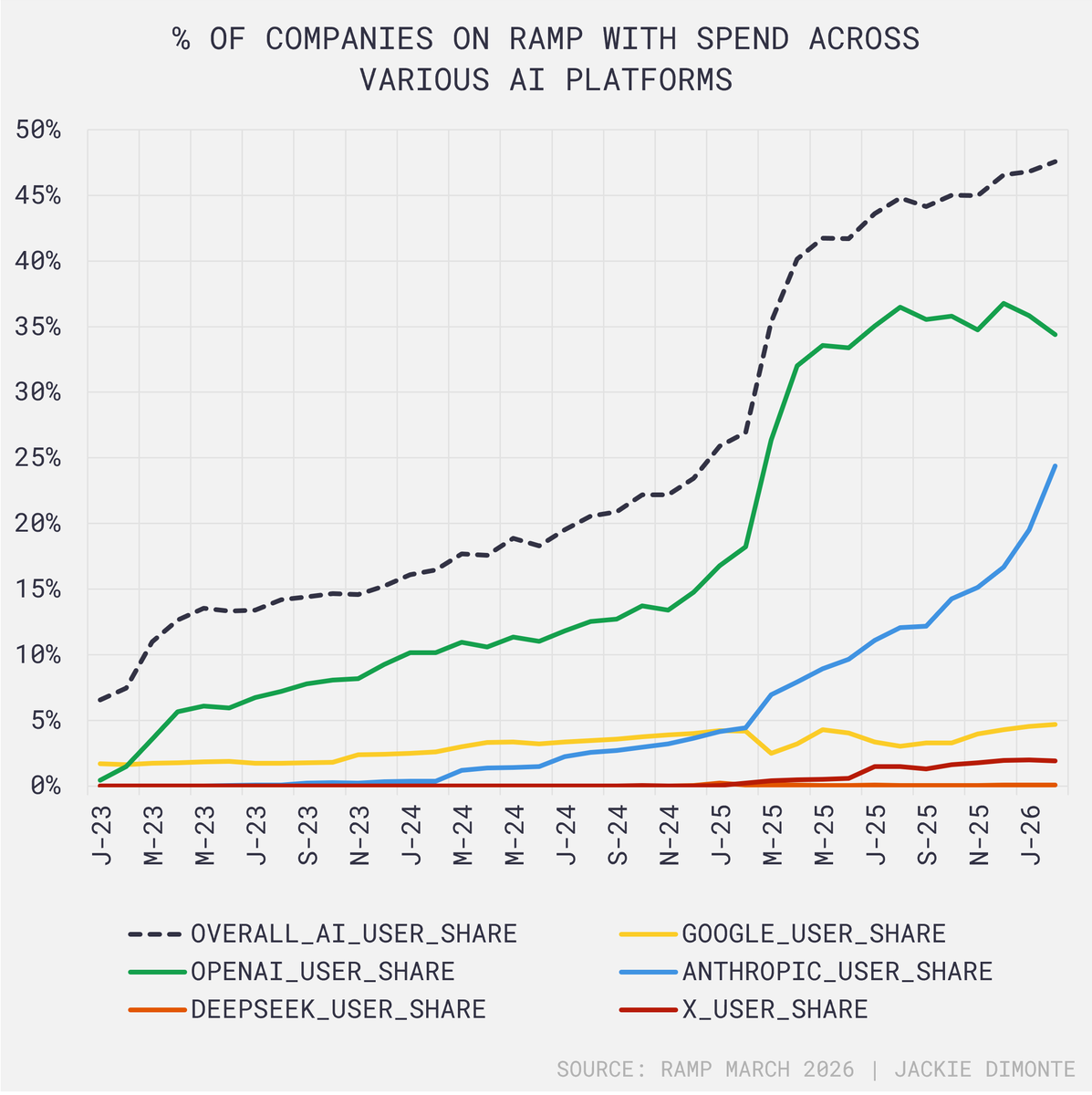

Ramp published data on the percentage of their customers purchasing AI tools, and it's wild. Some notes:

Almost 50% of businesses are paying for AI, up from 5% roughly three years ago.

Increased adoption of 🟢 OpenAI and 🔵 Claude is fueling most of the growth. The former was quick out of the gate, the latter is accelerating fast. 🟡 Google, despite a built-in distribution advantage, hasn't seen meaningful incremental spend.

What's different this last year is that businesses are spending on 🟢 🔵 🟡 MULTIPLE platforms.

Early last year was the first time we saw meaningful overlap. Now, nearly 20% of volume comes from companies paying for more than one provider.

We've framed this market as a battle of the models, perhaps so much so that there will be one "winner." In reality, there'svery little loyalty and data moats aren't creating lock-in.

But unlike prior startup battles (i.e. Uber vs. Lyft), competition is happening through product advancement, not price. LLMs are not commodities (yet?).

With a prize so big, platforms are sprinting at it. New capabilities on what feels like a daily basis. For now, the consumer is the winner.

Excited to see how the next 3 years play out.

