37 Photos and videos

Your Forecaster Extraordinaire retweeted

May 20

Beautiful progress.

May 20

In 1960, around a fifth of all children died before their 5th birthday.

Today, that number has collapsed across nearly every country on Earth.

3

2

28

1,674

Your Forecaster Extraordinaire retweeted

May 18

Progress.

May 18

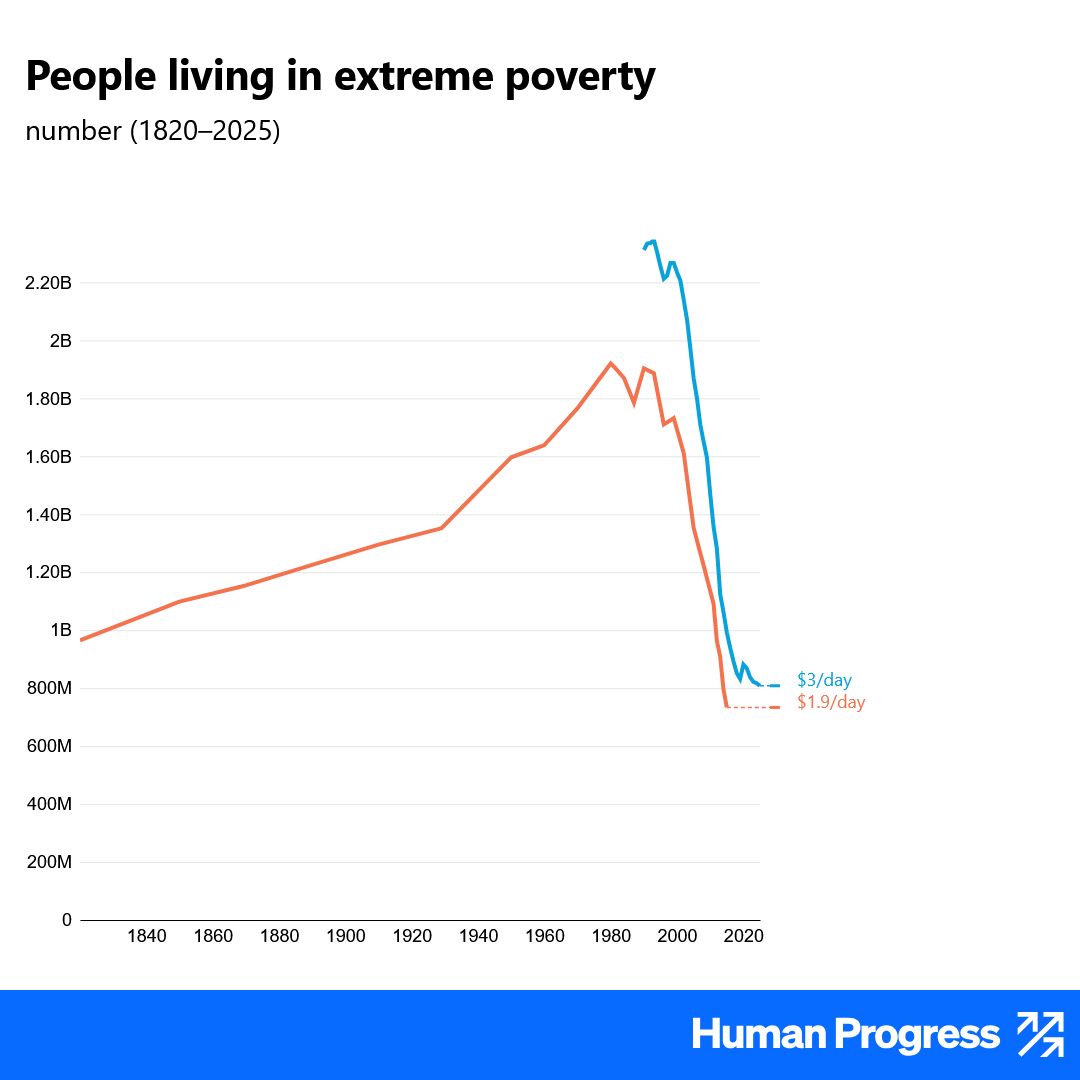

Today, despite the global population surpassing 8 billion, fewer people live in extreme poverty than 200 years ago, when the global population was just over 1 billion.

