Joined July 2024

- Tweets 789

- Following 42

- Followers 2,436

- Likes 797

176 Photos and videos

Valueverse retweeted

Jun 12

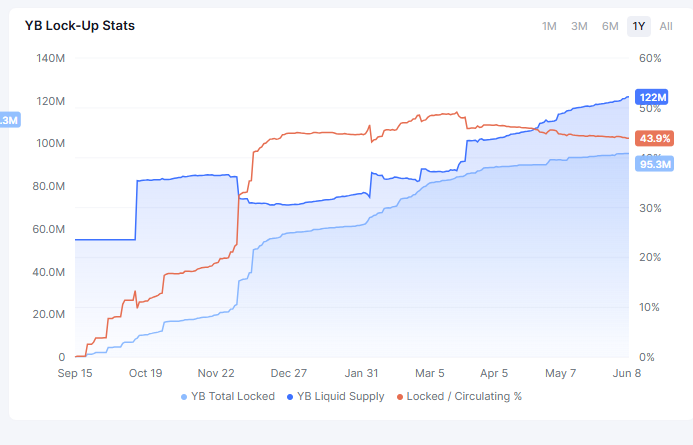

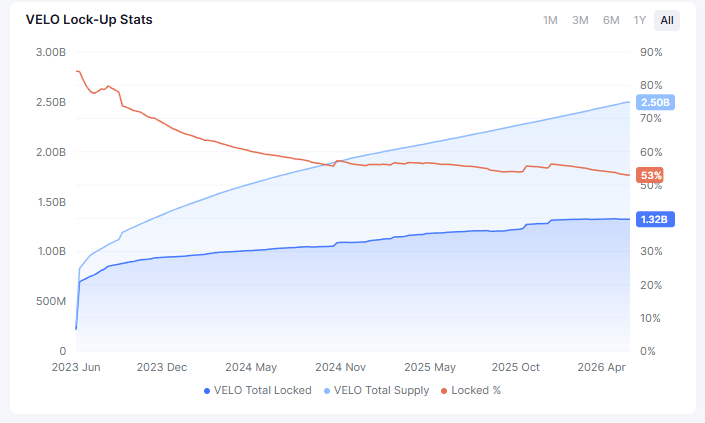

Will the bull run bring back veToken lockers?

@CurveFinance pioneered the model: lock tokens for up to 4 years in exchange for boosted yields and governance rights.

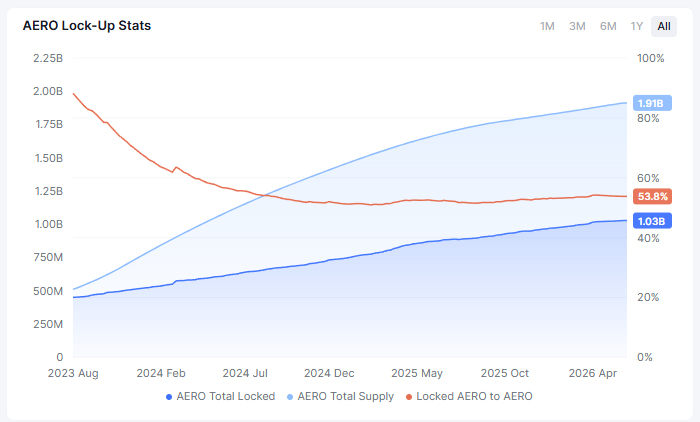

According to data from @valueverse_ai, the percentage of tokens locked has steadily declined.

@AerodromeFi and @VelodromeFi look healthier for now, with higher lock rates. @yieldbasis is the newest entrant, already sitting at around 40% locked, but it's starting to show the same trend.

The challenge is simple: investment funds rarely lock their tokens, and I'm not convinced retail participants from the next cycle will return with the same conviction.

Most veToken models reduce emissions over time, which slows the dilution but doesn't solve the issue.

I like these protocols, but I still struggle to model how they remain healthy over a 10-year horizon.

Jun 9

Will crypto ever value DeFi on cash flows?

I've been digging through @valueverse_ai data recently, and two metrics changed how I look at DeFi valuations.

> The first is Effective Market Cap.

Many DeFi tokens have emission schedules that dilute supply for years. Comparing revenue to FDV often tells you very little. A more useful approach is comparing revenue to the tokens actually circulating and locked in the market today.

> The second is FCFM.

It compares recent revenue to annualized revenue, helping distinguish between sustainable cash flows and short-term spikes.

A good example is @yieldbasis.

Recent volatility caused fees to surge, with a large portion of its annualized revenue generated in just a few days.

Then you have @VelodromeFi and @AerodromeFi.

Their revenue is far less exciting on a week-to-week basis, but it's remarkably consistent. I own some VELO because I find that type of predictability valuable.

