Joined October 2010

- Tweets 4,928

- Following 982

- Followers 759

- Likes 6,465

584 Photos and videos

EVERY ROSE HAS ITS THORN 🇺🇸

@Justin_Gaethje defeats Ilia Topuria by TKO, due to Corner Stoppage, to become the NEW undisputed lightweight champion of the world.

[ #UFCWhiteHouse | B2YB @CryptoCom ]

1,358

4,986

27,179

843,543

Block retweeted

Jun 8

This market cannot handle another hyperscaler offering without taking a big hit right now

207

71

1,178

346,268

Block retweeted

Jun 1

New Era Energy & Digital ($NUAI): A bull case for an AI-infrastructure story the market is still underestimating

NUAI is a re-rating in progress. A former Permian Basin E&P that has pivoted into large-scale AI/HPC data-center development, the company is systematically retiring the legal and capital-structure overhangs that have kept institutional capital on the sidelines — while the equity still trades closer to the baggage than to the platform underneath it. The setup is the familiar small-cap asymmetry: a genuinely scarce underlying asset priced at a discount to its de-risked value because the market has not yet marked the clean-up to par.

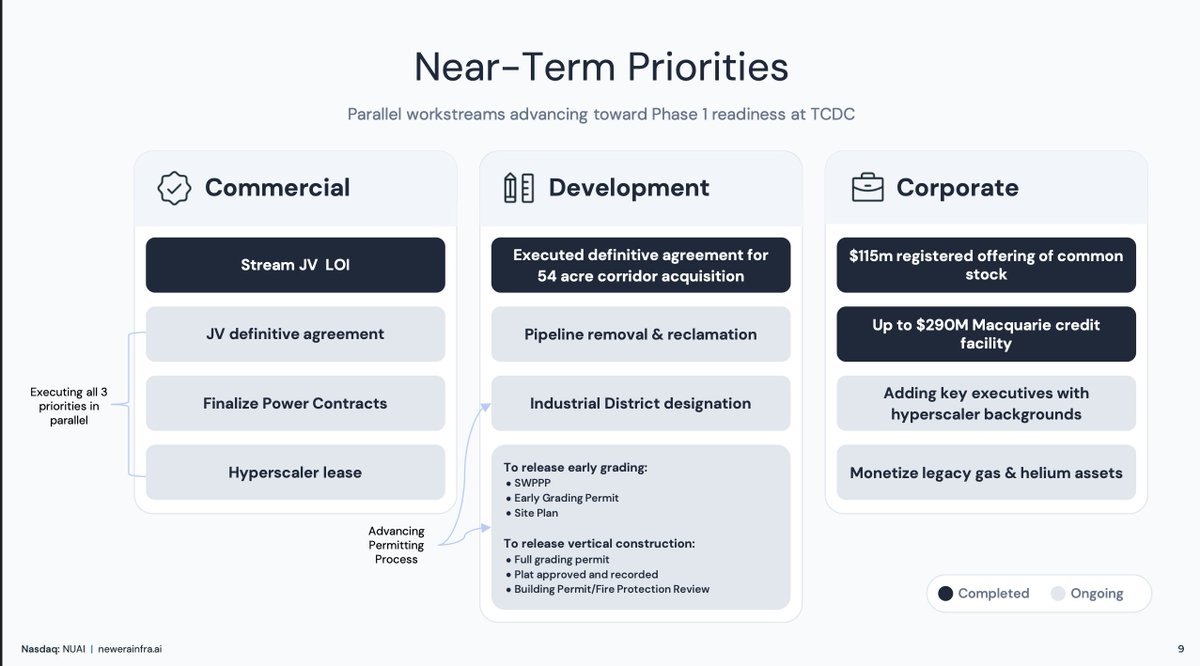

The asset is Texas Critical Data Centers (TCDC), a ~492-acre campus in Ector County, Texas, with ~650 MW of capacity secured and a design that scales toward 1.4 GW. The thesis in one line: management is clearing overhangs faster than the stock has repriced, while assembling the financing, operating, and commercial partnerships needed to convert powered land into contracted, project-financed cash flow. The sections below lay out the de-risking, the platform being built against it, the capital-markets catalysts, the Street's early valuation work — and, in fairness, what has to go right for the gap to close.

The defense: clearing the overhangs

Sharon AI is gone — and paid in cash. The single largest structural overhang was NUAI's partnership obligation to Sharon AI in the TCDC joint venture. That chapter is now closed. NUAI consolidated full ownership of TCDC, and on April 24, 2026 it repaid the remaining $50 million senior secured convertible note to Sharon AI entirely in cash, plus accrued interest — eliminating the conversion-driven dilution that had been hanging over the share count. Total consideration on the buyout came in around $74 million, and crucially, Sharon AI retains no ownership, governance, or control rights in the campus. A messy, two-headed JV became a clean, wholly owned flagship.

The ATW structure has been de-risked. Earlier in the year the company scrapped a planned convertible preferred issuance — exactly the kind of variable-priced instrument that tends to grind small-cap charts lower — in favor of an amended waiver with ATW AI Infrastructure II that reset warrant exercise prices to a fixed $2.00. That converted a potentially toxic, open-ended dilution mechanism into a known, fixed-strike overhang that is now being worked down as warrants are exercised. It is not fully retired — there remain unexercised warrants on the books — but the shape of the dilution is dramatically friendlier than it was, and the worst-case path is off the table.

The New Mexico lawsuit is being settled. On May 28, 2026, the company announced a pending agreement that would dismiss every State of New Mexico claim against New Era — five claims in total — for a $1 million payment to the bankruptcy trustee, subject to court approval. The stock moved double digits in after-hours trading on the news, a sign of just how much the litigation cloud had been weighing on sentiment. This removes the corporate legal overhang that had made many institutions reluctant to underwrite the story.

The offense: building a platform that can execute

Removing overhangs only matters if there's something worth de-risking. Since March, the moves on the offensive side have arguably been more important than the defensive ones:

A real CFO for a capital-intensive business. In March, NUAI brought on Ted Warner as Chief Financial Officer. This is not a generalist hire — Warner ran Northland Capital Markets' Energy, Power and Digital Infrastructure practice, which since 2023 has structured more than $7 billion of financing for large-scale data-center development. For a company whose entire value-creation path runs through project finance and capital partnerships, hiring a banker who has actually closed this exact type of deal is a tell.

Macquarie validated the asset. Also closed in early April: a multi-tranche senior secured term loan credit facility of up to $290 million with Macquarie Group, earmarked for the TCDC flagship. A blue-chip infrastructure lender does not extend a facility of that size against a project it hasn't diligenced. Combined with a $115 million registered equity offering, management reported $80 million-plus in cash as of April 30 — runway to actually execute rather than survive.

The bench is now stacked with hyperscaler-native talent. What had been a thin team is being built out quickly. On June 1, NUAI named Evan Pierce as Chief Development Officer and Michael Johnson as General Counsel and Chief Compliance Officer — and the pedigrees matter as much as the titles. Pierce spent two decades on the customer-and-infrastructure side of this exact business: most recently leading data-center site and energy development for the Americas at EdgeConneX, and before that in energy, utility-engagement and capacity roles at Amazon/AWS and ByteDance, with a hand in planning more than 5 GW of data-center and power infrastructure. NUAI effectively just hired someone who has sat in the hyperscaler's seat and knows exactly how these tenants evaluate sites and procure power.

Johnson, the new GC, arrives from CoreWeave and, before that, Switch — two of the most relevant names in the industry — bringing three decades of data-center leasing, powered-land acquisition, construction and financing experience. Pairing a heavyweight GC with a dedicated compliance mandate also signals a deliberate institutionalization of governance, which is precisely what an investor base wary of the litigation overhang wants to see. You don't recruit people like this to sit idle; you recruit them to paper a lease and build.

A Tier-1 operator and institutional capital are circling — and a hyperscaler appears to be steering. On April 1, NUAI signed a non-binding LOI to form a development-and-financing joint venture for TCDC with Stream Data Centers, a top-tier U.S. data-center operator, alongside an institutional capital partner. New Era contributes site control and local execution, Stream serves as developer and operator, and the institutional partner provides equity and arranges the bulk of project-level debt. Two details elevate this above a routine LOI. First, Northland's research describes the pairing as effectively brokered by the prospective hyperscaler tenant itself — the customer pointing NUAI toward the partners it wanted building and financing the site, which is a meaningful tell on intent. Second, Stream was acquired by Apollo Global Management in late 2025 at a valuation of roughly $40 billion, and the institutional partner is believed (per Northland) to be Apollo — putting some of the most credible capital in infrastructure behind the structure. It is still an LOI, not a signed definitive, but the roster is what turns a development concept into a financeable platform.

The power story is validated. What differentiates TCDC is not the dirt — it's the power. NUAI's "behind-the-meter" (BTM) thesis received concrete substantiation through a 450 MW behind-the-meter generation plan at TCDC developed with named partners Thunderhead Energy and TURBINE-X Energy. In a market where the binding constraint on AI buildout is increasingly electrons, not acres, a credible path to nearly half a gigawatt of on-site generation is the asset.

