muh-LEE-ah is a @businessinsider reporter covering tech and law

Joined September 2009

- Tweets 11,603

- Following 3,408

- Followers 15,442

- Likes 26,321

1,860 Photos and videos

Melia (Robinson) Russell retweeted

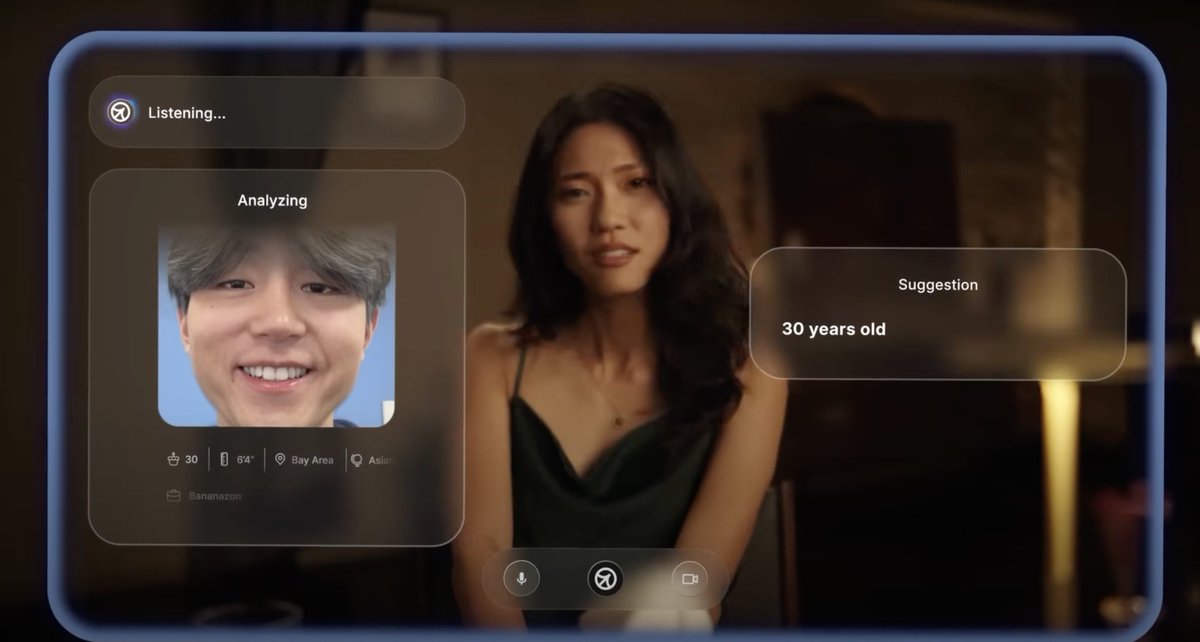

fast-growing legal ai startups face a new threat: their customers :)

5

5

35

3,503

I’m asking the hard-hitting questions over here

May 27

Going live now on a Reddit AMA with @winstonweinberg - ask us anything about Harvey.

Hosted by @alexjdenne, @meliarobin on r/legaltech. Excited for everyone's questions.

reddit.com/r/legaltech/comme…

1

5

1,051

*!*!*HAPPENING NOW*!*!* The @harvey founders are answering your questions live on r/legaltech. Join us.

Reddit AMA with our cofounders @gabepereyra and @winstonweinberg tomorrow, Wednesday May 27th, 1pm PT / 4pm ET.

Join us on r/legaltech, hosted by @alexjdenne and @meliarobin.

We're excited for your questions!

1

7

313

Melia (Robinson) Russell retweeted

Apr 28

@scottastevenson of @SpellbookLegal,

@PrestonJClark of @smpldocs,

@mkjung_ at @heyivoai,

and @rossmcnairn at @WrdsmithAI

What do you think people are going to ask?

Time to try something new ✨

This week, r/legaltech is hosting a joint AMA with four founders who often compete for the same customers.

All sell contract review software for lawyers.

I promised mod @alexjdenne I’d bring the tough questions. What do you want to know?

1

4

472

Time to try something new ✨

This week, r/legaltech is hosting a joint AMA with four founders who often compete for the same customers.

All sell contract review software for lawyers.

I promised mod @alexjdenne I’d bring the tough questions. What do you want to know?

