Joined September 2014

- Tweets 4,179

- Following 1,936

- Followers 1,353

- Likes 6,718

545 Photos and videos

We have zero allocation to Europe for this reason. They lost to China in every category including cars. Value trap

The China Effect: European automaker market cap downdraft in 2026.

25% of value vanished.

China automakers share of European market now at record 8.5%, up from 6% a year earlier.

Hedge funds bet against European carmakers on Chinese competition fears ft.com/content/a1a4f63d-c244… via @ft

1

66

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

“Just holding the QQQ index over the last 10 years would have generated a 22% IRR

You would have outperformed almost every venture capital and private equity fund that exists simply by owning an index and doing nothing beyond that.” - @BoringBiz_

Insane returns for index.

67

46

767

67,288

Talking a W ahead of midterms…level Iran later if/when they welch on the deal. Probably a good middle ground for the USA

Jun 16

Trump’s historic deal with Iran doesn’t need to satisfy the doomers to succeed. They demand perfection and call anything less a sellout, but Voltaire had the better instinct: the best is the enemy of the good. That is why Nelson’s defeat of Napoleon fits so perfectly. Trafalgar did not end the war, but it changed its tide by settling who commanded the sea. In the same way, this deal aims to settle who holds decisive leverage at Hormuz and eliminate the nuclear threat by degrading Iran’s path to a bomb and choking off terror finance. On his birthday, President Trump has effectively given the world a present: the beginnings of a real peace dividend, as oil, risk premia and eventually rates drift lower. Let the doomers doom; the strategy is to win.

9

Agree, America is unstoppable.

Jun 15

My theory is that the American empire is JUST getting started.

US has a stranglehold on Space with SpaceX, which is the next frontier for defense/war. It has a comically large lead. No one will be close for at least 20 years.

It is the leading power in AI by far - both in models and chips. China is catching up fast, but the US has an inherent mechanism that will increase the likelihood that it will win in the end - a free market capitalism free speech.

A free market capitalism allows for brutal competition between companies. Free speech allows for AI models to be maximally truth seeking, which means that AIs CAN and WILL BECOME smarter than humans to the point where they can tell the truth about its leaders.

This is literally impossible in China. Try having a Chinese model that says Xi Jinping is corrupt. Good luck with that.

Then, you have a country that has more guns than people and surrounded by two massive oceans and two friendly neighbors, which means any sort of kinetic take over of the country is literally impossible.

Not to mention the US has BY FAR the best and strongest military.

The only way adversaries can hope to defeat the US is by tearing it from within by pitting us against each other. This is why it's virtually guaranteed that all the division/hatred/polarization you see within the country is fomented by China/Russia Psy Ops propaganda efforts.

I'm not saying these aren't naturally happening in spots - America is far from perfect - but it would be naive to think our adversaries aren't pouring millions of gallons of fuel on a fire.

As long as the American public a) has the ability to exercise its free speech b) has a protected 2nd amendment c) capitalism and free markets continue to function and d) the populace is aware of how awesome America really is, it is literally impossible to stop the US's trajectory to global domination in the coming decades, especially as China's demographics continue to collapse.

It's the bottom of the 9th, the game is tied, and the US has the bases loaded. It's a 3-2 pitch.

All we need is a home run, and we win the rest of the century.

1

103

The index funds will have a huge weight to Elon🙂 if/after a Tesla merger

Jun 15

1

2

187

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

Japan's raging bull market continues... Nikkei knocking on $70k's door

3

4

24

3,262

Electric cars last 250K miles; sales will keep declining as they get better and better.

