✍️ PRO Analyst at @MilkRoad | 📊 Investing in liquid markets | Sharing insights along the way

Joined August 2016

- Tweets 2,818

- Following 1,039

- Followers 2,692

- Likes 4,021

452 Photos and videos

The Fed’s dot plot points to ~3.4% rates by end-2026.

DeFi rates move inversely.

Meaning @SkyEcosystem could likely offer 8% yields at scale by then.

With diversified yield sources, risk-tranching, and incentives driving adoption, it’s hard to see Sky’s savings supply not growing meaningfully from here.

3

20

6,005

SaaS pivoting into orchestrators delivering clear ROI are going to be the winners.

Jun 11

NBER asked nearly 6,000 executives about AI. 70% of firms use it.

Almost 9 in 10 say it's done nothing for productivity in three years.

After studying the companies beating that stat: @AnthropicAI, @tryramp, @AllicaBank and @bbva.

Here's what the exceptions do differently 🧵

3

881

The current AI mania reminds me of the DeFi mania of 2020/2021.

- Back then, high yields were everywhere, all driven by token incentives.

- Today, we get access to incredibly powerful LLMs, heavily subsidized by the labs building them.

But the subsidy era is showing cracks.

- Labs are signaling they'll cut subscription tiers or pull their best models from them.

- Meanwhile, Sam Altman says token prices need to come down because they're "too expensive" for some.

Two opposing signals. I lean toward the first as you can't burn money forever.

If real prices arrive, expect usage for frontier models to drop materially.

- Retail and SMEs are agile and price-sensitive, so they'll switch or leave.

- And big enterprises? They're only now realizing they can't extract ROI from AI on their own.

They'll need to outsource it to companies like ServiceNow that can actually operationalize it but it takes some time.

Which points to where the real opportunity is: the orchestration layer.

I see it building my own systems. The single most important agent in my stack is the one orchestrating all the others.

The market thinks AI kills SaaS. Some of it, sure.

But the SaaS companies that become the orchestration layer won't just survive. They will thrive.

The winners won't be whoever has the cheapest tokens. It'll be whoever makes those tokens actually produce ROI.

4

344

.$GLXY is up 20% today.

Not because of this new partnership with Morgan Stanley, but because @novogratz confirmed the next tenant (another 830MW contracted) will be locked by the end of summer.

He also said that this is going to be the biggest data center in the US.

It is by far my biggest position!

More than $2B of contracted revenue by the end of summer.

10% of that is coming online this quarter!

@galaxyhq was also confirmed to be a part of Batch Zero, which is going to advance their further approvals!

Crypto is just a call option.

Spin-off is inevitable at some point!

The stock will be triple digits by the end of 2028!

Jun 8

Morgan Stanley just opened a door to Galaxy and pointed their richest clients through it.

A client who already owns $BTC, $ETH, or $SOL can now:

- Hand those coins/tokens to Galaxy...

- Galaxy will mint brand-new spot ETP shares...

- Then deliver them back to the client's brokerage account...

(No sale in between.)