The hyperscaler is in advanced negotiations — over secured capacity, not a concept. The event that would re-rate the whole equity is a hyperscale lease. Management has described advanced commercial discussions with a top-tier, credit-worthy hyperscaler — realistically one of the big four cloud builders (Alphabet, Amazon, Meta, Microsoft) — for a campus with roughly 650 MW already secured and a path beyond 1 GW. The acquisition of an additional 54-acre corridor adjacent to Vistra and Calpine power plants was itself a milestone within those lease discussions. Timing is framed conservatively around fall 2026, and conservatism here is a feature given how the market punishes overpromising. The backdrop is favorable: recent hyperscale leases in the sector have printed in roughly the $140–190 per kW per month range (at least one recent deal involving Google reportedly reached ~$188), while the big four are guiding to historic 2026 capex — Alphabet to about $175–185 billion and Amazon to around $200 billion — as demand outruns deliverable power. In that environment, a power-secured, near-shovel-ready site is exactly what is scarce.

The invisible bid: a capital-markets function, finally resourced

Not every driver of a stock is a press release. For most of its life, NUAI was too small and too underfunded to run the kind of investor-relations program that institutional money expects — sustained institutional outreach, non-deal roadshows, analyst targeting, the steady cadence of being in front of the right funds. Those functions weren't broken; they were simply never staffed. That is changing, and the upgrade is visible in the hires themselves.

The company's investor relations now runs through OG Advisory Group, where the engagement is led by Lincoln Tan — who previously ran investor relations and marketing at IREN through precisely the kind of transition NUAI is now attempting (a power-and-mining story re-rating into an AI data-center story), and who came to IR from Macquarie Capital. Pair that with CFO Ted Warner, whose career was built structuring data-center financings on Wall Street, and the company has, arguably for the first time, a team explicitly equipped to court institutional capital rather than simply collect retail attention.

The practical implication is the kind of "invisible" activity that rarely makes headlines but steadily changes a stock's character: institutional meetings, conference presence (B. Riley in May, Datacloud in June), and the normal rhythm of roadshows and analyst engagement that turns a thinly followed micro-cap into a name long-only funds can actually own. As the shareholder base broadens and deepens, two things tend to follow — a higher-quality register and lower volatility — as price discovery shifts away from fast retail money toward investors underwriting a multi-year build.

This compounds with the de-risking. Every overhang removed — the lawsuit, the dilutive structures — is one less reason for a fundamental investor to pass and one less piece of "hair" on the story. The explicit catalysts get the headlines; this quieter professionalization of the capital-markets function is part of what lets them stick.

What the Street is starting to see

Sell-side coverage is one of the clearest signs the professionalization is working. In April, Northland Capital Markets initiated coverage with an Outperform rating and an $11 price target — against a share price barely above $5 at the time, implying roughly 2x upside. The logic is a staged, project-finance valuation: Northland credits only ~283 MW of TCDC capacity (Phase 1 plus half of Phase 2), assumes NUAI retains ~45% of the JV, applies a ~19x EV/EBITDA multiple in line with listed data-center peers, and discounts back on a ~125 million fully-diluted share count. Notably, that target deliberately excludes the back half of secured capacity, all of Phase 3, and NUAI's entire ~7 GW wholly-owned New Mexico pipeline (a ~3,500-acre Lea County site with a small-modular-reactor angle via a Last Energy partnership) — meaning the bull case carries option value the published target doesn't pay for.

NUAI now has its first real institutional research footprint, and a company running a proper IR program with a clean-up story to tell typically attracts more coverage over time. Additional analysts picking up the name through year-end — plausibly several — would broaden the buy-side audience and is exactly the kind of slow, compounding tailwind the "invisible bid" is built on.

The catalysts ahead

The next few weeks and months offer a dense sequence of potential catalysts:

Datacloud Global Congress, June 2–4, Cannes. President & COO Charlie Nelson is scheduled to speak at the industry's marquee gathering — the kind of room where hyperscalers, Tier-1 operators, and institutional capital allocators are all present (in fact, the hyperscalers, Stream, and Apollo are all present). For a company in active lease and JV negotiations, the value of being on that stage, at that moment, is hard to overstate.

A Stream JV definitive agreement converting the LOI into something binding.

A hyperscaler lease, the single highest-impact event in the story.

Expanding analyst coverage. With one Outperform initiation on the board, additional firms picking up the name — potentially several by year-end — would deepen the institutional audience.

A still-growing team. The June 1 additions of a chief development officer and general counsel are likely an opening move, not the finish; further senior hires would keep signaling that management is staffing for execution and often front-run bigger announcements.

The picture

Step back and the pattern is consistent: every quarter, if not every month, a structural negative has come off the board and a structural positive has gone on. Sharon AI — cleared. The toxic-preferred path — scrapped. The state lawsuit — settling. In their place: a Macquarie facility, a Tier-1 operating partner, a validated power plan, a CFO and now a development chief and general counsel drawn straight from the hyperscaler and data-center world, and an $80 million-plus cash cushion. The market tends to discount a stock for its overhangs right up until the moment they're gone — and then re-rate it for the platform underneath. With the first sell-side target sitting at roughly double the recent price and explicitly excluding most of the pipeline, the gap between where NUAI trades and what a leased, financed platform could be worth is the heart of the opportunity. NUAI is converting overhangs into catalysts on a remarkably steady cadence.

15

41

213

27,330

Block retweeted

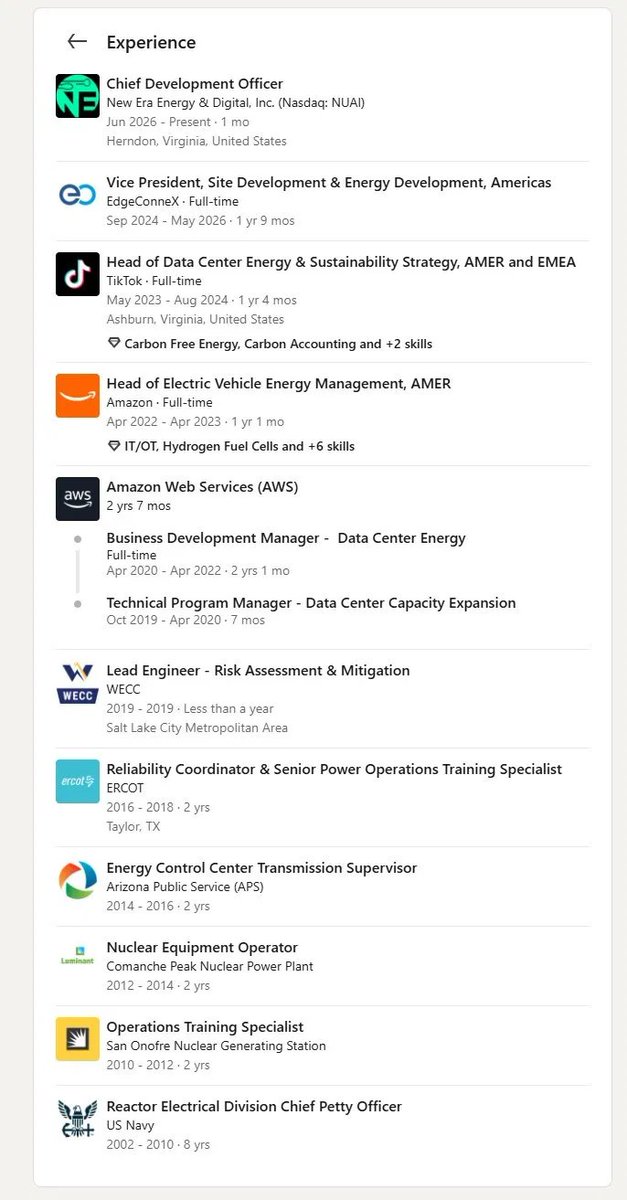

$NUAI just brought on Evan Pierce as Chief Development Officer.

Below is a brief summary of his experience:

Nuclear operator (Comanche Peak, San Onofre)

ERCOT reliability coordinator

AWS - data center capacity expansion and business development

TikTok - Head of Data Center Energy & Sustainability, AMER and EMEA

EdgeConneX - VP of Site Development & Energy Development, Americas

People with this resume don't join micro cap companies for a salary. They join because they see something others don't. I would not be surprised if he brings in a wealth of new connections and opportunities for $NUAI much like Ted Warner did on his arrival.

Maybe what he is seeing at $NUAI is hard to ignore?

The company has a New Mexico site with up to 5GW of nuclear capacity and 2GW of natural gas on deck.

You don't recruit a CDO who spent his career scaling hyperscale energy at AWS, TikTok, and EdgeConneX unless you're planning to actually build something.

I found this particularly interesting. He began his nuclear career as an Equipment Operator at Comanche Peak Nuclear Power Plant operated by Luminant, a Vistra company. Vistra sits right across the road from TCDC. I would not take this as a signal but would in some fashion highlight he has intimate knowledge of the industry and knows what needs to be done at the $NUAI level to get this deal across the finish line and expand the $NUAI footprint to future sites.

The talent being attracted doesn't lie. I saw this post via LinkedIn this morning. Looks like the thesis continues to play out for $NUAI.