However, what's most surprising is how little the market seems to care. Crypto still prices assets based on narratives, momentum, and liquidity cycles.

Meanwhile, some protocols are generating recurring cash flows while trading at valuations that would look absurdly cheap in traditional markets.

At some point, fundamentals have to matter.

8

4

39

5,009

Valueverse retweeted

Jun 11

Correct metric: Effective market cap/annualized token revenue.

It's P/FCF adjusted for eligibility. Available at app.valueverse.ai

Effective m.cap means only tokens that actually capture revenue (e.g. in ve-tokenomics only locked tokens count).

Jun 11

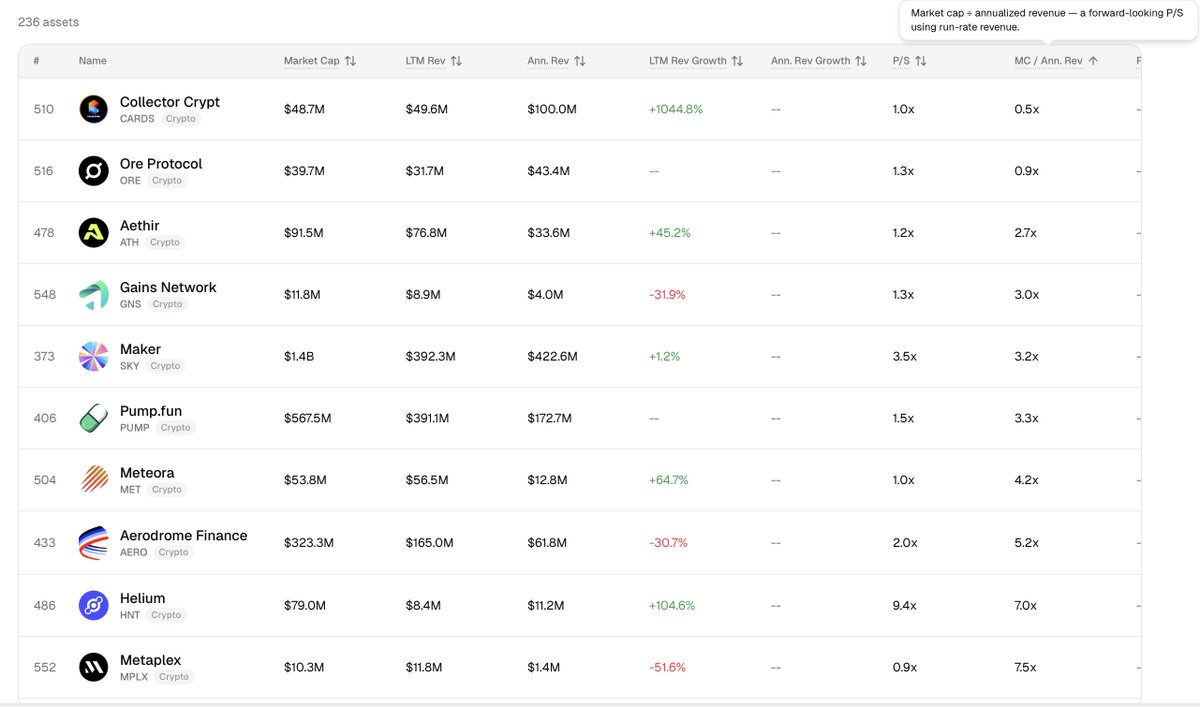

There's a metric I use to find undervalued assets on the market.

It's MC/ANN rev (market cap/annualized revenue).

The ratio compares how much the market values an asset vs. the revenue the protocol is currently generating.

Protocol revenue doesn't determine token value on its own, but a lower ratio can suggest an asset is cheap relative to what it earns.

I decided to see if that holds.

Already bought $1,000 each of the assets below, and I will personally test their price performance over the coming weeks.

Stay tuned.

1

6

452

Jun 9

Data Sources:

- $ABX: dune.com/aboreanfinance/abor…

- $NEST: app.usenest.xyz/analytics

- $DRV: app.derive.xyz/stats

1

1

417

Jun 9

1

156

Valueverse retweeted

Jun 9

Will crypto ever value DeFi on cash flows?

I've been digging through @valueverse_ai data recently, and two metrics changed how I look at DeFi valuations.

> The first is Effective Market Cap.

Many DeFi tokens have emission schedules that dilute supply for years. Comparing revenue to FDV often tells you very little. A more useful approach is comparing revenue to the tokens actually circulating and locked in the market today.

> The second is FCFM.

It compares recent revenue to annualized revenue, helping distinguish between sustainable cash flows and short-term spikes.

A good example is @yieldbasis.

