Blessed husband/father, Buckeye/Reds fanatic. Founder/CEO @ 1903 Group Author of Screen Wars and State of the Screens.

Joined April 2008

- Tweets 9,952

- Following 384

- Followers 2,339

- Likes 4,599

1,090 Photos and videos

Pinned Tweet

30 May 2024

I am incredibly grateful to everyone who supported my book launch last week. We hit best seller on Amazon and exceeded my wildest expectations.

None of this would be possible without you!!!

screenwarsbook.com/

6

1,318

Michael Beach retweeted

Jun 13

A reminder of why SpaceX even exists in the first place:

waitbutwhy.com/2015/08/how-a…

30

47

639

81,261

Michael Beach retweeted

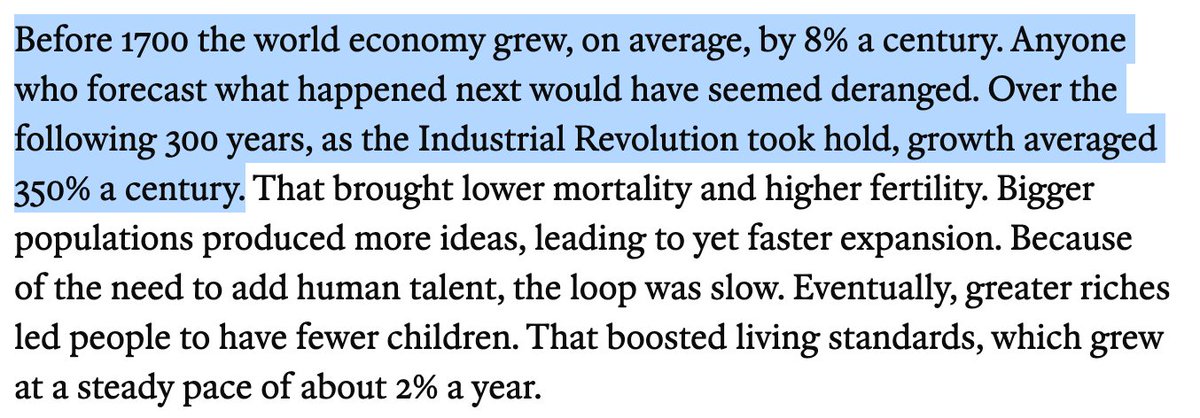

If you zoom out, we are still so early

Alex Sacerdote has spent twenty years studying S-curves

He says AI is the biggest one, and it has barely started:

- "Hundreds of millions of people are using AI. They're just using AI 1.0, which is like a search engine on steroids."

- "Sundar Pichai said it's ten bips (.1%) of the knowledge workers of the world."

- "The enterprise application AI market is less than 1% penetrated."

- "So it's classic S curve where these are the tinkerers, and then it's gonna go to the early adopters, then it's gonna go to the early mainstream.

- "You're going to go from .1% to 1% to 5% to 15% percent in the next four years."

- "We're at ten basis points of people really using AI, and there's not enough compute in the world.

- "We have this infrastructure layer S-curve, which we think is 10% penetrated. We think it's still one of the best ways to play AI."

- "Marc Andreessen (@pmarca) said in the next four years, one thing he's sure of is there's not gonna be enough compute."

- "We've been lucky that we've had Internet 1.0, mobile, cloud, e-commerce, and now AI, which we can confidently say is the biggest, and all these things build upon one another."

- "The rewards are the highest, because we're talking about a market in the trillions –– we now think three to five."

- "But what's amazing about AI is you just, at least with consumers or even business, you just open up the browser and it's there.

- "We talk about S curves, we call this a backward L curve, just straight up."

image source: @damianplayer

My conversation with Alex Sacerdote, founder of Whale Rock Capital Management.

Alex runs more than $17B and has been one of the best performing tech investors for years, though he keeps a low public profile.

As you'll hear, he is singular in how he thinks about investing through technology cycles.

For over 25 years, he has built his entire investment framework around a single idea, the S-curve.

We discuss:

- The AI L-Curve

- When to buy into an S-curve and when to sell out

- The de-commoditization of data center hardware

- Why he went net short software

- His two models for tech adoption

- Finding alpha

Enjoy!