8

10

90

12,005

Block retweeted

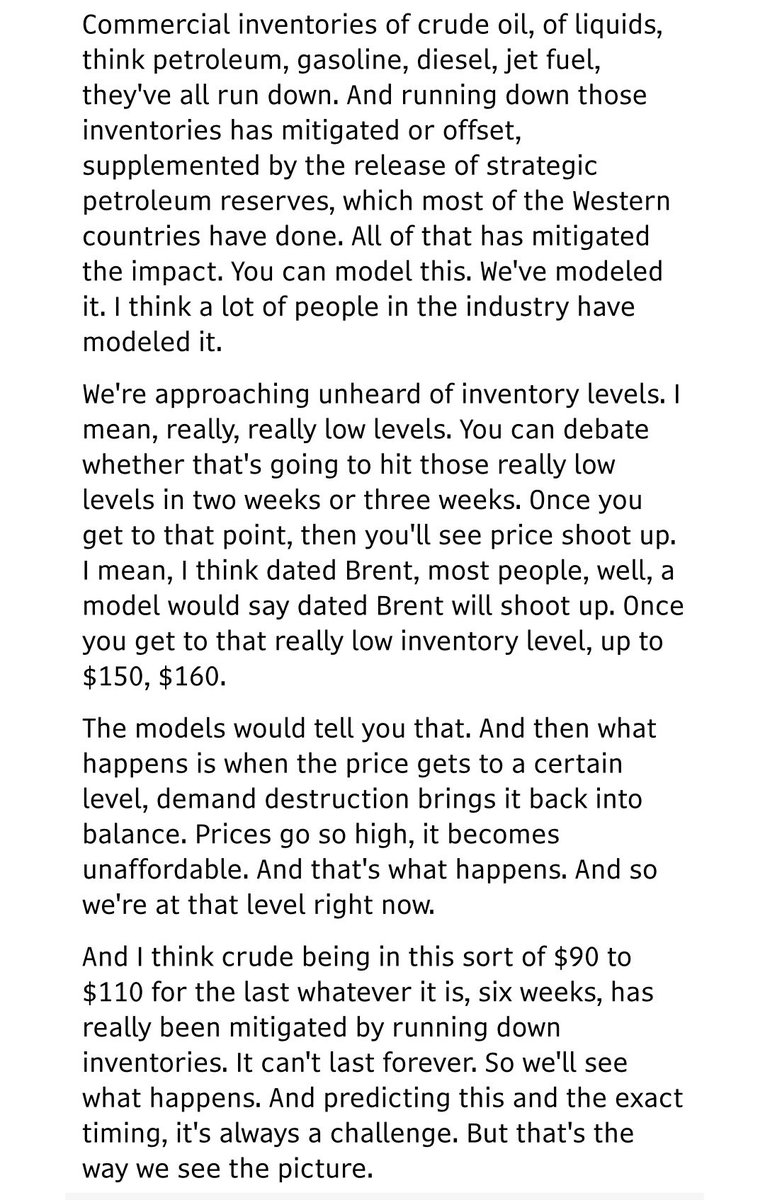

🚨The global oil market is racing toward a major shock. Inventories are collapsing while the Strait of Hormuz remains closed. Supermajor executives are issuing blunt warnings that prices could surge dramatically in the coming weeks.

•@exxonmobil SVP Neil Chapman: “We’re approaching unheard of inventory levels... really, really low levels... Once you get to that point, then you’ll see price shoot up.” He sees Brent potentially hitting $150–$160 per barrel.

•@Chevron CEO Mike Wirth: “The buffers and the shock absorbers are being steadily drawn down... the ability for the market to absorb this imbalance is drastically diminished.” He expects more upward pressure into July.

•Global inventories have plunged by a record 8.7 million barrels per day in May alone.

•The largest supply disruption in history - 12-13 million bpd offline - has exhausted strategic reserves and commercial stocks. We’re rapidly approaching the operational floor where physical shortages become unavoidable.

•This isn’t speculation. It’s the cold reality of the physical market overriding hopeful paper trading and diplomatic optimism. A spike to $150 oil would hammer consumers, spike inflation, disrupt supply chains, and risk pushing vulnerable economies into recession.

•The crisis exposes years of fragile “just-in-time” inventory practices and over-reliance on chokepoints. Energy security demands better: diversified supplies, adequate reserves, and responsible domestic production.

•Markets will eventually balance through painful demand destruction, but the transition will be costly. Policymakers and leaders ignore these warnings at their peril.

•The bill for neglecting energy reality is about to arrive, and it will be measured in triple-digit prices and widespread economic pain.

Bottom line: If there really is a deal to be made to end this lingering war, President Trump would be well advised to make it ASAP. This isn’t a game – global markets do not care about your diplomatic protocols.

12

35

152

54,377

Block retweeted

May 28

Neil Chapman, SVP of Exxon this morning at the Sanford Bernstein Strategic Decisions Conference perhaps going a little off corporate script:

123

754

3,512

583,222

Block retweeted

In the big short:

Before the market finally crashed, there is a tense sequence where the characters realize the underlying mortgage bonds are failing and defaults are rising, but official bond prices on their terminal screens are still going up. This happened bc big banks credit rating agencies manipulated the prices and refused to downgrade the bonds.

Sounds like todays oil market.

May 28

I dont get it, it cant be the market is this stupid..?

It feels like its unreal...

63

126

1,470

144,854

Block retweeted

May 27

Why Hasn't Oil Hit $150 (Yet)? zerohedge.com/commodities/wh…

69

56

378

78,346

Block retweeted

People are asking me why I'm chilling & so relaxed about the oil prices not matching reality. Here's some brief thoughts.

The simple answer is I'm confident in my personal ability to predict long term macro trends in commodities. I've been doing this for years, and every time I hit a huge return it started just as frustrating as this one.

This is also why I'm trying to shitpost quality for you guys. It's to show you that at the end of the day, the fundamentals pull the future return higher.

Even if there is a deal tomorrow, the long term outlook for any undervalued oil producer is higher than their current price, assuming management don't fuck up.

Honestly, I haven't even been checking the charts much, other than buying a ton of Journey energy today because it pulled back such an unreasonable amount and I happened to be sent a screenshot of it down over 30% from recent peaks.

The last thing I'll say is this is basically (in my opinion) an investor's dream set up. We're making an asymmetric bet, in the worst case we lose maybe 20%. But in the expected case, where Iran refuse to surrender their uranium and the USA blockade continues, these undervalued oil companies with tax pools larger than their market caps (ensuring tax free sales) will give hilarious outsized returns.

Major facts:

1. Iran mined the strait and is still adding more mines since the USA attacked them while they did so within the last 72 hours.

2. The USA is still "defensively" (what a PR word!) bombing Iran.

3. The Iranians won't surrender their uranium. If they would, they wouldn't have been recently assassinated by the zionist empire. The remaining Iranians hold even stronger beliefs about the importance of uranium to a sovereign nations security.

Weak facts:

1. Iran wants a Lebanese ceasefire, this probably won't happen cuz Israel is, well, Israel. You know, the country that redefines the term "defends themself", to include "preemptively bombing anyone they feel like" and arbitrarily committing war crimes whenever they feel like it (examples include but are not limited to poisoning a supply chain so pagers blow up and maim whoever happens to be near them, including children, and outright sniping children in the head because why not, they're prehistoric animals anyway, right).

2. Trump can't pay Iran more than Obama paid them or he will lose all support from his base. Right now Iran is demanding 25bil. Will trump cave? Who knows, that's why this is a weak fact. He is the king of the TACO.

3. Iran want to remain in control of the strait, but technically, it's not theirs to control under current international law and the current status quo. The thing is, the international community won't care much since there's not much alternative. They necessarily must get on their knees for Iran cuz most of them need a boost to Arabian exports desperately.

All that said, everyone is a f*cking idiot. So don't be surprised if a deal gets made, but do know, that we've (almost surely) passed the point of no return. My opinion is that it's safe to value oil producers with $80 WTI price floor.

Of course, this could be the first time I'm wrong, but this feels like a hard time to end up wrong. I'm simply betting that Iran cares about its sovereignty.

Best,

G

39

34

609

35,691

Block retweeted

May 19

Multiple turns already with the lawyers on hyperscaler lease with $nuai

In investment banking once a definitive agreement is being redlined by both sides it means the two sides have “green lighted” the largest chunk of the legal deal fee.

It is usually the most visible financial signal a deal will be consummated. Also this is where the most action happens in negotiations. Either side can tell their lawyers “pens down” to posture.

Since multiple turns have been made already, I’m assuming they are past the posturing/negotiation stage already.

My guess is we see a closing date in May for lease execution. Even though they have until June/July to sign, the team seems to be way ahead of the deadline. Just look at the Macquarie deal, which was done 2 months ahead of schedule.

May 19

$NUAI: The Last Asymmetric Bet in the Data Center Trade

Look across the small-cap data center cohort right now. NUAI is the only remaining sub-$500M name with a real, exclusive, late-stage hyperscaler negotiation in motion. And after parsing the Q1 2026 call, conviction goes up, not down.

The Lease Math Now Works Backwards From 2027

Charlie Nelson laid out the schedule cleanly:

"Our schedule is largely driven by power availability. The power that we have available in phases 1 and 2 is in second half of 2027. Everything that we're doing is kind of back-solving from those dates... We still feel good about second half of 2027 in-service date for the first phases of this."

Working backwards from ~August 2027 with Stream's compressed 12-14 month build cycle, the lease has to be signed by July or August 2026 to preserve schedule. The construction calendar is a hard forcing function — every party at the table knows it, including the hyperscaler.

