Economist @StanfordGSB | Likes Fast Cars

Joined July 2009

- Tweets 1,629

- Following 683

- Followers 1,946

- Likes 3,318

74 Photos and videos

Pinned Tweet

May 16

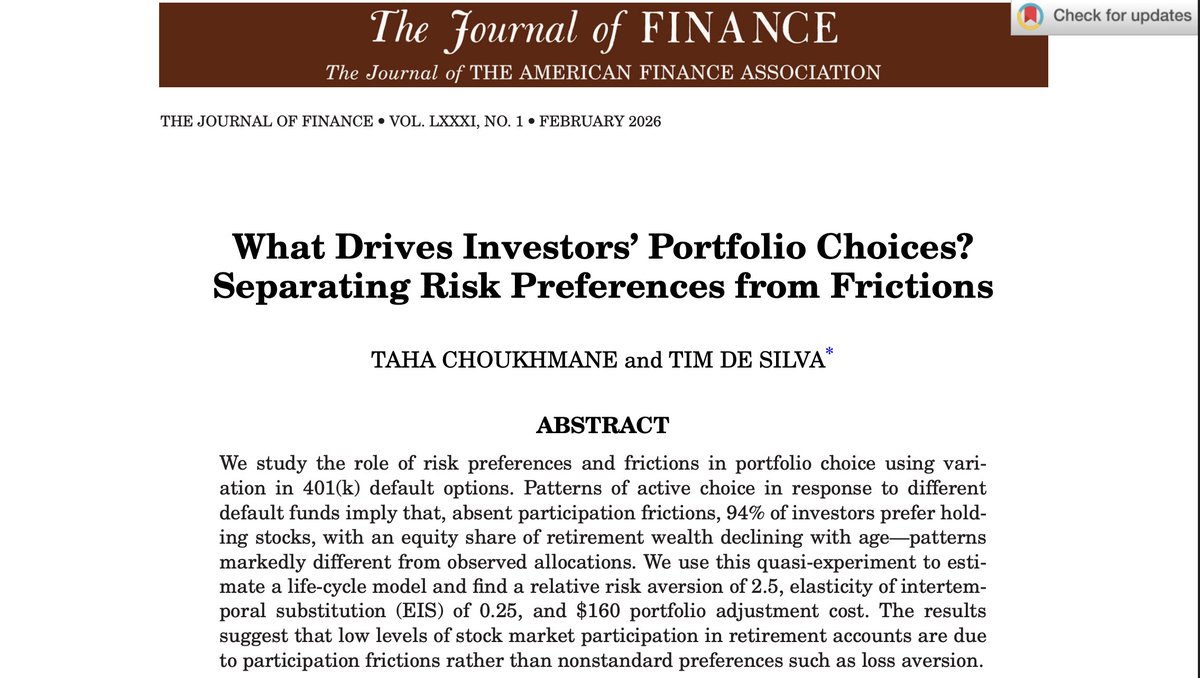

Great coverage by @USATODAY of joint work on LLM financial advice with @TahaChoukhmane, @wdwlin, and @AkuzawaMatthew!

usatoday.com/story/money/202…

4

14

1,404

Tim de Silva retweeted

Jun 6

One person who was completely vindicated in time was Shiller with his AEA address on narrative economics.

I was there at the time, and thought: cool idea, but no way you can operationalize this.

LLMs have made it much easier to study narratives

aeaweb.org/articles?id=10.12…

6

59

494

48,998

The fact that this is hard to internalize is exponential growth bias in reverse!

A closed human population needs about 500 women of reproductive age (15-45) to remain biologically viable in the medium run. That number is not what drives a population to zero: sub-replacement fertility does that on its own. The 500-floor mark is the point of no return: the size below which the gene pool is too narrow to recover, even if fertility later bounces back.

In a hypothetical scenario where Thailand maintains its total fertility rate (TFR) at the 2025 level of 0.87 and has no immigration, its population of women of reproductive age would fall below 500, entering the extinction-risk zone, around the year 2445.