4

11

78

2,805

Oregon is a microcosm for the US (although they are not as ingenious as MN in fraud dept)

oregonlive.com/health/2026/0…

171

Your Forecaster Extraordinaire retweeted

Feb 9

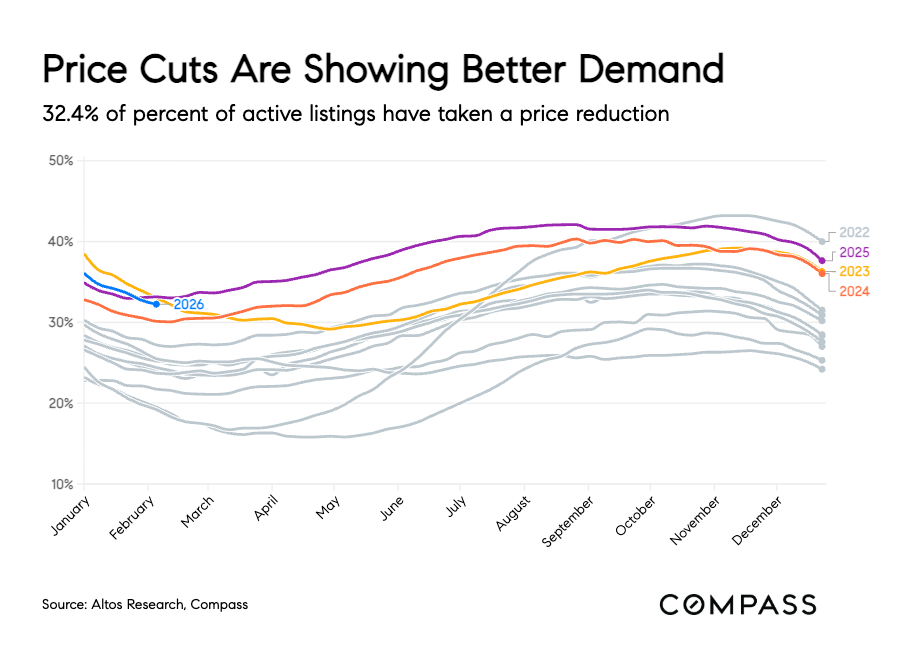

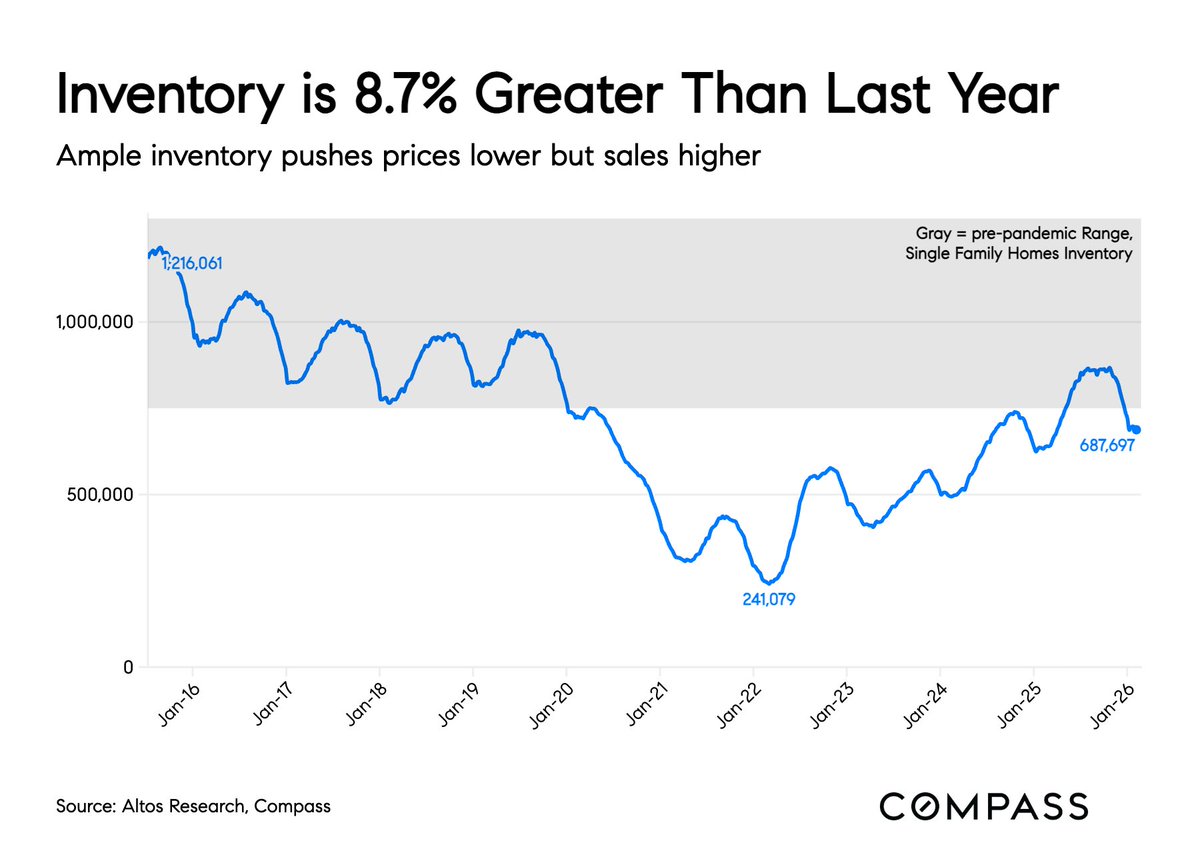

We're six weeks into the new year and the spring market is taking shape.

Home buyer demand is responding to cheaper mortgage rates. Pending sales are inching higher and the growth rate of inventory is slowing way down. If you're in the group expecting a surge of supply, watch the data closely. The inventory gap from 2025 is closing every day. From 30% growth in 2025 to just 8.7% now.

The data this week:

➡️688,000 single family homes on the market, only 8.7% more than last year

➡️Weekly pending sales averaging 3.5% more than 2025, though this week dipped with the deep freeze

➡️Price reductions at 32.4%, down 90 basis points from last year and falling when last year it was rising