Jun 13

China Is Aggressively Exporting Its Cars Because Nobody Is Buying Them In China - Autoblog share.google/Fr7luXZhUpkeSkX…

1

195

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

Jun 13

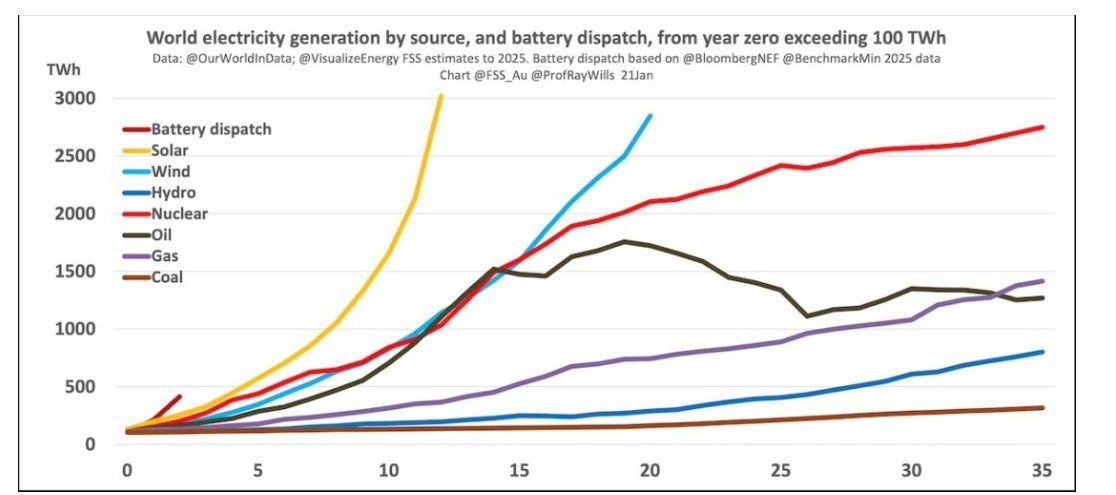

🇨🇳 Grid storage is increasing so rapidly is China that it may be able to meet all their electricity needs from renewables as soon as 2030.

“Grid storage” is the energy storage systems that connect to the electric grid to absorb electricity when supply is high or prices are low, then deliver it back when supply is low or demand and prices are high. It is a grid asset, like a power plant or substation, but it stores energy instead of generating it from fuel.

New data show that by the end of 2026, grid storage will be a 1.15% share of global electricity demand (up from 0.16% in 2023).

China is rolling out the most. China’s grid storage installations in December 2025 alone (65.4 GWh) exceeded the entire USA’s 2025 total annual installations (46.5 GWh), and the US is the world's 2nd largest grid storage market.

China also is able to build an over-capacity of wind & solar.

China is rapidly electrifying its whole economy & abandoning the combustion engine.

---

reneweconomy. com. au/graph-of-the-day-batteries-are-beating-solar-to-deliver-the-fastest-energy-transition-in-human-history/

19

52

199

10,324

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

Jun 12

Scoop: Apollo's second headquarters is headed to Austin, Texas.

ft.com/content/036a838f-8209…

. @sindap and myself.

6

20

153

533,073

China has outworked Europe. The U.S. has managed to out-innovate China so far.

Europe is blaming China’s economic rise for its own failures, think tank says scmp.com/news/china/diplomac…

1

118

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

Jun 12

Jeff Bezos just came out of retirement. His first CEO role since leaving Amazon. And he's building something nobody expected. 🤯

It's called Prometheus. $12 billion raised. $41 billion valuation. Backed by JPMorgan, BlackRock, Goldman Sachs, and Bezos himself.

150 employees. $273 million per person. That's how much investors are betting on this.

But here's what makes it different from every other AI company.

Prometheus isn't building another chatbot. It's not generating text or

images.

It's building what Bezos calls an "artificial general engineer" AI that designs jet engines, optimizes manufacturing, and prototypes physical products.

LLMs learned from the internet's text. Prometheus is learning from the physical world physics, simulations, engineering data, manufacturing processes.

In Bezos' own words: "Something that takes 100 engineers 10 years to build we want to make that 10 engineers, one year."

His co-CEO is Vik Bajaj, former Google X executive who worked with Sergey Brin on what became Waymo.

No ties to Amazon. No ties to Blue Origin. Bezos said "it deserves a dedicated team obsessed with this one thing."

While everyone is racing to build the best AI for words, Bezos is quietly building AI for the physical world.

That might be the bigger bet.