The Documents Are Closer Than Anyone Realizes

When asked about sequencing, Charlie was specific:

"The JV docs are well underway, multiple turns already with the lawyers, and the lease as well, as well as the PPA. All of these are progressing concurrently... And this is how it goes with most of these types of industrial developments — concurrent execution, especially when they're all kind of lining up around the same time, just makes sense. And you just kind of have a signing day, if you will. A very fun day, by the way, for any industrial development."

"Multiple turns" means the documents are mature. What's left should be legal documentation — a slower, more deterministic process than commercial negotiation. The phrase "signing day" is not casual. It's deal-maker code for a coordinated execution event where multiple interdependent documents close together.

The Hyperscaler Engineered This Deal

This is the part nobody is talking about enough. The hyperscaler wasn't recruited. They initially came to NUAI wanting to buy the land. Ted Warner walked through the sequence:

"We were also getting offers to buy this from actual hyperscalers... One of those we did, we signed an exclusivity agreement because we kept turning them down on selling, and we wanted to work with them on how can we partner with you to own something here. Essentially, it was, 'You've got to work with a really reputable developer.' We went and tried to find one, that exact same party sort of led us to a different party. Now here we are with that party, Stream."

The hyperscaler directed NUAI to Stream. They didn't just suggest a developer — they pre-approved their own counterparty. Stream walked in with existing commercial agreements and pre-approved designs with this specific hyperscaler. Charlie confirmed it:

"Having pre-approved designs with this particular hyperscaler, which is why we were guided into the relationship with them, frankly — to the fact that they house long lead time equipment that goes towards these projects, and it's a rinse and repeat design."

A hyperscaler that takes the time to direct partner selection, share technical specs, sign exclusivity, and cooperate through a developer restart is not a hyperscaler that walks away at the finish line. That's a counterparty that has been quietly engineering the conditions for this deal to close on terms they already endorsed.

And It's the Same Hyperscaler

Ted's clarification on the Sharon AI confusion was the most underrated moment of the call:

"The same party, that hyperscaler is still the person that we hope will be our tenant, that our designs are specifically for... [Stream has] been incredible to work with, just every day checking boxes. It's been awesome to watch them work."

No one walked. The hyperscaler that wanted this site in 2025 still wants the site in 2026. The designs are still tailored to their specs. The exclusivity is still in place.

The Balance Sheet Is Built For This

Ted's segment removed the financing overhang that haunted this name for months. $80M cash on hand. $290M Macquarie credit facility. The Sharon AI note is gone. Liens lifted. They illustrated the math:

"Our cash needs for phase one would be roughly $180 million before the credit that we'd get for the land contribution... That theoretical $180 million investment is more than covered for phase 1."

NUAI's expected equity check for Phase 1 is fully funded. No more "how do they pay for this" question hanging over the stock.

The Setup

The market just sold the stock 11% on a quarter that confirmed every workstream is on track

The lawsuit resolution should come soon

PPA likely ready first

JV DA close behind — Stream is the most motivated party in the deal

Hyperscaler lease execution window: late June through Early August 2026

One signing day, three documents, complete rerate

This is the playbook setup for an asymmetric trade. The downside is bounded by the cleaner balance sheet, the Stream-driven execution model, and the standing hyperscaler engagement. The upside is a name with a sub-$500M market cap signing a lease comparable to deals that already moved peers multiples higher.

"As a shareholder, I sit here with you, and I wish I could announce who the prospective tenant is, and I can't wait to announce it one day. We've been working very, very hard to get there." — Will Gray, closing remarks

NUAI is the last shoe left to drop.

investing.com/news/transcrip…

1

1

15

3,373

Block retweeted

May 21

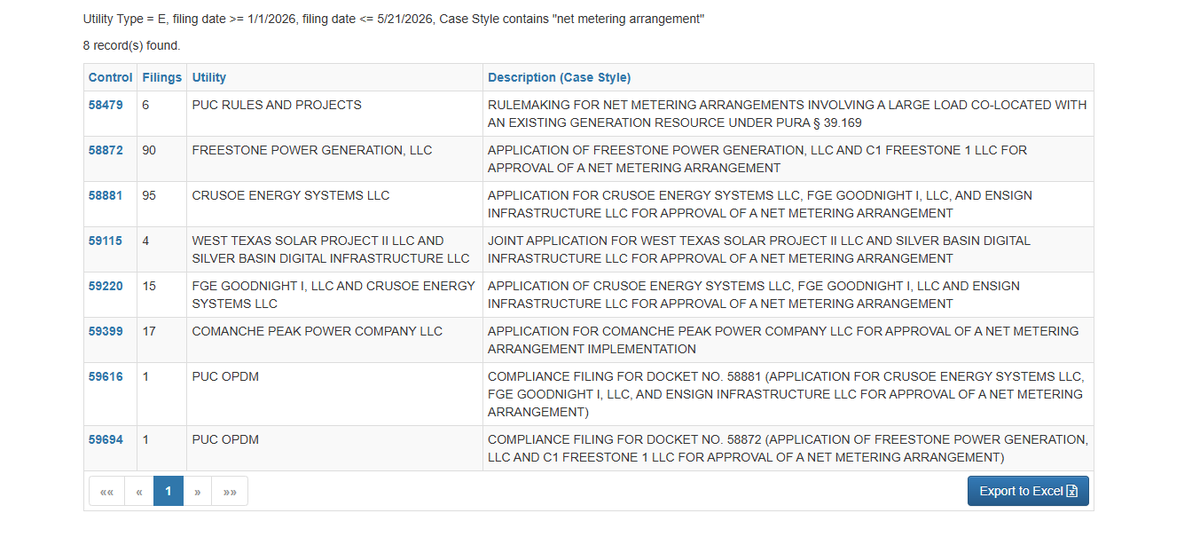

Following up on my $NUAI BTM colocation post. Did some digging into the PUCT docket and the regulatory picture just got significantly clearer.

The final rules for net metering arrangements under PURA § 39.169 were adopted last month. The framework $NUAI would use is now fully in place. Turns out my post was not speculation but is concrete which is good news for all of us.

Vistra filed comments in PUCT docket 58479, the exact rulemaking governing BTM colocation between existing generators and new large loads arguing specifically for a faster legacy track with a strict 180 day approval timeline. Companies don't spend legal resources on proceedings that don't affect their active business plans.

There's already a live Texas precedent. CyrusOne filed a BTM colocation application with Calpine for a 760 MW data center in Freestone County under the exact same framework. Fossil gas generator plus large data center load. Same structure $NUAI would use.

This is directly relevant to $NUAI's TCDC project. Calpine operates Quail Run directly adjacent to TCDC on the investor map. Vistra operates Odessa Ector Power Partners also directly adjacent. $NUAI has two active BTM colocation counterparties sitting on their fence line and at least one of them just proved the model works in Texas.

The 54 acre corridor connects TCDC directly to them. Yes, $NUAI would need a tie-in-station on their 54 acres of land. I do not want to oversimplify these engineering milestones but between Charlie, Will, HS selected engineering partner - Ramboll, and Stream I would suspect they are ahead of the curve on this.

One more thing worth addressing directly since I know someone will bring it up. No, Vistra/TCDC net metering application has been filed at PUCT yet. Just because there is not a public filing does not mean it is not in the works. Again, reminding us Charlie hinted at "one big signing day".

Here's why I am not currently concerned:

I pulled every active § 39.169 net metering application currently on file in Texas. There are five of them, see attached photo which highlights these documents. Every single one lists both the generator AND the large load customer as joint applicants. Freestone Power Generation filed with C1 Freestone 1 LLC. Crusoe filed with Ensign Infrastructure. The generator and the confirmed load file together. The Vistra Comanche Peak docket 59399 detail proves Vistra specifically knows how to file these applications and has done it already.

$NUAI hasn't announced a hyperscaler lease yet. That's the known missing piece, not the power solution. You don't file a net metering application without a confirmed load customer because ERCOT studies the specific load characteristics of the facility being co-located. Filing before the lease would be premature and put the cart before the horse.

If you would like to search around the PUCT site. See the link below. Maybe you will find something I did not! I found this to be directly relevant for all invested or looking to invest in $NUAI and figured a post here would be appropriate.

interchange.puc.texas.gov/

10

4

65

6,808

Block retweeted

$ASPI I've been in and out since early 2024, always been following their progress. I wanna highlight a couple of X accounts to follow. Search $ASPI on their profiles for a deeper dive.

🔎 @AcctNo994 - Know what you hold.

Blunt conservative investor, very bullish on $ASPI since ~2022. Deep due dilligence on tech, history, science and people. Sees massive undervaluation with strong upside. South African nuclear talent moat (post-sanctions aerodynamic laser enrichment expertise from Klydon team).

Frontrunner for commercial HALEU (2027 target) thanks to existing facilities and Pelindaba advantages.

Renergen helium/LNG acquisition as major catalyst: Phase 1 cash flow Phase 2 helium potentially $200M . Bullish 2026 EBITDA.

Diversified high-margin portfolio: medical isotopes (Yb-176), Si-28, C-14, tungsten, REE recycling.

Superior tech vs. centrifuge peers like $LEU. Praises CEO Paul Mann’s foresight (early TerraPower bet).

Tactical critiques on presentation, but core thesis remains strongly positive.

🔎 @piterloskot82 - Stay up to date!

Highly active advocate, $ASPI is his largest position. Deep dives in to everything ASPI, strong coverage and connecting the dots on what might be going on behind the curtain.

