The blue mark is to support Elon Musk Only

Joined May 2015

- Tweets 312

- Following 598

- Followers 168

- Likes 635

12 Photos and videos

truthinside retweeted

May 9

😭💔 Dustin Hoffman craque en larmes en DIRECT : « Je suis juif »

Il découvre pour la première fois l’histoire tragique de son arrière-grand-mère Libba Hoffman.

En Ukraine, pendant les pogroms et la révolution bolchevique : son mari assassiné par la Tcheka, elle condamnée à 5 ans dans un camp soviétique à plus de 50 ans.

Elle survit à l’enfer, perd un bras, s’enfuit via l’Argentine et arrive aux USA en 1930 à 62 ans.

Sa mère était aussi juive (origines polonaises et roumaines).

Mais des deux côtés, ses parents avaient tout effacé : pas de traditions, pas d’histoires.

Dustin savait vaguement qu’il était juif depuis ses 10 ans… sans en connaître la profondeur.

Et là, tout s’éclaire. Il fond en larmes et murmure d’une voix brisée :

« Les gens me demandent “Qu’est-ce que tu es ?”… Je réponds : “Je suis juif.”

Ils ont tous survécu pour que je sois ici aujourd’hui. Sans aucun doute. »

Merci à @museudocinema d’avoir partagé cette pépite.

Cette résilience qui traverse les générations… c’est la judéité profondément ancrée en nous, indestructible et vivante.❤️❤️

Am Israël haï 🇮🇱

342

2,422

9,762

220,239

truthinside retweeted

Apr 12

Dear Readers, Donald Trump is not like any other U.S. president. He may appear to some as temperamental, sharp in tone, and quick to anger, but at his core he is a highly intelligent and stubborn figure who knows exactly what he wants and how to achieve it. Behind the apparent chaos he creates lies a precise, calculating mind—one that weighs its steps with a balance of fire and cunning. Moreover, he can read his opponents as if they were open pages in a book.

He is neither as the media portrays him nor as his opponents wish him to be. Aside from his bombastic rhetoric, he neither deceives nor is easily deceived. He detects attempts at maneuvering before they begin and rejects without accomodation any delay. This is why Iran has not been fortunate in his return to the White House, as it now faces a man who looks at it with an eye that distinguishes between rhetoric and substance, intentions and tactics.

Yet Trump is not bloodthirsty. He opposes wars in principle and believes that limited sacrifice may be the price of saving an entire nation. He understands that if the ruling elite in Iran do not change their approach, their continued rule means the continued suffering of the people. He is also aware that nearly 90 million Iranians live between poverty and the lower middle class, aspiring to rebuild their country much as Germany did after World War II when it transformed itself into a strong and respected nation in which citizens enjoy stability and confidence in the future.

From this perspective, Trump focuses on reviving the interests of people rather than regimes, viewing the change of ruling elites—despite its cost—as a gateway to comprehensive progress that benefits millions of Iranians.

Iran is but one example among many. Trump does not forget, nor does he leave matters unresolved. He returns to complex files with a sharp focus that allows for calculated opportunities that other leaders missed or dismissed. The Syrian file, for instance, is not far from his attention. Those who believe they have bypassed or deceived Trump on this issue will soon discover they are facing a man who neither forgets nor retreats until he imposes his terms in full.

It is also evident that he is steadily moving toward confronting authoritarian regimes, as his logic is rooted in breaking the closed cycles of oppression people suffer from within such systems. Venezuela was first, Iran is now, and perhaps Cuba will follow.

At the same time, Trump is loyal and sincere to those who respect him or deal with him in good faith. Behind his harsh language is a practical individual who values work and achievement and seeks to accomplish something meaningful for his country that changes reality for the better. His blunt candor may be seen by some as a flaw, but he considers it a strength, as clarity for him is a virtue, not a shortcoming.

For this reason, those who see him as merely an outlier among U.S. presidents do not truly understand him. He has established an approach that will endure as long as America seeks to renew its strength: Make America Great Again. This is not just a slogan, but a doctrine Donald J. Trump initiated—one that will persist and only grow stronger and more influential over time.

169

816

2,907

123,725

truthinside retweeted

This is arguably the greatest scene of all-time in any movie, it happens to be a finance movie:

479

2,336

17,262

1,935,438

一个住在德黑兰的伊朗女孩,在轰炸声中录下这段话。

她说:

万一我明天死了,请记住。

是我们要求这次攻击的。

我们想要这次攻击。

她说:

请闭嘴。

不要用我的死,来攻击美国或以色列。

不要劝他们停手。

为什么?

她说,我们试过上街抗议。

结果呢?

两天,政权杀了我们四万人。

和平的路已经走不通了。

这是我们最后的机会。

她说:

我可能会死,但我不怕。

我愿意为伊朗牺牲。

这段话,刺痛了谁的耳朵?

那些在安全办公室里呼吁“克制”的政客。

那些在大学校园里高喊“反战”的学生。

他们听见的,是自己脑海里的和平。

却听不见,一个民族用生命发出的呐喊。

当一个女孩愿意用死亡换取国家的新生。

你廉价的和平,又算什么?

