startup (and coconut water) propagandist

Joined July 2024

- Tweets 1,619

- Following 1,379

- Followers 2,417

- Likes 13,237

109 Photos and videos

Pinned Tweet

Jun 10

Just think of how many cans of coconut water I could have bought instead of renting this.

6

36

3,270

Rob Giani retweeted

Jun 11

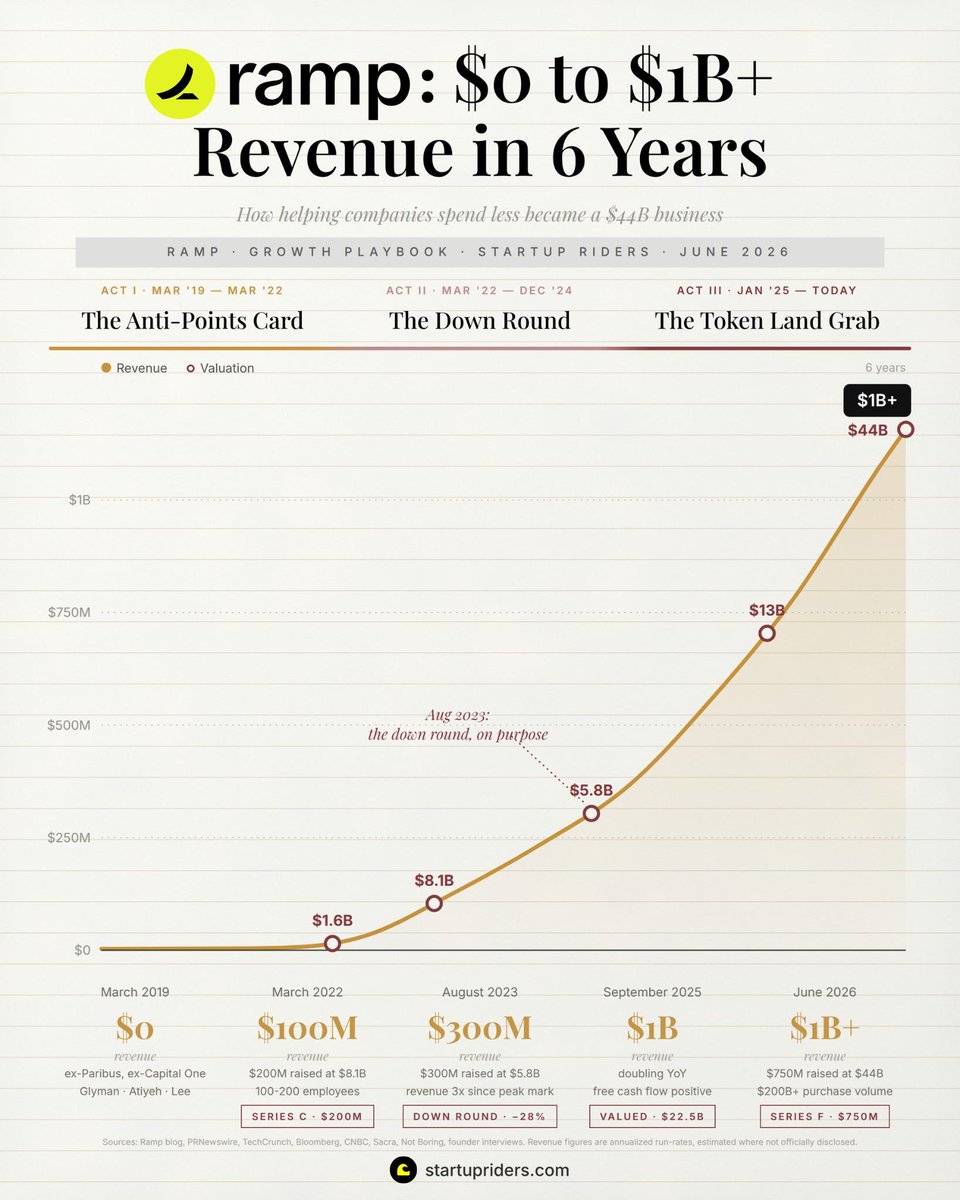

Ramp went from $0 to $1B in revenue in 6 years.

