Growth stock investor/blogger - Not advice

Joined April 2021

- Tweets 1,384

- Following 120

- Followers 7,800

- Likes 3,368

60 Photos and videos

May 28

Feels like the markets are screaming at us to start trimming our stratospheric holdings… and yet. I have not

2

13

1,173

2025 Portfolio: 33%

Cumulative Performance since 1/1/2020: 250%

Holdings:

APP 30%

IREN 10%

NBIS 10%

NVDA 9%

ALAB 9%

AXON 7%

MELI 6%

RDDT 5%

RBRK 4%

CRDO 4%

<= 3% : CASH, WYFI, CRWV, PGY, HIVE

2

24

2,555

exponentialdave retweeted

20 Nov 2025

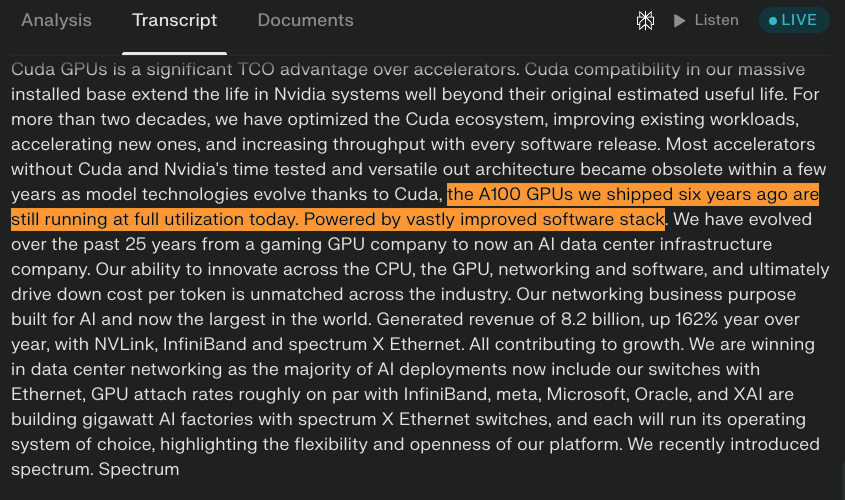

NVDA just told you the depreciation debate is irrelevant and nobody’s repricing.

Burry closed his fund after shorting NVDA, claiming companies overstate GPU useful life at 2-3 years. The market debates whether depreciation should be 3, 5, or 7 years. AWS just cut AI hardware depreciation from 6 years back to 5.

Then NVDA drops this in their earnings transcript: A100 GPUs shipped in May 2020 are still running at full utilization in November 2025, powered by vastly improved software.

That statement just invalidated the entire depreciation debate.

Here’s what people are getting wrong. They’re modeling GPU economics like traditional data center hardware with fixed depreciation curves. CoreWeave uses 6-year depreciation cycles. Microsoft and Alphabet extended server equipment to 6 years. Everyone’s arguing about the right number.

But NVDA just revealed the actual dynamic. The value isn’t depreciating on a fixed schedule. Software improvements are extending hardware utility faster than the hardware ages. CUDA optimizations, framework updates, and model efficiency gains mean a 2020 chip running 2025 software delivers more economic value than a 2020 chip running 2020 software.

Think about what “full utilization” means for data center economics. These aren’t spare chips sitting idle. They’re generating revenue at capacity 5.5 years after purchase. The software moat keeps expanding, which keeps old hardware economically viable.

This completely inverts the depreciation model everyone’s fighting about. The question isn’t “when does the hardware become obsolete?” The question is “how fast can software improvements extend hardware utility?”

A100 resale prices saw appreciation in early 2024 during H100 supply constraints, proving the market values backward compatibility and software leverage over raw specs.

The competitive dynamic here is brutal. NVDA controls the entire software stack. Every CUDA improvement, every framework optimization, every model efficiency gain extends the life of every GPU they’ve ever sold. Competitors need to match not just the current generation, but the accumulated value of 15 years of software development.

Burry bet on hardware obsolescence. NVDA just showed him software determines economic life, not silicon generations.

19 Nov 2025

$NVDA basically answering Burry:

“The A100s we shipped six years ago are still running at full utilization today, now powered by a much stronger software stack.”

