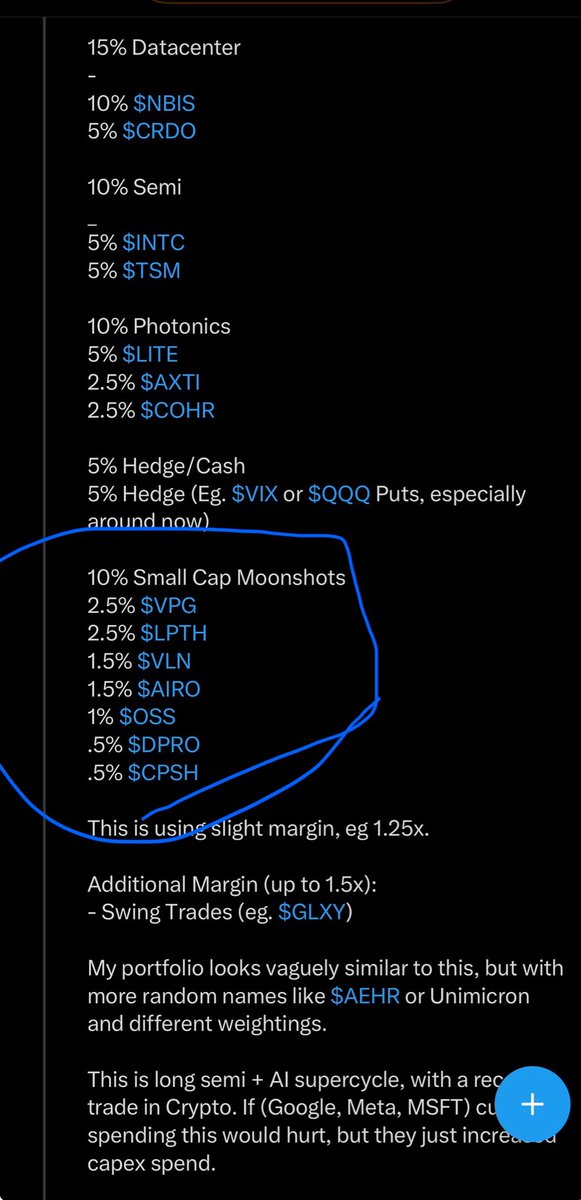

irresponsibly catching falling knives

Joined May 2025

- Tweets 2,143

- Following 732

- Followers 6,695

- Likes 15,149

161 Photos and videos

Jun 10

Market immediately started dumping again

Jun 10

IRAN MISSILE SHARDS STRIKE ISRAEL AIR BASE

Shrapnel from an Iranian ballistic missile reportedly hit an Israeli Air Force base in northern Israel on Sunday night, according to Israeli and military sources. The IRGC said it targeted the Ramat David base in an early missile barrage and released footage of launches. Israel says debris struck a structure and is assessing damage, with the incident still under investigation by the IDF.

6

1,043

Jun 10

Robinhood brokerage could take over “all their bases belong to us” style if we had:

1) international markets

2) same day tax lot sales

3) alerts on technicals like TradingView

And for me selfishly:

4) 10min candles

$hood @vladtenev

2

632

Jun 9

This aging very well currently.

Profit taking before release of

1) cpi

2) ppi

3) fomc

1

8

1,122

Jun 9

$keel surging 10% at open.

I didn’t catch the Iran war bottom but called it early.

The best is yet to come, wonder who they are signing.

$bitf renamed to $keel in 2026

10 Nov 2025

$BITF may be a "diamond in the rough".

Secret weapon: Scrubgrass site in Pennsylvania.

Potential of this one site = 1 GW capacity.

Company has 11 other sites, but we'll focus on Scrubgrass here. It'll make sense why.

Risks:

- Power not fully secured, yet.

- #1 in queue for application to be processed. Nobody can cut the line. Actively increasing the power request in application while all other companies must wait behind them.

- Company just secured $1B in liquidity to show regulators. Tick tock.

- Only public miner outside of Texas that has a 1GW potential.

- Proximity advantage to undersea fiber lines to Europe

- Power peaker plant located 2 miles north that absorbs power instead of generates power for the grid. Power abudance in area.

- 63MW energized today at Scrubgrass.

- Surrounded by hyperscaler data centers.

- Additional generation capacity of 500MW of natural gas which can be added to site.

