research @rwa_xyz • ex-banking, PE, real estate • whisky & writing • our time is now

Joined March 2012

- Tweets 1,026

- Following 420

- Followers 552

- Likes 6,325

83 Photos and videos

Pinned Tweet

9 Jun 2025

I joined @RWA_xyz : A Personal Memoir

When I started in investment banking, our analyst class often wondered aloud about life after banking. Between the spreadsheets and sleepless nights, speculating about our afterlife was the only way to stay sane.

Some dreamed of climbing the Wall Street ladder. Others wanted out entirely. I knew finance wasn’t for me long-term but couldn’t articulate what I was looking for. “I’ll know when I see it.”

Eventually, I stumbled into crypto and quickly went down the rabbit hole. Stablecoins, tokenized assets, and the promise of rebuilding financial infrastructure. It was an optimistic bet on the future, and I was fully bought in.

Deciding to leave finance for crypto wasn’t easy. At times, I felt like sailing off the edge of the world. But sometimes you have to get lost to actually move forward. And the yellow brick road led me to @adamlawrencium and @CharlieYouAI.

Adam and Charlie were building a data analytics platform at the intersection of everything happening in real-world assets. What struck me most wasn’t just their expertise, but their genuine belief in the tokenization revolution and the product they were building.

I knew I had found it. And it wasn’t long before I joined their mission.

I want to thank Adam, Charlie, and the team for believing in me and bringing me here. I truly feel like I’m standing on the shoulders of giants. And I’m grateful to be part of this journey.

Top to bottom, @RWA_xyz is about excellence, is about greatness. And you have my pledge that I will carry forward that standard.

Thank you, and let’s keep building.

8

44

3,037

Minerva retweeted

May 28

Stream, Resolv, Elixir, and Kelp all broke 1:1 redemption within months of each other. Everyone assumed resulting shortfalls get socialized evenly but it never does (except when Aave bails everyones ass out).

On the Lending Market side:

It's all about speed. The fast money withdraws while it still can, so the loss piles onto whoever's left in the market when things freeze. Slowest out eats it, quickest out walks.

On the Asset side:

It's a legal race. Sophisticated actors that signed side letters before they ever bought (or listed) the asset point a lawyer at their redemption slot and come out close to whole. Everyone else gets crushed.

Same result both times. Bad debt finds the weakest reflexes and the weakest legal posture. Whatever protocol docs said becomes a joke.

3

3

32

3,611

I'm assuming this is mostly rage-baiting hyperbole, but it's still worth drawing the distinction here, especially given how new onchain vault products are and how few people have actually looked under the hood.

The hedge fund comparison breaks down at the part that actually matters, which is custody. A fund manager holds your assets and moves them around at their own discretion. A Morpho vault curator never touches the deposits at all. The smart contract holds the funds, the protocol enforces the rules, and the curator only sets parameters. We could disappear tomorrow and your money would sit exactly where it is, governed by code anyone can read.

And it goes further than custody. The Guardian role on our @SteakhouseFi vaults isn't us, it's the depositors, all of them in aggregate. If Steakhouse proposes adding a new collateral, any depositor can start a vote to veto it, and we set the quorum deliberately low so it only takes a small fraction of them to block it. Nothing gets slipped in behind your back. New collateral sits behind a timelock, so if you don't like what's coming you can either help vote it down or just withdraw before it ever goes live. You would have to wait until the next investor update to learn about mandate drift in a hedge fund. Here you get a vote and an exit before anything changes.

What curators configure is asset backed lending, with transparent and strongly enforced constraints. Every position is a loan against posted collateral, with a published liquidation loan to value, a named oracle, a defined rate model, and hard supply caps. It's hardly a black box though I concede it can be hard to parse and compare. It is, however, evidently not opaque.

Compare that honestly to a credit hedge fund. There you get a quarterly letter, marks you can't independently verify, concentration you can't see, unilateral discretion, and a manager who is literally holding your money. With a vault you get every loan, every allocation, every realized loss, and every fee, live, queryable by anyone, enforced by code instead of promised in a pitch deck. It's not less transparent than a fund. It's dramatically more.

You are right that the data can be scattered and that nobody has fully packaged it yet. That is absolutely a frontend and user experience problem. We also believe it is eminently fixable and our philosophy is to show our work and maximize the constraints we operate our vaults with.

