routers eat the world; consilient software observer; crafting an alchemist's paradise.

Joined September 2020

- Tweets 8,050

- Following 587

- Followers 4,722

- Likes 6,834

690 Photos and videos

Pinned Tweet

29 Oct 2025

People know that enterprise software has never been that fancy, but that enterprise distribution is hard.

The first point is becoming clearer as software gets ever easier to build, but the distribution point means that the "incumbents can use Cursor too" argument should have legs. In other words, having the distribution apparatus built out should give incumbents massive advantage. But the market is obv. not buying that.

Two potential explanations:

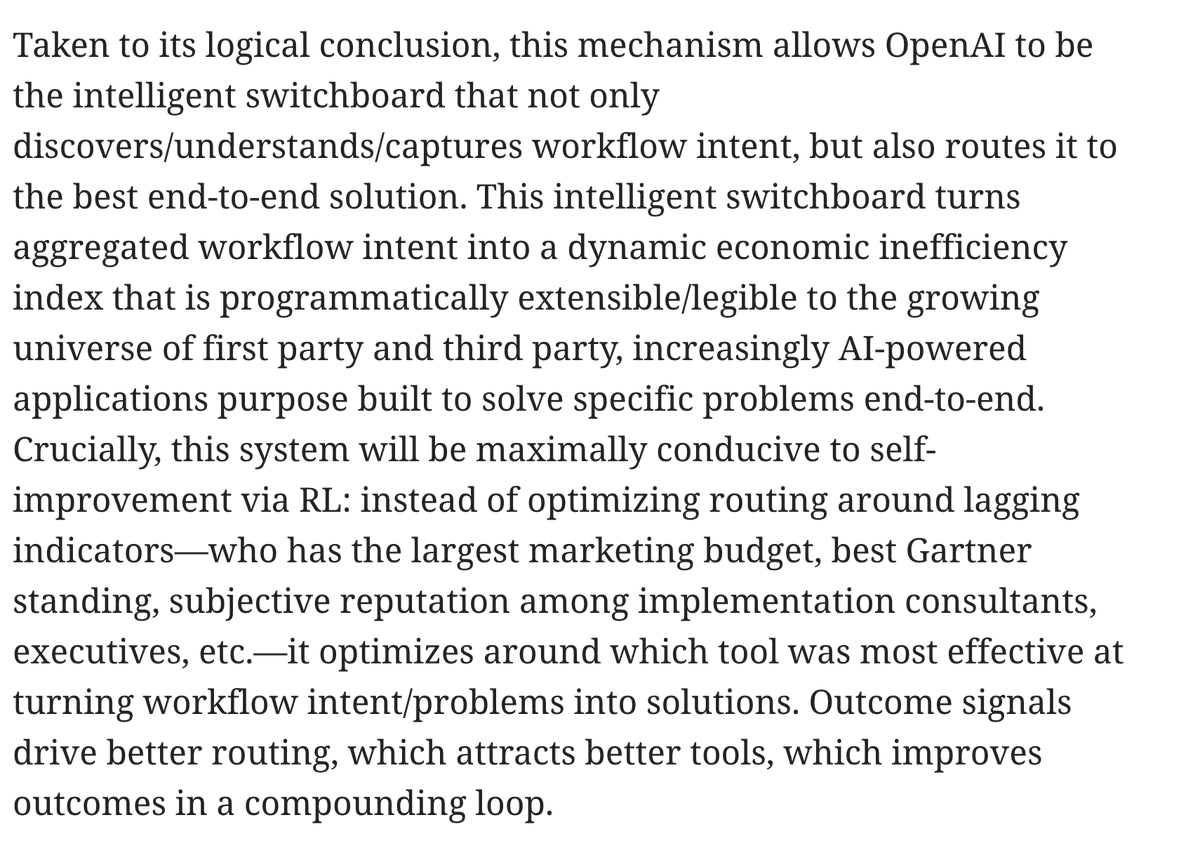

1) it's actually becoming less difficult to distribute software and to understand what to build. Biggest story here is @OpenAI as a workflow intent aggregator that can route that intent to the apps/tools best suited to solve the problem in question. If the primary interface becomes an AI system that routes requests to various specialized tools, then distribution increasingly means being the tool that ChatGPT (or whoever wins that aggregation race) chooses to route to.

