Joined October 2024

- Tweets 2,626

- Following 1,766

- Followers 15,704

- Likes 15,351

546 Photos and videos

Polyfactual retweeted

Prediction markets are getting their own creator economy.

@TradeRyno is building a platform where traders monetize their intelligence through callouts

Giving even smaller-bankroll traders a way to build a brand and earn.

Jun 12

🚨🚨The $1,500 Ryno World Cup Trading Tournament is live.

How it works: post your World Cup picks on Ryno. Every pick is timestamped, locked, and scored as 1 unit. All picks count, wins and losses. No cherry-picking, no deleted misses.

Best verified P&L over the tournament wins $1,000.🏆 Refer the most new traders and take another $500.🏆

To enter, you need to be a Ryno trader. Traders build a verified public track record and sell subscriptions to their picks. The tournament is free to enter, and onboarding takes minutes.

June 13 to July 19. Apply and full rules: traderyno.com/worldcup

2

4

15

1,294

Back in 2015, you had $100

No one really knew what would explode: crypto, gaming chips, or rockets that could actually land back on Earth

Here's how it played out 11 years later:

NVIDIA ( $NVDA ): $100 → $36,600

Alphabet/Google ( $GOOGL ): $100 → $1,310

Microsoft ( $MSFT ): $100 → $830

Bitcoin ( $BTC ): $100 → $27,600

Ethereum ( $ETH ): $100 → $167,000

Amazon ( $AMZN ): $100 → $1,100

Apple ( $AAPL ): $100 → $890

SpaceX ( $SPCX ): Valuation grew roughly 150-180x from 2015 to its 2026 IPO

For an average person, the most realistic way to get in early on SpaceX was to get a job there in 2015

Right now on Polymarket, traders are giving SpaceX an 88% chance of having the largest IPO of 2026 by market cap

In 2015, most of these looked risky or straight-up crazy. Very few people picked the winners

Today, it feels like we're at another turning point. The next big shift might be prediction markets - not just holding assets, but actually predicting the future you believe in

Where would you put your $100 today in 2026?

6

3

17

1,411

Polyfactual retweeted

Jun 12

You've never seen a prediction market move this fast.

We got a sneak peek of @KairosTradeX from the last Polyfactual pod with @thejay

btw, Kairos just launched a Trading Championship with @Polymarket and @TXODDSOfficial:

> $30,000

> four prize pools

> top traders vs top creators

Runs for the entire World Cup.

Jun 11

Introducing the Kairos × @Polymarket × @TXODDSOfficial Trading Championship.

$30,000

Top traders.

Top creators.

Four Prize Pools.

Bet on your favorite participants directly on Polymarket, or climb the ranks on Kairos and get featured yourself.

Think you can outperform the market?

Details Below:

15

8

45

7,847

Polyfactual retweeted

Jun 12

Clipped the live of Kairos CEO explaining the edge on 5-minute up/down

I tried trading 5-minute up/down markets and it's genuinely easy to scalp

I set the limit orders by Best bids

Get filled instantly without any cent paid in fees

I set the Trailing Stop

It adjusts in real time, moves along with my profits

And then it will never drop lower

To be simpler:

Once the odds pumped enough, you're is basically locked in profits

@KairosTradeX was released just today, already superiors other trading terminals

Picture of my recent profits on Kairos below in replies

$30,000 Trading Competition details in the tweet below

Jun 12

You've never seen a prediction market move this fast.

We got a sneak peek of @KairosTradeX from the last Polyfactual pod with @thejay

btw, Kairos just launched a Trading Championship with @Polymarket and @TXODDSOfficial:

> $30,000

> four prize pools

> top traders vs top creators

Runs for the entire World Cup.

15

4

67

2,494

Polyfactual retweeted

Jun 12

Another ACE round LIVE on Metalex right now is @polyfactual,

A serious media play in the Prediction market space.

