A tax barrister who tweets occasionally on tax-related matters. All tweets written in a personal capacity. Even in deserving cases no advice given via Twitter

Joined July 2009

- Tweets 5,403

- Following 30

- Followers 7,664

- Likes 2,708

582 Photos and videos

Pinned Tweet

1 Sep 2024

I have enjoyed not looking at X/Twitter for the past few weeks. I propose repeating the exercise indefinitely.

Please assume that I will NOT see your posts (even if I am tagged in).

18

7

33

4,505

5 Jul 2024

It does not seem that long ago that I expressed surprise that we had (I think) six living ex-PMs, possibly for the first time in history. In the next hour, that number will reach eight. For everyone's sake, please may that tally stay constant for a long time.

8

7

38

2,782

5 Jul 2024

But I have recovered my youth. The (still soon-to-be) Prime Minister is older than me.

1

1

4

1,853

27 Jun 2024

Just had a call from 02039057921 purporting to be from @virginmedia. I'm 99.9% sure it was a scam (and the caller would not wait 15 secs for me to be "ready to take his call" which undermined the alleged urgency of his call). Is there a way this activity can be blocked? #phishing

2

3

5

2,177

14 Jun 2024

Who has priority at a zebra crossing in this situation?

2

2

1,708

10 Jun 2024

I understand that the UT has issued a decision in the IR35 challenge against Adrian Chiles. I shall read the decision in the course of the day.

Plenty of time to digest it ahead of my talk on IR35 cases at the end of next week.

stepevents.org/event/a22f5c6…

gov.uk/tax-and-chancery-trib…

2

8

19

6,481

6 Jun 2024

Echoing the sentiments in this obit to the late Nuala Brice. She was an absolute delight to appear before - the epitome of judicial integrity. lawgazette.co.uk/obituary-dr…

2

7

1,234

17 May 2024

Congratulations to the many winners at last night's #TaxAwards2024. Good to see @BillDodwellTax @rbeccabeneworth @JeremyCokerJC on the podium with @VictoriaCoren (who won't remember me as it was almost 50 years when we last met!).

3

1

15

1,539

17 May 2024

Ditto to @petetaxmiller and @litrgnews - until I see the full list of winners at taxationawards.co.uk/website…, I realise I will keep missing out many worthy winners.

Of course, the LN staff deserve a day off.

1

5

870

2 May 2024

I think polling station staff need to be (re)trained on how to check voter ID.

My wife & I were checked as we entered the polling station. Fine.

At the desk, the clerk asked had we been checked as we entered and, when we said yes, that was considered sufficient.

