research on economics, technology, and history by @_peterryan

Joined April 2019

- Tweets 741

- Following 1

- Followers 835

- Likes 691

59 Photos and videos

Ryan Research retweeted

Jun 9

ESSAY:

I critiqued Piketty’s recent Global Justice Report for being pro-deindustrialization leveraging Reinert’s pov.

Piketty’s nice intentions could result in a reification of the same core-periphery dynamic which is the crux of global inequality.

1

2

7

1,332

Ryan Research retweeted

Jun 3

ESSAY:

The Irish Revolution Was Not Marxist

A debate arose on what economic ideology the Irish revolutionaries held. In response, I've catalogued primary sources during the years of the Irish Revolution which articulate a sufficient summary of their beliefs in their own words.

1

4

24

3,322

Ryan Research retweeted

Jun 1

What is the new "Hollywood / Platform model" of venture capital and why could it be bad for business?

"It all supports the idea that scale in venture capital is good because the bigger you are then the more attention you get and the bigger your brand etc. It's all pushing back on the idea that, if you look back on the historical data of venture capital, big is bad actually. Big funds mean worse returns...But they are desperate to challenge this idea because it challenges the entire thesis of scaled venture platforms. So they invent this stuff of platform teams and media arms to justify that scale has an advantage when the honest take on it is that it's a disadvantage." - @credistick

May 30

PODCAST:

I'm joined by @credistick of @JoinOdin to discuss venture capital and ask the question: is it in crisis?

We discuss VC history, how it works, good vs. bad models, IPOs, VC econ, govt's role, and the EU vs. US startup debate.

(link below)

1

2

4

1,052

Ryan Research retweeted

May 30

What is the difference between a16z vs. Union Square Ventures?

"The question you really have to ask is: which firm is doing more good for the world? I would say the case is pretty clear that it's Union Square Ventures.

Andreessen Horowitz manages so much money and has so many partners that they end up investing in stuff that, honestly, I think is so dumb that surely most of them can't know they even invested in this stuff because someone would say we shouldn't be doing this. Crypto casinos, weird degenerate NFT play-to-earn games...All this kind of stuff where the economics don't even make sense.

At some point, you are managing too much money to make good decisions with it."

- @credistick

May 30

PODCAST:

I'm joined by @credistick of @JoinOdin to discuss venture capital and ask the question: is it in crisis?

We discuss VC history, how it works, good vs. bad models, IPOs, VC econ, govt's role, and the EU vs. US startup debate.

(link below)

2

4

1,402

Ryan Research retweeted

May 30

"Would you describe the current state of venture capital as in a crisis?"

"Yes...if you look at how capital flows through all of this towards the exit. Then you have a bunch of managers with very large funds who are basically looking for places to allocate that money who can absorb it. All they really need is investments that will be marked up enough that they can raise the next fund and hopefully a larger fund. So they are looking for short term growth and that is fundamentally at odds with what venture capital should be which is patient money for long horizon ambitious ideas that may take 10 to 15 years to work out in some cases.

So then you have the problem of a ton of investors managing a ton of money investing in companies that can grow very well but maybe aren't producing the value that they need to to be attractive acquisition targets or IPO candidates so they can't exit."

- @credistick @JoinOdin

May 30

PODCAST:

I'm joined by @credistick of @JoinOdin to discuss venture capital and ask the question: is it in crisis?

We discuss VC history, how it works, good vs. bad models, IPOs, VC econ, govt's role, and the EU vs. US startup debate.

(link below)

3

10

2,208

Ryan Research retweeted

May 30

PODCAST:

I'm joined by @credistick of @JoinOdin to discuss venture capital and ask the question: is it in crisis?

We discuss VC history, how it works, good vs. bad models, IPOs, VC econ, govt's role, and the EU vs. US startup debate.