Here are some quick stats:

> AI infra integrated with 12 Poly trading terminals

> Next level network of trader's, founders and angels

> A top podcast in prediction markets

Might be time to get on the cap

Jun 10

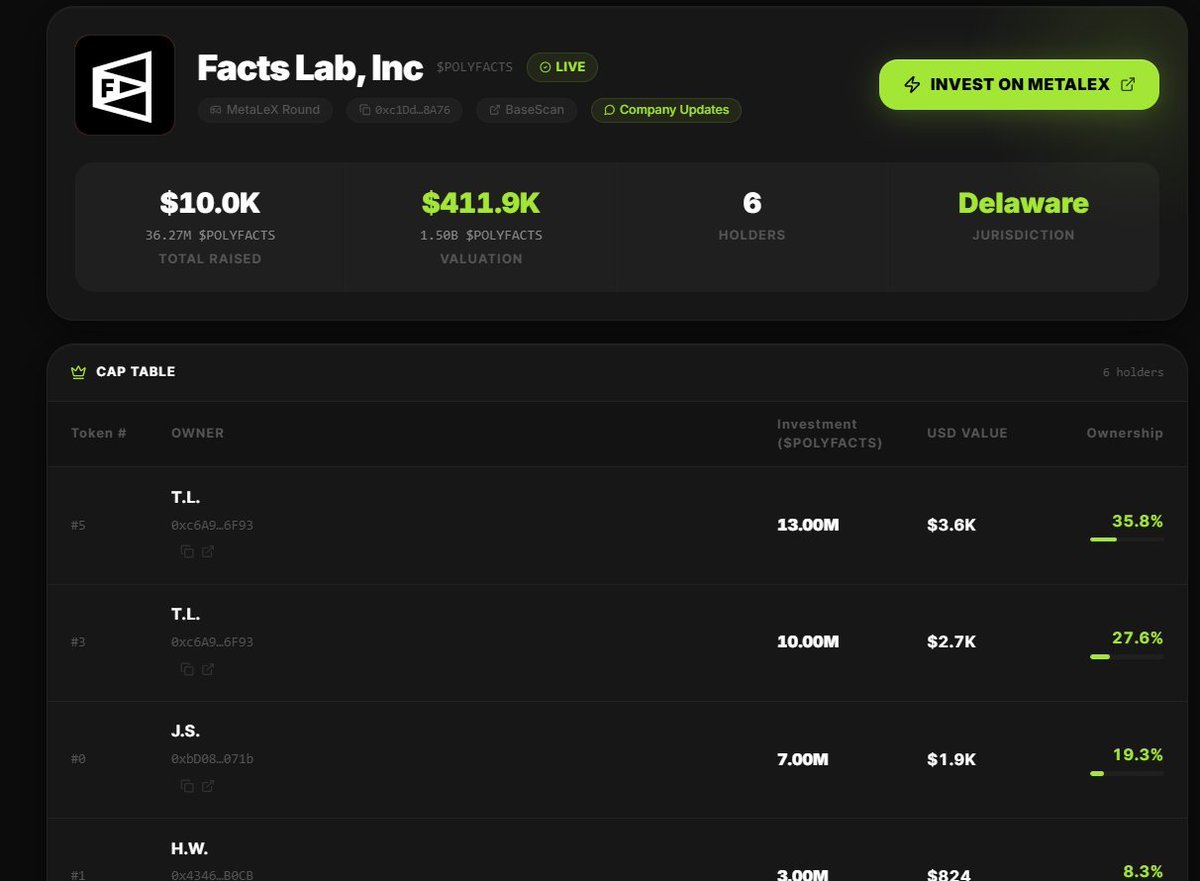

🚨 FROM $18M TO $270K. THE MARKET FORGOT ABOUT $POLYFACTS. THE WORLD CUP MAY REMIND THEM!

$POLYFACTS (@polyfactual) is one of the few real utility tokens in the prediction market ecosystem and is down ~98% from its $18M ATH.

Most people see a forgotten micro-cap. What they miss is that Polyfactual is building an AI-powered intelligence layer for prediction markets:

• Real-time news aggregation

• Sentiment analysis & confidence scoring

• FactsAI API with 700K requests processed

• Chrome extension for Polymarket traders

• Facts trade terminal, PolyBrain & PolyScan

• Premium research, governance & ecosystem utility powered by $POLYFACTS

The project also received a Polymarket grant and has multiple integrations across the prediction market ecosystem.