This advantages the orchestration layer/aggregators of course (see this interesting piece in the Diff for a fun theory there: thediff.co/archive/routers-a…), but also means that startups should have a relative advantage in optimizing everything for this new paradigm/definition of distribution. This is somewhat analogous (with caveats) to how Google partially shifted distribution from being contingent on salespeople and brand ads to SEO/adwords, but even more extreme.

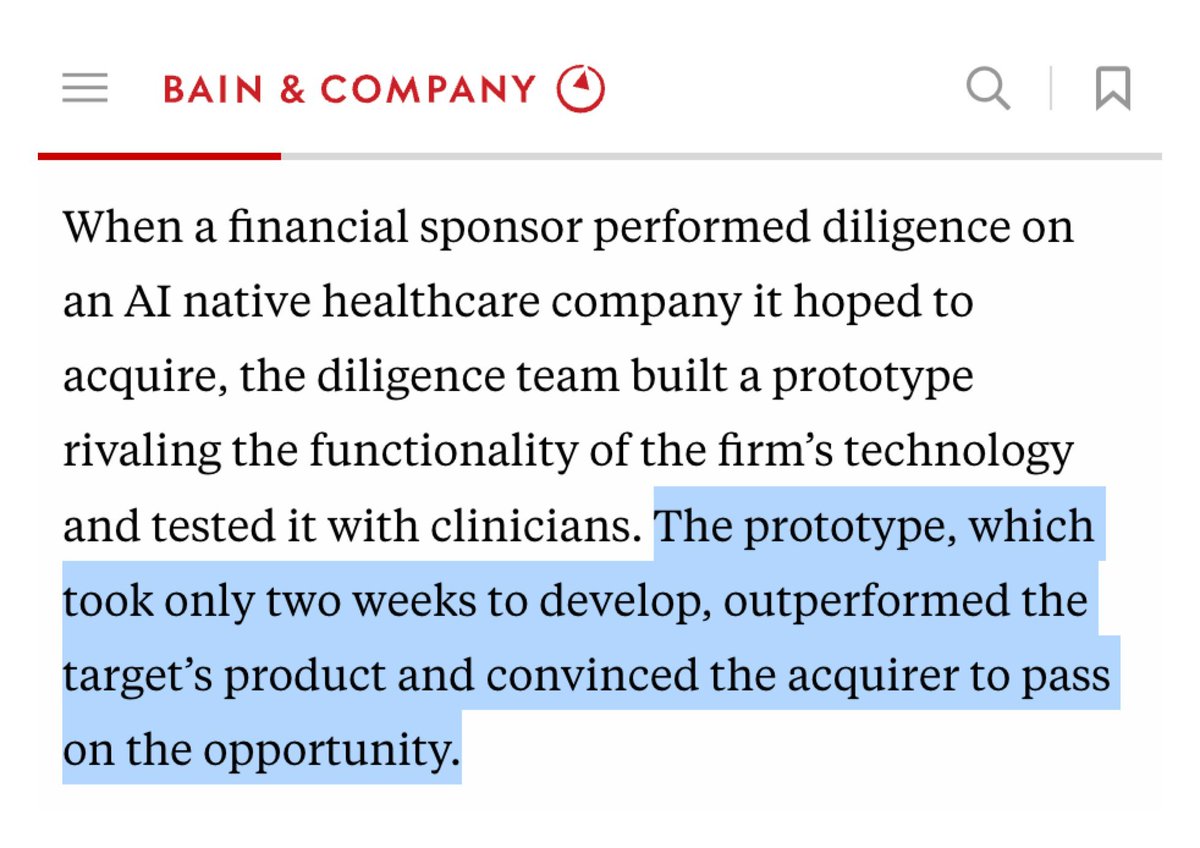

or 2) if you don't buy that, PE firms or these newish AI transformation firms (like Brain Co, GC's Percepta, SaxeCap, Palantir/Scale, Anthropic, etc.) will leverage their reputational capital, AI-native DNA, and/or ownership stakes to leapfrog both AI-native startups and incumbents by building and distributing/deploying tools themselves (the Bain anecdote).