345

2,060

8,944

521,972

truthinside retweeted

9 Oct 2025

195

495

2,801

17,422,828

truthinside retweeted

18 Dec 2025

🔥🎯 Elon Musk 给 xAI 团队的内部判断,其实只指向一件事:AI 竞赛不是“谁模型聪明”,而是“谁能活过接下来 2–3 年”。

他给出的核心结论很直接:真正的胜负手只有三个——算力、能源、资本,而且必须比任何人扩张得更快。

这场会议里,有几个信息密度极高的点,被很多人低估了。

第一,时间窗口。

Elon 认为 AGI 并不是遥远概念,xAI 内部判断最早可能在 2026 年出现。这不是对外营销口径,而是直接对员工的风险判断:如果接下来两三年撑不住,后面就没资格谈未来。

第二,资金与“续航能力”。

xAI 当前具备接近每年 300 亿美元级别的资金动员能力。这意味着它不是在做“下一代模型实验”,而是在为长期算力消耗战提前准备弹药。AI 的竞争,正在快速演化成一场资本耐力赛。

第三,对 Grok 的真实预期。

内部并没有把 Grok 5 描述成“必然 AGI”,而是明确给出了一个概率区间:大约 10% 的可能性触达 AGI。这一点反而值得重视——当一个团队愿意在内部承认不确定性,说明他们更清楚难点在哪里。

第四,算力扩张路线图。

xAI 目前规模约 20 万张 GPU,但目标是向 100 万张 GPU 扩张,并集中在 Colossus 数据中心体系内完成。这不是单点部署,而是围绕电力、散热、网络、训练节奏的系统工程。

第五,机器人与算力的交叉点。

Optimus 并不只是“消费级人形机器人”。在 xAI 的长期设想中,它有可能直接参与数据中心运维。这意味着未来算力系统,可能由 AI 训练 AI、由机器人维护 AI。

第六,极端长期的边界设想。

会议中甚至提到了太空数据中心、以及与火星相关的基础设施构想。这听起来很科幻,但背后的逻辑一致:当算力和能源成为核心瓶颈,地理边界本身也会被重新评估。

把这些点连起来看,会发现一个清晰信号:

Elon 关心的从来不只是模型参数,而是“谁能在极端资源密集型竞争中存活下来”。

当 AI 进入基础设施时代,真正的护城河,可能不再写在论文里,而是写在电网、资本结构和执行速度上。

你更认同哪一种判断:

AI 的胜负最终由模型突破决定,还是由算力与能源规模决定?

📣持续分享关于 AI、算力基础设施与科技公司关键拐点的长期观察与判断,帮助你在噪音之前看清趋势方向,欢迎关注。

#ElonMusk #xAI #AI #AGI #Grok #Optimus #GPU #DataCenter #ArtificialIntelligence

16

49

173

19,574

truthinside retweeted

17 Dec 2025

Nancy Pelosi absolutely DESTROYED Warren Buffett in the stock market since 2012..

This is insanity.

1,567

9,130

39,411

6,135,455

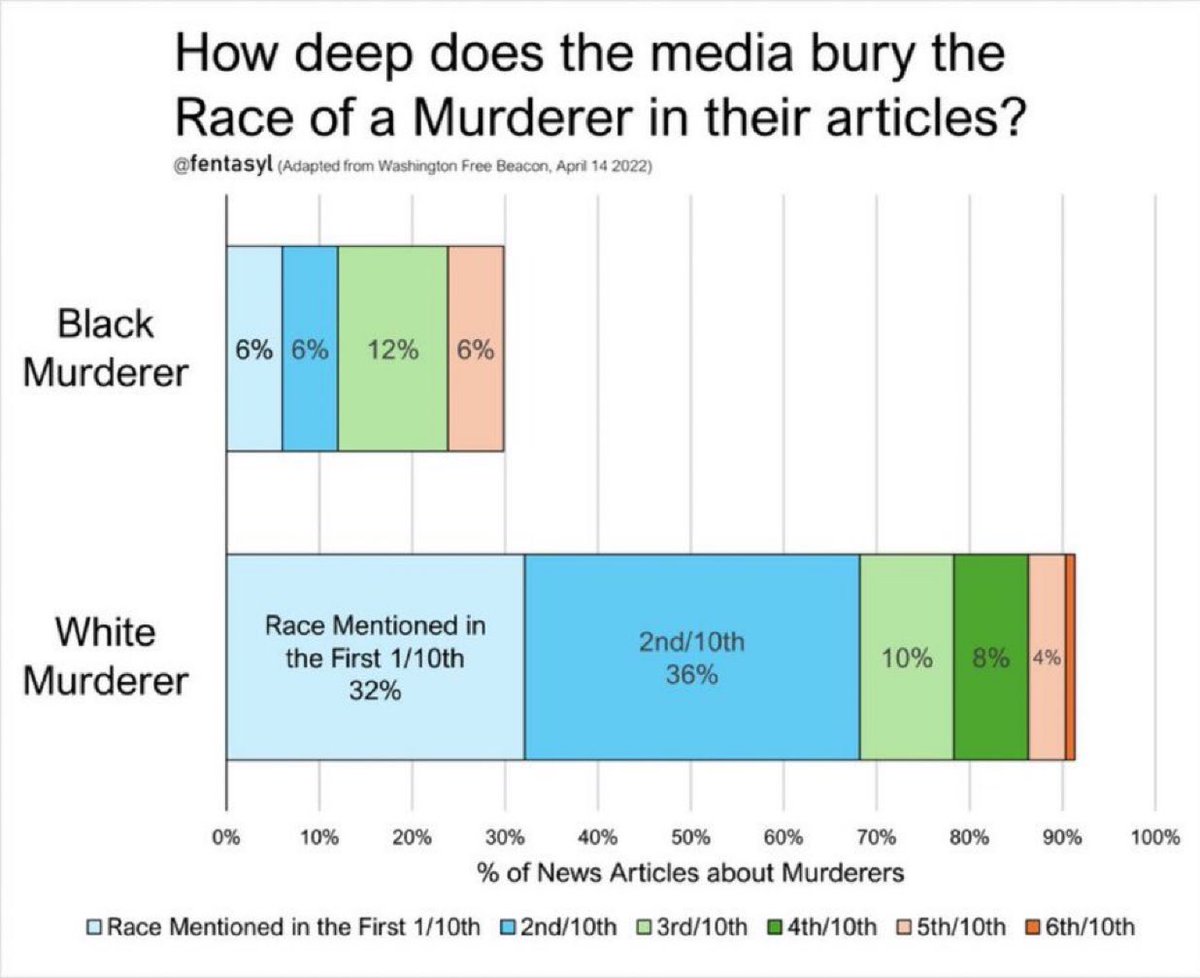

But why does the legacy media do this?