We can play with the numbers a bit (extending the fertile-age window, for example, or lowering the floor through medical advances), but the message holds. Any population that remains below replacement eventually goes extinct.

I make this point because when I write statements of the form “with its current TFR, country A will have a population of X in the year 2200,” I hear the reply “we can live with that.” That reply misreads the year-2200 population as a new stationary point. No, it is just a snapshot of a population still in decline. Sub-replacement fertility has no resting place above zero.

Now, one can legitimately argue that as the population falls, the TFR will rise again, perhaps due to cheaper housing or the selection of groups with higher fertility. (The “more natural resources per capita” story I trust least: the demographic transition broke the old Malthusian link between abundance and fertility, so in modern conditions the sign runs the other way.) These are possible mechanisms, and we can discuss another day whether, given the current evidence, they will be enough to get back to replacement (my two cents: I have run some quantitative simulations, and the answer is likely “no”).

I only want to force everyone to accept the realities of demographic accounting. If you tell me “we can live with that,” you are asking me to buy two separate claims: 1) that we can go from population X to 0.05X without a major social breakdown, and 2) that we will not only avoid that breakdown but also bring the TFR back to replacement by the time we reach 0.05X.

1

762

Tim de Silva retweeted

Jun 12

Ann Carrns from the @nytimes wrote a great article about our latest findings from the Personal Finance Index and yes, the data show we are moving in the wrong direction.

nytimes.com/2026/06/12/your-…

3

8

3,401

Tim de Silva retweeted

Jun 11

"We live in an age of manufactured scarcity”

I honestly struggle to think of one sentence that could be a worse description of recent decades.

Literally more than a billion persons have been lifted out of poverty over a few decades. It’s just an extraordinary achievement even at the scale of human history.

Surely we can do even better but I cannot see how their text can be read seriously.

It’s like we invented fire and they’d complain the night has never been darker and colder.

11

66

456

12,726

Jun 11

Thank you to the Swiss Finance Institute for recognizing our paper on LLM financial advice!

Press release: sfi.ch/resources/public/dtc/…

Paper: timdesilva.me/files/papers/l…

1

30

2,235

Tim de Silva retweeted

🏆 PSE & @ENS_ULM are pleased to announce the #DanielCohenAward 2026 winner: @AnanyaKotia, PhD student @LSEEcon, for his Job Market Paper "When Competition Compels Change: Trade, Management, and Productivity". 🔗 shorturl.at/Dws8D?utm_source…

