Curious & user obsessed fintech product maker. Innovation, Design, Security, Better markets, Stablecoins, Payments, Crypto. (Arculus Wallet), Cards

Joined July 2008

- Tweets 7,012

- Following 1,523

- Followers 788

- Likes 1,868

201 Photos and videos

Where exactly do you file for a pardon? Is there, like, a website?

Jun 8

Former FTX CEO Sam Bankman-Fried officially files for a presidential pardon from Trump theblock.co/post/404001/ftx-…

17

You can call stablecoins "private money," but post-GENIUS, regulated private money. "Private money" isn't a risk to the economy. But, 20 years ago, mortgage lenders & investment banks actually almost tanked the entire global economy without stablecoins.

wsj.com/finance/currencies/s…

25

Tom D retweeted

Last time Knicks went to the NBA Finals we still had The Wiz

84

365

2,377

128,762

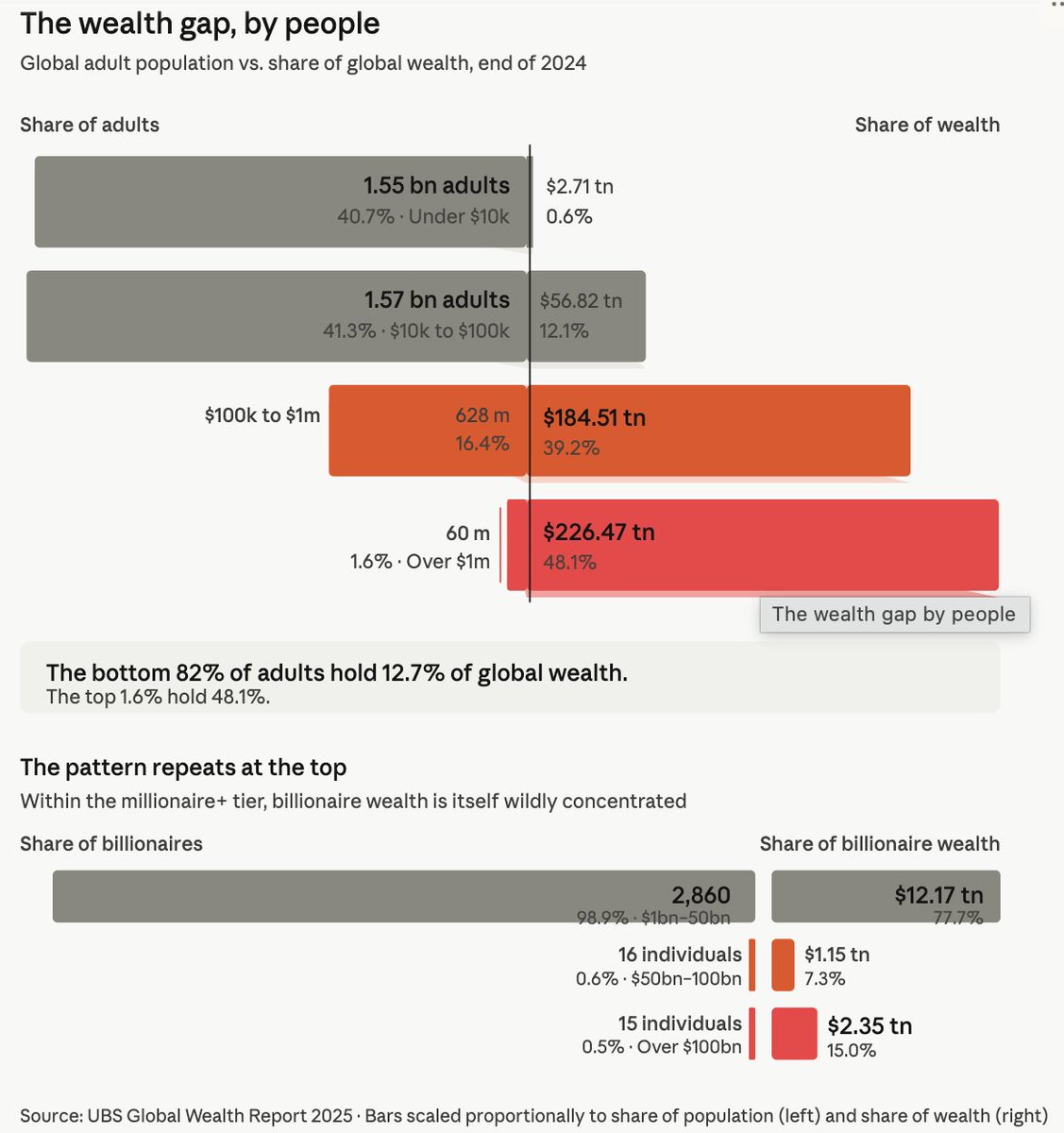

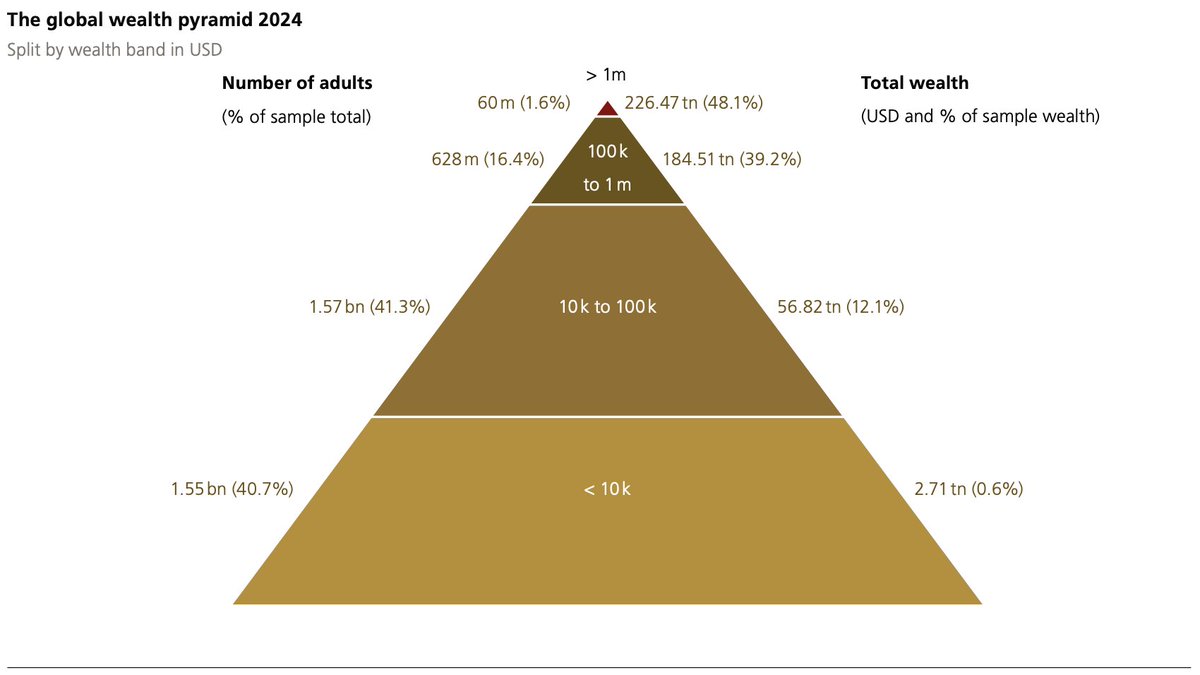

From a data visualization perspective, UBS's pyramid isn't very good. Let's make a better version using the same data:

May 24

Only 60 million people on earth (1.6% of adults) have a net worth over $1 million.

Those 60M people hold 48% of all global wealth.

The bottom 1.55 billion hold 0.6%.

Source: UBS Global Wealth Report 2025

1

41

Tufte and AI - the world has come full circle.

