161 Photos and videos

May 20

Since late last year, I’ve been working on a project related to agentic commerce. Today I’m excited to share a little bit more about that initiative and why I think it’s more timely and important than ever that we build better infrastructure for machines to move money.

In short, it’s obvious that we’re entering the “age of autonomy.” Smart machines are learning how to perform important tasks on behalf of humans and each other. But the tools available for these machines to make and accept payments today are no better than blunt rocks and clubs.

If we ever want machines to be able to conduct commerce at scale, then we need totally new financial primitives that are faster, more streamlined, simpler, and more robust than anything available today.

Final (@usefinal) is the new company I’ve formed to gather this work together. Part think tank, part factory, Final is a design workshop that’s building the new infrastructure for machines to move money.

For the last 8 years, our team at Flexa (@FlexaHQ) has been building onchain payments infrastructure for enterprise. Many of you are aware that Flexa today is the most licensed crypto payments provider in the US—and that’s with even more rails and corridors under active development.

I’m not leaving Flexa anytime soon. For all the reasons listed above, I expect Flexa to play a critical role in helping to deploy the new technology that Final is building. And if anything, I am hoping this initiative will enable Flexa to be even more intrinsic to helping crypto payments go mainstream—because at this point, I’m fully convinced that the rise of agentic commerce will come to be known as the biggest inflection point in crypto payments adoption, period.

I’ve posted some notes on how Final is approaching agentic commerce over at final.net. As the next few months unfold, I sincerely hope you’ll follow along to learn more about why we think a fresh perspective is warranted, and how equipping smart machines with better financial tools can benefit us all. More to come!

61

41

173

15,080

Jan 30

End of an era! Good-bye, old friedn... You will be missed.

📣 Important update: SPEDN is shutting down on March 31. 📣

For almost seven years, SPEDN has shown the world how easy it is to spend digital assets with Flexa. Today, with more and more businesses using Flexa to accept payments from any app, and with faster self-custody payments in apps like @baseapp, it’s time to say good-bye to SPEDN.

16

16

164

10,607

Jan 30

All joking aside, I’m so excited about the room this clears on our plates for what’s next... 😎