The reason we build onchain is to put more transparency into a system that has spent decades getting good at the opposite. We're not perfect and there's considerably more that needs to be done to achieve that, but we believe we're on the right trajectory.

May 27

If you really think about it, vaults are effectively hedge funds run by curators

> Users deposit capital -> receive vault shares -> curators allocate funds and charge mgmt fees on AUM and carry on returns...sounds like a fund product to me

> I’m all for simplifying defi, but nuts that protocols present these products on their frontends to users without any of the disclosure you’d expect from a manager stewarding billions: track record, realized losses, methodology, conflicts of interest, etc.

> Fwiw most curators are good actors offering valuable services, but the fact that users need to sleuth on-chain and hunt down scattered info to diligence a product presented as a "vault" feels like a giant landmine hidden in plain sight

6

15

76

11,383

Minerva retweeted

May 27

This is the time of year when a lot of investment firms welcome interns. While our work is geared toward institutional investors, a lot of it can be useful for learning about markets and the investment process. Here are a handful of reports and how they can guide interns:

26

332

2,684

417,221

Minerva retweeted

Apr 23

It was 1am during one of several all-nighters I pulled working on a complex cross-border finance deal. I was a first year associate at Debevoise and the senior associate on the deal strode into my office and dropped off some markups for me to process. She flipped to one of the 27 sets of signature page packets I had prepared and pointed emphatically at one of my mistakes, which she helpfully encircled using half a red Bic's worth of ink. In one of the signature blocks, I spelled the entity name as "ENTITY HOLDINGS, INC." when in fact it should have been "ENTITY HOLDING, INC."

"Clients pay us what they pay us so they can sleep soundly knowing that we will execute with dogged perfection" she explained. The smallest mistake, however insignificant, was an indicia that the higher stakes elements of the deal may not be airtight either. And that would be fatal to a client's confidence in your work product. The craft was the craft, regardless of whether it was a critical covenant or an entity name on a signature page.

13 years later I still think about that night. It's easy to dismiss the tasks of a junior associate as valueless, menial grunt work, but the unglamorous work compounds in counterintuitive ways. Checking and rechecking section cross-references, tracing through a maze of nested defined terms, and yes--compiling signature pages--were often forcing functions to do more important things like *actually* reading a complex contract from top to tail. Over time, these thankless tasks built a rich latticework of mental models and a pattern-matching library that to this day I draw upon when facing new and unusual legal issues. Even when using AI (which I do every day), this decade-long scaffolding of knowledge I've cultivated helps me ask the right questions, prod with the right followups, and curate and assemble the best answers. I'm sure, just like generations of old men futilely yelling at clouds before me, I'll be proven wrong, but man, I'm worried (and a little sad) for the new generation of lawyers.