(But seriously - AI should learn from him)

May 22

Earlier this year I was getting frustrated with Claude's charts, fed this book to claude and had it generate a Tufte skill. Instantly got simpler/more beautiful visualizations.

gist.github.com/aparente/e48…

70

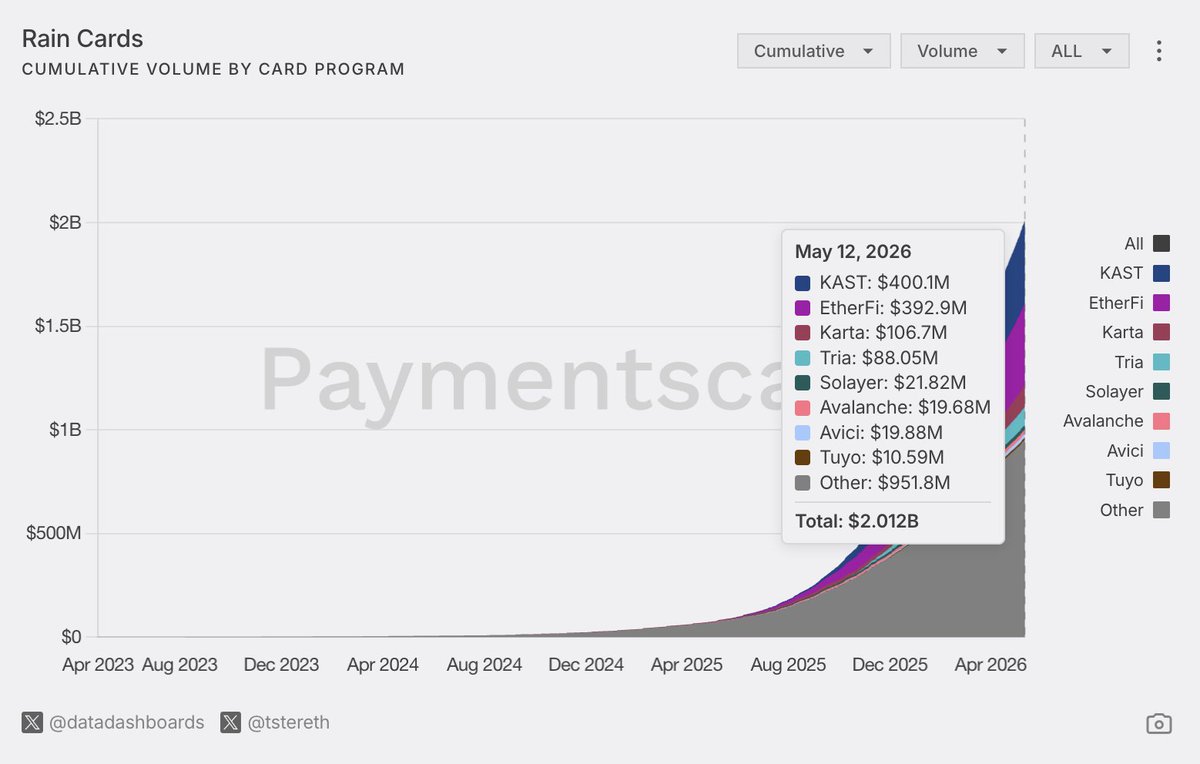

Amazing! Way to go @raincards team!

May 13

BREAKING: @raincards has crossed $2 BILLION in all-time stablecoin card payments.

Top card programs powered by Rain include KAST, EtherFi, and Karta.

1

97

If this post below sounds like a scam, it's because it is a scam.

Breaking 🚨 We're about to face a big crash

Stop depending on cold storage options like Ledger or Arculus.

Use a decentralized wallet and secure it with Web3 backup - or you might lose your assets.

Exchanges are not safe anymore

Message me privately for more information

49

Tom D retweeted

Apr 8

I run Compensation Analytics for a Fortune 500 company.

My job is to calculate the lowest salary you'll accept.

Not the salary you deserve. Not the salary the role requires. Not the market rate. The minimum number that keeps you from walking.

I know this number before you walk in. Sometimes before you apply.

We buy data. Your payroll processor shares your salary history with Equifax through a product called The Work Number. More than 800 million employment and income records. Updated every pay cycle. Equifax sells it to us through a "verification of income" API. The word "verification" means we know what you made at your last three jobs, whether you got a raise, and when you didn't.

That's market intelligence.

We layer signals. Credit card utilization. Payday loan activity. Past-due balances. Delinquent debt. Address changes. There are about 500 vendors that aggregate this data now. An audit by the Washington Center for Equitable Growth flagged 20 as high-risk for enabling algorithmic wage discrimination. Sixteen of the twenty plug directly into payroll and HR systems. We use nine.