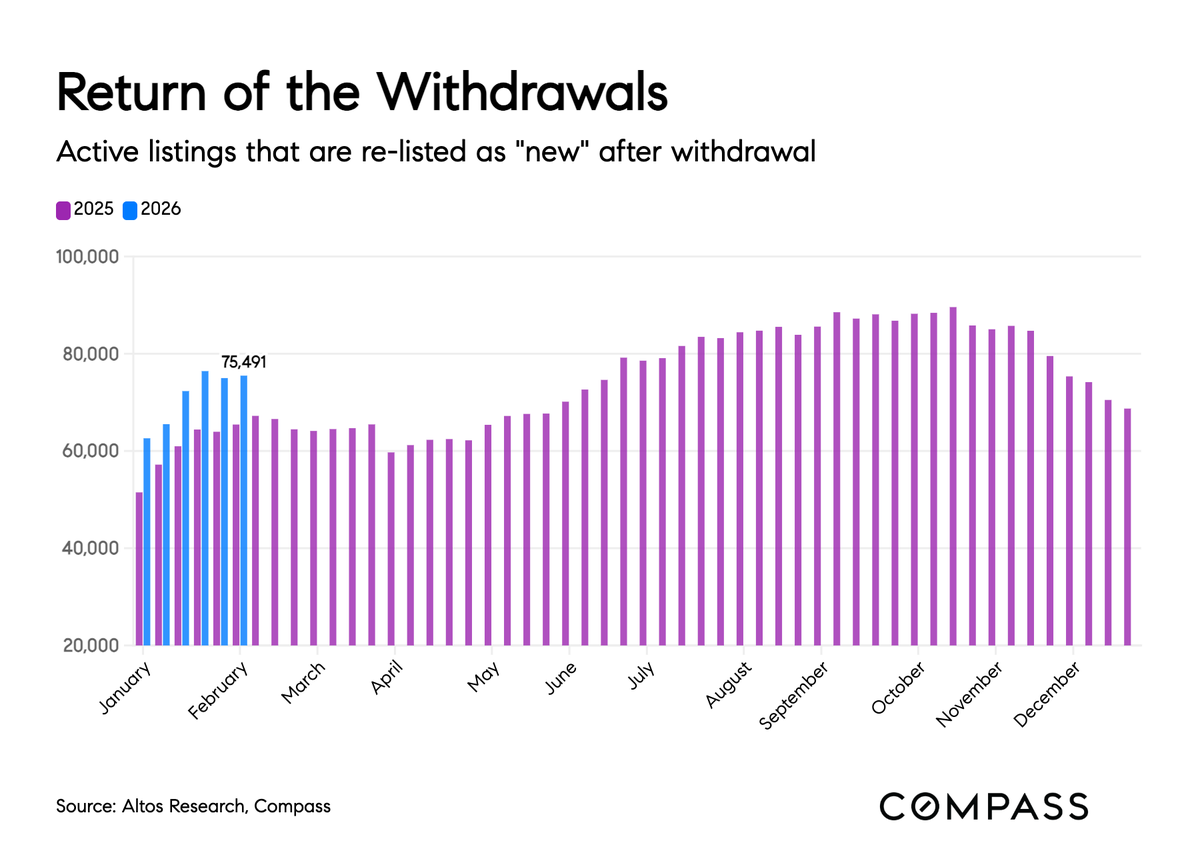

➡️75,000 re-listed homes from last fall now back on the market

➡️Median pending price $388,475, barely 1% higher than a year ago

➡️Asking price per square foot 1.7% lower than last year

Here's what I'm watching: the price reductions data is a powerful leading indicator. Right now fewer sellers are cutting prices compared to last year. That tells us demand is improving where last year it was deteriorating. If this line dips below 30%, that signals sufficient demand for sellers to hold firmer on pricing.

But we're not there yet. Buyers are still in the driver's seat in most of the country.

Home prices still have negative momentum. Mildly improving demand isn't enough yet to change that pattern. There are early leading indicators suggesting prices aren't in for a big drop, but demand hasn't picked up enough to really move the needle.

If the inventory deceleration continues, by summer we could be looking at inventory declines compared to last year. Rising rates create rising inventory. Falling rates, falling inventory. That's what's underway.

This is a very different market from a year ago.

13

17

64

10,096

"Too Late" Powell is trapped. Using the rear view mirror to drive forward is never safe. A .25 point cut will have little impact. Liquidity is drying up. States w/ sales tax will see falling income while their deficits increase. Net outflow from immigration exacerbates it.