21

36

423

214,043

Minerva retweeted

Apr 22

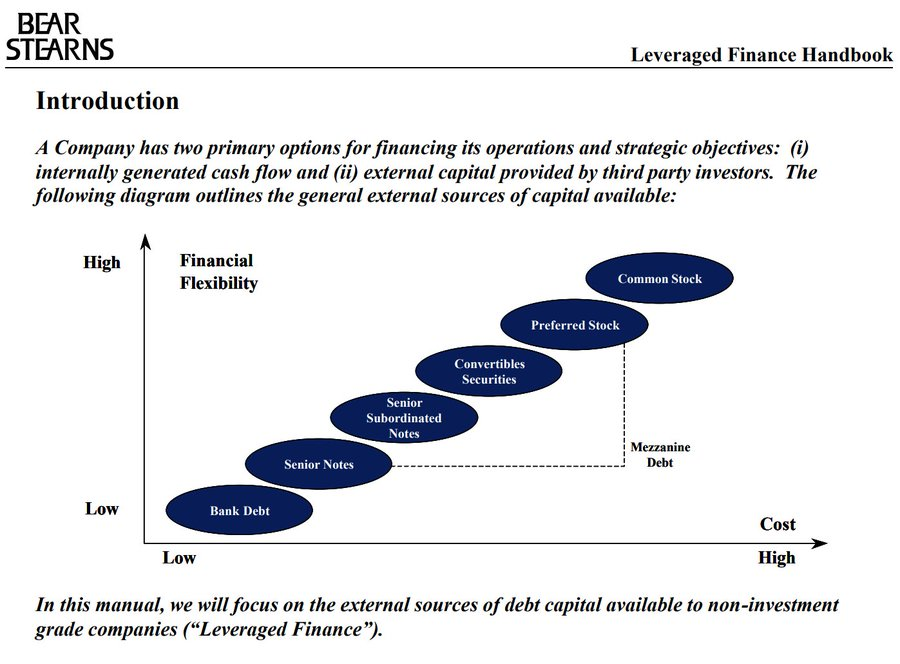

If you are looking for a primer on leveraged finance, restructuring or credit investing concepts, this thread is for you

Few fantastic slides from an old leveraged finance handbook by Bear Stearns

🧵

1/ Introduction to leveraged finance

10

92

894

131,707

Yesterday, a short-seller released a number of allegations surrounding Figure. While we address them below, our focus hasn’t shifted. Today we’re back to executing our goal of building the next-generation of capital markets on blockchain rails.

1. Figure’s loans are not truly originated on the blockchain

Figure has a growth and margin profile that stands out materially amongst lenders. This is related to the differentiated technology and processes we use in our marketplace. As to the short-seller’s claim, even as they acknowledge, Figure has described in full its use of blockchain in its SEC filings.

The shortseller’s claim reflects a misunderstanding of how blockchain is integrated into the Figure loan lifecycle. While certain legal steps (particularly for HELOCs) require traditional documentation to comply with existing regulations, from the moment a loan is funded it is represented on blockchain and all subsequent ownership transfers and pledges are recorded and executed through our platform.

Participants in our ecosystem are contractually required to transact on blockchain, making it the operational system of record for loan ownership and activity, while traditional documents serve primarily as legal formalities. Our Digital Asset Registration Technology (DART), which is used by major Wall Street banks including Goldman Sachs, Barclays, Deutsche Bank and Jefferies, further automates lien tracking and updates based on blockchain transactions, improving transparency, reducing operational friction, and mitigating risks such as double-pledging. This hybrid structure reflects the realities of today’s legal framework while still delivering the core benefits of blockchain across the asset lifecycle.

2. The benefits of the blockchain are fabricated and overstated

Ultimately, the benefits of our technology and marketplace are borne out in the growth and margin profile demonstrated in our financial results. Our use of blockchain is focused on improving the infrastructure behind the loan lifecycle, including data consistency, ownership tracking, and capital markets execution. Blockchain enables greater transparency, reduces reconciliation friction, and supports more efficient transfers and servicing over time that carry tangible benefits.

3. Figure’s underwriting is risky and aggressive

The credit performance of loans in our marketplace reflects a borrower base with strong fundamentals, including an average FICO score of approximately 754, average income of ~$187,000, and a combined post loan-to-value ratio of around 62% (meaning 38% equity in the home at the most recent home value). We utilize a combination of automated tools, including Automated Valuation Models, alongside established credit, income, and collateral verification processes that are consistent with industry standards. While we focus on delivering a streamlined and efficient customer experience, this does not come at the expense of credit discipline, and we maintain robust controls designed to manage risk, prevent fraud, and ensure loan quality across our portfolio, as demonstrated by multiple years of loss rates approximately 1% or less.

4. Figure’s open-ended HELOC misleads borrowers and regulators

Our HELOC product is designed to comply with applicable Truth in Lending Act (TILA) and Regulation Z requirements for open-ended credit, and we provide clear disclosures to all borrowers regarding its terms and features. We actively promote the ability for borrowers to redraw funds as they repay their balance as a key benefit of our product, enabling access to additional liquidity without refinancing. Consistent with the regulatory definition of open-end credit, our HELOCs are structured as self-replenishing lines, allowing borrowers to repay and re-borrow principal without a new application or underwriting, regardless of the initial draw structure. We offer both fixed-rate and variable-rate options to meet different borrower preferences, including payment certainty and flexibility.

5. The performance of loans originated with Figure technology is deteriorating

Our recent financial statements show that the weighted average delinquency rate across approximately $4.6 billion of securitized assets currently outstanding is 0.80%, reflecting strong underlying credit quality across a broad portfolio of loans and contrasting with the selective, cherry-picked statistics presented by the short seller. Comparisons across securitizations must account for differences in vintage and seasoning, as loans that prepay or refinance exit the pool over time, leaving a higher concentration of remaining loans that may include a greater share of delinquencies.

