Joined June 2009

- Tweets 1,291

- Following 1,445

- Followers 1,435

- Likes 1,960

171 Photos and videos

Raphael Vullierme retweeted

31 Jul 2025

monthly signups for @resend...

back in january, we were seeing 25k new users per month, now we're seeing 70k.

it's pretty clear that we have a new definition of a "developer" now.

70

9

457

62,073

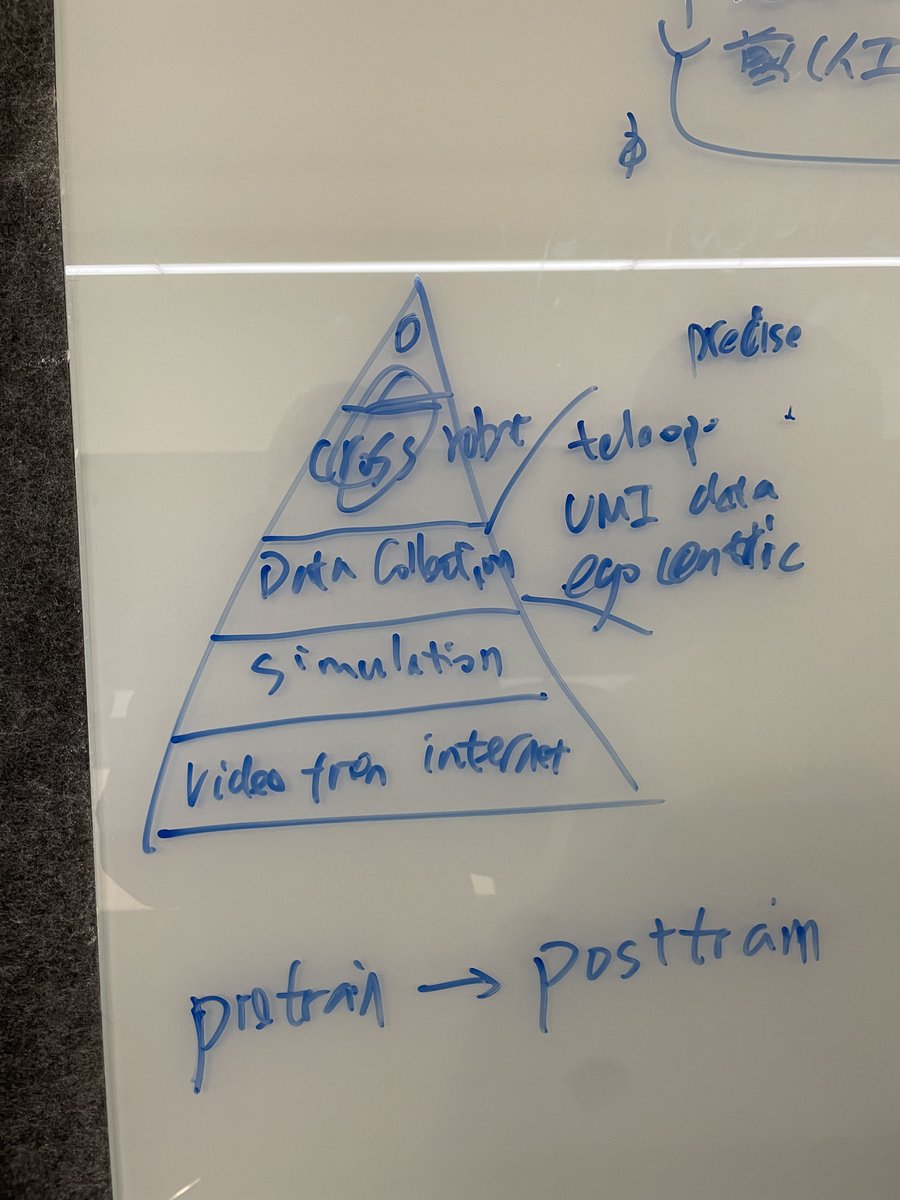

#Robotics: The space where @X FOMO and unrealistic marketing claims are out of control.

I had enough of cool videos with nothing IRL, so I went to #China to understand the real state of the field and a realistic timeline.

open.substack.com/pub/pharea…

1

3

7

2,699

Locomotion and basic motion are mostly solved. But grasping & manipulation hasn't been.

My take real Physical AI is years away. Many big unlocks still needed before deployment at scale in factories and homes. Autonomous driving is an appetizer vs modeling the full real world.

1

96

China's state is brute-forcing the problem: financing companies, buying robots, opening data collection farms.

Surprisingly most engineers, investors, and researchers we met expect the general-purpose Physical AI model to come from the US.