The reason this exists comes down to tax. 👇

5

14

120

11,397

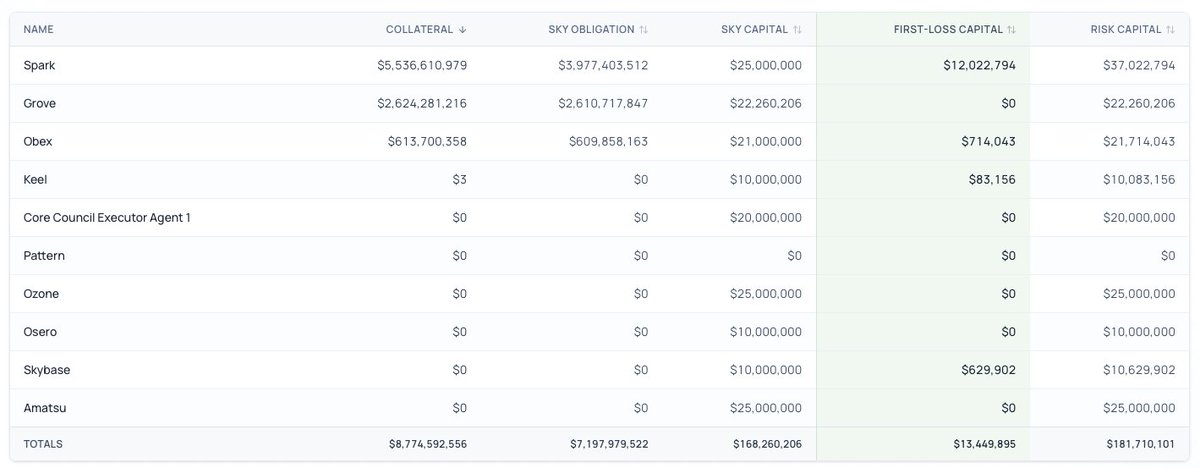

I am still bullish ethereum:0x56072c95faa701256059aa122697b133aded9279 but the key thing for me is seeing real evidence that the multi-agent prime model works in practice, not just in theory.

Right now only @sparkdotfi , @grovedotfinance , and @obexincubator (100% funds in solana:AvZZF1YaZDziPY2RCK4oJrRVrbN3mTD9NL24hPeaZeUj ) have allocations from Sky.

What I want to see is genuine exposure to more heterogeneous, crypto-uncorrelated yield strategies and broader distribution across primes.

The current edge for (s)USDS is liquidity.

People hold it despite a yield below US Treasuries because they can move a billion with no slippage, something onchain Treasuries can't match today.

I don't think that advantage is defensible long term.

Once Treasuries scale onchain, there will be almost unlimited liquidity for Treasuries everywhere, and the moat erodes.

That's why the next leg up depends on the primes.

They need to generate yield meaningfully above Treasuries while staying risk-adjusted, because in a couple of years, with Treasuries essentially risk-free and USDS still carrying risk, there's no reason to hold (s)USDS unless it pays more.

Liquidity won't carry it.

Risk-adjusted yield above Treasuries has to be the selling proposition.

3

3

10

2,074

Galaxy (GLXY) is my biggest position, and I'm now even more bullish.

It comes down to location.

Helios sits in West Texas, a region packed with wind and solar farms, where power prices are among the lowest in the state. That's no accident.

Around 2005–2008, Texas realized it had huge wind potential out west but no way to move that power to the cities. So it created Competitive Renewable Energy Zones (CREZ) and spent billions on thousands of miles of transmission lines. It worked almost too well: wind blew past its targets, solar piled on top, and the region now often generates more power than the lines can carry east. When supply overwhelms demand and transmission capacity, wholesale prices can fall to zero or even turn negative.

One nuance: Galaxy isn't the one paying for the power. Its tenant is (CoreWeave). But that doesn't weaken the case; it strengthens it. Cheap, abundant power is exactly what AI customers are hunting for, and anyone deploying billions in GPUs cares deeply about both long-term power economics and availability.

West Texas offers both, which makes Helios far more attractive than data centers stuck in power-constrained or higher-cost regions.

And the bigger advantage isn't even the low prices. It's the availability.

Power has become one of the main bottlenecks in AI infrastructure. Plenty of operators can raise money and buy GPUs, but securing hundreds of megawatts is getting harder by the day.

As AI demand exploded, that power became worth far more than before, and it's an asset competitors would find extremely hard, expensive, and slow to replicate.

That's a structural advantage, I think the market still underappreciates.

Bullish $GLXY!

5

7

85

7,731

Micron ($MU ) is being rerated as a non-cyclical company, with multiple analysts raising price targets across the board.

SK Hynix is the market leader with better technology and is set to enter the US market in Q3. You can get exposure through SK Square at a ~50% discount. This is a no-brainer.

Soon to become my largest position if nothing materially changes.

Jun 1

Goldman just raised SK Hynix 2027 operating profit estimates by 22% and 2028 by 24%. The new 2027 number is roughly $266B in operating profit.

Our PRO analysts flagged this opportunity well before the upgrade hit.

SK Hynix has been running Nvidia-style margins while trading around 4.5x earnings, but most Western investors haven't been paying attention to Korean memory names until recently.