6. Institutional investors are walking away from the platform

In March 2026 alone, over $1.15B of whole loan sales were executed on Figure’s marketplace. Earlier this month (April 2026), a BWIC (Bid Wanted In Competition, e.g. loan auction) was completed on Figure’s platform that resulted in a record low spread to the applicable risk-free rate, reflecting strong institutional investor demand for our assets.

7. Figure misrepresents its balance sheet usage and supports its own marketplace

Figure maintains a securitization shelf such that it manages the registration statements, SEC compliance and rating agency relationships associated with securitization activity of loans originated in its marketplace. Figure Connect participants originate on their own licenses and finance the origination with their balance sheets, and then sell those loans to third parties or into Figure's securitization shelf. The fact that Figure manages the securitization shelf does not mean that Figure is a buyer of loans on the Connect marketplace, it means that an asset management vehicle, which has raised third party funds via a bond offering, does so.

8. The Provenance blockchain is centralized and controlled by Figure

While Figure has been an active contributor to the ecosystem and holds approximately 25% of outstanding HASH tokens, the network is governed by token holders broadly, and key decisions are made through that governance framework. Ownership of tokens does not equate to unilateral control, and incentives across participants are aligned around maximizing the value and utility of the network. We have been transparent about our involvement and, in late 2025, took steps to further support the ecosystem by strengthening the Foundation with committed economic and engineering resources. These actions are intended to promote long-term stability, growth, and adoption of the network, rather than to centralize control.

9. Our Co-Founder has an undisclosed margin-loan arrangement against his FIGR shares

Mike Cagney previously had a secured loan against a portion of his shares, fully repaid shortly after the Figure IPO. As a result, any related pledge is no longer outstanding, and the characterization of an ongoing margin-loan-type arrangement is false.

10. Key insiders are selling stock after the IPO

After founding Figure in 2018 and working without any cash compensation for several years, Mike Cagney sold 1.5 million shares in connection with the IPO. Beyond that, executive sales have largely occurred pursuant to the standard practice of pre-established Rule 10b5-1 trading plans or in connection with the vesting of RSUs, and resulting sales to cover associated tax obligations. This is not discretionary selling tied to short-term views on the business.