Current stats:

• ATH: $18M MC

• Current MC: $270K

• 4.1K holders

• Listed on MEXC, LBank, WEEX, Raydium & Meteora

The thesis is simple:

If Polymarket activity continues to grow throughout the FIFA World Cup 2026 cycle, demand for research, data, analytics and trading tools could grow with it.

At just $270K MC, $POLYFACTS remains one of the highest-conviction asymmetric bets on the prediction market narrative.

CA: FfixAeHevSKBZWoXPTbLk4U4X9piqvzGKvQaFo3cpump

⚠️ NFA. High-risk micro-cap. Always DYOR and manage your risk.

#POLYMARKET #WORLDCUP #SOLANA

2

2

11

734

Jun 12

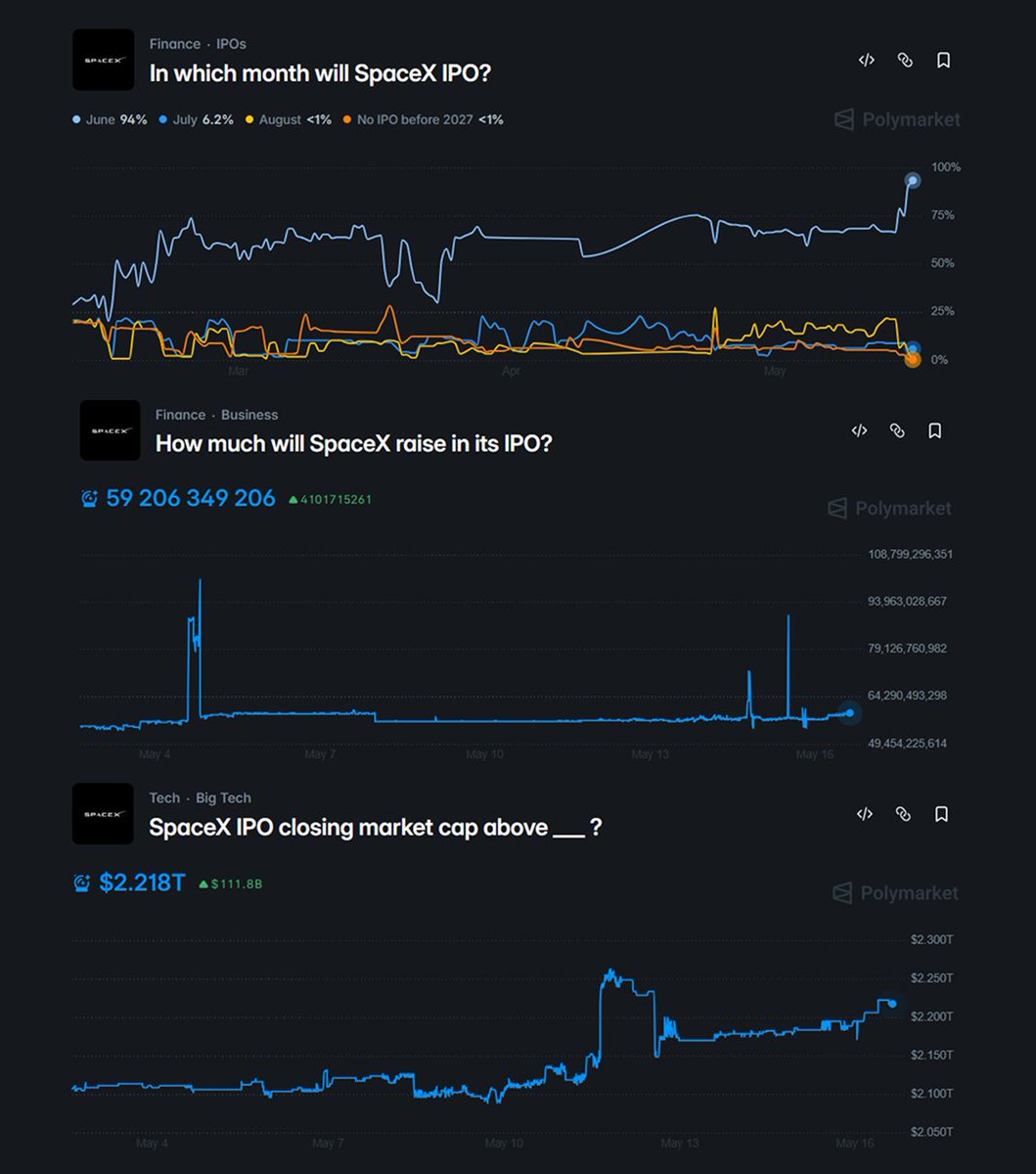

SpaceX just went public

SpaceX started trading on Nasdaq today under ticker $SPCX

Shares surged as much as 28% during the day, briefly pushing the market cap above $2.2 trillion

Polymarket: 88% chance of closing in the $2-2.5T range

SpaceX is using a gradual unlock instead of a standard 6-month lock-up:

- After Q2 earnings (August): 20% another 10% if the stock stays above $175.50 for 5 out of 10 trading days

- 7% unlocks every 15-20 days from late August to late October

= After Q3 earnings: 28% becomes available

- Final unlock: December 9, 2026

- Elon Musk and major shareholders are locked until June 2027

Analyst targets:

>Average: $165

>ARK Invest: $2.5T by 2030

>Morningstar: $780B (most bearish)

According to many analysts, selling pressure is expected to remain relatively low until August

The biggest risk period comes after Q2 earnings, when the first major wave of shares unlocks

What are your thoughts on SpaceX's gradual lock-up schedule?

8

4

27

919

Polyfactual retweeted

May 16

SpaceX IPO is Cleared for Takeoff

Here's the latest as of today:

➡︎ Which month will the SpaceX IPO happen?

June - 93% on Polymarket

Roadshow starts June 4, pricing June 11, trading begins June 12 on Nasdaq (ticker $SPCX)

Why is the market still pricing 7% for July?

Classic insurance. Bankers always leave a small buffer in case the SEC wants last-minute changes or the market gets choppy.

➡︎ Closing market cap on first day of trading?

Above $2T - 68% on Polymarket

The filing targets $1.75T. But up to 30% goes to retail investors, plus huge hype and the Musk effect.