1

2

8

1,659

2 May 2024

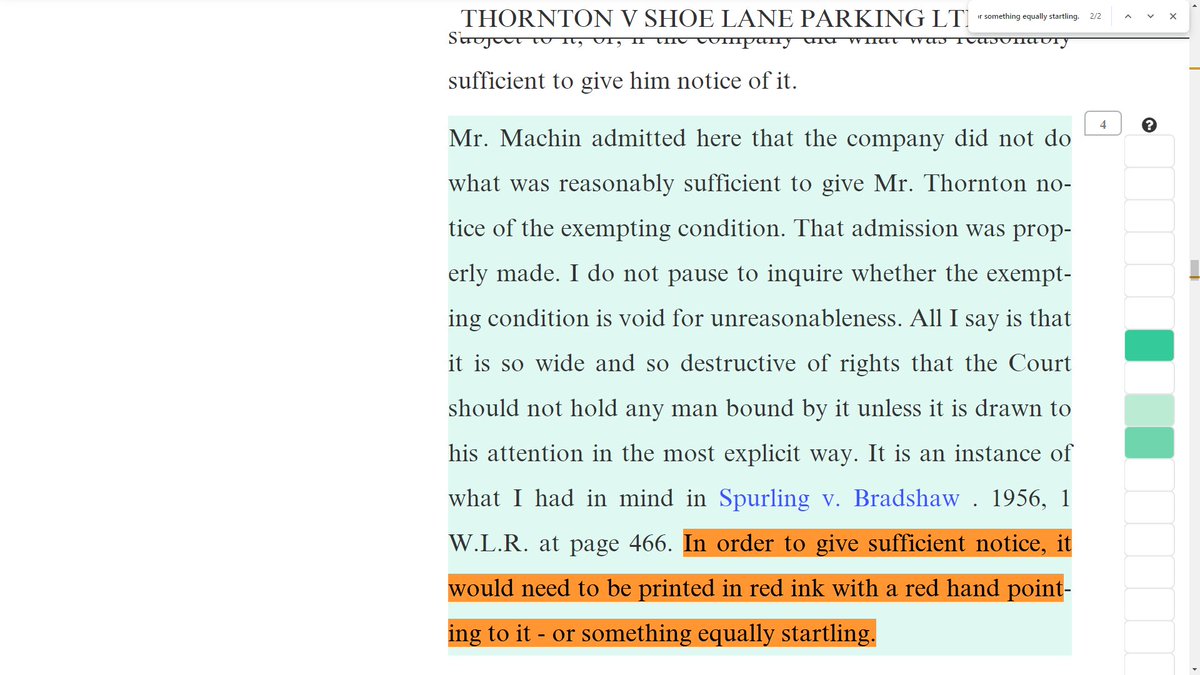

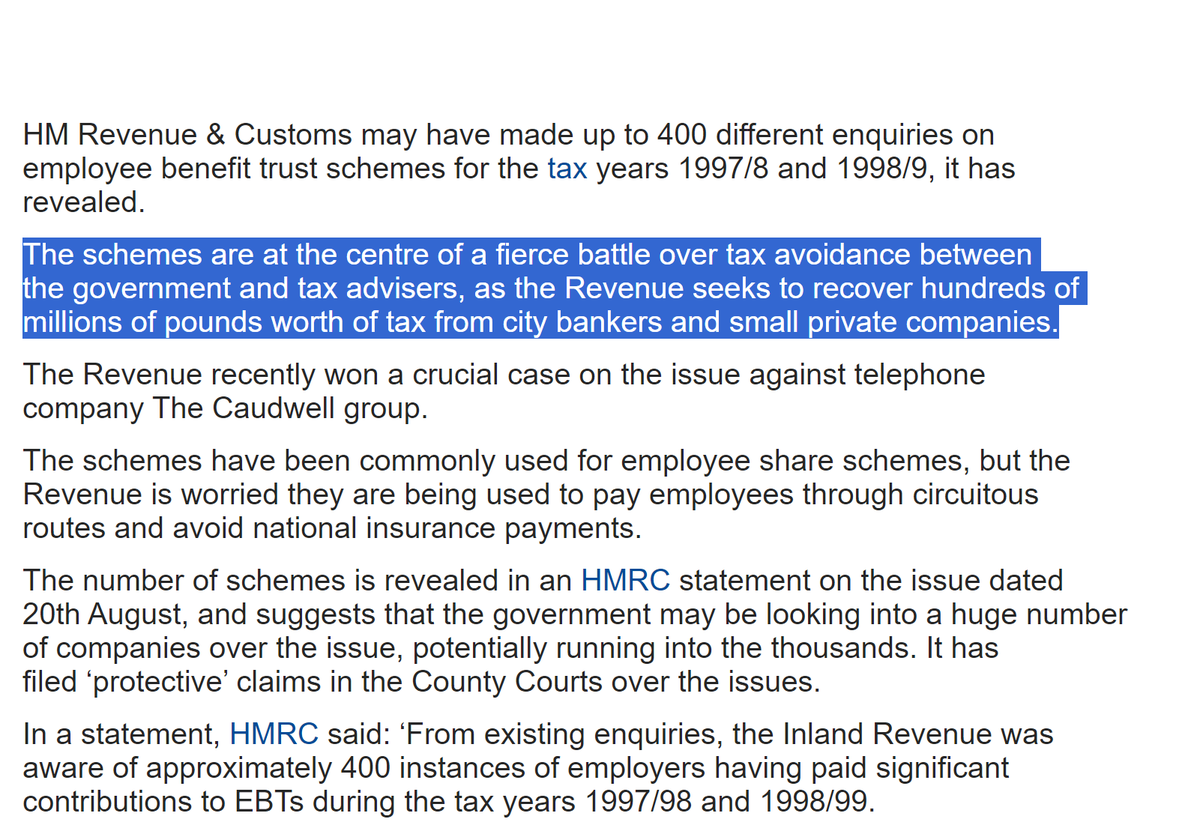

This article contains HMRC's statement that they "noted" the s684 power in their evidence provided to Lord Morse. I infer that this means a footnote rather than anything clear. Anyone who has studied Lord Denning's judgment in the Shoe Lane Car Park case will recognise the point.