Recent volatility caused fees to surge, with a large portion of its annualized revenue generated in just a few days.

Then you have @VelodromeFi and @AerodromeFi.

Their revenue is far less exciting on a week-to-week basis, but it's remarkably consistent. I own some VELO because I find that type of predictability valuable.

However, what's most surprising is how little the market seems to care. Crypto still prices assets based on narratives, momentum, and liquidity cycles.

Meanwhile, some protocols are generating recurring cash flows while trading at valuations that would look absurdly cheap in traditional markets.

At some point, fundamentals have to matter.

9

9

58

9,071

Jun 6

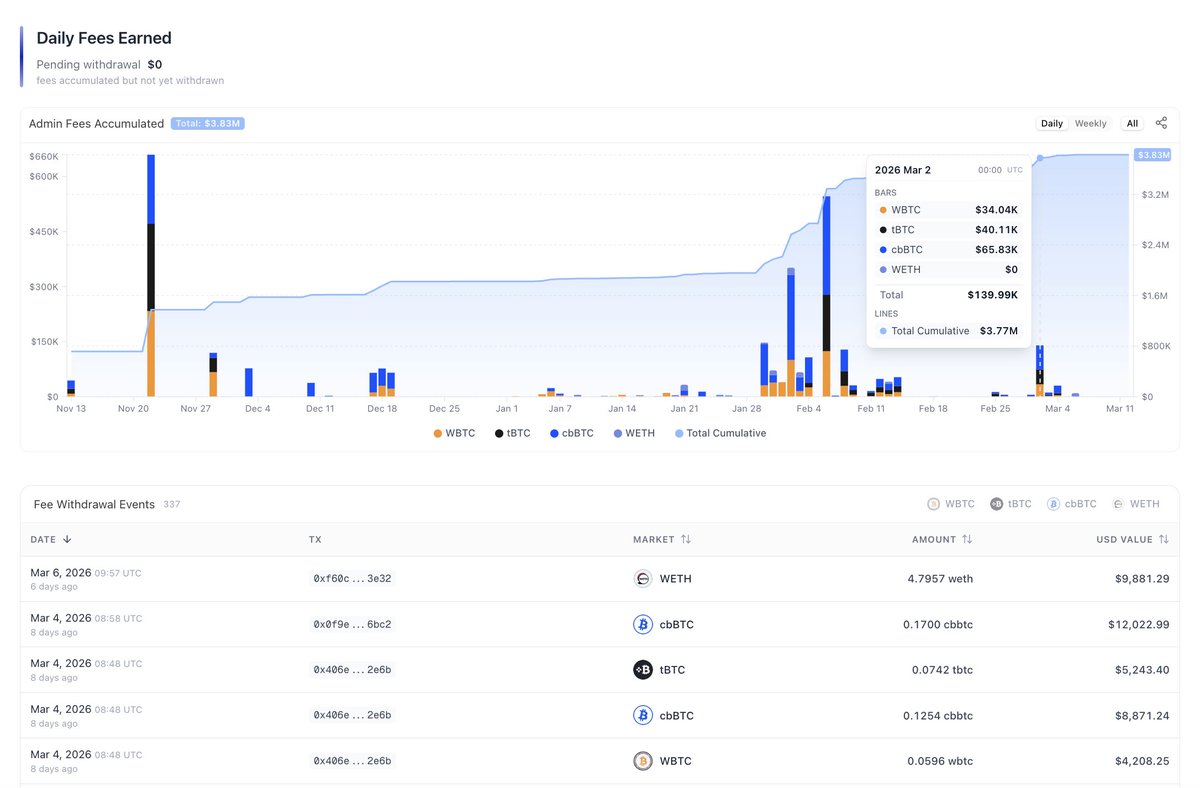

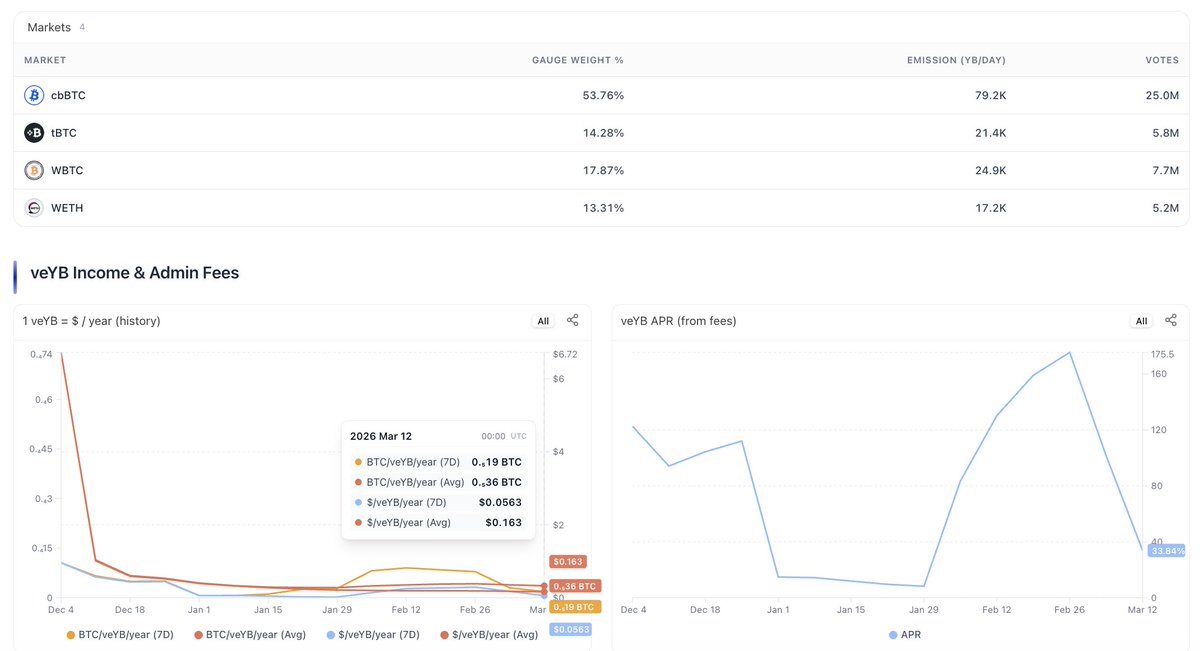

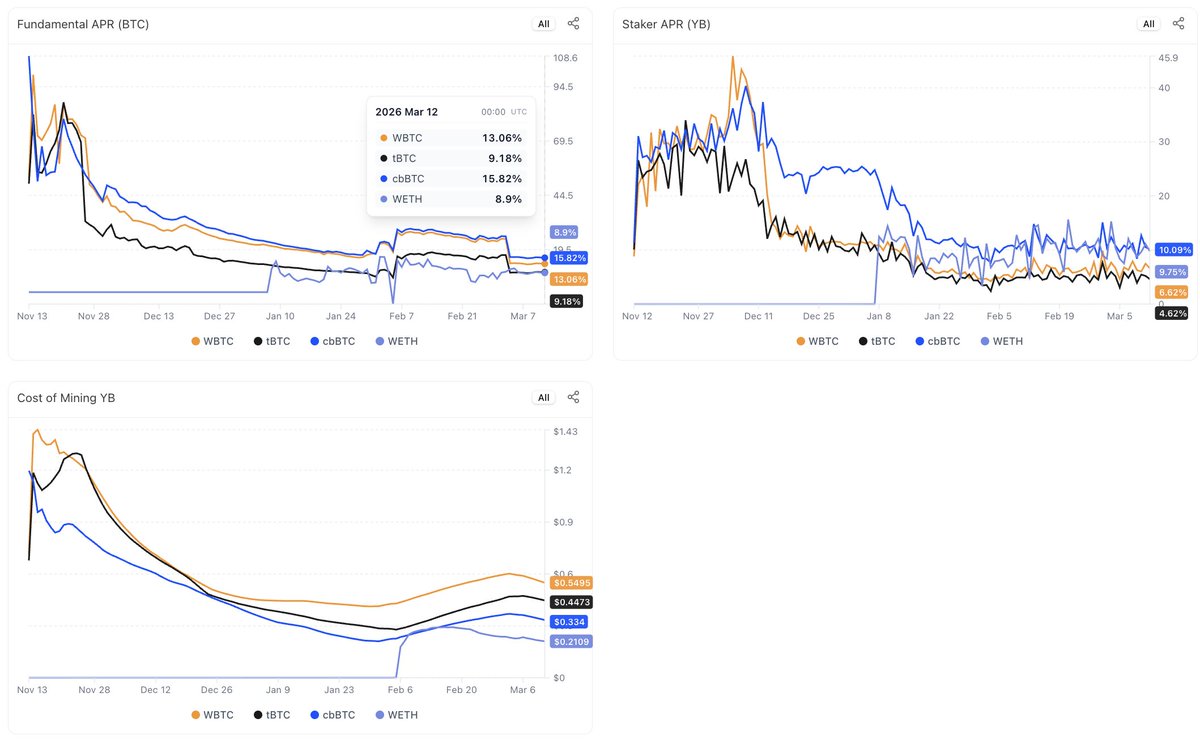

V3 pools and all other stats for $YB @yieldbasis were updated a while ago

v2->v3 transition live

1

2

4

767

Jun 6

371

Valueverse retweeted

Truly agree.