Qualitative:

- CEO @hashoveride (Ben) has 92-95% of his net worth is tied up in his $BITF stock. He's only sold shares once since he joined the company 7 years ago, in November 2021. @ericjackson might like that.

- New CFO Jonathan joined 10/26/25. Multidecade project finance experience. Negotiated deals on the other side of table.

- 40 of 40 institutions elected to subscribe to their convertible note round. 9x oversubscribed. Unheard of before. There was enough subscription to raise $2.6B in 48 hours. However, $BITF only decided to expand their round from $300M to $500M instead.

- T5 partnership: Built & operated data centers for 30 years. Well known and trusted by hyperscalers. They validate architecture & engineering. Handhold the permitting applications to line up with what hyperscalers are looking for. Flat fee based structure with no pro forma ownership thereafter.

- Capped calls on convertible from 30-125% of premium to keep it antidilutive for legacy shareholders. Only one reason they'd elect to do that.

- Strategy upfront is colocation only and just execute until the right time to sign a deal. Everytime a deal is signed, the remaining unsigned MW on the market become more valuable.

- Direct operating margins for GPUS = 85-90%. Meaning energy costs contribute minorly to operating margins for cloud providers. Paying a few points higher for energy costs just to be plugged in and making revenue far outweighs any alternative. The longer they wait for a deal, the more valuable the unsigned MW become.

Macro:

- By 2030, we need about 120-130 GW of power for AI data centers.

- Today, there's about 10 GW of power for ai data centers.

- The pipeline consists of 40-50GW to be built from now through 2030.

- 10 GW today 45 GW announced pipeline (mid point) = 55 GW potentially available. The need is greater than 100GW by 2030. We have a deficit of 45-75GW in the industry by 2030.

-Every MW or GW uncontracted becomes more valuable as each deal gets announced.

- Every minute a GPU isn't plugged into power equates to greater opportunity cost.

Conclusion:

- a combination of $BITF's footprint, liquidity, operating team, plus CEO @hashoveride YOLO'ing into this = I'm betting on this.

- stock is $3.69 as I'm writing this. your welcome.