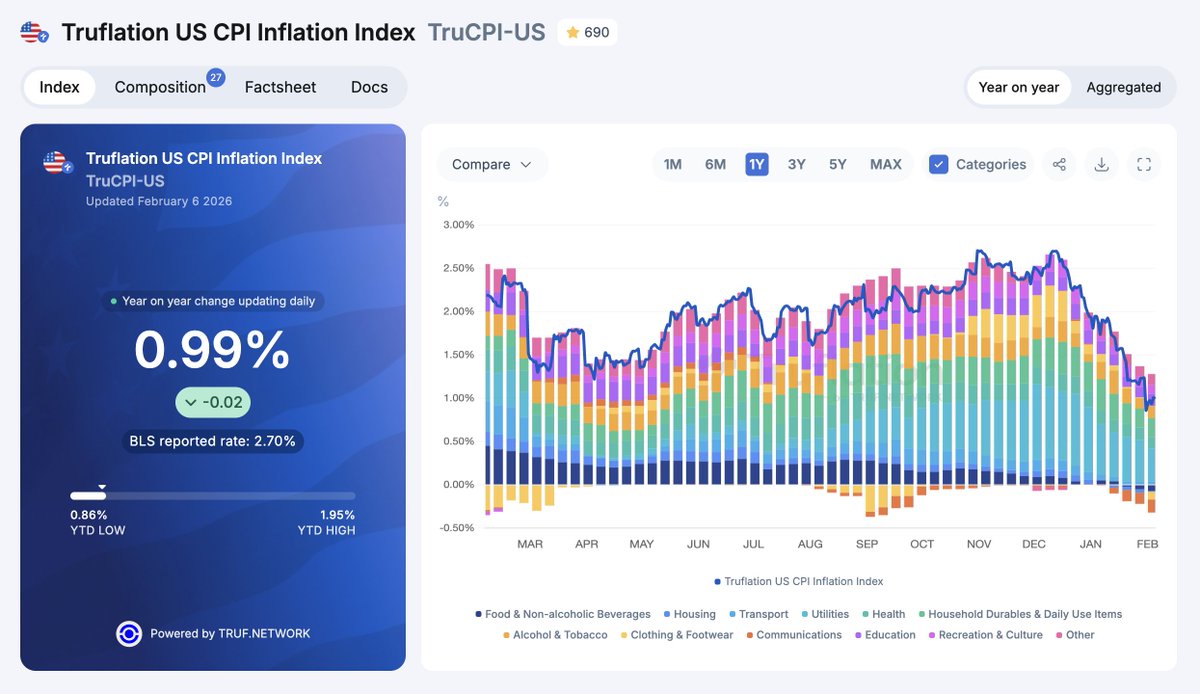

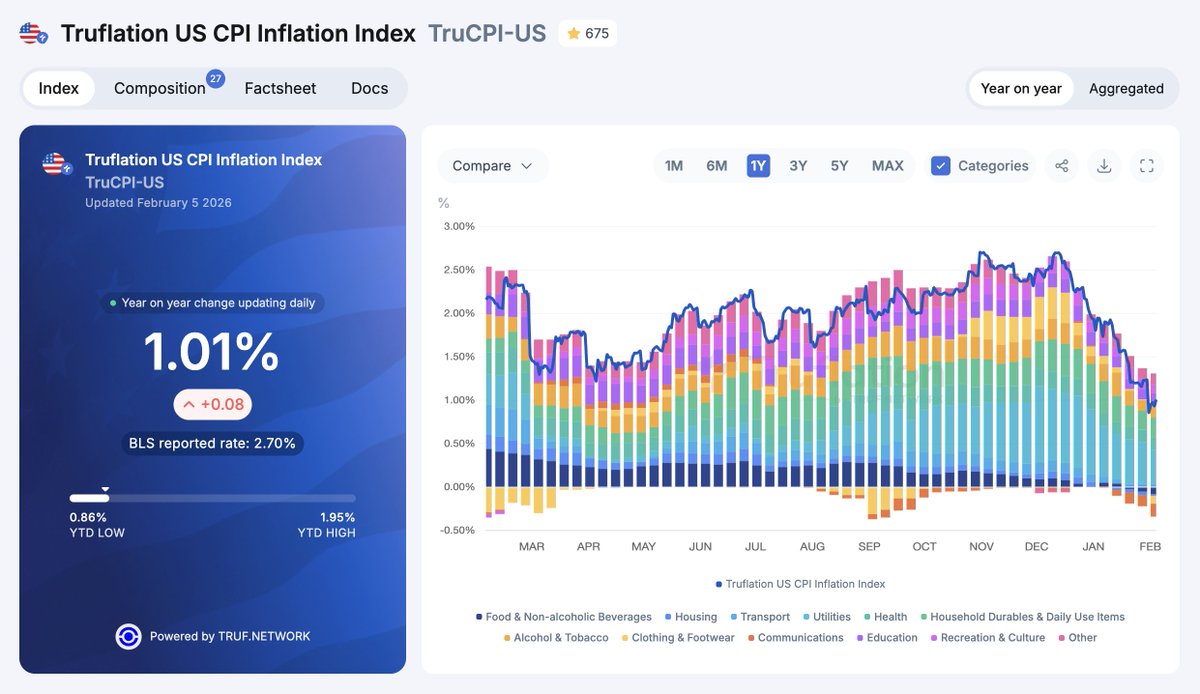

Feb 6

US inflation today, according to real-time price data:

Truflation US CPI: 0.99% Y/Y

A few product and service categories are now in slight negative territory, meaning deflation, namely: communications, clothing, food, and housing.

226

Sell off market wide but the implications for software long term. Lower seat counts due to AI related layoffs. . Gov seat reductions from austerity at city/state/federal level. More efficient usage through AI analysis. Lower barrier to entry for new competitors.

Feb 5

.@DivesTech of Wedbush Securities says he's never seen a structural software stock selloff like this in 25 years, but he's still bullish on tech stocks. He speaks on "Bloomberg The Close" bloom.bg/4cdnbCH

114

Your Forecaster Extraordinaire retweeted

Feb 6

Jensen is pushing back on the AI will kill all software narrative just like he pushed back last year on the DeepSeek panic. He was right then. He will be right again.

"There's this notion that .. the software industry is in decline and will be replaced by AI. You could tell because there's a whole bunch of software companies whose stock prices are under a lot of pressure. Because somehow AI is going to replace them. It is the most illogical thing in the world and time will prove itself. .. If you were an artificial general intelligence, would you use the tools like ServiceNow and SAP and Cadence and Synopsys? Or would you reinvent a calculator? Of course, you would just use a calculator."

40

52

458

112,439

Two things can be true at once. It's going to be a rocky three months then it's going to rip. Head on a swivel time. Cash or short until Junish then ready to bet the house.

