building paperplane.club -- the hotel savings club for family vacations. twin dad. prev. co-founded @StoaHQ

Joined January 2010

- Tweets 30,397

- Following 1,459

- Followers 39,020

- Likes 53,643

1,750 Photos and videos

Pinned Tweet

3 Feb 2025

The Ghosts We Inherit: India's 'New Money' Story

My mother reuses tea leaves until the water runs clear. My friend's father keeps a wooden box in his closet, with carefully folded bills arranged by denomination. Another's maintains a small diary tracking every household expense down to the last rupee. These aren't quirks – they're battle scars from a generation that survived on less.

We are their children. We carry their financial trauma in our wallets, even as we tap them against sleek payment terminals at craft coffee shops.

119

873

5,400

665,228

Jun 8

Habuild Protein Atta will take them to ₹3000 Cr run rate ✅👍

Jun 8

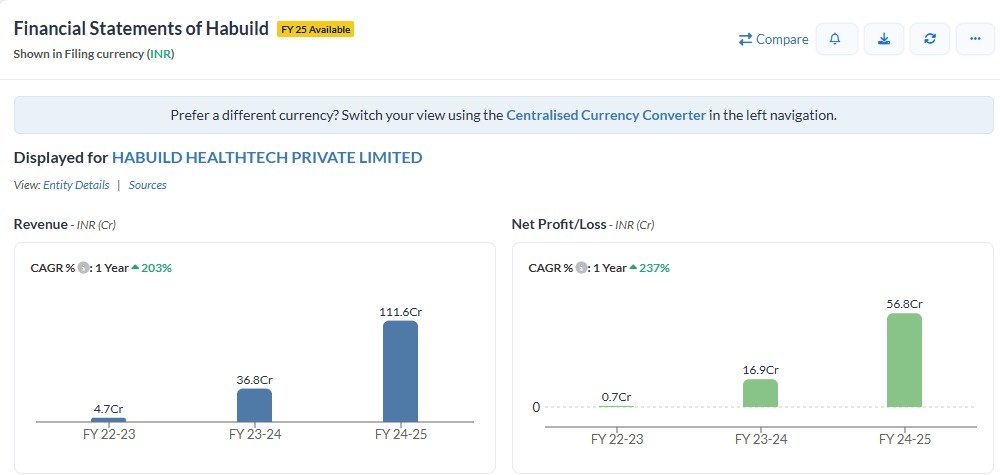

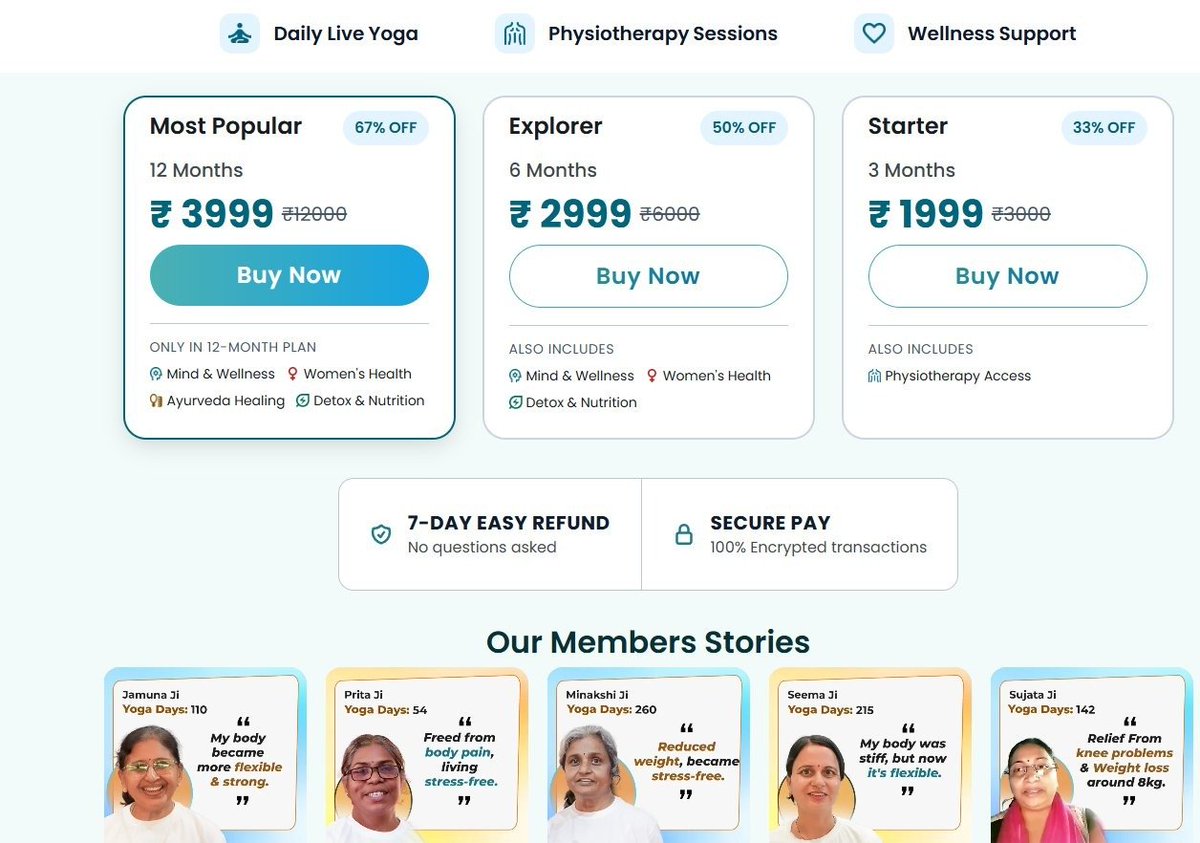

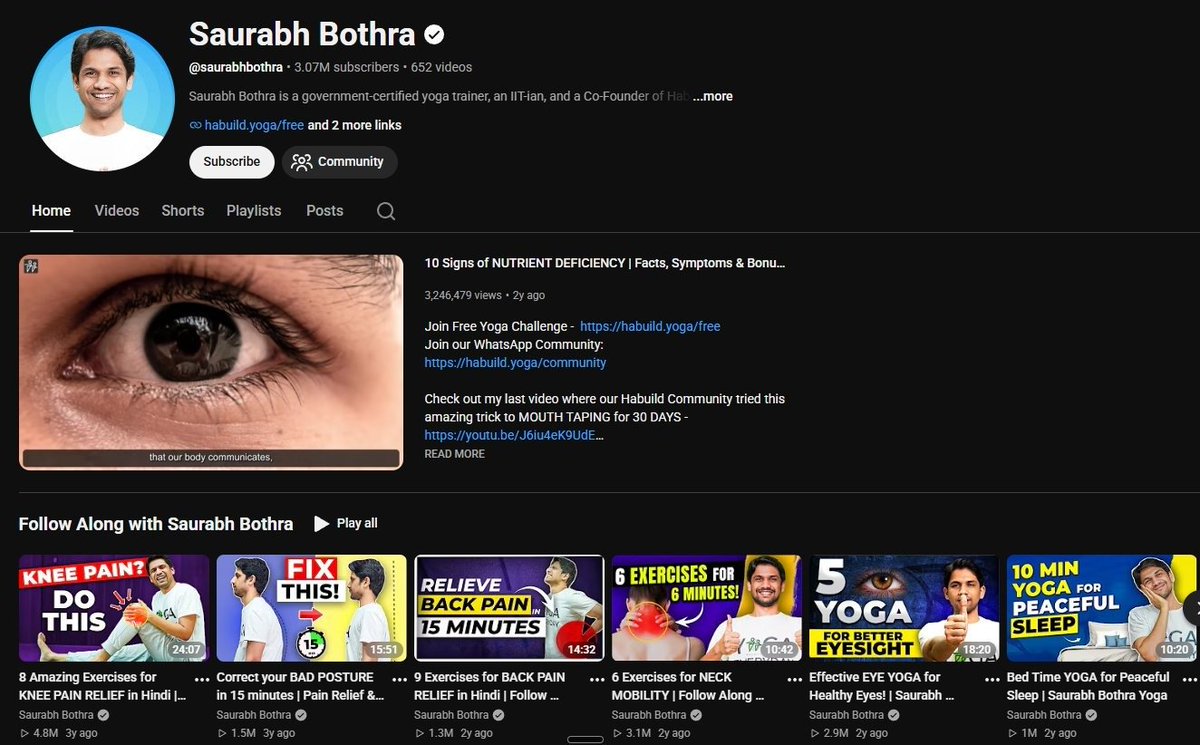

Say hello to the GRAND DADDY of all consumer startups in India. Does 70% EBITDA, 60% PAT @ 300Cr run rate (approx). Habuild is probably the craziest thing I've seen come out of India