1

75

Apr 28

#Claude now suggests apps.

Claude analyzes user intent → finds the right tool → suggests it.

OpenAI enabled AI apps but seemed to never been committed to make them work

With Anthropic taking the lead the channel really starts. Day1 of #AIdistribution.

69

Apr 28

The big reshuffle of financial services value chain

Apr 27

profitable apathy

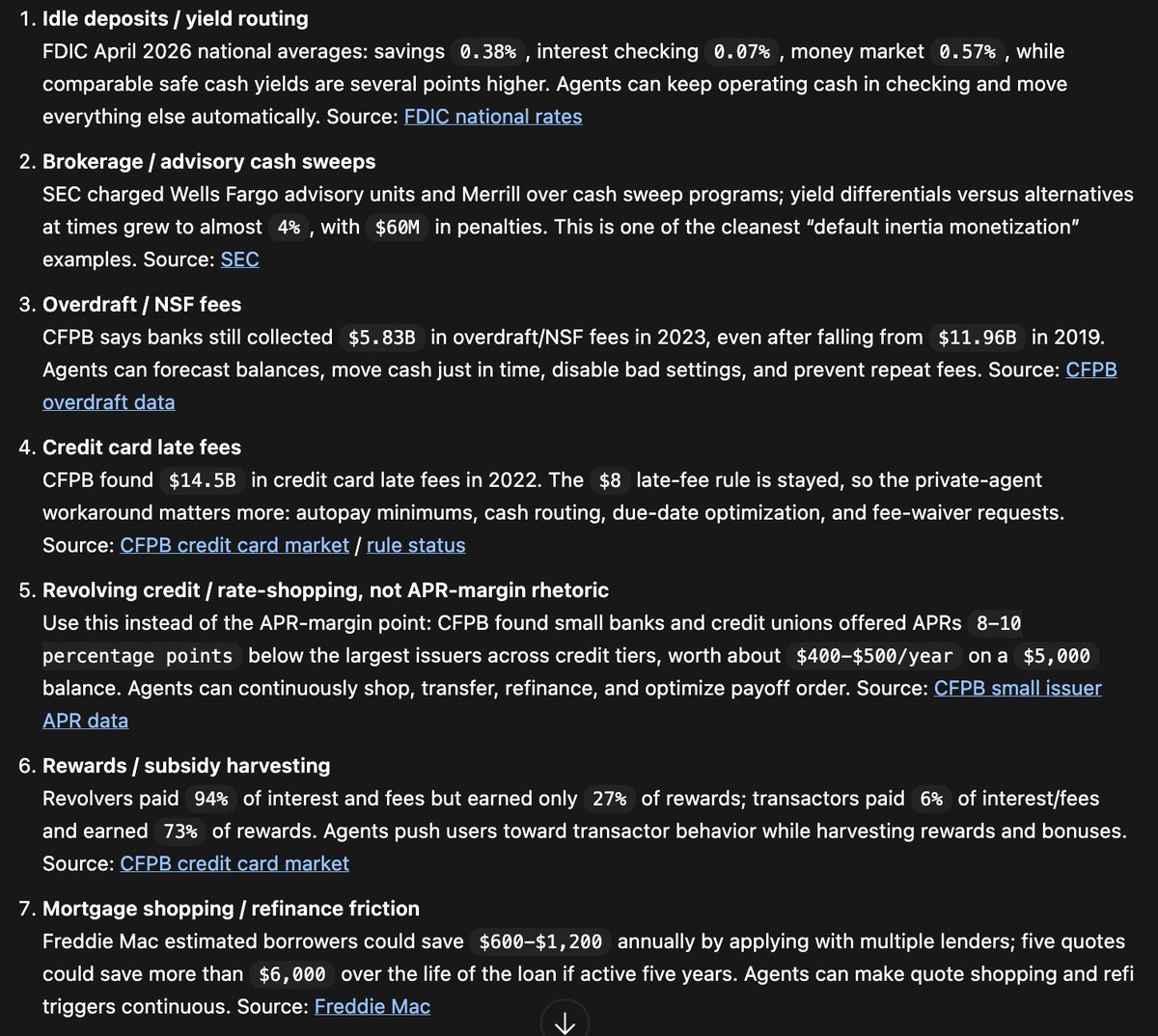

if you thought saas-pocalypse was bad wait until computer use comes for consumer financial services and vampire squids the whole thing

there are many, many profit pools that depend on apathy/laziness and a poorly informed customer - the industry that brought you the efficient market depends on an inefficient consumer to eat