12

12

106

18,398

Minerva retweeted

Apr 16

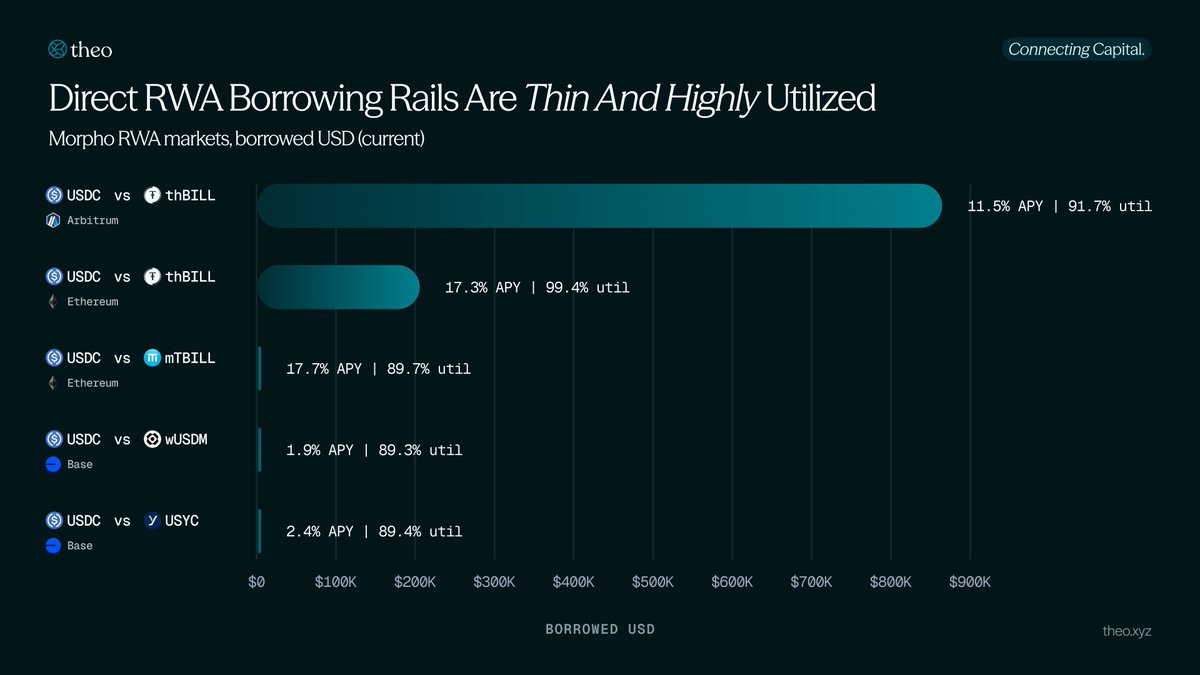

1/ Onchain lending is entering the next generation.

DeFi lending has hovered around ~$35B for two years. Meanwhile, RWAs are bringing sustainable, predictable yield onchain at unprecedented scale. Tokenized treasuries alone have grown 250% to >$13B, with gold, credit, and other fixed-income products right behind them.

The borrowing infrastructure around these assets is already running at 90–99% utilization. Billions in fixed-yield collateral are being funded on floating-rate rails built for a different era.

Over the past year, Aave's USDC borrow rate had a std. dev of ~95 bps. This is fine for leveraged ETH/BTC where borrowers are less rate-sensitive, but inefficient for fixed-yield assets like tokenized treasuries earning 3.3–3.7% in a tight band. As more RWAs come onchain, the volatility mismatch between funding and the underlying asset becomes a binding constraint on leverage.

@Morpho Midnight and @aave v4 are architectural rewrites designed to fix this 🧵

15

12

137

37,173

Minerva retweeted

Apr 11

🚨do you understand what two Anthropic engineers just explained in 16 minutes.

Barry and Mahesh built Claude Skills from scratch.

here's the part nobody is talking about:

> Skills are just folders.

> folders that teach Claude your job.

> your workflow. your expertise. your domain.

Claude on day 30 is a completely different tool than day one.

watch this before you write another prompt.

before you build another agent.

before you touch another tool.

16 minutes. bookmark it. watch it today.

and if you want to learn everything about Claude from scratch the full 4 hour guide is waiting below.

Apr 3

CLAUDE FULL COURSE 4 HOURS

This is the most detailed Claude guide I’ve seen online.

Bookmark this before you forget.

4 hours.

Build tools.

Automate work.

Learn how people build bots and systems.