Funded by Boussard & Gavaudan and AFPSE

2

8

73

24,280

Tim de Silva retweeted

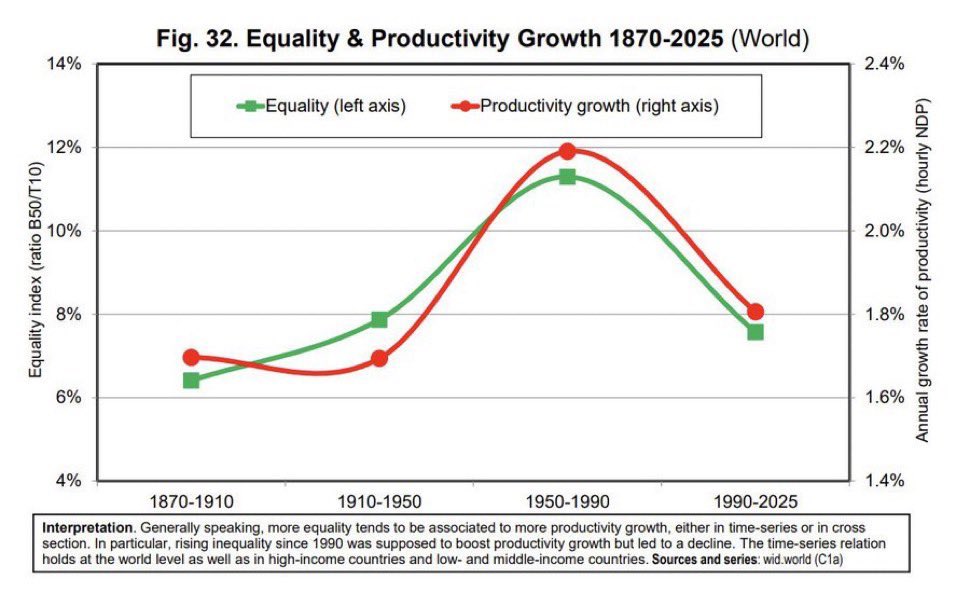

Jun 8

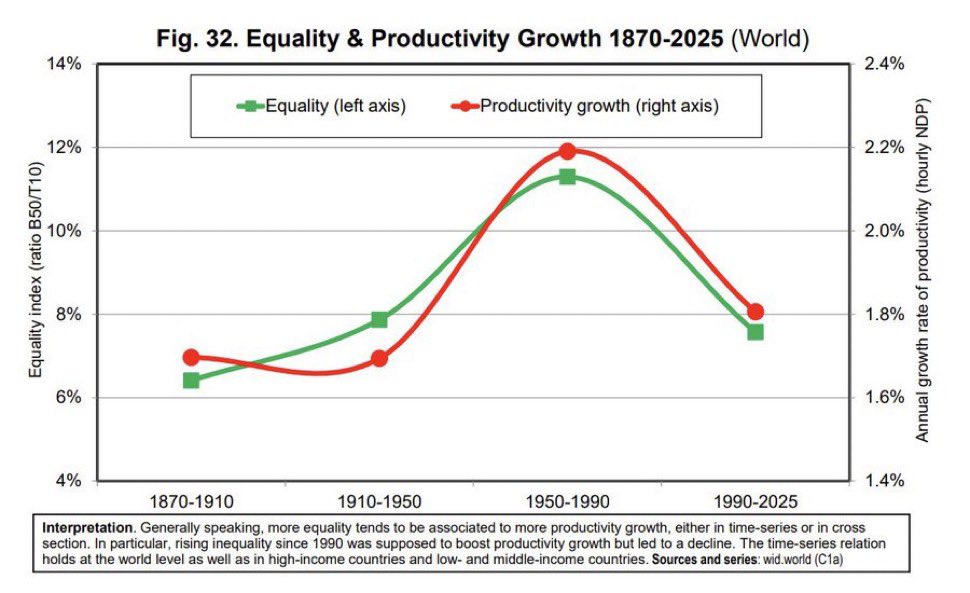

The notion that the world is less equal today than it was between 1910 and 1950 is just historically ridiculous and really makes the point that all these metrics should take much more seriously the vast welfare state systems that emerged during and in the immediate aftermath of this period.

This is the main blind spot of Piketty, Saez and Zucman’s empirical view of the world. They consider the distribution of tax rates, of which a substantial part fund social insurance, without considering the distribution of transfers and benefits. They consider the distribution of wealth without considering the value of entitlements…

This approach creates inequality metrics that would improve if we were to dismantle the welfare state. Which is exactly what this graph suggests by implying that the world is just as unequal today as it was during a period that saw two world wars and the greatest economic depression since the Industrial Revolution.

You cannot celebrate Roosevelt, Attlee and so on and use inequality metrics that make social insurance programs look like they foster inequality

9

100

421

58,021

For those interested, here are my slides from yesterday's Cowles Lecture at the Econometric Society Meetings @YaleCowles @econometricsoc

benjaminmoll.com/cowles_lect…

Thanks so much for listening and for the great discussion and comments!