Understanding how distribution dynamics/difficulty are trending feels like it should be very important if you want to have a sophisticated view on how software economics will eventually look, but it's pretty understudied imo. Especially relative to the question of how much easier it is becoming to build product.

1) taken to it's logical conclusion means that @OpenAI (or whoever wins) matches workflow intent to digital services/solutions as effectively as search/social match consumer intent to consumer goods. And that OpenAI/AI more broadly makes the production of digital services as automated/fossil-fueled as the production of physical goods.

If you are building/selling software this means you have two new/more powerful rent seekers than in the past: the aggregators/orchestration layer and the chip/infra layer. This sounds a lot like e-commerce market structure/economics to me. They also pay large rents to aggregators (meta, amazon, google, etc.) and infrastructure layer (manufacturers).

In e-commerce, moats exist in the form of brand, economies of scale (in certain instances), etc. but moats and margins in e-commerce are obviously weaker than moats and margins in enterprise software.

Folks like @cpaik have argued that AI will make the economics of software look more like the economics of media, which is sort of the maximalist take on vibecoding completely eliminating software moats.

But the reality IMO (at least for foreseeable future) will be somewhere closer to e-commerce. Software won't become completely free like a lot of media has, but just selling software will become less lucrative. Some solutions will commoditize significantly, like certain consumer goods did when mass manufacturing and search/direct response ads went live. Some will retain/command more pricing power as a function of true account/data gravity, regulation/compliance, end-to-end workflow complexity etc. (this is probably why you see vertical solutions outperforming).

In any case, I find it harder and harder to argue that the long run equilibrium isn't relatively bleak unless you're an aggregator, vertically integrated operating company (the AI-native opco/AI transformation approach), or NVIDIA.

would love thoughts @matt_slotnick, @sebkrier, @ChairliftCap, @MangotreeA, @huntermmonk , @yrechtman, @BucknSF

7

6

66

34,937

Jun 13

China can distill Fable, but they can’t distill SpaceX’s ability to put 100 metric tons into orbit at less than $200 per kg.

The govt banned Fable because Anthropic wanted the precedent of centralized control of AI to be set. Everything they’ve said and done points to this as their desired outcome.

As the current leader, they think centralization is the only way to secure their primacy. And the govt unfortunately believed them.

What they don’t realize is that Anthropic’s desire to centralize AI (to create one super intelligent model to rule them all) ensures that China will win. Because China’s ability to circumvent data and compute bottlenecks (through centralization) will be impossible to match. If we play that game.

The only way we will win is through emergent super intelligence, born of our frontier firms privately instrumenting their scarce context (knowledge and knowhow) in a way that compounds (recursively self improves a la @Memetic_Theory) and emergently results in superior collective capability. @PalantirTech, @appliedcompute, @mercor_ai, and @joinHandshake are necessary to usher in this future.

2

2

33

18,863

Jun 13

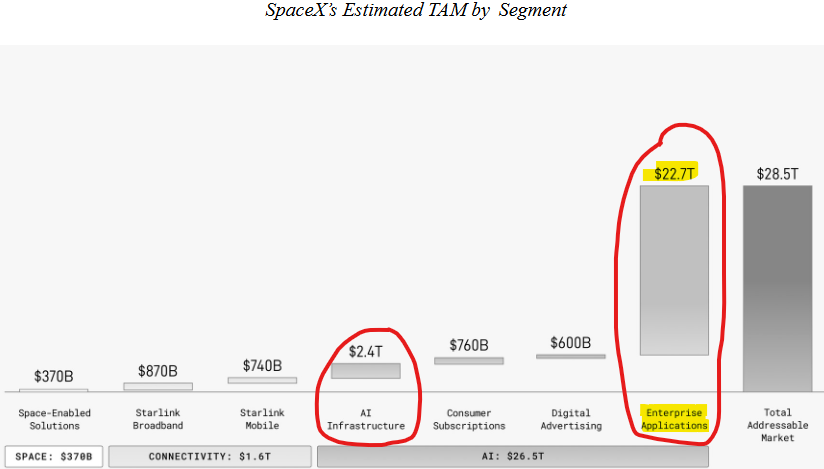

Some thoughts on the SpaceX IPO:

I’m not surprised. What you are buying is an allocation in the best existence proof we have of an entity (Elon) that identifies the most (valuable) pressing risks to human progress, continuously marshalls and coordinates resources in a way/at the scale that’s necessary to defuse those risks, and in doing so, captures unprecedented amounts of economic value. If you look at SpaceX equity as a bet on that, it’s pretty hard not to allocate. It just cannot be understated how rare such an entity is.