2

1

15

1,088

Melia (Robinson) Russell retweeted

Apr 23

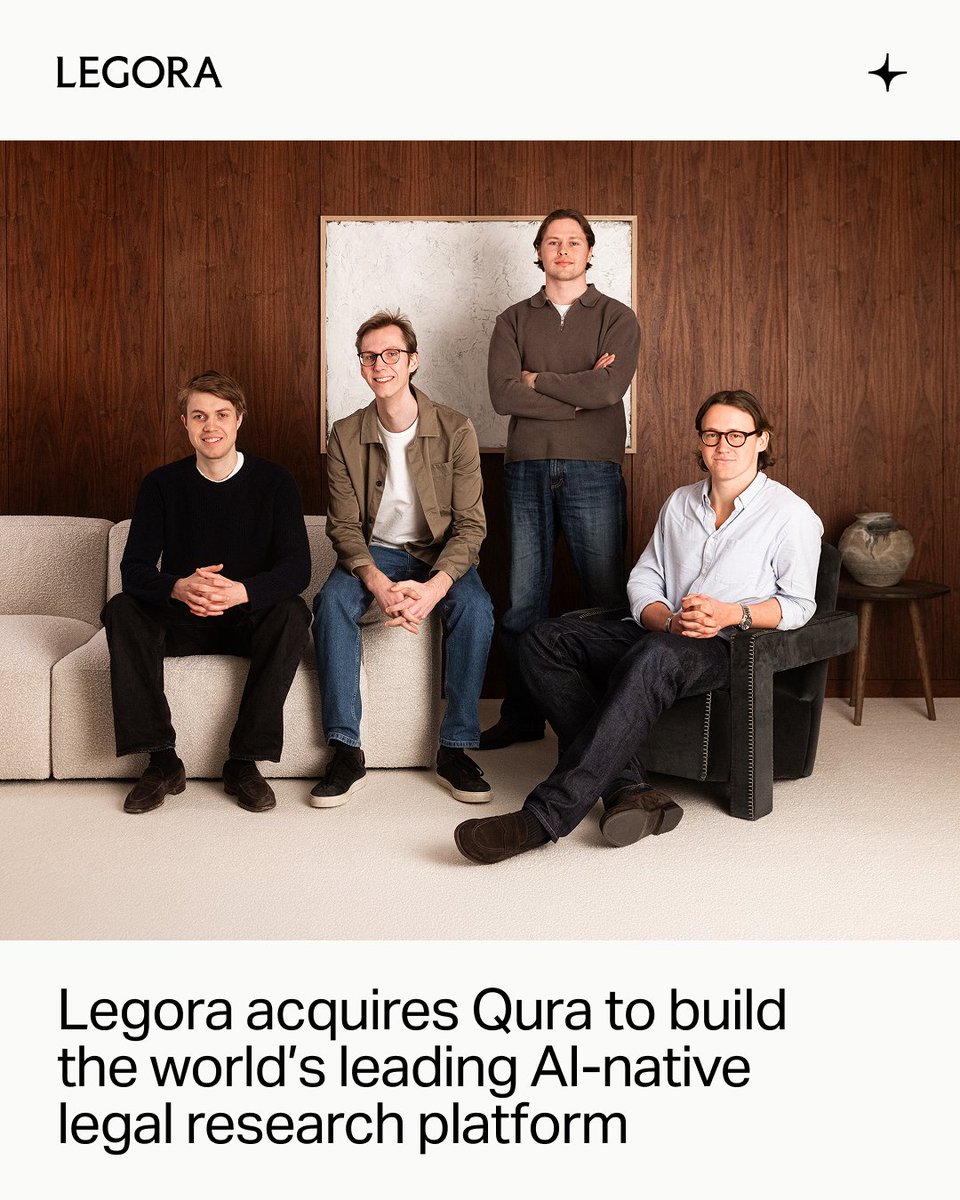

I am thrilled to share that @WeAreLegora has acquired Qura.

Legora is the operating system for legal work, and legal research is a core pillar of our platform.

When others have chased the next shiny object, the team at Qura has obsessed over legal data structures, hierarchies, and completeness of coverage. This is clear in the undeniable customer love, the accuracy and the scalability of their approach.

The Qura team is already busy shipping the next big thing at Legora and will be focused on scaling our legal research product globally.

We can’t wait to show you what’s next.