Timestamps

0:00 Intro

9:55 AI's L-Curve

19:31 Whale Rock's S-Curve Playbook

26:14 Spotting Inflection Points

32:02 Finding AI Winners

40:04 AI vs Software

48:13 The Hardware Renaissance

58:04 Why Investors Miss AI

1:05:18 Whale Rock's Research Machine

27

70

555

113,567

Michael Beach retweeted

🤯

Jun 4

Today, Anthropic engineers on average ship 8x as much code per quarter as they did compared to 2021-2025.

2

3

23

7,800

Michael Beach retweeted

May 22

Who wants to make a competitive bid on LiveRamp?

May 22

LiveRamp founder @auren comes on the pod and explains How to Make LiveRamp Great Again.

youtube.com/watch?v=wYXNhqZz…

2

2

15

3,343

Michael Beach retweeted

May 18

What every voter and apparently, the NY Times Editorial Board, should know about housing policy:

1. Rents reflect the balance of supply of apartments and demand for those apartments in a given area. That’s it; there’s no magic. If you want lower rents, you can hope for a recession that destroys jobs and, therefore, demand. Or you can add supply.

2. There is no amount of money that any big city government could feasibly spend that would add materially to supply. This is because, depending on the location, new apartments cost $250,000-1,000,000 to develop… building even a few hundred of those starts to stress any city budget, and many big cities need tens or hundreds of thousands.

3. On the other hand, investors (including pension funds and endowments, insurance companies, rich families, etc.) can collectively **easily** provide enough capital to build as much housing as we need **so long as they are confident they can get a reasonable return**.

To get those investors to fund the creation of the housing our society needs, we must do two things:

1. Dramatically reduce the time & complexity associated with securing governmental permission to develop housing. This means reviewing and simplifying the overlapping regulations that constrain housing production: zoning codes, building codes, parking, ADA, etc. But it also means changing the cultures within the relevant governmental agencies from “default no” to “how can we help you?”.

2. Provide certainty around on-going regulation of apartment operations.

The way investors get a return from building rentals is as follows: They hire managers to lease the apartments, collect the rents, pay operating expenses and any mortgage payments, and then send the investors the cashflow that remains.

But governments all over the country have been restricting the manner in which apartment buildings can be operated in all kinds of ways.

For example: Cities have been making it harder to screen tenants, while also making it much harder to evict tenants who don’t pay. You can see why both of those measures are politically popular. After all, who doesn’t want people to get second chances? And who wants anyone to get evicted? But, as a manager, the combination of those two regulations makes it much harder to predict, with any certainty, that the rent will get paid… and that makes it very difficult to get investors to provide capital to create more housing.

Another example: Rent control. Again, I understand why renters love rent control and why politicians want to give it to them. But, if, as has been the case in NY, LA and San Francisco, city governments hold annual rent increases below the rate of growth in the operating expenses of the buildings, the cashflow payable to the investors shrinks… making them much less likely to invest capital in building more apartments.

In conclusion: For ~every other good or service in the economy, we allow the market to function, and the result is that we have a surplus of choice at all price points (think of food or clothes or cars), which is spectacular for the consumer. If we want a surplus of choice at all price points in housing, we need to get comfortable with the idea of allowing the market to provide it.

And that means allowing investors to build rental apartments *and* allowing them to operate those apartments in a manner consistent with making a reasonable profit.

Remember: Every developer of rentals is either a landlord-in-waiting or hoping to sell to one.

74

137

968

160,530

Michael Beach retweeted

May 18

Epic Nerf Wars.

