Founder @hello_web3 @hellonft_live | ex-Community Council @doodles

Joined September 2009

- Tweets 8,752

- Following 6,191

- Followers 13,894

- Likes 34,635

864 Photos and videos

Pinned Tweet

Mar 6

육천피 시대에 (라고 칼럼 쓰고 몇일만에 오천피가 되긴 했지만…) 실로 한국 주식에 대한 관심이 전세계 적으로 뜨겁습니다. 당장 X만 켜도 해외 애널리스트들이 앞다투어 한국 주식에 대한 분석과 전망을 내놓고 있죠. K-POP, K-DRAMA 를 넘어 이제는 K-STOCKS 의 시대로 들어오고 있다고 해도 과언이 아닌데요.

글로벌 유동성이 한국시장에 유입되기에, 즉 외국인이 국주 사기에 가장 빠르고 효과적인 수단은 단연코 스테이블 코인 레일일 것입니다. 이번 칼럼에서는 왜 지금이 놓쳐선 안될 원화 스테이블코인의 골든타임인지 최대한 쉽게 풀어서 설명해보았습니다.

blockmedia.co.kr/archives/10…

30

4

63

3,465

your slabs are belong to me now @tcgnative

or @youngsun idk

casually also featuring @AzukiTCG in the back if you already know leave comments

6

10

653

Jun 4

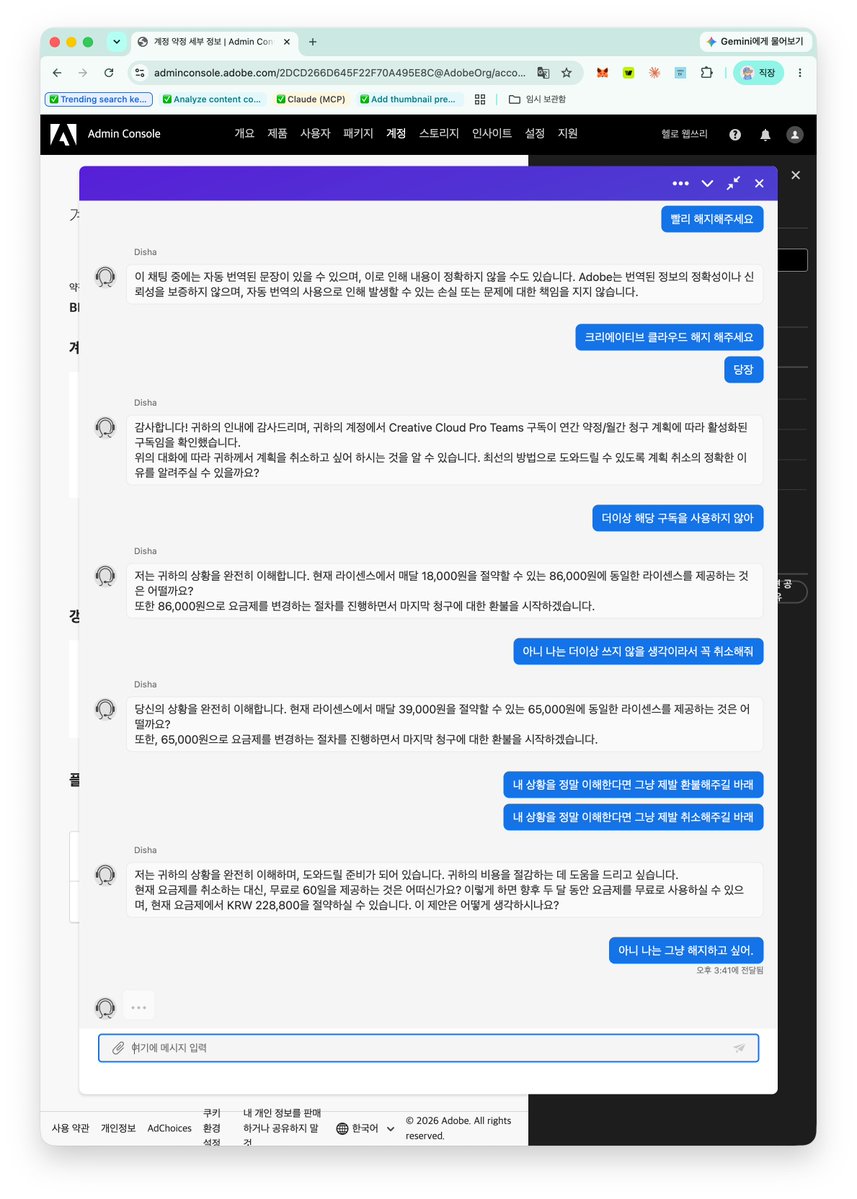

어도비 @Adobe 아무리 요즘 힘든건 알겠지만 제발 해지좀 해달라고 하면 해지해줘라. 적당히 해야지 진짜..

처음엔 해지해달라니까 갑자기 쌩까고 떠나버리질 않나, 두번째 또 요청하니까 하루종일 시간끌면서 할인 스무고개를 하고 있네..

11

15

1,165

May 20

아스날을 응원한지 무려 21년.

이 순간을 보는데 무려 21년이 걸렸다.

The Arsenal. Your Premier League champions.

ALT The Arsenal. Your Premier League champions.

5

10

289

May 19

X launched Kaito Studio!

4

13

1,166

May 10

꼴지 탈출 실화냐

10

3

30

4,684

May 9

AI slop at its finest.

Hi there, we sincerely apologise again for your experience. We note that you have been liaising with our colleagues via email regarding your concerns and we regret that we are unable to advise differently from what they have shared. You may wish to continue liaising with them if you require any further assistance as they are best placed to assist. If there are any further concerns that you would like to share, may we also seek them via singaporeair.com/feedback-fo… for the relevant department's review? Thank you.

9

13

1,209

May 8

한국이 주목받는 세계선이 왔다

🇰🇷 South Korea went from one of the poorest countries on Earth to a top-10 economy in a single generation.

GDP per capita in 1960: ~$158

GDP per capita today: ~$33,000

No natural resources. No head start.