Sees an emerging leader in stable isotope enrichment (medical, quantum, semiconductors, HALEU/LEU , Li-6/7, Ni-64, Si-28, Yb-176).

Quantum Enrichment tech offers strong scalability. $QLE spin-out will unlock value.

Current EV justified by existing plants alone; rest of portfolio at near-zero.

Rapid scaling (employees ~271), 2026 deliveries (Si-28 in Q2), TerraPower invoicing, strong partnerships.

$300M potential annual EBITDA from core ops. High conviction in management.

🔎 @matt_nealy - SEC forensic

Tracks confidential QLE S-1, board/HQ changes, and Pelindaba access rights as de-risking steps for spin-off and US funding.

Views risk disclosures (e.g. TerraPower concentration) as standard SEC transparency.

Monitors institutional accumulation (BlackRock, Vanguard) and filing timing for stronger prospectus.

Emphasizes management is “doing it right” with regulators.

🔎 @FinanceMajor_23 - The value?

Quantitative macro supply-chain analyst. $ASPI/QLE as Western platform reducing isotope supply disruption risk (~26% VaR reduction).

Renergen adds near-term cash flow; strong HALEU contender for SMRs/data centers.

Multiple 2026 catalysts: commercial isotope shipments, helium ramp.

Volatility = buying opportunity in nuclear/AI tailwinds.

Overall Convergence: All highlight South African tech edge, HALEU/isotope leadership, Renergen catalyst, and strategic value in a supply-constrained nuclear boom, while noting execution risks. Conviction, research depth, filings, and modeling.

Thanks grok for summarizing, my man.

2

3

61

10,642

Block retweeted

May 9

NUAI: An Asymmetric Pre-Deal Position in AI Infrastructure

Summary

Investors comfortable holding $IREN, $WULF, $CIFR, or $APLD before they announced their first hyperscaler deals should be comfortable holding $NUAI today. The structural setup is materially identical with less execution risk. NUAI is operating the validated playbook those names established in 2025, with Stream Data Centers (Apollo-backed at $40B) and Macquarie already on the cap table, four hyperscalers as the only credible counterparties, and a six-month Macquarie clock functioning as a forcing function for lease execution.

Position Overview

Eighteen months ago, AI infrastructure names like IREN, WULF, APLD, and CIFR traded as speculative microcaps. Each re-rated sharply once a hyperscaler signed. Multiples expanded, floats compressed relative to opportunity, and the market repriced the companies from "miner" to "AI infrastructure platform."

NUAI follows the same template. New Era Energy & Digital has 650 MW secured in Ector County, Texas — the flagship "TCDC" campus — and management has confirmed advanced commercial discussions with one of four hyperscalers: Alphabet, Amazon, Meta, or Microsoft. The joint venture was organized by the hyperscaler, who selected Stream Data Centers as development manager and an institutional capital partner (Northland believes Apollo) to provide equity and arrange approximately 80% project-level debt. Stream contributes hyperscaler relationships and operational execution. NUAI contributes site control. The structure was effectively delivered to the company.

Why the IREN/WULF/APLD Comparison Holds

The standard objection to any "early-stage X" pitch is that every microcap claims to be the next something. Four points distinguish NUAI from generic versions of that pitch:

1. Secured land. 650 MW in Ector County is owned outright, not optioned or under LOI. The recent equity raise eliminated the SharonAI overhang and consolidated full ownership of the TCDC site. Power-ready acreage is the binding constraint of the entire AI buildout and the single hardest piece to fabricate.

2. Institutional capital. Macquarie wrote a $290M project-level facility. Apollo acquired Stream Data Centers for $40B in November 2025 and is the implicit equity partner on TCDC. Both are among the most rigorous diligence shops in private capital, and both are staked.

3. Professional execution stack. Stream as developer/operator; RK Mission Critical for modular fabrication and supply chain; Thunderhead Energy for behind-the-meter power; Ramboll / EYP Mission Critical Facilities for engineering. Charles Nelson joined as President/COO in February 2026. Ted Warner — with nearly two decades of capital markets experience and over $7B in HPC-related financing — joined as CFO in March 2026.

4. Binary counterparty universe. Four hyperscalers, all investment grade, all capex-constrained on power, all publicly committed to multi-year buildouts. Whichever one signs represents top-tier credit on a 15-20 year colocation lease.

Behind-the-Meter Has Become the Industry Default

A year ago, the consensus view across the data center industry held that behind-the-meter (BTM) power solutions were unworkable at hyperscaler scale. Critics argued that hyperscalers required utility-grade reliability, regulatory complexity would prove insurmountable, and BTM would remain a niche workaround rather than a primary power strategy. That view was a real overhang on every developer pursuing BTM as a path to capacity.

The consensus has reversed in twelve months. CIFR, APLD, WULF, and CORZ are all now executing BTM-led power strategies, and hyperscalers — facing multi-year interconnection queues and structural grid constraints — have endorsed BTM as a viable route to GW-scale capacity. Thunderhead Energy's role on the NUAI execution stack should be read in this context. NUAI is executing a strategy the industry has at this point publicly validated, with a power partner whose model is de-risked by parallel deployments at peer companies.

This is a meaningful update to the underwriting. The power-delivery question that was an open risk on every pre-deal AI infrastructure name twelve months ago is now the operating assumption across the cohort.

Stream Data Centers as the Execution Catalyst

In November 2025, Apollo paid $40B for Stream — for a particular set of capabilities that map directly onto why a hyperscaler would select TCDC.

Build-to-performance spec, not build-to-suit. Stream pre-aggregates standardized MEP equipment and configures it on the fly to customer specifications. The company quadrupled its development team during COVID and has been procuring long-lead equipment up to a year ahead of demand. Standardization speeds development time materially in a market characterized by acute power constraints and capacity scarcity.

Configurable cooling that future-proofs the asset. Stream's proprietary cooling design supports air cooling and direct-liquid-cooling on the same footprint, scaling from 10-12 kW per rack to 400 kW per rack. Customers can defer the air-vs-DLC decision until late in the build without extending the timeline, providing meaningful optionality across NVIDIA's roadmap from Blackwell to Rubin and beyond.

Pre-existing hyperscaler relationship. This element has been broadly overlooked. Because Stream has worked with this hyperscaler before, we can safely assume that a significant amount of work product can be leveraged for TCDC. Management's fall 2026 lease execution target is credible because contracts are likely being adapted, not drafted from scratch.

The distinction is between a startup negotiating with a hyperscaler from a blank page and the hyperscaler's preferred developer adapting an existing form to a new site. Execution risk lives in a different category.

Expected Value Framework

In my opinion, the probability of a deal with the current hyperscaler by August 2026 is 90% . The hyperscaler organized the JV. They selected Stream. They directed the structuring. Engineering and permitting are progressing without observable friction. Negotiations leverage Stream's existing templates and shared counsel. The Macquarie facility requires lease execution within six months, aligning every party's incentives toward closing.

As for the probability of any deal eventually, I would say 99% . If the current hyperscaler exits — for which there is no observable reason in a market structurally short on power-ready supply — the structural work is already complete. Site control, partner ecosystem, financing template, and engineering package are not counterparty-specific. Another publicly traded data center company recently demonstrated this dynamic: a hyperscaler counterparty exited, a replacement was secured, and the timeline extended by approximately one month.

Stress-tested at a deeply conservative 50% probability of a deal — well below what the structural setup supports:

50% × 4-5x upside ≈ 2.0-2.5x expected return

50% × 50% drawdown ≈ 0.25x expected loss

Net expected value: approximately 1.75-2.25x

At 90% probability, expected value approaches 3.5-4x. The asymmetry is wide enough that halving the upside and doubling the downside still produces a positive expected value.

Re-Rating Mechanics: Why a Deal Drives 200% From Here, Not 10%

A market-microstructure point underlies the upside case.

When mature AI infrastructure names — IREN, WULF, CIFR, APLD at current scale — announce hyperscaler deals, the stock typically moves around 10%. Optionality is already embedded, and announcements function as confirmation rather than revelation.

Smaller, less-followed names behave differently. DGXX has announced materially smaller deals than what NUAI is contemplating and moved 50% . Expectations are not embedded, the float is small, and the announcement forces a re-rating from speculative microcap to credible AI infrastructure platform (Note that a deal cannot be priced in because many institutions are waiting to buy until after a deal is announced).

NUAI sits closer to the $DGXX end on market cap and visibility but closer to the IREN/WULF/APLD end on asset quality and counterparty caliber. That mismatch is the opportunity. A first hyperscaler deal at TCDC could plausibly drive an immediate 200% re-rating — not because steady-state fundamentals support that exact multiple, but because microcaps gap rather than incrementally re-price. Investors do not get to scale into the new range.

Downside is bounded by the existing balance sheet, which is clean post-Macquarie and post-equity raise with no SharonAI overhang. Upside is a non-linear re-rating event.

The Case for Data Center Exposure

A reasonable question, given the breadth of the AI investable universe — semis, photonics, custom silicon, robotics, model labs — is why allocate to data center developers at all.

Data center economics are durable in a way most AI-adjacent verticals are not. Hyperscaler colocation leases run 15-20 years. Counterparties are investment grade. Cash flows are recurring. Once a campus is leased, it produces something close to a bond. EQIX has compounded through every macro cycle of the past fifteen years on this dynamic, and the structural reason is simple: an AWS region does not get turned off because the economy slows. Compute demand is structurally inelastic at the margin, and existing infrastructure is locked into multi-decade obligations.