That should deliver a strong first-day pop. Bankers are already floating valuations above $2T to potential investors

➡︎ How much will SpaceX raise in the IPO?

My base case: $70-80 billion (currently 24% on Polymarket)

All fresh reporting points to $75 billion. That would instantly become the largest IPO in history (2.5x bigger than Saudi Aramco)

This isn't just an IPO. This is the moment a company that controls around 80-85% of all commercial space launches goes public and could immediately break into the top 10 largest companies on the planet.

10

7

37

9,779

Polyfactual retweeted

Jun 10

A mathematics professor from New York spent four decades proving that markets were not nearly as random as everyone thought,

He never became a television personality and neither did he build a consumer product, Yet he quietly built the most successful money-making machine in financial history

A machine so effective that Wall Street still debates whether it was genius, science, luck or some combination of all three.

His name was Jim Simons.

This is the story of the man who changed investing forever, and in the process created a new species of trader.

As opposed to a Banker, Economist or Stock picker profile type of trader, he followed the approach as of that of a Scientist

Jim Simons was born in 1938 in Massachusetts. As a child he loved numbers, patterns, and puzzles. While other kids sold lemonade, Simons was fascinated by probability and games of chance

He eventually earned a doctorate in mathematics from the University of California, Berkeley at just 23 years old. His career initially had nothing to do with finance

He taught mathematics at the Massachusetts Institute of Technology. He worked as a codebreaker for the Institute for Defense Analyses during the Cold War. He became one of the world’s leading geometers and, together with Shiing-Shen Chern, developed what would become known as the Chern–Simons theory, a mathematical framework that would later find applications in modern physics

By any normal standard, that would have been a complete career. But Simons had become obsessed with a different puzzle called,

Financial Markets.