28

33

178

14,104

Trevor Filter retweeted

26 Dec 2025

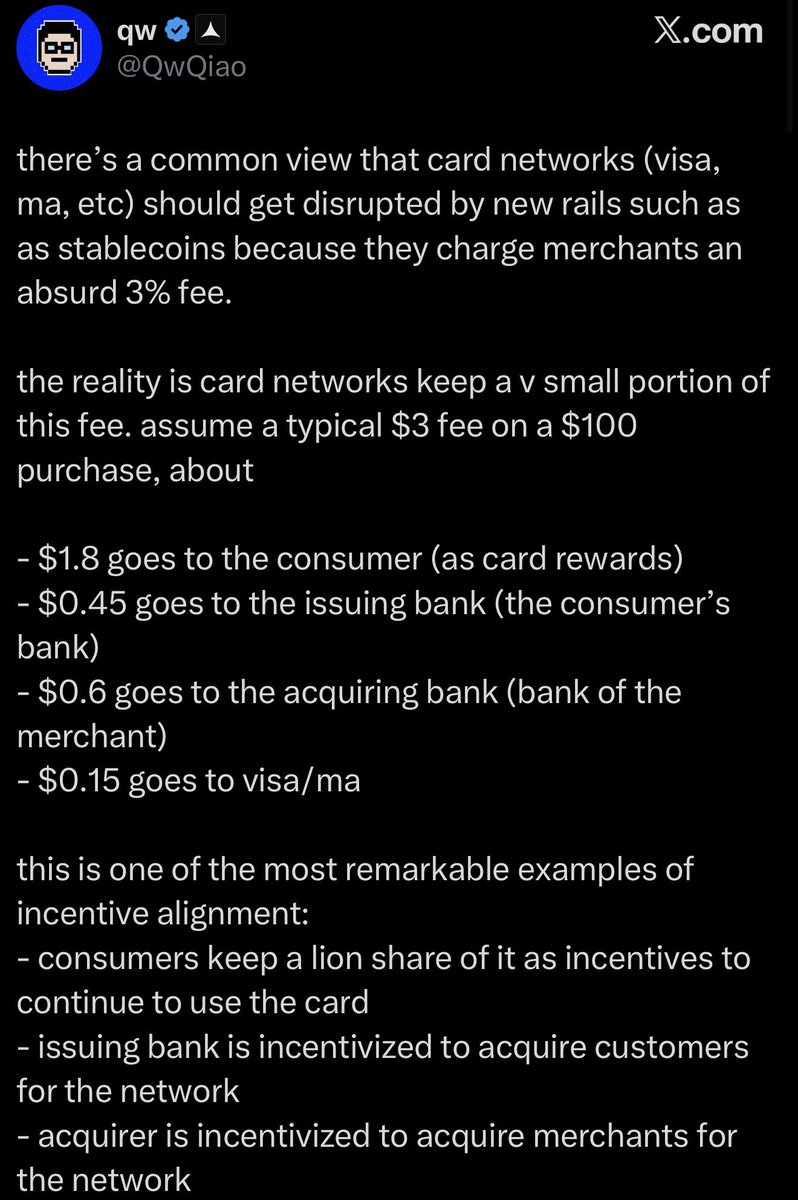

This is factually incorrect. In practice, rewards don’t come from card networks being generous. They’re funded in three main ways:

> Merchants fund a large part of rewards

Many rewards are effectively merchant-paid. Merchants agree to higher fees or marketing programs to boost sales, visibility, or conversion. When I was at Amex, we used to run these programs where, merchants routinely paid to run offers and reward boosts because cards drive demand.

> Consumer leakage pays for power users

A lot of cardholders don’t optimize:

- they pay annual fees

- they revolve balances and pay interest

- they don’t redeem points efficiently

That money subsidizes the rewards for people who use cards “well.” If everyone maximized rewards, the system wouldn’t work.

> Interchange is recycled to lock in the network: Visa, Mastercard, etc collect interchange and then give parts of it back as incentives to issuers and acquirers to onboard users and merchants. This isn’t neutral alignment, it’s strategic redistribution to keep the network dominant.

Cards are an incredible network effect, but not because incentives are fairly aligned.

They work because merchants have the least bargaining power, consumers are financially inefficient, banks monetize credit and float, and networks sit in the middle at near-zero marginal cost.

73

30

373

32,918

Trevor Filter retweeted

19 Nov 2025

Start accepting crypto payments with @FlexaHQ.

Instant authorization across 99 assets, fraud-proof settlement with zero chargebacks, compliant rails, and flexible payouts.

Low-code or no-code. Built for builders who want to ship fast.