(link below)

2

3

7

5,582

Ryan Research retweeted

May 15

ESSAY: The Man Who Created Ireland's Celtic Tiger

Economist Erik S. Reinert's role in catalyzing Ireland's Celtic Tiger in the 1980s as the thinker behind the Telesis Report.

ryanresearch.substack.com/p/…

1

3

12

1,199

Ryan Research retweeted

May 15

ESSAY: Irish Solidarity with Cuba, Dominican Republic, and Haiti Against Wall Street Imperialism

Early 20th century nexus of financial anti-imperialism from pov of Irish revolutionaries sympathizing with "dangers of American finance" in island nations.

ryanresearch.substack.com/p/…

1

5

9

1,218

Ryan Research retweeted

May 1

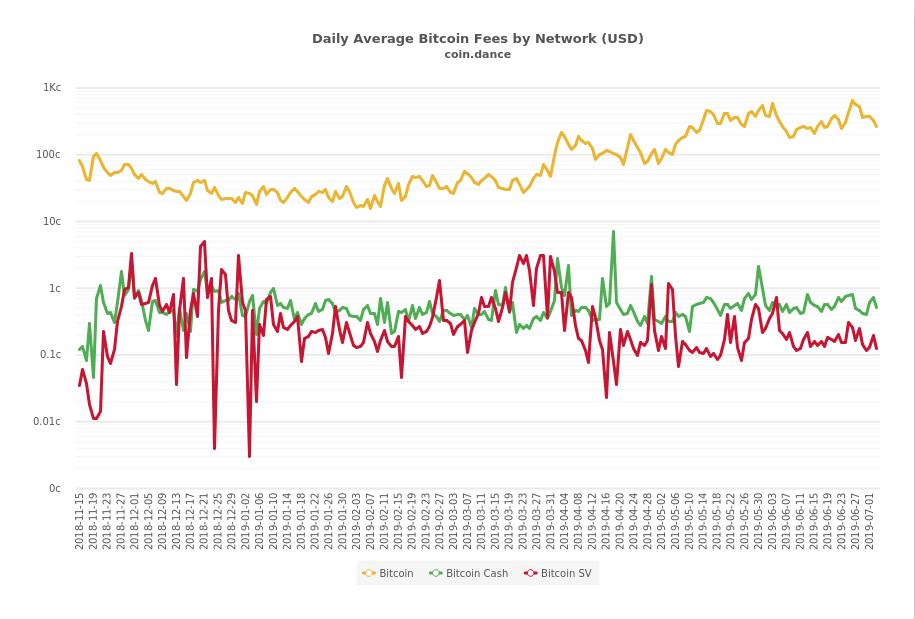

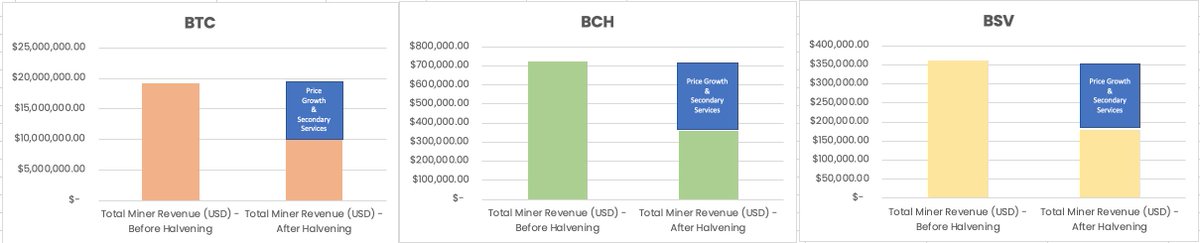

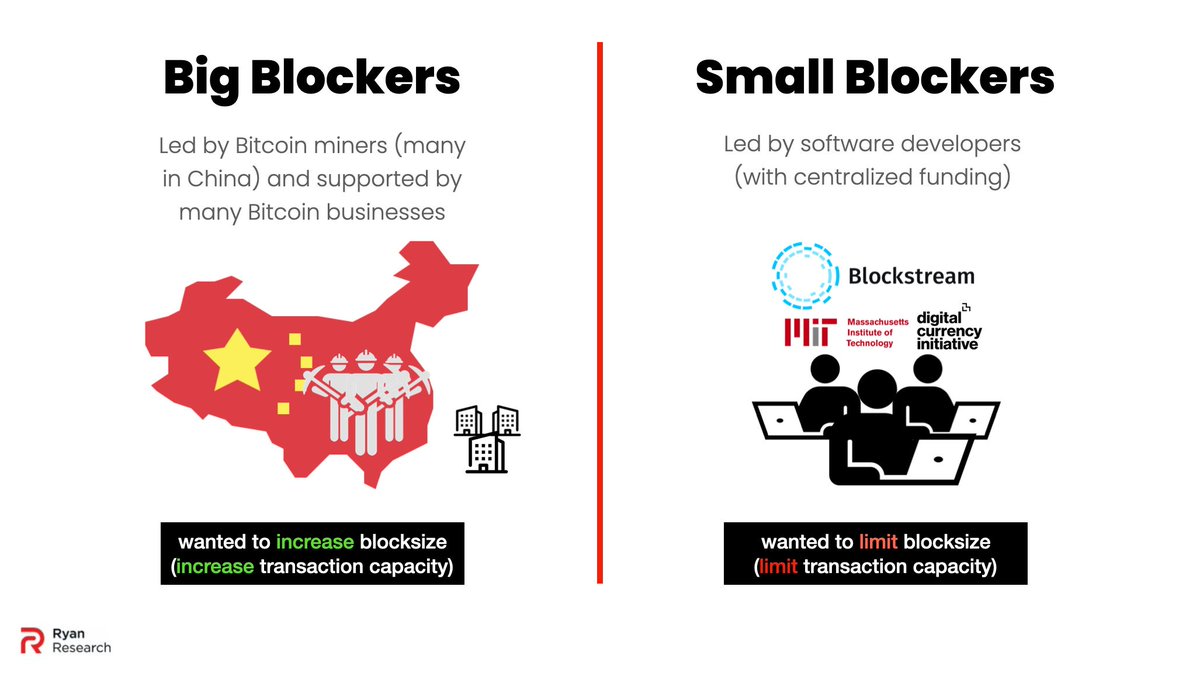

I released an excerpt of my “Money by Vile Means” ebook to layout the definitive yet untold history of the Bitcoin Scaling War. you can’t know Bitcoin, if you don’t know this history. Once, you understand this, everything falls into place. Ultimately, it shows why Bitcoin and its libertarian / decentralized philosophy is wrong.

May 1

ESSAY:

A History of the Bitcoin Scaling War (2014-2019)

It demonstrated the failure of Bitcoin theory to reflect Bitcoin reality. The only way to understand Bitcoin is to understand the Scaling War.

ryanresearch.substack.com/p/…

1

4

509

Ryan Research retweeted

May 1

ESSAY:

A History of the Bitcoin Scaling War (2014-2019)

It demonstrated the failure of Bitcoin theory to reflect Bitcoin reality. The only way to understand Bitcoin is to understand the Scaling War.