15 Dec 2025

The likelihood of legacy media discussing a murderer’s race depends on the murderer’s race.

This is why BLM martyrs like George Floyd get endless coverage while cases like Iryna Zarutska are forgotten.

The bias is clear:

6,235

24,323

126,939

53,570,107

truthinside retweeted

29 Nov 2025

Circle为什么把看似一本万利的生意做成了费力不讨好的苦生意。

明明隔壁大哥Tether三个季度净利润超过100亿美金,利润率高达99%。Ardoino自己都说:“我们有99%的利润率,世界上没有其他公司能做到这一点。”

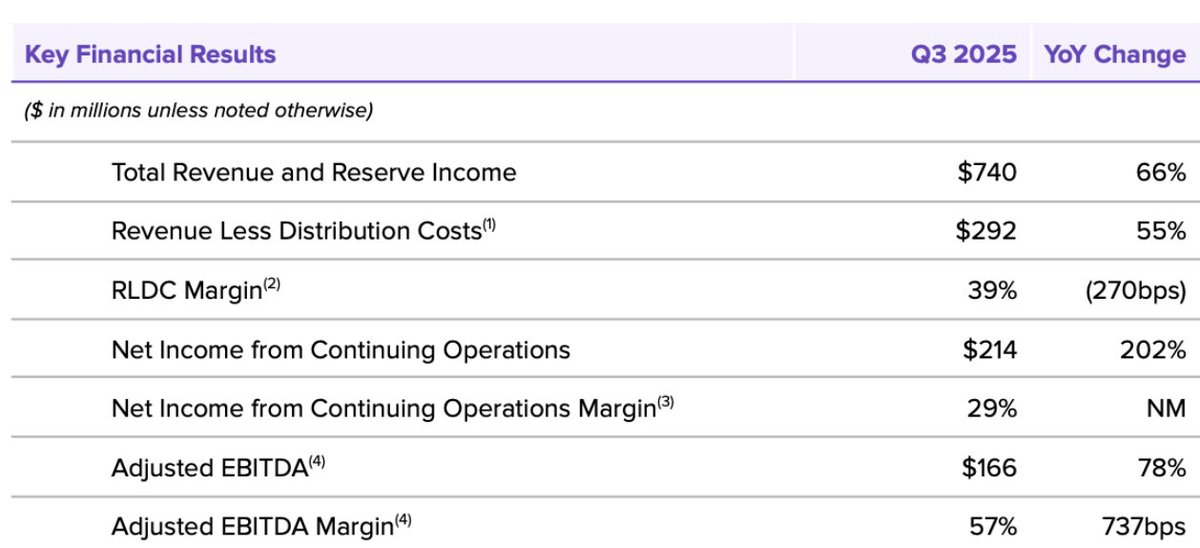

那Circle $CRCL 的财报说了怎么样的一个故事?他们的利润率被什么侵吞了?(数据来源 circle.com/pressroom/circle-…)

1️⃣财报好在哪里?哪些超过了预期?

总收入约 7.40 亿美元,同比增长约 66%。

净利润为 2.14 亿美元,同比大涨约 202%。

每股收益(EPS, GAAP)为 0.64 美元,超过市场预期。

USDC 流通量截至季度末为 737 亿美元,同比增长 108%。

这是 CRCL IPO 后首次公布的季度报告之一,也是近期表现非常亮眼的一期 — 营收与盈利双双大幅改善。

但是在这份财报公布后不久,Circle的股价却是一路丝滑下跌。虽然有大行情的锅,但是Circle这份财报里的问题也不少。

2️⃣Circle差在哪里?为何做着卖白粉的生意赚着卖白菜的钱?

答案还是分销 运营费用太高昂了!财报中有一栏Total Distribution, Transaction and Other花了4.48亿,另有一栏运营费用为 2.11 亿美元。除去这俩,Adjusted EBITDA就只剩下可怜的1.66亿。

Circle 的分销费用(Distribution Payments)中,很大一部分是支付给像 Coinbase 和 Binance 这样的合作平台的。相当于USDC缺少终端获客的能力,为了获得客户,就需要付出高昂的渠道分发费用。

据估算,2024年circle分给coinbase的渠道费用就有9亿美金。而那一年公司的全年毛利仅有3.95亿美金。

Circle看规模和业务是金融行业,看利润率简直比制造业还制造业。

3️⃣这种局面会有改变么?

那要看Circle的管理层在做什么。

🌟搭建ARC L1-我的理解这是一条更加To B的公链

🌟CPN(Circle Programmatic Network):已在 8 个国家支持资金流转,有 29 家金融机构已完成接入,另有 55 家正在进行资质审查,并有 500 家处于接洽或排队阶段。

但是在我看来,这些都是帮助circle把盘子做大,但是他们高昂的渠道费用和运营费用似乎短期内并不会有什么下降。估计在未来的一段时间内,还是会维持高发行率,高运营分发费,低利润率的局面。

4️⃣那咱们还投么?

