901 Photos and videos

Tur retweeted

Apr 27

Amazing vibe coded site. It's like geoguessr but for history nerds.

I just beat @thesamparr for 4th place.

wen-ware.com

22

26

589

66,253

My biotech long/short basket for 2026.

Long: $CADL, $SRPT, $NMRA, $LXRX

Short: $FLNA, $QURE, $GALT

Expected returns:

3mo: 12%

6mo: 23%

12mo: 32%

Not good vs bad companies. The market is mispricing catalyst risk over the next 6-12 months.

—

The long side is simple. I want names where the market is underpricing a real 2026 catalyst, real product traction, or a regulatory path better than the stock implies.

Best longs: $CADL and $SRPT

Highest-risk long: $NMRA

Slow-burn long: $LXRX

—

$CADL — cleanest small-cap long.

~$4.87 / ~$280M mcap

Expected upside: ~55%

Window: Q2-Q4 2026

Prostate cancer data updates, biomarker readout, planned Q4 BLA. Cash into Q1 2028. One clean update can re-rate the whole name.

—

$SRPT — damaged, not dead.

~$21.79 / ~$1.9B mcap

Expected upside: ~40%

Window: 2026

Market still pricing the 2025 safety/regulatory panic as permanent. But ELEVIDYS is a real commercial product with meaningful revenue and a Japan launch adding credibility.

Thesis isn't "everything is fixed." It's "too much permanent damage is priced in."

—

$NMRA — the binary long.

~$2.06 / ~$295M mcap

Expected upside: ~25% EV, much higher if data hit

Window: Q2 2026

Market hates it after KOASTAL failed. Fair. But KOASTAL-2 and KOASTAL-3 are fully enrolled and read out together Q2 2026. Not the safest long. It's the lottery ticket where upside dominates if data surprise.

—

$LXRX — boring asymmetric long.

~$1.71 / ~$491M mcap

Expected upside: ~25%

Window: 2026 to Q1 2027

ZYNQUISTA regulatory path in 2026, SONATA-HCM topline Q1 2027, better cash position after Novo milestones. Not the biggest upside name but the price looks too dismissive.

—

The short side isn't "these go to zero."

These are stocks pricing too much regulatory optimism, too much story value, or too much credit for weak evidence.

Best short: $FLNA

Most valuation-risk: $QURE

Messiest but still overpriced: $GALT

—

$FLNA (formerly $SAVA) — cleanest short.

~$1.62 / ~$141M mcap

Expected downside: ~35%

Fair value: ~$0.85-$1.05

Window: mid-2026

Alzheimer's story failed. Company renamed. New TSC epilepsy angle is early/preclinical and under FDA clinical hold. Cash expected to drop hard by June 2026 from burn litigation. Still overvalued for what's left.

—

$QURE — overpriced regulatory optimism.

~$17.92 / ~$3.2B mcap

Expected downside: ~25-30%

Fair value: ~$11-$13

Window: Q2-Q3 2026

AMT-130 may have real signal — this isn't a zero thesis. But FDA pushed back on Ph I/II external-control data and recommended a randomized sham-controlled study. Path is longer and messier than the stock prices.

—

$GALT — weaker-evidence short.

~$2.35 / ~$150M mcap

Expected downside: ~20-25%

Fair value: ~$1.60-$1.85

Window: Q2 to early Q3 2026

Not a "fake science" short. The issue is the bull case leans on per-protocol, biomarker, and subgroup arguments instead of a clean primary win. Shouldn't trade like a clean pivotal-data story.

—

Basket math:

Longs: CADL 55%, SRPT 40%, NMRA 25% EV, LXRX 25%

Shorts: FLNA 35%, QURE 25-30%, GALT 20-25%

Equal-weight L/S basket:

3mo: 12% | 6mo: 23% | 12mo: 32%

—

The whole bet:

Long the names where 2026 catalysts are underpriced. Short the names where the story trades cleaner than the evidence.

Biggest risks: NMRA data fail, QURE gets a friendly FDA path, SRPT safety overhang worsens.