18

98

297

27,886

19 Nov 2025

Get in, Marty. We’re reinventing crypto payments (again). flexa.co/terminal

32

85

312

21,179

19 Nov 2025

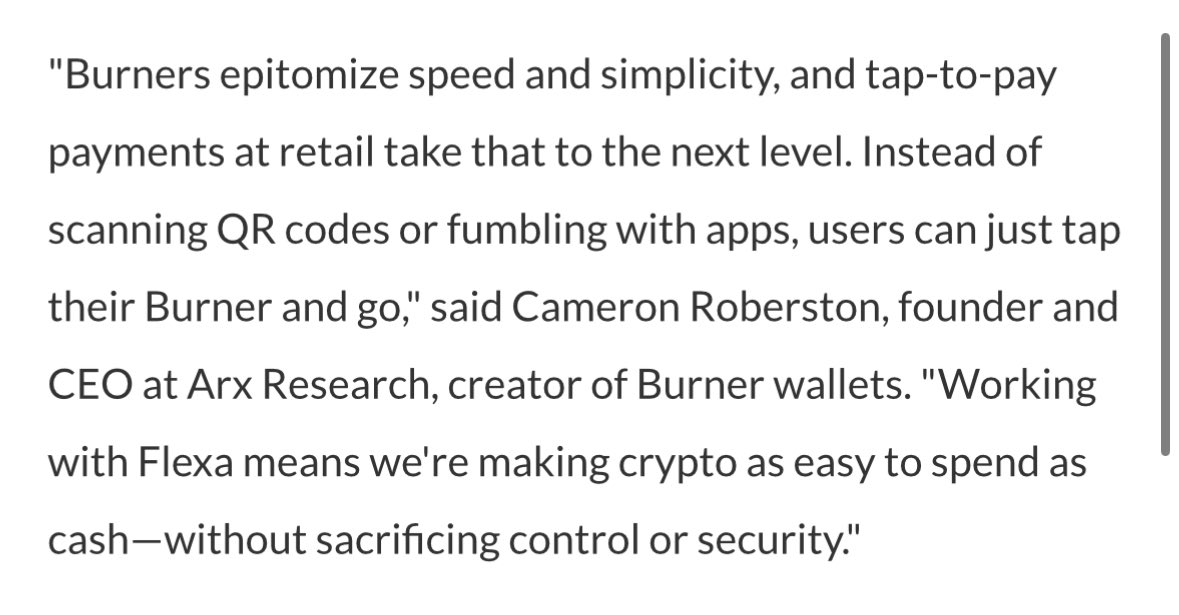

We’ve been working with @useburner to bring a totally new point-of-sale form factor to life for digital asset payments. Flexa Terminal is the answer to crypto and stablecoin acceptance that small businesses have been looking for.

9

20

152

3,116

19 Nov 2025

It must go without saying at this point, but it’s always such a privilege and a pleasure to push the crypto payments envelope with @ccamrobertson, @digit & the entire Burner team! 🙌🙌🙌

3

7

111

2,255

Trevor Filter retweeted

23 Oct 2025

A few things have changed in Zcash since Jan 2024:

- @zashi_app, launched world-class UX for ZEC

- @ShieldedLabs, new team of core contributors

- integration with @FlexaHQ for retail payments

- 2nd Zcash halving

- fundamental gov change (no ECC/ZF control)

- no direct dev fund (all grants based)

- the community has grown massively w/ fresh voices

- shielded hardware w/ @KeystoneWallet

- @near_intents w/ Zashi integration for swaps

- @Maya_Protocol DEX support

- @ebfull driving Tachyon to deliver scale

- wrapped ZEC on @solana

- Perps on @HyperliquidX and @rhea_finance

- 4X shielded pool growth

- 9X shielded tx growth (tz, zt, zz 30dma)

What'd I miss?

82

149

687

136,995

Trevor Filter retweeted

24 Oct 2025

Buy @ChipotleTweets with @base pay in under 10 seconds

- Mobile-first with the @baseapp

- Pay right from the @FlexaHQ mini app

- Near-instant confirmations

- Zero fees on Base

Everyday payments are finally onchain

22 Oct 2025

Hey @jessepollak a friend of mine told me you wanted to bring @ChipotleTweets onchain