Programmable value accrual from transparent onchain business models is the future

And @valueverse_ai is independent analytical tool to track that

Tokens are better than stocks

Every step of the way, even raising funding is more streamlined and transparent

Our space was just filled with scammers who pretended to be good actors by using our good faith tools

But if genuine people used these tools to build real companies it would be an unlock in a lot of ways... As collateral, borrowing, liquidations, getting liquidity, seeing revenues, accounting, etc.

Thankfully we have hyperliquid - the golden star that proved this

In the coming year, a few more projects will shine through and we can stop being a blackpilled gambling scammer crime fuelled branded industry

Because in the last few years everyone that got attracted was dumped on with valueless not even governance tokens

So whats gonna bring them back when the stock market is the new casino with better “investor protections”?

More hyperliquids

Strap in, prove you're not a scammer, and be rewarded with the cleanest financial instrument in history: tokenization

1

4

565

Jun 4

Token fundamentals have a particular valuation.

It’s revenue multiplier, accounting only token holders’ revenue.

app.valueverse.ai

1

3

293

May 29

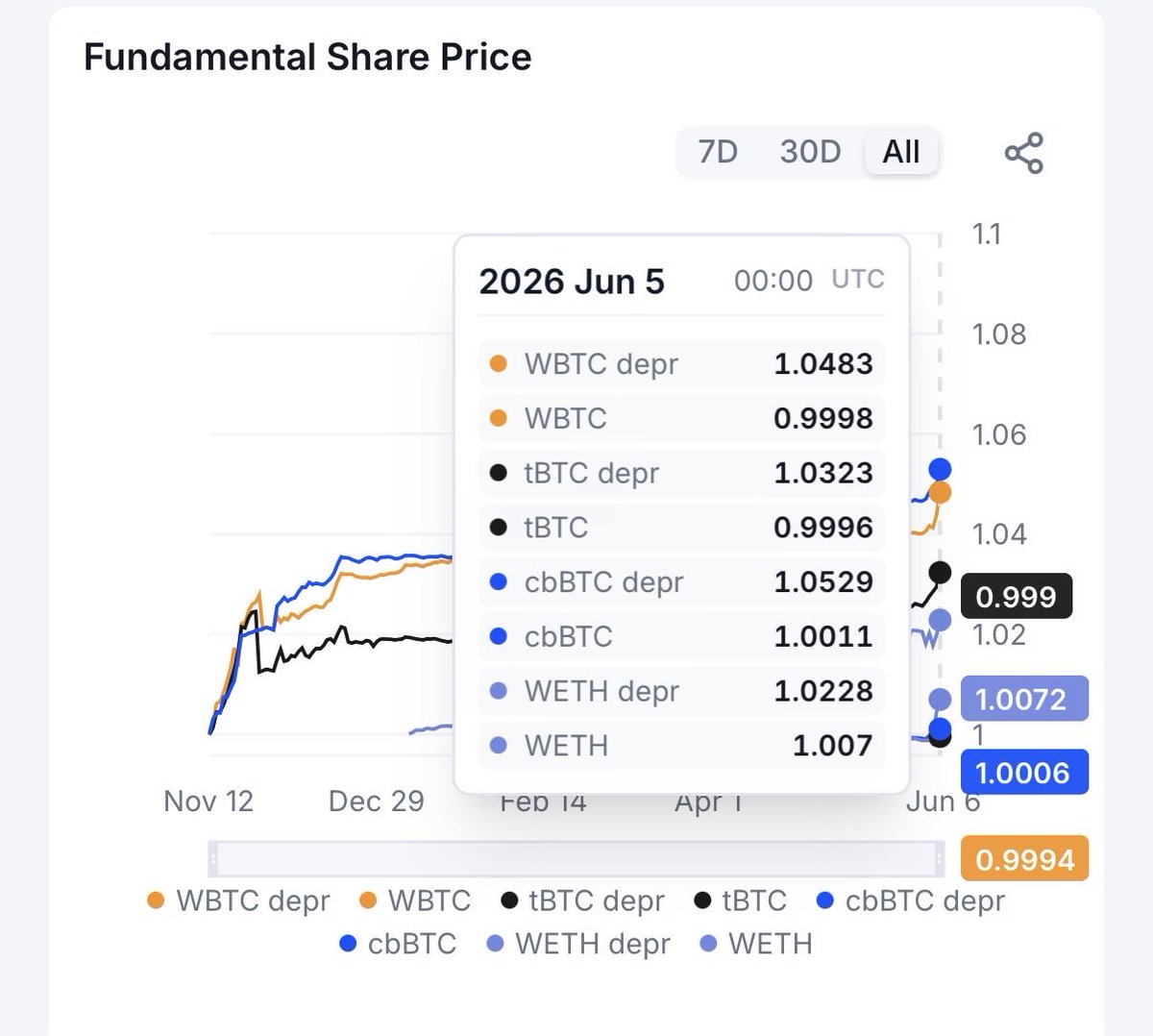

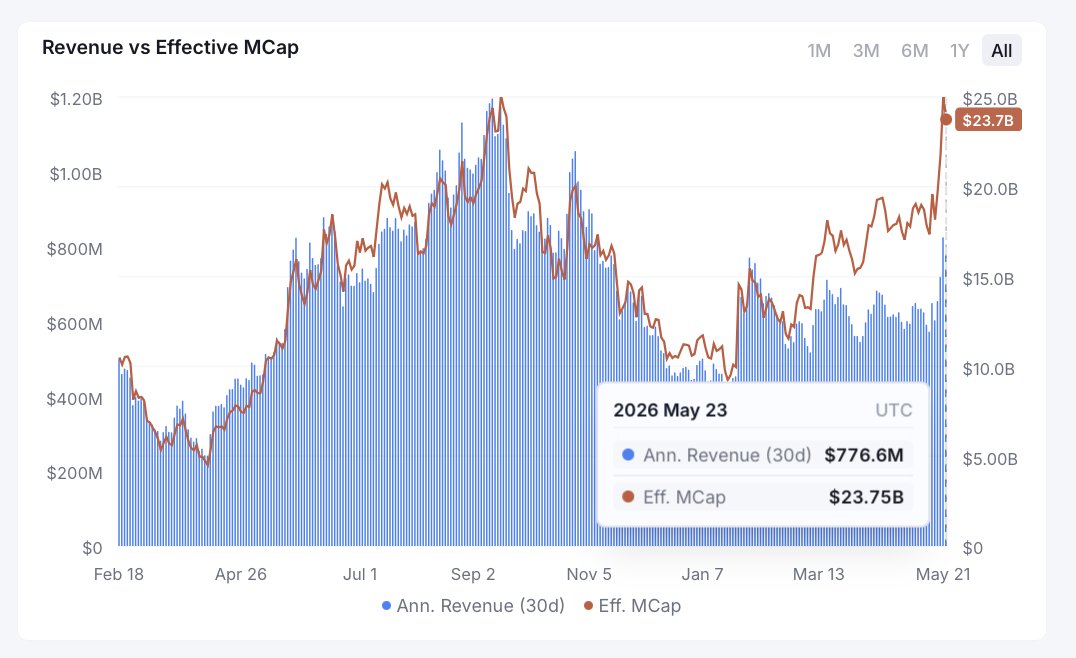

We count $HYPE M.Cap as ~$23.7B (effective)

Effective M.Cap = Total Supply - Future Emissions

We account staked team tokens in Effective Cap since they are economically active.

Revenue streams for $HYPE holders:

- $HYPE Buybacks

- $HYPE staking income (emissions)

- HyperEVM/HyperCore $HYPE burn

DeFi Monk explains why Hyperliquid shouldn’t be valued using FDV