ryanresearch.substack.com/p/…

2

4

1,670

Ryan Research retweeted

Apr 28

ESSAY:

Arthur Griffith's Economics: The Economic Doctrine of the Original Sinn Féin and the Revolutionary Irish Republic

ryanresearch.substack.com/p/…

3

8

789

Ryan Research retweeted

Apr 27

1/ ESSAY:

From Wall Street to Weird Street: A History of Venture Capital

America was seen as the beacon of free market capitalism, but in recent years it has become a dumpster fire of venture capitalism.

How did that happen? Or more so, when did it go wrong?

1

4

11

2,923

Ryan Research retweeted

Apr 22

NEW PODCAST:

@1DimeOfficial joined me to chat about our shared desire to critique contradictions and insufficiencies of the left-right dichotomy in pursuit of substance.

We cover economics, history, politics, and philosophy for a very deep conversation.

Link below:

1

3

5

1,627

Ryan Research retweeted

Mar 25

PODCAST:

Realism vs. Imperialism with @ChrisDMott of @Diplomacy_Peace.

We discuss the history and current iteration of American imperialism, and then contrast that with Mott's "Washingtonian Realism."

Listen below and on all major podcast platforms.

2

6

7

2,940

Ryan Research retweeted

Mar 12

9/ Bottom-line: There are problems with the Irish banking sector and investment environment, but this new scheme has many risks. Harris’ proposed investment scheme could end up decreasing economic activity inside Ireland while sending money off to the rest of world. Ireland should find other solutions closer to home like inflicting bank penalties, encouraging new entrants, and upgrading its postal banking system.