1

3

349

Feb 18

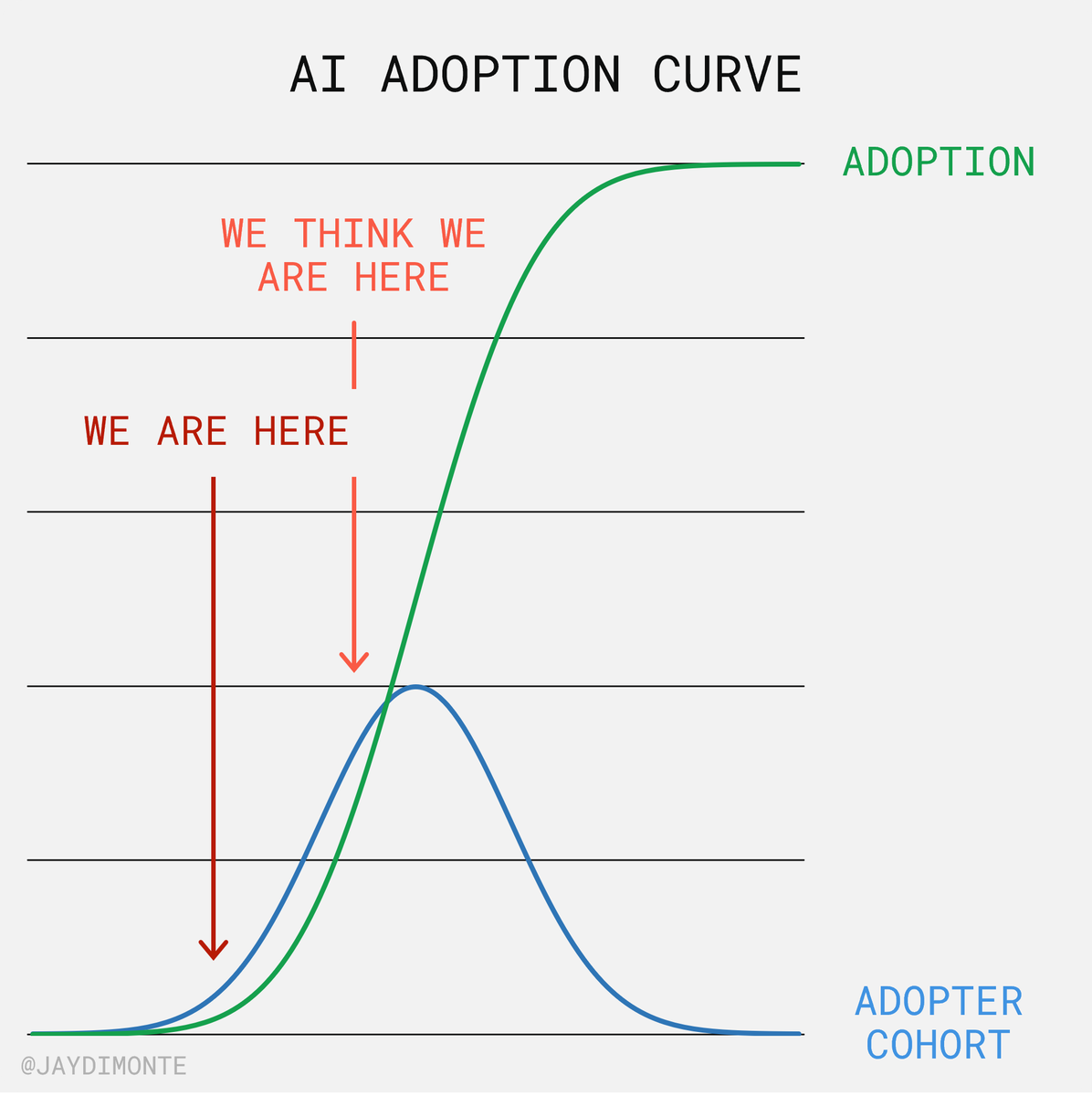

📊 45% of workers say they “use AI.”

The real number is so much lower than that.

Most people aren’t using AI the way people in tech mean it 𝘵𝘰𝘥𝘢𝘺. They’re using LLMs to edit emails, summarize documents, or replace search.

Meanwhile, the pace of change is so fast that “using AI” isn’t a one-time adoption event. It requires constant learning, unlearning, and tinkering.

Every new wave of AI capability resets the adoption curve. So, where we think we’ve hit the majority, it’s still the early adopters leading the charge.

I’m seeing two opposing forces at work:

📉 Some people fall off the learning curve completely, adopting one use case and getting stuck there.

📈 Each advancement makes the most powerful features easier to access, pulling new users in.

A lot of the anxiety about the future comes from confusing those two curves.

We may think we’re "late" but I think we’re just getting started.

Think of... what's the best thing you can do with AI now that you couldn't three months ago?