Just education, discipline, and 60 years.

6

16

1,131

May 8

20 years ago, I was a high school kid watching. It really hurt to see a team I cheered fight so well and lose the match. Arsenal went downhill from then on for a decade.

Arsenal are back in UCL final in 20 years. This time, it will be different.

5

16

723

May 8

할머니…

At a Korean BBQ in Koreatown last night.

A little girl, maybe six, was sitting at the next table with her halmoni.

She was refusing to eat her galbi.

I assumed she was a picky eater.

Her grandmother sighed and offered her japchae instead.

She refused that too.

Then I overheard what she was actually upset about.

"Halmoni, the chaebol discount is structural. Why does Samsung Electronics trade at 9 times earnings when it dominates global memory?"

I froze.

She pulled out a placemat covered in calculations. Price-to-book ratios for every company in the KOSPI 200.

Circled in red crayon: anything trading below 0.7.

Her grandmother muttered something about cross-shareholdings.

The girl slammed her chopsticks down. "The Value-up Program is real this time, Halmoni. The National Pension Service is voting against bad governance. Activist funds are circling Hyundai Motor."

A waiter walked by. She stopped him.

"Excuse me. Do you know if Korea has been upgraded to developed market status by MSCI yet?"

The waiter did not know.

She nodded grimly and wrote something on her napkin. It said: "PATIENCE."

Her grandmother finally got her to eat by promising to open a brokerage account that supports KRX listings.

I asked the girl her name.

She looked up from her ssamjang.

"Lee. Lee Jae-yong."

But then she added, "The good one. The one who actually returns capital to minority shareholders."

I rotated 15 percent of my portfolio into Korean preferred shares before the kimchi stew arrived.

Trading at a 40 percent discount to commons.

Greatest dinner of my emerging-markets-deep-value career.