“Right now we think it should probably be somewhere in between, if not closer to circulating”

“That’s a massive shift in the story if all of a sudden Hyperliquid is not worth like $60B. I’ve had a background in equities before and there is no such thing as an FDV for the average stock”

“No one ever sits down and goes what is the maximum amount of shares Nvidia could ever issue over the entire history of the stock. I think now that we’re introducing HYPE to this more traditional investor, we kind of need to speak on their terms”

“The reality is the 40% or so of supply allocated for future incentives, I just don’t think that makes sense to be including in any sort of real market cap discussion”

“One, we have no idea when and if that supply will ever come online and two, if it does, I think there’s a real chance Jeff and the team decide to use it in an accretive way where let’s say a dollar worth of HYPE incentives generates a dollar or more of HYPE buybacks”

“So what is inflation really? It’s probably just staking rewards and team unlocks. That’s basically what investors should be focusing on”

1

4

262

May 25

Institutional capital is allocating to digital assets at scale.

The data layer beneath those allocations is built on assumptions borrowed from the wrong asset class.

🧵

1

2

4

380

May 25

ACCRUAL represents a standard for that layer..

- human-verified holder cashflow, isolated from protocol revenue

- independent research focused on value accrual mechanisms & stats

- proprietary calculated data

- expressed as Holder P/FCF, Cashflow Yield, FCF Momentum, Yield-to-Vol

TradFi-legible. Designed to add revenue fundamentals to a scope of an IC meeting.