4

1,125

Jun 8

Buy up. Premarket going crazy

Jun 8

IRAN DECLARES END OF MILITARY OPERATIONS AGAINST ISRAEL: FARS

6

917

May 29

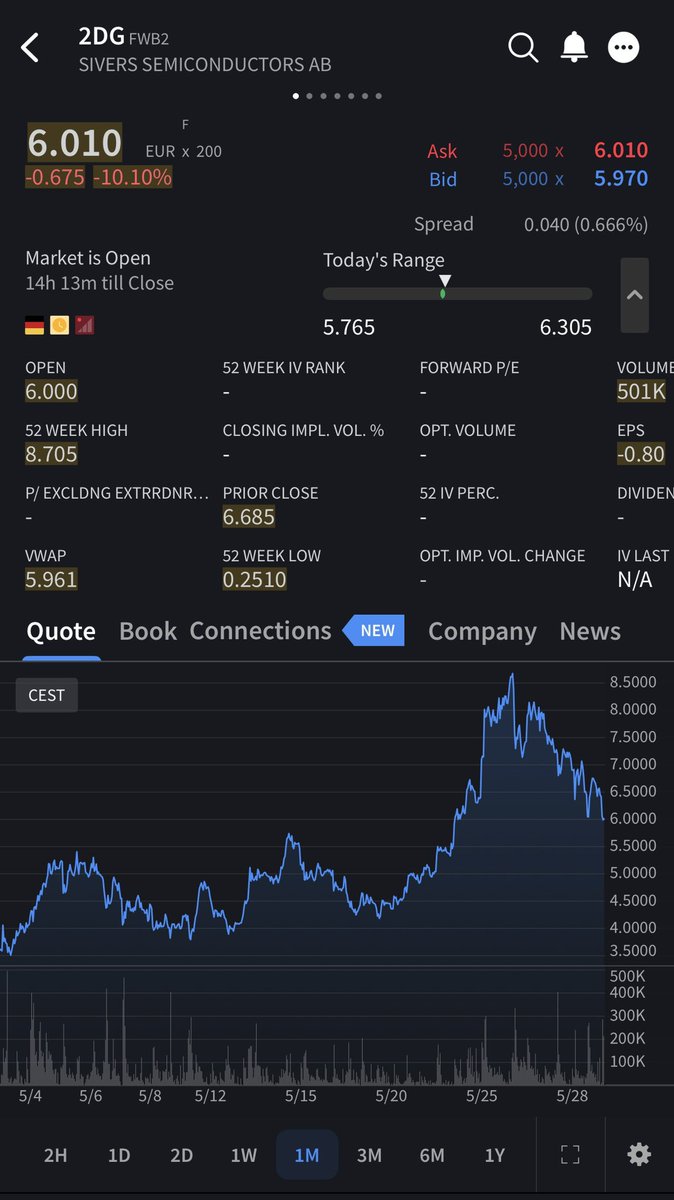

$SIVE Q1 2026 earnings release observations:

22% revenue miss looks ugly on the surface, yet nothing here breaks the actual bull case. The thesis for 2027 inflection just got stronger imo.

1) Pipeline exploded 77% to $799M YTD (most important takeaway)

2) Jabil 1.6T win validates the laser tech for AI datacenters (most important takeaway)

3) Lidar ramp holds for Q4 2026

The setup for a probable 2027 inflection is there. However, shareholders have to survive the liquidity issues before that, they will run out of cash in 3-4 quarters or less.

Q1 results:

- Cash down to 26.6M SEK

- Q1 burn 49.2M (3x last year)

- 125M raise closed April, but that’s <1yr runway

Management says FX headwinds and US defense budget plus shutdown delays pushing revenue from Q1/Q2 into H2 2026:

- Revenue 61.9M SEK, −22% YoY (miss vs 74M consensus).

- Defense budget delays FX pushed sales into H2.

Both segments shrank:

- Wireless −16%

- Photonics −32%

2

2

9

2,456

May 29

$ASTI - Ascent Solar

A toaster sized satellite making 150W. That’s power normally seen on craft 10x bigger. $asti’s flexible solar “blankets” make it possible. They’re on NOVI’s Pathfinder, targeted to launch spring 2026 on Falcon 9. If the constellation scales, $asti gets to power all of it (that’s the lotto ticket).

Why asti’s flexible solar panel is different:

The core idea is a solar panel you can roll up like a yoga mat. It’s a game changer because:

1) Weight. This is the big one. Far lighter per watt than rigid silicon, which is everything in SPACE and on DRONES where every gram costs money to lift.

2) Flexibility. It rolls tightly for launch, so it takes up little stowed volume, then unrolls in orbit.

3) Durability. No glass to shatter. If struck by debris in space, it fragments less, which matters for orbital safety.

- company is about 20 people in Colorado

- debt free, $16M cash, basically considered pre revenue and burning cash.

- runway about 2 years based on $2M/qtr burn

CIGS = how much of the sunlight hitting a solar cell gets converted into electricity.

- asti CIGS (flexible panels) = 15.7%

- Mainstream CIGS (rigid silicon) = 20-22%

Asti’s 15.7% cigs must be respected. In space the metric that matters is power per kilogram, not power per square foot. Same with drones.

Upcoming catalysts:

- NOVI Pathfinder launch on Falcon 9, spring 2026.

- NOVI constellation scale up. The real prize.

- potential Defiant and NASA deals.

1

18

2,655

May 28

Correction:

the alsic for rubin thesis is wrong for $cpsh. semianalysis already did the work

rubin and rubin ultra at 1800w to 2300w are not getting alsic lids. the thermal stack disclosed by nvidia at ces 2026 and detailed by semianalysis is:

copper base lid with electroplated gold (to resist indium tim2 corrosion)

stiffener added for warpage control

microchannel lid (mcl) etched into the copper itself

liquid metal indium tim2

gold plated copper cold plate

no aluminum silicon carbide anywhere in the spec

the two taiwan winners are:

jentech precision (tpe: 3653) sole supplier of tsmc cowos lids and stiffeners. 100% share in ai chip lids. mcl asp is 7 to 10x the blackwell lid. if all nvda chips migrate, jentech revenue could grow 50%

asia vital components (avc, tpe: 3017) partnered with nvidia on the microchannel cold plate for rubin ultra

amd mi450x at 2500w follows the same roadmap. nvidia, amd, aws, google are all converging on copper mcl, not alsic

alsic is a real material with real defense and space and power electronics uses, but it is not the rubin packaging material. the entire ai bull case people are putting on $cpsh is built on a thesis the original substack author rated low probability and that semianalysis never even mentioned

if you want the rubin thermal trade, the names are 3653 tt and 3017 tt, not $cpsh

May 26

Serenity was early, again.