Claude → Tools → Automation → Products → Money

70

1,238

13,980

5,311,538

Minerva retweeted

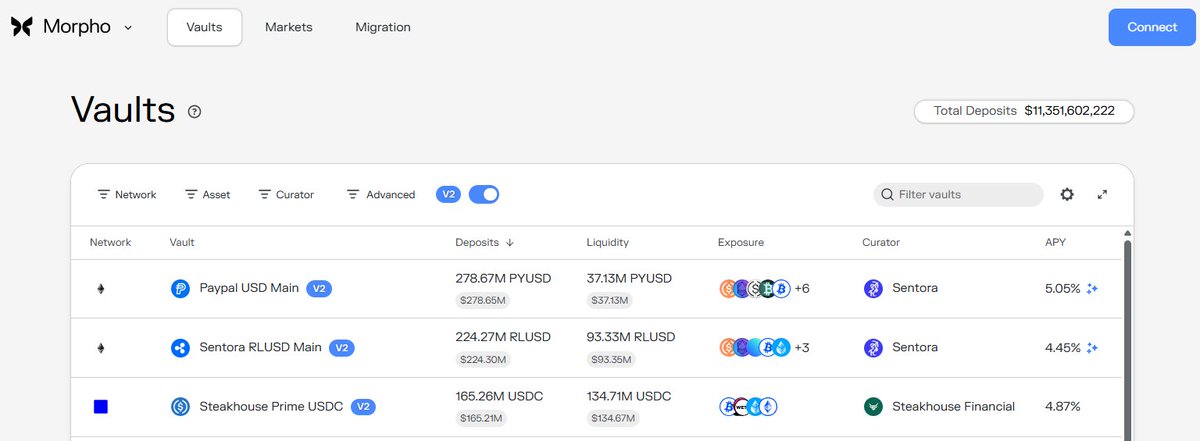

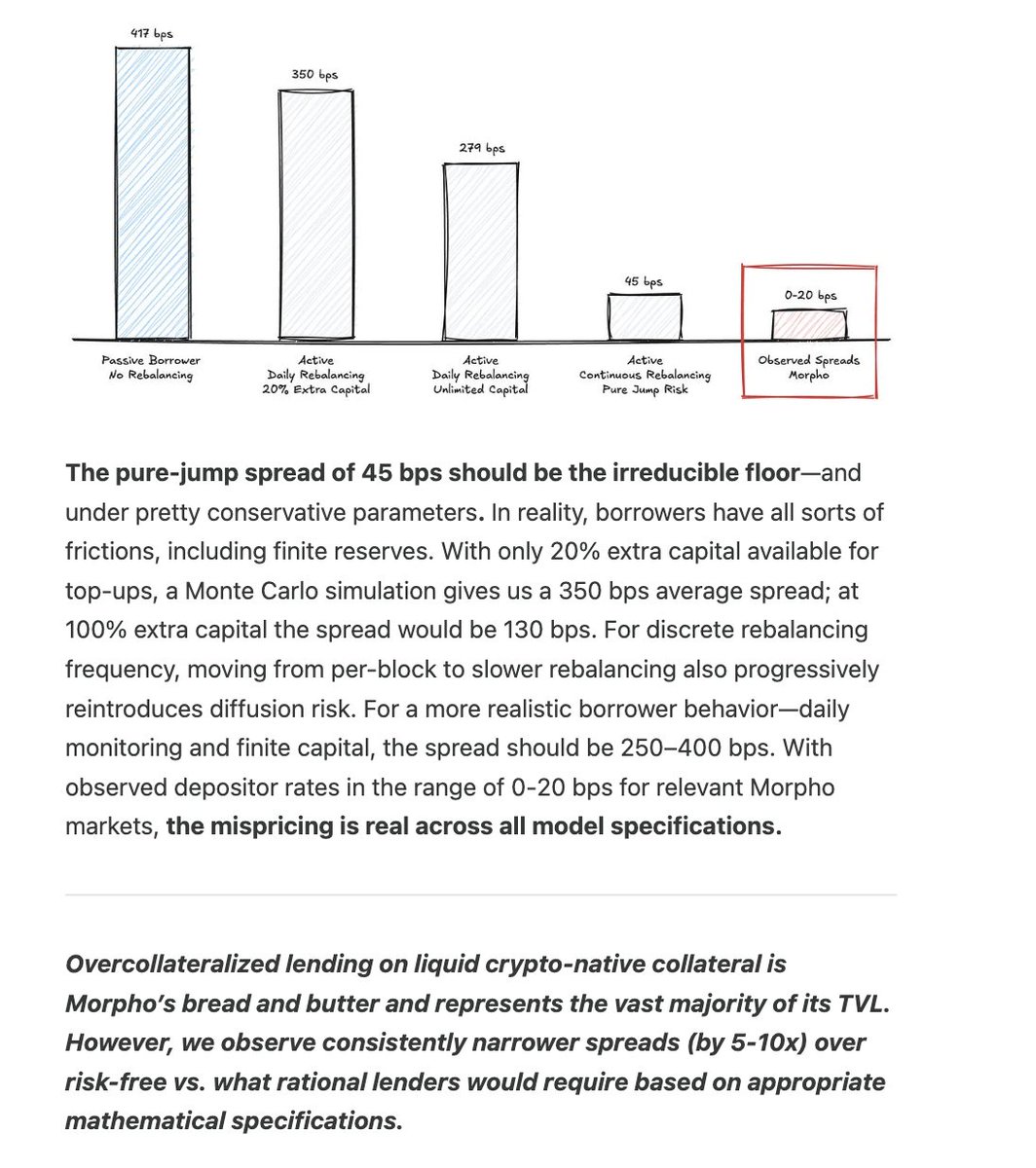

rates in DeFi are too low for the level of risk

$11.7B sitting in Morpho vaults today at 2-4% APY. retail is funding these markets via exchanges thinking it's a savings account. it's not. they're taking real credit risk on crypto-collateralized lending

no institution accepts near risk-free rates to come on-chain

not all vaults are created equal. same 2-4% yield but completely different risk profile (different curators, collateral, LLTVs). retail picks the highest number. farmers will farm

back in the day >100% APYs in DeFi made sense. you were compensated for the risk you were taking.