- Founder is an IIT BHU grad that just taught Yoga/mediation after unit

- Amassed a massive following - 3M on Youtube to be precise

- Bootstraps Habuild with his sister and uni friend in 2022

- Biz blitscales, growing 3x YoY. 6L reported users now, 240Cr run rate @ 3499 avg package

- Users seem to be mostly baby boomers and senior citizens, untapped market imo

- My estimate is that this is probably more now, given these guys have a GREAT engine for user acquisition

- So many fitness products (Sarva, Cult etc) have come out of India, but I've never seen something like this. Even Pankaj Chaddah (ex Zomato founder) is still building something similar in the Yoga/meditation space (Mindhouse/Shyft), but nowhere close

Fkn mental, only early Physicswallah probably comes close

3

44

13,586

Jun 3

Imagine if marketers were judged by how much ad spend they indulged in…

2

9

3,057

Jun 1

Noice

Jun 1

The rotation:

Carrot Halwa Cardamom

Alphonso Mango

Tender Coconut

Thandai & Saffron Kulfi

Rose Falooda

Masala Chai Biscuit

Kesar Pista Shrikhand

Paan & Candied Fennel

Mysore Pak Brittle & Brown Butter

Ras Malai Tres Leches

Sitaphal Cream

Gulab Jamun & Salted Saffron Cream

2

871

Raj Kunkolienkar retweeted

May 31

One of the most amazing things I’ve ever seen: a standing ovation for the full Daraxonrasib results

I feel inspired and energised, to put it mildly — we have a targeted therapy for pancreatic cancer now, and nothing is undruggable anymore

104

1,499

9,553

1,972,050

May 29

Fun fact — Sanjay strategically spent two year at BITS before transferring out to UCB.

This was almost 10 years before @sabeer pulled off a transfer to Caltech from BITS.

May 29

Sanjay Mehrotra isn’t well known but he cofounded Sandisk (now worth ~250B), then left a decade ago, became CEO of Micron (now ~$1T).

The US denied Sanjay’s visa 3 times before he got in.

12

187

41,318

May 15

Given the way the rupee is performing, we’ll any way have to go to Bihar instead of Japan in the near future.

4

1

67

3,061

May 5

Can anyone here connect me to the folks over at Diners' Club India team?

Finding it hard to activate them on our PG, and it's not easy to seek redressal.