ryanresearch.substack.com/p/…

4

1

3

458

Ryan Research retweeted

Mar 12

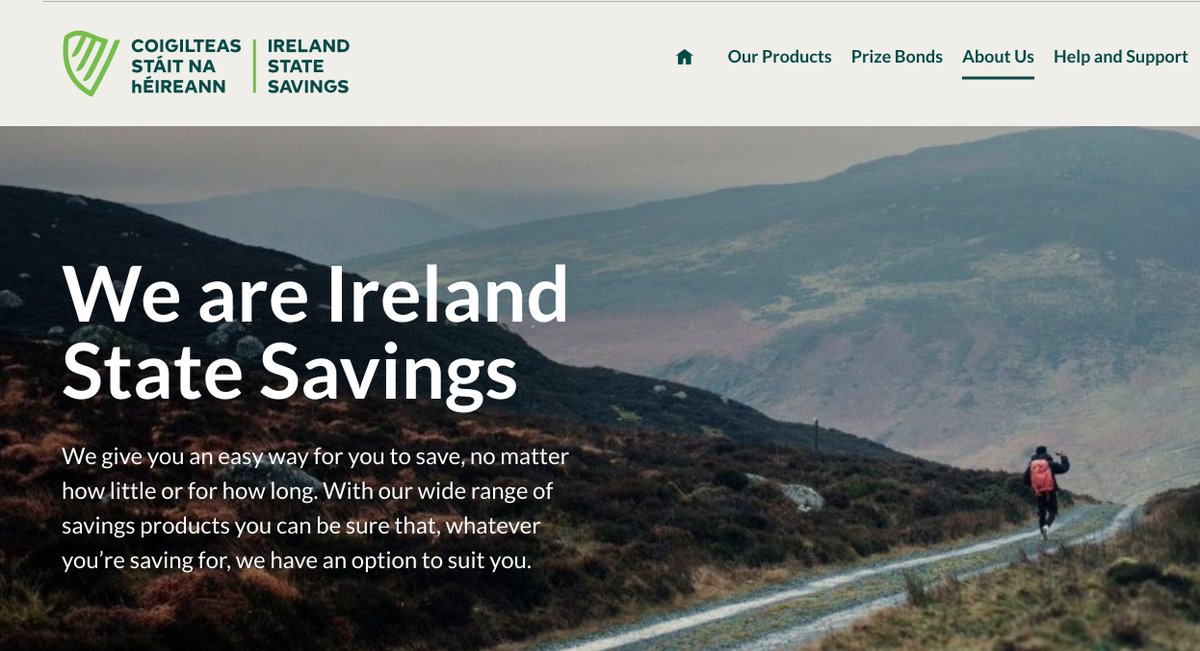

8/ The Irish government already has some measures at its fingertips. Ireland State Savings is the brand name used by the National Treasury Management Agency (NTMA), on behalf of the Minister for Finance. An Post acts as an agent of the NTMA in relation to the sale and administration of Ireland State Savings products. Ireland State Savings currently offers a deposit account paying 0.75 percent. Irish banks offer 0.13, as quoted by Pope last November, to 0.14 (nearly half the Euro Area average), according to the Central Bank of Ireland’s latest report.

A state-owned entity is already offering more than 5 times the amount of interest on deposits as Irish banks. Given that an Ireland State Savings / An Post account has the limitations of no online access, in-person transactions, and so forth, the Irish government should be interested in upgrading these services to make these accounts more accessible and useful to Irish depositors.

Postal banking is much more sound than Harris’ proposed scheme with unclear outcomes. The Roosevelt Institute’s Emily DiVito explained how postal banking systems are historically proven, reliable institutions, and progressive as they help the poorest most (corroborated by The Democracy Collaborative). Postal banking systems are also used all over the world and there are many models to learn from and implement in Ireland.

The Irish government should consider improving and expanding its role as a banking services provider. This would increase competitive pressures on Ireland’s uncompetitive banking sector to incentivize Irish banks to offer better deals to their customers. There could be other encouragements for new private entrants to increase competition, but this is a direct and readily available way to do it. It would enable the “hard-working people doing the right thing” (as Harris said) to be properly rewarded and for Irish money to stay inside Ireland to fund Irish businesses and not foreign ones.

ryanresearch.substack.com/p/…

1

1

2

234

Ryan Research retweeted

Mar 12

7/ It is unlikely that the proposed scheme will greatly expand investment inside Ireland. It risks actually contracting the economy by reducing the lending capacity of Irish banks and making foreign investments more attractive than Irish ones through tax incentives. If this scheme is derived from a desire to provide Irish depositors more interest on their deposits, then aren’t there better ways to go about it?