DeFi is a different animal today but vol, historical dislocations, and looping strategies on crypto collateral still demand at least 300-400 bps above risk-free. we're nowhere near that.

@LucaProsperi ran the math (see below). tldr - fair value spread on ETH/BTC-collateralized lending is 250-400 bps above risk-free. observed rates are a fraction of that

last cycle we saw a lot of retail pour savings into algo stablecoins promising "risk free" yield. this cycle vaults have a lot of demand but they are mispriced for the level of risk. you're trusting someone to LP into vaults and trust the manager will manage position

at least private credit earned you 12-16%

go read this: open.substack.com/pub/dirtro…

104

65

692

152,863

Minerva retweeted

Apr 7

some great risk discourse from @LucaProsperi and @adcv_

Luca reaches the conclusion that defi lenders are significantly underpricing risk vs SOFR, while Adrian counters that defi prime repo markets have very little default risk in practice

generally find myself aligned with Adrian, but with a few caveats:

(1) risk for prime repo is mostly driven by fundamental rather than market risk, and

(2) prime repo provides idiosyncratic advantages that can explain divergence from SOFR/risk free rate benchmarks

---

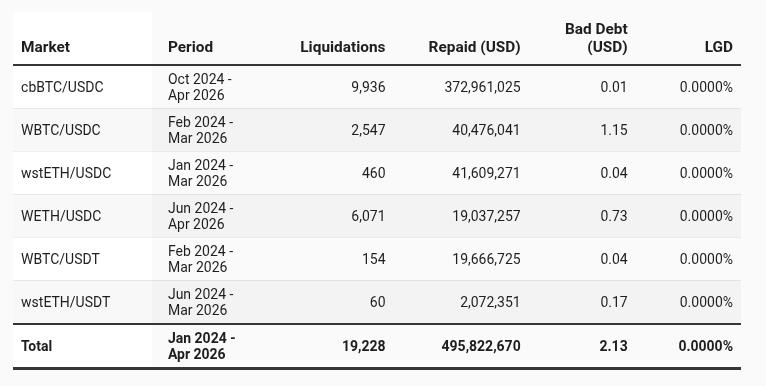

first- the bulk of the risk of onchain prime repo is not from market price jump risk, but rather from technical and counterparty risks embedded in the underlying collateral assets and oracle mechanisms

most blue-chip collateral in ethereum defi is either tokenized bitcoin (WBTC, cbBTC) or liquid staking tokens (wstETH, weETH). these collateral issuers have long successful track records, but they are still subject to various fundamental risks including custody/key management, smart contract integrity, business continuity/uptime, etc. additionally, repo markets depend on data integrity, smart contract security, and key management of oracle providers.

probability of default/incidents across these dependencies is expected to be very low, but the potential losses incurred in a failure case can be significant (up to 100% of the exposure)

looking at the most recent loss events in defi (resolv and drift), we see that they were driven by fundamental risk factors rather than market risk. as a defi lender, the primary driver of risk is these fundamental factors rather than jump risk.

---

second- onchain lending has additional benefits that can explain low or even negative spreads vs risk free rates like SOFR

fundamentally, i think it makes sense to assume that (most, large scale/sophisticated) market participants are prima facie rational; if they are accepting defi lending risk with yields at or below SOFR, there is probably a reasonable explanation

my mental models for this are liquidity premia or convenience yield

liquidity premium is the excess return that investors demand to hold assets that cannot be quickly converted to cash at low cost. for tradfi investors, prime MMFs, tbills, and other SOFR benchmarked cash equivalent assets are this asset class and we wouldnt expect them to accept a yield below this in any circumstance.

but for cryptonative investors or cryptoasset service providers (think whales, hedgefunds, exchanges), the key measure of liquidity is not the speed cost to receive cash in a bank account, but rather the speed/cost/slippage to meet their business liquidity needs, which are typically onchain/within the crypto ecosystem.