3

1

6

3,410

May 5

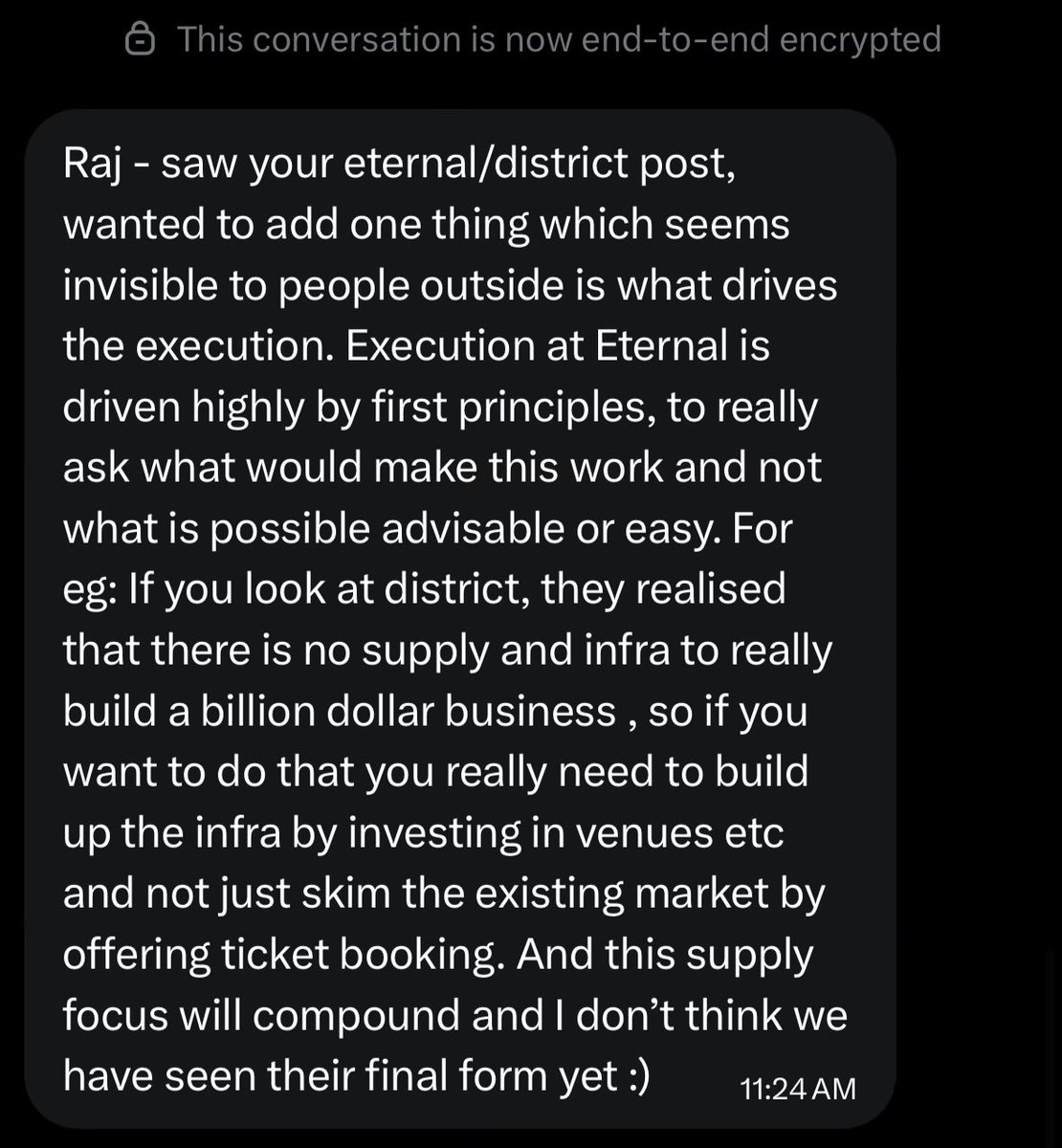

Confession: when District launched, I was bearish. Felt like a pretty lunatic move from Eternal (disclosure: shareholder).

India hadn’t produced any meaningful outcomes in ticketing, and this looked like another entrant chasing a category that’s chewed up capital before.

A year on, I’ve fully changed my mind. District is clearly turning into the king of India’s GenZ going-out economy.

What I underestimated was the cohort AND the actual business.

Post-COVID, an entire generation has started spending like there’s no tomorrow. The macro is a rollercoaster, the future feels uncertain, and somehow none of it matters. Going out is the default spend category for this group. GenZ has entered their working years inside this paradigm; they don’t really know any other version of adulthood. The spending will only take off further.

As for the business side of things, it is becoming clear that they aren’t a ticketing platform but a cultural IP platform (Rolling Loud, The Logout series, Touching Grass report). Great margins.

And to hold it up is a brand where it feels like GenZ is actually behind the wheel here and not just on the consumption side of it. Like FamPay did back in the day — the campaigns, the product, the comms all feel built by the cohort, not pitched at them.