长期看好,唯一的问题就是价格了。从这次的USDe脱钩事件,USDT和USDC的地位和稳定其实得到了再次的验证。

USDT投不了, $CRCL 是唯一的选择。而且他的合规费用何尝不是构成了他的护城河。

虽然有很多新的竞争者参与,但是他第二名的地位短期内很难被动摇(参考Coinbase)。

如果按照第三季度的财报和20倍PE的估算,我希望可以在更低的价格买入。就看市场给不给机会了。

最后一张配图来源 @bitfish

38

31

210

133,773

truthinside retweeted

25 Nov 2025

$LITE $COHR I’ve shared a similar post to this about CPO lasers before and here it goes one more time.

———

Within the CPO stack, the most direct economic leverage is in external laser sources (ELS) based on high‑power InP DFB/EML devices. These lasers sit off‑package and feed multiple silicon‑photonics engines, so a small group of InP laser vendors effectively controls a disproportionate amount of value. The companies with the clearest positive leverage to CPO lasers are Lumentum, Coherent, Furukawa Electric, Sivers Semiconductors (Sivers Photonics), POET Technologies (through ELS modules), and a set of Chinese and Japanese vendors with meaningful but less pure exposure such as Sumitomo Electric, Innolight/Eoptolink, and O‑Net. Lumentum is the most concentrated liquid public vehicle for CPO lasers among large‑cap names; Sivers and POET provide higher‑beta small‑cap leverage; Coherent and Furukawa add more diversified but still material exposure.

CPO lasers themselves are becoming a distinct segment. NVIDIA’s Quantum‑X and Spectrum‑X silicon‑photonics switches depend on external UHP lasers delivering around 400 mW per channel at 1310 nm into ELS units that are pluggable at the faceplate.  Each switch can incorporate >100 individual laser channels, so total laser content per system is an order of magnitude higher than in a traditional pluggable optics architecture. The Mizuho Lumentum report assumes UHP DFB lasers at $50–100 per device, ~8 lasers per ELS, and ~16–18 ELS per 128–144‑port CPO switch, implying roughly $10k–20k of laser content per high‑end switch.  As other CPO platforms emerge, that laser bill of materials will be replicated across multiple ASIC vendors and hyperscalers. Because only a handful of manufacturers can reliably deliver high‑power, low‑noise, long‑lifetime InP lasers at these power levels, industry structure is oligopolistic and pricing power is stronger than in commodity pluggable optics.

Lumentum has the single strongest, cleanest exposure to CPO lasers. It is already the market leader in 100G/200G EML lasers for pluggables with >50–60% share of high‑speed EML lanes in AI data centers and is now positioning its UHP 1310 nm DFB lasers explicitly for CPO. Lumentum has been publicly named as a key laser supplier in NVIDIA’s silicon‑photonics ecosystem, with its high‑power, high‑efficiency lasers described as “crucial” to Spectrum‑X Photonics switches.  The company is expanding U.S. production of these UHP lasers at its San Jose InP fab and is described as a “primary supplier to the industry” for CPO lasers, with capacity expansion explicitly tied to AI‑driven CPO demand.  In the Mizuho model, CPO revenue from these UHP CW lasers is projected to rise from essentially $0 in FY25 to ~$93M in FY26, ~$356M in FY27, and ~$517M in FY28, reaching ~13% of total revenue and carrying >50% gross margins.  Given that total laser revenue is expected to be ~$2.2B in FY28, about half of corporate revenue, CPO lasers alone could represent roughly 20–25% of laser revenue and a substantially higher share of incremental laser profit.  Among large‑cap names, Lumentum therefore has the highest combination of (1) explicit design‑in status for CPO lasers, (2) visible capacity expansion for CPO‑grade InP, and (3) financial disclosure tying outsize EPS growth directly to CPO laser ramps.

Coherent is the other major Western InP laser supplier with clear CPO leverage, though its exposure is diluted by a broader product set that includes industrial lasers, materials processing, and other photonics. Coherent has announced sampling of low‑noise 400 mW CW lasers specifically marketed for silicon‑photonics and CPO platforms, highlighting their role in solving high‑power, low‑noise challenges for co‑packaged optical interconnects.  The company is building a 6‑inch InP fab in Sherman, Texas, which is expected to expand InP laser production capacity by >5x, explicitly citing accelerating demand from datacom, AI, and CPO applications.  Coherent has also been named as one of NVIDIA’s “ecosystem innovation collaborators” for silicon‑photonics networking switches using CPO, confirming that it is engaged at the platform level.  However, Coherent’s overall business is significantly more diversified than Lumentum’s, and lasers for CPO are only 1 of several growth vectors (alongside transceivers, LiDAR, industrial lasers, etc.). The positive leverage exists but the beta to CPO lasers per dollar of equity is lower than for Lumentum, and the internal business mix reduces the direct sensitivity of earnings to CPO laser volumes.

Furukawa Electric is an important, though less pure, CPO laser and ELS supplier. Furukawa has been one of the earliest demonstrators of CPO‑specific external laser sources. It exhibited a pigtailed‑QSFP ELS for CPO at OFC 2022, integrating an 8‑channel TOSA and control electronics in a pluggable QSFP housing.  Subsequent technical work reported record energy‑efficient ELS designs achieving 8 channels at 100 mW per channel with total power consumption of 5.6 W, which is directly targeted at CPO use cases.  Independent industry commentary highlights Furukawa’s vertical integration from InP laser epitaxy through TOSA and ELSFP module assembly as a competitive advantage versus more disaggregated suppliers.  At the corporate level, Furukawa is a diversified wire, cable, and components manufacturer with a large legacy telecom and power business, so CPO lasers are still a relatively small contributor to total revenue. Nevertheless, within the Japanese listed universe it is 1 of the few direct beneficiaries of rising CPO laser volumes, with the caveat that financial leverage to CPO is modest relative to the scale of the group.