3

120

516

52,095

Tim de Silva retweeted

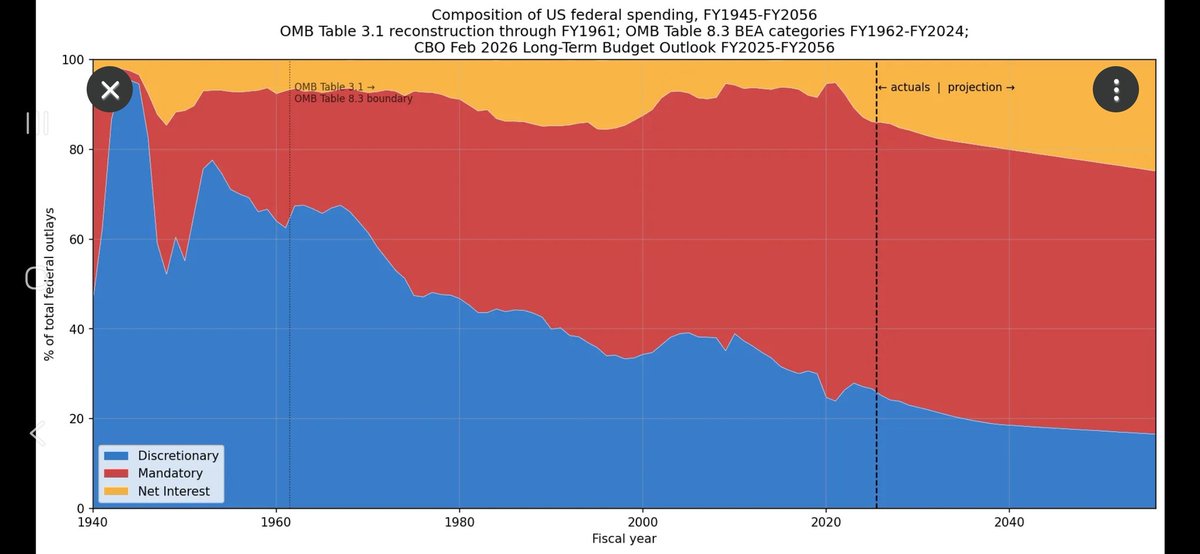

Beautiful post by @HannoLustig

arguing bond holders are the most junior claimants to tax revenue-because of the political power or retirees. (True everywhere.) I was struck by this chart showing how little of government revenue even in the US is used for doing stuff and how much more is just transfers. Our governments become gigantic insurance companies.

open.substack.com/pub/thetwo…

17

57

298

53,821

Tim de Silva retweeted

Excited to see this out! We come up with (AFAIK) a brand new way to solve for market-clearing prices: target an imbalance of zero like a moment condition. We expand the state space to include parameters and prices, so we can estimate and clear markets after solving the model once