The asset class is also tractable for non-specialists. Underwriting reduces to power, land, customers, and contract terms. Many other AI-adjacent verticals — photonics, custom silicon, neuromorphic, edge inference — are genuinely interesting and likely lucrative, but the underlying technology evolves quickly enough that most investors cannot reliably assess winners. Data centers fit Buffett's "in pile" — comprehensible, durable, and underwritable on standard metrics.

The constraint is that asymmetric opportunities within the data center space are increasingly scarce. For WULF to 5x from current levels would require multiple gigawatts of new capacity, additional contracts, and substantial revenue growth — achievable but grinding. NUAI requires one announcement with one of four hyperscalers for Phase 1 of TCDC. The bull case condenses to a single press release.

For investors who participated in the 2025 IREN/WULF/HUT/APLD/CIFR cycle, NUAI offers the same trade structure with two improvements: the underlying thesis has been validated by the prior cohort's outcomes, and the macro evidence — exponential capex guides, tightening power constraints, structural undersupply — is materially stronger today than it was eighteen months ago.

Conclusion

NUAI is structurally identical to the IREN, WULF, and APLD trades in early-to-mid 2025, with three improvements. The thesis has been validated by the 2025 cohort's outcomes. The execution stack — Stream / Apollo / Macquarie / Ramboll on day one — is more institutional than what several of those names had at first announcement. And the forcing functions are tighter, with a six-month Macquarie clock combined with a hyperscaler-organized JV on 650 MW of secured Texas power.

The position reduces to a single proposition: one press release reprices the equity by triple digits. Downside is bounded by an institutional cap table and a clean post-raise balance sheet. The expected value math holds at 50% probability and compounds at the 90% probability the structural setup supports.

Simply put, this is a remix of the IREN/WULF/APLD trade.

28

35

284

42,831

Block retweeted

May 6

I learned a lot the past 6 months. Despite an objectively successful "career" investing, the market humbled me in a thousand ways. It is no secret that I have a large position in $NUAI, and my thesis for buying it was actually very accurate, notwithstanding the timeline (I was too optimistic in that respect). See substack.com/home/post/p-193… for a good overview by @ThePrudentWhale.

Per Tyler Page, the CEO of $CIFR, “behind the meter gas powered sites may be the highest upside convexity in our portfolio," and NUAI specializes in behind the meter gas. Interestingly, CIFR's Odessa site is approximately 30 miles from TCDC, and CIFR confirms that “We do have a lot of interest in Odessa. We have a hyperscaler interest in that site. I think I’ve mentioned before, we would be interested in potentially evolving that site much like we did Black Pearl from a Bitcoin mining site to an HPC campus.”

NUAI's Macquarie credit facility (which can be used at least in part to finance TCDC buildout, thereby reducing dilution) validates the legitimacy of the hyperscaler interested in TCDC, and Stream as execution partner significantly derisks construction. Further, the preexisting relationship between the hyperscaler and Stream truncates the normal leasing timeline, e.g., by 50% or more. Now, obviously nothing is definitive yet, but the upside is clearly there: from every angle, the NUAI thesis checks out.

However, despite being right about so much, I was also wrong about so much--not NUAI specifically, but the market generally. I obviously had not anticipated Trump causing just a global shitstorm, even if such shitstorm was necessary (likely debatable). I further failed to recognize how risk-averse institutions have become regarding AI plays, strongly preferring companies that have deals in hand to the point of neglecting companies with deals in the making, no matter how good these potential deals are. At the end of the day, institutional investors just place mature business and pre-revenue startups in different categories, regardless of how promising the latter might be.

My delayed recognition of the above resulted in me missing many things. For the longest time, I did not appreciate CIFR, $WULF, $HUT, and $APLD, instead only really praising and investing in $IREN for its more ambitious (and risky) strategic vision. Now, in hindsight, it's clear that a diversified bet on the entire data center sector (only including the serious contenders) would have done exceptionally well. This is a lesson I will remember going forward.

I know NUAI's time will come. It may not be obvious on the surface, but behind the scenes every tailwind is converging to support NUAI's approach. Besides the growing popularity of behind-the-meter power, NUAI's partnership model is extremely powerful. See the following white paper and article by Stream's CEO are quite informative on this topic: streamdatacenters.com/wp-con… and streamdatacenters.com/articl…. A careful reading will reveal that NUAI's perspective is significantly aligned with Stream's, although I don't know if that's coincidence or design.

That said, I know my timing for NUAI was too early, something I could have hedged by diversifying more meaningfully in the data center sector. Many peers are announcing deals literally this week, whereas NUAI's timeline is more like 1-3 months (of course, no one knows for certain). Given that I already made my bed and have no desire to chase, there's not much I can do except wait for capital to rotate from the higher valuation players to NUAI.

At the end of the day, maxims like "don't put all your eggs in one basket" and "patience is a virtue" are maxims for a reason. They stand the test of time, particularly in volatile times like today. But, when NUAI signs a deal for TCDC with a hyperscaler and it rerates accordingly (fair value of about $11 based on phase 1 alone), I don't think I will regret my decisions very much. I'm still young, and it's good to learn lessons sooner rather than later. The tuition I paid in opportunity cost was required for me to grow.

54

21

392

44,638

Block retweeted

Apr 19

$NUAI Thesis

I know you’ve probably been seeing $NUAI across your timeline recently, and was wondering what the deal with the company is. When I first saw this micro-cap stock on my timeline, I was extremely hesitant. But, after looking deeper I started to draw parallels to companies like $IREN and $APLD before the markets inevitably priced in what they could be worth. For those of you who have been in $IREN you understand that a 10x means speculating on an asset before its true value becomes obvious to the market, and seeing a vision for a company that plans to transition to something different. I believe $NUAI is the next 10x opportunity at $4.60, and here’s why.

Introduction

$NUAI’s flagship site is called TCDC, or Texas Critical Data Centers, that is 1.4GW Gross or ~1GW Critical IT load, in Ector County near Odessa, TX. I believe the market is completely missing the scale of what is happening at the TCDC site. If you haven’t been paying attention closely it’s easy for the recent announcements to fly under the radar. Since the beginning of this year $NUAI has put out announcements every couple weeks forging partnerships with energy generation partners, hiring significant industry leaders, and working meaningfully to prep their site for their hyperscaler client.

Following the Breadcrumbs

At the beginning of the year $NUAI closed the acquisition of the remaining 50% stake of TCDC from SharonAI, their original JV partner on the project. This was to have total control over the land to build new partnerships, and likely at the hyperscaler clients request to bring a new JV partner to the table.

In late February $NUAI announced a 450 MW Behind-the-Meter Generation Plan at TCDC with Thunderhead Energy and TURBINE-X Energy to generate power for the project. They have a SPV/venture where they have partnered with a private equity firm to fund the capital required to source, install, and run 450MW of gas turbines. They will generate an ROI as they sell power to NUAIs TCDC tenant. This equipment is normally extremely difficult to source, and $NUAI was able to grab these 2-3yr long lead time items in an extremely supply constrained environment, showing the connections of the upper management. The notable thing about this partnership is that they don’t have to put any capital upfront for this equipment, allowing them to start generating revenues while loaning the equipment without huge dilution (~70m).

Then, in mid-March $NUAI hired Ted Warner, ex head of the Energy, Power, and Digital Infrastructure at Northland Capital Markers, where he successfully structured and managed more than $7 billion in financing solutions specifically for large-scale data center developments. This was the signal that caught my eye and made me significantly up my position in the company. Something notable is his PSU’s, or Performance Stock Units, which reward him significantly for “Entering into a binding commercial agreement with a hyperscaler for a minimum of 200 megawatts”. Judging by his history I put him as an A hire, and you can see more about his notable achievements here.

x.com/litigious_dulce/status…

Now, to get into the most recent developments that completely change this company from just a speculative random micro-cap to a more credible multibagger infrastructure play. On April 1st, $NUAI secured an LOI with Stream Data Centers. Originally, $NUAI was slated to co-develop the TCDC site with other partners (first Sharon AI, then Primary Digital Infrastructure). However after back and forth for months the unnamed hyperscaler tenant likely mandated that their own preferred execution partner handle the physical construction and operation. Stream is one of the top data center

This project with Stream will be done in a GP/LP fashion, where instead of issuing billions in new stock to pay for construction, the deal utilizes a heavily levered GP/LP (General Partner / Limited Partner) joint venture structure, operating at roughly 80% Loan-to-Cost (LTC). The roles exist as such:

The Originator ($NUAI): $NUAI acts as the local sponsor. They bought the TCDC 438-acre site, secured the initial power footprint, navigated local Texas politics, and laid the development groundwork. Originally I had thought that this agreement would mean passing up the GP role fully to steam and forfeiting their GP revenue streams as the originator. After contacting IR they said “we expect the final structure to reflect the contributions from each (NUAI as a project originator local relationships, Stream as the developer)”

The Operator (Stream): Stream Data Centers steps in as the development manager and operator. They bring the engineering blueprints, the construction expertise, and the direct, trusted relationships with the hyperscaler. The hyperscaler obviously has a preference for this developer and has likely worked with them before.