The financial world of the 1970s was dominated by personalities. Traders trusted intuition. Investors trusted stories. Analysts traveled the world meeting executives and trying to determine whether a stock was cheap or expensive

Everyone had opinions but very few had data.

Simons looked at markets the same way he looked at cryptography. What if prices contained hidden signals?

What if the movements of millions of buyers and sellers left tiny fingerprints behind? What if the answer was not inside company reports or economic forecasts, but buried inside the numbers themselves?

Most people thought this was nonsense. The prevailing belief was that markets were efficient and Prices already reflected all available information. Finding persistent patterns should have been impossible

Simons did not argue, He simply started collecting data. In 1978 he founded what would become Renaissance Technologies but the early years were messy

The computers were primitive. Historical market data was incomplete and storage was expensive. Processing power was laughably small by modern standards

But Simons was building something Wall Street had never seen. Instead of hiring traders, he hired mathematicians and instead of recruiting investment bankers, he recruited physicists.

Instead of asking whether a company had a good CEO, he asked whether a pattern repeated itself often enough to survive statistical scrutiny. At a time when most hedge funds looked like finance firms, Renaissance looked like a research laboratory

Many of the people walking its halls had never traded a stock in their lives. That was exactly the point. Simons believed expertise could become a trap. Financial professionals often carried assumptions about how markets should behave. Scientists arrived with fewer prejudices and a greater willingness to follow evidence wherever it led,

The goal was not prediction in the traditional sense, the goal was Discovery.

Somewhere inside billions of market observations there might be tiny, almost invisible regularities. A stock that tended to bounce after a particular type of decline. A currency pair that reacted strangely under specific conditions. A cluster of behaviors that appeared insignificant individually but became powerful when combined

No single signal mattered much, thousands of signals mattered enormously.

Over time, Renaissance built systems that consumed vast quantities of market data such as Prices, volumes, relationships between assets, historical anomalies and statistical deviations.

If a Trade had worked hundreds of thousands of times before, and the odds remained favorable, the machine acted. The beauty was that nobody inside the Firm needed to know why a particular stock existed or what product a company sold

Only the data mattered and the results became almost unbelievable.

In 1988 Renaissance launched what would become the most famous hedge fund in history. The Medallion Fund. Over the next three decades, Medallion achieved performance numbers that sound fictional

After fees, the fund reportedly averaged annual returns around 39 percent for decades. Before fees, estimates place performance above 60 percent annually. Not for a few lucky years but for decades

To appreciate how absurd that is, consider that some of the greatest investors in history spent their careers averaging 15 to 25 percent annually. Medallion operated in a different universe

One dollar invested near the beginning became millions, Millions became billions. The fund eventually became so successful that Renaissance largely stopped accepting outside capital. The opportunity set was finite and more money would dilute returns

Instead, the profits mostly flowed to employees. The firm became legendary for producing some of the wealthiest scientists on Earth

Naturally, competitors tried to copy it but many failed. They understood the idea but not the execution.

Quantitative investing sounds simple from a distance. Collect data, build models and find patterns. In reality it is one of the most difficult endeavors in finance. Most patterns disappear the moment they are discovered, others are statistical mirages. Some work beautifully until market conditions change. A signal that appears profitable can collapse when transaction costs are included

The challenge is not finding patterns, the challenge is finding real patterns. That distinction consumed generations of quantitative researchers and Simons understood this better than anyone

He approached markets with scientific discipline. Every hypothesis required evidence, every model required testing and every result required skepticism. Nothing was accepted because it sounded convincing

Everything had to survive contact with data, that philosophy reshaped Wall Street.

Today nearly every major investment firm employs quantitative researchers. Massive teams of physicists, statisticians, machine learning specialists, and data scientists compete to extract signals from oceans of information

The modern quant industry traces much of its intellectual lineage back to Renaissance. The language of finance changed because of Simons. Terms like factor investing, statistical arbitrage, alternative data, machine learning, signal generation and systematic trading moved from academic curiosities into mainstream investing.