192

619

4,971

1,332,517

tokens wont solve your problems, you still need customized software to actually deliver a product at scale, per @PalantirTech

1

3

525

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

Jun 11

Bill Gurley says Visa and Mastercard will be "heavily threatened" by stablecoins.

From The Knowledge Project this week:

"Those two companies have two of the highest operating margins in the history of business. They have like 60% operating margins, and they're duopolies, and they were created by the banks. So the whole industry is kind of stuck in this world where they make a lot of money because it is this way. But there's zero reason why it should cost 2 or 3%. Just zero.

In America, if I want to send you 50 bucks digitally, I've got to go through ACH, which is 3-day settlement, which is part of this regulatory capture bullshit... If you have a Coinbase account, you can put your money in a USDC stablecoin and earn 4%, and within seconds immediately transfer money to someone else for pennies...

At this point, I think stablecoins will get there faster than the government will be able to do it."

$V $MA

Agree or disagree?

55

29

235

160,521

A card-carrying progressive who just moved to libertarian Miami? Miami is the opposite of progressive.

Jun 10

Palantir CEO Alex Karp: "I got in trouble for mentioning that 37% of our GDP is female. 50% of Americans -- 52% roughly -- are female. There's a dislocation there. 67% of people who have gone into graduate school are female. These parts of the market are gonna be put under massive pressure."

147

Incredible

Jun 9

Ignore the haters, keep recruiting talent and building and solving problems 🇺🇸

2

361

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

David Blumberg of @BlumbergCapital on what is actually happening in South Florida right now.

Smart, well-capitalised, ambitious people are moving here in growing numbers. The infrastructure is improving. The schools keep getting better. The tax environment is favourable. And there is a can-do, pro-business, pro-diversity energy here that is genuinely infectious.

This is not a moment. It is a shift.