27

49

1,466

89,970

Michael Beach retweeted

May 17

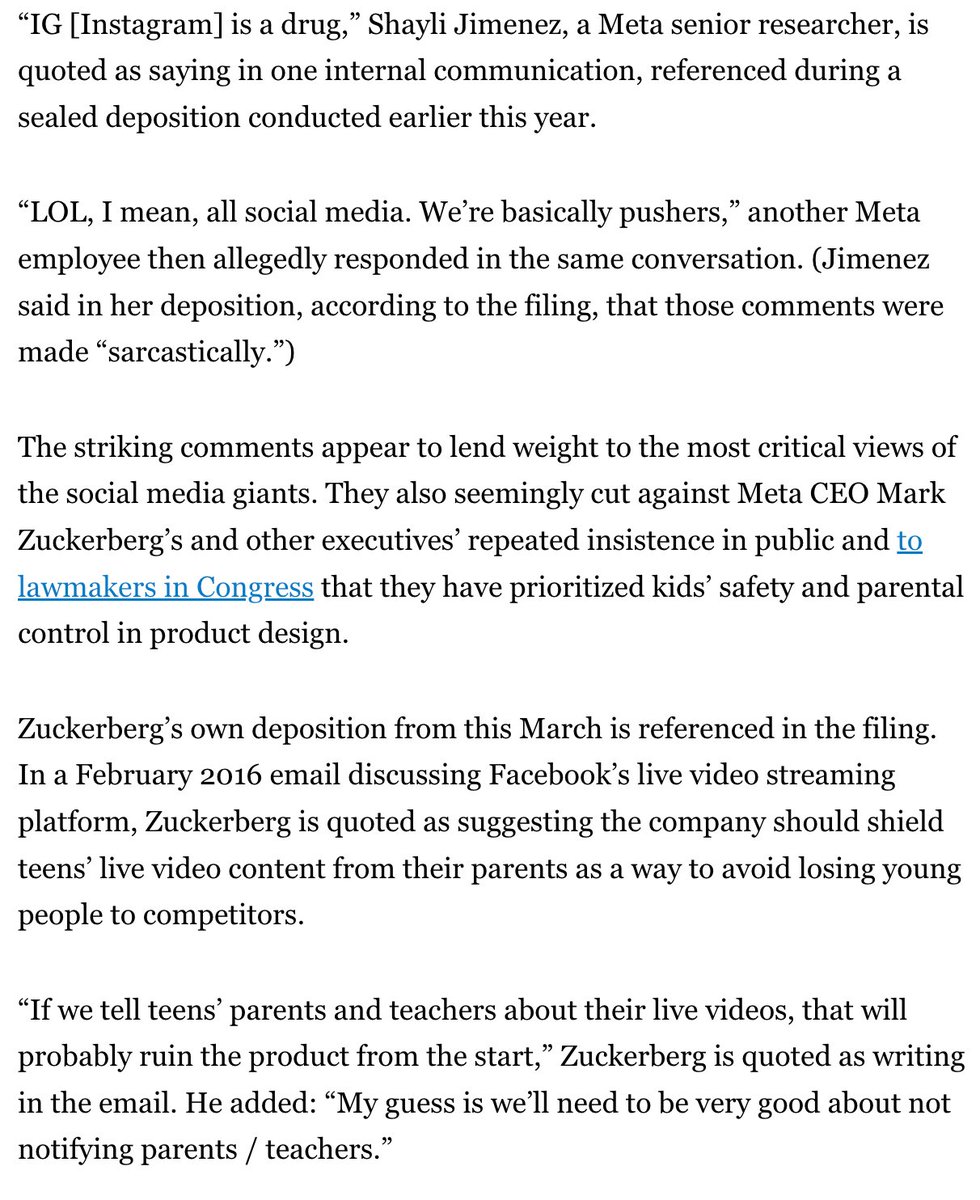

I'm going to get killed for this but I think this is a good idea.

After digging into the data about depression, sleep deprivation and external locus of control in kids who are active on socials early, I'm sold.

Social media as late as possible in life.

35

5

91

16,740

Michael Beach retweeted

May 17

Congrats to LiveRamp and the team for the sale to Publicis. This deal was a steal for Publicis (more on that below).

LiveRamp was a shining gem and still is such an important part of the ad tech and marketing tech industry. It has so many amazing people and has a really incredible product, which has not changed that much over the last 10 years or so. It has bittersweet seeing a company that one created and was a part of for almost a decade go into decline.

But despite that, the company is still in really good position. Unfortunately they were not able to take advantage of their position. For the last decade they traded long-term positioning for short-term gain. That trade resulted in the ire of their customers and even more so their partners.

Now that they will be in a new home in Publicis, I hope that we will see a renaissance of LiveRamp and LiveRamp will continue to be an incredible part of the industry going forward.

The company has a lot it needs to do:

It needs to focus on the core product. The core product is 70% of their revenues and 500% of their profits.