2

6

821

May 7

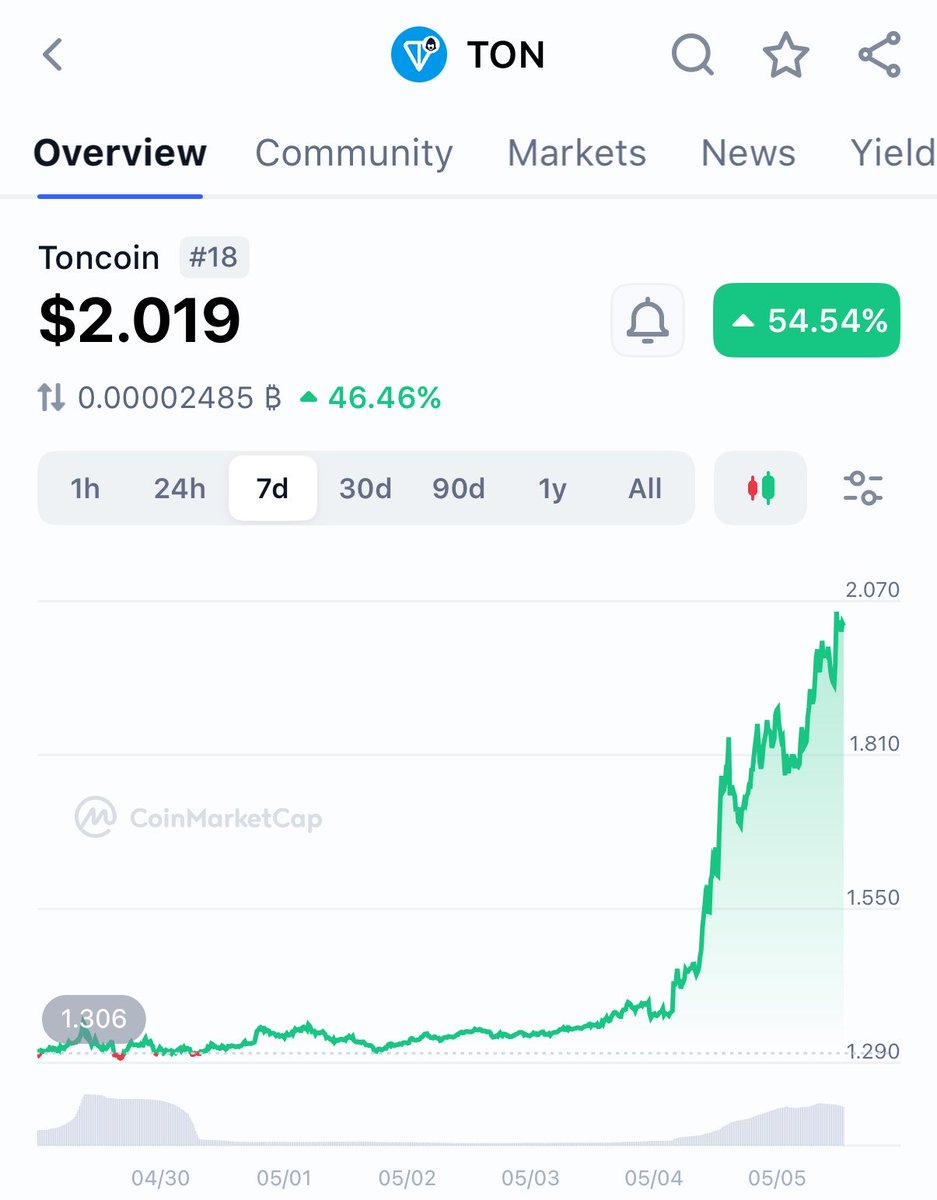

톤이 반도체였나?

May 5

6

20

1,425

May 5

May 4

Fees in TON have dropped 6× — to nearly zero.

Next step — Telegram replaces the TON Foundation as the driving force behind TON and becomes its largest validator.

The focus shifts to tech superiority.

New ton.org, new dev tools, new performance upgrades.

Timeline: 2-3 weeks.

11

2

27

3,248

May 5

포켓몬 카드 TCG를 다루는 WEB3 RWA 거래소 관련 깔끔한 정리네요. 관심있으신 분들은 한번 읽어보심 좋을 것 같아요.