2 May 2024

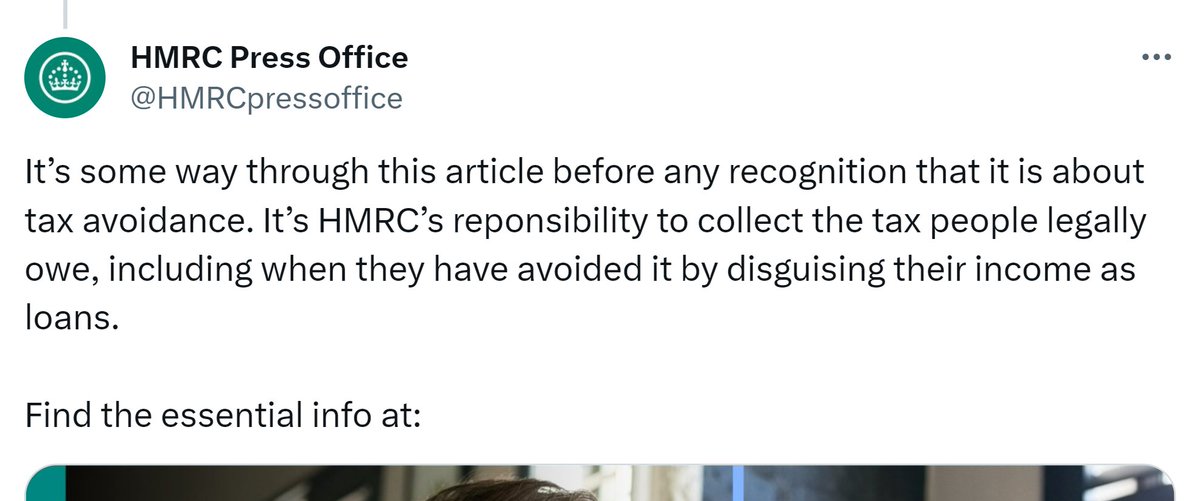

The latest element to #LoanChargeScandal, #s684 notices, highlighted in @MoneyTelegraph article. Thank you to @charlotte_giff and all featured.

x.com/MoneyTelegraph/status/…

4

67

97

5,736

18 Apr 2024

I have just learned of the death last week of one of my early mentors, Sir Stephen Oliver, the first President of the Tax Chamber of the First-tier Tribunal.

He will be much missed by the tax community and my condolences to his wife and wider family.