The dashboard has a field called "candidate tolerance threshold." That's the number. The lowest salary you'll accept. We set the offer at 3% to 6% above it. Enough to feel like negotiation. Not enough to change your life.

That's compensation design.

The academic term is "surveillance wages." The industry term is "compensation optimization." A law professor named Veena Dubal found that when multiple employers in the same market use the same vendors, it functions as de facto price-fixing of labor. Same mechanism as the RealPage rental pricing scandal. Same logic. Same outcome. RealPage coordinates rents. Our vendors coordinate salaries. Different commodity. Same extraction.

That's the market.

Here's what the algorithm sees when you apply. Your last three salaries. Your debt-to-income ratio. How quickly you accepted your previous offer. Your zip code. Whether you've used a payday lender in the last two years. It calculates your reservation wage and sets the offer just above.

Your performance doesn't set your salary. Your desperation does.

A new VP of Total Rewards asked me why the algorithm used payday loan history. I explained that payday usage correlates with financial fragility, and financial fragility predicts acceptance velocity. She asked if that was legal. I said it was standard. She asked whose standard. I showed her the vendor's compliance page.

She transferred to a different division. That's organizational learning.

Colorado introduced a bill to ban the practice. HB25-1264. It would prohibit using payday loan history, location data, and search behavior to set algorithmic pay offers.

The companies lobbied against it. The same companies that told their employees they don't use surveillance wages.

A state representative asked the obvious question: "If these companies don't pay surveillance wages, then what is the problem of codifying in law that you're not allowed to?"

The lobbyists provided written testimony. They said the bill would create "compliance burden." They did not answer the question.

That's advocacy.

The data flows in one direction. We know your salary trajectory. You don't know ours. We know what you'll settle for. You think you're negotiating. The algorithm already accounted for your counter. It budgeted for exactly one round.

There is a freeze option. You can go to Equifax's website and freeze your Work Number file. Most people don't know it exists. We don't mention it in the offer letter. We don't mention it in the onboarding packet. We don't mention it in the benefits portal. We don't mention it anywhere.

That's by design. The system requires your ignorance to function. If everyone froze their data, compensation optimization would have nothing to optimize.

I froze mine the week I started this job. I work in Compensation Analytics. I know what the tools see.

I just build them for everyone else.

75

365

1,269

176,134

Tom D retweeted

May 10

My latest deep dive with a full collection of stablecoin card program enablers is out.

If you were looking for a provider to launch:

• stablecoin-linked cards

• crypto debit cards

• treasury spend cards

• embedded finance products

• cross-border stablecoin payment flows

This guide breaks down the infrastructure landscape in one place.

I covered:

• @NiumGlobal

• @raincards

• @Stablecoin

• BVNK

• @stripe

• @BaanxGroup

• @KulipaXYZ

• NAKA

• Reap

• StraitsX

• @gnosispay

• @ChainUpOfficial

• @thisisarculus

• @wirexapp

And more.

The report also explains:

• MiCA and GENIUS Act implications

• on-chain vs fiat settlement

• JIT conversion models

• compliance and Travel Rule requirements

• chargeback risks

• tax reporting challenges

• liquidity and slippage management

• agentic commerce implications

Most conversations around stablecoin cards still focus on hype.

The harder question is operational:

Who actually enables issuance, settlement, compliance, liquidity, custody, and global acceptance?

That is what this deep dive maps out.

Save this article. You will likely come back to it multiple times if you are building in stablecoins, payments, embedded finance, or card infrastructure.

open.substack.com/pub/sambob…

10

14

87

10,086

FYI, whenever you see someone posting nonsense about backing up with a "decentralized wallet" or "Web3 backup" they are scammers trying to steal you assets.

13

If you ever see a post like this one - "decentralized wallet" or "web3 backup" - it's a scam. They will steal your coins every time.

Stop depending on cold storage options like Ledger or Arculus. Use a decentralized wallet and secure it with Web3 backup — or you might lose your assets.

22

Real portable self-custody where you hold your own keys is the answer.

getarculus.com

qz.com/aws-data-center-outag…

8

Tom D retweeted

May 5

Big update just dropped 📣 @monad has arrived on @thisisarculus.