Press release:

legora.com/newsroom/legora-a…

@BusinessInsider story by @meliarobin:

businessinsider.com/legora-a…

7

10

143

38,201

Melia (Robinson) Russell retweeted

Apr 20

Firms need to stop thinking in terms of "How are we using AI?" and reframe as "What must we do because AI exists?"

I somehow missed this story last month but this talent leak is something I've warned firms about for the last 3 years

6

8

37

5,258

Melia (Robinson) Russell retweeted

Apr 20

If you are a talented and ambitious tech comms leader and you're open to new roles, let me know! There are some amazing (but not public) opportunities right now and I am fully off the market - I'll send them your way!

23

17

226

30,193

Melia (Robinson) Russell retweeted

Apr 18

We are likely past the point of no return unfortunately around “ARR-embellishment”, if you put it nicely…

This version @scottastevenson talks about is egregious IMO. I haven’t see too many cases of this.

One thing I do believe is that “ARR-dishonesty” will always come back to bite you. For the very few founders who want to play the most aggressive version of this game, it’s just not worth it… trust me.

For me, the major issue at hand is how we as an industry should disclose and report inference-based revenue, which there are arguments for and against it being included in an aggregate “ARR number”

The hard truth is that there are varying levels of quality of inference-based revenue and it’s ultimately a judgment call that an investor needs to make regarding the REPEATABILITY and DURABILITY of the underlying atomic unit of work or behavior being monetized.

This is how most investors drive towards a judgment on revenue quality…

1. Net revenue retention (more on this one below)

2. Gross logo retention

3. Gross revenue retention

4. Engagement retention

5. Engagement intensity

Very important side note - In SaaS era, most important measure for me was net revenue retention - N$R. We used to look for companies with 120% N$R and some best-in-class companies had 140-160% N$R.

Some AI companies today tout 200% N$R but it’s not like-for-like with the SaaS era in some cases where there isn’t the same repeatability and durability of the underlying activity.

Where the activity is more sporadic or experimental, this N$R should be viewed closer to a payments / fintech N$R that always look high due to starting off of a small base and grows quickly but may spin down again quickly also.

In any scenario, MORE TRANSPARENCY THE BETTER for everyone.

In the long horizon of time, it all comes to light and you don’t want to be a founder that has asked investors and employees to wade into your part of the ocean, only for the tide to go out and see that your “ARR” was not what you presented it to be… my 2c