RIP

6

3

34

2,293

17 Apr 2024

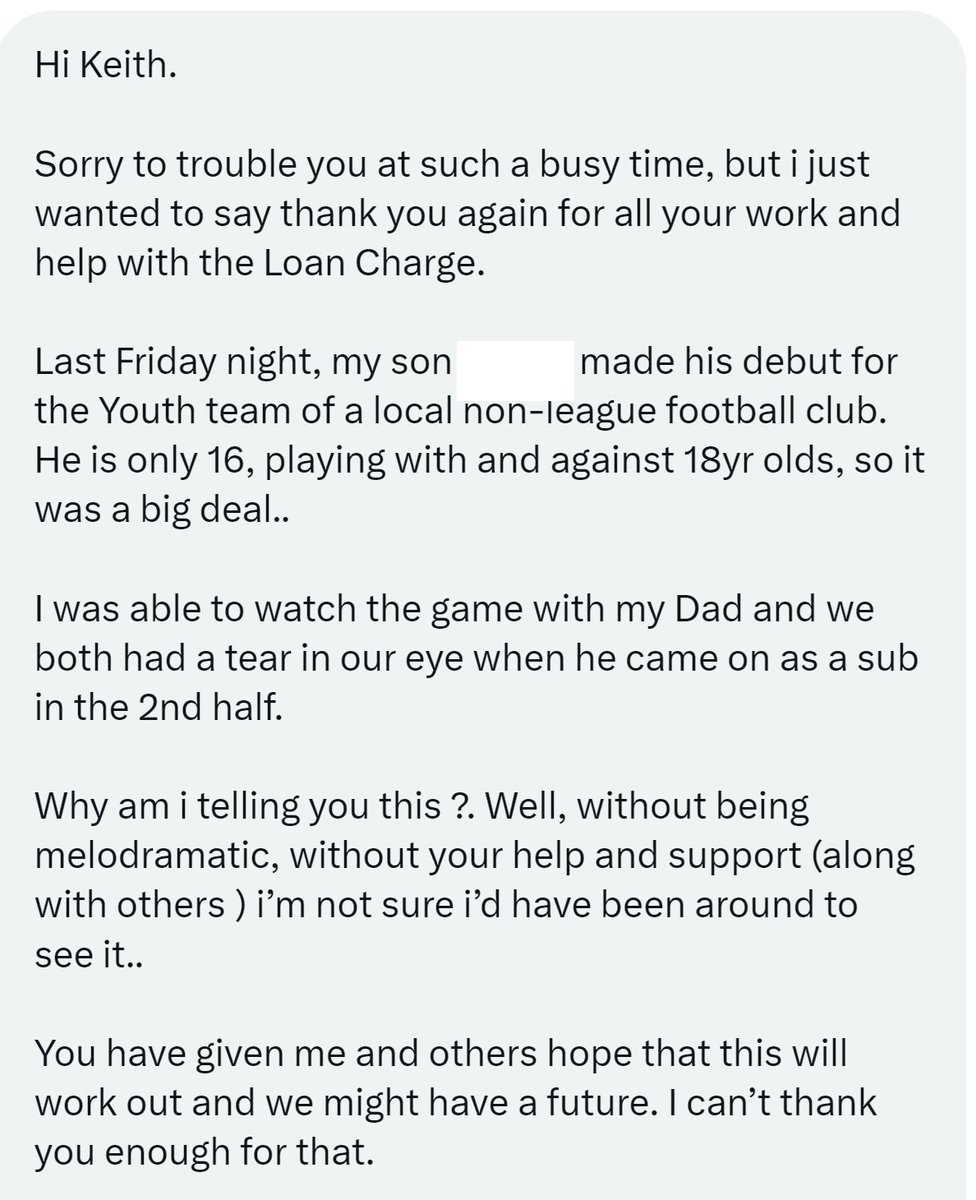

I have a limited update on the s684(7A)(b) letters which have been issued to catch the years taken out of the loan charge by the Morse review.

HMRC seem to have withdrawn some, effectively allowing the taxpayer to win his/her appeal without the case going to the Tribunal. 1/4

5

68

120

10,789

17 Apr 2024

Does it mean that HMRC agree Hoey was wrongly decided? Does it mean that there were certain factors in certain cases which made s684(7A)(b) inappropriate? Is it because these taxpayers (or their advisers) have identified a killer argument?

3/4

1

29

64

2,919

17 Apr 2024

I simply do not know the answers.

I certainly hope that HMRC will honour their pledge to treat taxpayers fairly and equally. If they now belatedly recognise the errors of their interpretation of s684(7A)(b) then they should make this clear and withdraw ALL such notices. 4/4