Crazy stat is that Elon captured more in personal profits (personal equity appreciation) over the last 5-6 years than was produced by the iPhone in the same time period.

And then if you believe we now have the ability to crystallize that predictive world model into technology, something eternal (an AI Elon) the NPV is essentially unbounded. I’m not saying this is what will happen. But there’s some probability that it does, and that’s what the bet is.

Jun 12

I believe that @SpaceX is the most important company ever

It transcends the scope of a traditional company

It will open up the Stars

Elon had the vision

And then the team pushed through limitless pain to get where they are

Which is just the beginning

1

5

1,035

Jun 13

Too late. You should have focused on creating the Whole Earth Catalog. Instead you wrote Situational Awareness, framed it as a set of predictions borne from divine benediction. But really it’s what you wanted to happen, what you thought needed to happen. From the beginning, because we conceptualized AI as god, we were doomed to centralization. Anthropic has always wanted AI with Chinese characteristics (AI controlled by the few)

Jun 12

Anthropic needs to hire Kevin Kelly as Chief Evangelist and have him paint an optimistic, wonderful, abundant vision of the future. Go into debt if you have to.

2

14

2,626

Jun 12

Anthropic needs to hire Kevin Kelly as Chief Evangelist and have him paint an optimistic, wonderful, abundant vision of the future. Go into debt if you have to.

4

3,112

Jun 11

“Mythos is a superweapon, please don’t release this” - Companies that had early access, probably saying this not because it's objectively true, but because they want to REMAIN the only ones who have access!

Jun 10

A wide-ranging conversation with Dario and Daniela Amodei, plus Claude Code creator Boris Cherny, about the AI future that’s coming — whether we’re ready for it or not.

Full show: youtu.be/v1wZwxY3CMg

1

3

612

Jun 11

“You can’t build something like a jet engine with words alone — not even the words of mathematical equations,” Dr. Bajaj said. “It is about multidimensional forces and fields and how they are changing over time.”

While OpenAI & Anthropic focus on turning the economy into code, Jeff Bezos and Vik Bajaj at Prometheus are focusing on industrial scale work data generation for chip design, jet/rocket engine manufacturing, automobile manufacturing, drug design/formulation, etc. Unlike @periodiclabs, they understand that the useful distribution of data for the underlying science (material science, physical chemistry, biophysics, etc.) is generated at the application layer: GE Aerospace is, for example, producing much more useful materials science data than anyone in a lab.

May 29

OpenAI & Anthropic are all in on turning the economy into code. They aren't betting on RL generalizing to the rest of knowledge work, they are betting on the rest of knowledge work turning into code or something that can be expressed in it!

New models are better at coding at the expense of other capabilities. I think this will be a VERY valuable local maxima, but a local maxima indeed.