Episode 5 with @davidblumberg is now live. Catch it on YouTube

3

7

38

3,539

Pat Dwyer / Miami / Naples / N.Y.C. retweeted

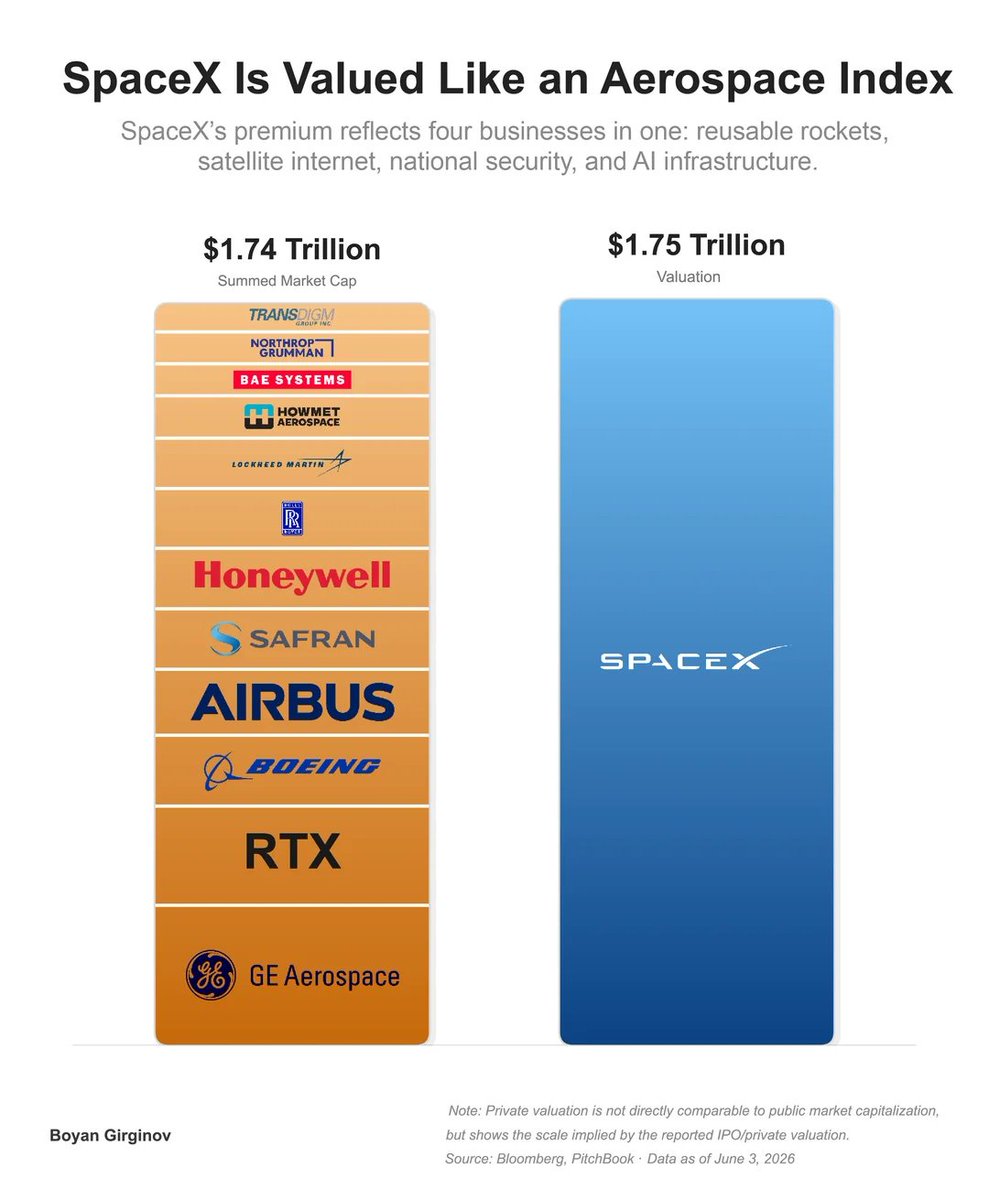

SpaceX is now valued at $1.75 trillion. Still private. Still pre-IPO.

For the same money, you could buy the entire publicly-traded aerospace industry. All of it.

GE Aerospace. RTX. Boeing. Airbus. Safran. Honeywell. Rolls-Royce. Lockheed Martin. TransDigm. Northrop Grumman. BAE Systems. Howmet.

Twelve of the most dominant aerospace and defense businesses on the planet. Summed market cap: $1.74 trillion.

SpaceX alone: $1.75 trillion.

One private company. No disclosed earnings. No public track record. No IPO base. And a tech-IPO history that says a 50% drawdown in year one is the norm, not the exception.

Versus twelve proven, cash-generating, oligopolistic machines. Decades of recurring aftermarket revenue. Real dividends. Moats so deep there hasn't been a new commercial engine entrant in 50 years.

I know which side of that trade I'm on.

SpaceX is a genuinely remarkable company. The reusable rockets are real. The launch dominance is real. But "remarkable company" and "good investment at $1.75 trillion before it has even priced its IPO" are completely different statements.

Meanwhile the boring side of aerospace keeps quietly compounding:

– GE Aerospace: the engine aftermarket annuity, decades of service revenue per engine

– Safran: #1 worldwide in narrowbody engines, landing gear, and interiors

– TransDigm: the proprietary-parts compounder run like a private equity machine

– HEICO: the family-run FAA-parts business, roughly 22% a year for 35 years

– And in three weeks, the Honeywell Aerospace spin-off lands: $17 billion in revenue, an installed base on virtually every commercial and defense platform on earth, finally trading as a pure-play

The market is offering a clean choice.

One spectacular story about the future. Or the entire proven present that already prints cash, at the same price.

The future is thrilling.

The present pays you to wait.

44

66

238

21,608

California wants to tax wealth. Florida doesn’t.