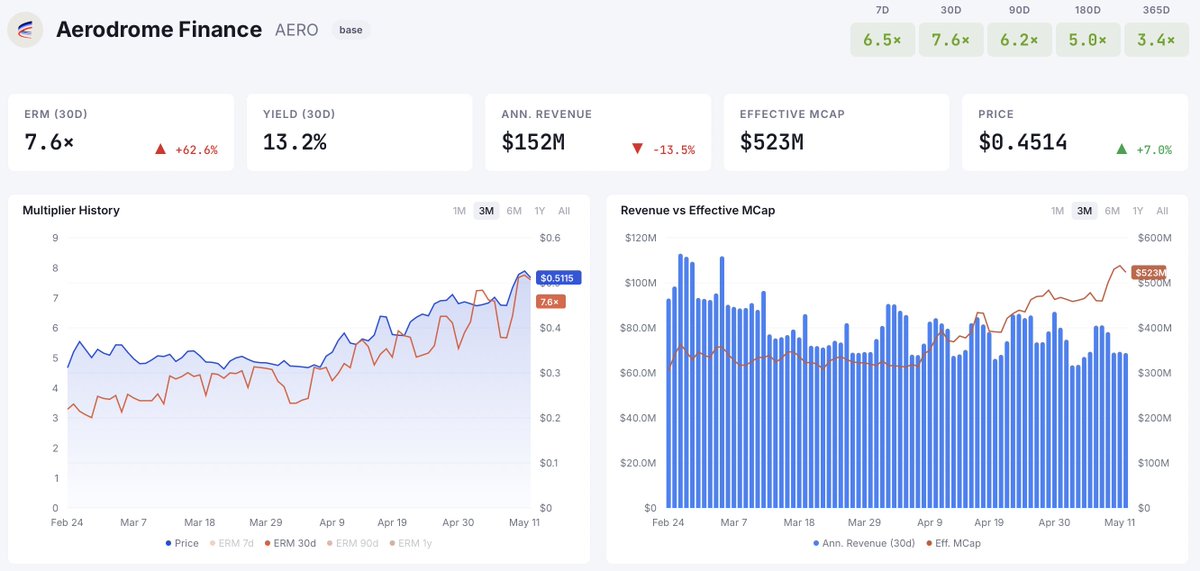

ALT $AERO multiplier history & effective MCap

1

1

188

May 24

Token Revenue Matters

Welcome to the "Selective Altseason"

Token revenue and multipliers: one of the clearest ways to identify fundamentally strong tokens early.

-> $RAIL @RAILGUN_Project $WALLET @ambire

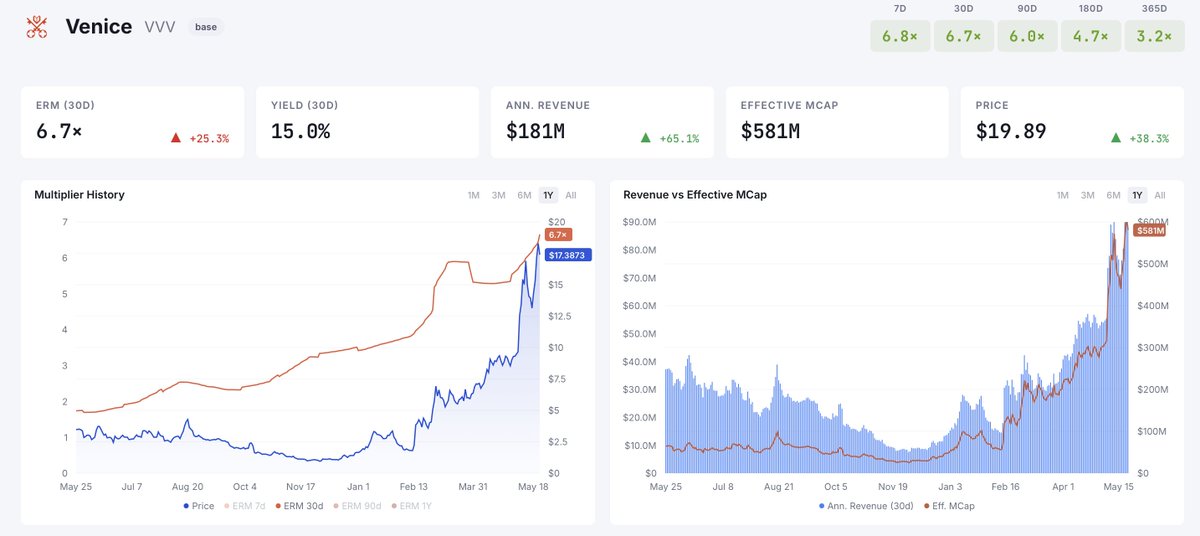

-> $VVV @venice_ai $POD @dphnAI

-> $NEAR @NEARProtocol

-> $HYPE & some HyperEVM's projects such as @Kinetiq_xyz $KNTQ, @NestExchange & $NEST

(all of them many others are on the Valueverse's listing track).