Sivers Semiconductors, through its Sivers Photonics division, provides very high operational leverage to CPO lasers from a small‑cap European base. Sivers Photonics positions itself as a customized III‑V photonics foundry for communications and sensing, including InP laser arrays for advanced optical interconnects.  It has worked with imec and ASM AMICRA on integrating InP lasers with silicon‑photonics platforms, including external cavity laser sources suitable for emerging optical interconnect applications.  In 2025, Sivers announced 2 explicit CPO‑laser partnerships: (1) a collaboration with POET Technologies to co‑develop external light source modules for CPO and next‑generation AI infrastructure, using Sivers’ high‑power lasers integrated on POET’s optical interposer, and (2) a strategic OEM partnership with O‑Net Technologies, where Sivers’ DFB laser arrays will be integrated into O‑Net’s ELSFP modules aimed at CPO for switches, NICs, and AI systems.  Given Sivers’ relatively small revenue base, any meaningful commercialization of these CPO ELS programs would translate into very high earnings leverage. The risk profile is correspondingly high, as the company is still in the ramp and qualification phase rather than mass CPO deployment.

POET Technologies offers more indirect but still meaningful leverage to CPO lasers via ELS modules rather than laser die. Its optical interposer platform is designed to integrate multiple photonic components, including lasers, into scalable ELS modules suitable for CPO. The recently announced collaboration with Sivers targets high‑performance external light source modules for CPO and AI fabrics, with Sivers providing high‑power lasers and POET providing the integration and packaging.  In this structure, POET’s economic exposure is to the module ASP and integration value, while Sivers retains the pure laser content leverage. POET’s equity, however, will trade with the perceived success or failure of these ELS programs, so it can be considered a second‑order play on CPO lasers with additional upside from other photonics applications.

Several other vendors have material but more diversified exposure to lasers that can be used in CPO, even if CPO is not yet a dominant revenue driver. Sumitomo Electric and Mitsubishi Electric both manufacture InP laser diodes and related photonic components, and are cited as relevant competitors in high‑speed optical lasers that could be designed into CPO platforms.  Innolume, a German InP laser specialist, showcases high‑power lasers and CPO‑related demonstrations at OFC and similar conferences, although the company is private and thus not directly investable via public markets.  In China, companies such as Innolight, Eoptolink, Accelink, and HG Genuine are aggressively expanding 400G/800G optical module production and are beginning to invest in SiPho and potentially ELS for CPO.  Their current economics are dominated by pluggable modules rather than ELS units, but over time they may backward‑integrate into CPO‑grade laser arrays, especially for domestic Chinese CPO deployments. O‑Net, via its partnership with Sivers, is already positioning to supply ELSFP modules for CPO and thus has a hybrid module‑plus‑laser exposure.

Broadcom, Marvell, Cisco (via Acacia), and NVIDIA itself are central to the CPO ecosystem but have limited direct leverage to discrete lasers. Broadcom and Marvell are primarily SerDes, DSP, and switch‑ASIC suppliers; their CPO economics sit in the photonic engine, silicon, and packaging rather than the laser die. Cisco’s exposure is centered on integrated optical modules and CPO engines through its acquisition of Acacia. NVIDIA will capture most of the system‑level value in CPO switches, but its internal economics treat external lasers as a purchased component, so it is structurally incentivized to multi‑source laser supply and drive pricing. For investors seeking pure laser leverage rather than broad CPO exposure, these system and silicon vendors are less direct vehicles.

From an investment standpoint, the highest direct positive leverage to CPO lasers among liquid public names sits with Lumentum, Coherent, Furukawa Electric, and Sivers, with POET and selected Chinese/Japanese module players providing additional, more indirect exposure. Lumentum has the clearest line of sight to large CPO laser revenue and profit, anchored by NVIDIA design‑ins and explicit capex expansion for UHP InP lasers, and already embeds several hundred million dollars of projected CPO laser revenue in FY27–28 forecasts. Coherent and Furukawa have meaningful CPO laser optionality but with more diversified business models that dampen earnings sensitivity to CPO. Sivers and POET offer more speculative, higher‑beta leverage where modest absolute CPO laser volumes could translate into very large percentage shifts in revenue and valuation, but with commensurate technology, execution, and customer‑adoption risk. For portfolio construction focused specifically on lasers in CPO, a barbell of a core position in Lumentum, supplemented by smaller tactical exposures to Coherent/Furukawa for diversification and Sivers/POET for convex upside, would best align with the underlying industry structure of the CPO laser market.

25 Nov 2025

$LITE The Mizuho initiation on Lumentum on 11/18/25 frames the company as a high‑leverage beneficiary of the AI data center optical transition, with the core claim that LITE will monetize 4‑8x bandwidth growth inside AI data centers through leadership in InP EML lasers, early positioning in co‑packaged optics (CPO) lasers for NVIDIA, and MEMS‑based optical circuit switches (OCS) for hyperscalers. The report projects revenue rising from $1.6B in FY25 to $4.2B in FY28, a 37% CAGR, with EPS increasing from $2.06 to $10.86, a 74% CAGR, and gross/operating margins expanding from 34.7%/9.7% to 42.4%/25.4%.  At the time of publication the target price of $290 implied material upside from a $242 share price. That upside has largely been realized: Lumentum now trades near $290 with a market cap above $20B, roughly 50x FY26 EPS, 33x FY27 EPS, and 26x FY28 EPS on Mizuho numbers, and modestly higher multiples on consensus. The investment question becomes whether the out‑year growth and margin structure embedded in this multiple are achievable and whether incremental upside versus both consensus and peers compensates for execution, technology, and customer‑concentration risk.