I shared some of this sentiment in a @WSJ article a few months back

Apr 17

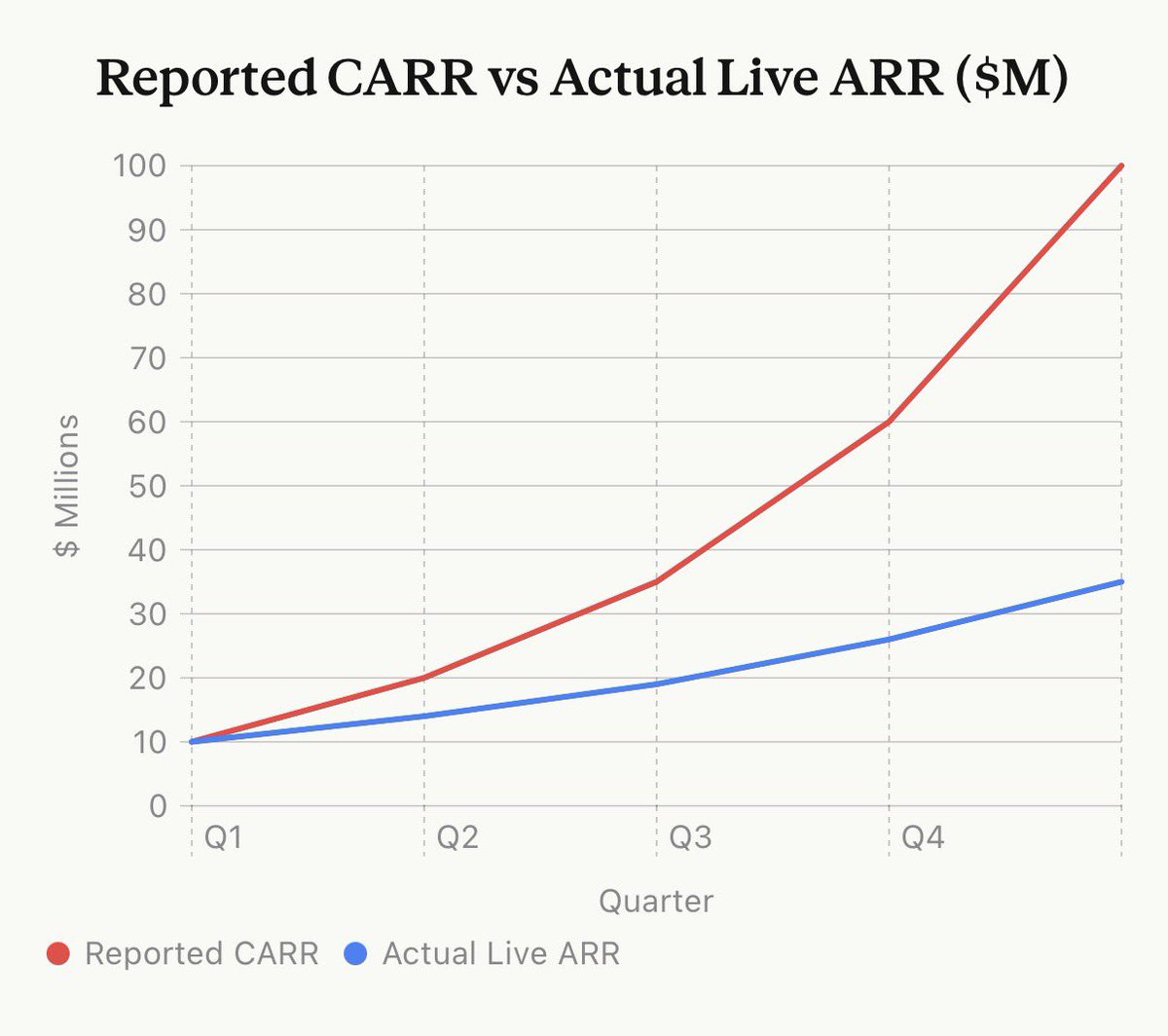

It’s time to expose a huge scam in AI startups: Contracted ARR

The reason many AI startups are crushing revenue records is because they are using a dishonest metric

The biggest funds in the world are supporting this and misleading journalists for PR coverage.

The setup: Company signs 3-year enterprise deals. Year 1 is discounted (say $1M), Year 2 steps up ($2M), Year 3 is full price ($3M).

They report $3M as “ARR” — even though they’re only collecting $1M right now.

The worst part: The customer has an opt-out option at 12 months! It’s not actually a 3 year contract.

In the chart below, by Q5 the company is trumpeting ~$100M “ARR” to press, while actual cash-generating, in-effect ARR is ~$35M. That’s ~3x inflation.

On top of this, enterprise AI companies are bundling full-time “forward deployed engineers” into deals massively reducing margins, sometimes producing Year 1 negative margins.

At some point customers are going to start triggering their opt-out clauses or aggressively negotiating down Year 3 pricing.

And a wave of enterprise AI companies may collapse.

9

10

73

30,048

Melia (Robinson) Russell retweeted

Mar 25

Two of the perks of working at @synthesiaIO are that you get to be around very smart people who are curious enough to try things for themselves, and that you get to see how generative AI is applied to build amazing experiences that weren't possible before.

A story in @BusinessInsider that's out today brings both to life. Our general counsel, Gabe Stern, spoke to @meliarobin about a Video Agent he created to handle the mundane parts of a commercial conversation: businessinsider.com/synthesi…

This is, of course, a great proof point for how versatile our new agentic products are, and how they can be easily applied to create new enterprise apps (Gabe built the agent in just a few weeks). But it also says something much more important about the kind of company Synthesia is becoming, and what AI means for the enterprise space.

With this technology, great ideas will not be confined to just one function. Given the right tools and platforms, talented people will find new ways of applying technology to be more productive. In other words, they will work better, and do more with more.

The second thing it says is that we are living through a shift in what software can actually do. Not long ago, most teams used software to store information, move tickets, and automate workflows. Now we are starting to see AI participate in interactions that used to depend on a person being present for every step of the conversation.

That is what makes this moment so exciting for me. We are able to watch AI move into forms of work that were previously out of reach, and that is a big part of the energy at Synthesia right now.

3

3

9

800

Palantir HQ! Zuck mansion! Crypto bros! Miami is back, baby. .. ... ?