3

3

21

1,095

Jun 11

The biggest myth about prediction markets:

They funnel money from regular people to a small group of geniuses.

@thejay points out how tradfi is intentionally complicated, to create a moat

Prediction markets remove that entirely.

From our talk with @KairosTradeX .

6

5

26

1,543

Jun 12

Watch the full podcast here: x.com/polyfactual/status/206…

Jun 4

LIVE with @KairosTradeX, Building the Next Generation of PM Infra x.com/i/broadcasts/1DxleeMPE…

2

267

Polyfactual retweeted

Jun 8

WWDC26 TODAY: What will Apple (AAPL) hit in June 2026?

Today at 10 AM PT - Apple's WWDC26 keynote

Everyone's expecting a big AI breakthrough… but history doesn't lie:

On WWDC keynote day, $AAPL usually drops:

2025 → -1.44%

2024 → -1.92%

2023 → -1.67%

2022 → -0.61%

2008-2017 - closed red 9 out of 10 times. Classic "sell the news"

Only 2018 ( 0.08%) and 2020 ( 2.10%) were the exceptions

Current AAPL price: $310.09

Polymarket:

↓ $304 Low: Yes - 76%

↑ $320 High: Yes - 67%

Which one do you think we'll touch first?

4

4

19

2,892

Polyfactual retweeted

Jun 11

The biggest myth about prediction markets:

They funnel money from regular people to a small group of geniuses.

@thejay points out how tradfi is intentionally complicated, to create a moat

Prediction markets remove that entirely.

From our talk with @KairosTradeX .

6

5

26

1,543

Jun 11

When Hyperliquid launched, everyone said the same thing: "No KYC? Regulators will shut this down."

Now stock exchanges are calling them, asking how to get listed.

The lesson: lead with innovation, not with what's "allowed" right now.

From our talk with @ashish24rawat founder of @polyfund

Jun 5

Prediction Market funds with @polyfund x.com/i/broadcasts/1kJzDDopd…

3

2

12

1,240

Polyfactual retweeted

Jun 10

🚨 FROM $18M TO $270K. THE MARKET FORGOT ABOUT $POLYFACTS. THE WORLD CUP MAY REMIND THEM!

$POLYFACTS (@polyfactual) is one of the few real utility tokens in the prediction market ecosystem and is down ~98% from its $18M ATH.

Most people see a forgotten micro-cap. What they miss is that Polyfactual is building an AI-powered intelligence layer for prediction markets:

• Real-time news aggregation

• Sentiment analysis & confidence scoring

• FactsAI API with 700K requests processed

• Chrome extension for Polymarket traders

• Facts trade terminal, PolyBrain & PolyScan

• Premium research, governance & ecosystem utility powered by $POLYFACTS

The project also received a Polymarket grant and has multiple integrations across the prediction market ecosystem.

Current stats:

• ATH: $18M MC

• Current MC: $270K

• 4.1K holders

• Listed on MEXC, LBank, WEEX, Raydium & Meteora

The thesis is simple:

If Polymarket activity continues to grow throughout the FIFA World Cup 2026 cycle, demand for research, data, analytics and trading tools could grow with it.

At just $270K MC, $POLYFACTS remains one of the highest-conviction asymmetric bets on the prediction market narrative.

CA: FfixAeHevSKBZWoXPTbLk4U4X9piqvzGKvQaFo3cpump

⚠️ NFA. High-risk micro-cap. Always DYOR and manage your risk.