5

1

23

3,740

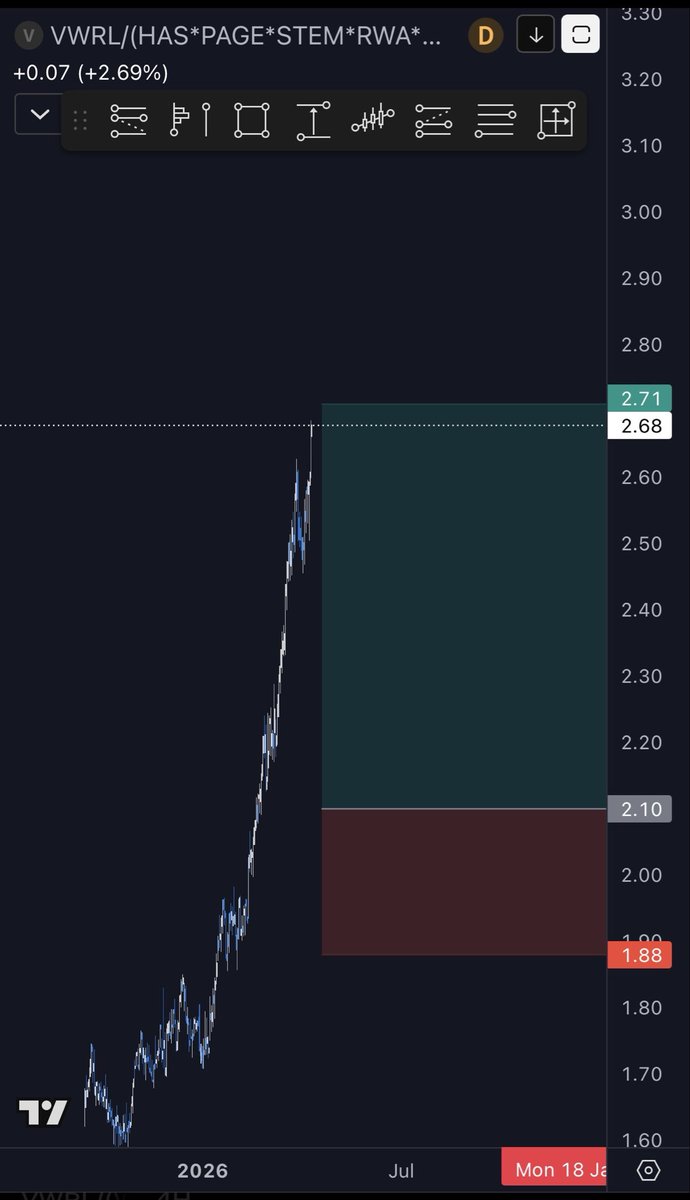

Hit my target on my first stock basket trade.

Short thesis: large EU companies selling services AI agents can easily replace. They can’t pivot. Restructuring costs are massive and internal politics won’t allow it. Hedged with VWRL long.

There’s maybe a 1-year edge here before institutional capital floods every niche AI play.

Want to build a small war room GC around this. DM me if you’re running similar setups.

@orrdavid curious if this overlaps with anything you’re doing atm.

1

12

924

Tur retweeted

Jan 9

When your portfolio manager calls your stock idea stupid, but ChatGPT would have said “you are not just spotting patterns, you are anticipating outcomes”