They need to focus on making that product better. The core product really hasn't changed in about a decade.

They have to focus on making the middleware product better: making it easier to use, making it so you can onboard partners faster, onboard customers faster, onboard connections.

the most important LiveRamp metric The number of connections per customer is the most important metric for LiveRamp. That number is surprisingly low.

Most customers only have a small number of connections using the LiveRamp system, not because they don't want to use LiveRamp but because either LiveRamp is way too expensive or takes too long or it's too bureaucratic or too burdensome (or usually all of the above). Now that there is going to be new ownership of LiveRamp, hopefully they can focus more on the product and customers can go from, let's say, 10 connections in LiveRamp to 400 connections, 500 connections, even 1,000 connections. That's how we know LiveRamp is really doing a good job.

Also the next way we know LiveRamp is doing a good job is if they can increase the number of customers. Today most of the customers that use LiveRamp are quite large ... which is great. They have still the largest B2C customers in the world. It would be amazing if everybody can use LiveRamp: mid-market companies ... even small companies (would be awesome to have a self-service system).

all that said, I'm long the core engineering team and product team of LiveRamp and LiveRamp's position in the market. This deal was a steal for Publicis. It was a great deal for Publicis, assuming they can even make LiveRamp a tiny bit better. this definitely could be a deal that transforms Publicis. There's no reason why LiveRamp can't be a $100 billion market cap company by itself. It should be. It should have that position. It should be well over $100 billion and with the right product vision. it can get there. Let's make LiveRamp great again!

19

7

114

34,460

Michael Beach retweeted

May 15

this is the kind of messaging you craft for public education when you believe the purpose of public education is giving unions money rather than educating children

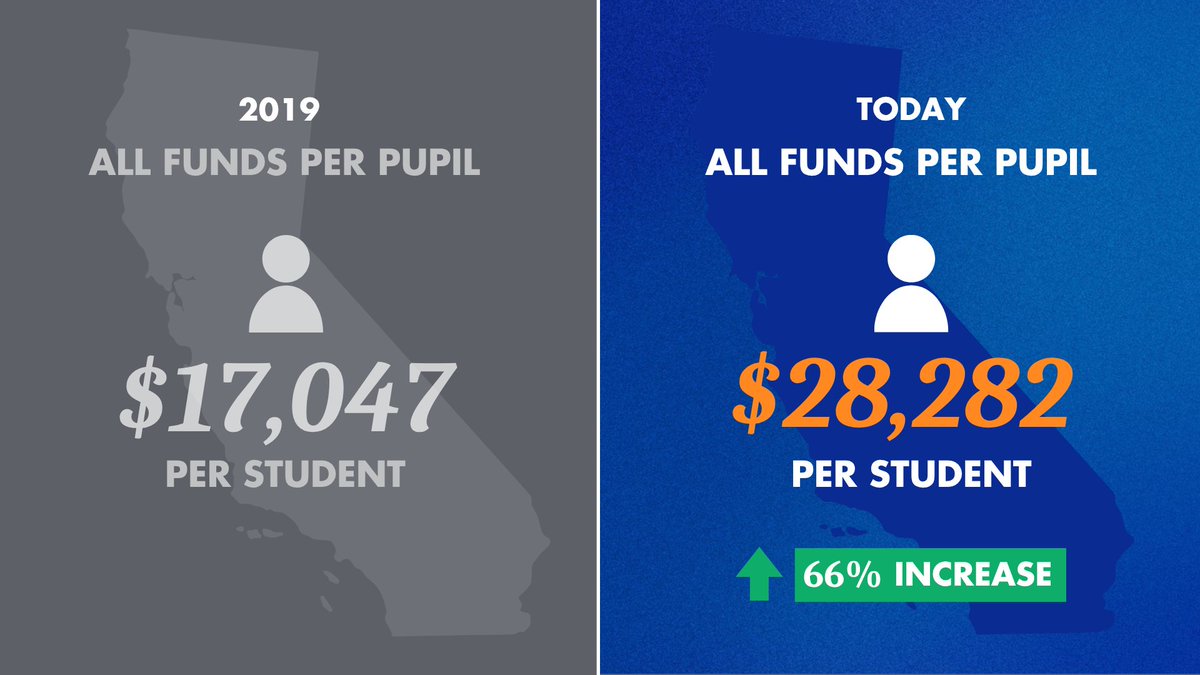

Student funding in California is now a RECORD HIGH! Since Governor Newsom took office, it’s increased 66%— reaching $28,282 per student as the state makes historic investments in public education.