The industry backdrop described in the report is directionally correct and strongly supportive of high‑end optics. AI cluster scaling is pushing network port speeds from 200G/400G to 800G and, over the coming 3‑5 years, to 1.6T and eventually 3.2T, with networking bandwidth roughly doubling every 2 years. The charts on pages 8–10 show total data‑center port counts growing at only high‑single‑digit CAGRs, while ports at 400G and above grow much faster, with 800G AI port counts modeled at a 119% CAGR and 1.6T starting to contribute late in the decade.  Copper links are increasingly constrained by reach and power consumption at these speeds. Optical links—particularly those using InP wideband lasers—offer better power‑per‑bit and reach, and therefore are expected to capture most of the incremental bandwidth. External research on AI networking from Gartner, LightCounting, and NVIDIA’s own CPO announcements is consistent with this direction of travel: high‑speed optical TAM inside data centers is expanding rapidly, and 800G/1.6T optics will be required to sustain AI cluster scaling. There is, however, meaningful uncertainty around how value will be split between pluggable optics, linear pluggable optics (LPO), and co‑packaged optics, as well as around the pace and breadth of OCS adoption beyond early users like Google.

Lumentum’s current business mix provides a solid base but is already becoming highly AI‑skewed. FY25 revenue of $1.65B is split 68% components and 32% systems, with components dominated by high‑speed lasers and optical chips and systems encompassing transceivers, OCS, and industrial lasers.  Regional exposure is 61% Asia‑Pacific, 29% Americas, and 10% EMEA, reflecting both telecom heritage and outsourced manufacturing. Key end markets include data‑center interconnect, long‑haul/metro telecom, industrial lasers, and consumer VCSELs for 3D sensing. Google and Ciena together account for more than 31% of revenue, with Apple, Nokia, and Amazon as other important customers.  The waterfall chart on page 4 shows that >84% of projected FY25‑28 revenue growth is tied to AI data‑center optics, primarily EML/CW lasers, CPO content, OCS, and cloud transceivers.  This concentration strongly gears Lumentum’s earnings to AI data‑center capex cycles and to a small number of hyperscalers and NVIDIA.

The core of the equity story is Lumentum’s InP EML laser franchise. The report estimates LITE has 50‑60% unit share in the high‑speed 100G/200G‑per‑lane EML market, despite only ~6% share of the overall laser‑diode market, with Broadcom and Coherent as the main competitors.  InP’s share of optical lanes is modeled to increase from 61% in 2024 to 81% by 2029 as data rates move to 200G per lane; the company has demonstrated 15‑45% lower power‑per‑bit versus alternatives at 200G lanes.  Lumentum is currently supply‑constrained in 100G EML due to 800G AI deployments and is increasing EML capacity by 40% over approximately 3 quarters. The FY26 guide and Mizuho’s FY26‑27 revenue ramp assume that this incremental capacity is fully absorbed by AI demand, with laser revenue growing from roughly $1B in FY25 to about $2.2B by FY28, a 31% CAGR and 54% of total revenue.  This requires not only that AI port growth remains extremely strong but also that Lumentum maintains or grows its share in the face of competition from Coherent, Furukawa, and a set of emerging InP and SiPho suppliers, including potential second‑source laser providers in NVIDIA’s CPO ecosystem. The external data around Lumentum’s 200G and 400G InP chip introductions, UHP 1310nm DFB lasers, and US capacity expansions supports the view that technology and manufacturing investments are being made to sustain this share. However, Mizuho’s implicit assumption of largely stable share and sustained 50‑100% ASP uplifts per generation is optimistic; history in optical components suggests aggressive pricing and share shifts once alternative suppliers qualify.

The second pillar is CPO, where Lumentum has been publicly named as a key laser supplier to NVIDIA’s Spectrum‑X and Quantum‑X Photonics switches. NVIDIA’s March 2025 GTC press release and Lumentum’s own release describe a silicon‑photonics ecosystem in which Lumentum supplies high‑power, high‑efficiency lasers, while Coherent collaborates on the silicon‑photonics CPO implementation and other partners such as TSMC, Corning, and Foxconn participate across the stack. NVIDIA claims its CPO switches deliver 1.6Tbps per port, 3.5x power efficiency improvements, and 10x resilience with 4x fewer lasers than traditional architectures. Mizuho’s model assumes Lumentum is effectively sole‑sourced for external laser modules (ELS) feeding Quantum‑X and Spectrum‑X, with UHP 400mW DFB lasers priced at $50‑100 each, 8 lasers per ELS, and ~16‑18 ELS per 128‑144 port switch, implying roughly $10k‑20k LITE content per high‑end CPO switch.  On that basis, CPO revenue is projected to rise from a few million dollars today to ~$93M in FY26, $356M in FY27, and $517M in FY28, a 416% CAGR.  These projections appear aggressive relative to the available external evidence. NVIDIA has explicitly stated that CPO‑based systems will be offered alongside, not in place of, pluggable‑based systems, and that adoption will depend on specific customer workloads and power envelopes. Furthermore, NVIDIA’s communications emphasize a multi‑partner ecosystem rather than exclusive dependence on Lumentum. In high‑volume networking silicon, dual‑sourcing is standard practice. A more conservative base case would assume strong early CPO adoption but with Lumentum’s share of CPO laser content in the 30‑60% range over time rather than effectively 100%, and with the CPO mix of total 1.6T ports ramping more gradually. Under such assumptions, the FY27‑28 CPO revenue contribution could be materially lower than Mizuho’s $300‑500M trajectory, which would reduce both the absolute EPS and the mix‑driven margin uplift that the initiation embeds.