50

60

452

86,170

7 Nov 2025

A little bit funny to see $IREN, one of my biggest holdings, DOWN today after reporting an absolute blockbuster earnings yesterday.

Says a lot about the state of the market right now, and not very much at all about Iren, who will be more than 10x'ing their revenue next year.

4

12

2,192

7 Nov 2025

I'm very aware of the stock price run up, and because this is Twitter, people will say "All that was already priced in".

But actually... all that was certainly not priced in. Who could have known that they're guiding for $3.4 billion of revenue next year?

1

2

1,243

7 Nov 2025

To take this a step further, $IREN is now down 9% and trading for LESS than it was *before* the microsoft deal! Talk about irrational markets... I have a huge Iren position already and I'm considering adding here, or converting some shares to options.

3

5

1,318

6 Nov 2025

Portfolio 56% YTD

Cumulative Performance since 1/1/2020: 312%

Holdings:

APP 24%

IREN 19%

NBIS 12%

NVDA 8%

AXON 7%

ALAB 7%

MELI 6%

RDDT 4%

<= 3% : WYFI, CRWV, PGY, CRDO, HIVE, RBRK

1

1

29

3,437

exponentialdave retweeted

3 Nov 2025

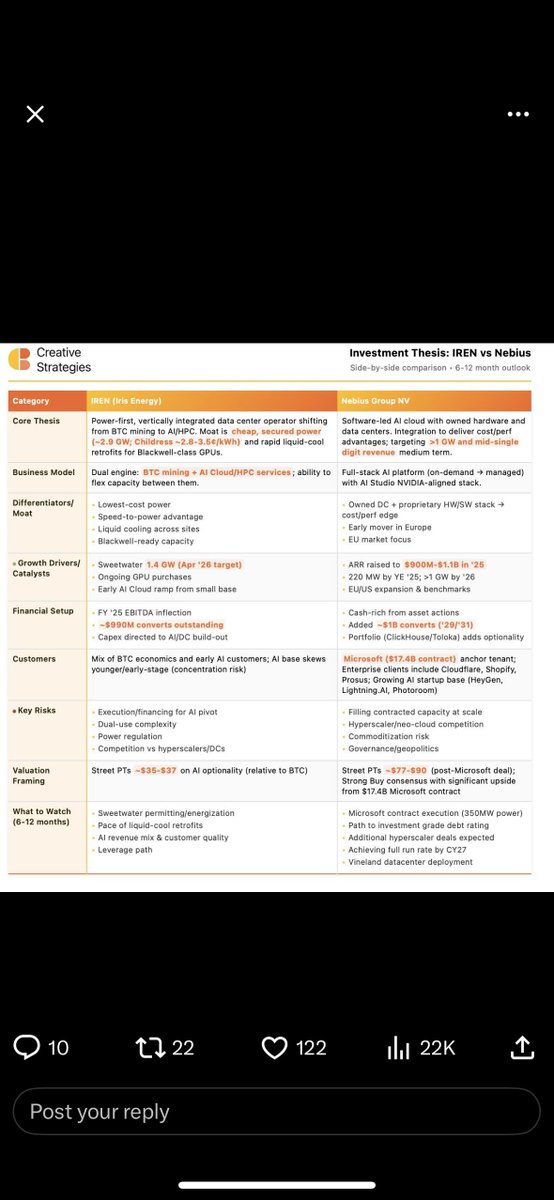

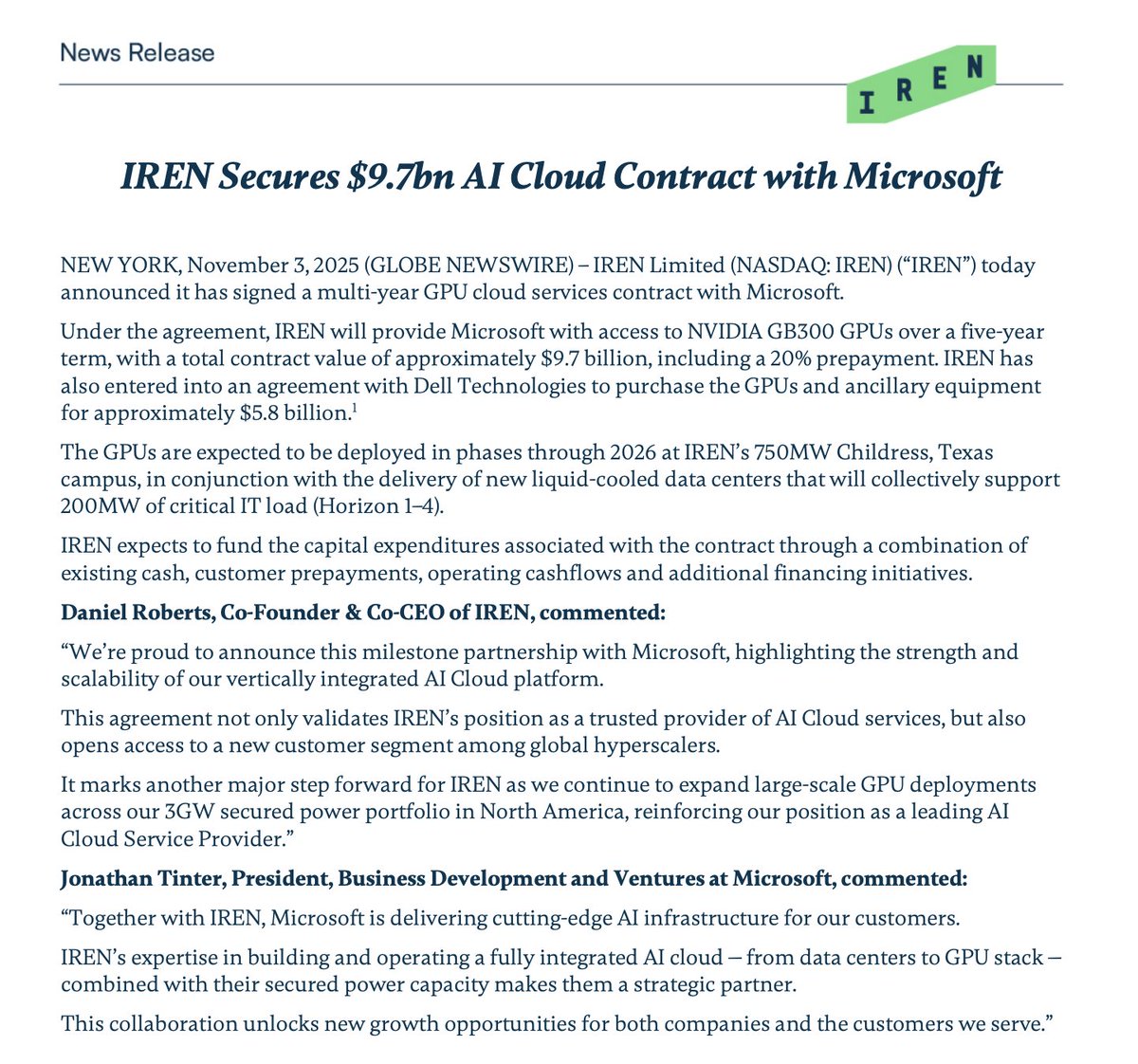

$IREN signing a $9.7b cloud contract with $MSFT is a thesis-defining moment for shareholders

For the last couple of years, doubters have argued that $IREN is just another $BTC miner or, in recent months, that they can’t compete with the likes of $NBIS or $CRWV because they lack "software orchestration".

Well, it turns out that all of these doubts were severely mis-guided.

Investors who did extensive research and analysis of the AI sector understood that it was always just a question of time — not merely because $IREN "has the power", but because they have world-class engineers and a one-of-a-kind CTO in Denis Skrinnikoff.

Combine that with excellent leadership at the top & this was a forgone conclusion.

Now keep in mind, this multibillion $ deal — which, on the surface, appears to have a very strong ROIC profile — barely encompasses 300 MW (gross) of $IREN's ~3 GW power portfolio.

There will be many more deals, whether in hyperscale cloud contracts or in the form of high-yielding “premium” colocation partnerships.

This is truly just the beginning...