3

175

Feb 17

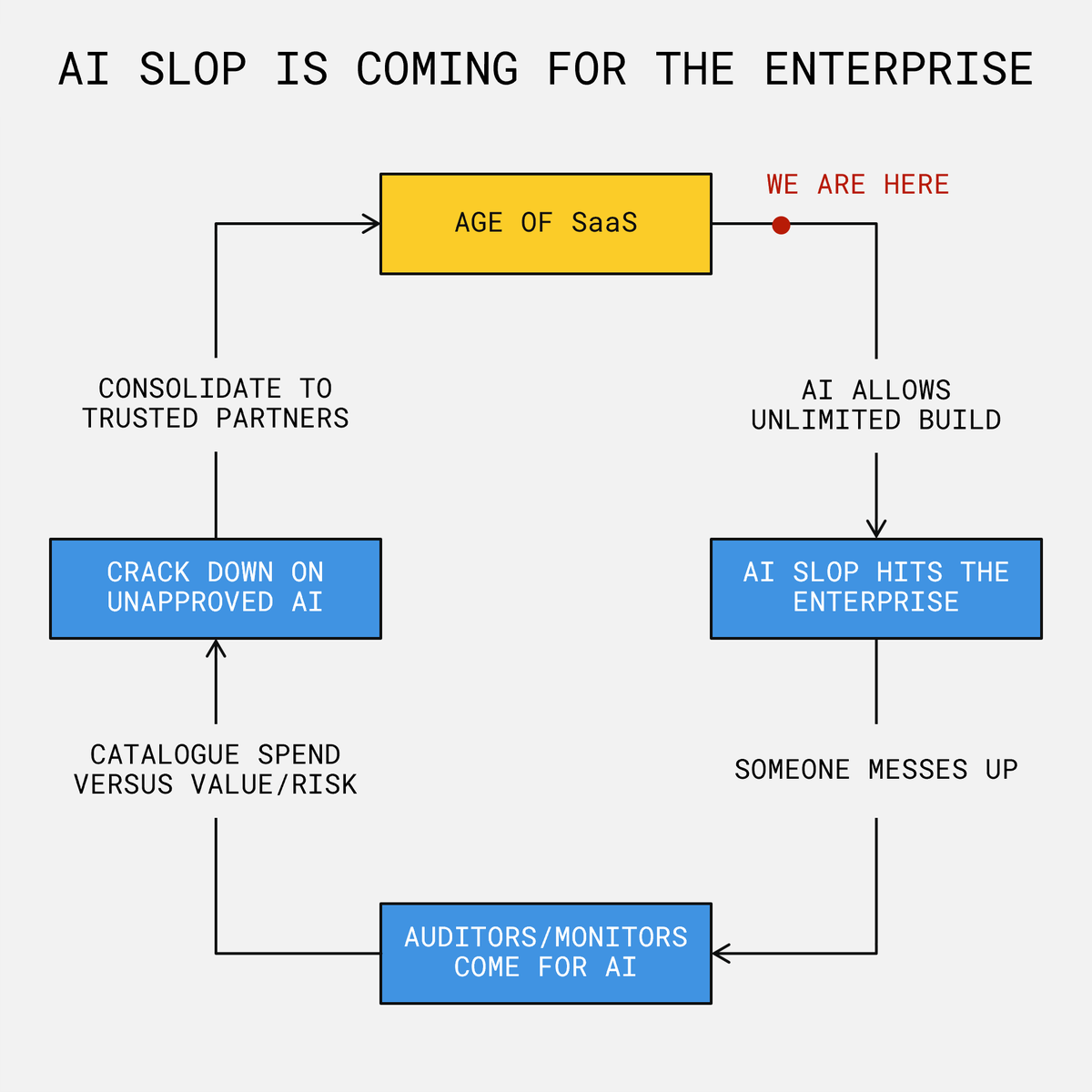

AI slop is coming for the enterprise.

Today, the 𝘱𝘦𝘰𝘱𝘭𝘦 𝘣𝘶𝘪𝘭𝘥𝘪𝘯𝘨 𝘵𝘩𝘦 𝘮𝘰𝘴𝘵 𝘸𝘪𝘵𝘩 𝘈𝘐 are early adopters. The 𝘤𝘰𝘮𝘱𝘢𝘯𝘪𝘦𝘴 𝘸𝘪𝘵𝘩 𝘵𝘩𝘦 𝘮𝘰𝘴𝘵 𝘱𝘦𝘰𝘱𝘭𝘦 building with AI are early-adopter companies.

That won't last.

As these tools improve, more people will use them across more companies. It won't just be the tech-natives. It'll be everyone.

🙅♀️ It'll be Pam from procurement who builds her own agent… that promptly rejects a PO from a new vendor for critical parts.

🙋♂️ It'll be Max from marketing who spins up a web app… that burns through $100K of compute when his branded meme generator goes viral overnight.

Now multiply that across every employee, every department. Think about how many mistakes we've already seen very capable people make with the release of clawdbot. Then scale that to the rest of the enterprise.

We're not yet in the age of "everyone builds." But when we get there, the real question won't be how. It'll be for how long.

Then it's back to permissioning, security, and… SaaS again.

It's one of the reasons behind why Grid is focused on net new operating systems and outsourced services [🔗substack.com/@jaydimonte/p-1…]. Everything in between feels somewhat cyclical at the enterprise.

5

9

324

Jan 14

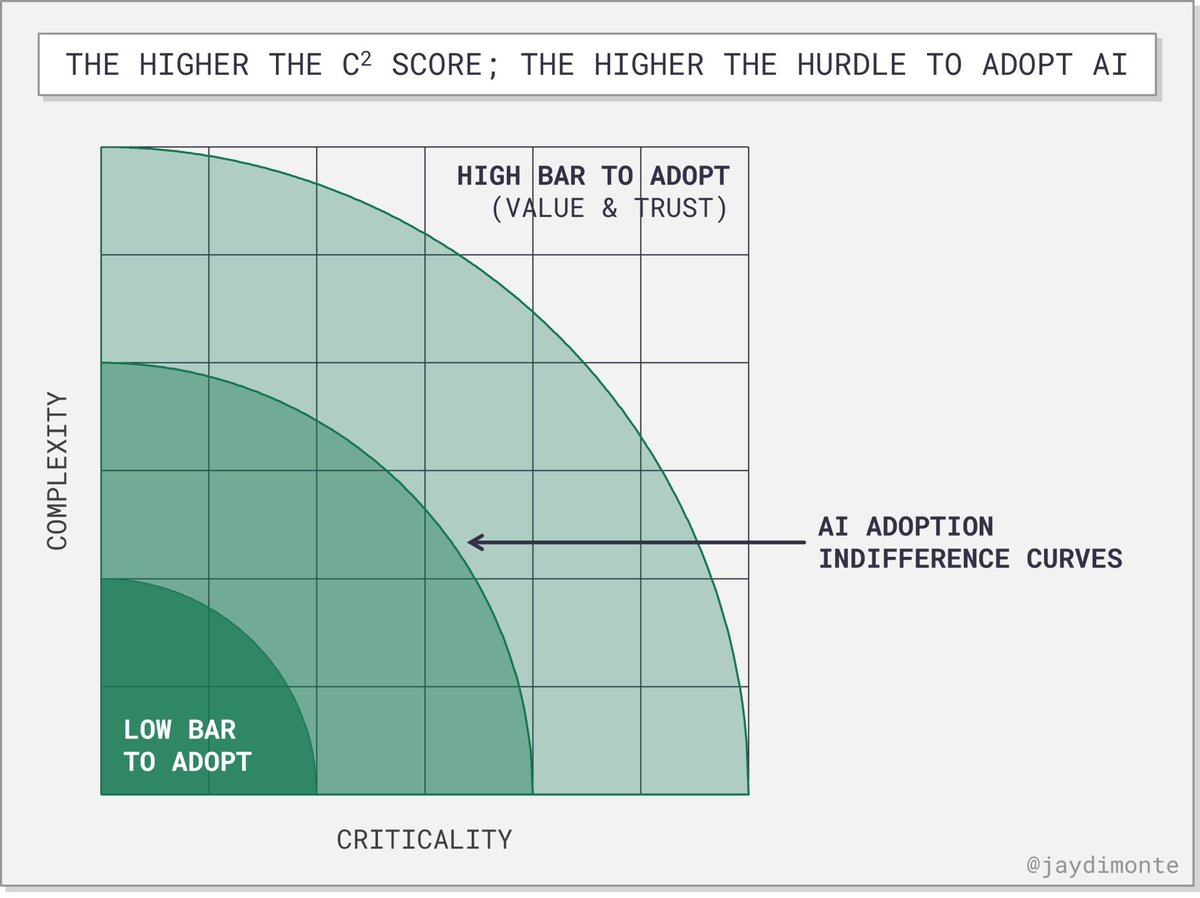

Building trust with customers is the #1 skill for vertical AI founders today.