5

37

83

3,476

Keith M Gordon retweeted

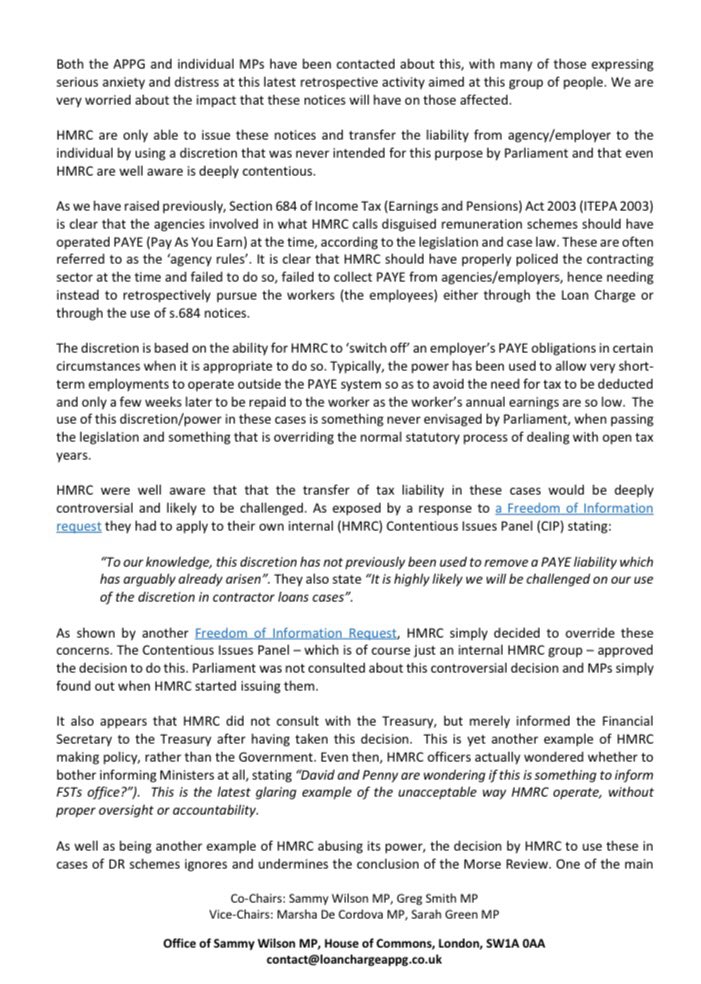

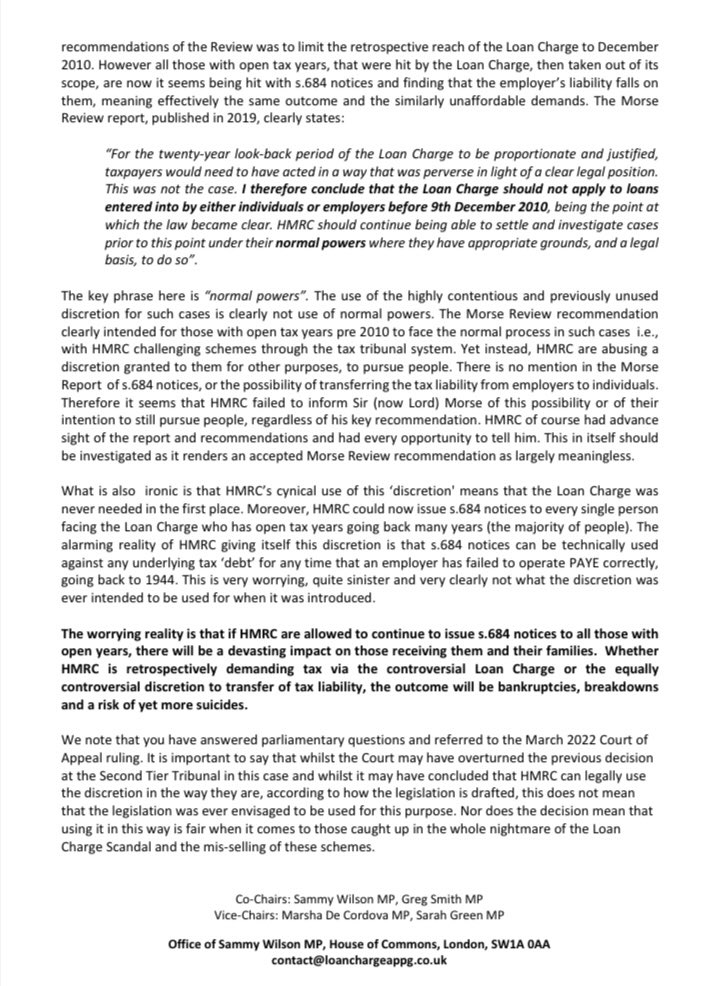

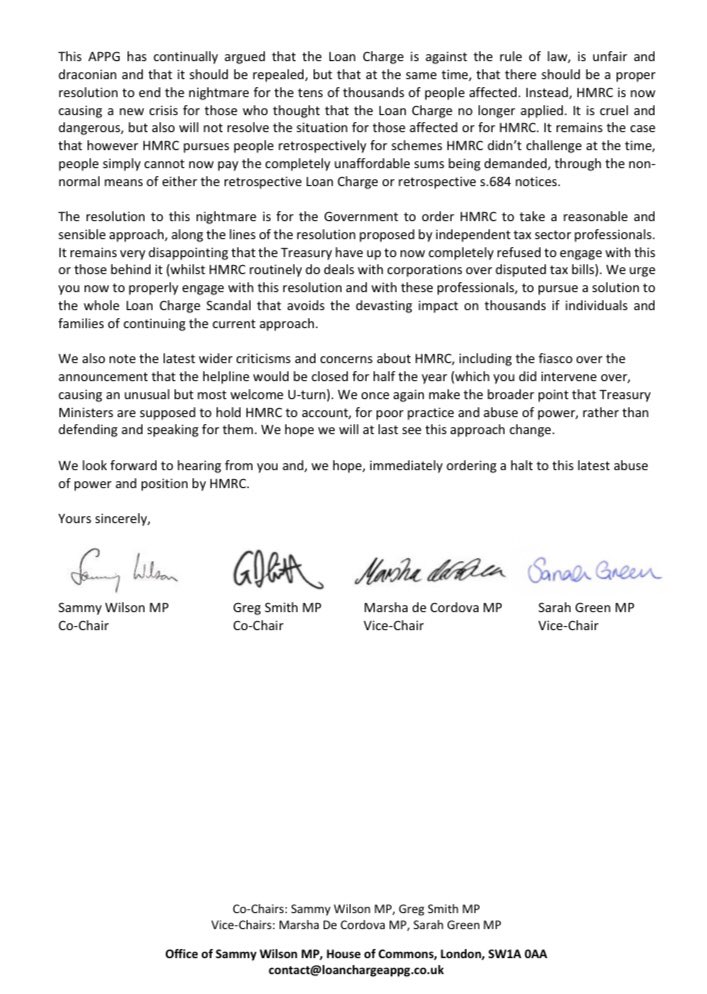

We’re very concerned about #HMRC’s use of s.684 notices, the latest way they’re retrospectively pursue people mis-sold remuneration schemes.

This is not using ‘normal’ powers as specified by the Morse Review, so it undermines a key recommendation & is another abuse of power.

6

79

133

43,804

Keith M Gordon retweeted

8 Apr 2024