5

25

137

14,127

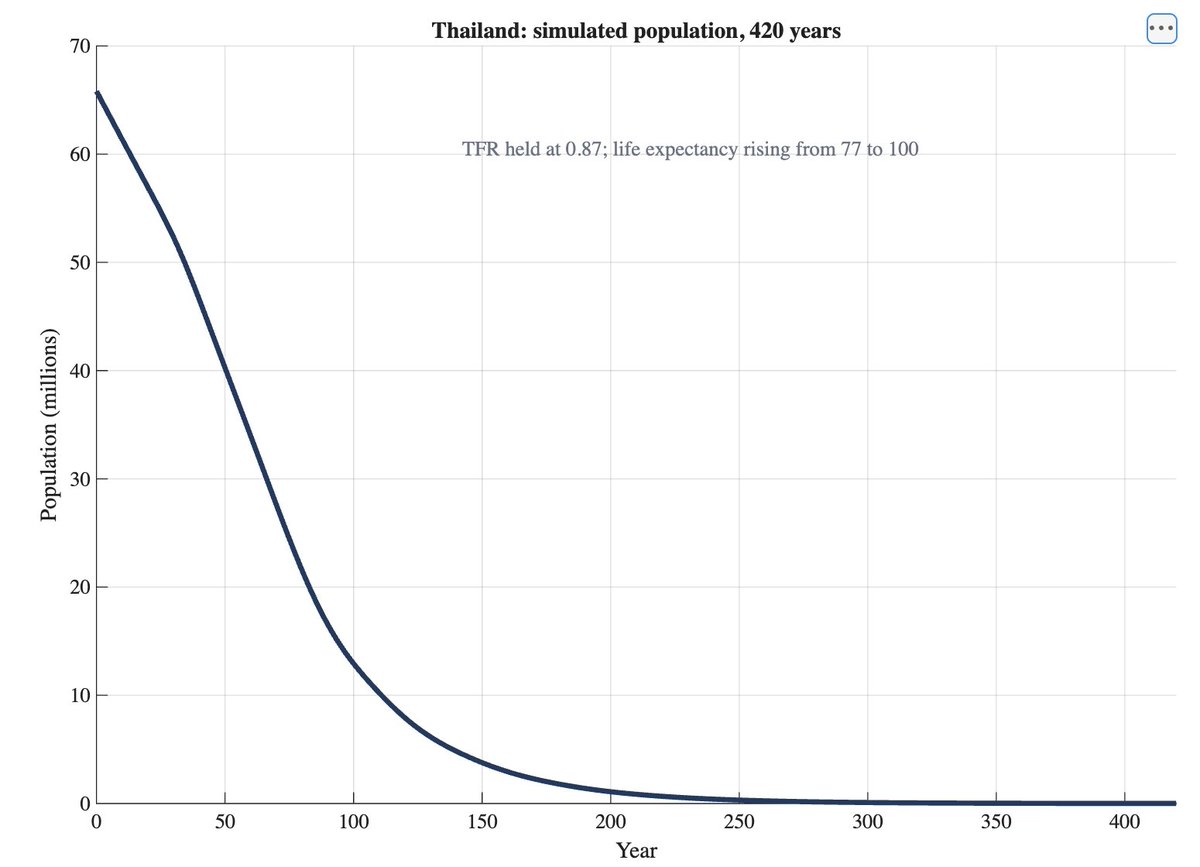

Tim de Silva retweeted

Thailand has one of the lowest total fertility rates (TFR) in the world. In 2025, the TFR was 0.87, and the preliminary numbers for the first months of 2026 are even lower. The rate is so low that deaths have exceeded births since 2021 and now run 34% higher than births.

Thailand’s fertility collapse has always fascinated me. With a flight to a Bank of Thailand conference in Bangkok ahead of me, I spent some time reviewing the data.

Thailand’s TFR fell below replacement in 1991. That is early. It means completed fertility has been below replacement for at least a full generation. In 1991, Thailand was neither rich nor well-educated. Even today, its income per capita (in PPP, the right measure here) is about Mexico’s level, around 28% of the U.S.

The standard theories for East Asian ultra-low fertility, such as a toxic educational arms race or extreme gender inequality, have little bite here. On the World Economic Forum’s Global Gender Gap Index 2025, Thailand scored 0.728 and ranked 66th. South Korea scored 0.687 (101st of 146), and Japan 0.666 (118th of 148, last in the G7).

I think Thailand is the clearest example of modernity without high income, and that combination is a recipe for demographic collapse.

To illustrate this point: if Thailand’s TFR remained at its current level for 200 years, the population would decline from 65.8 million in 2025 to 1.51 million in 2225. While this is a hypothetical scenario used to make the argument, not a forecast, it gives a sense of the magnitude of the population change involved unless TFR increases at some point. This is not about closing a few maternity wards or fixing Social Security, but about winding down an entire country.

Does anyone have a better theory? I don’t have enough information on Thai demographics, and I am happy to update my view.

Two caveats. First, I use Thailand’s official data from the National Statistical Office. The UN WPP data (and the databases built on it, such as the World Bank’s) are, as always, way off. Second, the official statistics may undercount births somewhat. Even if they do, the picture changes little.

123

219

978

197,751

Tim de Silva retweeted

Jun 7

Many of us thought that AI was behind finding the error in Tirole (1985) that Econometrica recently published. Turns out that was not the case. Actually, even after the fact, AI couldn't find the error: arxiv.org/pdf/2606.05383

8

44

269

47,743

Tim de Silva retweeted

Season 1 finale of Econ To Go is live. I joined Neale Mahoney, Director of the Stanford Institute for Economic Policy Research, for a conversation on financial literacy, why it matters, and what we can do about it. siepr.stanford.edu/av/Econ-T…

5

6

643

Tim de Silva retweeted

May 29

We took another look at the capability gap between open-weight and proprietary models. Since the start of the year, open-weight models have lagged the state of the art by four months.