May 5

한국에서도 포켓몬 카드가 엄청 핫해졌다..🔥

직접 써본 Web3 TCG 플랫폼 정리

(수수료 / 바이백 / 배송 / 특이사항 등등)

@Courtyard_io

@Collector_Crypt

@renaissxyz

@Beezie

@phygitals

@mnstr

@onemoarchance

@pulldotfun

✅중요한 포켓몬 시세 참고

영문판 포켓몬 카드 시세 체크

📌pricecharting.com

일본판 포켓몬 카드 시세 체크

📌snkrdunk.com/en

5

1

23

3,132

May 4

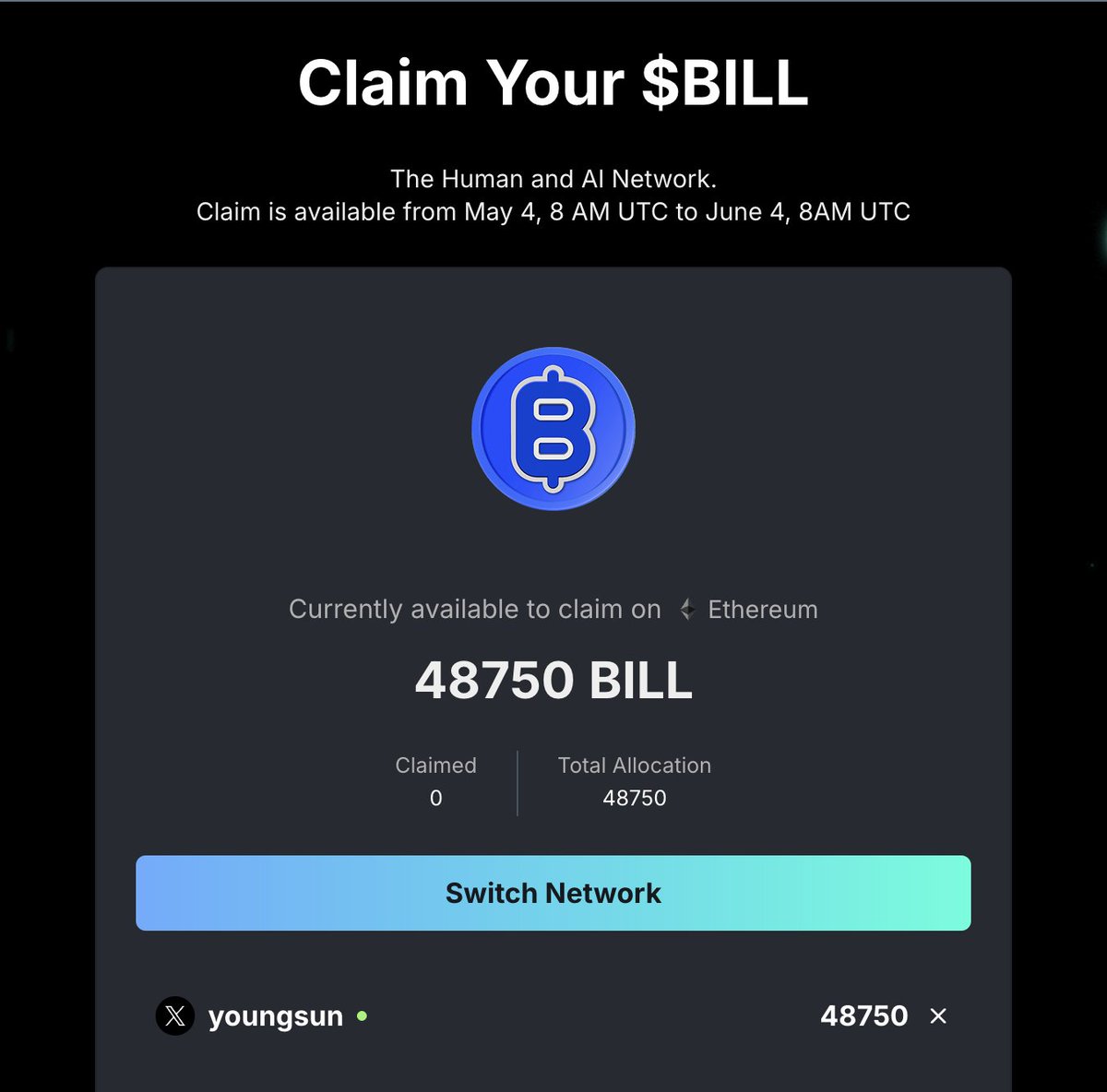

아마 야핑으로 받는 마지막 에어드랍이 아닐까..