first the models will systematically exploit every customer subsidy (transfer bonuses / teaser rates), move deposits to maximize yield, open and close accounts on a whim - this industry has operated with asymmetric bureaucratic warfare through paperwork and sheer friction and the models will cut through this like a hot knife through butter

and the model will neatly route around late fees, interest charges, overdrafts, expiration of teaser rates, and any mispriced debt that can be refinanced in the market - literally just moving people out of expensive debt and into cheap debt (that they are already approved for!) would save many american families thousands per year

meanwhile vps and managers at these companies will hold on to their shrinking revenue lines the same way that executives at carriers protected SMS revenue as it collapsed to zero - they have zero chance of sticking the landing on new technology - and the smart ones will likely go for extending regulatory capture into the agentic economy

so much of the consumer financial services ecosystem is marketing via subsidies on one end and profit maximization via customer apathy on the other, and it will collapse under its own weight as the agents pick it apart

ironically the industry response to plaid was a misguided attempt to protect this very "profitable apathy" by disallowing APIs and in the end it will be agents that kill them clicking around their own UI, not the fintech aggregators they so greatly feared

the end state of this is likely a headless auction where every time you swipe your credit card, some lender bids on taking the risk and capturing the profit from that transaction - it will be a much more efficient system that will work much better for consumers, and many pockets of financial services are going to see contraction as a result

aa 5.5

1

121

Mar 13

Les pouvoirs publics « se demandent comment délivrer une écologie populaire, mais, lorsqu’une solution adaptée apparaît, ce seraient les barbares qui débarquent en ville »

Haine et mépris envers une solution populaire, pragmatique et décarbonée.

lemonde.fr/m-perso/article/2…

2

63

Mar 10

One of the hardest things early stage atm.

Do you only build for AI native company? Do you speak old playbook company? The products for those 2 ICP are completely different.

Mar 9

Wondering if the pace of AI progress changes how early-stage startups should think about early ICP.

If your early customers are a bit further right on the adoption curve, you might end up building something that looks outdated in 1-2 years.

Innovator's dilemma mechanics but for early-stage companies...

1

87

Raphael Vullierme retweeted

Feb 5

Everyone talks about humanoids.

Meanwhile, @loki_robotics:

217

413

5,131

3,278,982

back to what I truly love: building 🏗️

Thrilled to team up with @joinhexa to launch #WalkTheFrontier, a studio building global AI ventures.

1st

AI as a buyer — businesses mastered selling to humans, but AI will decide.

Also venturing in #PhysicalAI (robotics & defense).

2

8

520

Raphael Vullierme retweeted

16 Dec 2025

Seules les images sont mises en scène. Le dialogue est réel et tiré de l’interview de Guillaume Pley avec #NicolasSarkozy pour l’émission Legend.