Goldman just confirmed the valuation gap our analysts caught more than 25 days ago.

Don't miss their next big trade - try Milk Road PRO for $1 for 7 days, through the link in our bio.

3

1,446

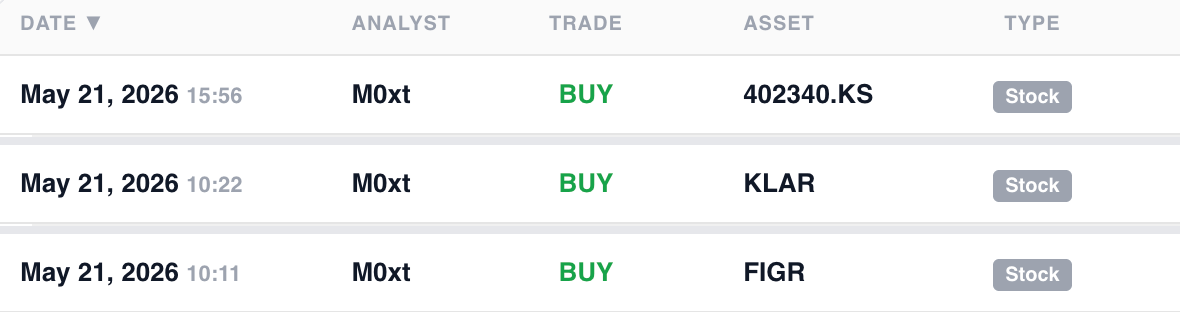

m0xt retweeted

May 27

Our lead crypto analyst @m0xt_ just bought into 3 different sectors in a single day:

Crypto, fintech, and AI memory (save this).

Here's what he's been buying...

First up: Figure $FIGR - the onchain lending platform.

Q1 results came in strong and the market couldn't have cared less.

Over the last few days the stock has dropped almost 20% with no real fundamental reason behind it.

When a business is performing and the price is falling on nothing, that usually points to short-term weakness rather than a broken business.

M0xt_ is using the pullback to size up.

Next was Klarna $KLAR.

Most people still see Klarna as a "buy now, pay later" company (and nothing more).

But m0xt_ just finished a full deep dive on the company and came away realizing that frame is way too narrow now.

Klarna has a real base across Europe, is pushing hard into the U.S., and keeps building financial services well beyond BNPL.

The stock IPO'd at a $15B valuation and has mostly traded down since.

The post-IPO unlock pressure is largely worked through, profitability is showing up in the numbers, and m0xt_ believes now is the moment the risk/reward starts to flip.

Finally - there's SK Square, the AI memory trade.

SK Hynix just raised its Q2 guidance on higher DRAM and NAND pricing, which tells you memory demand is running ahead of supply.

M0xt was hoping for a pullback to add cheaper, but every dip keeps getting bought up immediately - so he stopped waiting.

The big idea:

SK Hynix is one of the cleanest ways to own the AI agent buildout.

Agentic workloads are memory-hungry by design - long context windows and persistent state push memory needs way up.

As inference scales from chatbots to agents running continuously in the background, the memory cost per query keeps climbing.

But instead of buying SK Hynix directly, m0xt_ is buying SK Square, a holding company that owns a big chunk of its stock.

SK Square trades at a 50% discount to its net asset value, which means he's getting roughly the same exposure to the memory thesis at half the implied price.

If you want to see the exact position sizing on each of these three buys, plus the full Klarna deep dive m0xt put together...

Click link is in the first comment.

8

3

24

22,157

I’m still a long-term holder, but I trimmed some of my HYPE position.

I’m not convinced this uptrend is sustainable because it seems driven more by short-term momentum than by long-term investors reacting to underlying business growth.

May 20

HYPE >$50. Some thoughts:

Asset prices reflect the last trade in a market’s continuous auction. While this is often treated as “fair value,” only a small share of supply actually changes hands. As a result, price usually reflects the most aggressive buyers and sellers, and the premium or discount they are willing to accept relative to the recent price range. Still, over time, slower-moving supply and demand respond, and the market starts to re-equilibrate.