$cpsh ran from $7 to $10.82 intraday then $11.72 aftermarket. volume 17.5m vs 900k avg (19x normal). new 52w high

confirmed in $nasa tema space etf as of may 22: the ETF owns 1.82m shares, 0.76% of NAV, about 10% of cpsh float held by the etf

balance sheet: $12.5m liquid, zero debt, 18m shares outstanding (10% held by $nasa ETF)

concentration risk: top 3 customers = 64% of fy25 rev

segment potential:

- power electronics (the actual core, 60-70% of rev): hvdc, ev and hev inverters, wind, sic and gan modules. the $15.5m semi order lives here. q1 10q flagged this customer taking less than 50% of contracted qty.

- space (real but small): flight heritage on gps iii sats, mars 2020 rover, iss, methanesat. est $3-8 million today. golden dome and sda is the upside lever.

- defense (mixed real plus r&d): navy destroyer hybridtech armor with congress funding secured, ceo says modest scale. tungsten 40mm warhead phase ii sttr ($1.15m, 2 year r&d). uh 60 armor is sbir research. about 5% of rev from sbir per cfo

- ai and gpu thermal: current ai supply chain goat @aleabitoreddit posted a thesis on this ticker:

1) alsic could be spec’d as microchannel lid for 2300w plus chips. $cpsh would be one of few western suppliers. denka, sumitomo, byd are the incumbent risk.

2) laid out the materials science case for AlSiC in rubin/mi450x packaging at 1800 to 3000W TDPs.

3) mentioned as rubin's to scale up to 2300-2500W in 2027-2028, that same material may be used ai due to heat warpage.

my research on official filings and $cpsh management transcripts show zero company mention of nvidia, rubin, or gpu in any earnings call. but would trust serenity over myself sincr im not even close to an ai scientist

also watch:

- DOE nuclear (radiation shielding, snf transport)

- electric rail and subway mmc baseplates

- 5g and satcom hermetic packaging

- new commercial tungsten injection molding line (first order shipped apr 2026)