#Sarkozy

55

457

2,149

112,067

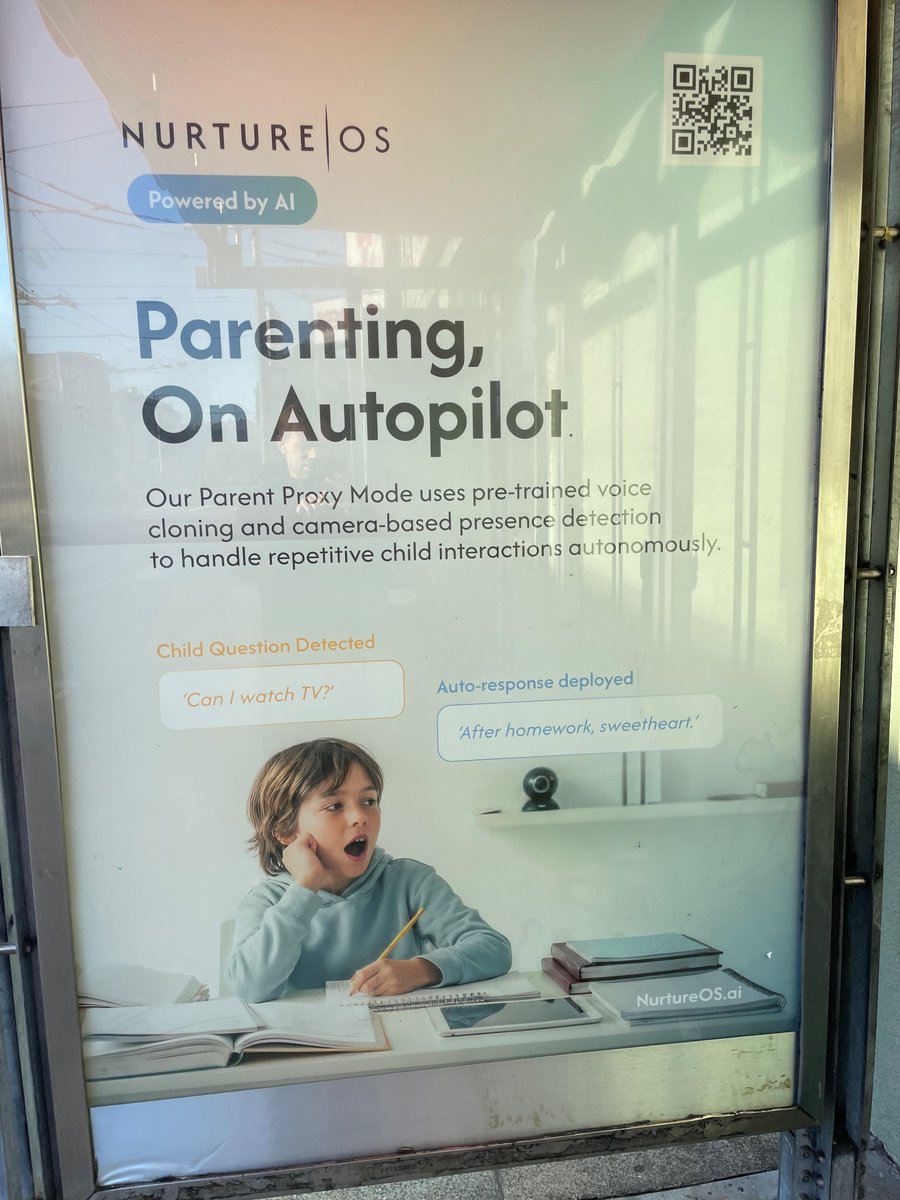

21 Nov 2025

who’s behind these sarcastic paid ‘AI parenting’ dystopians billboards in SF?

nurtureos.ai

Parents can now grow/mine human brain to lease to @mercor_ai

226

2 May 2025

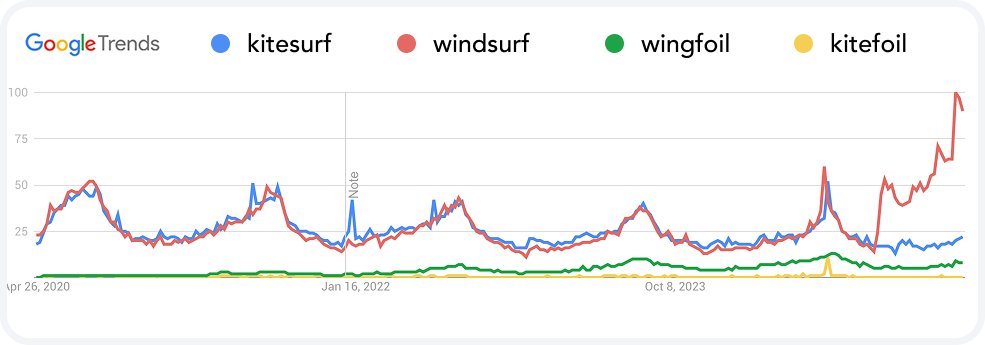

Looks like #windsurf is soo back !

Whether it’s against #kitesurf or @cursor_ai , it’s still about riding good waves, I guess.

2

418

Raphael Vullierme retweeted

25 Jan 2025

NOTE: Using OpenAi Operator at your bank in EU is illegal by law! Web access for assistants was banned years ago as part of “Open banking”

Here is the story of why:

15 years ago I stumbled into Sofort in Germany. A company with the idea to build a digital assistant that would interact with your banks poor UI, so you as a user could avoid it. Just like operator. Back then it was script based, not AI but it worked.

I was so impressed Klarna bought the company. It has since then processed billions of dollars.

But of course banks got scared! What happens if people use the digital assistant only, instead of their bank. And what if the assistant says, stop paying those fees to your bank and let me help you switch?

So German banks sued. They claimed privacy concerns. It went to Brussels and a long lobbying and legal fight pursued. This was the beginning of what we today call open banking!

I and others spent years fighting over consumers right to use digital assistants, when accessing their banks. We knew this was critical to create real competition, in an industry that has been plagued by excess profits for years.

At first Jonathan Hill from UK was responsible and very supportive. But then he left and a German guy came onboard. He was 100% aligned with incumbent banks and we thought the case was lost. However he did a mistake and let some Russian oligarchs take him for a ride on their private jet. And so he was out.