Deep-dived into 8 growth mechanics behind this $44B compounding machine that wins by "helping companies spend less"👇:

@eglyman and @karimatiyeh sold their first company to @CapitalOne in 2016 (Paribus = a tool that found you refunds on stuff you'd already bought). In 2019 they took the same idea to corporate cards, and now Capital One has bought their biggest rival (pretty poetic).

The market is a bit of a graveyard with Brex peaking at $12.3B then sold for $5.15B, Navan IPOing below its private mark and Divvy bought by Bill.

Meanwhile @tryramp compounded to $44B (with its trade-offs, also covered below)

The 8 growth mechanics I found most interesting after deep-diving into 20 founders interviews research:

1. Promised to cut your bill (flipped incentives): cards earn a fee per swipe so every card wants you spending more (that's what points are for). They pitched the opposite with a 1.5% flat cashback software that "finds waste", so CFOs trusted the card that wasn't profiting off their waste tend to move their whole spend over (nice).

2. Made the software "free" initially: Expensify or Concur charge per seat, ramp gives the same suite away because the swipe fee pays for it, so companies sign up with zero budget approval (hard to compete against).

3. Every new product recruits customers: thousands of companies came in through free bill pay or travel (aka never touched the card), each launch is a new acquisition channel (half of customers now use 2 products).

4. Shipped faster: $100M in revenue with fewer than 50 engineers and 5 PMs. Apparently one team built a Bill(.)com rival in 3 months (pre-vibe coding). Interesting product culture, @lennysan has a great deep-dive on this with @geoffintech from 2023.

5. Repriced to keep growing: cut their valuation 28% to $5.8B in 2023 while revenue 3x'd which let them keep raising hiring. Meanwhile brex defended $12.3B for 3 years and sold for $5.15B.

6. Hunted underpriced attention: a few examples of this in the playbook but direct mail for example looked like junk so nobody competed for the mailbox, which made it dirt cheap to test and ended up becoming one of their biggest channels.

7. Claimed a new spend category first: tokens are a fast-growing cost invisible to most finance tools for now and they moved first to build the tracker before the it had a proper name.

8. Turn data into free(ish) distribution: you've likely seen some of the great data produced by @arakharazianthey from their Economics Lab, they sit on real-time spend data from 50K businesses and publish it free every month, so it gets quoted a lot, great valuable loop.

Read the full deep-dive trade-offs, in my bio (@IvanLandabaso) or below 👇:

5

10

56

8,697

Rob Giani retweeted

Jun 12

Always check your DMs

1,956

1,247

25,632

2,149,213

Jun 10

I love creative OOH concepts

We just launched @eightsleep's first retail activation, and it has no fixed address.

The House of Sleep is a fully equipped Pod on wheels that drives to your neighborhood, parks outside your door, and gives you up to 30 minutes to feel what your bed has never done before.

Everyone told us to open a store. We made the store come to you. Now live in the Bay Area. eightsleep.com/house-of-slee…

2

1

20

5,815

Jun 9

I have coconut water you know what that means

1

21

1,850

Rob Giani retweeted

Jun 7

You’re always just a DM away from watching Leclerc crash out on the big screen.

Jun 4

Where are my Formula One friends at?

1

1

2

666

Jun 6

A San Francisco Grand Prix would be incredible.

4

1

146

8,587

Rob Giani retweeted

Jun 5

The @cantos thesis is basically: "Inconvenient truths"

My & @ameekapadia's text thread with Jake is at least 10% "YOU ORDERED WHAT?!?"

Jun 4

When people visit Pilgrim they are noticeably shocked by how simple it has been for us to obtain biological agents.

This is a major step in the right direction

2

1

13

4,545

Rob Giani retweeted

Jun 5

lol you just started the next thread. GP horror stories of dealing with bad LPs

Jun 4

If it makes you feel better, a LP we pitched in Fund 1 asked to meet at Monday 7am when my daughter was born 2 days before

They showed up 45 minutes late and ate a breakfast burrito during the pitch before telling me that they weren’t looking to add anything new to their book

9

2

106

73,706

Jun 5

WE ARE FINALLY MAKING IT HAPPEN

Jun 5

hola friends! rob and i are planning a pasta night in sf but we need a space. if you have a kitchen or venue we can hijack, we will literally make you the best handmade pasta of your life in exchange ❤️🔥

8

37

5,050

Rob Giani retweeted

Jun 5

My favorite comments on the FF Mafia video are all the people saying “why not Werewolf, Blood on the Clocktower, etc”.