Congrats @danroberts0101 & Team. Couldn’t be prouder as a shareholder today! 👏🎉

69

169

1,175

152,985

3 Nov 2025

Love when my tweets age well! $IREN 🚀 🚀

7 Sep 2025

I was wondering why some of my friends were buying stock in a bitcoin miner.

Then I saw its revenues are up 230% YoY in its most recent quarter. Ok, I'm interested, but it's still just a bitcoin miner.

If I wanted more BTC exposure, I'd just buy bitcoin.

8

2,954

14 Oct 2025

Portfolio 61% YTD

Cumulative Performance since 1/1/2020: 314%

APP 23%

IREN 15%

NBIS 14%

AXON 8%

ALAB 8%

NVDA 8%

MELI 5%

RDDT 4%

RBRK 4%

3% or less: WYFI, HIMS, CRWV, PGY, CRDO, HIVE

3

1

48

5,853

9 Oct 2025

I should give @GIMastery a finder’s fee for his work on $IREN.

Great job on that one!

1

20

1,859

6 Oct 2025

Adding in February at the beginning of the Applovin short report nonsense ended up being a great decision.

Similar theme today - probably a buying opportunity but at the end of the day no one really knows until the probe is complete

Long $APP

26 Feb 2025

$APP short reports are just making claims - no proof of anything (yet).

The company has already swiftly and forcefully pushed back against the claims.

I don't know everything - the claims could be true!

But for now, it's probably BS. I added to my already large position.

2

27

5,874

exponentialdave retweeted

20 Sep 2025

I think people forget how bad 2020/2021 was lol

$OKLO needs to 3-5x FROM HERE for it to be like 2021

2021 had 0 revenue companies like:

$LCID - $90B

$RVIN - $100B valuation during IPO(larger than ford at the time)

$NKLA - $30B ending up being a scam

$FSR (Fisker) - billions with 0 products

And that’s just a few names off the top of my head. Plenty of other.

THEN you had everyone and I mean everyone talking about stocks.

“What should I buy”

“How do I get rich”

Every friend I had was now an “options pro”.

THEN you had NFTs, selling for millions of dollars.

THEN you had $100Bs in Covid stimulus checks.

THEN you had FFR at near 0%.

This is NOT 2021. I’m not saying it’s not a local top but any comparison to 20/21’ is based on their own FOMO IMO.

32

19

215

37,342

21 Sep 2025

Lot of retail investors (myself included) posting their portfolios and high fives all around.

Is it a local top? Could be.

But is it actionable? For me.. no.

Macro is a highly uncertain endeavor. Even the smartest people typically get it v wrong.

So I'm staying the course.

6

1,281

21 Sep 2025

Portfolio 59% YTD

Cumulative Performance since 1/1/2020: 311%

APP 26%

AXON 9%

ALAB 9%

NVDA 7%

RDDT 6%

MELI 6%

IREN 6%

HIMS 5%

ZS 5%

RBRK 4%

NBIS 4%

IOT 4%

CRDO 3%

3% or less: TSLA, HNGE, DAVE, CRWV

4

1

47

4,094

19 Sep 2025

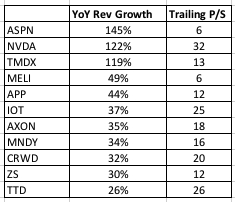

I rarely see $CRDO in my news feed. And there is a lot to like there.

Revenues up 274% YoY and 31% QoQ, gross margins at 67%, GAAP profitable to the tune of $63.4m.

Downsides are massive customer concentration, p/s ratio of 50, and lighter than usual quarterly rev guide.

2

14

2,056

18 Sep 2025

2) AI is only ~3% of revs today. But mgmt is guiding to $250m in 2025 (~33%). That’s a moonshot … and huge execution risk. Lots can go wrong.

Long $IREN

High risk, high reward

8

1,435

16 Sep 2025

This would be universally bad for all investors, but it would hurt retail more.

Investing in US companies would be much riskier and less transparent.

“Somebody knows something” would be the norm as we wait 6 months between reports to actually know what’s going on.

16 Sep 2025

BREAKING: The SEC says it is 'prioritizing' Trump's proposal to end quarterly earnings reports after his request

1

14

2,299