#POLYMARKET #WORLDCUP #SOLANA

3

5

18

2,060

Polyfactual retweeted

Jun 10

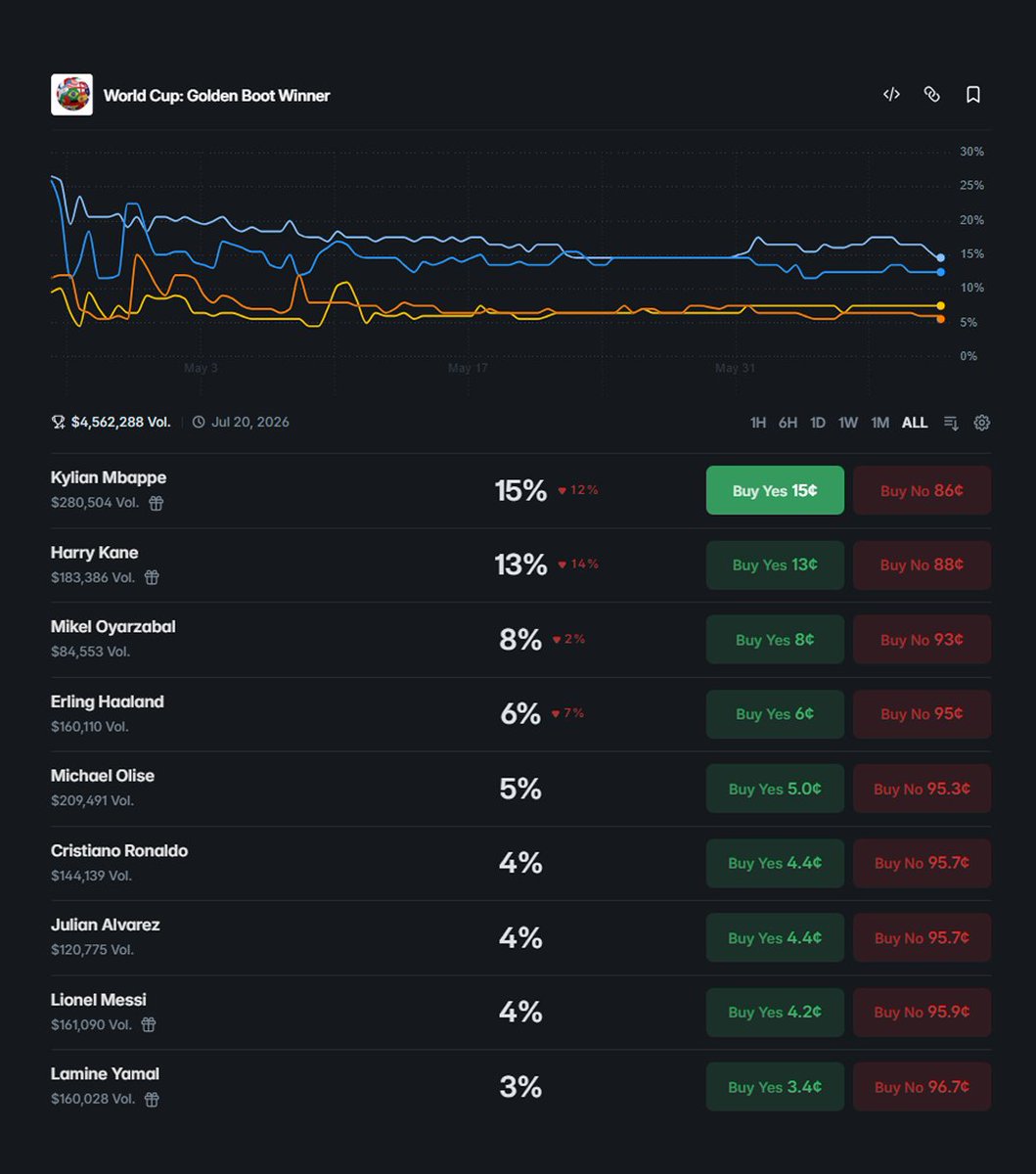

World Cup 2026 starts TOMORROW

Polymarket is where everyone is trading it right now:

>$1.86 billion traded on the World Cup Winner

France (16.2%) and Spain (16.0%) are the favorites

>$732k volume today on Golden Boot

Mbappe -17%, Kane - 13%, Yamal - 4%

>Combos are coming

How combos will work:

- You choose your legs (example: Spain wins their group Yamal scores 4 goals Spain reaches the quarterfinals)

- You send a Request and market makers compete in just 400 milliseconds

- You get one single YES/NO price, Last Look (1 second) and inventory support

What combo would you build first?

7

4

26

5,175