Why can’t the Irish banks provide more interest on deposits (especially when they are shown to be outliers in the prior country comparisons by the FT)? Why can’t the Irish government legislate that Irish banks should pass on more interest through tax penalties or the like? If it can’t be done at the national level, why can’t it be pursued at the European level? These are questions that should be asked and offer different policy paths than the one Harris is walking down.

ryanresearch.substack.com/p/…

1

1

2

189

Ryan Research retweeted

Mar 12

3/ Irish depositors are not fairly compensated by Irish banks relative to their counterparts in other countries. Harris was correct to criticize this. Thus, Harris devised that funnelling some of the deposits away from Irish banks to investment accounts would allow for Irish savers to get more return on their money. While this seems like it would better reward Irish savers and drive new investment, it could also impose problems.

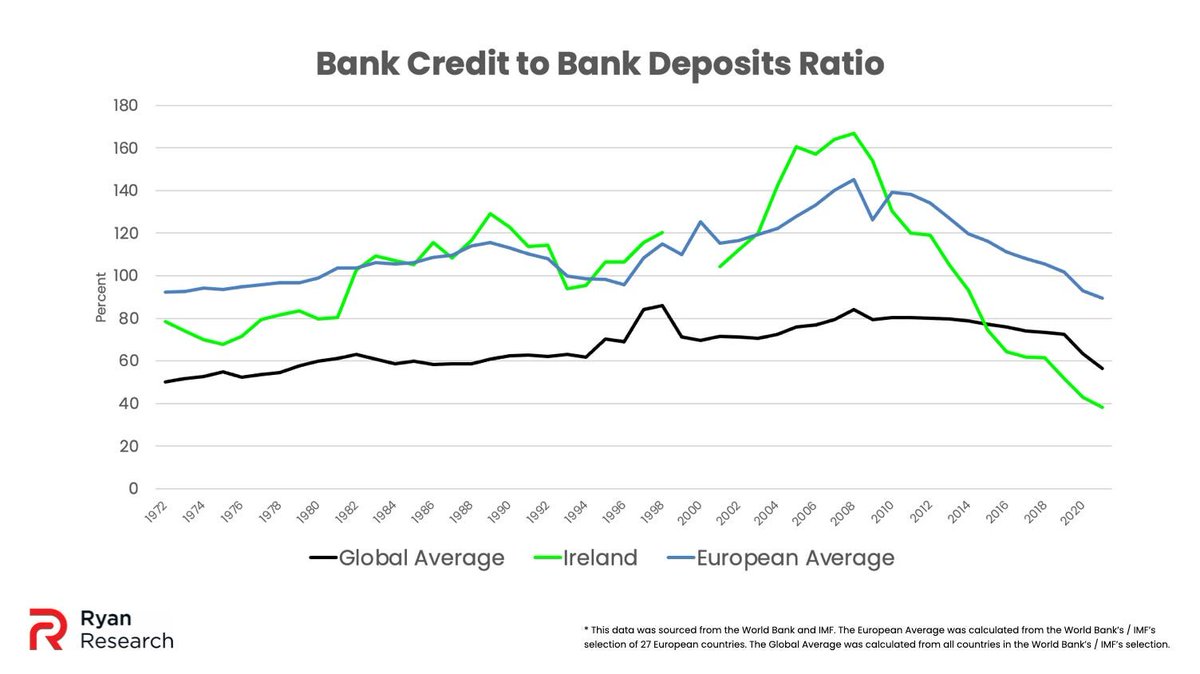

A bank is a business that takes deposits and transforms them into loans. In theory, the more deposits a bank holds, the more loans a bank can issue. If Harris’ goal is to decrease the amount of deposits held in banks, it must logically follow bank capacity to issue loans also decreases. Analysts speculated that Harris’ scheme would decrease deposits in Irish banks by 10 percent. This is in the context of an Irish bank loan shortage caused by many internal and external problems with the Irish banking sector.

“Ireland’s bank credit to bank deposit ratio was 38 percent as of 2021.” Relative to Ireland, “from 1972, the ratio declined by 52 percent. From 1960, the ratio declined by 38 percent.” Relative to Europe, “Ireland’s 2021 bank credit to bank deposit ratio was 57 percent below the European average. For example, it was 57 percent lower than Germany’s, 59 percent lower than the Netherlands’, 65 percent lower than France’s, 75 percent lower than Sweden’s, 78 percent lower than Norway’s, and 86 percent lower than Denmark’s. Ireland has the second lowest recorded ratio in Europe.”

ryanresearch.substack.com/p/…

2

1

2

329

Ryan Research retweeted

Mar 12

2/ Tánaiste and Minister for Finance Simon Harris proposed a new investment scheme to shift Irish bank deposits towards tax-incentivized vehicles. This would be in concert with a general European push for a similar strategy. Although suggested to be beneficial for the Irish economy, this new proposal could do more harm than good.