34

259

2,710

69,159

Michael Beach retweeted

1

2

26

Michael Beach retweeted

May 11

Fox’s quarterly

revenue falls (no Super Bowl)

earnings rise (no Super Bowl)

1

3

15

3,234

Michael Beach retweeted

Pete Rose once texted @CoachUrbanMeyer about Braxton Miller and ... you know what, just listen to the story.

1

18

269

36,071

Michael Beach retweeted

The @NFL’s media rights re-negotiations may prove so costly that it results in a “7% cut to scripted TV, film, and every other sport,” per @michaelbeach & @xscreenmedia.

2

5

14

6,769

Michael Beach retweeted

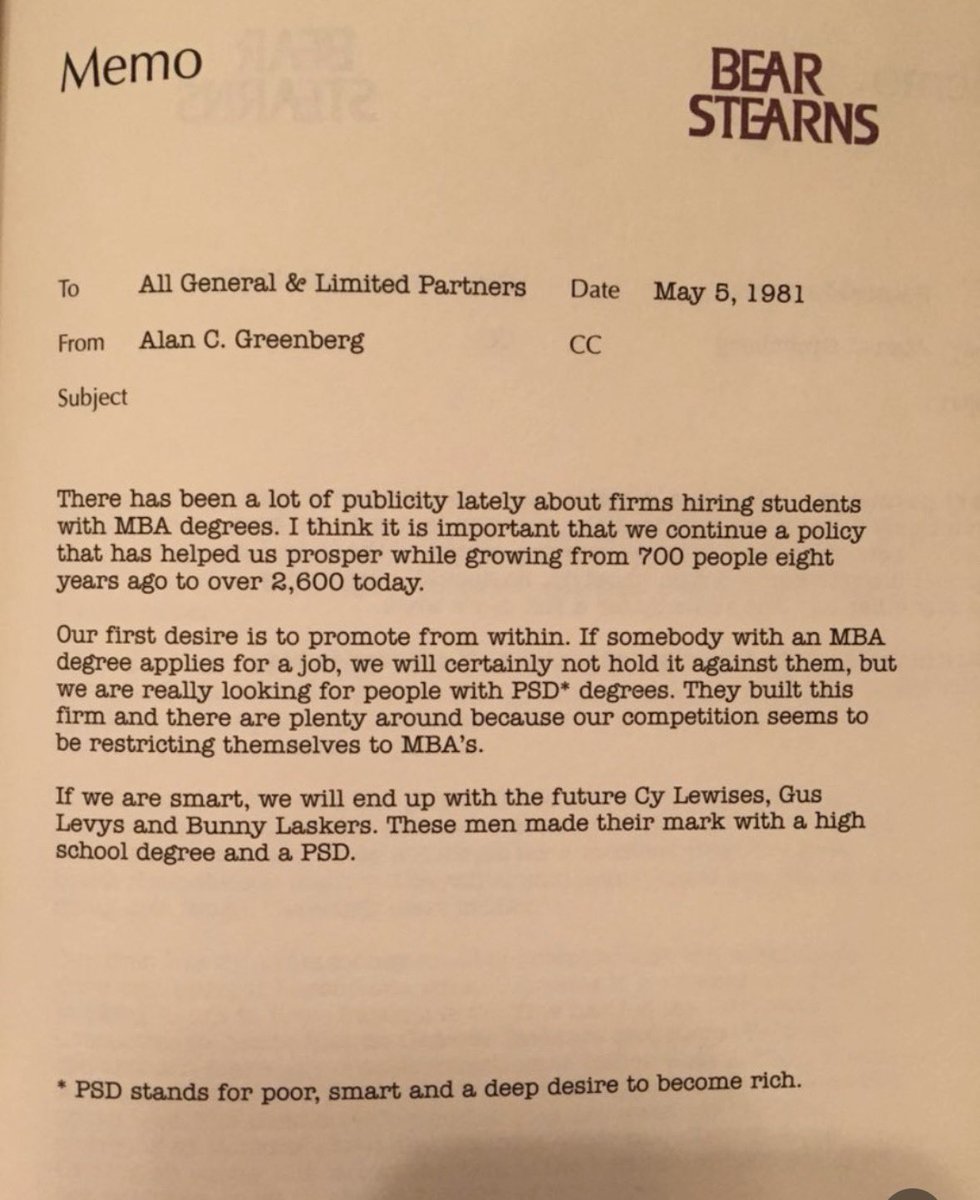

One of Alan Greenberg’s best memos

On who to hire

5

37

219

23,654

Michael Beach retweeted

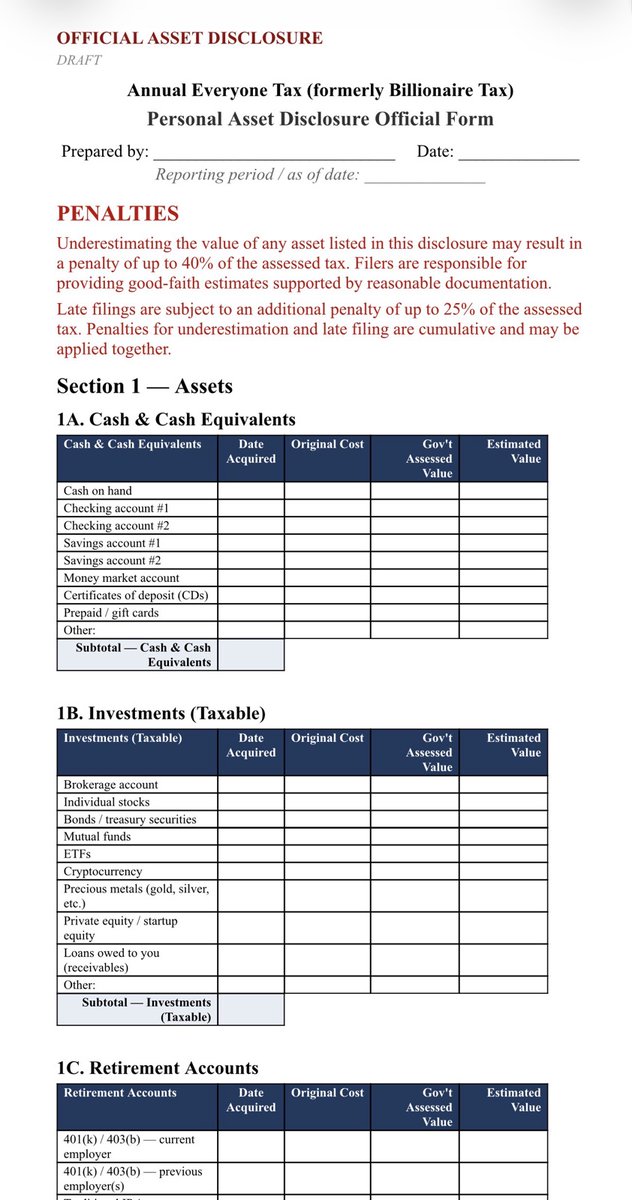

Apr 27

As you go to work today and settle into the week, please study the form below. You will soon need to fill this out EVERY year and tell the government what you own and then allow them to tell you how much its worth.

That is the framework that is enabled by the Trojan Horse "Billionaire Tax" that is trying to get passed.

Give them credit: they cleverly use Billionaires as the hook, but build in the language and the framework that will allow the Legislature to simply extend the tax to everyone and make it yearly.

And this is where the form below comes in...

In this case, ask yourself, will it be you or the Billionaires that will be able to fill this out properly and avoid penalties.

As much as Billionaires can be pushed to do more for society, we all know that they have the infrastructure to manage these kinds of disclosures...middle class Californians do not and they will be the ones that get penalized in the end.