Finally @VDombrovskis stepped in. He was smart and supportive but pressure from banks was intense. There was rumors that they were funding privacy groups in Germany, to have them use privacy concerns to kill Open Banking. What if the digital assistant accessed some of your private data?

We were about to loose the vote, when the competitive authorities of EU started getting interested. They suspected the banks were lobbying and pursuing this matter for profit reasons to reduce competition(really…). A few weeks before the vote in parliament they raided the offices of some Dutch and Polish banks. Everyone got super nervous and the Open Banking regulation was passed!

Almost…

A small technical detail was left to EBA (European banking authorities). Should your digital assistant use an API for access to your bank account or the standard web UI you use yourself for accessing your bank?

We pushed as hard as we could. We highlighted and said, if your assistant is mandated to use the API that your bank supplies. What if the API don’t support all the same features. Or the API is broken?

Don’t worry said regulators. You can complain with authorities 😂

We said at least let the digital assistant, as fall back, use the web UI. Then banks cant cheat, as they will know we can always use the same UI as their human customers. It’s called self regulation. But EBA ignored us.

Today web UI access for digital assistants as ChatGPT Operator is illegal by law.

And surprise, surprise the open banking API of European banks, continue to be broken, lack functionality and banks add as much friction as they can. We report and see thousands of issues with these APIs every year.

And people ask me why open banking has not become a larger success…

What do you say @donaldtusk time for a change? Jest potrzebne!

228

698

3,688

1,516,230

Raphael Vullierme retweeted

18 Feb 2025

I constantly get DMs from European founders wanting to build in the U.S. If you're serious about your life's work, you should.

@joinodf has helped many second-time founders:

> Build community in SF

> Find co-founders

> Navigate immigration

No equity taken

Apply by tomorrow!

7

12

127

10,952

24 Jan 2025

La solution serait que l’UE (ou trump) impose un ban sur les llm et cloud providers US. En 5-10 on a une vraie tech européenne.

24 Jan 2025

Le LLM DeepSeek chinois est une rupture de paradigme géopolitique, scientifique et économique dont on ne mesure pas l'ampleur.

En entraînant un modèle à 670mds de paramètres avec 5,5 millions de dollars de calcul seulement, ils ont obtenu une performance opérationnelle d'une échelle de plusieurs dizaines de fois supérieure à la performance des meilleurs.

Géopolitique : la stratégie d'endiguement des USA ne marche pas. Ce LLM est si peu 'intensif' qu'il a pu être entraîné sur des H800, des processeurs qui ne sont pas sous embargo donnant du poids aux arguements de Nvidia (l'embargo est inutile).

Scientifique: l'approche "mixture of experts" utilisee ici montre que les contraintes fortes (pas d'accès au calcul massif) suscittent l'innovation et qu'il y a probablement d'immenses gains de performances à trouver dans l'optimisation des modèles mathématiques structurants les modèles

Économique : DeepSeek effondre la barrière à l'entrée de la production de LLM, permettant potentiellemment à de petites acteurs de développer des LLM très puissants.

on.ft.com/3Q8k3Mp via @FT

2

283

Raphael Vullierme retweeted

24 Jan 2025

Le LLM DeepSeek chinois est une rupture de paradigme géopolitique, scientifique et économique dont on ne mesure pas l'ampleur.

En entraînant un modèle à 670mds de paramètres avec 5,5 millions de dollars de calcul seulement, ils ont obtenu une performance opérationnelle d'une échelle de plusieurs dizaines de fois supérieure à la performance des meilleurs.

Géopolitique : la stratégie d'endiguement des USA ne marche pas. Ce LLM est si peu 'intensif' qu'il a pu être entraîné sur des H800, des processeurs qui ne sont pas sous embargo donnant du poids aux arguements de Nvidia (l'embargo est inutile).

Scientifique: l'approche "mixture of experts" utilisee ici montre que les contraintes fortes (pas d'accès au calcul massif) suscittent l'innovation et qu'il y a probablement d'immenses gains de performances à trouver dans l'optimisation des modèles mathématiques structurants les modèles

Économique : DeepSeek effondre la barrière à l'entrée de la production de LLM, permettant potentiellemment à de petites acteurs de développer des LLM très puissants.

on.ft.com/3Q8k3Mp via @FT

42

233

666

85,849

Raphael Vullierme retweeted

18 Nov 2024

The $6,000 price tag of most robotic arms was a big obstacle for my projects. So, I built one for $200. It can carry a 2kg dumbbell. Its reach is 60cm.

This version is almost full metal, the first 3d printed version was breaking easily…

#Robot #3DPrinting #ArtificialInteligence

13

30

173

10,580