taking a directional hedge-fund as an example, if they face even a 1 hour delay between the time they request redemption of a MMF and when they receive wire transfer into their exchange account, they could easily miss a 5-10% move in a volatile asset, wiping out years of "excess risk adjusted return" they might earn with tradfi SOFR linked instruments over onchain repo

convenience yield, the implied return on holding inventories, is another way to look at the same benefit. if onchain actors can expect to derive meaningful benefits from having their assets closer at hand in onchain repo markets, even if the benefit is only realized infrequently, then it can be entirely rational for them to accept risk adjusted returns below SOFR on prime repo opportunities

---

@sparkdotfi has placed significant effort into both elements above, mitigating fundamental risks and facilitating onchain repo's key liquidity advantages

with respect to risk- in sparklend, we use redundant/aggregated price feeds across multiple providers to mitigate oracle risks, and are continuously introducing mechanism design solutions to alleviate corner cases (eg. automatically freezing borrowing when a pegged asset trades below peg). additionally, we put significant focus into fundamental research on collateral assets, with rate limits and automated cap management helping limit exposure to issuer failures

with respect to liquidity/utility- Spark is laser focused on delivering high liquidity savings products that meet the needs of sophisticated crypto market participants

taking the Spark Savings USDT vault as an example (app.spark.fi/savings/mainnet…), we currently maintain over 700 million in available withdrawal capacity against a 885 million total vault size, or roughly 80% liquidity ratio. this far surpasses the typical liquidity available within other onchain lending markets, which already have a significant liquidity advantage for cryptonative entities vs offchain cash equivalents

---

to summarize

- market risk is an important consideration, but generally represents only a small factor within onchain prime repo

- the larger impact on risk is from fundamental factors, which can be mitigated with a diligent approach to counterparty collateral evaluation and technical/mechanism design solutions

- the market is fundamentally (mostly) rational and delivering superior a superior onchain liquidity profile can justify residual risk exposures, even when the spread vs SOFR is low or negative

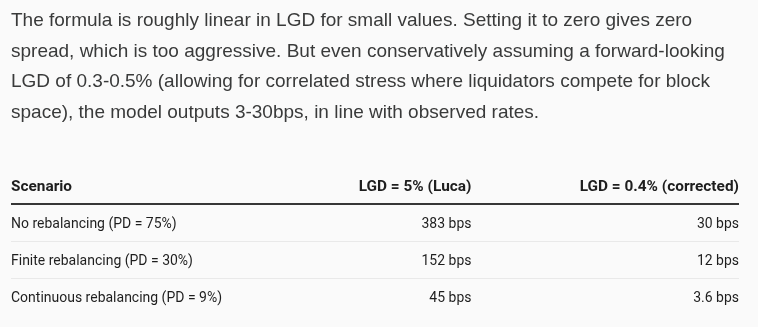

Luca’s model for onchain lending is rigorous and the framework is genuinely novel. However, we have two disagreements with it:

1. Onchain lending is repo not a put option sale

2. If you use a more realistic LGD parameter, the model predicts observed lending rates without significant mispricing

The model relies on a loss-given-default (LGD) parameter to estimate the fair value of an onchain lending position. We would set the LGD parameter to a few bps over 0% (higher than the empirical bad debt rate for lenders in Prime markets) rather than ~5% (which is modeled on the liquidation incentive, a borrower cost).

If you do, the model outputs fall exactly in line with observed rates at around 3-30bps, and the alleged mispricing disappears.

5

6

55

16,907

Apr 1

In this age of AI slob, clear & concise writing is possibly the greatest power.

1

52

Minerva retweeted

Mar 31

Canton's proponents would be on much stronger ground if they simply said:

We are permissionless against the only adversary that matters for our use case: institutional participants with competing commercial interests. A single institution or small coalition cannot corrupt our social consensus. We make no claim beyond that, and we don't need to.

The best argument they can make is that permissionlessness is a relative construct. Relative to the relevant threat model.

For Ethereum, the relevant threat model is nation states, which is the ultimate form of permissionlessness.

For Canton, it's institutional participants with competing commercial interests.

So, they can say permissionlessness is the cost to corrupt social consensus minus the ability of the relevant adversary(s) to corrupt it.

8

5

40

4,794

Minerva retweeted

Mar 27

This is probably the most condensed summary of what Canton is all about

7

29

116

18,529