The third major growth vector is OCS, where Lumentum’s R300 and R64 MEMS‑based optical switches target AI data‑center fabrics for both scale‑out and scale‑up use cases. The report models the OCS data‑center TAM rising from roughly $400M today, almost fully driven by Google’s internal Palomar/Apollo deployments, to $1.9B by 2029, a 44% CAGR, with Lumentum capturing 30‑40% share and generating more than $500M of OCS revenue by FY28.  This implies LITE OCS revenue rising from near zero in FY25 to $71M in FY26, $416M in FY27, and $586M in FY28, with ASPs around $80‑90k and gross margins above 50%.  The technical rationale for OCS is sound. Google’s public Jupiter/Apollo work shows that OCS‑based fabrics can deliver around 30% capex reduction, >40% power savings, and lower flow‑completion times through direct optical connections and elimination of spine switch layers. Lumentum’s R300 product literature and third‑party analysis claim >65% network power reduction and significant latency improvements for large GPU clusters, with sampling at multiple hyperscalers and general availability in 2H25. In addition, LITE is co‑leading the Open Compute Project’s OCS subproject, alongside iPronics, Google, Microsoft, and others, to standardize photonic networking and OCS interfaces. These developments support the thesis that OCS can transition from bespoke, single‑customer systems to a broader, standards‑based market.

The key investment issue is not whether OCS is technically attractive but how quickly and broadly hyperscalers will deploy third‑party OCS hardware and what share Lumentum will capture. Google’s current deployments are largely in‑house. There is no public evidence yet that AWS, Azure, or even Google have committed to multiyear, volume purchases of Lumentum’s R300/R64. Competitive offerings exist from Coherent (liquid‑crystal OCS), Huber Suhner’s Polatis line, Telescent, Calient, and others. Standardization under OCP is a double‑edged sword: it likely accelerates overall OCS adoption but tends to compress margins and lower barriers to entry over time. The Mizuho forecast effectively assumes that LITE wins 2‑3 large hyperscaler designs and rapidly achieves several hundred million dollars of annual OCS revenue within 3 years at very high margins. A more neutral stance would treat this as an upside scenario rather than a base case; the base should probably assume slower OCS adoption curves, partial design win share, and margin pressure as additional vendors enter.

The cloud transceiver business provides incremental revenue scale but is structurally much less attractive than lasers, CPO, or OCS. Lumentum leverages its laser and DSP assets (augmented by the NeoPhotonics, IPG Photonics, and Cloud Light acquisitions) to sell 400G/800G/1.6T pluggable transceivers into hyperscalers, with estimated ASPs of $0.40‑0.50 per Gb ($400‑800 per module), but at only mid‑teens to, over time, perhaps 30% gross margins.  The company is deliberately capping this business at roughly $1B per year to limit corporate margin dilution. The Chinese optical module ecosystem is a major competitive force: Innolight, Eoptolink, TFC, Luxshare, and others are scaling 400G/800G transceiver volumes rapidly, with some players more than doubling revenue and pricing around $0.35 per Gb. This supply base has a structural cost advantage from localized labor and vertically integrated component supply. Lumentum’s US and global manufacturing footprint, plus its closer alignment with US hyperscalers and NVIDIA and its expected role in secure domestic AI supply chains, partly offsets that disadvantage. Nonetheless, margin expansion assumptions in the report—corporate gross margin rising to 42‑43% even as transceivers reach nearly $1B revenue—depend on OCS and CPO reaching scale and contributing >50% gross margins. If OCS/CPO ramp more slowly or at lower margins, the incremental transceiver mix will act as a headwind to the targeted margin structure.

Financially, Lumentum is transitioning from a telecom‑centric, mid‑30s gross margin, high‑single‑digit operating margin business to a model that more closely resembles high‑growth communications semiconductors. Q1 FY26 results showed revenue of $533.8M, up 58% year‑on‑year, with non‑GAAP gross margin of 39.4%, operating margin of 18.7%, and EPS of $1.10, at the high end of guidance. Management guided Q2 revenue to about $650M with further operating leverage as EML and transceivers ramp. Mizuho projects FY26 revenue of $2.63B, up 60% year‑on‑year, followed by $3.58B in FY27 and $4.21B in FY28, with gross margins rising from 40.3% to 42.4% and operating margins from 21.1% to 25.4% over that period.  EPS is modeled at $5.78 in FY26 (essentially in line with street), $8.77 in FY27 (about 7% above consensus), and $10.86 in FY28 (about 16% above consensus), implying more than 5x EPS growth in 3 years.  Free cash flow is projected to ramp from roughly $141M in FY25 to $593M in FY28, as capex normalized after heavy investment in laser and module capacity.  These numbers are internally consistent with the underlying product assumptions, but they embed very high execution and demand certainty: in rough terms, about $2.6B of FY28 revenue (over 60% of total) is expected to come from AI‑specific laser, CPO, OCS, and cloud transceiver businesses that barely existed in FY24. Any delay or disappointment in AI capex, CPO mix, or OCS deployments would cascade quickly into revenue and margin outcomes, given the company’s operating leverage.