Therefore, while there are many ways to value an asset, the best way to contextualize its current value is:

1) What do short-term flows and asymmetries look like?

2) Where are longer-term buyers and sellers likely to step in?

For HYPE, short-term aggressive flows are clearly asymmetric to the upside. ETF access has started ($14.1M volume on May 19th), DATs are buying (Hyperliquid Strategies has $100M left), and the Assistance Fund continues to purchase $10M–$15M a week. On the market side, we are seeing tons of positive catalysts: Circle / Coinbase likely bringing in >$100M of stablecoin-related revenue for Hyperliquid, pre-IPO markets like SpaceX and potentially OpenAI from TradeXYZ bringing outsized TradFi attention, RWA open interest at $2.6B (up 2x from two months ago), and most recently regulatory momentum around tokenized stocks.

This leads to the second question: where do longer-term holders sell into this demand? HYPE spent nearly a year auctioning between $20 and $40, rotating supply into a new holder base. My bias is that much of this supply now sits with less price-sensitive holders: Deployers, the Assistance Fund, DATs, and stakers. If motivated sellers already had repeated exits around $38–$40, how much is left to sell above $50? Instead, we may see a reflexive dynamic where investors waiting for lower (e.g HYPE’s $8 Solana moment) are forced to rotate in.

My view is that flows and demand have already pushed many TradFi equities into extremely stretched valuations, while HYPE, despite being crypto’s clear winner, has remained relatively anchored to fundamentals. This break above the prior range, along with clear improvements in fundamentals (regulation, diversified revenue, 0-1 pre-IPO / 24/7 markets) and access (ETFs and DATs), could create an environment where price discovery turns reflexive and HYPE grinds much higher, detaching from traditional valuation anchors in the same way many high-growth L1s have in past cycles.

Hyperliquid

1

8

1,063

Sky is raising the bar once again.

You can clearly see how Sky generates revenue, how it gets distributed, and how much value flows to each layer.

Everything is out in the open.

This should be the standard for every crypto protocol.

Sky is setting a new benchmark for transparency in crypto.

Most protocols still keep their operating costs and revenue distribution vague or hard to track.

Seeing this level of clarity is refreshing, and honestly, it builds a lot more trust.

I am bullish ethereum:0x56072c95faa701256059aa122697b133aded9279.

2

2

32

8,304

Sky has repositioned itself not just around its product, but around its token as well.

They don’t want a retail-heavy holder base complaining about reduced buybacks or low staking yield.

They want a stronger cap table that supports building a sustainable business and prioritizing the highest-ROI use of capital over reflexive buybacks/dividends.

That repositioning made me revisit my view on Sky and ultimately add to my position again.

May 6

A month ago, our lead crypto researcher @m0xt_ sold his $SKY bag.

This past week, he bought it back.

Here's what changed (bookmark this)....

Sky just printed $46M in Q1 profit and revenue hit a record $123M - this is real cash flow from a working product.

The engine is $sUSDS.

It grew 72% quarter-over-quarter. At scale, onchain, with a 3.65% yield, it's pulling in capital that has nowhere comparable to go.

If you're sitting on size and you want yield without taking on degen risk, the options thin out fast. $sUSDS is increasingly the answer.

Ok, so what spooked @m0xt_ in the first place?

He sold Sky when the protocol cut its buybacks.

His view at the time: without the protocol bidding its own token, there might not be enough natural demand.

Reasonable thesis (but wrong).

What he didn't price in was who would show up to replace those buyers.

The holder base shifted. Cutting buybacks looked bearish on the surface, but it actually built a stronger capital buffer and signaled long-term thinking.

That filtered out the short-term flippers and pulled in a different kind of investor - the kind that reads the financials and understands why a protocol building reserves is healthier than one returning every dollar to holders.

A few things he's watching before sizing up further:

Q1 may have been effected by the monthly settlement cycle pulling forward revenue from Q4. Q2 will be the cleaner number.

Operating expenses came in at $2.35M for the quarter, a meaningful drop from prior levels. He wants to see that hold as the protocol matures and automation does more of the work.