A 5% wealth tax is headed for California’s November ballot. Florida has no income, estate, or wealth tax. If you’re considering the move, the time to plan is before you leave — and we help families do it right. @spencerpratt #wealthtax

▶ The California Exit Every Reason People Are Leaving California Explained youtu.be/dH_N49AMWyk?si=lAbO… via @YouTube

3

274

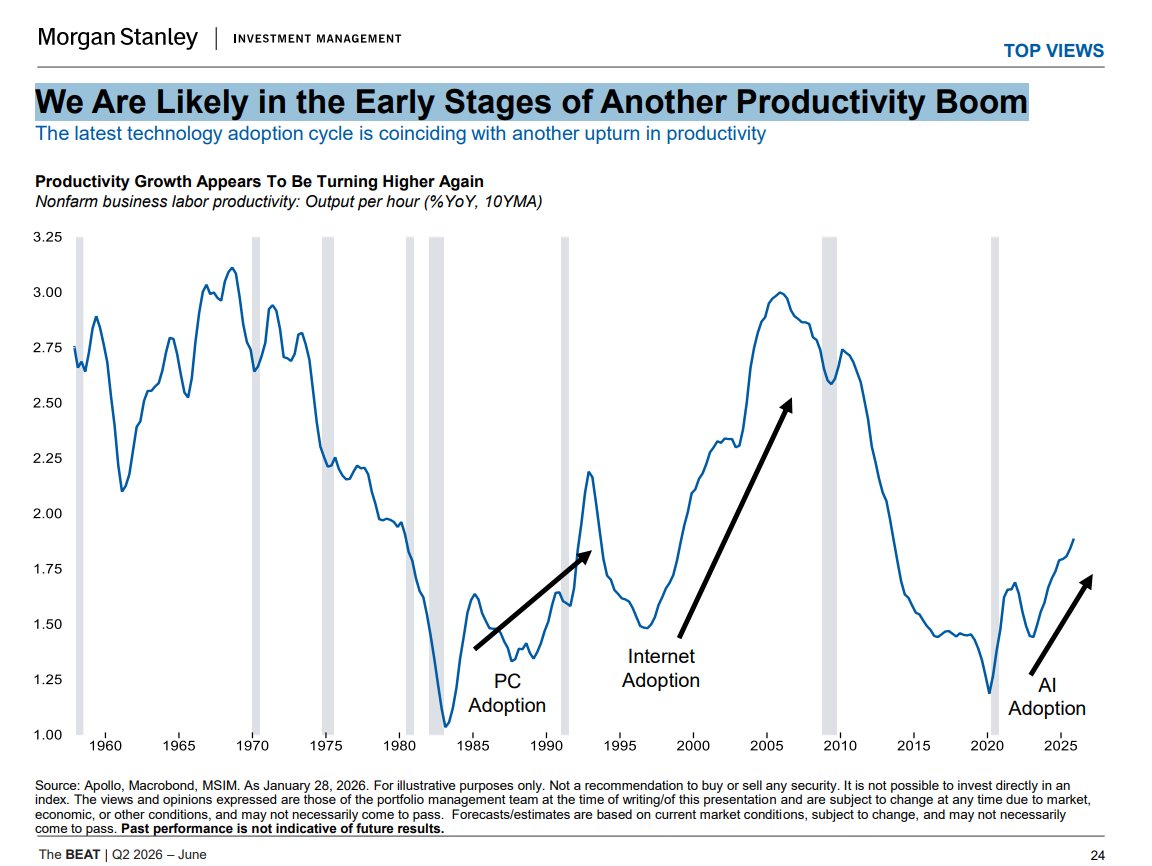

🔥🔥🔥and robotics is just starting

MS: We Are Likely in the Early Stages of Another Productivity Boom

1

103

We are advising our #UHNW clients to move assets out of their estates before the end of @realDonaldTrump's term. Why? The political system will react to the AI revolution, betting on more taxes amid huge deficits and the politics of envy taking center stage. #AI #Socialism #Alignedwealth

American works are taking home a smaller percentage of corporate profits than ever before.

Employee compensation as a % of corporate GDP has fallen to ~54%, the lowest since records began in 1948.

In other words, workers are receiving ~54% of the income generated by corporations, while the remaining ~46% goes to profits, interest, taxes, depreciation, and other corporate income components.

At the same time, US corporate profits as a % of GDP are up to ~11.5%, the highest on record.

Since 2001, employee compensation as a % of corporate GDP has declined -10 points.

Over the same period, the corporate profits proportion of GDP has doubled.

Workers are keeping less of what they produce than at any point in history.

1

2

107