2026 is set to rip, driven by:

• Trillions of investment

• Massive deregulation

• A pro-growth Fed

• The biggest tax cuts since 2017

All while deportations cut housing costs and crime rates.

Of course, journalists will keep promising breadlines and soup kitchens.

53

Toooooo Late.

Feb 5

🚨 BREAKING 🚨

🇺🇸 US JOLTs Job Openings came in at 6,542,000.

Expectations: 7,200,000

The labor market is cooked.

41

Your Forecaster Extraordinaire retweeted

17 Sep 2025

Why AI won’t destroy existing software

26

62

619

366,174

Your Forecaster Extraordinaire retweeted

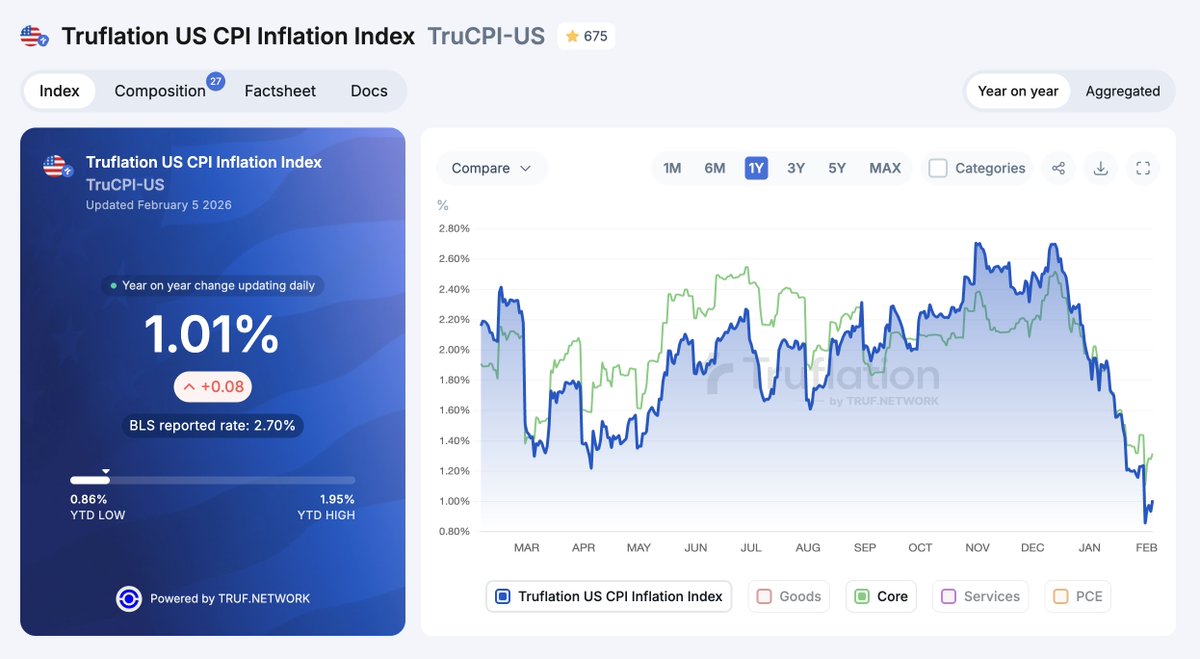

Feb 5

We recently calculated the effect of tariffs on our independent inflation index.

The effect was transient and estimated at about 0.8%.

If not for tariffs, our independent US inflation index would have been below 2% for almost the entire 2025.

However, tariff effects stabilized, and we are now back below 2% since January and near 1% since February.

Our index is based on millions of real price data points rather than the much smaller number of surveys used to calculate official inflation metrics.