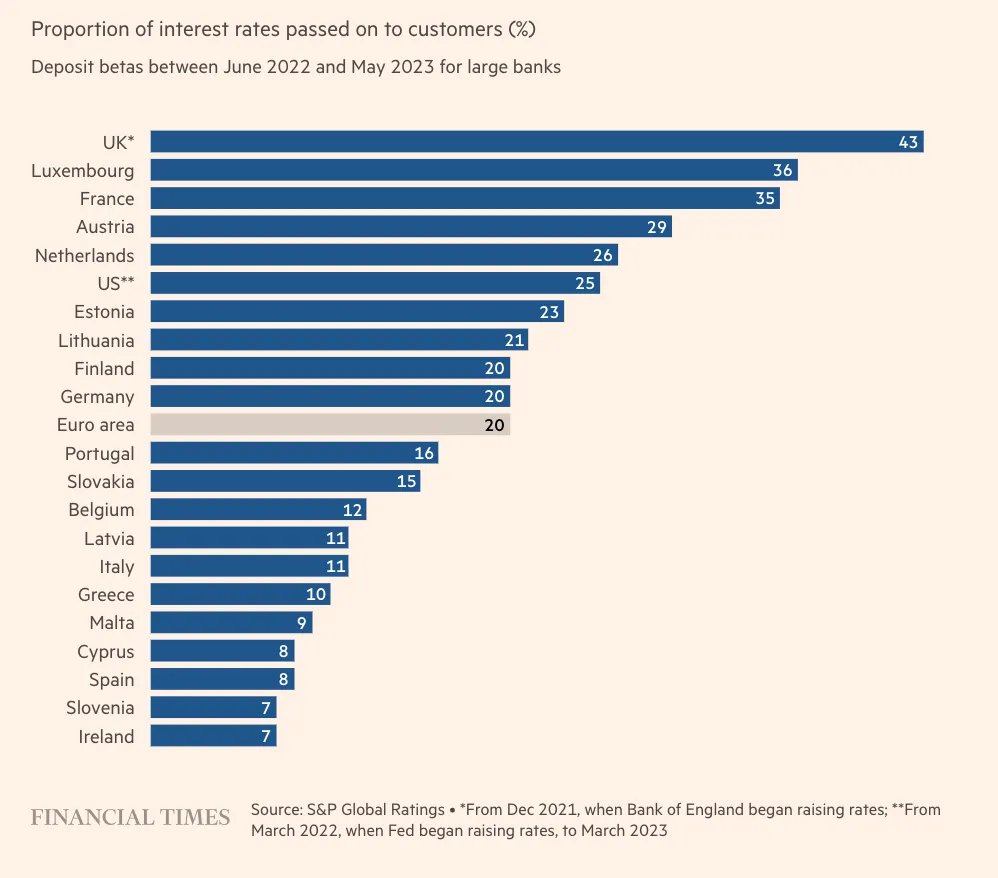

According to Harris, the primary motivation is that “hard-working people [are] doing the right thing - and that is saving - but not being rewarded for it.” In other words, Harris alleged the Irish banks are not paying sufficient interest to their depositors. This allegation was warranted. The Financial Times reviewed the proportion of interest rates passed on to customers by country. Of the sample, Ireland was the lowest ranked.

In the Irish Times, Conor Pope wrote, “Irish savers have been offered rates that could best be described as miserly for a long, long time. Those who have money on deposit have been getting some of the lowest returns in the euro zone over the last decade or so. A recent survey from fintech Raisin suggested that the average overnight deposit rate offered in Ireland was 0.13 per cent compared with 0.55 per cent in Germany.”

ryanresearch.substack.com/p/…

1

2

4

506

Ryan Research retweeted

Mar 12

1/ Harris' Investment Scheme Risks Sending Money Overseas and Squeezing the Economy at Home

Moving bank deposits to tax-incentivized investment accounts could do more harm than good.

Other solutions exist closer to home.

2

3

11

5,567