1

3

2,325

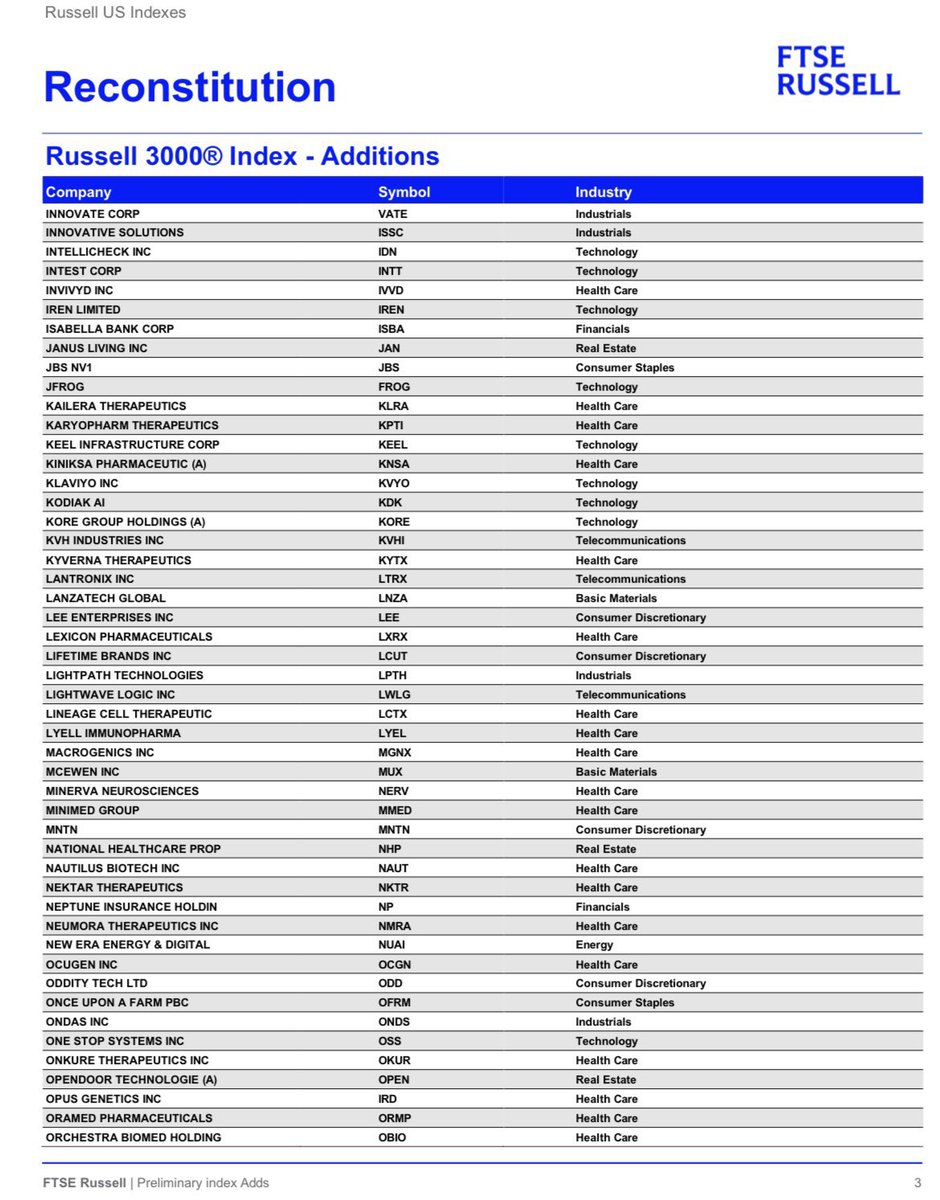

May 28

Is that $600M atm almost done yet for $aaoi?

Last time it took them 35 calendar days (25 trading days) to raise $500 million at the market when the stock price was around $90-100 dollars

The share price was somewhere between $170-190 during this the current ATM, my estimate is it should be done either this week or first week of June at the latest.

I think the best way to tell is to see if this stock can hit $190. If it does hit $190 again, then I think that the atm is done.

4

1

27

6,218

May 28

$cpsh is the most asymmetric small cap in space and defense right now.

One of serenity’s “moonshots” in her portfolio.

the story:

only western alsic pure play. sole source supplier per the 10k. flight heritage on gps iii, mars rovers, iss. navy hybridtech armor on aircraft carriers. dept of energy nuclear shielding. these are real, hard to replace positions

$nasa tema space etf holds about 10% of the float on an 18m share count. that is a structural buyer that did not exist 2 months ago

fy25 revenue up 54% to $32.6m. zero debt. and today they fortified the balance sheet with a $9.6m raise, taking liquidity to roughly $21m to fund the facility expansion. dilution is 6.7%, priced at $8, but it removes the financing overhang going into the growth phase

the kicker: ai thermal. as rubin and mi450 scale past 2000w, packaging warpage is a known issue. alsic is a candidate fix. if big tech specs it in, cps is one of the only non asian sources on earth. that call option is essentially free at this market cap

straight read: at $11 vs a $5.50 analyst target, a lot of this is narrative and momentum. q2 on jul 28 needs to confirm the recovery. but the risk reward on a sole source materials chokepoint with an etf bid is the kind of setup that does not show up often

1

4

18

2,925

May 26

Serenity was early, again.

$cpsh ran from $7 to $10.82 intraday then $11.72 aftermarket. volume 17.5m vs 900k avg (19x normal). new 52w high

confirmed in $nasa tema space etf as of may 22: the ETF owns 1.82m shares, 0.76% of NAV, about 10% of cpsh float held by the etf

balance sheet: $12.5m liquid, zero debt, 18m shares outstanding (10% held by $nasa ETF)

concentration risk: top 3 customers = 64% of fy25 rev

segment potential:

- power electronics (the actual core, 60-70% of rev): hvdc, ev and hev inverters, wind, sic and gan modules. the $15.5m semi order lives here. q1 10q flagged this customer taking less than 50% of contracted qty.

- space (real but small): flight heritage on gps iii sats, mars 2020 rover, iss, methanesat. est $3-8 million today. golden dome and sda is the upside lever.

- defense (mixed real plus r&d): navy destroyer hybridtech armor with congress funding secured, ceo says modest scale. tungsten 40mm warhead phase ii sttr ($1.15m, 2 year r&d). uh 60 armor is sbir research. about 5% of rev from sbir per cfo

- ai and gpu thermal: current ai supply chain goat @aleabitoreddit posted a thesis on this ticker:

1) alsic could be spec’d as microchannel lid for 2300w plus chips. $cpsh would be one of few western suppliers. denka, sumitomo, byd are the incumbent risk.