33

143

817

349,147

Tim de Silva retweeted

May 27

When SpaceX IPOs in June, this should finally provide all investors with an opportunity to express their views, including the pessimists who so far have not been able to express their views. Or, does it? Maybe not for SpaceX. Nasdaq specifically changed its rules to accommodate this listing. NASDAQ inclusion within 15 days is estimated to trigger about $7 billion of passive demand. S&P 500 inclusion, if and when it comes, brings another $40-50 billion. And the initial float is only $75 billion. Once you include closet indexers, that number could easily exceed $100 billion.

None of this capital expresses any view on whether SpaceX is worth $1.75 trillion. None of this demand is price-sensitive. It is completely inelastic, borrowing the Koijen-Yogo terminology.

As a passive investor, I'm not super excited about funding space exploration, at least not at these valuations.

This marriage of convenience between deep private markets and passive investing seems like one that is bound to be a rocky one. The whole idea of passive investing in public markets was that there was a deep pool of active investors who made sure prices in public markets were right. But there is limited price discovery in the private phase, because of the incentives of the institutional investors and the lack of shorting. And, given that companies can stay private much longer, companies that IPO are large enough to immediately attract tons of passive capital. Americans with a 401K will now provide immediate exit liquidity for the institutional investors who have been funding this venture.

thetwocents.substack.com/p/h…

6

20

83

15,617

Tim de Silva retweeted

May 26

The elasticity of derived demand is always higher than the world thinks. More generally: for every disruption there are many more margins of adjustment than people anticipate. See Ukraine, Covid (Zoom!). Adjustment is the magic of capitalism.

May 25

While we await for the deal, I think we can already highlight a few oil lessons:

1) Although we don’t yet understand how, China can reduce oil imports massively (>5m b/d cut)

2) Saudi/UAE bypass pipelines work

3) OECD nations can release their SPR at flow rates of >2.5m b/d

2

21

104

22,797

Tim de Silva retweeted

May 22

I write today in Silicon Continent with Jesús Saa-Requejo "Three Theses on AI Value Capture".

We argue that the leading AI labs are betting hundreds of billions on the idea that holds the best model captures the value. We think that's the wrong bet. The model layer is squeezed between customers who can switch with a simple change in configuration and suppliers who are each monopolists. Our hypothesis is that the surplus flows past the labs, to chips above and implementation below.

Hence the country that wins AI is not the one with the tokens on the frontier model. It's the one that is best able to implement the technology.

siliconcontinent.com/p/three…

11

29

115

61,851

Tim de Silva retweeted

May 18

If housing were more affordable in the UK and the US, the birth rate might be slightly higher but it would not reverse the overall trend. More at today's Chartbook Top Links!

5

19

94

14,388

May 24

Lots of economics in this thread!

May 23

Good morning my loves, happy Saturday. Sorry I've been quiet, obviously been busy, but thought it'd be nice to give you all the details on the multi-strategy absolute return program that experienced the 28% drawdown this year. (1/n)