Feb 5

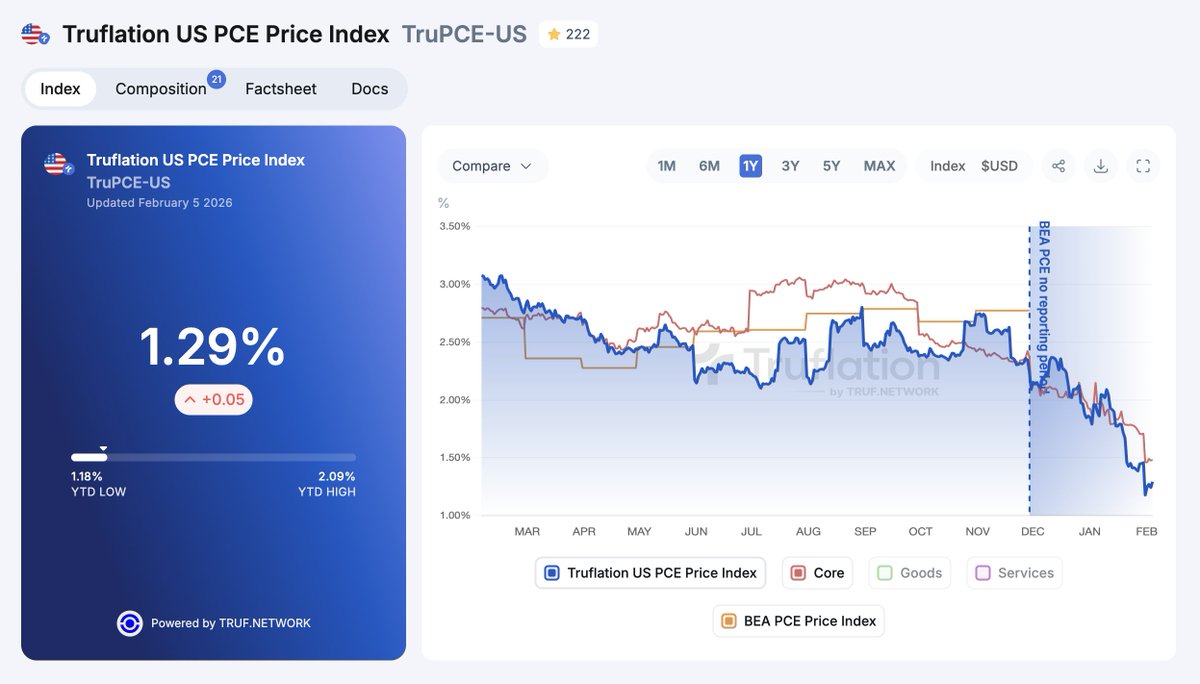

Today's US inflation, according to our independent price data aggregated daily:

US CPI: 1.01%

US Core CPI: 1.32%

US PCE: 1.29%

US Core PCE: 1.48%

US BLS Comparison: 0.53% (when applying BLS weights and categories to our data)

vs.

BLS CPI December: 2.7%

BLS (US Bureau of Labor Statistics) moved its Wednesday CPI (headline inflation) release to Friday because of the brief government shutdown, which also affected all of the BLS labor releases for this and next week.

While official inflation numbers remain stable but somewhat elevated, and Core PCE is even edging up from 2.7% to 2.8%, Truflation real price data suggest we are entering a period of cooling inflation.

The Truflation data trends have been shown to precede BLS data by between 45 and 72 days, although the raw numbers rarely overlap as the indexes differ in their methodologies, data weighting, data source types, and timing.

Truflation aggregates millions of real price data from multiple providers, delivering an early inflation gauge daily. The BLS analyzes much fewer consumer surveys and delivers monthly reports.

1

11

47

13,488

Even when you are right it can be painful.

4 Nov 2025

Any person telling you a price higher or lower for Bitcoin is a charlatan. Period end of story.

36

It's started in earnest.

18 Oct 2025

Lame theories on Trump and Bessent abound. What they are working towards is obvious, a market melt down which serves multiple purposes. 1. induces a fed rate cut 2. reduces chance of a melt down prior to the midterms. 3. Makes Democrats look bad for shut down

29

Your Forecaster Extraordinaire retweeted

22 Dec 2025

Trend Update: Deflation scare ahead. End of March will be super spicy. Risk assets are going to be in a bad spot. Fed rate decisions will have little impact as foreign bond rates climb causing US dollar liquidity strain.

1

66

Canada border today VS US border for past 4 years. Wow!

63

Your Forecaster Extraordinaire retweeted

Jan 19

Biden-Harris set up a hotline for unaccompanied migrant kids to report rape, assault, slavery with sponsors - then they blew off 65,000 calls because they assigned just one staffer!

Hearing bombshell: "How many staffers handled these phones and helping these kids?" "One."

From August 2023 to January 2025, pure neglect.

Dems trafficked these children deliberately. Every Democrat in Congress is complicit, including scumbag @AOC.

Trump's HHS triaged the backlog, processed 59,000 reports, sparked 4,000 leads on trafficking and crime. Rescued kids, arrested sponsors. MAGA's cleaning up this nightmare, putting kids first.

180

5,059

15,942

525,826