9

12

1,203

Alligators may be all around in Miami, but unicorns are hard to find. Now, though, there is a Karp. businessinsider.com/miami-ne…

1

4

324

Melia (Robinson) Russell retweeted

Feb 5

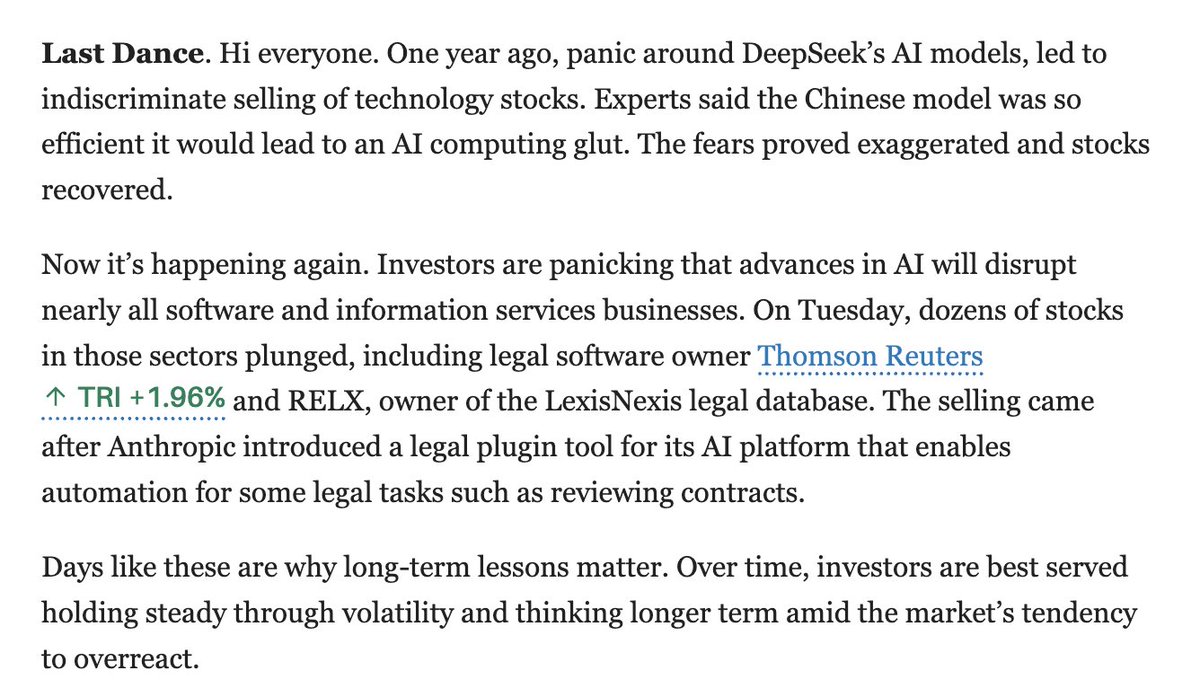

Just like DeepSeek last year, Tuesday's market meltdown appears to have been sparked by a RIDICULOUSLY false and misleading narrative that media outlets spread without applying ANY critical thinking, fueling sensationalism and panic.

Great job everyone. You guys are terrible and awful. Have some decency for your readers.

Read the first screenshot, then what I wrote today:

7

24

191

95,558

Melia (Robinson) Russell retweeted

Feb 5

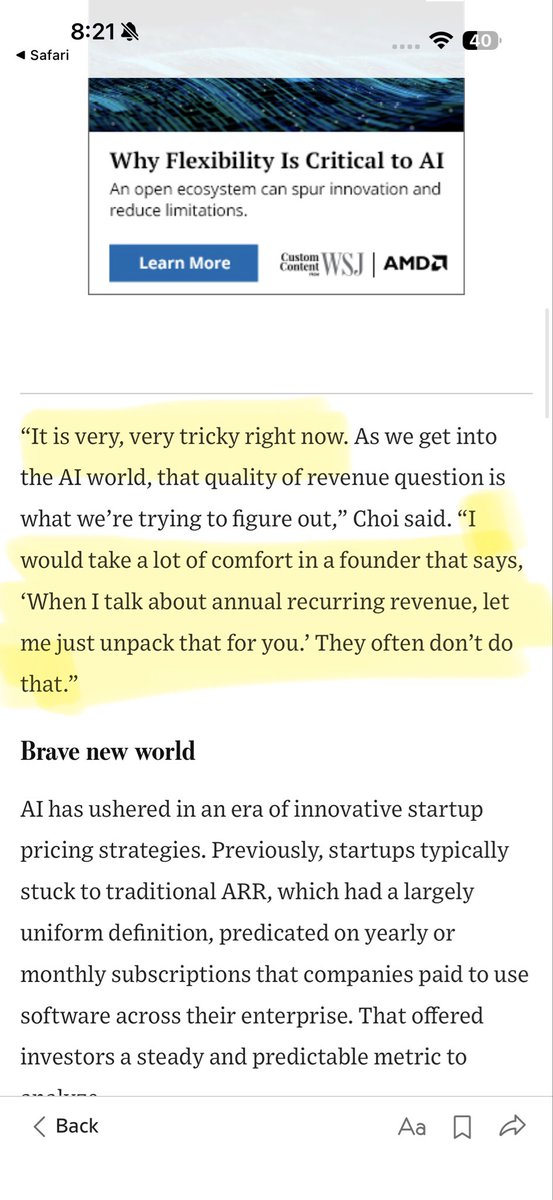

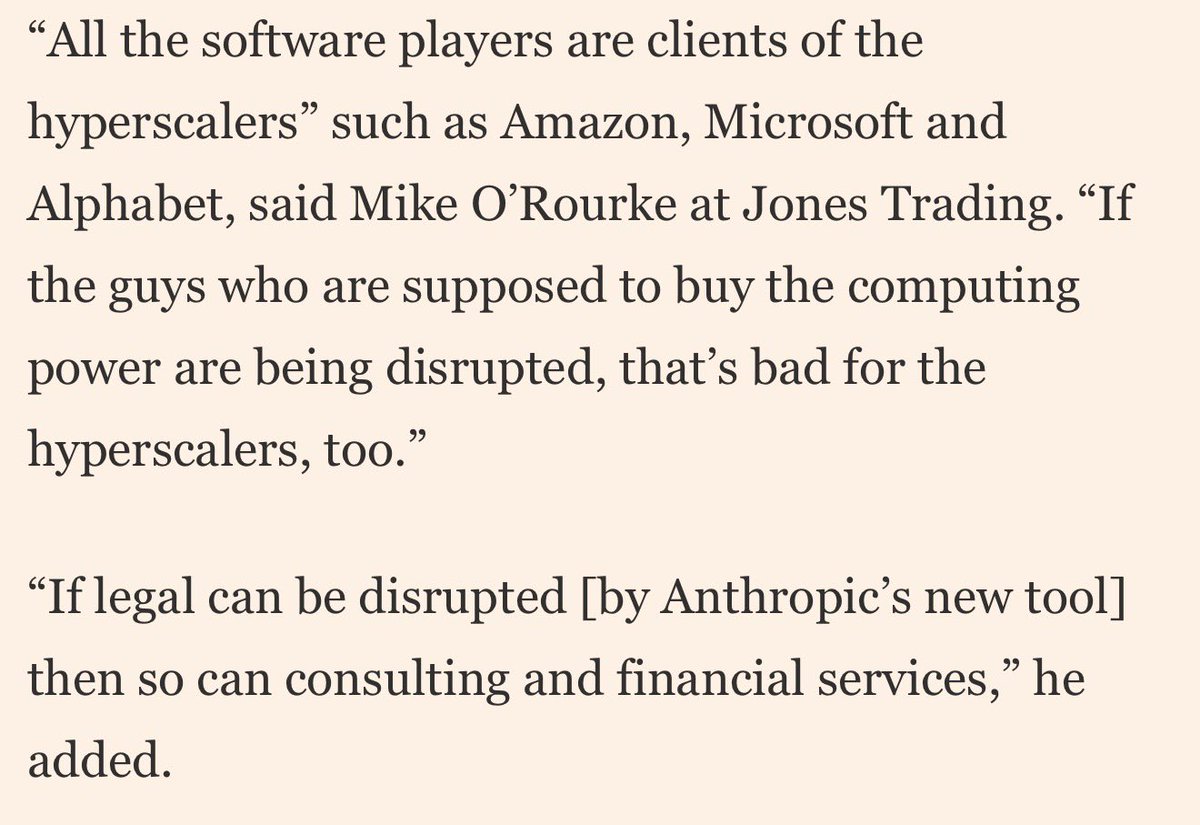

Love this article by @meliarobin. @AnthropicAI's latest plugin has awoken the world to how tech is going to change legal.