Especially in markets like manufacturing, healthcare, and construction where tolerance for error is near zero. Once a tool is in production, it has to work... and keep working.

At Grid, we spend a lot of time thinking about what makes AI hard to adopt in these sectors.

It usually comes down to two things:

1️⃣ Complexity — How hard is the organization, workflow, or task to model?

2️⃣ Criticality — How painful are the consequences if it fails?

The higher the C² score (complexity × criticality) the harder it is to drive adoption.

That’s why we’re focused on companies solving both the 𝘁𝗲𝗰𝗵𝗻𝗶𝗰𝗮𝗹 and 𝗰𝘂𝗹𝘁𝘂𝗿𝗮𝗹 side of the curve.

The ones who know: if you want to transform high-C² sectors, you have to earn your place in the hands of the operator first.

1

99

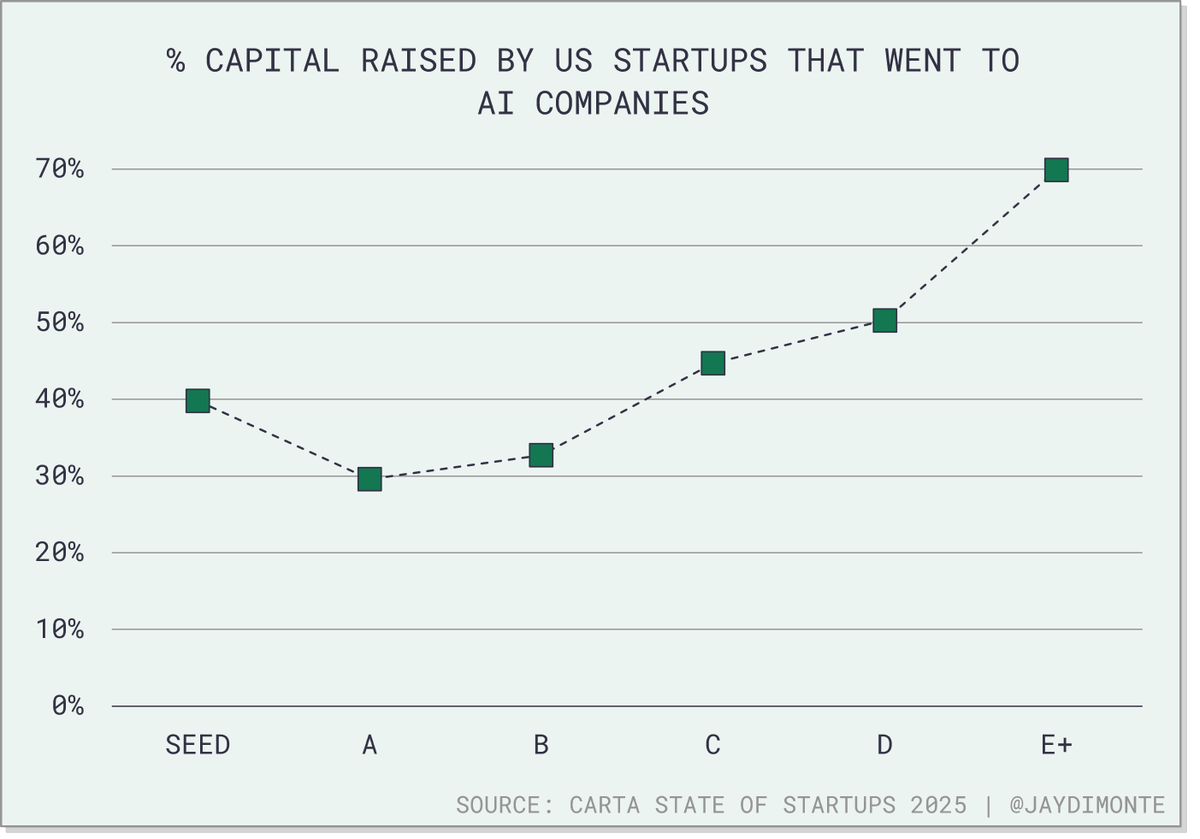

Jan 12

Everyone says we’re early in AI.

But capital flows suggest otherwise.

New data from Carta shows a clear trend:

The share of capital raised by AI startups increases sharply with stage, from 30% 𝘢𝘵 𝘚𝘦𝘳𝘪𝘦𝘴 𝘈 𝘵𝘰 70% 𝘢𝘵 𝘚𝘦𝘳𝘪𝘦𝘴 𝘌 .

That challenges the idea that AI is still exploratory. Instead, it suggests:

1️⃣ 𝗔𝗜 𝗶𝘀 𝗺𝗼𝗿𝗲 𝗰𝗮𝗽𝗶𝘁𝗮𝗹-𝗶𝗻𝘁𝗲𝗻𝘀𝗶𝘃𝗲.

It’s easy to start, but expensive to scale.

2️⃣ 𝗔𝗜 𝗺𝗮𝘆 𝗵𝗮𝘃𝗲 𝗽𝗲𝗮𝗸𝗲𝗱.

What’s happening today at Seed and A will be reflected at C in a few years.

3️⃣ 𝗧𝗵𝗲 𝗔𝗜 𝘄𝗶𝗻𝗻𝗲𝗿𝘀 𝗮𝗿𝗲 𝗿𝗲𝗮𝗹𝗹𝘆, 𝗿𝗲𝗮𝗹𝗹𝘆 𝘄𝗶𝗻𝗻𝗶𝗻𝗴.

Power laws are amplifying; mega funds are piling into perceived outliers.

Either way, I’m glad to be investing early.

Late-stage looks like a race for allocation in named winners.