2) laid out the materials science case for AlSiC in rubin/mi450x packaging at 1800 to 3000W TDPs.

3) mentioned as rubin's to scale up to 2300-2500W in 2027-2028, that same material may be used ai due to heat warpage.

my research on official filings and $cpsh management transcripts show zero company mention of nvidia, rubin, or gpu in any earnings call. but would trust serenity over myself sincr im not even close to an ai scientist

also watch:

- DOE nuclear (radiation shielding, snf transport)

- electric rail and subway mmc baseplates

- 5g and satcom hermetic packaging

- new commercial tungsten injection molding line (first order shipped apr 2026)

Jan 29

I've initiated positions in $CPSH as a US AlSiC pure play chokepoint.

They represent ~25% of the near-term semi-grade AlSiC market.

Their customers:

- U.S. Navy (War)

- U.S. Army (War)

- U.S. Dept. of Energy (Energy / Nuclear)

- U.S. Space Force / NASA (Space)

- Lockheed Martin ( $LMT )

- Raytheon ( $RTX )

- Northrop Grumman

- General Dynamics

- The U.S. Navy uses $CPSH for ballistic protection systems of the newest carriers (like the USS Gerald R. Ford and USS Abraham Lincoln). As well as other fleets like the Danish Navy through Lockheed.

- US Army uses $CPSH for 40mm Tungsten Warheads and UH-60 Black Hawk Helicopters.

- The US Dpt of Energy uses $CPSH for impact limiters when transferring nuclear fuel (SNF) and high-level radioactive waste via rail.

- U.S. Space Force / NASA uses $CPSH for GPS satellites and it sits in many electronic systems in the International Space Station. (Also not including Mars Rover missions)

- Lockheed, Raytheon, Northrop, and General Dynamics uses $CPSH for missile heat-shielding components. AlSiC housings for radar systems, and thermal management materials.

AlSiC or (aluminum silicon carbide) is a well known material composite that handles extreme thermal conditions for many applications above from space to defense.

But as architectures from $NVDA Rubin to scale up to 2300-2500W in 2027-2028, that same material may be used AI due to heat warpage.

My thoughts were that the tiny TAM material used to handle extreme changes in heat from hypersonic missiles to rocket nose cones may likely be used for AI deployments.

This is similar to how InP (niche TAM for Telecom) became a bottleneck as photonics scaled up. Or how Toto's fine ceramics for toilets were critical to memory.

AlSiC (esp. post-processing) may become a potential chokepoint as AI ramps up to Rubin generation chips.

Majority of the world's AlSiC production still originates in East Asia (Denka,Sumitomo, BYD, JFC).

But CPS is currently the primary "US/Western hedge" and CPSH states they represent roughly 25% of the near-term available AlSiC market (CPS Technologies AGM Presentation).

And that percentage of the supply chain is only worth ~$100 MC right now.

Their balance sheet:

$12.7M – $13.8M (pro-forma) cash. Almost 0 debt. Inventory ~5.4M, Liabilities: ~$5.06M (eg. $3.53M for aluminum and silicon carbide)

Y/Y revenue is 8.8M, up 107.29%.

Y/Y Net income is up 207.96K ( 119.94%).

Healthy balance sheet and US Government strategic interest Defense Contractors gives $CPSH low downside risk at $100M or even at $200M as the leading Western AlSiC supply chain.

There were new contracts eg. $15.5M order from the leading Semi likely ~Infineon last October, that more visibility into revenue upside. And they are expanding production (funded by their Oct 25th raise), which hints to higher demand.

"We believe we are the world leader in the design and manufacture of AlSiC... Many of our products are designed specifically for a single customer application, making us the sole-source provider for those components." (10-K filings)

TLDR: The AI upside depends entirely on a material pivot by big tech. Similar to the Toto toilet maker for memory type but the AI fit seems strong.

But the benefit is that its existing list of US DoD contractors gives the company lower downside risk.

This is just my own personal thesis I wanted to share.

But personally I've taken positions in $CPSH as an AlSiC play (and long US supply chains) as it may play an important role with thermal warpage with AI in 2027-2028 as we expand to 2000W .

3

1

16

6,950