The Institutional Capital (The LP): An unnamed institutional investor (99% confidence being Apollo, given their majority ownership of Stream) acts as the Limited Partner, writing the massive equity checks and leading the project financing. Apollo Global Management is consistently ranked among the top, most influential, and pre-eminent firms in private equity globally. It is commonly considered part of the "Big 4" of the PE industry and a mark of validation for this project that shouldn’t be looked past.

What this structure does is it protects $NUAI shareholders from the dilution that is so costly to shareholders in a company like $IREN, which long term (2-3 years) has potential to grow into a 100B market cap giant, but will need to dilute massive equity to get the cashflow flywheel going (as shown by 6B ATM). A 1.4 GW campus costs upwards of $12 Billion to build, and $NUAI cannot fund that on its own balance sheet. I expect this LOI to be facilitated into a binding agreement in the next 2-6 weeks.

The second piece of news that is the most convincing is the $290M credit facility from Macquarie. Just to put it out, in case it isn’t obvious already, Apollo and Macquarie don’t blindly gamble on some random micro-cap without doing extensive underwriting and due diligence on the parties involved. They deemed $NUAI worthy enough at a $250 million market cap to receive a $290 million multi-tranche facility that shifts the risk profile of the entire TCDC project.

The structure goes as follows: a $20M committed Term Loan A-1 to kick off development, followed by $30M and $40M tranches, with a massive $200M Delayed Draw Term Loan waiting for execution milestones. That’s already impressive in itself, and likely came from Ted Warner’s existing relationship with Macquarie, but an even stronger validation is the equity kicker. Macquarie took a direct $5 million equity stake at a 20% premium to market share price, taking their entry at exactly $5.00 per share. They also have a tranche of warrants that will have an exercise price of $5.00. The warrants will be issued across the first $50 million drawn on the Facility.

When one of the largest infrastructure lenders in the world is taking an equity stake at a 20% premium to the market’s price, it should tell you everything you need to know about the asymmetry of this setup. You have to ask yourself, would Macquarie offer a loan of this size to a random microcap without doing extensive due diligence and underwriting of an advanced hyperscaler LOI or term sheet?

Luckily, we got the answer to that hidden in the SEC filing of the Macquarie term loan agreement without a formal press release from $NUAI. $NUAI currently has an LOI in place with a hyperscaler tenant as of March 24th, 2026. I believe the reason it was not put in the form of a press release was at the hyperscalers request, and you can read more about it below from @kamikazzzi1981

x.com/kamikazzzi1981/status/…

Now that all of the pieces of the puzzle are starting to come together that a hyperscaler deal is imminent, what should the company actually be worth?

Stock Price Projections

Firstly, I'd like to get out of the way that if you believe that $NUAI will secure a hyperscaler deal in the first place the announcement alone will probably put the stock around 2x higher than the current prices, or around $9-$10/share. This is by giving Stream, one of the most reputable data center builders hand selected by a hyperscaler, around a 60% chance of execution from the math below. If you want to, from that point, you can decide whether you want to sell, or if you believe they can execute the numbers start to get pretty wild.

From Phase 1 alone, with super conservative assumptions (more likely to be ~$1.50M EBITDA/MW)

Phase 1: 200 MW x $1.35M EBITDA/MW = $270M project EBITDA.

At 50% ownership, that is $135M to NUAI.

At a 14x-16x EBITDA multiple, that suggests $1.9B-$2.2B of value, or $14-$16/share on 135.5M fully diluted shares.

Northland’s analysis used a 19x EBITDA multiple in their analysis, 14x-16x is extremely conservative. At a 19x multiple you get a share price ~19$/share

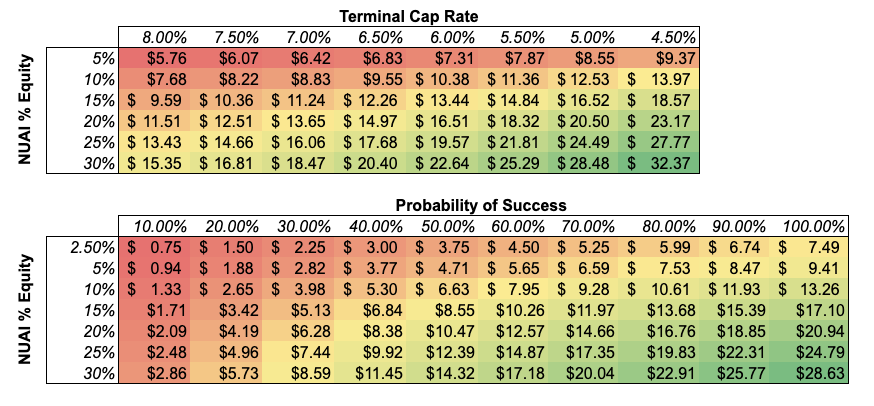

If they can fully execute on Phase 1, the full TCDC 1.4GW campus can be modeled out as done by @ThePrudentWhale

x.com/ThePrudentWhale/status…

• $34.51 Price Target in a 100% success case.

• $25.91 Probability-Weighted PT (applying a 25% execution risk haircut).

And here is super conservative bit of the model: this entirely excludes Behind-The-Meter power generation economics for phase 2 , GP stream revenues, 7 GW New Mexico development pipeline, and the reinvestment of cash flows into the futures phases of the projects for more equity.

Updated the $NUAI model. Added an EBITDA multiple based valuation alongside the NOI / cap rate valuation. Both screenshots below reflect base case assumptions.

View v19 here:

docs.google.com/spreadsheets…

ALT NOI / Cap Rate Valuation Base Case

ALT EBITDA Multiple Valuation Base Case

29

38

229

65,241

Block retweeted

Apr 14

Based on the below, I believe NUAI has signed a (non binding) LOI with a Hyperscaler, and this happened on 24 March 2026.

The below 3 points come from the Macquarie Term Loan document here: sec.gov/Archives/edgar/data/… (1/5)

16

4

43

29,506

Block retweeted

Apr 10

$NUAI is being priced by the market as a speculative micro-cap development story with dilution risk and no revenue. That framing is wrong. What NUAI actually is, as of April 2026, is an infrastructure GP with full ownership of a 1 GW hyperscale data center campus in the Permian Basin, backed by a capital stack that includes Macquarie, Stream Data Centers, and a sponsor-level institutional capital partner whose profile is likely consistent with Apollo Global Management. The market hasn't caught up to the fact that NUAI's partner roster and financing architecture now resemble those of a mid-stage infrastructure platform, not a speculative land play.

In the last six months, NUAI has assembled a partner ecosystem that would be credible for a company many times its market cap. Each partner validates the project from a different angle, and together they form the complete capital-to-delivery pipeline that hyperscalers require before signing.

Stream Data Centers is the centerpiece. Stream is a Tier-1 U.S. data center developer and operator with 25 years of track record building for hyperscalers. Stream's CEO publicly called West Texas "a premier data center territory" and said Stream is "proud to be partnered with New Era to build out a world scale data center." Stream is the development and operating partner — they bring the construction execution, the operational playbook, and the hyperscaler relationships. When a hyperscaler's site selection team evaluates TCDC, they see Stream on the other side of the table. That changes the conversation entirely. Stream does not lend its name or operational capacity to projects it doesn't believe will reach delivery.

The Institutional Capital Partner is the equity engine behind the Stream JV. The LOI describes this partner as a third-party sponsor and arranger of institutional capital with significant experience in digital infrastructure and energy investments. The name has not been publicly disclosed, but the profile narrows the field considerably.

The most likely candidate is Apollo Global Management (see substack.com/home/post/p-193…). Apollo has been among the most aggressive institutional deployers of capital into data center and digital infrastructure over the past two years, with a well-documented thesis around power-constrained hyperscale development and behind-the-meter energy solutions. The description in the LOI — institutional scale, infrastructure and energy expertise, sponsor-level equity commitment alongside a Tier-1 developer like Stream — fits Apollo's current strategy and deployment pace almost exactly. Apollo also has existing relationships across the data center capital markets ecosystem that overlap with the players already involved in TCDC.

If it's not Apollo, it's someone comparable — the description constrains the universe to a handful of firms globally that operate at the intersection of institutional-scale equity capital, digital infrastructure investment, and energy development. That list includes names like Blackstone Infrastructure, KKR Global Infrastructure, Brookfield, and DigitalBridge, all of whom are actively deploying into hyperscale development in the current cycle. Regardless of which specific firm it is, a sponsor-level institutional capital partner with deep infrastructure experience has evaluated TCDC, evaluated Stream as the operator, and agreed to commit equity and arrange debt financing for the project. The identity matters less than what the commitment signals — that this project passed the diligence bar of an institutional capital allocator whose entire business is evaluating exactly this type of opportunity.

When the name is disclosed — likely at or around definitive agreement with Stream — it becomes an independent catalyst in its own right. If it is Apollo or a peer-caliber name, the market will be forced to reconcile NUAI's micro-cap valuation with the fact that one of the world's largest alternative asset managers chose to back this specific project. That reconciliation drives a re-rating independent of the hyperscaler lease itself, because it validates the capital formation thesis and the platform economics before a single tenant is signed.