Google is taking a different approach. As are labs like @si_pbc

1

2

743

Jun 11

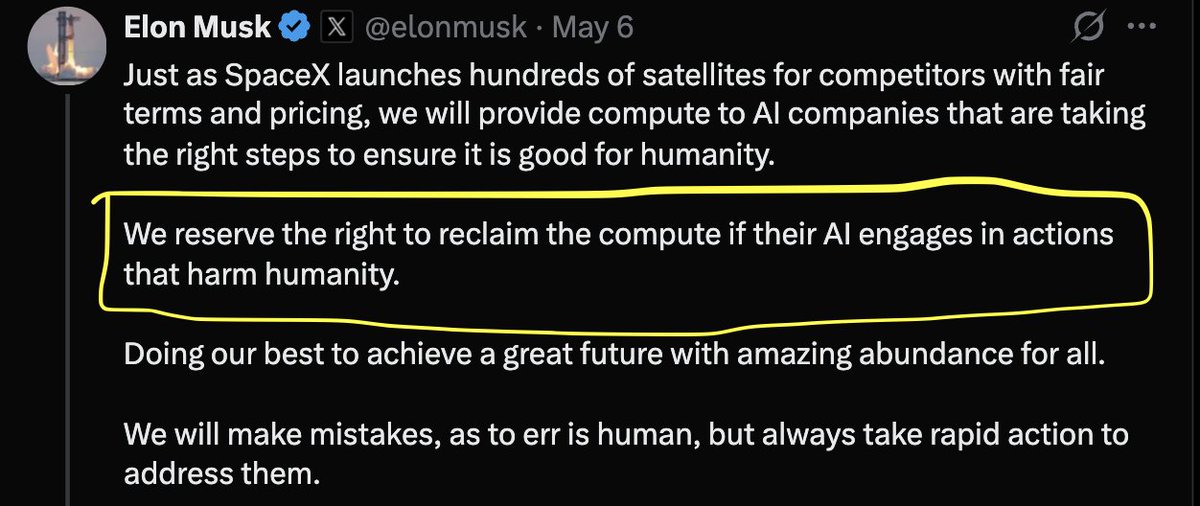

Do we think they released Fable 2 days before the SpaceX IPO so Elon couldn't pull their compute allocation? Because I don't think @elonmusk approves of this in the slightest.

Jun 10

The issue isn't the existence of safeguards. It is that:

- the classifier is terrible, exceedingly trigger happy, unusably so for many

- silently degrades responses if it's about AI

- captures all user data

These are *actively* bad, not just a mistake.

There are real tradeoffs in safety, and this release chose none of those. It basically nerfed the model in the most blatant way possible, taking none of the nuances into account. AI safety researchers can't use it. Bio researchers can't use it. Cybersec researchers can't use it.

Even by the system cards own admission this isn't in "immediately develop superweapons" territory, which makes it even more egregious. They did it because they can. Which invites scrutiny, how can you trust anthropic to do the right thing when it counts?

We just had this argument about their fight with DoW. That anthropic didn't want to be the final arbiter, just wanted safety. This is the opposite, they really do want to be the final arbiter.

9

1,141

Jun 10

Michael, blink twice if they’re holding you hostage.

Michael Truell (@mntruell) fell in love with coding at 12. The company he co-founded, @cursor_ai, went from 15 people to 700 in two years.

Today, over 60% of the Fortune 500 build with its AI coding platform.

1

18

5,357

Jun 10

x.com/lefttailguy/status/205…

Now the last question is, which context factories should you acquire and operate? How do you select/ design/instrument them such that they have and maintain a monopoly on legibilizing the most valuable parts of reality now and into the future?

Jun 10

does everyone understand the game now

you are competing on the aggregation of capital to more cheaply acquire and operate trusted actuator Context Factories

labs practically can’t play this game because Context Factories run on (what will be) commodity AI

2

2

14

1,812

Jun 10

Might this be bullish China? They don't have good chips but they can theoretically make up for this through 1) absolute wattage, and 2) the CCP mandating the production and collection of work data on an industrial scale.

Jun 9

the scaling laws in models might feel like inevitable progress if compute and data continue growing. but data has some underrated limitations…

a thread on a new kind of data ("Work Data"): what it is, and why labs now need to build and sell product for continued growth

1

1

6

1,064

Jun 9

Cursor sold itself to a lab 1) because they know harness-model co-optimization is necessary to stay competitive (and that its only a matter of time before model companies restrict access) and 2) that in the fullness of time, and in this paradigm of the technology, the organizations with the most compute and real world work data will be strictly superior from a cost-perofrmance standpoint. This is also why Google is still undervalued IMO. Also, in the medium term a rising tide lifts all boats, but in the end, those with the best demand and supply side scale economies will win.

This is not necessarily true for every domain, but for coding, it certainly is.

Jun 9

cursor, lovable, cognition numbers all a big narrative violation. wasn’t everything in the path of agi labs (especially the #1 fight, coding agents) supposed to die, not accelerate

4

6

176

50,001

Jun 9

AI is a conscientiousness prosthetic

Jun 9

AI will disproportionately benefit ADHD minds because it externalizes the boring, parts of cognition like planning, sequencing, drafting, remembering, prioritizing and amplifies the parts ADHD minds often cook at: rapid association, novelty-seeking, pattern recognition, emotional intensity, and divergent synthesis

10

672