1

5

3,705

Tim de Silva retweeted

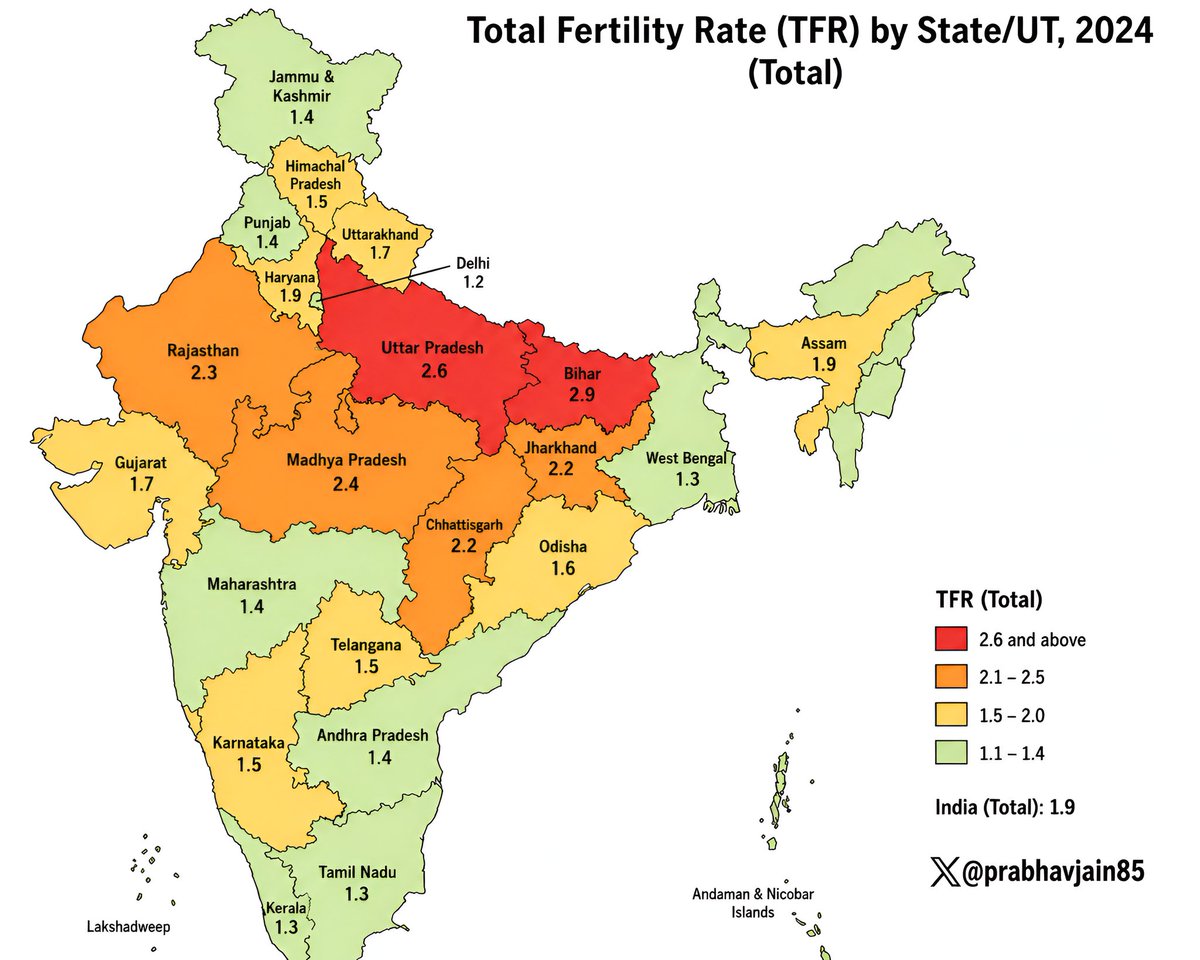

This map, from @prabhavjain85, is fascinating.

Much of India already has TFRs on par with those of Western Europe or Latin America. Look at West Bengal, Tamil Nadu, or Kerala: 1.3! That is below Brazil’s (1.52) or the United Kingdom’s (1.44) and getting close to Italy’s (1.14).

If you are going to tell me some hypothesis about India’s family structure being “different” (i.e., higher marriage rates) in keeping fertility high, you’d better have a good explanation for West Bengal, Tamil Nadu, and Kerala.

At the same time, you still have Bihar at 2.9 and Uttar Pradesh at 2.6.

So right now, the best way to think about India demographically is as two distinct countries: a region with a high TFR and a region with quite a low TFR. Of course, this will have large consequences for the internal politics of India.

48

103

509

49,557