You need not surface-level “good to know” data, but investable data that drives actual allocation decisions.

Great time to be in crypto. Early access -> link in comment👇

1

1

14

2,306

May 22

There are much more protocols doing that, ~80

May 21

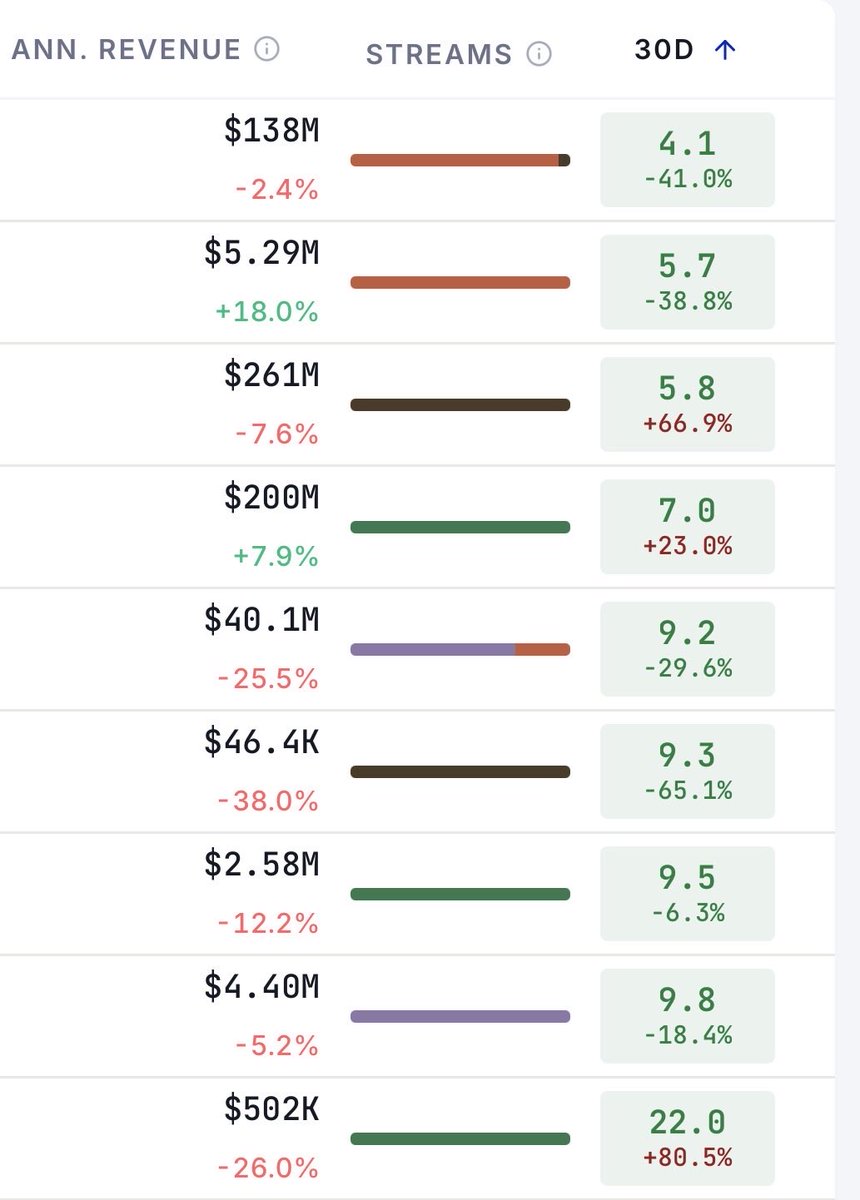

Only 17 protocols paid their token holders last month.

Here they are, ranked by holder revenue:

1. @HyperliquidX: $50.8M

2. @edgeX_exchange: $22.0M

3. @Pumpfun: $20.4M

4. @chainlink: $4.5M

5. @AerodromeFi: $3.8M

6. @Uniswap: $3.2M

7. @OREsupply: $2.4M

8. @PancakeSwap: $2.2M

9. @lighter_xyz: $2.1M

10. @JupiterExchange: $2.0M

11. @helium: $1.4M

12. @THORChain: $1.4M

13. @SkyEcosystem: $1.1M

14. @Raydium : $866K

15. @GEODNET : $700K

16. @pendle_fi: $625K

17. @gmx: $550K

Out of over 1400 protocols, only 1.3% of the industry actually pays you.

3

415

May 21

Cannot wait to add v3 pools to yb.valueverse.ai

The most detailed independent data source for @yieldbasis protocol

1

4

501