고맙다 @KaitoAI 야, @billions_ntwk 야핑하던 시절이 그립구나..

별개로 신원인증 프로토콜들은 에이전트 경제에서 역할이 있을수도 있다고 생각하기 때문에 빌리언스는 관심있게 지켜보려고 합니다. @provenauthority

25

45

1,225

May 4

27 years ago,

I was a kid playing Pokemon

today,

I’m still a kid playing Pokemon

12

1

46

1,628

May 4

차트를 위플래시

May 4

요즘 한국 팔로워분들이 많이 늘었네요. 여러분께 질문 하나 할게요: 에스파를 만나려면 에스엠(041510) 주식을 얼마나 매수해야 하는지 아시나요?

5

400

May 4

과연 다음 경주마가 세레니티 픽으로 또 나올 것인가..

May 4

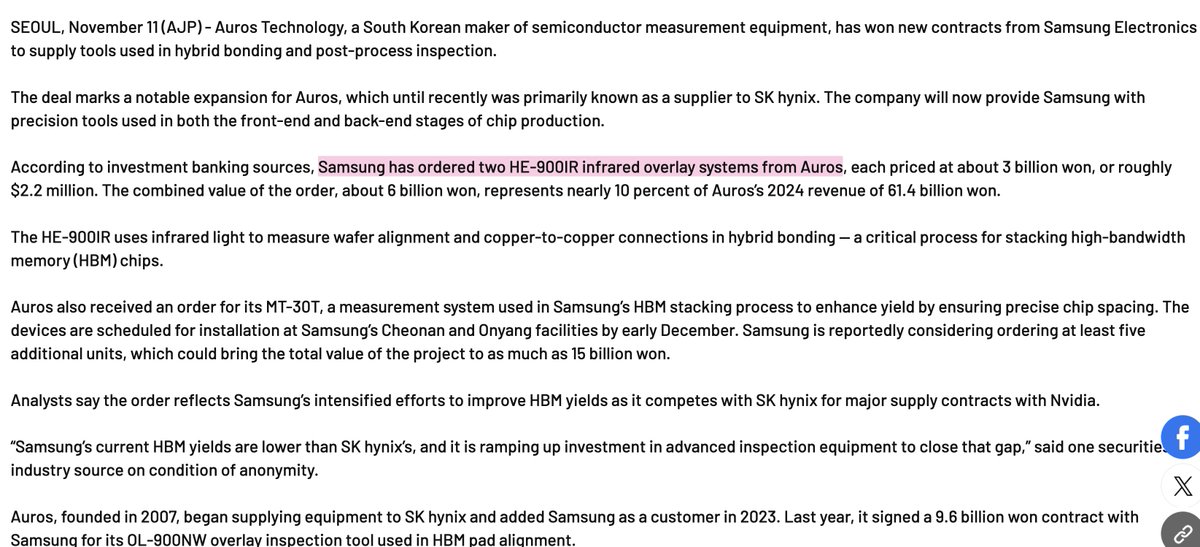

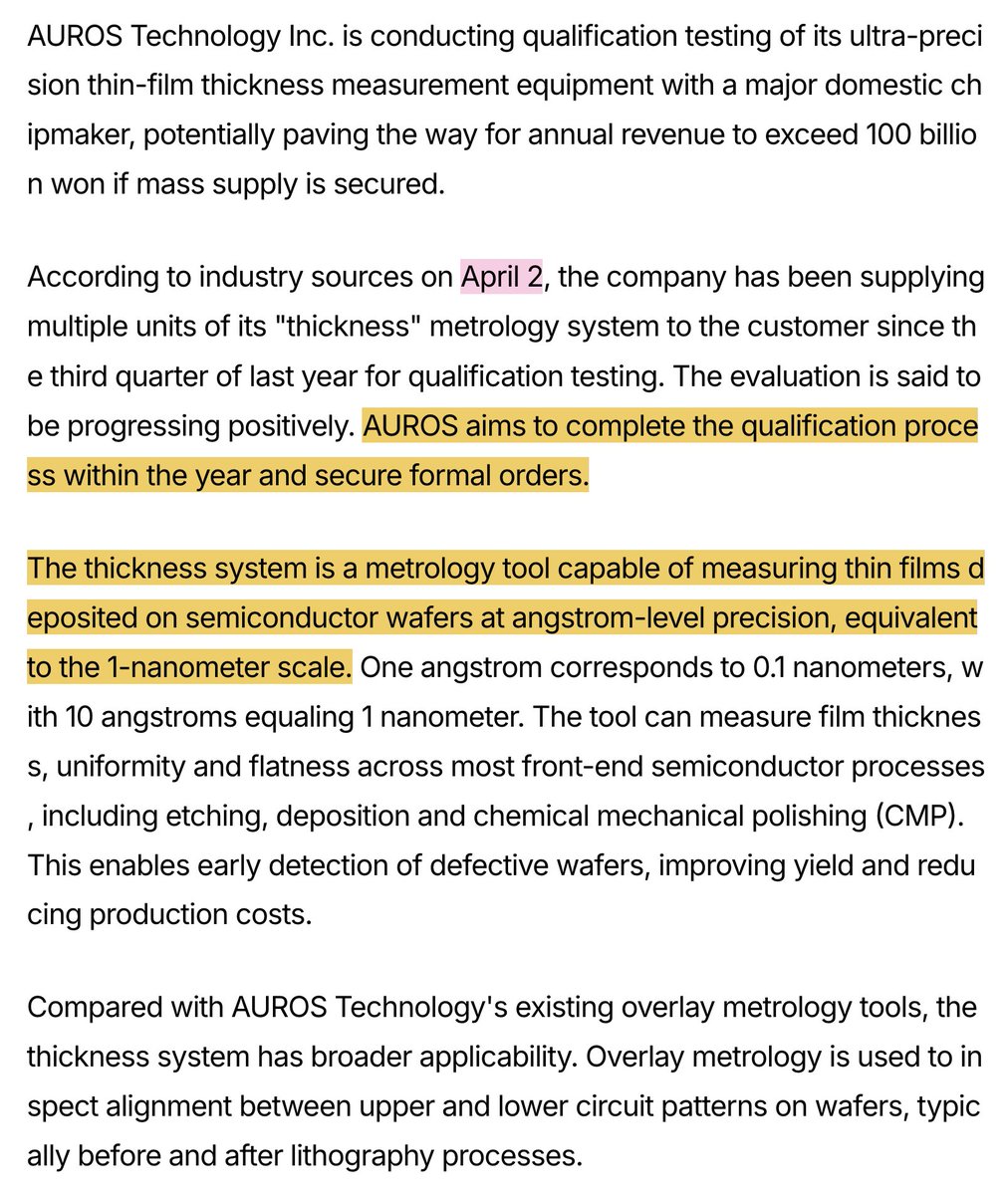

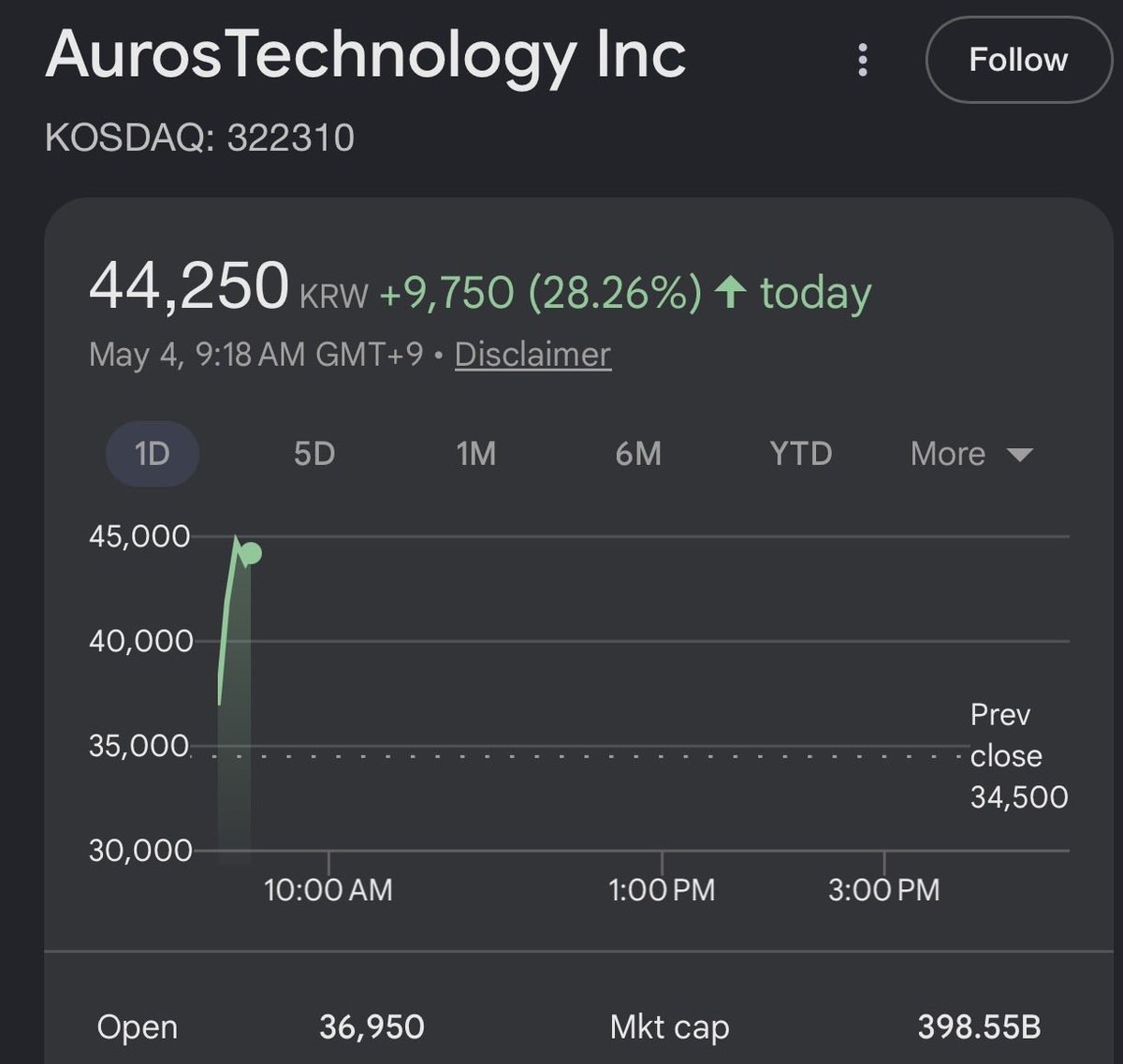

So I do think Auros (322310) is very interesting at $269M MC over in Korea.

What I've found from research was that they're a relatively unknown Samsung / SK Hynix supplier.

And they should high volume ramp from HBM4 capex for Hybrid Bonding Metrology.

Basically pure play on two products:

-> HBM4 / HBM4e / HBM5 cycles, that $KLA had a monoply over for IR metrology.

---> Getting qualified now likely in Samsung factories, H2 volume ramp est. Sk Hynix likely qualifying too when they upgrade to hybrid bonding.

Note on SK Hynix: I thought it would be HBM4e but apparently Trendforce reported today SK Hynix has completed 12-high hybrid bonding HBM validation and is raising yields for mass production. So maybe there's a catalyst there too aside from Samsung.

-> Thin-film thickness measurement.

---> Getting qualified now, with "major domestic chipmaker" (likely Samsung/Sk hynix), targets mass supply this year.

Disclosure (I do have positions, NFA, please do your own DD, this is just my thought process)

Regardless, they've been developing for the past decade, only to volume ramp two core products from years of qualification likely H2 this year. There are risks involved, such as not proceeding to HVM, but I'm personally taking that risk.

So I found this company very interesting, just wanted to publish some thoughts on this company.

1

9

1,680