And the big one...

Does $sUSDS keep growing at 3.65% yields? If so, it confirms there's nowhere better at scale for stablecoin yield onchain.

The setup right now: strong growth, real profitability, opex under control, and a valuation that hasn't caught up to the fundamentals.

That's why he's buying it back.

Want to see exactly how much he added and how Sky is now weighted in his portfolio? Click the link in our bio.

1

10

1,137

I haven't tweeted in a while. The reason is simple.

I've been in full builder mode with real FOMO since Openclaw launched.

But the more I sat with it, the clearer one thing became: Once you start working with agents, there's no going back. You don't see the world through the same lens.

So last week I took time off.

I wanted to step back, digest everything, and reflect on what the last few months have been for me, my family, my portfolio, and my future.

I'm rethinking a lot of things, and I'll probably keep rethinking. That's the nature of being an investor.

But if I had to land on one conclusion: people with strong analytical thinking who can leverage AI are best positioned to benefit from the disruption that's coming.

Because execution is becoming cheap.

The new bottleneck is framing the right problem, building the system, directing the agents, and judging what comes back.

That's where analytical thinkers compound.

1

10

578

m0xt retweeted

Our macro channel has been an incredible resource to stay up-to-date on what’s happening in Iran

It’s timely and it’s laid out in a simple and understandable way

This channel should be a follow for everyone in markets

HERE’S EVERYTHING THAT HAPPENED TODAY IN THE WAR:

1. The US has sent multiple peace proposals to Iran.

2. Proposals included an immediate ceasefire and reopening the Strait of Hormuz.

3. Iran rejected all US proposals.

4. Iran responded with its own 10 point plan.

5. Their key demand: compensation for war damages.

6. Trump said Iran’s proposal is “not good enough.”

7. He’s holding firm on the Tuesday deadline to reopen the Strait.

8. If not, Trump has threatened to destroy all power plants and bridges in Iran.

Big picture:

There’s a lot of talk but still no real progress.

Negotiations are active but both sides remain far apart on core demands.

3

5

15

3,277

I wonder if we are about to see more moves like this one!

3

14

1,107

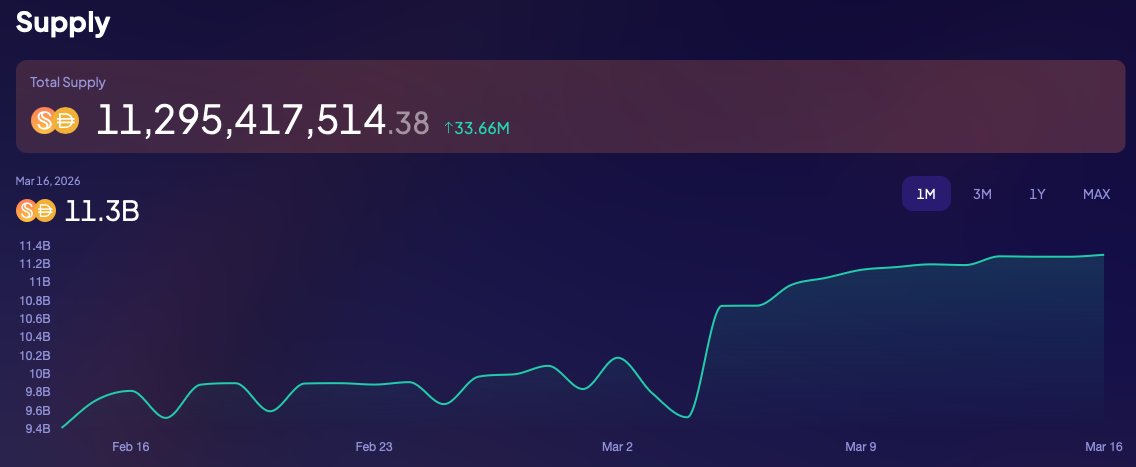

Nobody really talk about @SkyEcosystem.

But everyone should.

Their supply just surpassed $11B.

Their business model is immune to crypto prices.

Their portfolio of accessible strategies keeps growing.

4

1

21

960