Dudes. Just let it be what it is.

Do you watch the NBA Finals and say “you know, this would be better if they played with a football instead”?

14

4

248

37,045

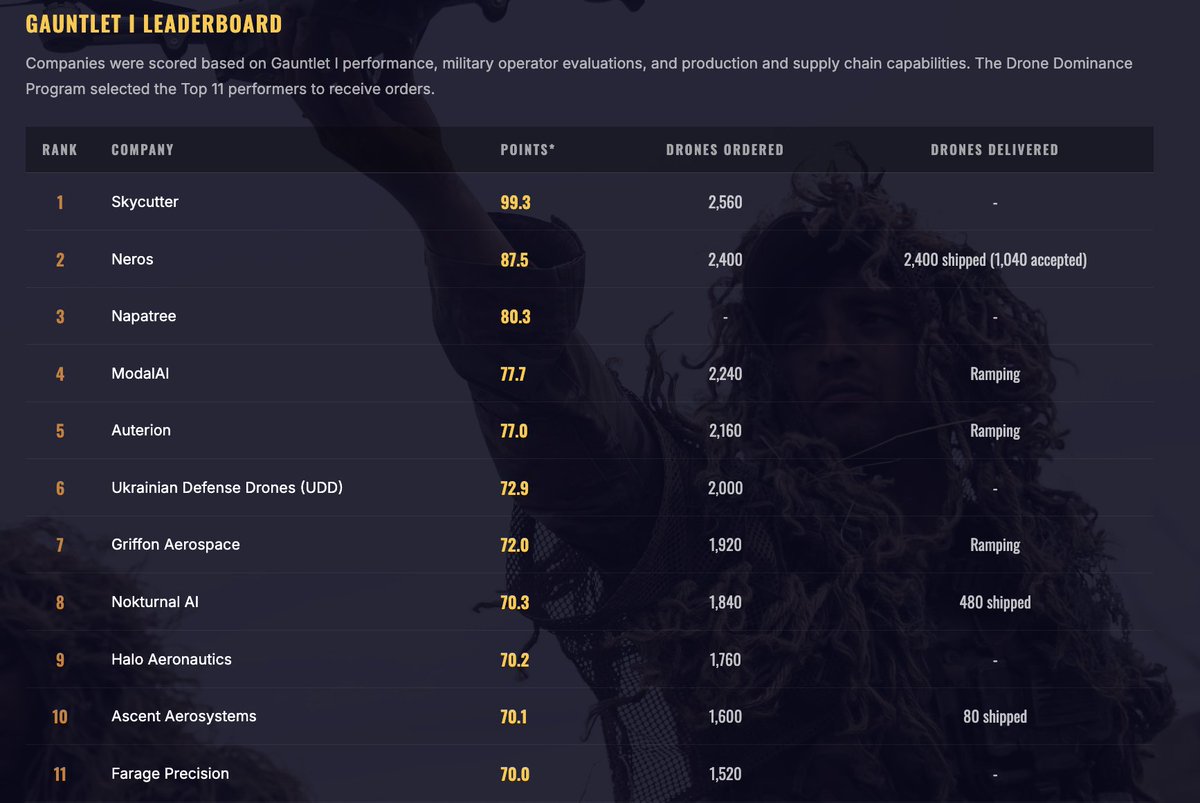

Rob Giani retweeted

Neros: 2,400

Ten other companies combined: 560

The first batch of drones ordered under the Drone Dominance Program have been accepted, and we’re just getting started. Nearly 2,000 additional units have shipped. Many more are ramping up for fulfillment.

Next up is the Gauntlet Phase II qualifiers, set to begin at Camp Grayling, Michigan next week.

dronedominance.mil/leaderboa…

#MayTheBestDroneWin

18

10

183

28,472

Jun 5

FF is about to start clipping a game show and it's going to RIP on X

11

2,294

Jun 4

Rented a movie theater to watch the Monaco GP on Sunday. Super fans only :)

Jun 4

Where are my Formula One friends at?

1

8

727