1

4

130

14 Apr 2025

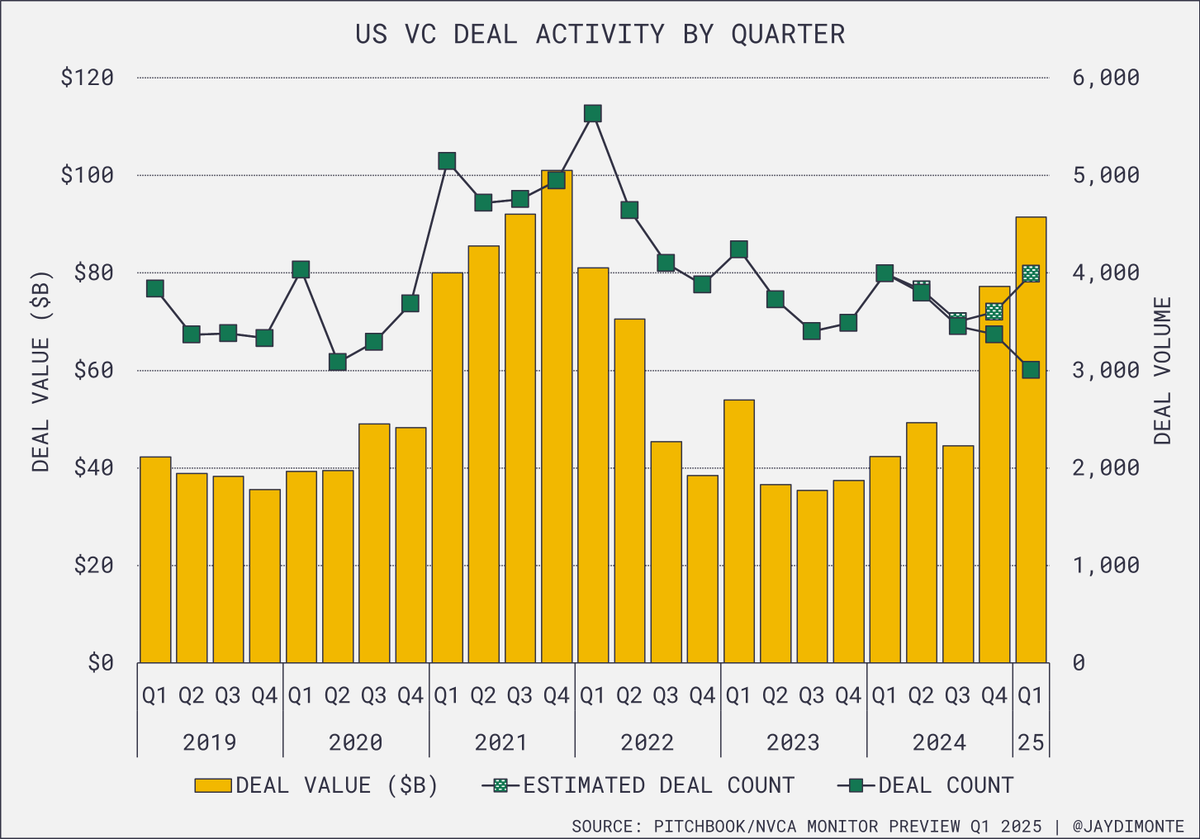

Q1 numbers are in... Are frothy markets back?

Deal value is back at 2021 peak levels.

Deal volume, meanwhile, remains consistent with historical norms—between 3,000 and 4,000 deals closed per quarter.

The driver isn’t surprising: AI now accounts for 70% of total deal value, but only 33% of volume.

A few thoughts:

🔵AI requires significantly more capital? The “one-person, billion-dollar company” is out of reach for foundational AI companies. It may still apply to those building with AI—but not those building the infrastructure itself.

🔵Similarly for obvious AI-applications (think agents for X), the abundance of teams changing the opportunity will lead to / has led to overfunding and a massive spend on customer acquisition.

🔵However, in certain markets that still lack modern “core systems,” the ROI story can be compelling and the customer acquisition differentiated, leading to efficient growth.

It’ll be worth watching if this continues throughout 2025. A dozen multistage funds raised massive pools capital in 2024, and they’ll need to deploy. Meanwhile, mega rounds in Q4 and Q1 are skewing the market.

The question now is whether liquidity will support continued reinvestment in venture capital—or if the pace slows.