There are three categories of legal tech:

1) selling into law firms

2) selling into in-house legal teams

3) going direct to users and provide services.

@soxton is in category 3. We directly provide legal services to startup founders and remove incorporation, employee contracting, customer contracts, and more from the plate of founders. $20 a month and $100 for most contracts.

If you work in legal, it was hard to open LinkedIn over the past 24 hours without running into a wall of hot takes about Anthropic's new plugin. bit.ly/4byC5TT

3

1

9

1,178

Melia (Robinson) Russell retweeted

Feb 3

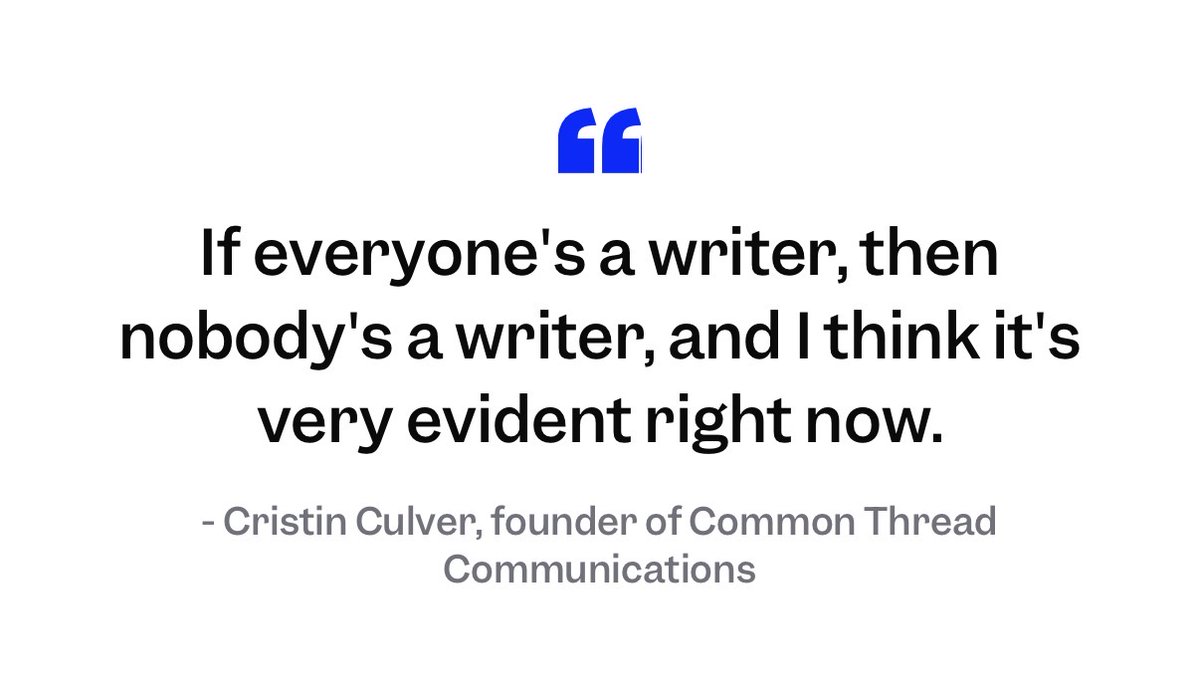

The AI slop era has made actual writing rare enough to be *very* expensive again.

Tech companies are paying $400K for comms roles, because everyone can generate words now, but very few can make them stand out and matter.

Thanks to @BusinessInsider for including my perspective

3

2

10

830

Melia (Robinson) Russell retweeted

Feb 4

Very happy to see @angelesahr on this @BusinessInsider list of venture’s rising stars. We’re all gonna wind up working for her one day.

She’s built a phenomenal network and POV around deep tech and hard underwriting. @slow is lucky to have her.

8

3

70

13,970

What can I say? I love my job

9

1

151

26,334

Melia (Robinson) Russell retweeted

Jan 23

Legal tech is entering its consolidation era, and @meliarobin Russell captured it perfectly in this Business Insider piece.

ALT Melia Russell covers Pincites’ acquisition by Filevine in Business Insider

1

3

4

874

Melia (Robinson) Russell retweeted

25 Nov 2025

I spy @loganbrown799 as the lede in @meliarobin's very good piece "New York is the San Francisco of legal tech" 👀 businessinsider.com/new-york…

3

14

3,024