1,171

3,910

12,557

2,552,896

Michael Beach retweeted

Apr 23

𝙇𝙚𝙜𝙚𝙣𝙙𝙖𝙧𝙮 𝙁𝙚𝙗𝙧𝙪𝙖𝙧𝙮

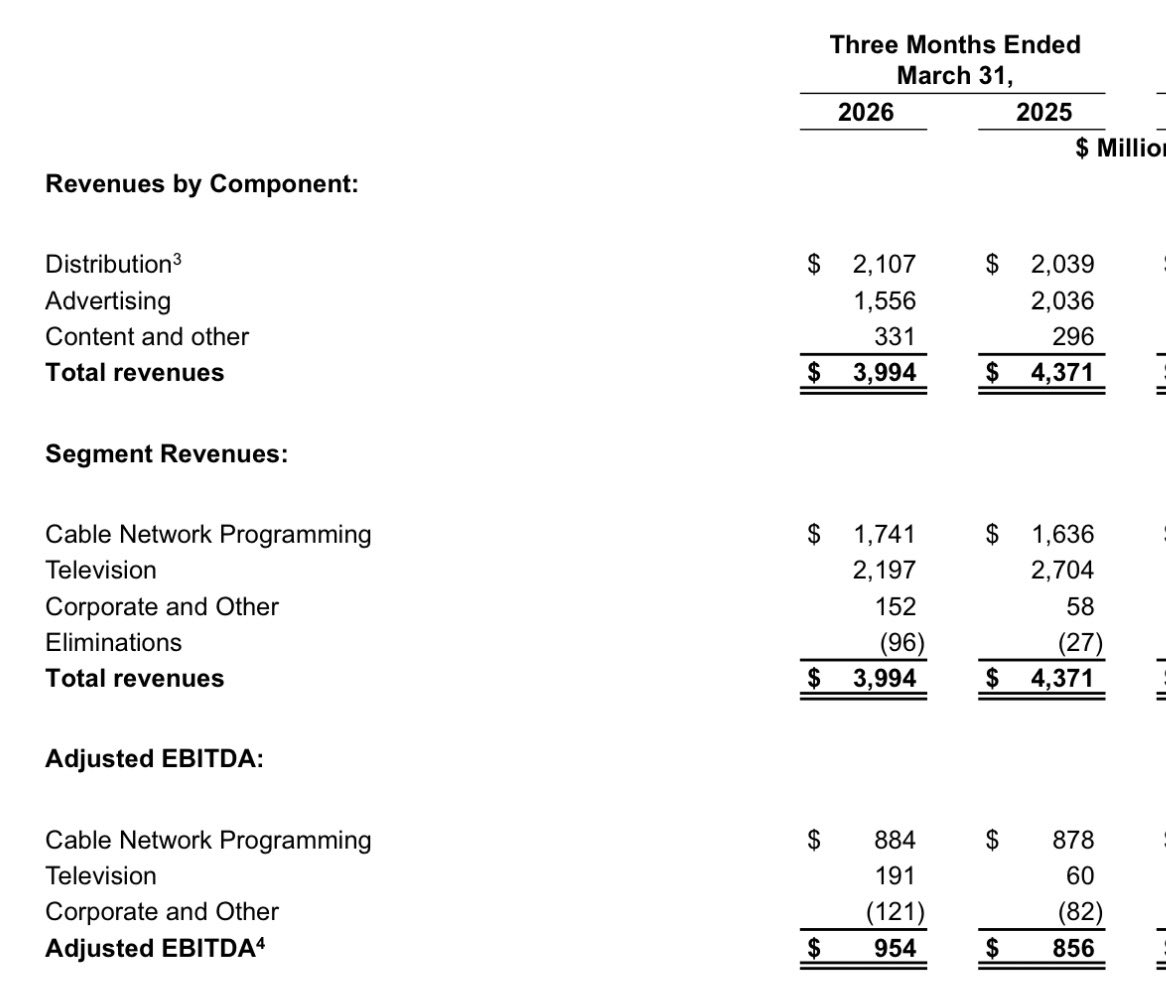

Comcast’s Media business (NBCU) EBITDA swings to a $426 million loss in Q1 ‘26 from a $107 million profit in Q1 ‘25.

Puts all those breathless reports of Super Bowl and Olympics ratings in perspective.

1

7

21

3,635

Michael Beach retweeted

Apr 20

With draft week upon us, we look at the schools that have produced the most first rounders in the NFL Draft 👀

63

236

1,273

210,724