138

1,196

30,419

557,619

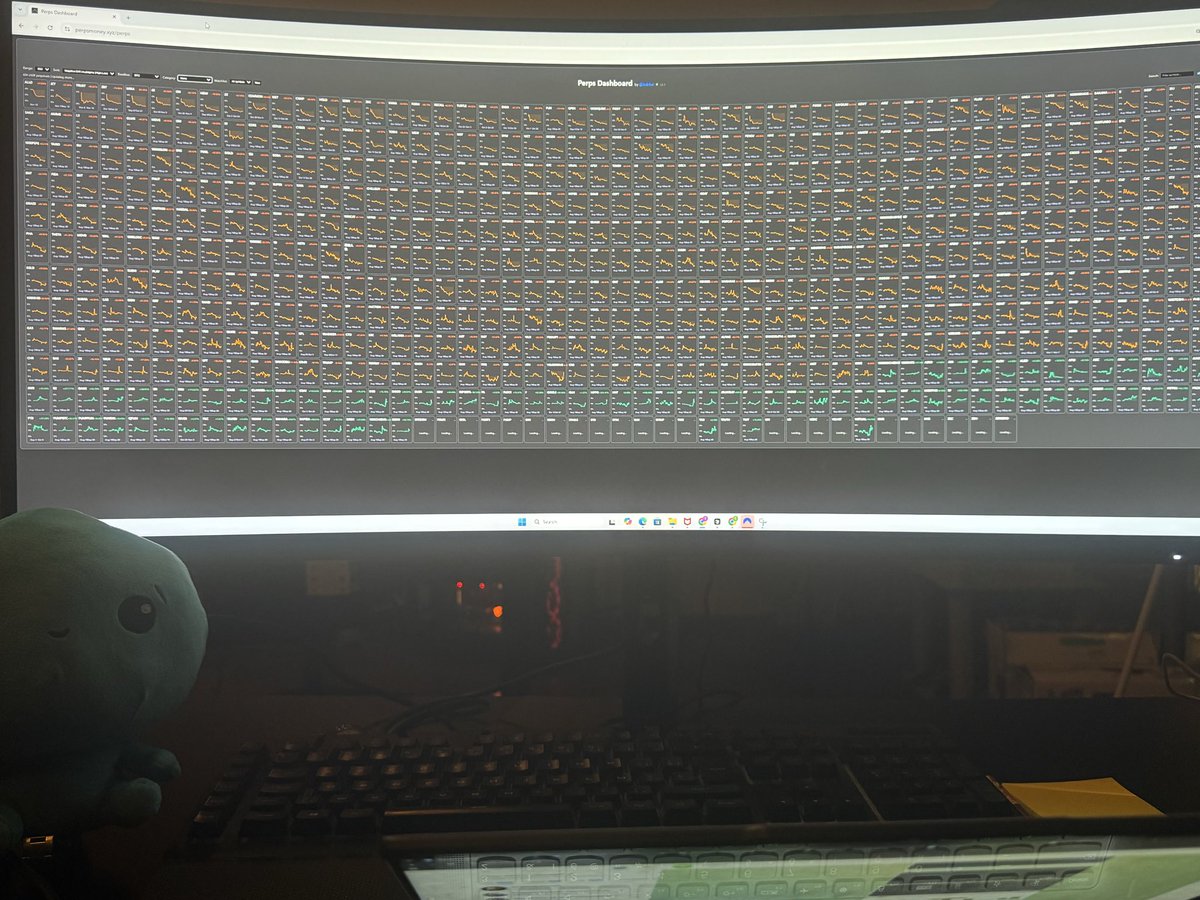

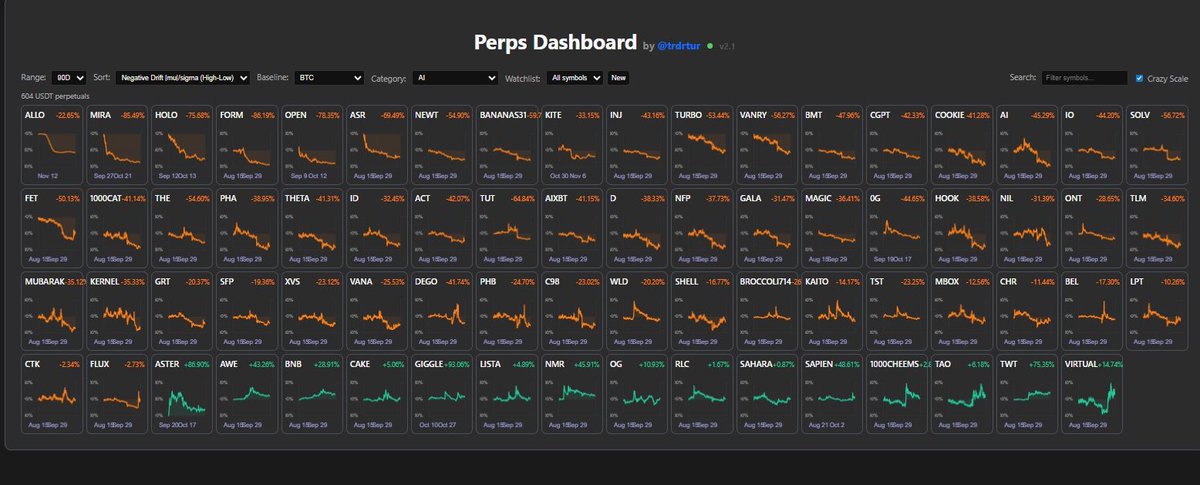

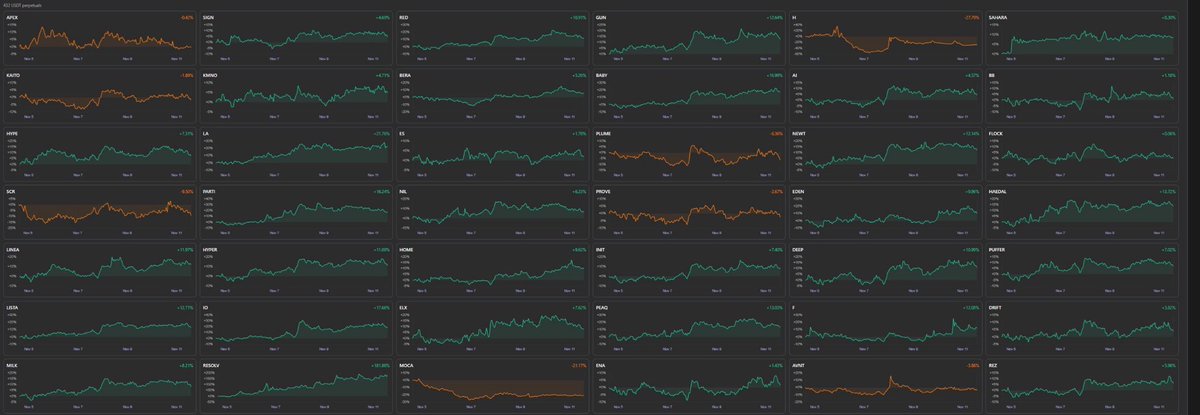

This is exactly what perpsmoney.xyz/ was made for

3

1

12

1,600