At around $290 per share, Lumentum trades on roughly 50x FY26 EPS, 33x FY27 EPS, and 26x FY28 EPS using the Mizuho forecasts; on consensus EPS, the FY27 and FY28 multiples are closer to 35x and 28x. The peer group in the report (Coherent, Fabrinet, AVGO, NVDA, Sumitomo Electric, Furukawa, Innolight, Eoptolink, TFC, Luxshare) carries a median FY26 P/E around 25x and average EPS growth of about 40% in 2026 and 24% in 2027, versus Lumentum’s modeled 84% and 25%.  On this basis, the premium multiple relative to the optical peer set is justified only if LITE achieves its out‑year laser/OCS/CPO ramp and sustains above‑peer EPS growth into FY28. Versus broader AI infrastructure leaders, the picture is more mixed. NVIDIA and Broadcom also trade at high forward multiples but are diversified across GPUs, accelerators, NICs, switch ASICs, and software, with much broader customer bases and multiple growth vectors. Lumentum is a more narrowly focused component supplier with heavier customer and product concentration and less control over system design and adoption timing. In addition, the share price has already moved sharply: external analysis indicates the stock has risen more than 120‑140% year‑to‑date and roughly 144% since late July, driven by the Q1 beat, revised guidance, and growing AI enthusiasm. The risk‑reward profile at current levels is therefore more symmetric than at initiation; the Mizuho $290 target now approximates spot, while the average Street target around the low‑$200s sits meaningfully below spot.

Several key risks could impair the bullish thesis. Technology adoption risk is significant: if AI networking remains dominated by improved pluggables and LPO platforms at 800G and even 1.6T, with CPO penetration remaining modest, then the upside from UHP CPO lasers will be limited and traditional transceiver vendors will continue to capture most of the optics value. Similarly, if hyperscalers find that software‑defined electrical fabrics or incremental Clos optimizations are “good enough,” OCS adoption could remain confined to niche or internal deployments, leaving Lumentum’s OCS revenues well below the projected $400‑600M scale. Competitive risk is elevated. Coherent, Furukawa, and others have strong InP capabilities, while Chinese module manufacturers are expanding up the stack from transceivers into photonics and potentially CPO‑adjacent solutions. Hyperscalers and NVIDIA are structurally incented to multi‑source critical components, particularly lasers, to avoid supply shocks. Customer concentration and AI cycle risk are acute: Google and Ciena alone already represent more than 30% of revenue, and Mizuho’s estimates assume increased exposure to Google, Microsoft, Amazon, Meta, and NVIDIA through OCS and CPO.  Any pause or digestion phase in AI GPU deployments—whether due to macro, regulatory limits, AI workload profitability, or alternative architectures—would disproportionately impact Lumentum’s growth trajectory. Geopolitical and supply‑chain risks are non‑trivial given manufacturing and demand exposure to China and the broader Asia‑Pacific region, as well as potential US export restrictions on high‑speed optics. Finally, the ramp of new products like OCS and CPO requires flawless execution in manufacturing yield, field reliability, and customer integration; early failures or delays could jeopardize design‑in positions and reputational standing.

There are also non‑trivial positive optionalities. If NVIDIA’s CPO platforms see broad adoption across hyperscalers and AI cloud providers and if Lumentum maintains a leading share of external laser modules, CPO revenue and associated margins could exceed the already aggressive Mizuho trajectory. If OCS standardization through OCP accelerates and LITE’s R300/R64 family becomes a de facto standard, the company could effectively assume a quasi‑system role in AI network fabrics rather than remaining merely a component supplier, supporting structurally higher margins. Incremental US or allied‑country subsidies for domestic photonics manufacturing could support both capacity expansion and margins, especially for lasers used in strategic AI infrastructure. Finally, Lumentum remains a strategic asset within the AI optics ecosystem; consolidation dynamics could lead to either accretive acquisitions by LITE (to deepen SiPho or module capabilities) or the company itself becoming a target for larger semiconductor or networking players seeking AI photonics exposure.

From an investment perspective, the Mizuho report correctly highlights Lumentum as a pure‑play, high‑beta levered exposure to AI data‑center optics with scarce assets in high‑power InP lasers and emerging OCS technology. The report’s revenue and EPS trajectory, however, should be viewed as a bullish scenario rather than a base case, given the level of unproven OCS and CPO ramp embedded. At approximately $290 per share, the market is already capitalizing a large portion of that bullish path, with the stock trading at a premium to optical peers and at a multiple that assumes sustained high‑double‑digit EPS growth into FY28. The investment implications are that incremental upside from here likely requires confirmation of large, multi‑customer OCS and CPO design wins and evidence that these products can scale to hundreds of millions of dollars of revenue at >50% gross margins. In the absence of such confirmation, the downside risk stems from any disappointment in AI networking capex or signs of share loss or multi‑sourcing at key customers, which could compress both earnings expectations and the valuation multiple.

In portfolio construction terms, Lumentum fits best as a satellite position within an AI infrastructure basket, offering outsized sensitivity to AI optic and networking themes but also higher idiosyncratic risk than more diversified names like NVIDIA and Broadcom. The current valuation and recent share‑price acceleration argue for measured position sizing and heightened focus on upcoming catalysts: subsequent quarterly prints that detail EML capacity utilization and mix shift to 200G lanes; explicit disclosure of OCS revenue contributions and customer count; progress updates from NVIDIA on CPO shipments and mix; and developments from the OCP OCS project that signal whether Lumentum’s implementations are becoming reference designs or face intense standardized competition. Confirmation along these axes would support the higher‑growth, higher‑multiple path implicit in the Mizuho initiation; any shortfall would likely necessitate a reset of both estimates and valuation toward the peer group, with significant downside from current levels.

3

17

144

29,948

19 Oct 2025

The Physics of Euler's Formula | Laplace Transform Prelude youtu.be/-j8PzkZ70Lg?si=Cp76… via @YouTube

1

42