1

2

6

1,101

10 Apr 2025

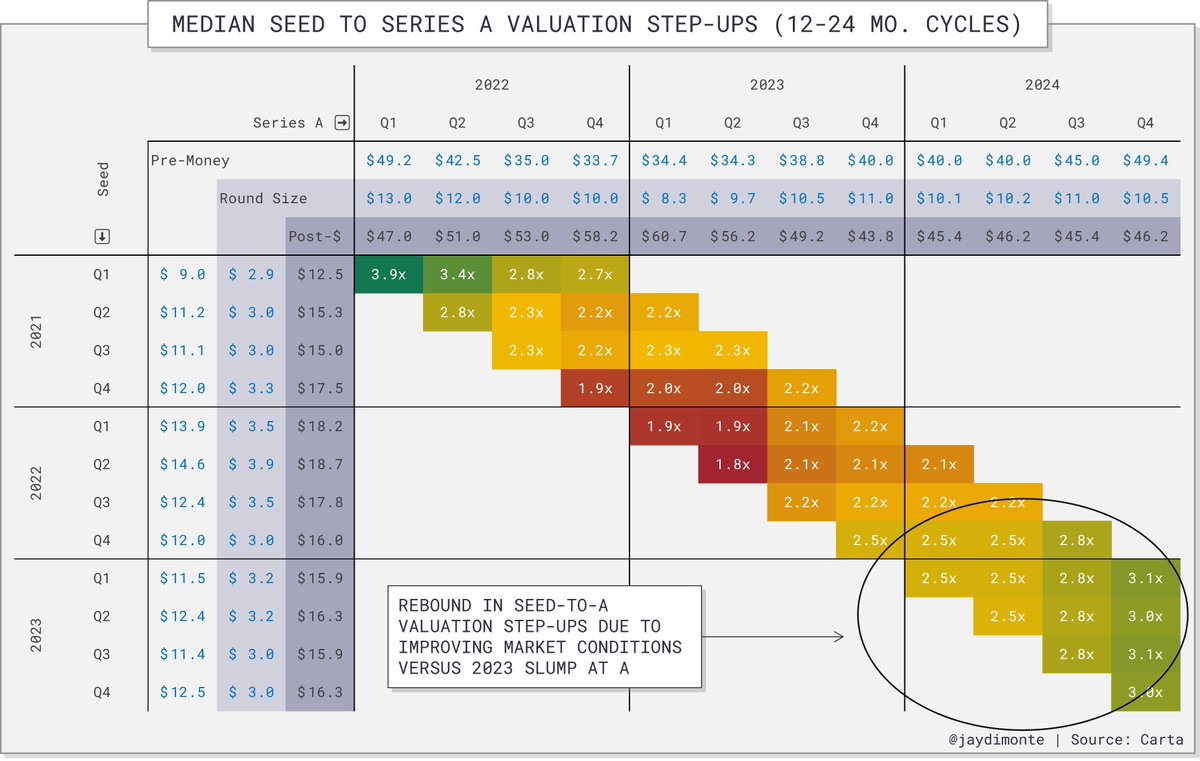

Conventional wisdom says you can’t time the market. But if you raised a Series A last year—you did. Will that hold in 2025?

Seed-to-A step-ups returned to the 2.5–3.0x range as median Series A pre-money valuations approached $50M. These are multiples we haven’t seen since—and valuations that now exceed—the 2021–22 peak.

(Step-up = seed post-money vs. Series A pre-money, 12–24 months later)

On the surface, it looks like a rebound. But zoom out, and it’s just more evidence of continued market volatility and shifts in the venture market.

📌 Inputs worth watching:

➡️ Time between rounds – Companies are raising later, meaning more mature companies at each stage

➡️ Graduation rates – higher step ups might be skewed by a flight to quality at A

➡️ Pricing equilibrium – With both seed and A climbing, are we in sync—or headed for another disconnect?

Seed valuations rose in 2023 too (not shown—those rounds haven’t hit A yet) so it's critical to see just how healthy the A market remains:

📉 If A valuations dip, we could see another reset like 2022–23.

📈 If A holds—or keeps rising, especially with AI strength—seed may inflate further as multi-stage firms move earlier and seed funds chase higher ceilings.

How do you see this playing out over the next 12 months?

1

1

3

272

8 Apr 2025

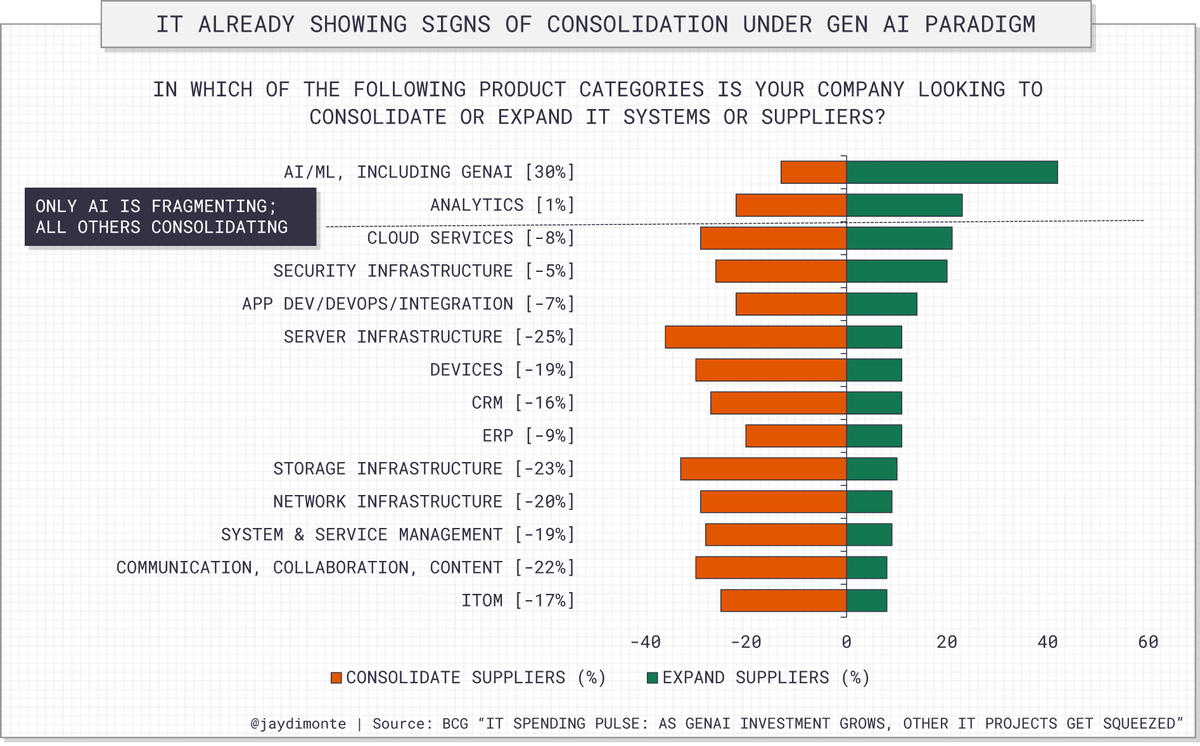

Enterprises are consolidating spend across nearly every IT category—except AI.

According to BCG, companies are reducing suppliers in infrastructure, cloud, CRM, ERP, and more.

But AI is the outlier. It’s the only category where supplier bases are expanding. This is a temporary trend. Orgs are still in discovery mode—testing tools, experimenting with platforms, and figuring out what processes make sense for them. As adoption matures, AI will absorb into enterprise software, and consolidation will follow.

I wrote I wrote last week about how this leads to a barbell market—core systems on one end, outsourced services on the other.

So the question is, if consolidation has already started: What platforms are in a position to absorb? Or be absorbed?