Well thanks to @FlexaHQ you can make it happen in the @baseapp

28

47

208

16,273

20 Oct 2025

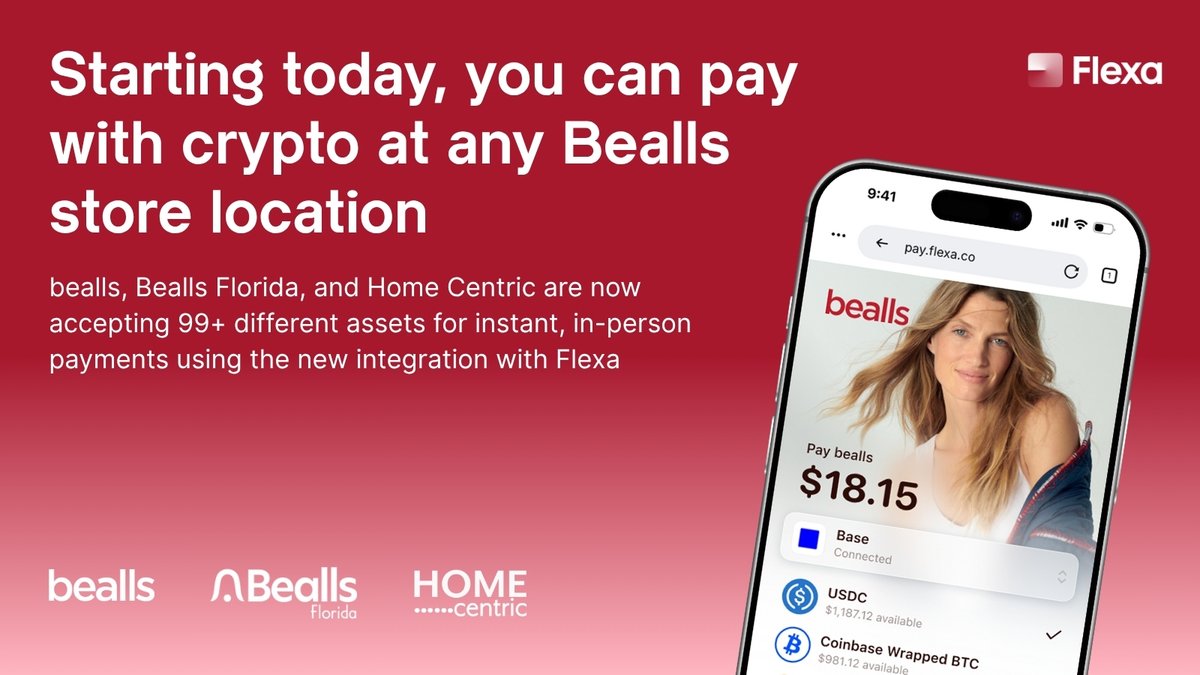

Bealls is celebrating their 110th anniversary this year—it’s incredible that such a storied retailer would be among the first to adopt in-person crypto payments!

Flexa is very proud to partner with @MBeallX and team in bringing this experience to life across the entire Bealls, Inc. footprint.

Starting today, you can spend your USDC, bitcoin, ether, and more at any any @beallsinc, @BeallsFL, or @shophomecentric location—with instant digital asset payments across more than a dozen blockchains powered by Flexa.

Read more: flexa.co/newsroom/bealls

21

58

239

14,058

Trevor Filter retweeted

16 Oct 2025

We worked with @FlexaHQ to enable USDC checkout via @base pay at more places you love

@baseapp users can now spend their USDC earnings at @ChipotleTweets, @BNBuzz, or @RegalMovies through their mini apps

From burritos to books to movie tickets, pay straight from the Base app

Now available: faster, more seamless USDC checkout with Base Pay.

Flexa and @base are teaming up to make it easy for any merchant to accept digital asset payments with the fastest onchain checkout experience for USDC.

No wallets to manage, no risk of fraud, no added complexity. Base Pay is now a default payment option in every Flexa Payments experience—from QR codes to mini apps, payment links, and more.

Now you can accept USDC with Base Pay and receive payouts in any currency of your choice—all with integrated and automated reconciliation and settlement.

It’s yet another step toward fast, secure, and accessible digital payments for merchants everywhere. Only at flexa.co/base-pay.

30

73

278

19,329

16 Oct 2025

🟦 Base Pay is an n-of-1 checkout experience in crypto—there’s really nothing else like it.

So, when the @base team asked us how we could get this UX live for @FlexaHQ merchants in the most seamless and easy-to-integrate way possible, we jumped at the challenge.

It’s been an incredible collaboration these last few months, and I’m so excited to share that as of today, Base Pay is now default-on for all Flexa Payments integrations—including Mini App Payments, online checkout, and in-person payments with Flexa QR Codes.

Major thanks to @jessepollak, @davidtsocy, @WilsonCusack, and the entire Base team for the continued partnership! LFB!

Now available: faster, more seamless USDC checkout with Base Pay.

Flexa and @base are teaming up to make it easy for any merchant to accept digital asset payments with the fastest onchain checkout experience for USDC.

No wallets to manage, no risk of fraud, no added complexity. Base Pay is now a default payment option in every Flexa Payments experience—from QR codes to mini apps, payment links, and more.

Now you can accept USDC with Base Pay and receive payouts in any currency of your choice—all with integrated and automated reconciliation and settlement.

It’s yet another step toward fast, secure, and accessible digital payments for merchants everywhere. Only at flexa.co/base-pay.

41

129

400

51,713

Trevor Filter retweeted

17 Jun 2025

The GENIUS Act has passed the Senate.

609

2,122

16,053

1,403,546

Trevor Filter retweeted

27 Feb 2025

My finance degree is proud today after snagging a quote in @AmerBanker

27 Feb 2025

Really enjoyed speaking with Emma Kinery at @AmerBanker about Flexa Tap to Pay, and how we’re continuously pushing the boundaries of crypto payments to make them more powerful, accessible and affordable than ever! americanbanker.com/news/excl…

1

16

109

10,567