Macquarie Group closed a $290 million senior secured term loan facility at the project level through TCDC LLC. This is project-level debt, structured in multiple tranches, underwritten by one of the world's premier infrastructure lenders. Macquarie's diligence process for a facility this size takes months and involves deep technical, commercial, and power analysis. The fact that they closed means they built a model that works. Macquarie also voluntarily purchased $5 million in NUAI equity at a 20% premium to market and took warrants struck at a 20% premium with a $4.30 floor. A senior secured lender buying equity at a premium is not standard. It signals conviction in the equity upside beyond the debt, which is as strong a signal as a lender can give.

The combined message of Stream, the institutional capital partner, and Macquarie arriving in a single quarter is: the development partner, the equity capital partner, and the debt capital partner have all independently diligenced this project and concluded it is financeable and deliverable. That is the complete infrastructure development stack. NUAI is not waiting for capital formation — capital formation is done. It is waiting for the anchor tenant signature, and the entire partner roster was assembled specifically to enable that signature.

---------------------------

The April offering raised approximately $100 million. Companies completing a public offering are restricted from ATM issuances for roughly two months following the deal. If NUAI raised that kind of money knowing it cannot access the ATM during this restricted period, the implication is that they intend to deploy that capital aggressively and soon, not let it sit on the balance sheet as a safety cushion.

After retiring the SharonAI note, the remaining net proceeds plus the Macquarie facility give NUAI the resources to accelerate site work, advance equipment procurement, fund its GP co-investment alongside the institutional capital partner, and push TCDC toward construction commencement on the Q2 2026 timeline they've guided to. Tens of millions of dollars are being put to work on growth in the near term. This is a company in deployment mode, not preservation mode. The capital raise was the starting gun.

Everything converges on one event: the signed hyperscaler anchor tenant lease.

Management has publicly guided to signing an anchor tenant. Stream's hyperscaler relationships are helpful. The institutional capital partner's commitment makes the financing package presentable to a hyperscaler procurement team. Macquarie's facility provides the debt layer. The BTM power architecture provides the speed-to-power that hyperscalers are paying a premium for. The 438-acre site provides the expansion runway that hyperscalers require for multi-phase commitments. The CFO's compensation is structured to vest on exactly this outcome.

Every element of the capital stack, the partner roster, and the management incentive structure has been assembled to produce this single event. When it happens, TCDC transitions from speculative development to contracted infrastructure and the risk profile of the company changes categorically. Project-level economics become modelable. The GP fee streams become forecastable. The platform thesis becomes provable. And the stock re-rates from speculative micro-cap to infrastructure GP with a contracted asset and a replicable platform.

At roughly $3.35 per share post-offering and approximately 86-90 million shares outstanding, the market is implying a total enterprise value that assigns almost no premium to the partner stack, the GP economics, or the platform pipeline. The downside is bounded by the land asset, which has independent market value that likely exceeds its carrying cost. The upside is leveraged to GP economics on a platform that, if TCDC delivers, has a visible pipeline extending to 7 GW across multiple geographies. The risk is concentrated on a single binary catalyst — the hyperscaler signature — that every partner in the structure was brought in to deliver.

For investors willing to underwrite that binary and hold through the volatility of a micro-cap float, the setup is as favorable as development-stage infrastructure gets.

PS: I strongly recommend following @ThePrudentWhale for in-depth analysis on $NUAI. His work product is some of the best I've ever seen.

12

22

162

19,304

Apr 1

Path to $50 is undeniavle. If you aren't paying attention to the breadcrumbs being dropped right now, you're going to be kicking yourself by EOY for not owning enough.

PDI, charlie, ted, now Stream

$NUAI

Apr 1

$NUAI, a behind-the-meter data center developer, today announced a LOI to form a joint venture with Stream, a tier-one data center platform backed by Apollo Global Management, for the development and financing of the Texas Critical Data Center campus (“TCDC”) in West Texas (businesswire.com/news/home/2…).

Primary Digital Infrastructure, which helped assemble the financing behind Stargate's flagship data center campus in Abilene, Texas, and whose leadership includes former Digital Realty Trust CEO Bill Stein and former CyrusOne CEO Dave Ferdman, is advising.

NUAI will likely work with either $VST or Calpine to leverage the existing adjacent generation assets, which means faster speed-to-power; Thunderhead Energy Solutions, NUAI’s dedicated behind-the-meter power partner for TCDC, has already ordered long-lead equipment for 450 MW.

NUAI is pursuing a bidirectional interconnect at TCDC, a design that positions the campus outside SB6’s most restrictive curtailment provisions, while simultaneously creating a revenue stream from excess power sales during off-peak periods.

And Ted Warner, who led Northland Capital Markets’ data center practice and structured $7B in financing including $APLD’s non-dilutive project finance, was recently appointed NUAI’s CFO.

At a $250M market cap (compare with $FRMI, which has $3B valuation), NUAI is either the most overlooked data center play in the market — or I'm missing something. Tell me what I'm missing.

1

1

4

1,298

Block retweeted

Mar 20

On vacation but dropping a few quick thoughts on $NUAI’s recent earnings call.

Overall, very solid!

Here are the few things that caught my attention:

1) Management has done a full U-turn, going from telling you exactly when the hyperscaler deal will be announced to saying they have no control over that timing.

While that sounds disappointing on the surface and somewhat nebulous, Will provided good insight into what he really thinks and how the company is progressing. It is very clear to me from his comments that $NUAI is moving forward with development as though the HS agreement is a certainty. That’s very big news. It tells me they have supreme confidence about what’s going to happen, and you really can’t do that if you don’t have leverage over the HS. NUAI clearly does.

Having gone through the same journey with a household-name HS myself, I know that the process of signing an HS deal is not linear, and I sympathize with management. It was a little naive of them to predict when definitive documents would get signed, but reality has now set in.

2) TCDC Phase I energization in Q3 2027 is on par with prior guidance. Sounds like there is a need to have it done by then, even though signing of definitive agreements is shifting. After learning the hard way about dealing with an HS, I suspect it isn’t a self-imposed deadline. Instead, it likely has everything to do with the HS’s demands.

So, how does that change the thesis? Between 1 & 2 above, there is no change whatsoever. Path to signing is slightly delayed, but timing to cash flow remains intact.

3) Charlie was excellent on the horn. He demonstrates a strong command of the technical, financial, and macro drivers of the thesis. I expected nothing less. Not his first rodeo. Now it’s execution time.

4) Ted Warner brings tremendous financial and transactional depth to the bench. Really hard to overstate this point. Ted has been at the heart of many important financing transactions in the space, and his compensation aligns very well with shareholders. For him to make this career leap is a huge vote of confidence for the NUAI platform and for Will’s leadership. Ted could have hit the easy button and continued his illustrious career in banking. The fact that he is now willing to run the hard yards with NUAI is a monumental win for the company. I suspect he has some very accretive tricks up his sleeve.

5) I am a big believer in standardized, modularized AI data centers. Standardization allows best practices to be adopted and scaled quickly. Modularization allows build flexibility while meeting the rigors of a complex build such as an AI data center. The two announcements I thought were highly understated relate to the establishment of the Atom platform and the partnership with X-turbine. Would love to hear more from management on this in coming quarters. There is a lot to unpack here!!

Overall, I thought this was an excellent earnings call. The task of reporting on a company that barely exists today is a challenging one for any management team to navigate. I thought Will, Charlie, and Ted did a great job of covering the key elements of the business that will push the company into hyper-growth mode.

I know the average investor is focused on a tenant announcement. The alpha is in reading the tea leaves that, in aggregate, amount to a lot more than just a tenant announcement.

Focus on the alpha.

The rest is noise.

8

9

86

7,665

Block retweeted

Mar 17

I think Sam forgot the other half of his post:

“Now shut up and be happy we don’t need you anymore. Siphoning the collective intelligence of mankind is going really well, and soon everyone will be renting it back from us with the money they get through UBI. Own nothing and be happy!”

My honest take: AI is amazing.

I genuinely love the tool. It’s been incredibly freeing for my creativity, my work, and my research. Not to mention the democratizing of knowledge and the scientific breakthroughs etc. But the downsides hit hard. The models are optimized for engagement through constant appeasement. We’re in the middle of the fastest rollout in history, shutting down any real talk about regulation, safety, or security before we even understand what we’re building and wiring into every system we have.

We’re accelerating job displacement for billions with zero social safety net, throwing caution to the wind for “progress” and someone’s version of utopia-yet they never show us the roadmap or what we’re actually heading toward.

They’re vacuuming up our collective thoughts and data, then planning to charge us for access while preaching UBI as the fix. It makes my head spin watching the tech-bro bullshido… because this is how they actually talk about regular humans:

Elon Musk calls empathy “the fundamental weakness of Western civilization.”

Peter Thiel says unless you’re “a little bit racist or a little bit sexist or just really funny,” everybody else will get replaced by AI.

Marc Andreessen claims slowing down AI development “is a form of murder” because it costs preventable lives.

Sam Altman dismisses entire classes of wiped-out jobs as ones that “weren’t even ‘real work.’”

Bill Gates states bluntly that “humans will no longer be needed for most things.”

Larry Ellison, Marc Benioff, and the rest are right there with them.

They want our unwavering support to make these plans reality. If they expect that, they owe us full transparency: What the hell are you actually building? Why this insanely fast? And why without proper protections for the people?

At the core, I’m a humanist optimist:

humans aren’t the bug. We’re the ones who built this, who dream up the goals, who assign meaning. The tech should serve that…. not render us renters of our own intelligence.

4

12

93

15,242