1

2

6

484

3 Apr 2025

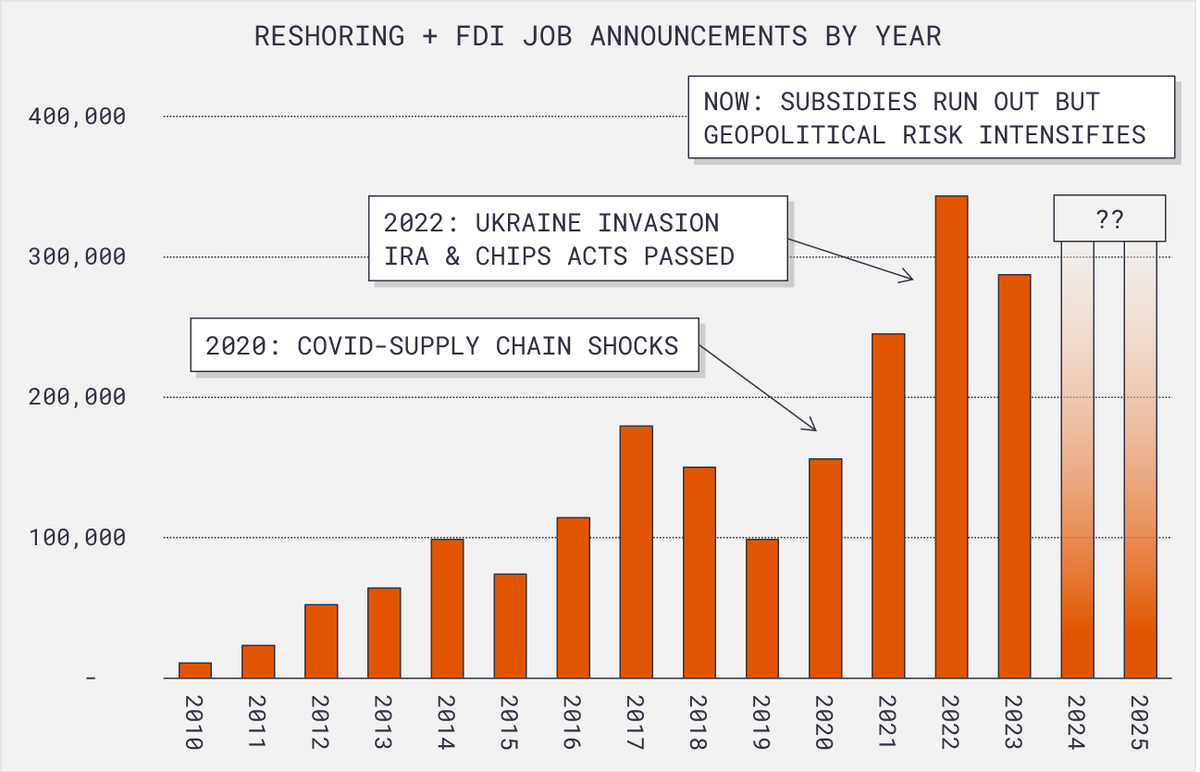

𝐓𝐨𝐝𝐚𝐲 𝐈 𝐰𝐚𝐬 𝐚𝐬𝐤𝐞𝐝 𝐡𝐨𝐰 𝐭𝐚𝐫𝐢𝐟𝐟𝐬 𝐰𝐢𝐥𝐥 𝐢𝐦𝐩𝐚𝐜𝐭 𝐀𝐦𝐞𝐫𝐢𝐜𝐚’𝐬 𝐫𝐞𝐢𝐧𝐝𝐮𝐬𝐭𝐫𝐢𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧.

In some ways, that question is a red herring.

Whether the latest tariffs are short-lived or enduring, they’re just one piece of a much larger picture: the ongoing reinvestment in America’s industrial base and workforce.

The chart below tracks reshoring and FDI job announcements in the U.S. You can clearly see the inflection points:

📈 2020: Supply chain shocks

📈 2022: Ukraine invasion, IRA & CHIPS Acts

🌐 Now: Subsidies begin to sunset, but geopolitical risk—and importantly tariffs—are on the rise.

We’ve gone from one administration’s carrot to another’s stick. But the fundamentals haven’t changed:

Skilled labor is constrained. Supply chains are still volatile. Building capacity and resilience remain critical.

Those are the kind of challenges I'm excited about solving.