I mean, they’ve got Ye to come to India. And if anyone can get Taylor Swift down to India, it is them.

In hindsight, it is insane though is how badly the incumbents fumbled the bag on this. They’ve had two decades of incumbency, supplier relationships, a head start on data, and never once translated that grip into a leap from being a utility to being a cultural force.

District just walked over and picked up the crown with insane execution. Mad respect. 🫡

May 5

Someone made a weekend hotlist on District, won ₹50k in promo credits, and is now on a billboard in their city.

The ROI on "going out more" has never looked better on paper.

9

4

165

57,830

May 5

More stories from the inside — very rare cultural trait btw

1

19

1,354

Apr 29

In case you’re looking for inspiration on what to gift your friends with an infant…

14

1,199

Apr 28

Died in the tarpit once, please avoid.

Apr 28

This is going to be a tarpit idea. It’s good in theory, but impossible to pull off unless it’s an internal company effort by a tyrant like CEO.

An external company will never be able to build a software that results in a company brain. It’s mostly because no tool will have perfect adoption from all employees and data will always be fragmented across new systems.

Chaotic systems are very hard to capture. It’s impossible to perfectly extract data from all sources as companies evolve and introduces new data sources.

You will spend all the time keeping track of the data instead of doing actual work. This is same trap that the second brain productivity folks fall for.

1

24

7,258

Apr 26

Thank the lord if you’re getting a monthly salary hit in your bank

Apr 26

IMO it’s sort of a miracle if you’re running a profitable company in India. Most reasonably good companies I know cannot charge their way into profits because customers are so price conscious

2

18

3,334

Raj Kunkolienkar retweeted

Apr 24

Almost all of my positions selling some kind of AI/agentic SaaS tool have (either by foresight or customer demand) pivoted to some kind of business model where they “forward deploy” to the customer first and then sell the system they create back to them as SaaS. 99% of “normie” businesses have 0 idea how to use AI tools to achieve their business goals

Imo most VCs are still behind on understanding this

Apr 22

If you read this and don’t understand why it’s happening it’s an opportunity to reset your understanding of how the real world works.

The real world will need a ton of help actually getting agents going in the enterprise. Companies have legacy tech stacks they need to modernize, data in tons of fragmented tools, knowledge that isn’t captured or digitized, and change management needed to actually utilize agents effectively. And they have to do all this while still running their business day-to-day, unlike startups.

This is why there is so much opportunity for companies (software or services) to actually deploy agents in specific domains and workflows. This remains a big opportunity for both existing services providers but also tons of new startups as well. Every new technology wave produces a new era of consulting firms that can deliver on that technology.

It’s also why the FDE model is going to be alive and well for a long time because companies will want to have their vendor actually help drive the change management and implementation for their new workflows.

The people aren’t going away. Far from it.

27

17

406

60,224

Apr 23

Everyone’s doing everything all at once

Apr 22

Today Fin moves beyond Customer Service

Fin now does specialized roles, starting with Sales, live today

Fin already knows your business products perfectly, it's already integrated with your systems and matches your brand

Now Fin engages, qualifies, and books leads too!

1

5

1,679

Apr 22

While Goa chases some crap glass wall Airbnb architecture, Kerala architects are the bosses when it comes to tribal architecture.

If I ever get a house built out, will likely call in an architect from Kerala.

Here’s proof that we need better layouts..

This 2,912 sq ft home in Thalassery, Kerala, fits a full family program; four bedrooms, private courtyard, lily pond, well, kitchen garden; not by building bigger but by building around three distinct functional zones organized from a central axis.

Exposed laterite walls. Clay tile roof. 35% of the wood and roof tiles salvaged from the old house that stood on the same site. Solar panels. Rainwater harvesting feeding the lily pond.

Nothing imported that didn’t need to be. Nothing wasted that could be reused.

Architects: TWO i Architects, Kannur, Kerala. Completed 2022.

The house your community has always built was never the problem. It was the decision to stop refining it.

More images in the comments 🧵

8

25

402

37,945