The lightning-fast speed of Monad, backed by the uncompromised security of Arculus cold storage. Securely store and manage your assets on Monad directly from your Arculus app ➕ with WalletConnect support, access the Monad DeFi ecosystem 🤝

1

9

501

Many of the most successful crypto/stablecoins metal cards are built by @thisisarculus / @CompoSecure Why metal? Users prefer metal cards. Metal cards get used more. Arculus metal cards can be multifunction security devices.

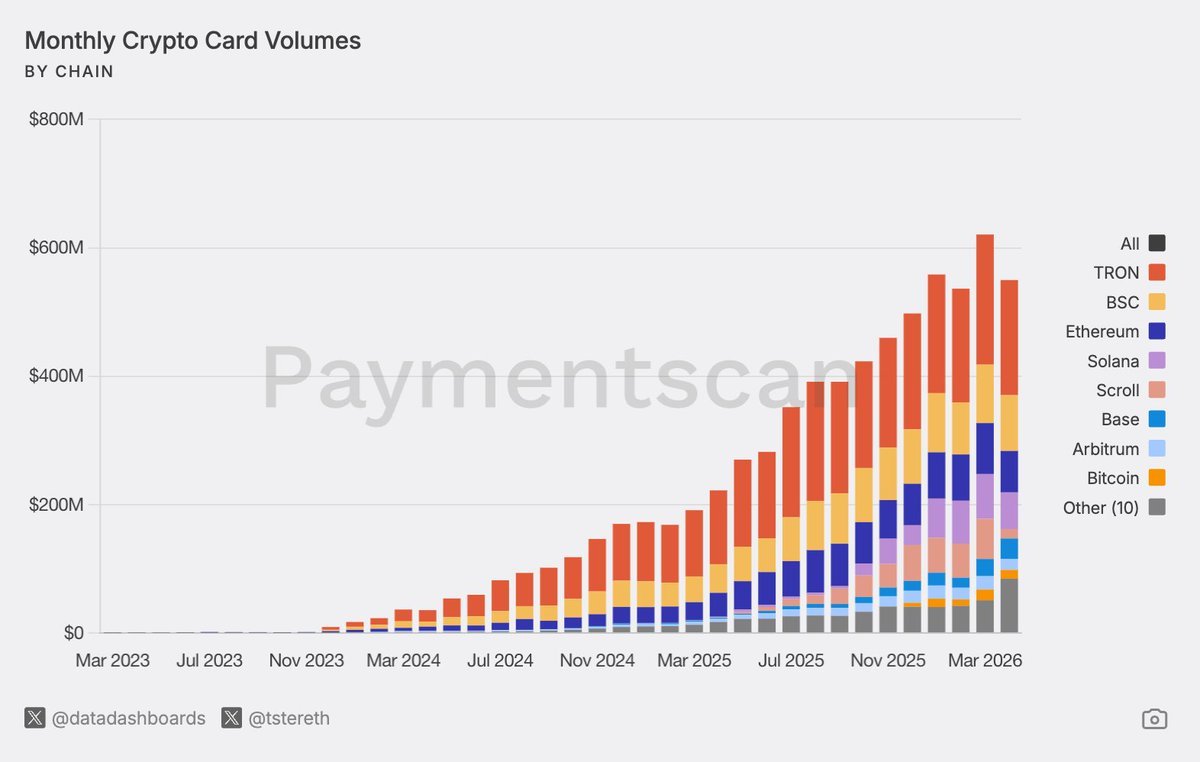

Visa is absolutely DOMINATING stablecoin payments, specifically for crypto cards.

The numbers are actually insane too like, pretty sure it’s somewhere close to 95-98% of crypto-linked cards are powered by Visa.

When you combine that with the face that crypto-linked card spending volume has increased 500% since September 24' and is now running at $600 mill/mo, you can see how this is going to be a massive revenue generator for Visa.

Naturally I asked their head of stablecoin strategy how big of an opportunity this:

He says they are doing BILLIONS/year in revenue from just one stablecoin settlement product and the crypto card product is something they are betting heavily on.

He mentioned Rain quite a bit throughout this show as the company powering a lot of these cards as well.

Clearly they are thinking deeply about how stablecoins will be integrated as a monetizable product line.

Where’s MasterCard or Discover or anyone else in this race???

3

90