1

2

200

2 Apr 2025

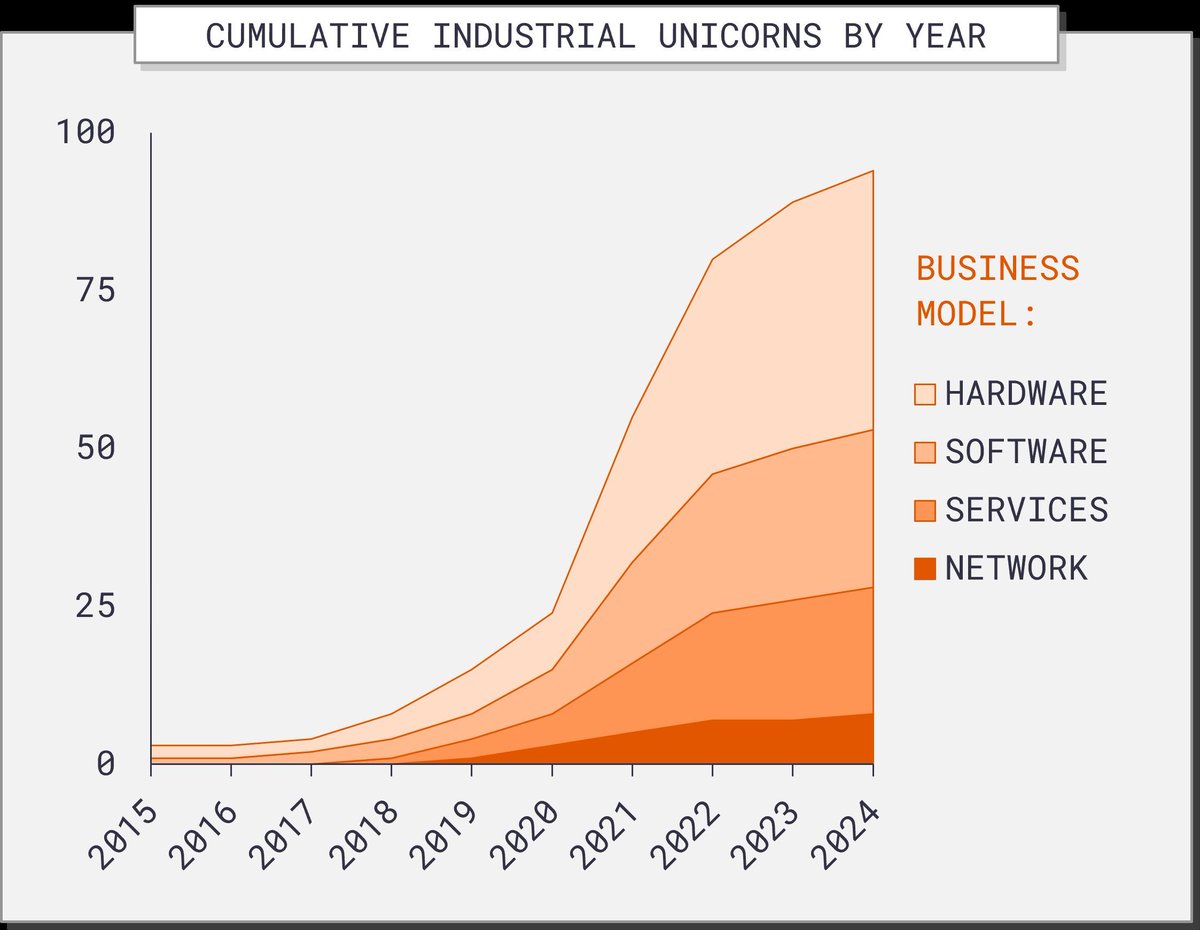

There’s a reason we’re excited about the rise of industrial unicorns—and it’s not about $$$.

Over the past decade, the number of venture-backed companies in manufacturing, construction, resources, and logistics has grown 10x.

That didn’t just bring capital—it built a talent base. Today, there are 30–100x more people who understand the expectations of high-growth technology and the realities of operating in industrial markets.

That’s the foundation founders need to build the next generation of industrial systems and AI-enabled services.

🏭 And it’s a big reason why we’re so energized at Grid—to back those building the new industrial era.

1

1

5

679

1 Apr 2025

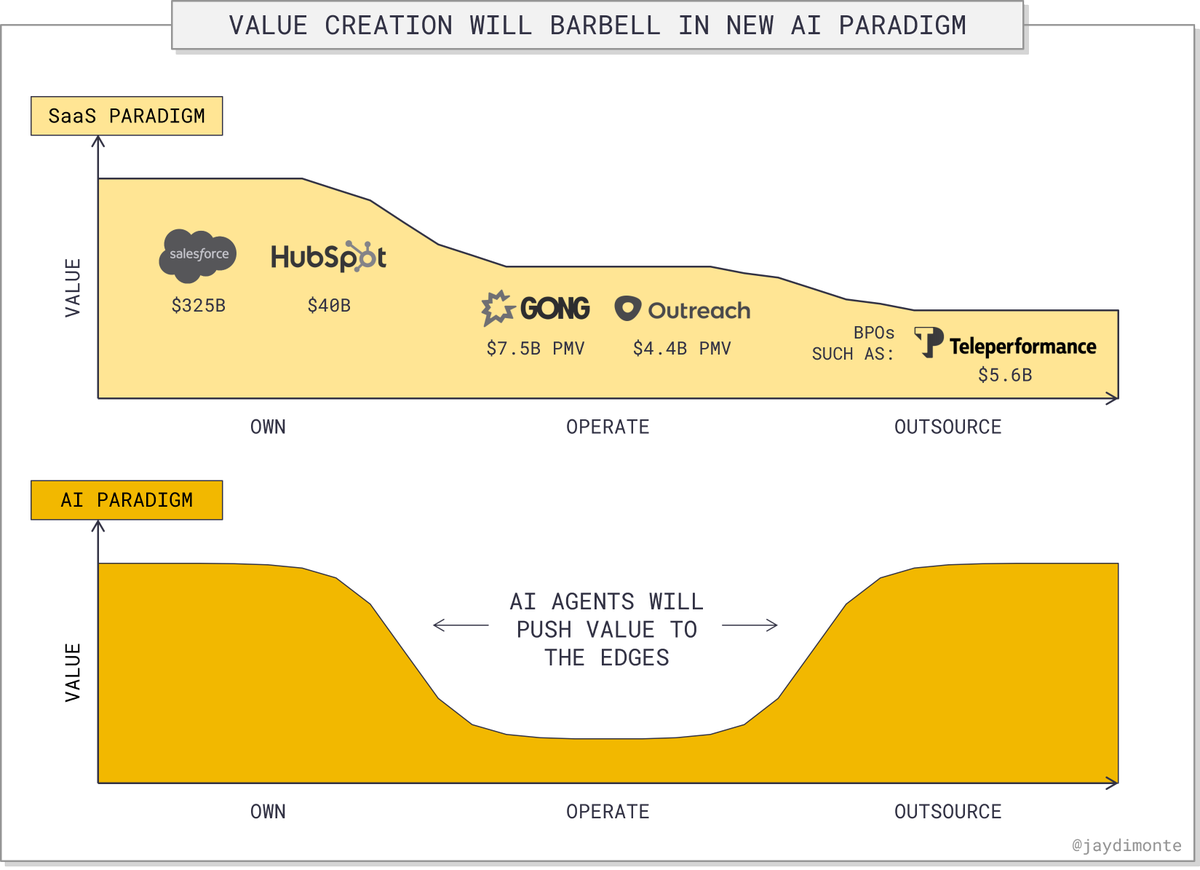

📈In the SaaS era, most value accrued to platforms that let users own their workflows.

The further you got from being a source of record, the less value you created. Services businesses lagged even further, constrained by margins and growth ability.

📈In the AI era? Value will barbell to the edges.

AI agents will automate large swaths of “operate” workflows—compressing the middle. That means more value flows to platforms (own) and services (outsource) with clear responsibility and better economics.

2

2

223