While one can sympathise with the problem @HMRCgovuk are trying to address, the #LoanCharge as a solution has proven to be futile for @HMRCgovuk. The Morse review has made little difference. It is time to return to the drawing board, wipe the slate clean and start over. /ends

4

39

70

2,112

8 Apr 2024

My thoughts as expressed to @NickFerrariLBC this morning on the "Angela Rayner" property tax story (or non-story).

youtu.be/2bNZTpsiRhs

4

14

42

4,161

5 Apr 2024

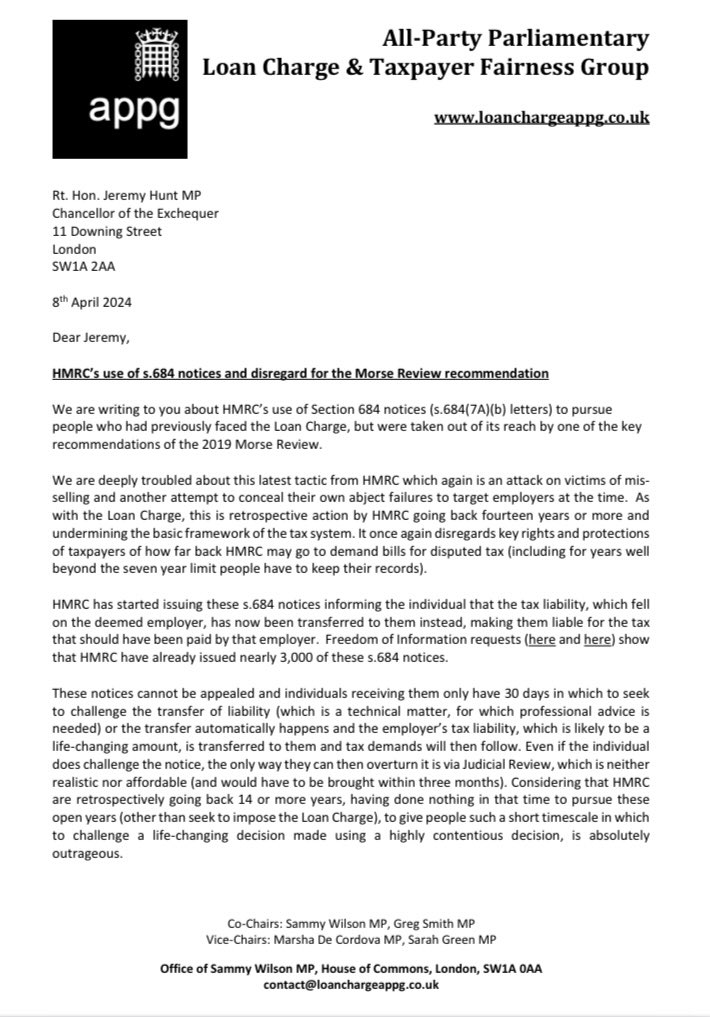

And as if by magic, the following pops up.

LCAG's letter to Lord Morse on the (mis)use of s684(7A)(b).

1

38

73

3,722